diwali special picks - religare · pdf filebajaj corp holds the lion’s share in the...

TRANSCRIPT

Diwali Special Picks

Rationale The company has shown strong financial

performance in recent quarters as low raw material

prices aided the growth. The earning trajectory is

likely to continue in the near future as well due to

soft raw material prices.

The company has signed an MOU with the Govt. of

Andhra Pradesh for setting up 400,000 KL paint

manufacturing facility at Vishakhapatnam district. It

has a capex plan of Rs 700 for FY16.

The company is also in discussions with the Govt. of

Karnataka to set up another paint manufacturing

facility at Mysuru district. Both these proposals are

towards fulfilling the long term capacity

requirements and are subject to the demand

conditions.

The company continues to remain very cautious on

the domestic demand outlook. However, its

industrial products demand would need further

push in investments to see sustainable growth.

Asian Paints Ltd Sector : Paints

CMP – ` 814.2 Target – ` 935 BSE Code : 500820

NSE Code : ASIANPAINT

Key Data

Market Cap (` Cr) 79455

Equity Cap (` Cr) 95.92

Face Value 1

Book Value 52.36

RoE (%) 33.9

52 Week High-Low 926.80 / 637

Avg Volume (Wkly) 2311454

Price Chart

Financial Summary - (` Cr)

Revenue EBITDA Adj. PAT Adj.EPS (`) EV /

EBITDA (x) P/BV(x) P/E (x)

FY14 12581.6 1864.7 1208.9 12.8 43.9 20.4 67.0

FY15 14005.3 2057.9 1367.6 14.8 40.0 17.4 57.9

FY16E 15200.2 2603.9 1823.6 19 31.7 14.2 45.2

FY17E 17634.8 3186.0 2229.3 23.2 25.6 11.6 36.9

Rationale Bajaj Corp Ltd (BCL) is one of India's leading FMCG

company with major brands in Hair care category.

Bajaj Corp holds the lion’s share in the light hair oil

segment. Bajaj Almond Drops Hair Oil is the second

largest brand in the overall hair-oil segment, with

over 60% market share of the light hair-oil market.

Bajaj NOMARKS cream is currently No. 1 cream in

the Anti-Marks segment & Bajaj NOMARKS Face

Wash is currently the 2nd largest Anti-Marks Face

wash. Its growth strategy focuses on converting

coconut hair-oil users to light hair-oil (LHO) through

sampling, targeted advertising, campaigns, product

innovation and creating awareness about product

differentiation including communicating the

advantages of LHO.

The company seeks to consolidate its position in

FMCG segment by continuously evaluating

inorganic acquisition opportunities. The inorganic

growth opportunities will focus on targeting niche

brands which can benefit from BCL’s strong

distribution network.

Bajaj Corp Ltd Sector : FMCG

CMP – ` 415.7 Target – ` 500 BSE Code : 533229

NSE Code : BAJAJCORP

Key Data

Market Cap (` Cr) 6185

Equity Cap (` Cr) 14.75

Face Value 1

Book Value 39.74

RoE (%) 40.54

52 Week High-Low 522 / 265.20

Avg Volume (Wkly) 119827

Price Chart

Financial Summary - (` Cr)

Revenue EBITDA Adj. PAT Adj.EPS (`) EV /

EBITDA (x) P/BV(x) P/E (x)

FY14 671.7 186.0 177.5 12.0 33.9 12.5 36.5

FY15 825.6 239.2 219.6 14.9 26.6 13.3 29.5

FY16E 949.7 294.6 257.9 17.5 21.6 11.8 25.2

FY17E 1096.7 336.8 293.7 19.9 18.9 10.6 22.1

Diwali Special Picks

Rationale Divi’s Lab is engaged in manufacture of generic APIs

and custom synthesis of APIs, wherein; it caters to

innovator Pharma companies for their patented

products through its custom synthesis basis. The

company operates predominantly in export markets

and has a broad product portfolio under generics

and custom synthesis.

The company has been able to register high profits

even during the down cycles, a lot of credit for this

goes to Divis’ strategy of leveraging on its India-

centric low-cost manufacturing base and not

focusing much on the acquisitions abroad as the

cost of manufacturing in India is less than half that

of regulated countries.

Divi’s Labs’ new plant at Kakinada, Andhra Pradesh,

is expected to commence operations by mid of

FY17; this would boost the growth for the company.

