internship report - ningapi.ning.com/files/jgjvjrjg6hi-wlbhseafr00pg5f4uwc4... · web...

TRANSCRIPT

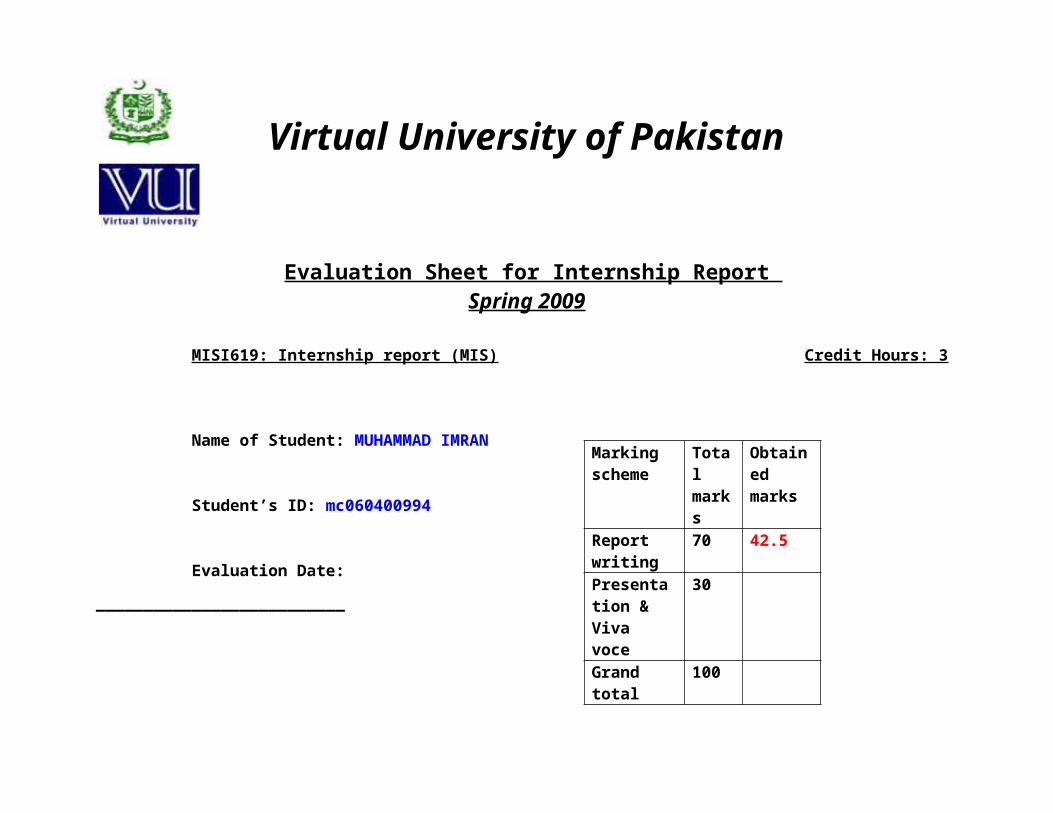

Virtual University of Pakistan Evaluation Sheet for Internship Report

Spring 2009

MISI619: Internship report (MIS) Credit Hours: 3

Name of Student: MUHAMMAD IMRAN

Student’s ID: mc060400994

Evaluation Date: __________________________

Supervisor: _______________________________

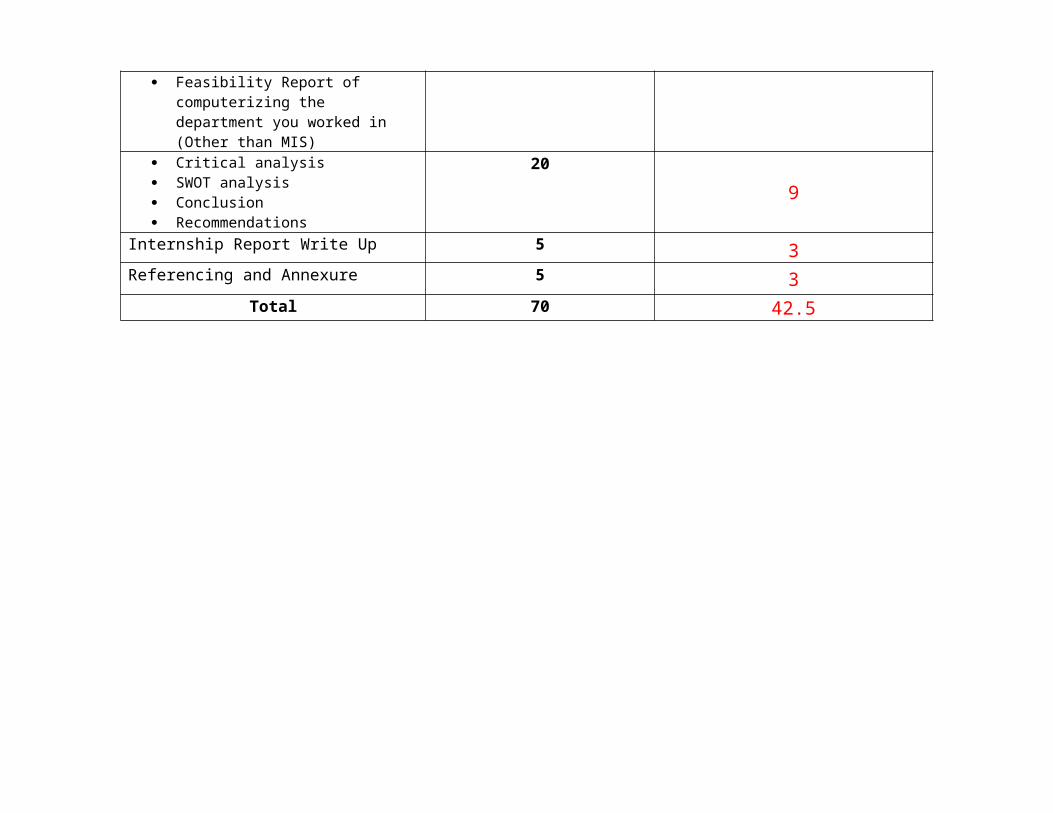

Marking scheme

Total marks

Obtained marks

Report writing

70 42.5

Presentation & Viva voce

30

Grand total 100

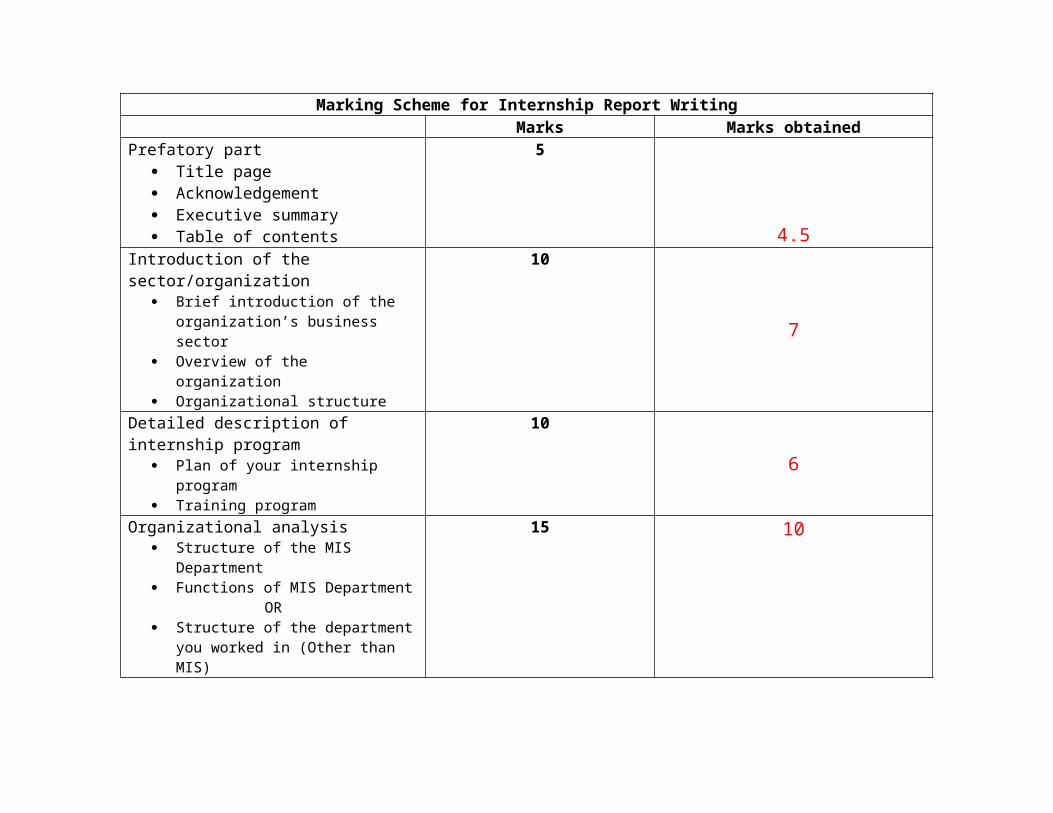

Marking Scheme for Internship Report WritingMarks Marks obtained

Prefatory part Title page Acknowledgement Executive summary Table of contents

5

4.5Introduction of the sector/organization

Brief introduction of the organization’s business sector

Overview of the organization Organizational structure

10

7

Detailed description of internship program Plan of your internship program Training program

106

Organizational analysis Structure of the MIS Department Functions of MIS Department

OR Structure of the department you worked

in (Other than MIS) Feasibility Report of computerizing the

department you worked in (Other than MIS)

15

10

Critical analysis SWOT analysis Conclusion Recommendations

209

Internship Report Write Up 5 3Referencing and Annexure 5 3

Total 70 42.5

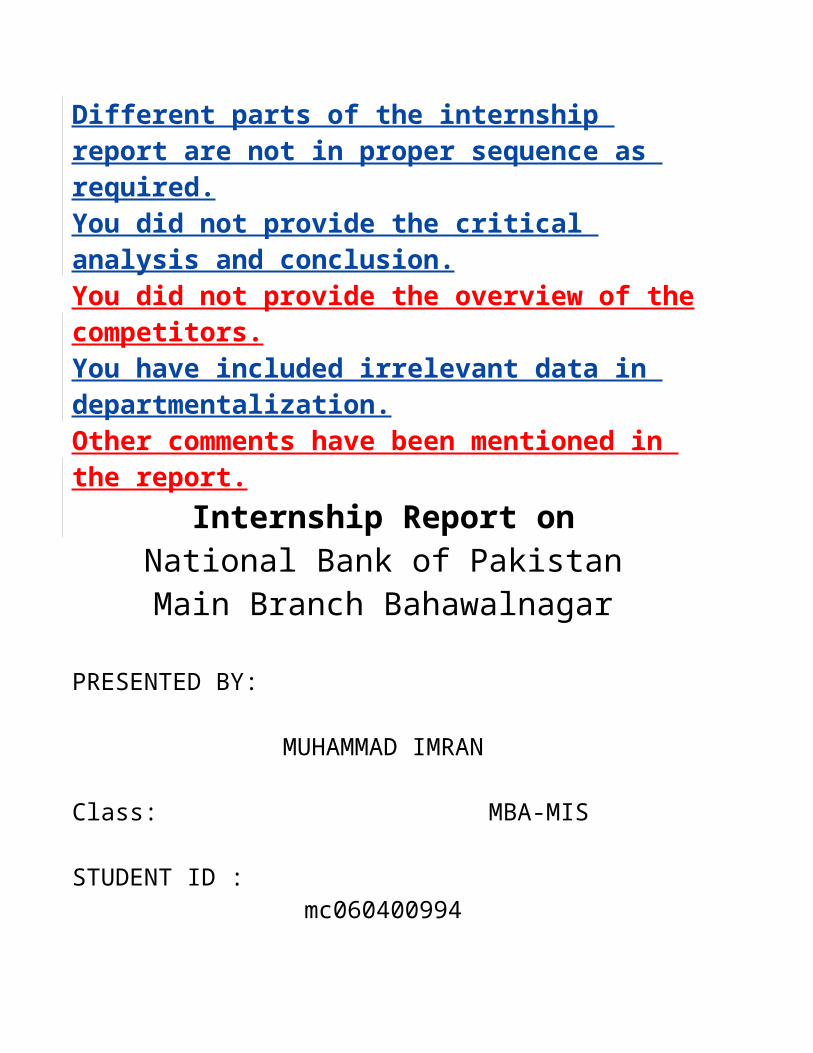

Different parts of the internship report are not in proper sequence as required.You did not provide the critical analysis and conclusion.You did not provide the overview of the competitors.You have included irrelevant data in departmentalization.Other comments have been mentioned in the report.

