doctors insurance solution - icici prulife

TRANSCRIPT

Doctors Insurance Solution

You have worked hard to achieve…

Success at work

Hence you deserve to create and live the best…

desired life for yourself

As medical professionals you have been helping

your patients lead a healthy life

Now is the optimum time to achieve

and secure your emotional goals

Child’s education Retirement planning Child’s marriage

…and achieve your professional aspirations

Visiting Faculty or

Resident Doctor

Own Clinic Own Poly Clinic Own Nursing home

However every profession is exposed to certain amount of…

Even medical practitioners carry substantial risk in their professions

What is the risk?

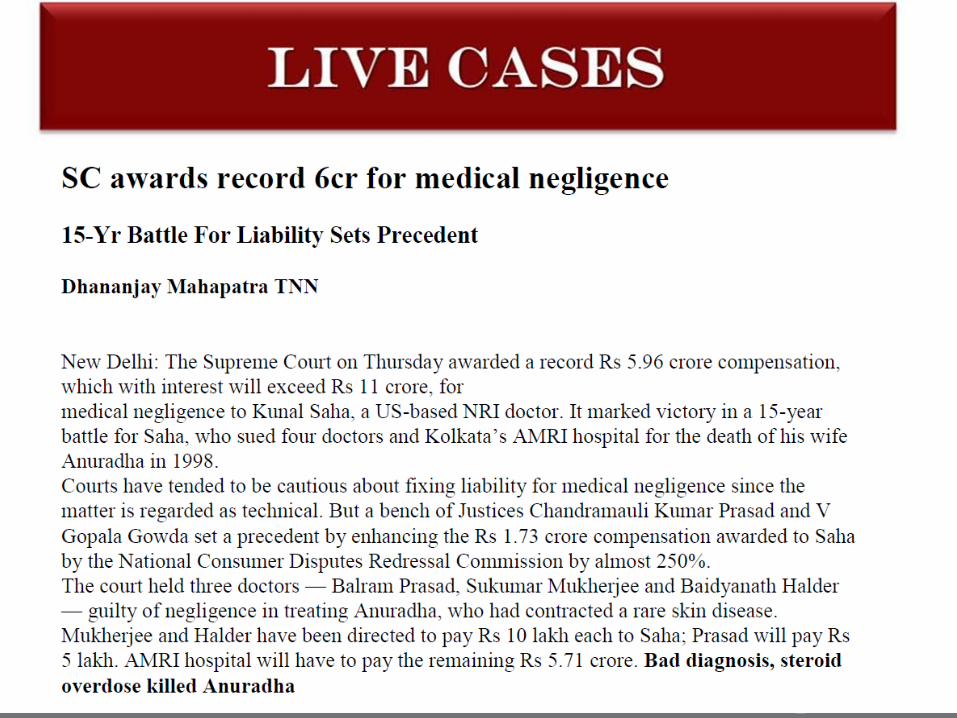

A doctor may have to pay a huge financial compensation, in case a patient being treated by the doctor dies/suffers loss, the patients family can file a

case against the doctor.