Also the contribution from the company’s

carotenoids business which registers a healthy profit

margin is expected to increase significantly in the

near term.

Divi’s Laboratories Ltd Sector : Pharmaceuticals

CMP – ` 1189.6 Target – ` 1305 BSE Code : 532488

NSE Code : DIVISLAB

Key Data

Market Cap (` Cr) 29460

Equity Cap (` Cr) 53.09

Face Value 2

Book Value 134.18

RoE (%) 25.68

52 Week High-Low 1242.35/786

Avg Volume (Wkly) 276220

Price Chart

Financial Summary - (` Cr)

Revenue EBITDA Adj. PAT Adj.EPS (`)

EV / EBITDA

(x) P/BV(x) P/E (x)

FY14 2518.7 1039.1 773.3 29.1 27.8 9.7 37.4

FY15 3095.9 1149.1 851.5 32.1 25.1 8.3 33.9

FY16E 3845.2 1499.6 1127.8 42.5 19.2 6.9 25.6

FY17E 4575.8 1738.8 1311.1 49.4 16.6 5.7 22.0

Diwali Special Picks

Rationale The bank has reported robust financial performance

over the past five years. Its net profit has grown a

CAGR of 38.63% and Net Interest Income (NII) has

grown by 31%. During FY15 its net profit has grown

by 27.4% to Rs 1793.72 crore and net interest

income has grown by 18.3% to Rs 3420.28 cr.

IndusInd Bank net profit has grown by 25% over the

past nine quarters. The net interest margin, has

remained in a narrow but robust band of 3.6% to

3.8%, while its gross non-performing assets ratio

was between 0.8% and 1.1%.

The bank is focusing on growing its retail book

faster and aims to take the retail book to 48% of

total loans versus 42% currently. The bank is

confident of maintaining the margins even in a

falling interest rate cycle, on the back of levers such

as a fixed-rate vehicle finance book (25% of loan

book), improvement in Casa, or current and savings

accounts, and loan book rebalancing.

IndusInd Bank Ltd Sector : Private Banks

CMP – ` 911.85 Target – ` 1200 BSE Code : 532187

NSE Code : INDUSINDBK

Key Data

Market Cap (` Cr) 54734

Equity Cap (` Cr) 592.21

Face Value 10

Book Value 277.06

RoE (%) 18.98

52 Week High-Low 989.30 / 685.70

Avg Volume (Wkly) 1752512

Price Chart

Financial Summary (Consolidated) - (` Cr)

Net Interest

Income

Pre-Provisions

Profit Adj. PAT Adj.EPS (`)

Gross NPA

(%) P/BV(x) P/E (x)

FY14 2890.7 2596.0 1408.0 26.9 1.1 5.5 35

FY15 3420.3 3098.2 1793.7 34.0 0.8 4.7 27.6

FY16E 4367.7 3997.5 2354.0 43.4 0.9 3.5 21.7

FY17E 5506.9 5025.3 2995.7 53.9 0.8 2.9 17.4

Diwali Special Picks

Rationale The company has started commercial production at

its new greenfield integrated cement plant from

September 2015. The new project, located near

Chittapur, District Gulbarga, Karnataka has an

installed capacity of 3.0 million tonnes per annum

(MTPA). With the commissioning of this new unit,

the total installed capacity of Orient Cement has

increased to 8 MTPA. The company has planned to

reach 15 million tonnes per annum (MTPA) capacity

by year 2020.

During H1 FY16, the company posted muted

performance. Its net profit fell 28.5% to Rs 55.91

crore on 8% decline in total income to Rs 708.99

crore (YoY). We expect a rebound in the next fiscal

with the commissioning of new 3 MTPA plant at

Karnataka.

As cement demand stayed low during the year, the

company saw an opportunity to enhance value

across dimensions by making a strategic shift

towards PPC (Portland Pozzolana Cement) cement.