Internship Report onNational Bank of Pakistan

Main Branch Bahawalnagar

PRESENTED BY:

MUHAMMAD IMRAN

Class: MBA-MIS

STUDENT ID : mc060400994

Session: Spring 2009

Internship Date: Nov 11th to Dec. 22nd 2008

Report completed: June 27th 2009

VIRTUAL UNIVERSITY OF PAKISTAN

DEDICATION

I dedicate to my Dear Parents & my respectable teachers whose assistance is always with me. And I personally do great respect by heart.

Acknowledgement

Here very thanks to Almighty Allah whose guidance helped me to be trained in a top class organization, NBP, as well as to complete this report in a very limited time.

My thanks also to young, dynamic, congenial, and qualified staff of NBP who never let me alone in different situations related to my internship. Without their humble help, it was not easy.I am thankful to the Bank Manager,Muhammad Arshad Nagra,NBP Nain Brach Bahawalnagar.He guide me during my intership from Nov.11th to Dec.22nd 2008.

Executive summary

This report is about my internship program with NATIONAL BANK. In this comprehensive report, I have discussed about every major aspect of the bank, which I observed and perceived during my internship program. In this report you will find the detail about the bank right from its incorporation to the current position. Along with it, the processes, policies and procedures of the bank are also discussed in detail.

As the main purpose of internship is to learn by working in practical environment and to apply the knowledge acquired during the studies in a real world scenario in order to tackle the problems using the knowledge and skill learned during the academic process.

In this report the detailed analysis of the organization has been done and the financial, technical, managerial and strategic aspects have been evaluated to analyze the current position of the organization.

This report also contains my perceptions about the employee’s satisfaction, motivation level and the working environment of the organization.

Table of contents should be on separate page.TABALE OF CONTENTS:

Sr.# Contents Page #1. INTRODUCTION 6

2. EVOLUTION OF BANKS IN PAKISTAN 73. PRESENT STATUS AND HISTORY 84. Banking Reforms 1972 9

5. FINANCIAL POSITION 12

6. PRODUCTS OF NATIONAL BANK OF PAKISTAN 15

7. SAIBAAN SCHEME 16

8. FOREIGN CURRENCY 17

9. EXPORT DEPARTMENT 19

10. IMPORT DEPRTMENT 19

11. DIFFERENT SCHEMES CONDUCTED BY NBP 21

12. ORGANIZATIONAL STRUCTURE 22

13. Plan of My internship program 27

14. DEPARTMENTALIZATION 29

15. DEPARTMENTATION OF NBP BAHAWALNAGAR MAIM BRANCH.

43

16. General observation during Training Program 46

17. MANAGEMENT INFORMATION SYSTEM (MIS 54

18. Structure of the MIS Department 57

19. Functions of the MIS Department 58

20. SWOT ANALYSIS 59

21. COMPETITIVE ANALYSIS 6322. SUGGESTION: 6523. RECOMMENDATIONS 63

24. References 74

1. INTRODUCTION

Definitions of Bank

“Bank”

"A financial institution, which deals with money and credit. It acceptsDeposits from individuals, firms and companies at a lower rate of Interest and gives at higher rate of interest to those who need them.”

A financial establishment which uses money deposited by customers for investment, pays it out when required, makes loan at interest, exchanges currency, etc.J.W Gilbert in his principles and practice banking defines a banker in these words:

“A banker is dealer in capital or more properly, a dealer in money. He is intermediate party between the borrower and the lender. He borrows of one and lends to another”.The American defined the term banker in a very broad sense as under:

“By banking, we mean the business of dealing in credits and by a ‘Bank’ we include every person, firm or company having a place of business where credits are opened by deposits of collection of money or currency. Subjects to be paid or remitted on Cheques or order, money

is advanced or loaned on stocks, bonds, bullion, bill of exchange, promissory notes are received for discount or sale”.

Scope of Studies As an internee in National Bank of Pakistan the main focus of my study research is on general banking procedures in one of the branches of NBP in MIS environment. These operations include remittances, deposits, advances and foreign exchange.Similarly different aspects of overall of NBP are also covered in this report.

Research Methodology

The report is based on six weeks internship program in National Bank of Pakistan. The methodology reported for collection of data is primary as well as secondary data. The biggest source of information is my personal observation while working with staff and having discussion with them. Formally arranged interviews and discussions also helped me in this regards.

2.EVOLUTION OF BANKS IN PAKISTAN

There are different opinions that how the word ‘Bank’ originated. Some of the author’s opinion that this word is derived from the word ‘Bancus’ or Banque’, which means a bench. The explanation of this origin is attributed to the fact that the Jews in Lombard transacted the business of money exchange on benches in the market place; and when the business failed, the people destroyed the ‘bench’. Incidentally the word ‘Bankrupt’s said to have evolved from this practice.Some of the authors are of opinion that the word ‘Bank’ is derived from the German word back, which means ‘joint stock fund’. Later on when the German occupied major part of the Italy the word ‘Back’ was italicized into ‘Back’.In fact human left the need of bank when it begins to realize the importance of money as a medium of exchange. Perhaps it where the Babylonian who developed banking system as early as 2000 BC. At that time temples were used as banks because of their prevalent respect. During the rule of king Hamurabi (1788 – 1686 BC) the founder of Babylonians Empire, loans were started being granted for interest. The borrower has to provide guarantee or he had to pledge his goods or valuables. King Hamurabi drew up a code wherein he laid down standards rules for procedures for banking operations by temples and great landowners. Also in Greece, the temples were used as banks, where the people deposited their money and other valuables for safe custody and security. In Europe with the ‘revival of civilization’ (Renaissance) in the middle of twelve century, trade and commerce started expanding and this development compelled the business community to borrow the money from the Hebrew money lenders on high rates of interest and usury. Seeing the great demand, these moneylenders started organizing themselves and bank

started up at the principle seaports of southern Europe. Soon Venice and Geneva became the most important money markets of the time and banking though different from its present form, flourished. What we know as ‘modern banking’ originated in the 14th century in Barcelona National Bank of Pakistan (NBP) was established under the National Bank of Pakistan Ordinance 1949. The primary objective of NBP was to purchase jute from the growers in the former East Pakistan and also to perform the commercial banking functions in the country.

National Bank of Pakistan is now the biggest financial institution with assets totaling over Rs.310 billion with 1428 local and 23 foreign branches. The bank is the higher financer in agriculture and commodity operation sector.

As part of the academic requirement for completing MBA (MIS) Master Business Administration of the students are required to under go six/eight weeks of internship with an organization. The internship is to serve the purpose of acquainting the students with the practice of knowledge of the discipline of banking administration. This report is about National Bank Pakistan. NBP was established in 1949 and since then, it has expended its network, becoming the largest commercial Bank of the country. It offers different products of services to its customers..

3.PRESENT STATUS AND HISTORY

National Bank of Pakistan maintain its position as Pakistanis premier Bank determined to set higher standards of achievements. It is the major business partner for the government of Pakistan with special emphasis on fostering Pakistanis economic growth through aggressive and balanced lending policies, technologically oriented branches.

The National Bank of Pakistan came into existence on 20th November 1949 under the National Bank of Pakistan Ordinance No.21 of 1949.It is a semipublic bank and functions like other commercial banks. Therefore it receives funds from the depositors and provides loans/credit facilities in all sectors including trade, industry and agriculture. It also functions as an agent of the Central Bank and operates the treasuries at places where no branch of State Bank of Pakistan exists. The National Bank of Pakistan was also nationalized, along with other banks, in January 1974. The Bank of Bahawalpur was also merged into this Bank.

MANAGEMENT

An Executive Board composed of six Senior Executives of the Bank and the President who is also the Chief Executive supervises the affairs and business of the Bank.

CAPITAL

The authorized capital of the Bank is Rs.2500 million divided into 100 million ordinary shares of Rs.10 each. After nationalization, all the shares held by persons other than the Federal Government or Corporations i.e., owned and controlled by the Federal Government was considered as transferred and vested in the Government.

BRANCHES

The Bank had a network of 1531branches in the country and 28 branches in foreign countries. These countries are as follows:1) - United States of America2) - United Kingdom3) - France4) - Germany 5) - Africa, Middle East Region6) - Bahrain Obu7) - Asia Pacific Region 8) - Japan9) - Republic of Korea10) - Central Asian States11) - Bangladesh12)-Peoples Republic of China13) -Pakistan.

The main of the study in hand is together relevant information to compile internship report on National Bank of Pakistan.

To observe, analyze and interpret the relevant data competently and in a useful manner. To work practically in an organization. To develop interpersonal communication.

4.Banking Reforms 1972

After the assumption of office by a new government in 1971, may 1972 different reforms were introduced to make the banks more responsive to the requirements of economics growth with social justice. The reforms aimed at bringing about a more purposeful and equitable distribution of bank credit, improving the soundness and efficiency of the banks, and securing greater social accountability of the banking system as a whole.The role of the banking system had been truly spectacular in mobilizing savings of the community and meeting the credit needs of the economy. But at the same time, the banks had generally neglected their role in promoting social justice and had failed to play an effective role in ensuring a wider and more equitable dispersal of the benefits of economic growth. In particular the inter locking of ownership with commercial and industrial interests had led to the misuse of bank resources. There was a heavy concentration of credit in big accounts and in urban area. Credit facilities for agriculture, small business, newly emerging exports and housing had remained obviously inadequate while the banks indulged in capital financing in few selected

business sectors and issued guarantees on behalf of favored clients, term clients, term financing facilities for industry were wholly absent.Under the banking reforms introduced in May 1972 the state bank of Pakistan was accorded wider powers. It was authorized to remove directors or managerial personnel, if necessary and supersede the board of directors of a banking company and appoint administrators during the period of such super session. It was also empowered to nominate directors on the board of every bank. As regard bank directors, it was provided that anyone defaulting in meeting his obligations to bank would forfeit his directorship. Moreover, it was laid down that no person could serve as director of a bank for more than six years continuously. Each bank was required to have a paid up capital of not less than 5 percent age of its deposits to be progressively build up to 10 percent age over a period of time. The banks were also required to transfer 10 percentage of their profit their reserves every years after the reserve became equal to the paid up capital. With a view to diversity the ownership of the banks, the banks were required to raise new capital from the market. Unsecured loans to directors, their families or firms and companies, were totally prohibited. The bank reforms also brought about the establishment of new institutions to achieve new objectives. A national credit consultative was setup under the supervise of the state bank with representation form the government and the private sector. It was assigned the task of determining of economy’s annual credit needs within the safe limits of monetary and credit expansion with reference to the annual development plan. Such a credit plan was to cover the public and private sectors. Alongside the National credit council and Agricultural Advisory Committee was formed to allocate agriculture credit for various purposes, to coordinate the operation or the agriculture credit agencies and to oversee the flow of credit to the designated targets. A standing committee on exports in general and the new emerging exports in particular, was also established. With a view to encourage the banks to extend credit to small borrowers, a credit guarantee scheme was introduced under which the state bank under took to share any bonfire losses incurred by the commercial banks in case of small loans of advances to agriculture.At the same time two financing institutions were established. The people’s Finance Corporation was designed to provide finance to people of small means while the National Development Finance Corporation was setup of finance public sector owned and managed industries and enterprises.

The banking reforms turned to be transitional and interim step and when they were hardly eighteen months old the government nationalized the banking systems, with the following main objectives.

To enable the government to use the capital concentrated in the hands of a few rich bankers for the rapid economic development of the country and the more urgent social welfare objectives.

To distribute equitably credit too different classes sectors and regions. To coordinate the banking policies in various area of feasible joint activity without

eliminating healthy competition among banks.

The act passed for the nationalization of banks is known as the banks Nationalization Act 1974. Thus under this act the state bank of Pakistan and all the commercial banks incorporated in Pakistan and carrying business in or outside the country were brought under government ownership with effect from Jan 1, 1974. The ownership, management and control of all Pakistani banks stood transferred to and vested in the Federal government. The shareholders were provided compensation in the form of federal government bonds redeemable at par anytime within the period of fifteen years. Under the Nationalization act, the Chairman, Directors and Executives of various banks, other than those appointed by federal government were removed from their offices and the central boards of the banks and all local bodies were dissolved. Pakistan banking council was established to coordinate the activities of the Nationalized Commercial banks. At the time of Nationalization on December31, 1973 there were following 14 Pakistani commercial banks with 3323 offices allover Pakistan and 74 offices in foreign countries:

National banks of Pakistan Habib bank limited Habib bank (overseas) limited United bank limited Muslim commercial bank limited Commerce bank limited Standard bank limited Australia bank limited Bank of Bahawalpur limited Premium bank limited Pak Bank limited Sarhad bank limited Lahore commercial limited Punjab provincial co-operative bank limited

The Pakistan banking council prepared a scheme for the recognition of banks. The bank (amalgamation) scheme 1974 was notified in April, providing for the amalgamation of the smaller banks with bigger ones and following the five units in there phases:

National bank limited Habib bank limited United bank limited Muslim commercial bank limited Allied bank of Pakistan limited

The first phase was completed on 30th June. 1974. When the bank Bahawalpur was merged with the National Bank of Pakistan. The premier Bank Limited with Muslim Commercial Bank limited and Sarhad Bank Limited and Pak bank limited and renamed as Allied Bank of Pakistan limited.