Medical Negligence Law

LIVE CASES

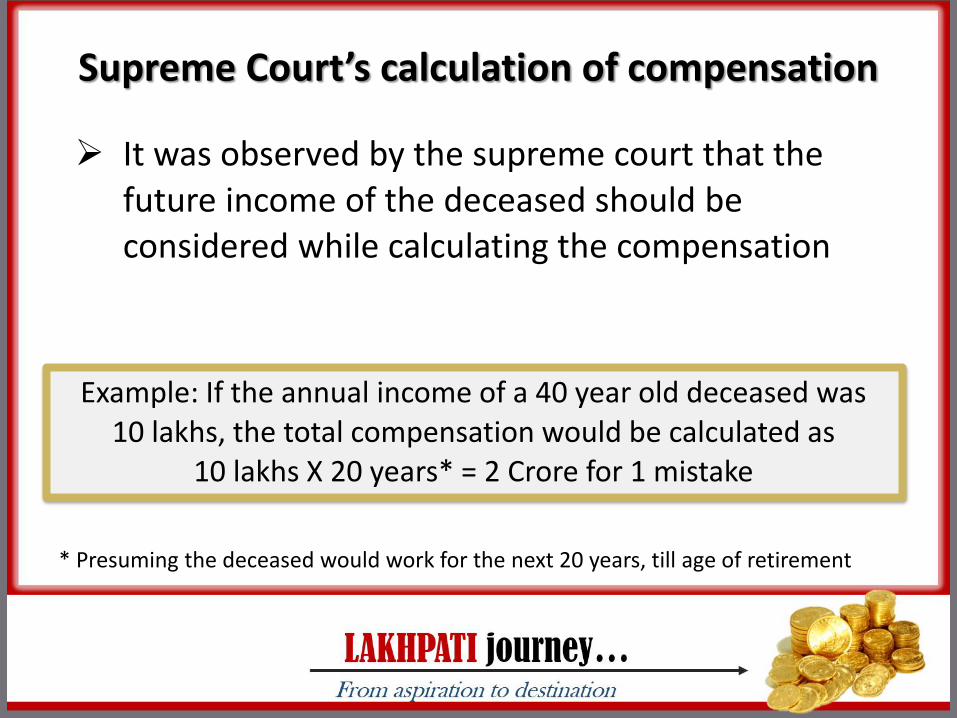

Supreme Court’s calculation of compensation

It was observed by the supreme court that the future income of the deceased should be considered while calculating the compensation

Example: If the annual income of a 40 year old deceased was 10 lakhs, the total compensation would be calculated as

10 lakhs X 20 years* = 2 Crore for 1 mistake

* Presuming the deceased would work for the next 20 years, till age of retirement

Such compensations may eat away all your savings or assets

Professional Indemnity Policy

• which is substantially low compared the kind of claims that may arise

• Cover inadequate as maximum basic cover allowed is 6 times of annual income

An imperative protection solution

Solution :Married Woman’s Property Act 1874

What is MWP Act?

Section 6 of the Married Women Property Act, 1874 providesthat the policy of insurance effected by any married man, onhis own life, and expressed on the face of it to be for thebenefit of his wife or his wife and children or any of them,shall ensure and deemed to be a trust for the benefit of hiswife and children, or any of them according to the interestsso expressed and shall not so long as any object of the trustremains, be subject to the control of the husband, or of hischildren, or form part of his estate.

MWP Act: Interpretation

Section 6 of the Married Women Property Act, 1874 providesthat the policy of insurance (MF, FD, Postal cash , gold or anyother financial product not allowed) effected by any marriedman, on his own life, (self proposed policy and not proposed onlife of his wife or child) and expressed on the face of it (hasto be a fresh application, existing policies cannot be includedpost issuance) to be for the benefit of his wife or his wife andchildren or any of them, shall ensure and deemed to be a trustfor the benefit of his wife and children, or any of themaccording to the interests so expressed and shall not so long asany object of the trust remains, be subject to the control of thehusband, or of his children, or form part of his estate.

Who can initiate an MWPA?A Married Man (“Married Man” would include widowers and divorcees - the last two would apply where the beneficiaries are the children of the man)

Who can be the beneficiary?wife; wife and any of his child/children; any of his child/children

How does it safeguard the asset?Since a Policy effected by a Married Man under the MWP Act results in a trust, the Life Insured does not have any interest in, nor can he control the Policy The Policy will not be a part of his estate, and cannot be targeted by his creditorsThe intended beneficiaries therefore may enjoy encumbrance free the proceeds of the liquid asset

How do I initiate a MWP for a Policy?A simple addendum has to be filled with the application formIt can only be done at the proposal stage of the policy only with a new insurance policyOld or existing policies cannot be covered under the MWP Act