Orient Cement Ltd Sector : Cement

CMP – ` 157.9 Target – ` 210 BSE Code : 535754

NSE Code : ORIENTCEM

Key Data

Market Cap (` Cr) 3459

Equity Cap (` Cr) 20.49

Face Value 1

Book Value 50.34

RoE (%) 21.59

52 Week High-Low 199.75 / 128

Avg Volume (Wkly) 46143

Price Chart

Financial Summary (Consolidated) - (` Cr)

Revenue EBITDA Adj. PAT Adj.EPS (`)

EV / EBITDA (x)

P/BV(x) P/E (x)

FY14 1430.2 206.5 101.0 4.9 17.1 4.3 35.2

FY15 1535.3 295.0 194.8 9.5 12.9 3.6 18.3

FY16E 1515.1 261.4 155.9 7.6 17.7 3.3 22.8

FY17E 2386.7 511.3 249.6 12.2 9.3 2.7 14.3

Diwali Special Picks

Disclaimer: http://www.religareonline.com/research/Disclaimer/Disclaimer_RSL.html

Before you use this research report , please ensure to go through the disclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014 and Research Disclaimer at the following link : http://old.religareonline.com/research/Disclaimer/Disclaimer_RSL.html

Specific analyst(s) specific disclosure(s) inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regula-tions, 2014 is/are as under:

Statements on ownership and material conflicts of interest , compensation– Research Analyst (RA)

[Please note that only in case of multiple RAs, if in the event answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) below , are given separately]

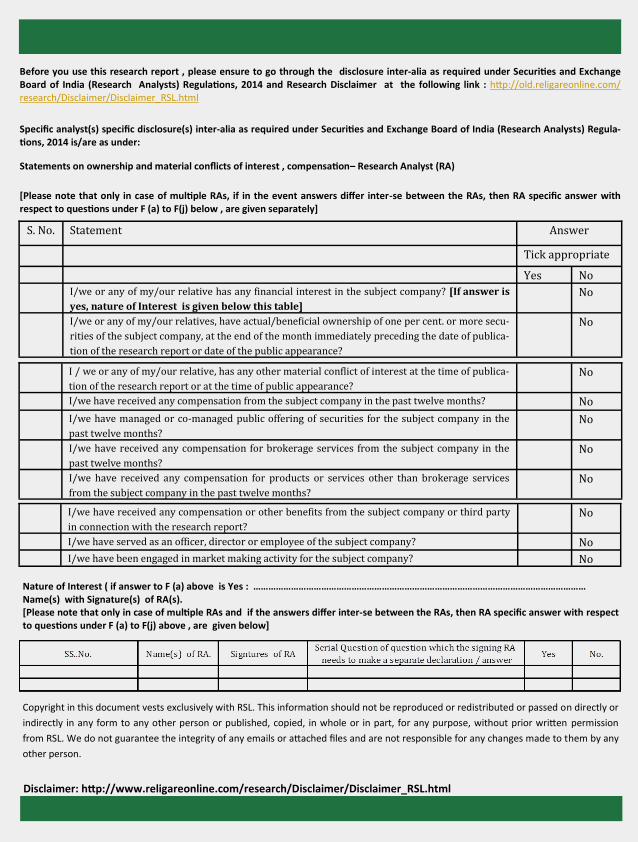

S. No. Statement Answer Tick appropriate Yes No

I/we or any of my/our relative has any financial interest in the subject company? [If answer is

yes, nature of Interest is given below this table] No

I/we or any of my/our relatives, have actual/beneficial ownership of one per cent. or more secu-

rities of the subject company, at the end of the month immediately preceding the date of publica-

tion of the research report or date of the public appearance?

No

I / we or any of my/our relative, has any other material conflict of interest at the time of publica-

tion of the research report or at the time of public appearance? No

I/we have received any compensation from the subject company in the past twelve months? No I/we have managed or co-managed public offering of securities for the subject company in the

past twelve months? No

I/we have received any compensation for brokerage services from the subject company in the

past twelve months? No

I/we have received any compensation for products or services other than brokerage services

from the subject company in the past twelve months? No

I/we have received any compensation or other benefits from the subject company or third party

in connection with the research report? No

I/we have served as an officer, director or employee of the subject company? No I/we have been engaged in market making activity for the subject company? No

Nature of Interest ( if answer to F (a) above is Yes : …………………………………………………………………………………………………………………… Name(s) with Signature(s) of RA(s). [Please note that only in case of multiple RAs and if the answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) above , are given below]

Copyright in this document vests exclusively with RSL. This information should not be reproduced or redistributed or passed on directly or

indirectly in any form to any other person or published, copied, in whole or in part, for any purpose, without prior written permission

from RSL. We do not guarantee the integrity of any emails or attached files and are not responsible for any changes made to them by any

other person.