The second phase was completed on 31st Dec.1974, when the commerce bank limited merged with the United Bank limited. The third and the final phase were completed on 30th June, 1975 when the standard bank limited was merged with Habib Bank limited.

The nationalization was very smooth and gave very positive results.The number of branches, which stood at 3397 on Dec31, 1973, reached on 7661 by end June 1992. The bank deposits which stood at Rs. 1925 corers at the end 1973 reached the highest mark about 323 corers

5.FINANCIAL POSITION

Different facts and figures of opening balances of the year 2007 about National bank of Pakistan which show the financial position are as under:

CAPITAL STRUCTURENational bank of Pakistan was incorporated with an issued capital of Rs. 15 million.

AUTHORIZED CAPITAL

The bank has now the Authorized Capital of Rs. 25 billion.

SUBSCRIBED AND PAID-UP CAPITALThe Subscribed and Paid-up Capital is Rs. 1.46 billion.

TOTAL DEPOSITSNational bank of Pakistan is the largest commercial bank of the country and has Total

Deposits of Rs. 362.87 billion.

ADVANCES The total Advances stood at Rs. 140.55 billion made by NBP in the form of money at

call and short notices, cash credit, loans for short and long periods.

INVESTMENTSThe total Investment rose to Rs. 143.53 billion. This total Investment includes PTC,

TFC, and securities of Provincial of Federal Government.

PRE-TAX PROFIT The pre-tax profits of NBP have gone up to Rs. 6.05 billion.

AFTER-TAX PROFITThe after-tax profits of NBP have been Rs. 2.26 billion.

TOTAL ASSETSThe Total Assets of NBP are Rs. 432.81 billion which is a great achievement.

TOTAL EXPENDITURESThe Total Assets of NBP are Rs. 26.30 billion which are very less as compared to

previous years’ expenditures.

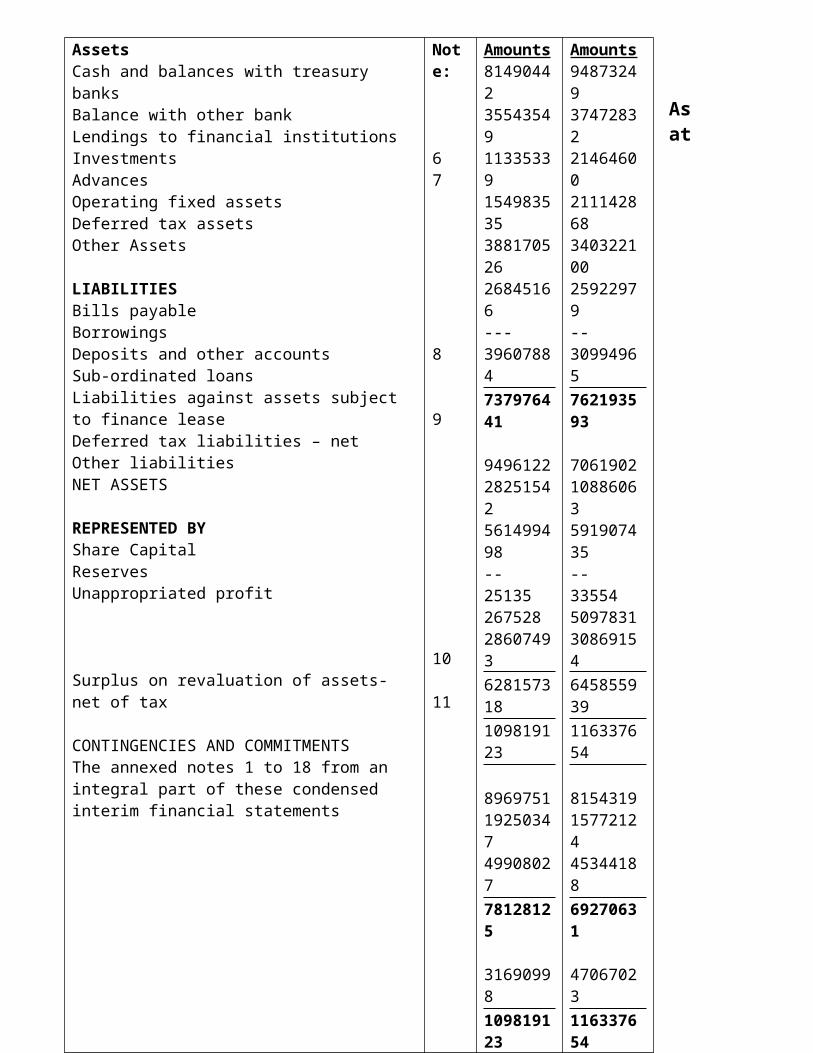

Interim Balance Sheet

As at September 30, 2008

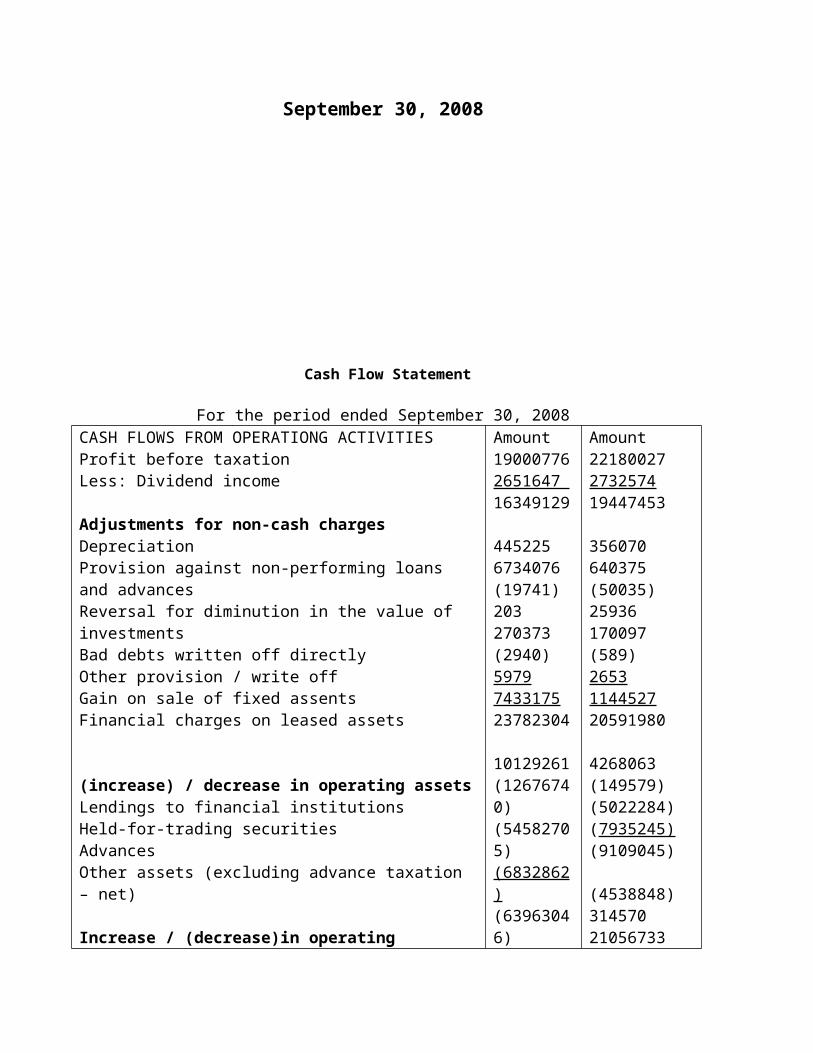

Cash Flow Statement

For the period ended September 30, 2008

AssetsCash and balances with treasury banksBalance with other bankLendings to financial institutionsInvestmentsAdvancesOperating fixed assetsDeferred tax assetsOther Assets

LIABILITIESBills payableBorrowingsDeposits and other accountsSub-ordinated loansLiabilities against assets subject to finance leaseDeferred tax liabilities – netOther liabilitiesNET ASSETS

REPRESENTED BYShare CapitalReservesUnappropriated profit

Surplus on revaluation of assets- net of tax

CONTINGENCIES AND COMMITMENTSThe annexed notes 1 to 18 from an integral part of these condensed interim financial statements

Note:

67

8

9

10

11

Amounts81490442355435491133533915498353538817052626845166---39607884737976441

949612228251542561499498--2513526752828607493628157318109819123

8969751192503474990802778128125

31690998109819123

Amounts94873249374728322146460021114286834032210025922979--30994965762193593

706190210886063591907435--33554509783130869154645855939116337654

8154319157721244534418869270631

47067023116337654

CASH FLOWS FROM OPERATIONG ACTIVITIESProfit before taxationLess: Dividend income

Adjustments for non-cash chargesDepreciationProvision against non-performing loans and advancesReversal for diminution in the value of investmentsBad debts written off directlyOther provision / write offGain on sale of fixed assentsFinancial charges on leased assets

(increase) / decrease in operating assetsLendings to financial institutionsHeld-for-trading securitiesAdvancesOther assets (excluding advance taxation – net)

Increase / (decrease)in operating liabilities Bills payable BorrowingsDeposits and other accountsOther liabilities

Income tax paid Financial charges paid

Net cash flow from operating activities

CAS FLOWS FROM INVESTMENT AXTIVITIESProceeds from / net investment in available-for-sale securitiesProceeds from sale of held-to-maturity securitiesProceeds from sale of investments in associatesDividend income receivedInvestments in operating fixed assetsSale proceed of fixed assets disposed offNet cash from / (used in) investing activities

CASH FLOWS FROM FINANCIG ACTIMITIESPayments of lease obligationsDividend paidNet cash used in financing activates

Effects of exchange rate changes

Amount190007762651647 16349129

4452256734076(19741)203270373(2940)5979743317523782304

10129261(12676740)(54582705)(6832862)(63963046)

243422016684982(30407937)(2312138)(13600873)

(10282712)(5979)(10288691)(64070306)

54350515(3654448)--2651647(1367412)294051983242

(8419)(6115740)(6124159)

2208636

Amount22180027273257419447453

356070640375(50035)25936170097(589)2653114452720591980

4268063(149579)(5022284)(7935245)(9109045)

(4538848)31457021056733148746718319922

(8302250)(2653)(8304903)21497954

(38720937)1010022201952732574(672686)569(35630263)

(26921)(2827029)(2853950)

154669

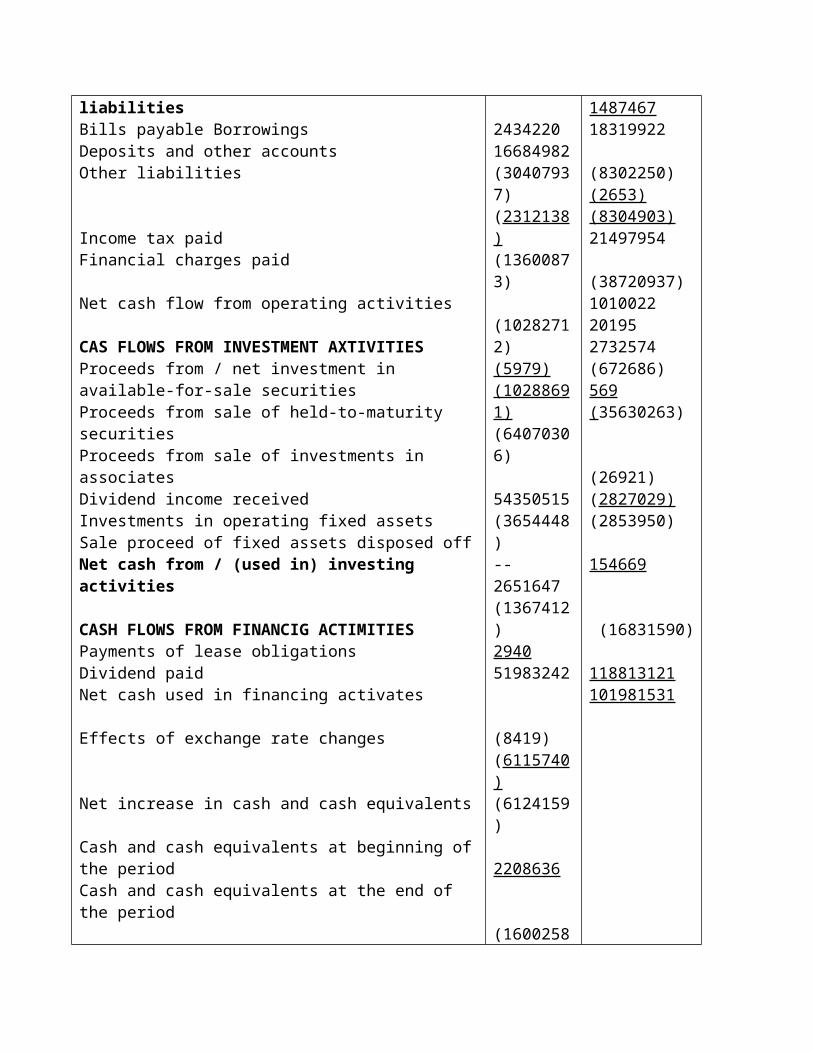

Net increase in cash and cash equivalents

Cash and cash equivalents at beginning of the periodCash and cash equivalents at the end of the period