It is prudent to ring-fence 10% of your liquid assets

Instrument Recommended Product undermwpa

Mutual Funds Elite Wealth II

Stocks Elite Wealth II

Fixed Deposit Savings Suraksha

Cash Guaranteed Wealth Protector

Gold Guaranteed Wealth Protector

Investment by an individual in various liquid

instruments

Our recommendation to ring-fence is by investing 5-10% in a similar kind of

instrument

Safety with Returns

Despite a safer solution , returns not compromised

8%

Net Fund Value

of a Flat FMC

instrument / No

Sum Assured

1 1000000 30000 966292 16773 4800 8021 1017780 1.35 10,02,815 10,53,035

2 1000000 30000 966292 15331 4800 9576 2101945 1.35 20,71,224 21,61,917

3 1000000 30000 966292 13701 4800 11221 3257136 1.35 32,09,627 33,29,609

4 1000000 30000 966292 12569 4800 13048 4487297 1.35 44,21,906 45,59,229

5 1000000 30000 966292 10894 4800 14936 5797838 1.35 57,13,400 58,54,062

6 0 0 0 10524 0 11156 6154930 0.95 60,88,947 61,64,531

7 0 0 0 10624 0 11817 6560191 0.95 64,89,867 64,91,466

8 0 0 0 10551 0 12500 6993045 0.95 69,18,084 68,35,740

9 0 0 0 10222 0 13199 7455662 0.95 73,75,749 71,98,273

10 0 0 0 9496 0 13901 8024753 0.75 79,39,544 75,80,032

11 0 0 0 7451 0 14624 8561508 0.75 84,86,179 79,82,038

12 0 0 0 5685 0 15351 9153632 0.75 90,73,104 84,05,364

13 0 0 0 3261 0 16068 9790020 0.75 97,03,906 88,51,142

14 0 0 0 454 0 16813 10474227 0.75 1,03,82,108 93,20,561

15 0 0 0 0 0 17929 11311247 0.75 1,12,12,685 98,14,875

Effectiv

e FMC

Flat FMC @

2.25%Fund at End

Indicative figures @ 8 % ROI considering a 40 year old male opting for an equity fund in Elite Wealth II

Policy

Year

Annualis

ed

Premium

Premium

Allocatio

n Charge

Amount

available

for

investment

Mortality

Charge

ICICI Prudential , Elite Wealth II with reducing FMC post 6th year onwards,

because of Loyalty Additions & Wealth Boosters

Vs.