(16002587)

131456989115454402

(16831590)

118813121101981531

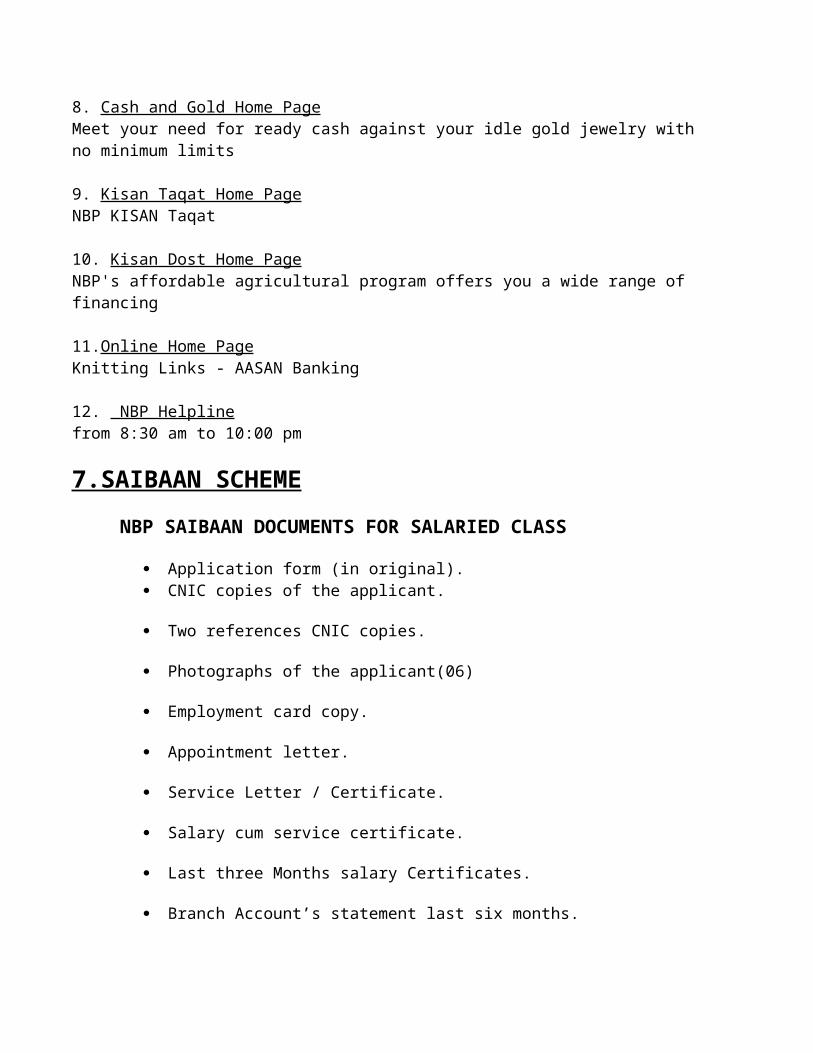

6.PRODUCTS OF NATIONAL BANK OF PAKISTAN

Retail Product

1. Premium Aamdani Home PageUnprecedented Safety - Unprecedented Return

2. Premium Saver Home PageUnprecedented Safety - Unprecedented Return

3. Karobar Home PagePresident's Rozgar Scheme - Easy financing for self employment

4. Saibaan Home PageAffordable, Flexible & Convenient home financing for all

5. Advance Salary Home PageTake up to 20 Advance Salaries - Affordable Installations from 1 - 60 months

6.Cash Card Home PageOne Card does it all - ATM plus Debit Card in one

7. Investor Advantage Home PageInvest with Confidence - Marginal Finance Facility

8. Cash and Gold Home PageMeet your need for ready cash against your idle gold jewelry with no minimum limits

9. Kisan Taqat Home PageNBP KISAN Taqat

10. Kisan Dost Home PageNBP's affordable agricultural program offers you a wide range of financing

11.Online Home PageKnitting Links - AASAN Banking

12. NBP Helplinefrom 8:30 am to 10:00 pm

7.SAIBAAN SCHEME

NBP SAIBAAN DOCUMENTS FOR SALARIED CLASS

Application form (in original). CNIC copies of the applicant.

Two references CNIC copies.

Photographs of the applicant(06)

Employment card copy.

Appointment letter.

Service Letter / Certificate.

Salary cum service certificate.

Last three Months salary Certificates.

Branch Account’s statement last six months.

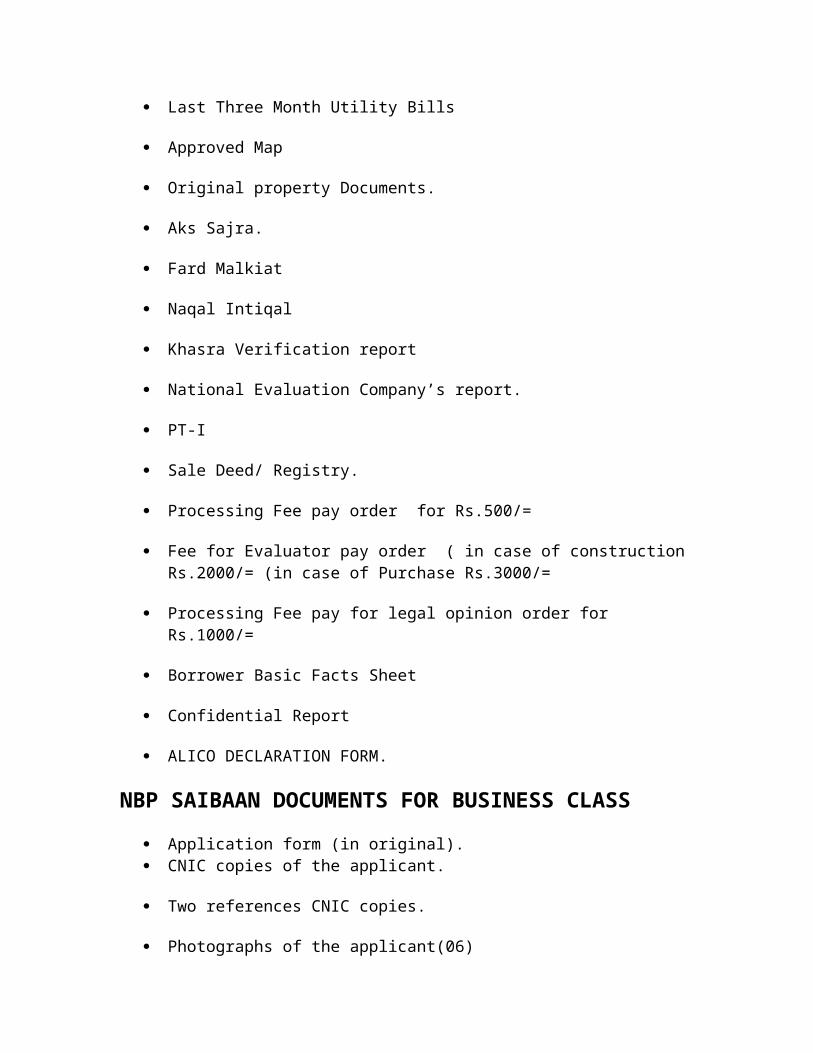

Last Three Month Utility Bills

Approved Map

Original property Documents.

Aks Sajra.

Fard Malkiat

Naqal Intiqal

Khasra Verification report

National Evaluation Company’s report.

PT-I

Sale Deed/ Registry.

Processing Fee pay order for Rs.500/=

Fee for Evaluator pay order ( in case of construction Rs.2000/= (in case of Purchase Rs.3000/=

Processing Fee pay for legal opinion order for Rs.1000/=

Borrower Basic Facts Sheet

Confidential Report

ALICO DECLARATION FORM.

NBP SAIBAAN DOCUMENTS FOR BUSINESS CLASS

Application form (in original). CNIC copies of the applicant.

Two references CNIC copies.

Photographs of the applicant(06)

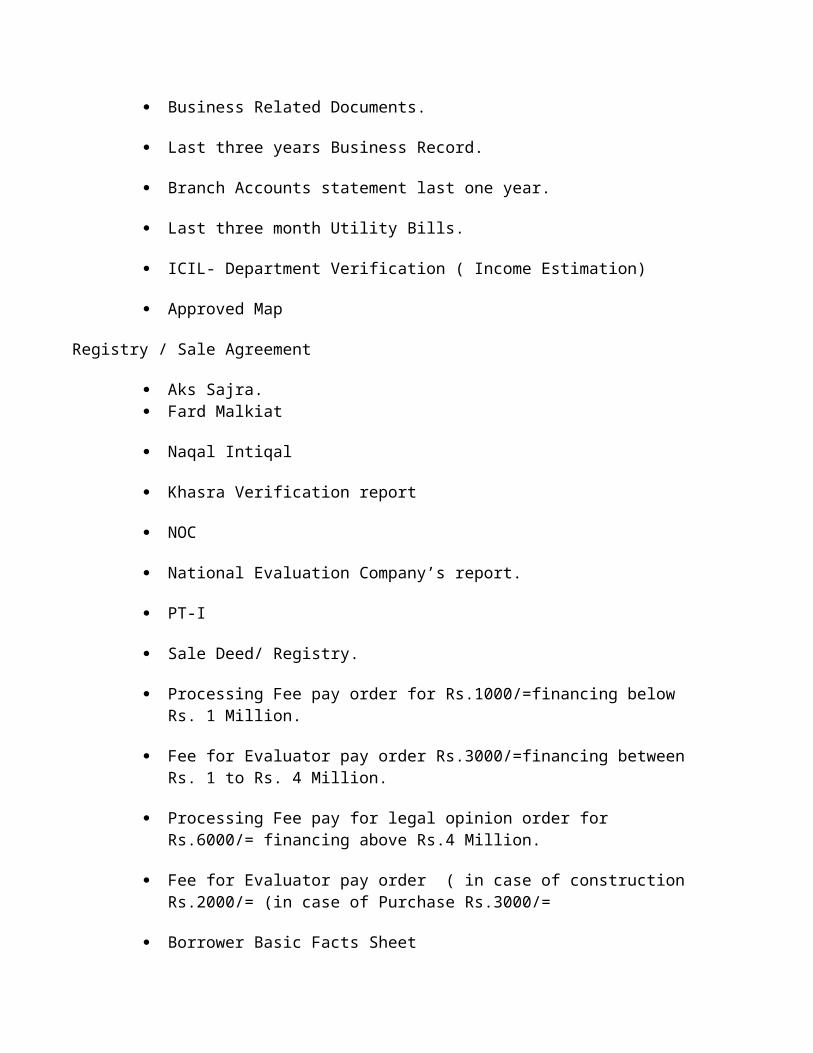

Business Related Documents.

Last three years Business Record.

Branch Accounts statement last one year.

Last three month Utility Bills.

ICIL- Department Verification ( Income Estimation)

Approved Map

Registry / Sale Agreement

Aks Sajra. Fard Malkiat

Naqal Intiqal

Khasra Verification report

NOC

National Evaluation Company’s report.

PT-I

Sale Deed/ Registry.

Processing Fee pay order for Rs.1000/=financing below Rs. 1 Million.

Fee for Evaluator pay order Rs.3000/=financing between Rs. 1 to Rs. 4 Million.

Processing Fee pay for legal opinion order for Rs.6000/= financing above Rs.4 Million.

Fee for Evaluator pay order ( in case of construction Rs.2000/= (in case of Purchase Rs.3000/=

Borrower Basic Facts Sheet

Confidential Report

ALICO DECLARATION FORM.

8.FOREIGN CURRENCYGuaranttee The word guarantee means under taking.

Three parties are involved during the process of Guarantee

Principal (Seller). Guarantor (Bank).

Beneficiary (Buyer).

Outward Remittance The outward remittance is the term which emphasizes that to transfer amount from one country to another country.

The sources used to transfer the amount are Transfer Transactions (TT), Demand Draft (DD).The procedure of outward remittance is initially been undertaken that when account holder fill the request letter. The request letter contain following information are

Request of debit. Amount to be mentioned.

Beneficiary name.

Beneficiary account no.

There is the concept of two accounts are NOSTRO A/C, VOSTRO A/C.Western Union Western Union is the name of Australian Bank which provide facility of providing payment with out wasting time. There are 259 banks in world wide who provide the facility where no bank exist

The amount sent to other place for this we do require certain documents are ID copy name of the person to whom the amount is sent .Then Bank will assign PIN CODE .The amount is send with in 15 minutes. When the receiver go to the bank to receive the amount he had to show his ID COPY or ORIGINAL PASSPORT then the authorize officer will identify through NADRA its identification.

CHARGES

Minimum charges will be received is $20.

Commission will be charged or Rs. 1200.

Inward Remittance In this department the process is contrary to outward remittance the amount from foreign country to the Pakistan. In this case the amount received is in the form of cheque, Pay order etc.

9.EXPORT DEPARTMENT Collection The collection Department is the initial phase of the export department.

First E-Form is to provided to the party .It is given on following criteria

The current account of the exporter should be activated for the issue of the E-Form.

TYPES OF E-FORM

There are four types of form are

Original. Duplicate.

Triplicate.

Quadrapled.

The Banks are involved between the parties .All deals and documentation are made between the banks. The bank of Seller and Buyer contact with their party about the transaction when there is no conflict between the party the process goes on until transaction is completed.

10. IMPORT DEPRTMENT In this department they deal with the following section to process the Import Department.

LC opening. Lodgment.

Retirement of LC.

LC OPENING

Firstly Importer presents the Proforma Invoice to the bank Then Importer will fill the form (IB-8) which cost Rs.100 .Proforma should not be expired.

C&F(exporter will pay ),FOB( Importer will pay shipment charges) should be mentioned on the form. The LC opening application form requires certain documents are

Name and address of the applicant. Name and address of the beneficiary.

Insurance detail.

Nature of LC.

Commodity.

LC LODGEMENT

After LC opening Exporter bank will send document to the Importer Bank for the purpose of LC. Advisory bank is the correspondent bank. In case of any discrepancy found and is accepted then the $50 is charged for further processing. Normally the discrepancy is created after shipment. When the documents are accepted by Importer and Exporter then payment is to be made.

RETIREMENT OF LC

At time of payment or retirement we deal with following Import channel are LC.

Advance Payment. Payment after shipment.

Foreign DD & TT.

LETTER OF CREDIT

LC further categorize in to two things are Sight.Usances.

In case of sight the charges are taken as follows

MARK UP = B.E*Days* 0.4%

1000

In case of Usance the charges are

P&T charges of Rs.400.

Service charges of 0.1%of B.E

Commission is deducted from the party at the time of expiry. When the period is delayed of 1 month then charge 0.1%, if the period is 2 month then charges is 0.2%.FED 5% on total commission

SERVICE CHARGES

The charges of 0.1% of Bill of Exchange is charged. After the period of 15 days then the commission is charged .FED is charged on 5% on commission.

ADVANCE OF PAYMENT

The payment is made to the party in advance to the exporter through bank. The bank also deduct margin from the Importer so that bank could serve itself

SERVICE CHARGES

Minimum commission for the amount less $400.At increase of every $1000 $ is charged.

FED is to be charged of 5%on commission amount.

P&T is charged of Rs.400

11.DIFFERENT SCHEMES CONDUCTED BY NBP National Bank of Pakistan always makes efforts to improve its goodwill in the

general public. It introduces different kind of schemes time to time.

The most popular schemes conducted by NBP are as under:

1 ... ... Hajj Mubarak Scheme

2 ... ... NBP Advance Salary Scheme

3 ... ... Fund Management Scheme

4 ... ... LG TV Scheme

1. HAJJ MUBARAK SCHEME For the convenience of a person with a limited income who desire to perform Hajj, Hajj

Mubarak Scheme is introduced. Moreover, National Bank of Pakistan process the Hajj

applications of thousands of people successfully more than any other bank in Pakistan.

2. NBP ADVANCE SALARY SCHEME

Do you need urgent funds? If yes then head to National Bank of Pakistan and avail “NBP

Advance Salary Scheme”, which allow you to draw three months salary in one go. This facility is

available to permanent employees of the:-

1 ... ... Federal and Provincial governments

2 ... ... Semi-governments, autonomous, semi-autonomous, local bodies, and

government corporations

3 ... ... Other corporations approved by NBP

No guarantee, collaterals, or insurance is required to avail this scheme. NBP gives the

facility to repay the excessive amount within 1 to 36 months. The procedure is very easy, just fill

the application form and choice between 1 to 36 months and take your NBP Advance Salary

within 3 days after submitting your form.

3. FUND MANAGEMENT SCHEME This scheme is offered to corporate under customer and is aimed at providing better rate of

return up to 15% per annum. One of the objectives of the scheme is to develop the secondary

market for government securities.

4. LG TV SCHEME It is the most popular of NBP schemes for people. corporates with LG Appliances

Corporation. If you want a TV set but has not enough money to purchase it then head to NBP,

fill an application form of LG TV Scheme. NBP gives you the facility to pay for the TV set in

smaller installments during a time period of 2 years.

Any one can avail this scheme. Two government employees are required to present the

witness to repay the loan if the applicant is unable to repay the loan or the applicant should have

the Fixed Term Deposit in NBP more worthily than the amount advanced to the applicant and it

should have the duration of more than two years.

12.ORGANIZATIONAL STRUCTURE

In this section four topics are discussed. The major topics of this section are:

1. Management and Organization of a Commercial Bank

2. Senior Management 3. Regional Structure 4. Branch Structure

1. MANAGEMENT AND ORGANIZATION OF A COMMERCIAL BANK

The ownership, management, and control of all the commercial banks were taken over by the Government of Pakistan on January 1st, 1974.

A banking council was formed under the Nationalization Act 1974. The banking council was set up for making policy recommendations to the Federal Government, formulating policy guidelines for the banks and their reorganization.The management and organizational structure of the nationalized banks have uniformity. This management and organizational structure is briefly described as under:

Board of Directors Executive Board Chief Executive Divisional Chiefs Provisional Chiefs Circle Executive Zonal Heads Branch Managers

1.1 Board of DirectorsIn the management of the banks, the board of directors is at the top of the controlling body. Since there are no private share holders now, so there is no general meeting of the share holders and no elected directors. The BOD consists of a nominated President, a Secretary, and 9 other members. The board has limited administrative powers because after the Nationalization Act 1974, most of powers are transferred to the Banking Council and Executive Board.

1.2. Executive BoardThe general direction and supervision of the affairs of commercial banks lies in their respective Executive Boards. An EB also consists of a President, a Secretary, and 9 other members, appointed by the Federal Government. 1.3. Chief Executive

The President of the Executive Board is the Chief Executive. He is the administrative head of a bank and presides over the meetings of Executive Board. 1.4. Divisional Chiefs

In order to improve the management and operation of a bank, it has been split up into a numbers of divisions. Each division of a bank is placed under the supervision and control of Divisional Chief (also called the Senior Executive Vice President or Executive Vice President) 1.5. Provisional ChiefsIn order to improve the performance of banking system, each bank has a Provisional Chief. PC has the powers for sanctioning finance and other credit facilities. Each headquarter is situated in each province e.g. in Lahore, Peshawar, Quetta, and Karachi.

1. 6. Circle ExecutiveEach commercial bank has a number of circles placed directly under the control and supervision of Chief Executive. 1.7. Zonal HeadsEach circle is divided into a number of zones. These zones are administered by Zonal Heads who hold the posts of Vice President or Assistant Vice President. 1.8. Branch Managers Each zone of commercial bank is divided into several branches. The control and supervision of each branch is mostly entrusted to Assistant Vice President or Officer G-II.

Complete organizational hierarchy chart has not been provided.

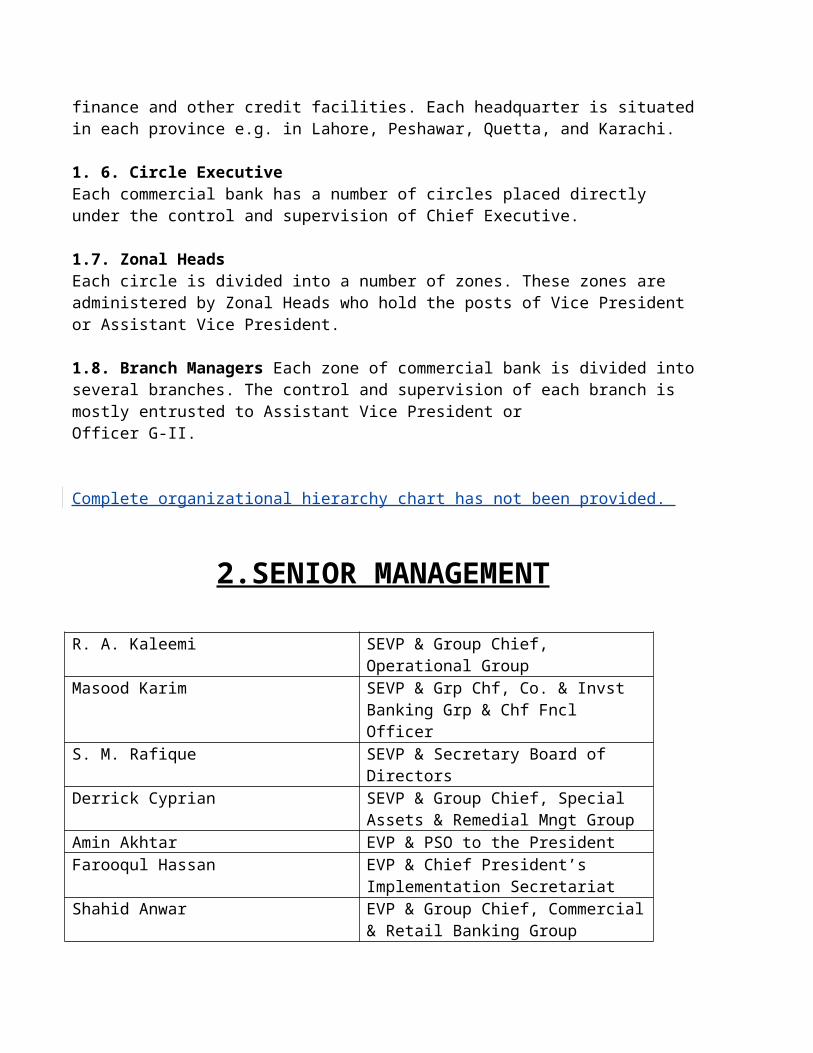

2.SENIOR MANAGEMENT

R. A. Kaleemi SEVP & Group Chief, Operational GroupMasood Karim SEVP & Grp Chf, Co. & Invst Banking

Grp & Chf Fncl OfficerS. M. Rafique SEVP & Secretary Board of DirectorsDerrick Cyprian SEVP & Group Chief, Special Assets &

Remedial Mngt GroupAmin Akhtar EVP & PSO to the PresidentFarooqul Hassan EVP & Chief President’s Implementation