Service

Tax

Fund before

FMC

Policy

Admin

Charge

Scenario 2Life with mistake

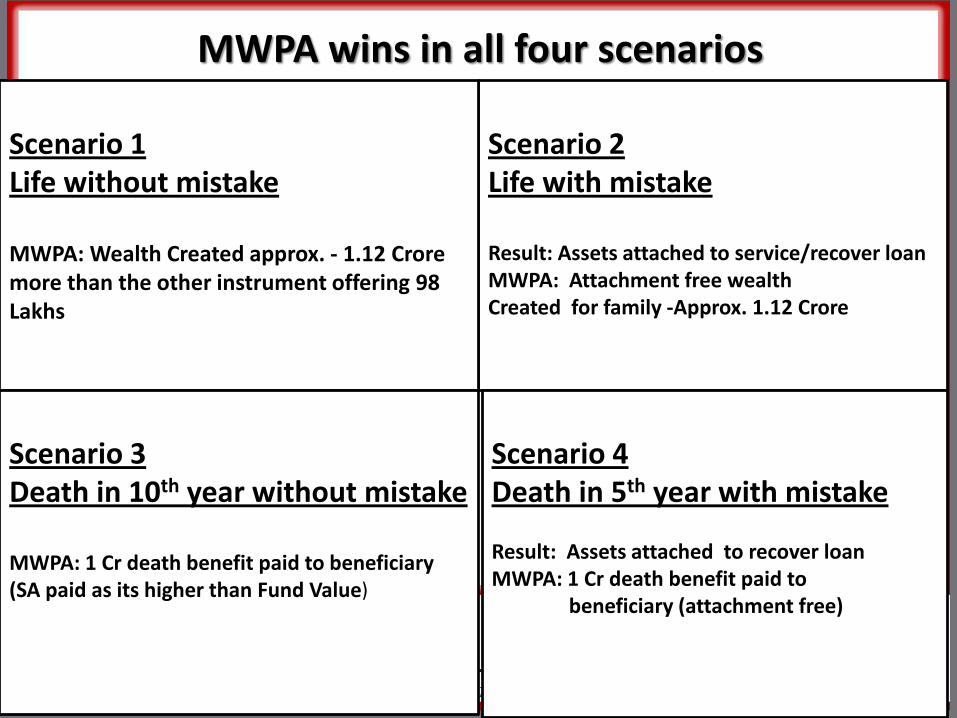

Result: Assets attached to service/recover loanMWPA: Attachment free wealth Created for family -Approx. 1.12 Crore

MWPA wins in all four scenarios

Scenario 1Life without mistake

MWPA: Wealth Created approx. - 1.12 Crore more than the other instrument offering 98 Lakhs

Scenario 4 Death in 5th year with mistake

Result: Assets attached to recover loanMWPA: 1 Cr death benefit paid to

beneficiary (attachment free)

Scenario 3 Death in 10th year without mistake

MWPA: 1 Cr death benefit paid to beneficiary (SA paid as its higher than Fund Value)

Safety with Returns

1 1000000 0 128189 10320472 0

2 1000000 600000 258941 10769132 964257

3 1000000 900000 392308 11220355 2010686

4 1000000 2000000 528343 11674194 3154200

5 1000000 2500000 667099 12130701 4378200

6 1000000 3000000 808629 12269456 5690086

7 1000000 3500000 952990 12410987 7098886

8 0 4200000 1100239 12555348 7590800

9 0 4200000 1250432 12702596 8118400

10 0 4200000 1403629 12852790 8684686

11 0 4550000 1559891 13005987 9292886

12 0 4550000 1719277 13162248 9946629

13 0 4550000 1881851 13321635 10649971

14 0 4550000 2047677 13484209 11407429

15 0 0 2216819 13650034 11973543

Estimated death

benefit

Assumed investment return of 8%Non Guaranteed

Surrender Value

ICICI Pru Savings Suraksha

Policy YearAnnualised

premium

Guaranteed

Surrender

Estimated accumulated

reversionary bonus

Guaranteed Maturity Benefit 64,09,430

Guaranteed Additions 16,02,358

Estimated accumulated reversionary bonus 22,16,819

Estimated terminal bonus 24,77,366

Estimated total maturity amount 1,27,05,972

Benefit summary

• Considering 10 lakhs investment per annum in debt instrument for a tenure calculated basis no. of years left for maturity i.e. 15 years

• Maturity with tax deduction and reinvestment considered at end of every 10 years• Maturity post tax arrived after deducting individual tax liability @ 30% on interest earned

Debt instrument @ 8% compounded interest p.a

Investment 1st 2nd 3rd 4th 5th 6th 7th Total maturity After tax maturity

1 1000000 1080000

2 1000000 1166400 1080000

3 1000000 1259712 1166400 1080000

4 1000000 1360489 1259712 1166400 1080000

5 1000000 1469328 1360489 1259712 1166400 1080000

6 1000000 1586874 1469328 1360489 1259712 1166400 1080000

7 1000000 1713824 1586874 1469328 1360489 1259712 1166400 1080000

8 1850930 1713824 1586874 1469328 1360489 1259712 1166400

9 1999005 1850930 1713824 1586874 1469328 1360489 1259712

10 2158925 1999005 1850930 1713824 1586874 1469328 1360489

11 1956147 2158925 1999005 1850930 1713824 1586874 1469328

12 2112639 1956147 2158925 1999005 1850930 1713824 1586874

13 2281650 2112639 1956147 2158925 1999005 1850930 1713824

14 2464182 2281650 2112639 1956147 2158925 1999005 1850930

15 26,61,317 24,64,182 22,81,650 21,12,639 19,56,147 18,35,247 17,23,303 1,50,34,486 1,26,24,140

Scenario 2Life with mistake

Result: Assets attached to service/recover loanMWPA: Attachment free wealth Created for family -Approx. 1.27 Crore

MWPA wins in all four scenariosScenario 1Life without mistake

MWPA: Wealth Created approx. - 1.27 Crore more than the other instrument

Scenario 4 Death in 10th year with mistake

Result: Assets attached to recover loanMWPA: 1.28 Cr death benefit paid to

beneficiary (attachment free)

Scenario 3 Death in 10th year without mistake

MWPA: 1.28 Cr death benefit paid to beneficiary

The pre-tax maturity amount from the debt instrument would be more than the maturity from Savings Suraksha, even then MWPA wins in 3 scenarios.

Safety with Returns

1 1000000 60000 932584 16843 6000 12408 979716 12801 4741 0 0 960005 1050080

2 1000000 50000 943820 15472 6000 13296 2029516 26345 9757 0 0 1988952 2152748

3 1000000 40000 955056 13910 6000 14324 3153944 40850 15130 0 0 3091045 3310638

4 1000000 40000 955056 12888 6000 16800 4344553 56213 20820 0 0 4257999 4526516

5 1000000 40000 955056 11371 6000 19368 5605744 72485 26846 0 0 5494136 5803284

6 0 0 0 11147 6000 15060 5909357 76403 28297 13833 0 5805549 6093913

7 0 0 0 11508 6000 15839 6245020 80738 29903 14604 0 6135307 6399097

8 0 0 0 11773 6000 16650 6600595 85330 31604 15434 0 6484642 6719565

9 0 0 0 11878 6000 17487 6977482 90196 33406 16313 0 6854916 7056081

10 0 0 0 11693 6000 18338 7377310 95356 35317 17245 224187 74,71,918 74,09,451

Investm

ent

Loyalty

Addition

Wealth

Booster

Policy

Admin

Service

Tax

Fund

before

Premium

Allocation

Amount

available

Mortality

ChargeFMC

Flat FMC

@ 2.50%

Fund at End

ICICI Prudential Guaranteed Wealth Protector @ 8% annual returns with loyalty additions getting added from 6th year onwards and wealth booster added in the 10 years

Policy

Year

Annualised

Premium

Despite a safer solution , returns not compromised

MWPA wins in all four scenarios

Scenario 2Life with mistakeResult: Liquid/ personal assetsattached to service/ recover loan

MWPA: Attachment free wealthCreated for family – Approx.75 lakhs

Scenario 1Life without mistakeMWPA: Wealth created approx. 75 lacs more than the other financial instruments

Scenario 4 Death in 10th year with mistake Result: Liquid/ personal assets attached to recover loanMWPA: 1 Cr death benefit paid to beneficiary (attachment free)

Scenario 3 Death in 10th year without mistakeMWPA: 1 cr death benefit paid tobeneficiary which is more thanmaturity amount from otherfinancial instruments

“MWPA has withstood the test of time…

Instances where

MWPA has helped in ring

fencing personal assets…

P. Balamba Vs. K. Krishnayya And 3 Ors.

on 11 April, 1913

Krishna Lal Sadhu And Anr. Vs. Pramila

Bala Dassi on 22 February, 1928

S.VenkatasubramaniaSarma Vs. United

Planters' Association Of ... on 23 September,

1937

D. Mohanavelu Mudaliar Alias D. ...

Vs. The Indian Insurance And

Banking ... on 16 July, 1956

Income-Tax Officer Vs. Damodardas K.

Shah on 24 September, 1984

Shri Harshavardhan B. Doshi Vs.

Controller Of Estate Duty on 20 March,

1991

MWPA cases over the last 139 years…

Thank You

Fill your Lakhpati tracker for securing emotional goals against professional risks…