SecretariatShahid Anwar EVP & Group Chief, Commercial & Retail

Banking GroupSafdar Khawaja EVP & Group Chief, Audit & Inspection

GroupAsif A. Brohi EVP & Group Chief, Strategic Planning &

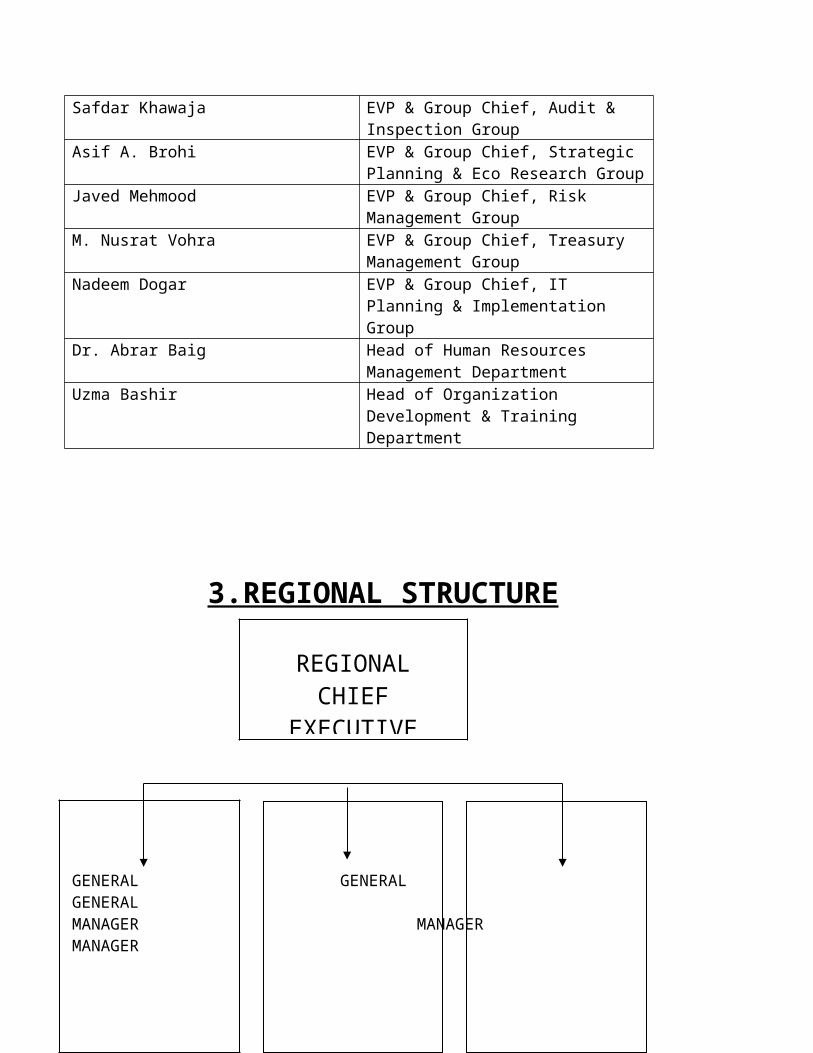

Eco Research GroupJaved Mehmood EVP & Group Chief, Risk Management

Group

REGIONALCHIEF

EXECUTIVE

M. Nusrat Vohra EVP & Group Chief, Treasury Management Group

Nadeem Dogar EVP & Group Chief, IT Planning & Implementation Group

Dr. Abrar Baig Head of Human Resources Management Department

Uzma Bashir Head of Organization Development & Training Department

3.REGIONAL STRUCTURE

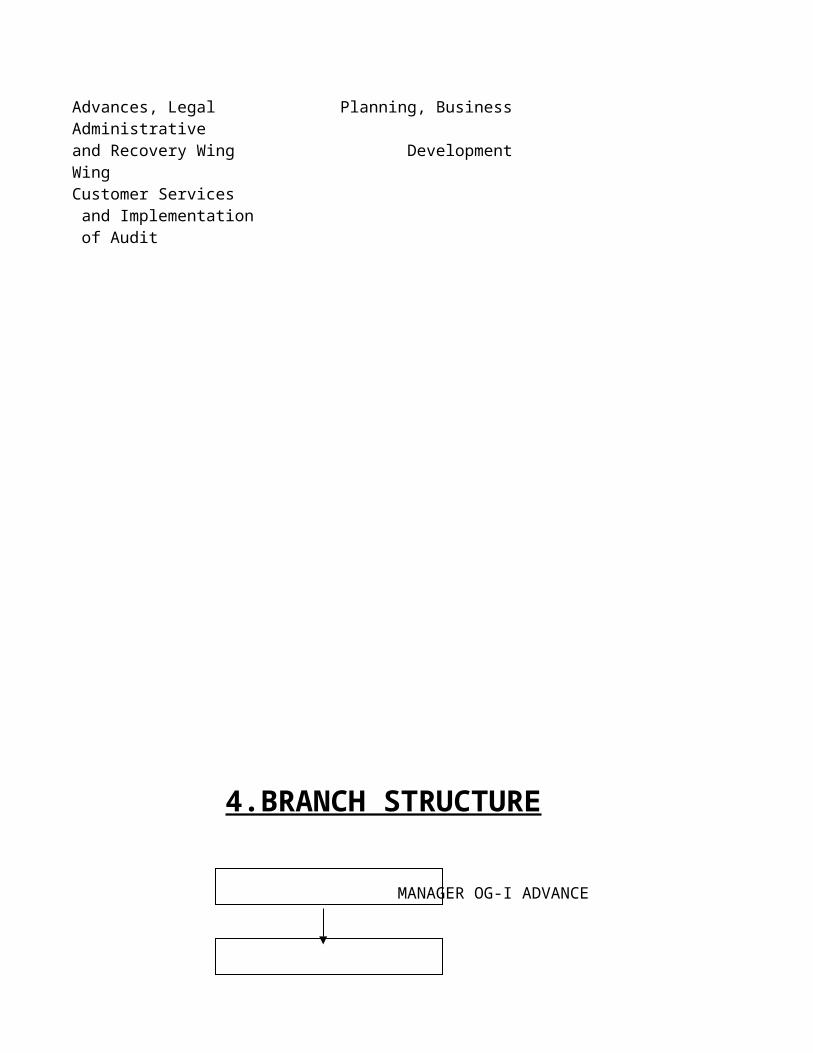

GENERAL GENERAL GENERALMANAGER MANAGER MANAGERAdvances, Legal Planning, Business Administrativeand Recovery Wing Development WingCustomer Services and Implementation of Audit

MESSANGER

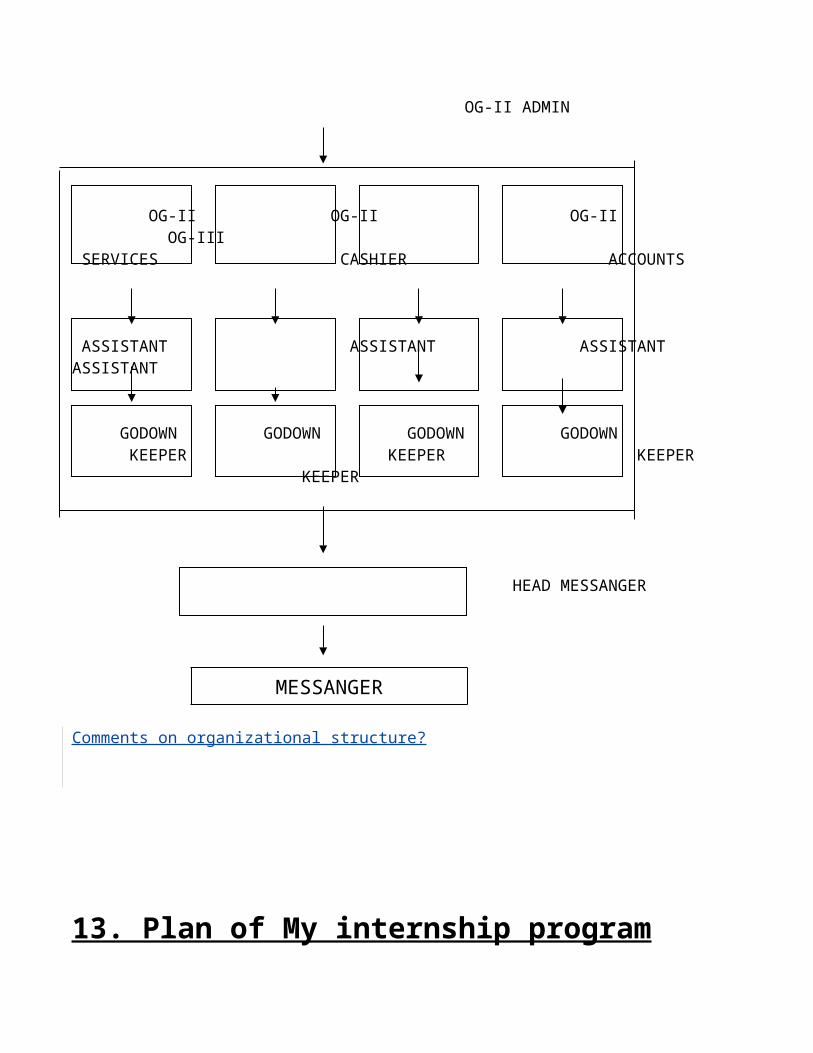

4.BRANCH STRUCTURE

MANAGER OG-I ADVANCE

OG-II ADMIN

OG-II OG-II OG-II OG-III SERVICES CASHIER ACCOUNTS

ASSISTANT ASSISTANT ASSISTANT ASSISTANT

GODOWN GODOWN GODOWN GODOWN KEEPER KEEPER KEEPER KEEPER

HEAD MESSANGER

Comments on organizational structure?

13. Plan of My internship programPlan of internship is not according to the format. You did not provide the starting and ending dates of internship program, brief introduction of the branch.Writing an Internship Program Plan

I carefully planed and wrote out my internship program and goals. The internship program and goals were measured by Bank management team and others in organization. Structuring the internship ahead of time provided me with tangible goals and objectives that enabled me to prove myself for understanding the importance of the organization’s decision-makers and value of a well-developed internship program.In creating my internship program plan, it includes specific ideas, proposals, and logistical information. I constructed my plan based on organization’s needs and resources. The questions that follow many assist me in formulating an internship program and plan.What about general support around the workplace? Does their organization need an intern to perform administrative and support functions including data entry, answering telephones, filing, etc.? If so, approximately what percentage of the intern’s time will be spent on these activities?

Does the Bank want to give the intern a taste of everything that company does? How will cross-training be structured into the intern’s schedule?

How much time will need to be devoted to department/area?

Have employees from each department been designated to mentor the intern on their particular department functions?

Will bank pay the intern? If so, how much?

Where should I do internship?

Do I have adequate workspace there?

Where will be the best environment and supportive persons etc.?

Who will have the primary responsibility for the intern?

Will that person be a mentor or merely a supervisor?

The assignment of mentor who will work closely with the intern can be essential in creating a successful experience for the organization and then intern. Ideally, the mentor should be someone from the department where the intern is working and who is very familiar with the projects and tasks the intern is working on. This person doesn’t have to be a teacher per se, but should be selected because he or she likes to teach or train and has the resources to do it. If the person you select has never mentored an intern before, providing basic supervision and mentoring guidelines and training may enhance the experience for both the mentor and the intern.

What will the intern be doing? Be as specific as possible.Interns, like others in the process of learning, need structure so they don’t become lost, confused or bored.

Do you want to plan a program beyond the work you give your interns? Will there be specific training programs, performance reviews, lunches with executives or social events? Keep in mind that your interns are walking advertisements for your company. If they have a good experience working for you, they’re likely to tell their friends—word gets around. A bad internship, by contrast, can only hurt your chances of attracting good students for next year.

Managing the Internship Starting out

I set up regular contact with the faculty sponsor. I Planed to email (meet) with your professor regularly over the term to discuss activities and review your internship and progress towards your academic learning objectives. At a minimum, plan on keeping in regular touch via email.Arrange regular meetings with site supervisor. It is vital you meet regularly with your site supervisor for direction, feedback, and answers to questions. Ideally this should be weekly, or at least bi-weekly. I completed the required Orientation Check In form. After your first couple of weeks working in your site, complete this form and return it to the Internship Program office. It is very important that you get a solid start in your internship, and this is largely determined by how well you are initially oriented and trained. I used the form as a way to talk with my supervisor to identify areas i need or want additional direction. This communication helps our office identify internships that may warrant a bit more attention early on to help make productive for me. Also, on the form I am asked to note my work schedule so we can begin planning site visits for the middle of the term.

During the internship

I completed the required Evaluation of Intern form. I met with my site supervisor to review, signed and returned this form to the Internship Program office by the requested date. Site visit. The Internship Program Director and/or my faculty sponsor may contacted me to arrange a site visit to meet with me and my supervisor. This is a wonderful chance to discuss how the internship is going and to share some of the work you are doing in the internship. Problems? If, at any point during the internship, I was having problems that were interfering with the quality of the learning experience, I contacted the Internship Program Director for support and assistance.

Finishing up

I completed the required Final Evaluation of Intern form. As I approached the end of the term, met with my site supervisor to review and signed this form and returned it to the Internship Program office. A copy of this is sent to your faculty sponsor who uses it to help determine a final grade for your internship experience.Closure with my host organization I communicated in writing my appreciation to my supervisor and co-workers for the attention and management they provided me during my internship. This is an important professional courtesy and can benefit me in future networking.Closure with my Instructor I arranged a final meeting with my by mail instructor to review the internship, discuss future plans, and submit my required assignment(s) as outlined in my Learning Contract. This must be done prior to the last day of class for the semester so my Instructor has time to submit a grade for your internship.

Irrelevant data has been provided in this section.

14.DEPARTMENTALIZATION

Dividing an organization into different parts according to the functions is called departmentalization. So NBP is divided into Departments.

1. CASH DEPARTMENT

2. CLEARANCE DEPARTMENT

3. ADVANCES DEPARTMENT

4. REMITTANCE DEPARTMENT

5. Department of HUMAN RESOURCE MANAGEMENT

6. DEPOSIT DEPARTMENT: -

7. FOREIGN EXCHANGE/DEPARTMENT:

1. CASH DEPARTMENT Cash department performs the following functions1.1) Receipt The money, which either comes or goes out from the bank, its record should be kept. Cash department performs this function. The deposits of all customers of the bank are controlled by means of ledger accounts. Every customer has its own ledger account and has separate ledger cards.Payments It is a banker’s primary contract to repay money received for this customer’s account usually by honoring his cheques.1.3) Cheques and their Payment The Negotiable Instruments. Act, 1881, “Cheque is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand”. Since a Cheque has been declared to be a bill of exchange, it must have all its characteristics as mentioned in Section 5 of the Negotiable Instruments Act, 1881. Therefore, one can say that a Cheque can be defined as an:“An unconditional order in writing drawn on a specified banker, signed by the drawer, requiring the banker to pay on demand a sum certain in money to, or to the order of, a specified person or to the bearer, and which does not order any act to be done in addition to the payment of money”. (Law of Banking by Dr. Hart, p.327).1.4) the Requisites of Cheque There is no prescribed form of words or design of a Cheque, but in order to fulfill the requirements mentioned in Section 6 above the Cheque must have the following.

It should be in writing The unconditional order Drawn on specific banker only Payment on Demand Sum Certain in money Payable to a specific person Signed by the drawer

1.5) Parties to Cheque The normal Cheque is one in which there is a drawer, a drawee banker and a payee, or no payee but bearer.

The Drawer The Drawee The Payee

1.6) Types of Cheques Bankers in Pakistan deal with three types of chequesa) Bearer Cheques Bearer cheques are cashable at the counter of the bank. These can also be collected through clearing.b) Order cheque

These types of cheques are also cashable on the counter but its holder must satisfy the banker that he is the proper man to collect the payment of the cheque and he has to show his identification. It can also be collected through clearing. c) Crossed Cheque These cheques are not payable in cash at the counters of a banker. It can only be credited to the payee’s account. If there are two persons having accounts at the same bank, one of the account holder issues a cross-cheque in favour of the other account holder. Then the cheque will be credited to the account of the person to whom the cheque was issued and debited from the account of the person who has actually issued the cheque.

1.7) Payment of Cheques It is a banker’s primary contract to repay money received for his customer’s account usually by honouring his cheques. Payment of money deposited by the customer is one of the root functions of banking. The acid test of banking is the receipt of money etc. from the depositors, and repayment to them. This paying function is one, which is the distinguishing mark of a banker and differentiates him from other institutions, which receive money from the public. However the bankers’ legal protection is only when payment is in ‘Due Course’. The payment in due course means payment in accordance with the apparent tenor of the instrument, in good faith and without negligence to any person in possession thereof under circumstances, which do not afford a reasonable ground of believing that he is not entitled to receive payment of the amount therein mentioned. It is a contractual obligation of a banker to honor his customer’s cheques if the following essentials are fulfilled.

Cheques should be in a proper form: Cheque should not be crossed: Cheque should be drawn on the particular bank: Cheque should not mutilated: Funds must be sufficient and available: The Cheque should not be post dated or stale: Cheque should be presented during banking hours:

2. CLEARANCE DEPARTMENT A clearinghouse is an association of commercial banks set up in given locality for the purpose of interchange and settlement of credit claims. The function of clearinghouse is performed by the central bank of a country by tradition or by law. In Pakistan, the clearing system is operated by the SBP. If SBP has no office at a place, then NBP, as a representative of SBP act as a clearinghouse.

After the World War II, a rapid growth in banking institutions has taken place. The use of cheques in making payments has also widely increased. The collection as settlement of mutual obligations in the form of cheques is now a big task for all the commercial bank. When Cheque is drawn on one bank and the holder (payee) deposits the same in his account at the bank of the drawer, the mutual obligation are settled by the internal bank administration and there arises no inter bank debits from the use of cheques. The total assets and total liabilities of the bank remain unchanged.

In practice, the person receiving a Cheque as rarely a depositor of the cheque at the same bank as the drawer. He deposits the cheque with his bank other than of payer for the collection of the amount. Now the bank in which the cheque has been deposited becomes a creditor of the drawer’s bank. The depositor bank will pay his amount of the cheque by transferring it from cash reserves if there are no offsetting transactions. The banks on which the cheques are drawn become in debt to the bank in which the cheques are deposited. At the same time, the creditors’ banks receive large amounts of cheques drawn on other banks giving claims of payment by them.

The easy, safe and most efficient way is to offset the reciprocal claims against the other and receive only the net amount owned by them. This facility of net inter bank payment is provided by the clearinghouse.

The representatives of the local commercial banks meet at a fixed time on all the business days of the week. The meeting is held in the office of the bank that officially performs the duties of clearinghouse. The representatives of the commercial banks deliver the cheques payable at other local banks and receive the cheques drawn on their bank. The cheques are then sorted according to the bank on which they are drawn. A summary sheet is prepared which shows the names of the banks, the total number of cheques delivered and received by them. Totals are also made of all the cheques presented by or to each bank. The difference between the total represents the amount to be paid by a particular bank and the amount to be received by it. Each bank then receives the net amount due to it or pays the net amount owed by it.

2.1) In-Word Clearing Books The bank uses this book for the purpose of recording all the cheques that are being received by the bank in the first clearing. All details of the cheques are recorded in this book. 2.2) Out-Word Clearing Book: The bank uses outward clearing register for the purpose of recording all the details of the cheques that the bank has delivered to other banks.

3. ADVANCES DEPARTMENT

Advances department is one of the most sensitive and important departments of the bank. The major portion of the profit is earned through this department. The job of this department is to make proposals about the loans. The Credit Management Division of Head Office directly controls all the advances. As we known bank is a profit seeking institution. It attracts surplus balances from the customers at low rate of interest and makes advances at a higher rate of interest to the individuals and business firms. Credit extensions are the most important activity of all financial institutions, because it is the main source of earning. However, at the same time, it is a very risky task and the risk cannot be completely eliminated but could be minimized largely with certain techniques. Any individual or company, who wants loan from NBP, first of all has to undergo the filling of a prescribed form, which provides the following information to the banker.

3.1) Name and address of the borrower.

Existing financial position of a borrower at a particular branch.Accounts details of other banks (if any).

Security against loan. Exiting financial position of the company. (Balance Sheet & Income Statement). Signing a promissory note is also a requirement of lending, through this note borrower

promise that he will be responsible to pay the certain amount of money with interest.

3.2) Principles of Advances

There are five principles, which must be duly observed while advancing money to the borrowers.

Safety Character Capacity Capital Liquidity Dispersal Remuneration Suitability Forms of Loans Cash Finance Overdraft/Running Finance Demand Financing/Loans

a. Safety Banker’s funds comprise mainly of money borrowed from numerous customers on various accounts such as Current Account, Savings Bank Account, Call Deposit Account, Special Notice Account and Fixed Deposit Account. It indicates that whatever money the banker holds is that of his customers who have entrusted the banker with it only because they have full confidence in the expert handling of money by their banker. Therefore, the banker must be very careful and ensure that his depositor’s money is advanced to safe hands where the risk of loss does not exist. The elements of character, capacity and capital can help a banker in arriving at a conclusion regarding the safety of advances allowed by him. b. CharacterIt is the most important factor in determining the safety of advance, for there is no substitute for character. A borrower’s character can indicate his intention to repay the advance since his honesty and integrity is of primary importance. If the past record of the borrower shows that his integrity has been questionable, the banker should avoid him, especially when the securities offered by him are inadequate in covering the full amount of advance.

It is obligation on the banker to ensure that his borrower is a person of character and has capacity enough to repay the money borrowed including the interest thereon.

c. CapacityThis is the management ability factor, which tells how successful a business has been in the past and what the future possibilities are. A businessman may not have vast financial resources, but with sound management abilities, including the insight into a specific business, he may make his business very profitable. On the other hand if a person has no insight into the particular business for which he wants to borrow funds from the banker, there are more chances of loss to the banker.

d. CapitalThis is the monetary base because the money invested by the proprietors represents their faith in the business and its future. The role of commercial banks is to provide short-term capital for commerce and industry, yet some borrowers would insist that their bankers provide most of the capital required. This makes the banker a partner. As such the banker must consider whether the amount requested for is reasonable to the borrowers own resources or investment.

e. Liquidity Liquidity means the possibilities of recovering the advances in emergency, because all the money borrowed by the customer is repayable in lump sum on demand. Generally the borrowers repay their loans steadily, and the funds thus released can be used to allow fresh loans to other borrowers. Nevertheless, the banker must ensure that the money he is lending is not blocked for an undue long time, and that the borrowers are in such a financial position as to pay back the entire amount outstanding against them on a short notice. In such a situation, it is very important for a banker to study his borrower’s assets to liquidity, because he would prefer to lend only for a short period in order to meet the shortfalls in the wording capital. If the borrower asks for an advance for the purchase of fixed assets the banker should refuse because it shall not be possible for him to repay when the banker wants his customer to repay the amount. Hence, the baker must adhere to the consideration of the principles of liquidity very careful.

f. Dispersal The dispersal of the amount of advance should be broadly based so that large number of borrowing customer may benefit from the banker’s funds. The banker must ensure that his funds are not invested in specific sectors like textile industry, heavy engineering or agriculture. He must see that from his available funds he advances them to a wide range of sector like commerce, industry, farming, agriculture, small business, housing projects and various other financial concerns in order of priorities.Dispersal of advances is very necessary from the point of security as well, because it reduces the risk of recovery when something goes wrong in one particular sector or in one field.

g. Remuneration A major portion of the banker’s earnings comes form the interest charged on the money borrowed by the customers. The banker needs sufficient earnings to meet the following:Interest payable to the money deposited with him.

Salaries and fringe benefits payable to the staff members.

Overhead expense and depreciation and maintenance of the fixed assets of the bank. An adequate sum to meet possible losses. Provisions for a reserve fund to meet unforeseen contingencies. Payment of dividends to the shareholders.

h. Suitability The word “suitability’ is not to be taken in its usual literary sense but in the broader sense of purport. It means that advance should be allowed not only to the carefully selected and suitable borrowers but also in keeping with the overall national development plans chalked out by the authorities concerned. Before accommodating a borrower the banker should ensure that the lending is for a purpose in conformity with the current national credit policy laid down by the central bank of the country.

i. Forms of Loans In addition to purchase and discounting of bills, bankers in Pakistan generally lend in the form of cash finance, overdrafts and loans. NBP provides advances to different people in different ways as the case demand.

j. Cash Finance This is a very common form of borrowing by commercial and industrial concerns and is made available either against pledge or hypothecation of goods, produce or merchandise. In cash finance a borrower is allowed to borrow money from the banker up to a certain limit, either at once or as and when required. The borrower prefers this form of lending due to the facility of paying markup/services charges only on the amount he actually utilizes. If the borrower does not utilize the full limit, the banker has to lose return on the un-utilized amount. In order to offset this loss, the banker may provide for a suitable clause in the cash finance agreement, according to which the borrower has to pay markup/service charges on at least on self or one quarter of the amount of cash finance limit allowed to him even when he does not utilize that amount.

k. Overdraft/Running Finance This is the most common form of bank lending. When a borrower requires temporary accommodation his banker allows withdrawals on his account in excess of the balance which the borrowing customer has in credit, and an overdraft thus occurs. This accommodation is generally allowed against collateral securities. When it is against collateral securities it is called “Secured Overdraft” and when the borrowing customer cannot offer any collateral security except his personal security, the accommodation is called a “Clean Overdraft”. The borrowing customer is in an advantageous position in an overdraft, because he has to pay service charges only on the balance outstanding against him. The main difference between a cash finance and overdraft lies in the fact that cash finance is a bank finance used for long term by commercial and industrial concern on regular basis, while an overdraft is a temporary accommodation occasionally resorted to.

l. Demand Financing/Loans When a customer borrows from a banker a fixed amount repayable either in periodic installments or in lump sum at a fixed future time, it is called a “loan”. When bankers allow

loans to their customers against collateral securities they are called “secured loans” and when no collateral security is taken they are called “clean loans”.The amount of loan is placed at the borrower’s disposal in lump sum for the period agreed upon, and the borrowing customer has to pay interest on the entire amount. Thus the borrower gets a fixed amount of money for his use, while the banker feels satisfied in lending money in fixed amounts for definite short periods against a satisfactory security

4. REMITTANCE DEPARTMENT Remittance means a sum of money sent in payment for something. This department deals with either the transfer of money from one bank to other bank or from one branch to another branch for their customers. NBP offers the following forms of remittances.

Demand Draft Telegraphic Transfer Pay Order Mail Transfer

4.1) Demand Draft Demand draft is a popular mode of transfer. The customer fills the application form. Application form includes the beneficiary name, account number and a sender’s name. The customer deposits the amount of DD in the branch. After the payment the DD is prepared and given to the customer. NBP officials note the transaction in issuance register on the page of that branch of NBP on which DD is drawn and will prepare the advice to send to that branch. The account of the customer is credited when the DD advice from originating branch comes to the responding branch and the account is debited when DD comes for clearance. DD are of two types.

Open DD: Where direct payment is made. Cross DD: Where payment is made though account.

NBP CHARGES FOR DD5 Up to Rs. 50,000/- is Rs 50/- only Over Rs. 50,000/- is 0.1%

4.2) Pay Order Pay order is made for local transfer of money. Pay order is the most convenient, simple and secure way of transfer of money. NBP takes fixed commission of Rs. 25 per pay order from the account holder and Rs. 100 from a non-account holder.

4.3) Telegraphic Transfer Telegraphic transfer or cable transfer is the quickest method of making remittances. Telegraphic transfer is an order by telegram to a bank to pay a specified sum of money to the specified person. The customer for requesting TT fills an application form. Vouchers are prepared and sent by ordinary mail to keep the record. TT charges are taken from the customer. No excise duty is charged on TT. The TT charges are:Telegram/ Fax Charges on TT = Actual-minimum Rs.125.

Cable telegram transfer costs more as compared to other title of money. In cable transfer the bank uses a secret system of private code, which is known to the person concerned with this department and branch manager.

4.4) Mail Transfer When the money is not required immediately, the remittances can also be made by mail transfer (MT). Here the selling office of the bank sends instructions in writing by mail to the paying bank for the payment of a specified amount of money. Debiting to the buyer’s account at the selling office and crediting to the recipient’s account at the paying bank make the payment under this transfer. NBP taxes mail charges from the applicant where no excise duty is charged. Postage charges on mail transfer are actual minimum Rs. 40/- if sent by registered post locally Rs.40/- if sent by registered post inland on party’s request.

5. Department of HUMAN RESOURCE MANAGEMENT Human Resource plays a vital role in the success of every service organization. They interact between man and machine. Their attitude can win or loose the customer. The positive attitude could only be created in a conducive environment, which can make the staff dedicated towards the organization and its objectives. In reality the man is more important than machine as it is the human which could get maximum out of machine to keep a happy customer. However, most organizations give little importance to this very important asset.Various aspects related to human resource of National Bank of Pakistan are critically examined in the following text:

5.1) Selection & Recruitment Although the Bank believes in merit but in practice the selection of employees is not done on merit. Most of the employees are low educated. This shows that candidates with some strong family background or political pressure are given preference in recruitment and qualified candidates are sometimes left behind.

5.2) Job for Life Like the employee of public sector organizations in Pakistan, the employees of NBP also enjoy their job for life. Since there is no risk of early retirement or redundancy in rank, they do not perform with their full potentials. This is one redundancy in rank, they do not perform with their full potentials, and this is one of the reasons responsible for the low productivity of the employees of the Bank.

5.3) Performance Appraisal The performance of employees of the Bank are appraised though their annual confidential reports at the end of each year. This has become an outdated method of performance appraisal and no longer used due to the following reasons:

The performance of employees is evaluated after quite a long time. Element of subjectivity is involved in this method. Employee’s participation is not ensured in the process of evaluation. Objectives of employee’s are not quantified.

5.4) Inter Personal Relationship Modern management acknowledges human resources as one ‘of the most important assets of an organization. But by their very nature, human beings are also the most unpredictable. Where a number of persons work together, interactions among them, of necessity, will lead to conflicts and NBP is no exception. Most interpersonal conflicts in NBP can be traced back to the following major heads.

Lack of Communication Lack of communication is for the biggest reason for conflicts. Not only it is due to the failure to send a massage but to an interpretation given to the

massage by the receiver is different from that intended.

5.5) Diversity in Values Diversity in values, perceptions, cultural background and life-style is another reason responsible for inter personal conflicts in NBP. Different values and perceptions about the same issue, event or personality hinder understanding. When things come to such a pavement, therefore, interpersonal conflicts are generated.The dominant trend in all modern industrial societies of the world is merit and expertise, which helps promote cohesion and reduce conflicts. But the feudalistic mindset is still very strong in our set up and there is no tradition of tolerance for differing viewpoints. Hence, interpersonal conflicts are generated.

5.6) Corruption Our social acceptance of corruption gives rise to corruption at every level of social and organizational set up. Corruption involves financial embezzlement, favoritism, nepotism, cronyism and other number of such practices. All these cause resentment that keep building up and lead to conflict sooner or later. In the past few years, some cases of frauds have happened in different branches. The reasons can be linked with the employee dissatisfaction of NBP.

5.7) Discipline & Authority Maintaining discipline and implementation of authority (tables) in letter and spirit is the key to success of any organization. In NBP, The authority tables are not strictly maintained. Line managers are not fully equipped with the authority with no vertical or horizontal interference.

6.) DEPOSIT DEPARTMENT: -

It controls the following activities:

A/C opening. Issuance of cheque book. Current a/c Saving a/c Cheque cancellation Cash

6.1) Account opening The opening of an account is the establishment of banker customer relationship. Before a banker opens a new account, the banker should determine the prospective customer’s integrity, respectability, occupation and the nature of business by the introductory references given at the time of account opening. Preliminary investigation is necessary because of the following reasons.

Avoiding frauds Safe guard against unintended over draft. Negligence. Inquiries about clients.

There are certain formalities, which are to be observed for opening an account with a bank. Formal Application Introduction Specimen Signature Minimum Initial Deposit Operating the Account Pay-In-Slip Book Pass Book Issuing Cheque Book

6.1.1) Qualification of Customer The relation of the banker and the customer is purely a contractual one, however, he must have the following basic qualifications.

He must be of the age of majority. He must be of sound mind. Law must not disqualify him.

The agreement should be made for lawful object, which create legal relationshipNot expressly declared void.

6.1.2) Types of Accounts Following are the main types of accounts

Individual Account Joint Account Accounts of Special Types Partnership account Joint stock company account Accounts of clubs, societies and associations Agents account Trust account Executors and administrators accounts Pak rupee non-resident accounts Foreign currency accounts

6.2 Issuing of cheque book:

This deptt issue cheque books to account holders.Requirements for issuing cheque book

The account holder must sign the requisition slip Entry should be made in the cheque book issuing book Three rupees per cheque should be recovered from a/c holder if not then debit his/her

account.

6.3 Current account These are payable to the customer whenever they are demanded. When a banker accepts a demand deposit, he incurs the obligation of paying all cheques etc. drawn against him to the extent of the balance in the account. Because of their nature, these deposits are treated as current liabilities by the banks. Bankers in Pakistan do not allow any profit on these deposits, and customers are required to maintain a minimum balance, failing which incidental charges are deducted from such accounts. This is because the depositors may withdraw Current Account at any time, and as such the bank is not entirely free to employ such deposits.Until a few decades back, the proportion of Current Deposits in relation to Fixed Deposits was very small. In recent years, however, the position has changed remarkably. Now, the Current Deposits have become more important; but still the proportion of Current Deposits and Fixed Deposits varies from bank to bank, branch to branch, and from time to time.

6.4) Saving account

Savings Deposits account can be opened with very small amount of money, and the depositor is issued a cheque book for withdrawals. Profit is paid at a flexible rate calculated on six-month basis under the Interest-Free Banking System. There is no restriction on the withdrawals from the deposit accounts but the amount of money withdrawn is deleted from the amount to be taken for calculation of products for assessment of profit to be paid to the account holder. It discourages unnecessary withdrawals from the deposits. In order to popularize this scheme the State Bank of Pakistan has allowed the Savings Scheme for school and college students and industrial labor also. The purpose of these accounts is to inculcate the habit of savings in the constituents. As such, the initial deposit required for opening these accounts is very nominal.

6.5) Cheque cancellation: This deptt can cancel a cheque on the basis of;

Post dated cheque Stale cheque Warn out cheque Wrong sign etc

6.6) Cash This deptt also deals with cash. Payment of cheques, deposits of cheques etc.

7. FOREIGN EXCHANGE/DEPARTMENT:

This deptt mainly deals with the foreign business. The main functions of this deptt are: L/C dealing. Foreign currency accounts dealing. Foreign Remittance dealing.

7.1) L/C dealing NBP is committed to offering its business customers the widest range of options in the area of money transfer. If you are a commercial enterprise then our Letter of Credit service is just what you are looking for. With competitive rates, security, and ease of transaction, NBP Letters of Credit are the best way to do your business transactions. 7.2) Foreign currency account dealing: This deptt deals with the foreign currency accounts which mainly include dollar account, euro account etc. 7.3) Foreign Remittance dealing.This is very important function of this deptt.

15. DEPARTMENTATION OF NBP BAHAWALNAGAR MAIM BRANCH.

I did internship in Main branch BWN (Bahawalnagar) in Punjab province. Here the Manager, Muhammad Arshad Nagra and the Operational Manager Muhammad Amin and other staff members give full assistance and cooperation during my internship period. The stating date was November11 2008 and ending date was December 22 2008 of my internship period. This is the core section of your internship report. You should provide the detailed description of the tasks assigned to you during your internship program, and this section should be under training program.The tasks assigned to me during internship duration.During the internship period I was assigned the tasks as fallow:1. Data entry in computer2. Maintaining D.Ds and T.Ts. Registers 3. Customer Dealing about the bank’s products4. Maintaining the cash department.5 Maintaining the I.T Department6. Accounts opening and closing7. Online banking8. Maintaining saving and current accounts.9. Observing the managerial decision making

Dividing an organization into different parts according to their functions is called departmentation. So NBP Bahawalnagar branch is divided into parts.

Cash Department General Banking Departments

1. Cash Department:

Cash department mainly deals in cash. The Head of department is Mr. Umair Rao and two cashier Maher Shah and Muhammad Ali.

The objective of cash department:

“To facilitate people in the payments of their bills and taxes and repayments of cash”There are two main functions of cash department.

i. Payment ii. Receipts

Payments are the function that they pay their cheques and pay cash. Receipts mean collection of utilities bills, taxes etc.

2. General Banking Departments In this section of the bank the general banking function is performed. It is divided into five departments.

Remittances Department. Computer Department. Advances Department. Clearing Department. Establishment Department.

2.1 Remittances Department:This department is header by Zahid Ahmad a very competent person. The objective of this department is:-

“To transfer the money of people from one place to another place in safe and comparable way”The main functions of this department are:

Issuing of demand draft. Issuing of Mail transfer. Issuing of Telegraphic transfer. Issuing of payment order. Issuing of call deposit. Pension payments etc. Closing and scrolling of government collections.

2.2 Advances department:Every bank has a department which advances money to borrowers. In NBP

Bahawalnagar branch the advances department is head by the Business Manager Sir Asim and Operation Manager Sir Amin. Both are very competent persons. The objective of Advances Department is

“To facilitate people by giving short term and long term loans on easy terms and conditions”.The main function of this Department is to take surplus money from the people at low rates and lend this money to borrowers at high rates to earn profit.

2.3 Clearing Department: A clearing house is an association of commercial banks set in State Bank of Pakistan for the purpose of interchange and settlement of credit claims.In NBP Bahawalnagar Branch this department is headed by Ameer Shehzad having experience of about thirty years. The objective of this department is to “To facilitate customers for payment their Cheques of other banks”.

Two type of clearing books are maintained.

i) In word clearing books:The bank uses this book for the purpose of recording all the cheques that are being received by the bank in the first clearing. All detail of the cheques are recorded in this book.ii) Out word clearing book:The bank uses outward clearing register for the purpose of recording all the details of the cheques that the banks have delivered to other banks.

2.4 Computer Department: This department headed by the accountant Mr.Saad and two other persons Mr. Junaid and Mr. Shahid are performing the real function.

The objective of this Department is to facilitate customers in payment of their cheques”.The main functions performed by this department are:

Checking balance. Deduction from balance on clearing cheques. Issuing bank statements. Dealing Western Union.

2.5 Establishment Department: NBP Bahawalnagar Branch having an Establishment Department. This Department consists of only one person Nasir Baig very competent and experienced person. This department mainly deals with the branch employees. The main objective of this department is to “To regulate bank business”.

Main functions of this department are: Keeps the record of attendance of employees. Employee’s salaries distribution. Employee’s bonuses etc.

16.General observation during Training Program

TRAINING SUBSTANCE

In this section topic discussed is as under:

Work performed by me

Tasks assigned to you should be under this section.Tasks assigned to you should be under this section.

WORK PERORMEDBY ME

I joined National Bank of Pakistan, Main Branch Bahawalnagar on 11th November, 2008. First day, the manager introduced me about the functioning of the branch and the staff. The manager told me that counter is the most important place of the bank. During the six weeks of my internship, I worked in different departments of the branch and did the maximum practice of banking system details of which is as under:

GENERAL BANKING

First of all, I was asked to work in different sections of general banking. I was attached to

Counter with Mr. Kashif who has good command on this section. Here we dealt with new

customer who wanted to get information and to deal with the branch. This is a very interesting

department because here we met people of different types and deal with them accordingly. In this

section, I observed the following functions: