district health boards recognise that drug margins is a ... · district health boards recognise...

TRANSCRIPT

District Health Boards recognise that Drug Margins is a significant issue for the Sector. In January 2015, the Community Pharmacy Services Programme received the mandate to address this issue. To inform the Programme, Deloitte was commissioned to undertake an Environmental Scan on Drug Margins. The Deloitte Report specifically informs the multiparty Pharmaceutical Margins Taskforce that will be making recommendations to the Community Pharmacy Services Governance Group on this matter. The Deloitte Report was never intended to be a public document, yet due to the high level of interest is now being made publicly available.

Environmental Scan Regarding

Drug Margins

Corporate Finance

January 2015

Cover head

Second line lorem ipsum – Arial 10pt Bold

Contents

Glossary of Terms 1

1. Executive Summary 2

2. Introduction 6

3. Current Supply Chain and Funding 7

4. Unique Aspects of NZ Supply Chain 13

5. International Comparisons 14

6. Summary of Pressure Points 18

Appendix 1 29

About Deloitte 31

Environmental Scan Regarding Drug Margins – January 2015 1

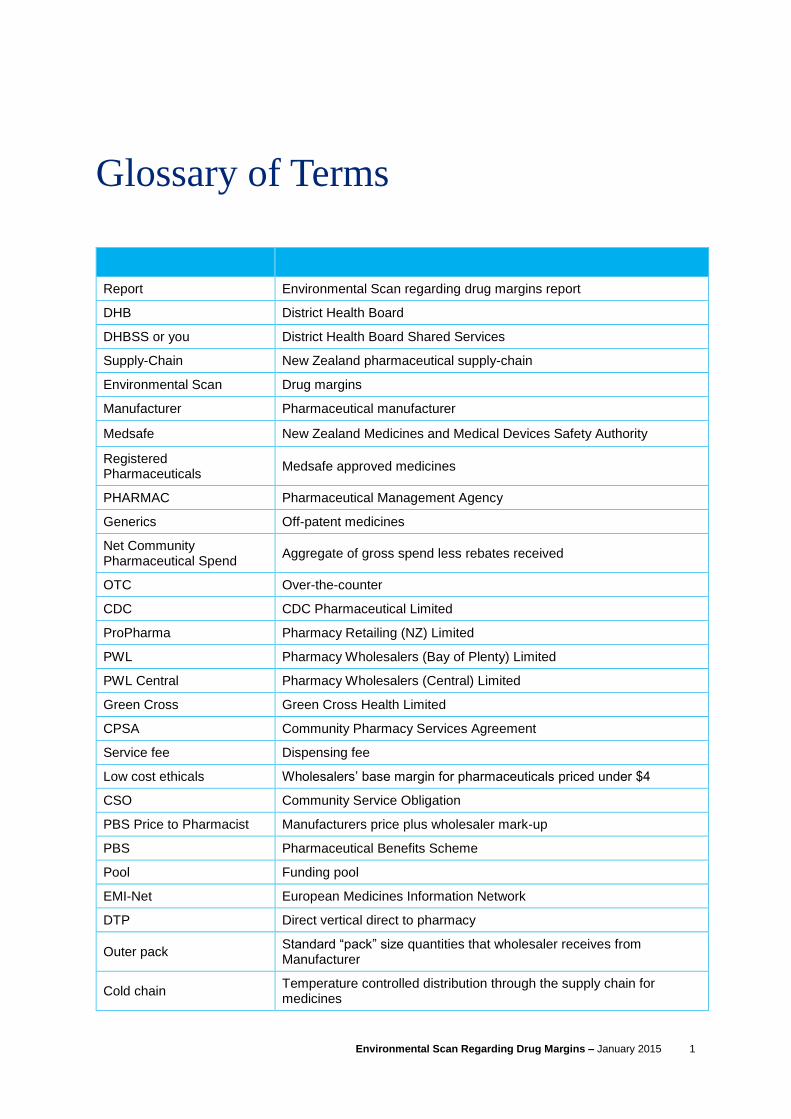

Glossary of Terms

Report Environmental Scan regarding drug margins report

DHB District Health Board

DHBSS or you District Health Board Shared Services

Supply-Chain New Zealand pharmaceutical supply-chain

Environmental Scan Drug margins

Manufacturer Pharmaceutical manufacturer

Medsafe New Zealand Medicines and Medical Devices Safety Authority

Registered Pharmaceuticals

Medsafe approved medicines

PHARMAC Pharmaceutical Management Agency

Generics Off-patent medicines

Net Community Pharmaceutical Spend

Aggregate of gross spend less rebates received

OTC Over-the-counter

CDC CDC Pharmaceutical Limited

ProPharma Pharmacy Retailing (NZ) Limited

PWL Pharmacy Wholesalers (Bay of Plenty) Limited

PWL Central Pharmacy Wholesalers (Central) Limited

Green Cross Green Cross Health Limited

CPSA Community Pharmacy Services Agreement

Service fee Dispensing fee

Low cost ethicals Wholesalers’ base margin for pharmaceuticals priced under $4

CSO Community Service Obligation

PBS Price to Pharmacist Manufacturers price plus wholesaler mark-up

PBS Pharmaceutical Benefits Scheme

Pool Funding pool

EMI-Net European Medicines Information Network

DTP Direct vertical direct to pharmacy

Outer pack Standard “pack” size quantities that wholesaler receives from Manufacturer

Cold chain Temperature controlled distribution through the supply chain for medicines

Environmental Scan Regarding Drug Margins – January 2015 2

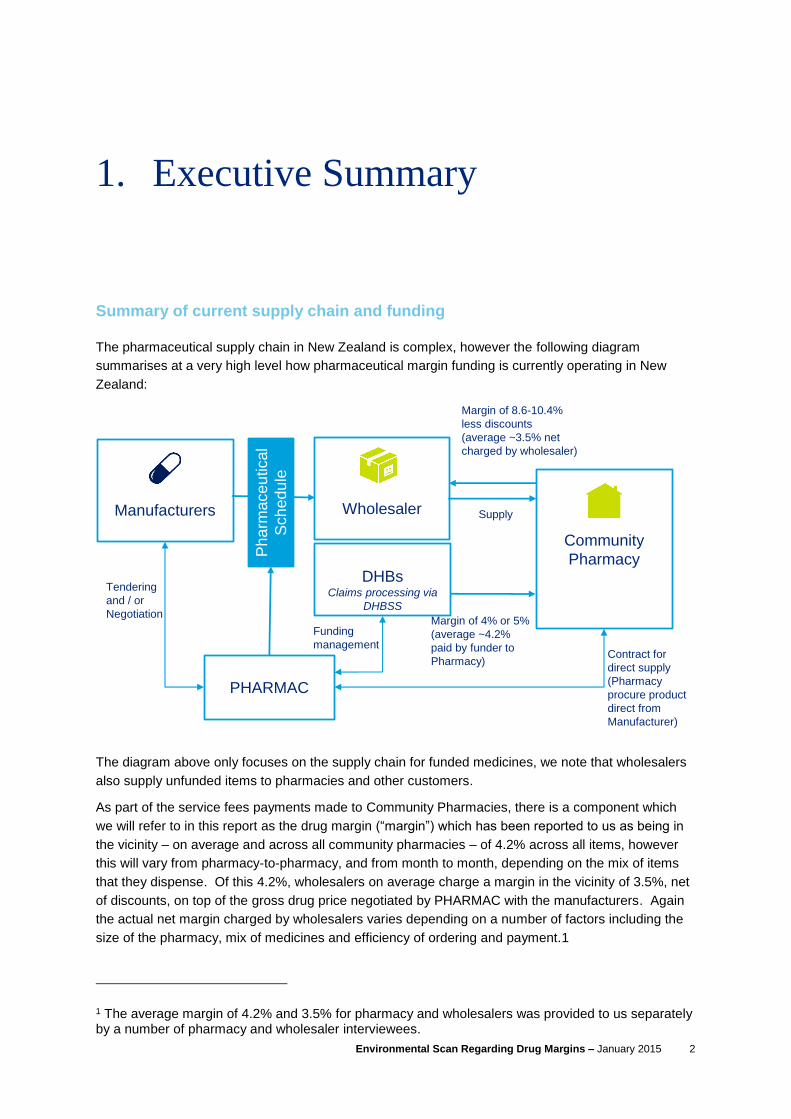

1. Executive Summary

Summary of current supply chain and funding

The pharmaceutical supply chain in New Zealand is complex, however the following diagram

summarises at a very high level how pharmaceutical margin funding is currently operating in New

Zealand:

The diagram above only focuses on the supply chain for funded medicines, we note that wholesalers

also supply unfunded items to pharmacies and other customers.

As part of the service fees payments made to Community Pharmacies, there is a component which

we will refer to in this report as the drug margin (“margin”) which has been reported to us as being in

the vicinity – on average and across all community pharmacies – of 4.2% across all items, however

this will vary from pharmacy-to-pharmacy, and from month to month, depending on the mix of items

that they dispense. Of this 4.2%, wholesalers on average charge a margin in the vicinity of 3.5%, net

of discounts, on top of the gross drug price negotiated by PHARMAC with the manufacturers. Again

the actual net margin charged by wholesalers varies depending on a number of factors including the

size of the pharmacy, mix of medicines and efficiency of ordering and payment.1

1 The average margin of 4.2% and 3.5% for pharmacy and wholesalers was provided to us separately by a number of pharmacy and wholesaler interviewees.

PHARMAC

DHBsClaims processing via

DHBSS

Community

Pharmacy

Wholesaler

Margin of 4% or 5%

(average ~4.2%

paid by funder to

Pharmacy)

Margin of 8.6-10.4%

less discounts

(average ~3.5% net

charged by wholesaler)

Manufacturers

Tendering

and / or

Negotiation

Ph

arm

ace

utica

l

Sch

ed

ule

Contract for

direct supply

(Pharmacy

procure product

direct from

Manufacturer)

Supply

Funding

management

Environmental Scan Regarding Drug Margins – January 2015 3

Wholesalers offer discounts that are dependent upon pharmacy paying promptly, ordering efficiently,

order volumes and monthly value of purchases. This figure also takes into account rebates provided

at year end to pharmacies that are members of wholesalers that operate under a co-operative

structure.

The margin “M” is defined in the CPSA contract document as "a margin towards the procurement and

stockholding costs for the Pharmaceutical”. Most interviewees interpreted the margin component as

being a payment to cover this specific basket of costs, although DHBs tended to take a broader view

that the overall service payments, which included the component “M”, was intended to purchase a

bundled service to patients rather than a set of aggregated services funded individually.

However, even amongst those who viewed the margin component as a payment for a specific cost or

service, the nature of the ”procurement and stock-holding costs” that the payment was considered to

cover was not consistently interpreted by interviewees, with views that included the margin covering

all or some of the following costs within the Supply Chain:

Cartage, including “cold-chain” refrigeration;

Stockholding required to fill scripts under the requirements of the CPSA and associated

facilities including refrigeration;

Any repackaging or pouring required;

Wastage;

Expiry;

Recalls;

Inventory management software (e.g. SAP for wholesalers; Toniq and HealthSoft for

Pharmacy);

The cost of staff time associated with the above functions, compliance (including Section 29)

and changes to the pharmaceutical schedule; and

Wholesalers’ and pharmacies return on investment.

Common themes

Our findings are informed largely through interviews with a variety of sector participants. The themes

discussed were very consistent across interviewees and highlighted a number of pressure points for

both pharmacy and wholesalers under the current funding structure. Overall there was a feeling that

the New Zealand pharmaceutical supply chain is currently operating very efficiently, especially in the

context of other international models. Both wholesalers and pharmacy are increasingly squeezed by

reduced margin funding on increasing volumes and at the same time increased costs. Pharmacy and

wholesalers were consistently of the view that they bear significant stock-holding risk that is heavily

influenced by decisions made by PHARMAC and DHBs who do not in-turn bear any risk.

Environmental Scan Regarding Drug Margins – January 2015 4

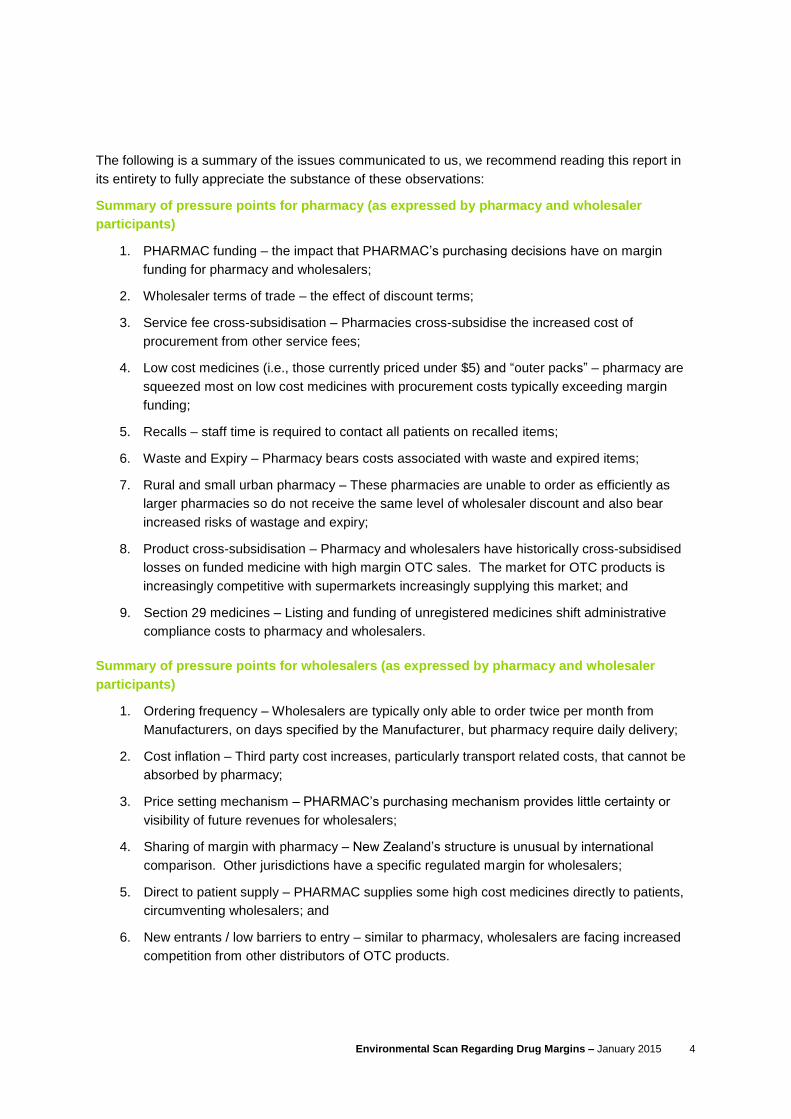

The following is a summary of the issues communicated to us, we recommend reading this report in

its entirety to fully appreciate the substance of these observations:

Summary of pressure points for pharmacy (as expressed by pharmacy and wholesaler

participants)

1. PHARMAC funding – the impact that PHARMAC’s purchasing decisions have on margin

funding for pharmacy and wholesalers;

2. Wholesaler terms of trade – the effect of discount terms;

3. Service fee cross-subsidisation – Pharmacies cross-subsidise the increased cost of

procurement from other service fees;

4. Low cost medicines (i.e., those currently priced under $5) and “outer packs” – pharmacy are

squeezed most on low cost medicines with procurement costs typically exceeding margin

funding;

5. Recalls – staff time is required to contact all patients on recalled items;

6. Waste and Expiry – Pharmacy bears costs associated with waste and expired items;

7. Rural and small urban pharmacy – These pharmacies are unable to order as efficiently as

larger pharmacies so do not receive the same level of wholesaler discount and also bear

increased risks of wastage and expiry;

8. Product cross-subsidisation – Pharmacy and wholesalers have historically cross-subsidised

losses on funded medicine with high margin OTC sales. The market for OTC products is

increasingly competitive with supermarkets increasingly supplying this market; and

9. Section 29 medicines – Listing and funding of unregistered medicines shift administrative

compliance costs to pharmacy and wholesalers.

Summary of pressure points for wholesalers (as expressed by pharmacy and wholesaler

participants)

1. Ordering frequency – Wholesalers are typically only able to order twice per month from

Manufacturers, on days specified by the Manufacturer, but pharmacy require daily delivery;

2. Cost inflation – Third party cost increases, particularly transport related costs, that cannot be

absorbed by pharmacy;

3. Price setting mechanism – PHARMAC’s purchasing mechanism provides little certainty or

visibility of future revenues for wholesalers;

4. Sharing of margin with pharmacy – New Zealand’s structure is unusual by international

comparison. Other jurisdictions have a specific regulated margin for wholesalers;

5. Direct to patient supply – PHARMAC supplies some high cost medicines directly to patients,

circumventing wholesalers; and

6. New entrants / low barriers to entry – similar to pharmacy, wholesalers are facing increased

competition from other distributors of OTC products.

Environmental Scan Regarding Drug Margins – January 2015 5

International comparison

We have researched how pharmaceutical supply chains operates in Australia and in the European

Union member states.

A number of the pressure points felt by pharmacy and wholesalers in New Zealand are consistent

with reports from other jurisdictions. However, there are unique aspects to the New Zealand funding

structure that support the assertion that New Zealand operates an efficient supply chain by

international standards. Most notably New Zealand’s progressive margin structure is unique, most

other countries had regressive structures for both wholesalers and pharmacy. The Czech Republic

was the only country to fund a single pharmaceutical margin to cover costs incurred in the supply

chain for both wholesalers and pharmacy. Other jurisdictions also had regulated funding for margins

as opposed to a contracted arrangement.

Environmental Scan Regarding Drug Margins – January 2015 6

2. Introduction

Deloitte was asked to undertake an Environmental Scan of drug margins in the New Zealand pharmaceutical supply chain.

2.1. Purpose and Scope

The purpose of this report (the “Report”) is to provide District Health Board Shared Services

(“DHBSS” or “you”) with an assessment of the New Zealand pharmaceutical supply-chain (the

“Supply-Chain”) with a particular focus on drug margins (the “Environmental Scan”).

DHBSS specifically engaged us to undertake the following tasks as our scope of work:

A description of how the supply chain currently operates in New Zealand, specifically from the

drug manufacturer to the patient;

A comparison of the Supply-Chain to other comparable international pharmaceutical supply

chains;

Identification of the unique aspects of the Supply-Chain;

Provide transparency of funding flows through the supply chain, including (if possible)

i. the terms and conditions between wholesales and pharmacy;

ii. the costs of procurement and stock-holding for pharmacy; and

iii. reimbursement from DHBs to pharmacy.

Identify and describe where there are “pressure points” in the Supply-Chain or other observed

issues.

We have interviewed a number of key sector stakeholders and participants (listed in Appendix 1).

Our Report is principally informed by these interviews.

The structure of all interviews was for each stakeholder to “vent” issues that they perceived to exist in

the current Supply-Chain. We have then collated these issues into common themes to identify the

“pressure points”.

Environmental Scan Regarding Drug Margins – January 2015 7

3. Current Supply Chain and

Funding

This section provides a high level summary of how the drug supply chain operates in New Zealand

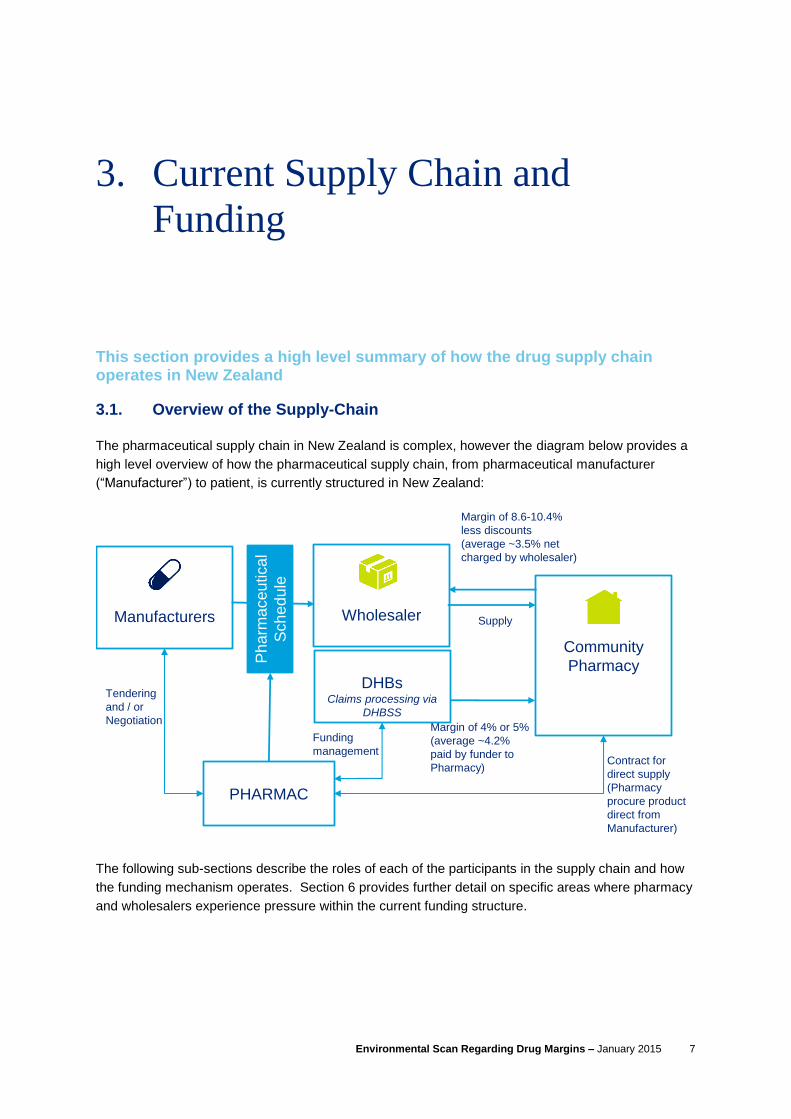

3.1. Overview of the Supply-Chain

The pharmaceutical supply chain in New Zealand is complex, however the diagram below provides a

high level overview of how the pharmaceutical supply chain, from pharmaceutical manufacturer

(“Manufacturer”) to patient, is currently structured in New Zealand:

The following sub-sections describe the roles of each of the participants in the supply chain and how

the funding mechanism operates. Section 6 provides further detail on specific areas where pharmacy

and wholesalers experience pressure within the current funding structure.

PHARMAC

DHBsClaims processing via

DHBSS

Community

Pharmacy

Wholesaler

Margin of 4% or 5%

(average ~4.2%

paid by funder to

Pharmacy)

Margin of 8.6-10.4%

less discounts

(average ~3.5% net

charged by wholesaler)

Manufacturers

Tendering

and / or

Negotiation

Ph

arm

ace

utica

l

Sch

ed

ule

Contract for

direct supply

(Pharmacy

procure product

direct from

Manufacturer)

Supply

Funding

management

Environmental Scan Regarding Drug Margins – January 2015 8

3.1.1. The role of PHARMAC

Pharmaceuticals are approved and registered by the New Zealand Medicines and Medical Devices

Safety Authority (“Medsafe”) (“Registered Pharmaceuticals”). The Pharmaceutical Management

Agency (“PHARMAC”) was created in 1993 to actively manage Government spending on

pharmaceuticals.

PHARMAC manages spending on pharmaceuticals within a budget set by the Ministry of Health

following advice from PHARMAC and DHBs. DHBs in-turn provide funding for Community

Pharmaceuticals and PHARMAC negotiates with Manufacturers on behalf of DHBs.

Manufacturers must negotiate and contract with PHARMAC for their products to be eligible for

subsidised funding in New Zealand. Pharmaceuticals that meet eligibility criteria and receive

subsidised funding from PHARMAC are listed on the Pharmaceutical Schedule.

There is no obligation for PHARMAC to fund all Medsafe Registered Pharmaceuticals. Patients can

access all Registered Pharmaceuticals but will not be subsidised for pharmaceuticals that are not

listed on the Pharmaceutical Schedule. PHARMAC can also choose to list pharmaceuticals that are

not (or no longer) Registered Pharmaceuticals on the Pharmaceutical Schedule (referred to as

Section 29 Pharmaceuticals) but will generally only do so where no Registered substitutes are

available.

The contracts between PHARMAC and the Manufacturers stipulate the terms of supply including:

security of supply; pricing; and standard quantities / pack sizes. Manufacturers competitively tender

for exclusive rights to supply Community Pharmacy with off-patent medicines (“generics”). This

tendering process involves nearly half of subsidised pharmaceuticals in New Zealand (by volume),

represents c.20% of total pharmaceuticals costs and generates around $40m to $60m in savings per

annum.

Manufacturers contract a “gross” price with PHARMAC. This gross price is listed on the

Pharmaceutical Schedule. In some instances Manufacturers will grant PHARMAC annual rebates

due to PHARMAC’s purchasing power and the volume of product ordered. These rebates are

returned centrally to PHARMAC as part of managing its budgeted spend and do not flow through to

pharmacies. These rebates, combined with savings generated through tenders for off-patent

medicines are vital for PHARMAC to deliver the government’s funding budget objectives for

Pharmaceuticals supply. The level of rebates can vary significantly from year to year.

PHARMAC’s annual pharmaceutical expenditure is the aggregate of gross spend less rebates

received (“Net Community Pharmaceutical Spend”). The budget for Net Community Pharmacy spend

is communicated publically, however, rebates received from Manufacturers are based on confidential

terms and therefore budgeted rebates and budgeted gross spend are not published in advance. Net

Community Pharmaceutical Spend represented all of PHARMAC’s net spend up until 2010. From

2011, PHARMAC’s net spend has also been applied to areas outside of Community Pharmacy

including Pharma cancer treatments, vaccines and nicotine. These areas are funded as they are

considered to be community managed conditions.

Environmental Scan Regarding Drug Margins – January 2015 9

The net effect is that the level of gross spend that is channelled through Community Pharmacy via

wholesalers is not known in advance and can be quite variable. Perceived issues related to this are

discussed in Section 6.2.2.

3.1.2. The role of the Wholesaler

PHARMAC negotiates with Manufacturers and agrees to the terms of supply, however, it does not

directly purchase, stock or distribute pharmaceuticals.

The role of purchasing and distributing pharmaceuticals to the community in New Zealand is largely

undertaken by dedicated wholesaler entities. Wholesalers purchase pharmaceuticals directly from

Manufacturers at the prices negotiated by PHARMAC and listed in the Pharmaceutical Schedule.

Wholesalers purchase, stock and distribute both prescription, Pharmacy-only over-the-counter

(“OTC”) pharmaceutical products and other general stock-lines to community pharmacies and supply

specialist pharmaceutical products to hospitals. DHBs directly distribute a small volume of very high

value medicines to patients. DHBs also directly procure for supply into hospitals.

We understand that there are currently three major pharmaceutical wholesalers in New Zealand:

CDC Pharmaceutical Limited (“CDC”);

Pharmacy Retailing (NZ) Limited (“ProPharma”), a wholly owned subsidiary of EBOS Group

Limited; and

Pharmacy Wholesalers (Bay of Plenty) Limited (“PWL”).

CDC was recently granted clearance by the Commerce Commission to merge with Pharmacy

Wholesalers (Central) Limited (“PWL Central”).

Both CDC and PWL are co-operatives that distribute surpluses back to their member pharmacies

annually. CDC operates warehouses in Dunedin, Christchurch, New Plymouth, Wanganui and Napier

and Wellington supplying predominantly to retail pharmacies in the South Island, Central North Island,

Wellington and Auckland. PWL concentrates on the Bay of Plenty, Waikato and Auckland.

ProPharma wholesales to customers nationwide.

The CDC and PWL businesses have not vertically integrated into manufacturing or retail pharmacy.

ProPharma, as part of EBOS Group, has a sister company (Pharmacy Choice) that own a retail

pharmacy brand in Australia. However, ProPharma has not vertically integrated beyond wholesaling

the New Zealand supply chain.

Green Cross Health Limited (“Green Cross”) represents approximately 300 retail pharmacies under its

Unichem, Life Pharmacy and Radius brands. Whilst we have made mention of the lack of direct

vertical integration in the supply chain, we are aware that ProPharma does have an indirect

shareholding and representatives on the board of Green Cross. We also acknowledge that CDC and

PWL, by virtue of being co-operatives, are owned by their pharmacy customers.

Environmental Scan Regarding Drug Margins – January 2015 10

We understand from our interviews that Manufacturers typically allow wholesalers to place up to two

orders per month. Wholesalers allow pharmacies to place orders at any time to meet the

requirements of the Community Pharmacy Services Agreement (“CPSA”) that stipulates:

90% of scripts be filled within 1 hour (requiring pharmacies to hold sufficient stocks);

99% of scripts filled before the end of the next business day (overnight delivery required); and

100% within two business days.

These requirements mean that pharmacy must maintain or be able to access adequate stocks to

meet these time limits. From interviews with pharmacy and wholesalers we understand that the

obligation to keep adequate stocks also results in most pharmacies receiving daily deliveries and in

some instances two deliveries per day from wholesalers and wholesalers need to stock low volume

items (“service” lines). Rural pharmacies typically rely upon next day deliveries as same day

deliveries are not practicable.

3.1.3. The Drug Margin Mechanism and Wholesaler / Pharmacy Relationship

DHB funding of prescription pharmaceuticals is made up of the following components:

1. The Manufacturers’ selling price, typically equal to the list price that PHARMAC provides for

the pharmaceuticals in the Pharmaceutical Schedule. A premium may apply to some

pharmaceuticals for which the consumer pays;

2. A margin on PHARMAC’s list price. This margin is currently 4% for items under $150 and 5%

for items above $150 and special foods (“pharmaceutical margin”); and

3. A service fee (“dispensing fee”) that is reimbursed to Community Pharmacies.

The margin “M” is defined in the CPSA contract document as "a margin towards the procurement and stockholding costs for the Pharmaceutical”. Most interviewees interpreted the margin component as being a payment to cover this specific basket of costs, although DHBs tended to take a broader view that the overall service payments, which included the component “M”, was intended to purchase a bundled service to patients rather than a set of aggregated services funded individually.

However, even amongst those who viewed the margin component as a payment for a specific cost or

service, the nature of the ”procurement and stock-holding costs” that the payment was considered to

cover was not consistently interpreted by interviewees, with views that included the margin covering

all or some of the following costs within the Supply Chain:

Cartage, including “cold-chain” refrigeration;

Stockholding required to fill scripts under the requirements of the CPSA and associated

facilities including refrigeration;

Any repackaging or pouring required;

Wastage;

Expiry;

Recalls;

Inventory management software (e.g. SAP for wholesalers; Toniq and HealthSoft for

Pharmacy);

Environmental Scan Regarding Drug Margins – January 2015 11

The cost of staff time associated with the above functions, compliance (including Section 29)

and changes to the pharmaceutical schedule; and

Wholesalers’ and pharmacies return on investment.

Commercial terms of trade between wholesalers and pharmacy determine how the margin is split

between each respective party. For the purposes of this paper, in a supply chain sense wholesalers

and pharmacy “share” this margin to cover “procurement and stockholding” costs.

The wholesalers’ price to pharmacy will include a “base margin”, which is typically between

approximately 8.65% and 10.4%, that is then discounted where applicable for the following:

Prompt payment;

Efficiency in buying (i.e. “out of packs”, timely etc); and/or

Volume of business undertaken.

Pharmacy and wholesaler interviewees estimated that approximately 90% of orders from pharmacy to

wholesaler are processed electronically through pharmacies’ computerised stock management

systems (Toniq and HealthSoft).

Pharmacies do not contract with wholesalers, the relationship is under normal terms of trade, so there

are no formal restrictions on pharmacies to change their preferred wholesaler. Pharmacies typically

align with a single wholesaler in order to maximise the discounts and favourable terms of trade that

they receive by virtue of a single supplier relationship. This was a common theme in our interviews,

particularly for prescription pharmaceuticals, however some felt that pharmacies shopped around

wholesalers for OTC products in some instances.

Interviews with pharmacy and wholesalers indicate that the weighted average margin funding

received by pharmacy is understood to be c.4.2%; i.e. the weighted average of i) items below $150

that receive a 4% margin; and ii) items above $150 that receive a 5% margin.

The respective “share” of this margin as between wholesaler and pharmacy then differs based on the

price of pharmaceuticals and discounts offered by wholesalers:

Wholesalers’ base margin for low cost pharmaceuticals under $5 (“low cost ethicals”) is up to

c.10% prior to discounts;

A large range of discount are available for pharmaceuticals priced between $5 and $150. In

some cases pharmacies may pay less than the scheduled price; and

For pharmaceuticals priced above $150 the wholesaler margin typically nets to 3.5% in

almost all cases after discounts.

Wholesalers’ final, weighted average, share of this margin is estimated to be anywhere between 3.5%

and 4.0% (post co-op rebates where applicable). If you accept the view that the margin is intended to

specifically cover certain costs, this leaves pharmacies with a margin of 0.25% to 0.75% to cover all

remaining procurement costs.

Environmental Scan Regarding Drug Margins – January 2015 12

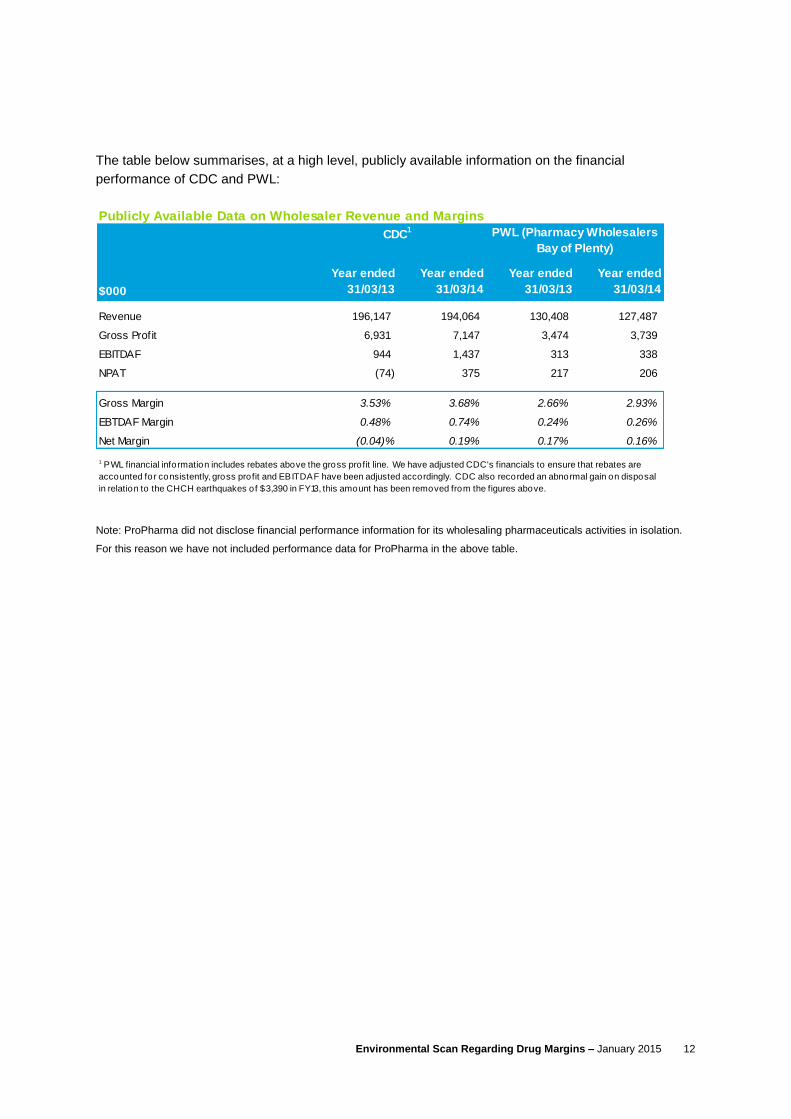

The table below summarises, at a high level, publicly available information on the financial

performance of CDC and PWL:

Note: ProPharma did not disclose financial performance information for its wholesaling pharmaceuticals activities in isolation.

For this reason we have not included performance data for ProPharma in the above table.

Publicly Available Data on Wholesaler Revenue and Margins

$000

Revenue 196,147 194,064 130,408 127,487

Gross Profit 6,931 7,147 3,474 3,739

EBITDAF 944 1,437 313 338

NPAT (74) 375 217 206

Gross Margin 3.53% 3.68% 2.66% 2.93%

EBTDAF Margin 0.48% 0.74% 0.24% 0.26%

Net Margin (0.04)% 0.19% 0.17% 0.16%

CDC1 PWL (Pharmacy Wholesalers

Bay of Plenty)

Year ended

31/03/14

Year ended

31/03/13

Year ended

31/03/14

Year ended

31/03/13

1 PWL financial information includes rebates above the gross profit line. We have adjusted CDC's financials to ensure that rebates are

accounted for consistently, gross profit and EBITDAF have been adjusted accordingly. CDC also recorded an abnormal gain on disposal

in relation to the CHCH earthquakes of $3,390 in FY13, this amount has been removed from the figures above.

Environmental Scan Regarding Drug Margins – January 2015 13

4. Unique Aspects of NZ Supply

Chain

4.1. Role of PHARMAC

The role of PHARMAC is unique to the New Zealand environment. Wholesalers typically engage

directly with Manufacturers in other jurisdictions.

4.2. Contracting model

DHBs contract with pharmacy by way of the CPSA. In other jurisdictions margins and service

obligations are typically regulated. The differences attributable to the contracting model may be more

in form rather than substance as other models do appear to involve a significant level of collective

bargaining on the level of funding available to pharmacy.

4.3. Progressive margin structure

New Zealand appears to be unique in having a progressive pharmaceutical margin (i.e. increasing

from 4% to 5% as price increases). Our review of Australia and European margin structures found

that regressive margins or mark-ups (i.e. decreasing as price increases) were most common, followed

to a lesser extent by, linear margins or mark-ups (i.e. flat percentage for all levels of price).

New Zealand’s progressive structure has two categories (4% for less than $150 and 5% for more than

$150). Australia has six regressive categories for pharmacy and most countries in Europe had more

than four categories for both pharmacy and wholesaler.

4.4. Sharing of margin between wholesaler and pharmacy

Our review of Australia and European margin structures only found one market (the Czech Republic)

where a single pharmaceutical margin covers costs incurred in the supply chain for both wholesalers

and pharmacy in a similar way to New Zealand. In the case of the Czech Republic the margin was

regressive rather than progressive.

Wholesalers are able to apply a margin of their choosing in New Zealand whereas in other

jurisdictions, notably Australia, there is a specified and regulated wholesaler margin.

Other markets applied separate margins for wholesaler and pharmacy respectively.

Environmental Scan Regarding Drug Margins – January 2015 14

5. International Comparisons

5.1. Australia

5.1.1. Overview of the funding structure

Australia’s public funding structure for pharmacy has similarities to that of New Zealand,

notwithstanding differences in terminology and the uniqueness of PHARMAC and contracting to the

New Zealand environment.

In Australia the principal differences are i) the application of a mark-up, rather than a margin, that is

reimbursed to pharmacy; ii) the separation of wholesaler and pharmacy mark-up; and iii) the

Community Service Obligation (“CSO”), described in more detail in section 5.1.2.

The diagram below provides an example of the cumulative funding structure in Australia for a

pharmaceutical with a Manufacturer’s price of $10.00:

PBS Manufacurer's Price:$10.00

Wholesaler mark up: $0.752"PBS Price to Pharmacist":

$10.75

Pharmacy mark up (15%):$1.61

Dispensing Fee: $6.76

"Dispensed Price": $19.13

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

$11.00

$12.00

$13.00

$14.00

$15.00

$16.00

$17.00

$18.00

$19.00

$20.00

Axi

s Ti

tle

Figure 5.1: Example of cumulative mark-ups

PBS manufacurer's price Wholesaler mark up Pharmacy mark up Dispensing fee

Environmental Scan Regarding Drug Margins – January 2015 15

The wholesaler receives a flat mark-up of 7.52% that caps out at a Manufacturer’s price of

$930.06, for pharmaceuticals priced above this point the wholesaler mark-up is flat at $69.94.

From interviews we understand that wholesalers’ weighted average mark-up is about 6.9%

(taking into account the cap). After applying discounts Australian wholesalers typically

achieve a c.4.5% mark-up (i.e. pharmacy receive a discount of c.2.5%);

The pharmacy mark-up is a regressive mark-up that is based on the “PBS Price to

Pharmacist” (Manufacturers price plus wholesaler mark-up). More detail on the pharmacy

mark-up is provided in the chart in figure 5.2;

A flat dispensing fee of $6.76. This is indexed on 1 July each year.

Special handling fees also apply for dangerous drugs ($2.71) and extemporaneously

compounded drugs ($2.04).

The chart below shows how the regressive pharmacy mark-up is structured in Australia. The

percentage mark-up decreases as the PBS Price to Pharmacist increases:

Pharmacists receive a 15% mark-up for pharmaceuticals with a PBS Price to Pharmacist up

to $30;

A flat $4.50 for pharmaceuticals between $30 and $45;

A 10% mark-up between $45 and $180;

A flat $18 between $180 and $450;

A 4% mark-up between $450 and $1,750; and

A flat $70 above $1,750.

4.50

18.00

70.00

0

10

20

30

40

50

60

70

80

0 30 45 180 450 1,750 1,800

Ph

arm

acy

mar

k-u

p (

$)

PBS price to Pharmacist

Figure 5.2: Pharmacy mark up

15% mark-up

10% mark-up

4% mark-up

Environmental Scan Regarding Drug Margins – January 2015 16

5.1.2. Other aspects of the Australian funding mechanism

Australia has a history of periodic funding “crises” in its pharmaceutical funding that trigger funding

responses from the Commonwealth Government.

One such crises occurred in 2006 and the response was to put in place CSO for wholesalers to be

eligible to participate in the sector and gain government funding.

Wholesalers must meet seven standards to be eligible under the CSO:

1. Supply any pharmacy (rural, small, urban etc)

2. Supply any brand of PBS medicine;

3. Maintain specified stocks of PBS medicine;

4. Must supply low volume medicines i.e. high cost per unit pharmaceuticals. This standard was

put in place to limit the growth of short-line wholesalers that were only stocking high volume

medicines, targeting urban areas and damaging the business of genuine full line wholesalers;

5. Supplying PBS medicine at or below the “approved price” (i.e. cost + 7.52%);

6. Supply within 24 hours with the exception of six pharmacies in particularly remote locations;

and

7. Must make a daily delivery structure available.

In return for agreeing to the CSO and a reduction in wholesale margin from 10% to 7% wholesalers

have had an additional funding pool made available. This pool is currently A$196 million per annum

and is adjusted annually by the wage cost inflation index. The pool is split between wholesalers

based on the volume and is paid monthly in addition to the mark-up.

Australian wholesalers currently offer pharmacy a discount of approximately 2.5% on orders. This

has decreased in recent years from 3.5% and is expected to continue to decrease in the medium

term. The decrease is being driven by PBS reforms and increasing costs to wholesalers and is not

considered a desirable outcome for a functional market - it is expected to result in limited competition

as wholesalers will have little to differentiate on.

Australia is also experiencing similar issues to New Zealand regarding the increased number of

generic medicines coming to the market; an increasing number of generic medicines coming to the

market ultimately results in price reductions and lower mark-ups to both wholesalers and pharmacy.

5.2. Europe

We did not conduct interviews with any sector participants from Europe, however we have reviewed a

2011 report by European Medicines Information Network (“EMI-Net”) of the pharmaceutical

distribution chain in the 27 EU member states at that time2.

2 European Medicines Information Network, The Pharmaceutical Distribution Chain in the European Union: Structure and Impact on Pharmaceutical Prices, March 2011

Environmental Scan Regarding Drug Margins – January 2015 17

The EMI-Net report found that the majority of member states have a regulated mark-up / margin

scheme to both or either wholesalers and pharmacies. Regressive mark-up / margin schemes are

very common, but some countries also apply linear mark-ups / margins.

Only one country, the Czech Republic, had a shared margin between wholesaler and pharmacy. All

other countries had separate wholesaler and pharmacy margins:

The majority of countries had wholesaler margins ranging between 4% to 8% of the

pharmacy retail price;

There was considerably less information available on average pharmacy margins with

margins ranging between 12% and 50% of pharmacy retail price.

Discounts, as in New Zealand, play an important role in defining exactly what mark-up / margin

wholesalers and pharmacy receive respectively.

Manufacturers have been exploring alternative wholesale distribution arrangements in Europe,

establishing direct vertical direct to pharmacy (“DTP”) links with retail businesses to guarantee

efficient distribution at low cost. Wholesalers were interviewed and felt squeezed by those practices

and by the purchasing power of pharmacy chains. Actual margins for wholesalers ranged between

1.5% and 3.5%.

In some jurisdictions Manufacturers have set up reduced wholesaler model schemes to supply

pharmacy. Under these schemes the Manufacturer uses a “very small” number of wholesalers to

distribute product. “Very small” is defined as one to three wholesalers.

The traditional full-line wholesaler model is under pressure (i.e. stocking the widest range of products,

easy access to stock with frequent and timely delivery). The increasingly competitive environment is

resulting in greater demand and supply of generic products. Again, this is a similar dynamic to New

Zealand. Wholesalers operate on very low net margins and are unable to reduce margins further due

to the increased use of generics, public services obligations and frequent distribution. These factors

are leading to questions over the sustainability of market structures for distribution.

In some countries there have been concerns over the availability of medicines and the risk that his

could lead to shortages. Wholesalers have introduced a number of additional surcharges in recent

years with most now charging fuel surcharges, stock return surcharges and underspend surcharges.

Pharmacists in Europe feel they are asked to do more for less and that there is a reluctance by

“payers” to remunerate them for additional services. As a result other segments of pharmacy are

cross-subsidising the prescription only medicine segment.

Environmental Scan Regarding Drug Margins – January 2015 18

6. Summary of Pressure Points

6.1. Pressure points for pharmacies (as expressed by pharmacy and wholesaler participants)

The pressure points for pharmacies, as expressed by pharmacy and wholesaler participants, fall into

the following categories:

1. PHARMAC funding;

2. Wholesaler terms of trade;

3. Service fee cross-subsidisation;

4. Medicines priced under $5 and “outer packs”;

5. Recalls;

6. Waste and Expiry;

7. Rural and small urban pharmacy;

8. Product cross-subsidisation; and

9. Section 29 medicines.

Each of the above categories is described in the following subsections:

6.1.1. PHARMAC funding

A common theme in our interviews with pharmacy and wholesaler stakeholders was the influence that

PHARMAC’s purchasing decisions have for both wholesalers and pharmacy. Within the sector there

is a strong appreciation for how effective PHARMAC is at managing the pharmaceutical budget and

particularly in negotiating low prices for pharmaceuticals.

However, the pharmacy and wholesalers consider that PHARMAC’s efficiency has also resulted in a

number of unintended consequences at the wholesaler and pharmacy level, most notably:

Significant reductions in price and therefore margin when generics become available;

There is little linkage between PHARMAC’s purchasing decisions and the resulting costs and

workload for pharmacy;

Diversion of budget outside of Community Pharmacy; and

Distribution of medicines directly to named patients.

Environmental Scan Regarding Drug Margins – January 2015 19

Reduction in margin due to generics

Understandably, as New Zealand’s population ages there is increased pressure on New Zealand’s

health spend and subsequently PHARMAC’s role of negotiating for low cost pharmaceuticals on

behalf of the Community Pharmacy sector becomes increasingly important.

PHARMAC has shown itself to be very successful in reducing the price of pharmaceuticals. As

patents lapse PHARMAC’s position to negotiate on price is far stronger as an increasing number of

Manufacturers are able to tender to supply generic versions of medicines.

We understand that it is not uncommon for PHARMAC to negotiate prices on generic versions that

are up to 80% to 90% cheaper than the previous price under patent. This reduction in cost to DHBs

is, in-of-itself, universally recognised as a good outcome for health spend.

However, these significant reductions in price also result in significant reductions in margin for both

wholesalers and pharmacies who must stock and distribute these pharmaceuticals. Pharmacy and

wholesalers have told us that the reduction in margin is not matched by a commensurate reduction in

supply chain costs associated with these products. These costs to wholesalers and pharmacy remain

relatively constant, or even increase in some instances, when a pharmaceutical is available as a

generic. This issue is exacerbated by the increased prescribing of lower cost generic products once

the patent lapses.

This reduction in margin, and associated reduction in income, is a source of considerable uncertainty

for both wholesalers and pharmacy. Particularly if the saving is not recirculated back into Community

Pharmacy.

Linkage between PHARMAC purchasing decisions and pharmacy workload

PHARMAC’s purchasing decisions also have implications for the workload of pharmacies. Again, it is

acknowledged that PHARMAC’s current funding criteria do not require it to give consideration to the

consequences that its purchasing decisions may have for wholesalers and pharmacy.

When PHARMAC negotiates with Manufacturers on the price of pharmaceuticals it is not required to

give regard to the way a Manufacturer may choose to package that pharmaceutical. This issue is

also closely related to the increased prevalence of generics; indeed, generics provide a good example

of how PHARMAC’s purchasing decisions affect pharmacy workload.

We understand from interviews with pharmacy and wholesalers that generics are typically supplied in

loose form and/or in larger pack sizes by Manufacturers compared to pharmaceuticals under patent.

This has two implications for pharmacy:

1. The pharmacy must repackage loose form pharmaceuticals and large packs into appropriate

quantities for dispensing; and

2. Pharmacy may not receive the same level of discount from wholesalers. Wholesalers

typically offer “outer pack” discounts to pharmacy, i.e. a discount due to pharmacy ordering a

standard quantity that doesn’t require the wholesaler to repackage.

Environmental Scan Regarding Drug Margins – January 2015 20

Diversion of budget outside of Community Pharmacy

Since 2011 PHARMAC has allocated an increasing proportion of its budget to pharmaceuticals that

are delivered outside of Community Pharmacy. These include pharmaceutical cancer treatments,

vaccines and nicotine treatments. We understand from our interviews that PHARMAC has redirected

savings that it has made in Community Pharmacy spend into these areas as i) these are also

considered to be “community managed” conditions and ii) the interpretation of “best value for money”

is not limited to Community Pharmacy and broader trade-offs are likely into the future.

Pharmaceutical cancer treatments, vaccines and nicotine treatments accounted for approximately

$122 million, or 13.2%, of PHARMAC’s 2013 total gross spend (15.6% of net spend).

A consistent theme from our interviews was that increased volumes of medicines are being delivered

through Community Pharmacy while the cost of medicines and therefore PHARMAC spend is

reducing. Reduction in spend, as mentioned, leads to a reduction in margin to wholesalers and

pharmacy.

An issue for wholesalers and pharmacy is that these increased volumes and inflation over the period

have increased supply-chain costs whilst funding received from the pharmaceutical margin has

decreased. Pharmacy are prohibited from on-charging patients from the increasing costs charged by

third parties.

Direct to patient supply

PHARMAC delivers “directly” to a low number of named patients for particularly high costs medicines.

PHARMAC distributes these medicines via a contracted pharmacy or distributor that then forwards

these medicines to relevant Community Pharmacies. PHARMAC pay a service fee directly to the

pharmacy that organises distribution.

We understand that this direct supply mechanism involves approximately $37 million of medicines.

This method circumvents the normal distribution network and as a result wholesalers and pharmacy

do not receive the usual 5% margin payment on these high cost medicines (split 3.5% to wholesaler

and 1.5% to pharmacy).

There is a perception within wholesalers and pharmacy that this practice undermines the current

funding structure.

The alternative view is that this is the most cost effective method of delivery to these patients and

avoids the risk of stock-holding to wholesalers and pharmacy for unusual, very high cost medicines.

6.1.2. Wholesaler terms of trade

A number of pharmacy and DHB interviewees commented on the complicated nature of terms offered

by wholesalers. The various discounts offered make it difficult for many pharmacies to understand

the true cost of procurement and current software systems do not provide cost outputs that are easily

interpreted by pharmacy. However, the use of various discounts to incentivise the right buying

behaviours and efficient purchasing practices was acknowledged by non-wholesalers.

Environmental Scan Regarding Drug Margins – January 2015 21

The intention of wholesaler terms is to reward larger pharmacies with efficient ordering and payment

behaviour. Wholesalers consider this to be in consistent with DHB’s preference for some site

consolidation and less wastage.

Pharmacies are typically 100% loyal to a single wholesaler, subject to availability of urgent medicines,

due to loyalty incentives and the structure of discounts based on volume and efficiency of ordering.

Australian and European research has noted low barriers to entry into wholesaling for vertical

integrators, these same conditions appear to exist in New Zealand. However, the structure of

discounts and the co-operative model can be a psychological barrier to change for pharmacy and

some interviewees were of the view that the indirect vertical integration and concentrated nature of

the sector creates additional barriers to new entrants.

Wholesalers and pharmacy also note that, to a smaller extent, it is very difficult for some rural

pharmacies to switch suppliers due to the location of distribution warehouses. IT systems are not

seen as a barrier to switching wholesalers and that the electronic ordering system is well integrated.

We understand from interviews with pharmacy stakeholders that pharmacy’s net share of the

pharmaceutical margin is small and declining due to wholesalers increasingly seeking to pass through

rising costs associated with distribution. As volumes increase the costs of distribution, particularly

transport and cold-chain related costs, have put pressure on wholesalers.

Pharmacy are particularly squeezed on margin when urgent medicines are required and not available

from their usual wholesaler. If urgent medicines are not available from their usual wholesaler the

pharmacy is forced, under the requirements of the CPSA, to inefficiently order from another

wholesaler and therefore does not receive any wholesaler discounts. In these instances the

wholesaler margin may significantly exceed the pharmaceutical margin.

6.1.3. Service Fee cross-subsidisation

Pharmacy receives service fees from DHBs in recognition of the professional services provided to

patients. The overall vision for the CPSA is to incentivise pharmacy to provide an increasing level of

advice and services to patients (an increasingly “patient-centric” model).

Most wholesaler and pharmacy interviewees were of the view that the “dispensing fee” (handling fee x

multiplier) component of the service fee payment should not be cross-subsidising procurement and

stock-holding costs, or vice-versa. DHB interviewees disagreed with this interpretation and asserted

that the dispensing fee and margin funding were components of a bundled service from community

pharmacy, including both supply of the pharmaceutical to the service user and associated

professional pharmacist care to help the service user use the pharmaceutical safely and to best

effect.

Pharmacy’s share of the pharmaceutical margin is estimated by interviewees to be approximately

0.25% to 0.75%. Many of the pharmacy and wholesaler stakeholders that we interviewed suspected

that this share of the pharmaceutical margin is exceeded by stock-holding and procurement costs. As

mentioned previously there is no consistent view on what “stock-holding and procurement” includes

and is variously interpreted as some or all of the following costs:

Environmental Scan Regarding Drug Margins – January 2015 22

Stockholding required to fill scripts under the requirements of the CPSA and associated

facilities including refrigeration;

Any repackaging or pouring required;

Wastage;

Expiry;

Recalls;

Inventory management software (Toniq and HealthSoft); and

The cost of staff time associated with the above functions.

Larger pharmacies, due to the volume they order and critical mass of patients, are better placed to

minimise shortfalls and manage these costs as they arise. For smaller pharmacies these costs can

be material, particularly the cost of staff time involved in these activities.

If these costs exceed pharmacy’s share of the pharmaceutical margin then the dispensing fee is

required to cross-subsidise procurement costs. Pharmacy stakeholders have stated that, in many

cases, practitioners do not have the time, tools, financial literacy or capability to accurately assess the

costs of procurement.

The risk that high procurement costs may result in perverse incentives and undesirable behaviours

was highlighted by a number of interviewees. These behaviours may include pharmacies directing

patients to other pharmacies to obtain high cost drugs because they have chosen not to stock high

cost drugs at a loss. This behaviour is not considered to be an issue currently and pharmacists are

regarded as highly ethical, however there is a strong perception that the current model is not

sustainable.

6.1.4. Medicines priced under $5 and “outer packs”

Pharmacy and wholesaler interviewees made particular note of the margin issues regarding:

Pharmaceuticals priced under $5 (or “low cost ethicals”); or

Pharmaceuticals not purchased “outer pack” from wholesalers.

It is clear that procurement costs to Pharmacy exceed the margin for many of these medicines.

If a pharmacy is not able to secure all available wholesaler discounts on an order then procuring at a

loss is almost an inevitability on these medicines. This issue is thought to impact rural pharmacies to

a greater extent due to inefficient purchasing patterns and is becoming an increasing issue as more

generics come to market and . This is a particular issue for rural and small pharmacies and is

discussed in detail in Section 6.1.7.

Low cost ethicals

The concern from pharmacy regarding this issue has strengthened as PHARMAC has continued to

successfully contract more medicines at cheaper prices. PHARMAC’s success has pushed more

pharmaceuticals into the sub-$5 price bracket. This is because the margin received on these

medicines is 4% under the CPSA and the margin paid to wholesalers is typically 8% to 10%, resulting

Environmental Scan Regarding Drug Margins – January 2015 23

in a loss to pharmacy. Interviewees were well aware of New Zealand’s unique progressive margin

structure and had a strong feeling that this was particularly “unfair” for pharmaceuticals under $5.

Wholesalers are responsible for setting the price point for low cost medicines within their terms of

trade and that any changes to this price point and the availability of discounts is at their discretion.

Notwithstanding this issue, Pharmacies may still be receiving a proportion of the margin for a “basket

of goods” (i.e. across a number of transactions, a “basket of goods”, pharmacy are able to cover the

margin charged by the wholesaler.

Not purchasing “outer pack”

Pharmacies are encouraged to purchase “outer pack” from wholesalers. That is, to purchase

quantities in the same standard “pack” size that the wholesaler receives from the Manufacturer.

This issue is three-fold for pharmacy:

i. If a pharmacy chooses to purchase “outer pack” then it receives a discount on the purchase

but then bears the risk of product stock-holding, wastage and/or expiry;

ii. If a pharmacy purchases “outer pack” but then must dispense a quantity that is different to the

original packaging. The pharmacy then incurs additional costs of repackaging or re-pouring

and the risk of wastage on residual stock; or

iii. If a pharmacy does not purchase “outer pack” then it reduces the risk of stock-holding,

wastage and/or expiry but does not receive the wholesaler’s discount. We understand that

without the “outer pack” discount, items are procured at a loss of up to 6% to 7% as

pharmacy pay wholesalers up to 10% for items.

6.1.5. Recalls

Costs associated with product recalls are not specifically funded under the CPSA.

Pharmacies are required to contact each patient that has received the medicine in the event of a

recall. Pharmacies report material cost, in the form of staff time, associated with undertaking this

activity for which they do not have control over and are not responsible.

We were told that wholesalers receive some payment from Manufacturers to cover the costs of

managing the recall on their behalf. Wholesalers are increasingly seeking to pass on the cost of

administering recalls to Manufacturers or refusing to undertake services if Manufacturers are not

willing to pay. Wholesalers consider that Manufacturer led administration of recalls would be a more

time-consuming, expensive and inconvenient service for Community Pharmacy.

Most interviewees acknowledge the burden of cost for pharmacies, however of these, some strongly

held the view that costs related to recalls are not and should not be covered by the pharmaceutical

margin but could potentially be addressed through other mechanisms.

Environmental Scan Regarding Drug Margins – January 2015 24

6.1.6. Wastage and expiry

Both pharmacy and wholesalers bear the risk and cost of any wastage or expiry of product. This is

closely linked to previous discussion regarding PHARMAC funding (Report section 6.2.1.); Service

Fee cross-subsidisation (6.2.3.); and Medicines priced under $4 and “outer packs” (6.2.4.).

PHARMAC’s terms with Manufacturers do not typically require the Manufacturer to supply packs in

quantities convenient for dispensing. Pharmacy must then repackage or pour medicines into the

correct quantity for dispensing, the residual quantity left is then subject to wastage risk.

Wastage and expiry risk is heightened for low volume, high cost medicines. Increasingly pharmacy is

questioning the sustainability of stocking high cost medicines due to these risks.

Both pharmacy and wholesalers have highlighted the risk and cost of wastage associated with

PHARMAC’s notification periods. Recent short notification periods have led wholesalers and

pharmacy to bear increased risk of stock write downs as they are unable to sell through stock on hand

in the change-over period agreed between the suppliers and PHARMAC.

6.1.7. Rural and small urban pharmacy

Interviewees noted that rural or small urban pharmacies do not receive the same level of discount

from wholesalers as larger urban pharmacies as they order smaller volumes and are generally more

susceptible to inefficient ordering practices.

As mentioned previously, some isolated rural pharmacies may be limited to a single wholesaler due to

the location of distribution warehouses. Their choice will be limited to that wholesaler to ensure

security of supply to meet the requirements of the CPSA.

These rural and small urban pharmacies typically order higher quantities from wholesalers less

frequently to maximise discounts for efficient ordering. For this reason there is a higher risk of

wastage, stock-holding and expiry for these pharmacies, particularly on low volume, high cost

medicines.

Some of those interviewed were of the view that smaller urban pharmacies typically operate in areas

where patients have sufficient access to pharmacy, if required, and therefore the sustainability of

these businesses is not necessarily a concern in all cases. However, rural pharmacies concerns in

this regard were generally considered to be valid.

6.1.8. Product cross-subsidisation

There is a strong perception from most interviewees that margin on OTC products has historically

cross-subsidised losses incurred in the procurement of subsidised prescription medicines.

New entrants, including supermarkets, are increasingly supplying OTC products to consumers in New

Zealand. Interviewees believe that these new entrants are, and will continue to, erode OTC market

share for both pharmacy wholesalers and therefore could compromise their ability to cover the cost of

procuring prescription medicines.

Environmental Scan Regarding Drug Margins – January 2015 25

6.1.9. Section 29 medicines

The Medsafe website provides the following guidance on “Section 29 medicines”:

“Section 29 of the Medicines Act permits the sale or supply to medical practitioners of medicines that

have not been approved, and requires the "person" who sells or supplies the medicine to notify the

Director-General of Health of that sale or supply in writing naming the medical practitioner and the

patient, describing the medicine and the date and place of sale or supply, and the number of packs

supplied…

On occasions a pharmacist working in a pharmacy may be involved in the supply of an unapproved

medicine as the medical practitioner's agent. If the pharmacy has imported the medicine, it is the

pharmacist's responsibility to ensure that the details of supply are sent to Medsafe. If the medicine

has been obtained from a distributor for an identified patient then that distributor should be given all

information required to be held, according to section 29…

Section 29 supply will be audited as part of the annual audit for a Wholesale licence.”

The requirement to submit details regarding the supply of Section 29 medicines leads to a

disproportionate administrative burden for both wholesalers and pharmacy.

Wholesalers have recently started to charge pharmacy an administration fee of $3 per item for

Section 29 orders. Under the contract pharmacy is unclear whether pharmacy is permitted to on-

charge this cost to patients but we understand that, anecdotally, on-charging does occur to cover the

administration fee on these items.

Some Manufacturers consider the cost and compliance associated with Registering certain medicines

in New Zealand to be unviable due to low volumes or older medicines. There are minimal incentives

for Manufacturers to register in these situations and the consequence is compliance costs are shifted

to the Supply Chain.

6.2. Pressure points for wholesalers (as expressed by pharmacy and wholesaler participants)

Many of the issues confronting pharmacy are also a concern for wholesalers, not least due to

wholesalers’ interest in the going concern and sustainability of their customers’ business.

Non-wholesaler interviewees generally were of the view that wholesalers were not profligate with their

current business and operated effectively given the revenue they receive and costs they bear.

The following are additional pressure points to wholesalers, as expressed by pharmacy and

wholesaler participants, in the Supply Chain:

Ordering frequency;

Cost inflation;

Price setting mechanism;

Sharing of margin with pharmacy;

Direct to patient supply; and

New entrants / low barriers to entry

Environmental Scan Regarding Drug Margins – January 2015 26

Wholesalers’ share of the pharmaceutical margin must cover costs associated with:

Cartage;

Stockholding;

Wastage;

Expiry;

Inventory management software (SAP); and

The cost of staff time associated with the above functions.

6.2.1. Ordering frequency

Wholesalers are typically only able to place two orders with Manufacturers each month but must be

able to supply pharmacy daily given pharmacies’ CPSA requirements.

This places additional stock-holding risk on wholesalers who must ensure they hold enough stock for

pharmacies to call on. The frequency of orders received from pharmacy is also the major contributor

to cartage costs incurred by wholesalers.

6.2.2. Price setting mechanism

Wholesalers have no influence over the price setting mechanism or sole supply decisions made by

PHARMAC. However, PHARMAC’s purchasing decisions, as described in 6.2.1, have a significant

impact on the revenue received by wholesalers and pharmacy from the pharmaceutical margin.

Wholesalers have difficulty planning ahead as there is a high degree of uncertainty regarding

PHARMAC’s gross spend in any given year. This is linked to the issue of transparency regarding

rebates, the increasing number of medicines moving to generics and PHARMAC redirecting savings

outside of Community Pharmacy. We do note that, despite issues of transparency and budgeting for

wholesalers and pharmacy, margin funding is paid based on gross spend, so rebates do not affect the

funding paid to Community Pharmacy. Some interviewees were of the view that rebates in fact keep

margin funding artificially high for a period.

As the number of medicines priced under $4 increases, the margin to wholesalers and pharmacy

decreases. This reduced margin coupled with increased medicine volumes is squeezing the margin

of wholesalers.

6.2.3. Cost inflation

Wholesalers cover the cost of transport and cartage within their share of the pharmaceutical margin.

Wholesalers incur similar costs when distributing a $1 or $100 medicine of similar physical size.

The cost of transport is a large contributor to the relatively high wholesaler margin placed upon low-

cost ethical medicines. A significant issue for interviewees was the high costs related to “cold chain”

and special foods.

Cold chain, i.e. temperature controlled distribution through the supply chain for medicines, was a

particular concern as the cost of this process is high. Similarly special foods are typically bulky

products that incur high transport costs due to their size and/or weight.

Environmental Scan Regarding Drug Margins – January 2015 27

Third parties, including transport providers, have increased their costs at the same time that revenue

from margins have decreased and volumes have increased. Increased volumes results in more

deliveries and increased transport charges.

Wholesalers have indicated that they will continue to seek to recover costs, within the confines of the

competitive marketplace, in areas where it is uneconomic for them to supply and this is likely to be for

products that require specialist services such as cold-chain. On-charging would only squeeze

pharmacy further as they currently have no means to on-charge these costs to the patient.

6.2.4. Sharing of margin with pharmacy

As mentioned in section 5, Unique Aspects of the NZ Supply Chain, New Zealand differs from other

jurisdictions in having a shared subsidised pharmaceutical margin for wholesalers and pharmacy.

Other jurisdictions provide separate margins for wholesalers and pharmacy respectively. In Australia

the wholesaler margin is regulated at 7.52% whereas in New Zealand wholesalers are able to choose

what margin to apply but must be mindful about how this impacts pharmacy as their customer.

6.2.5. Direct to patient supply

As discussed in Section 6.1.1, PHARMAC has recently started distributing high cost medicines

directly to patients. This method of distribution is typically used for unusual medicines when the

patient receiving the medicine is known.

Wholesalers are concerned that PHARMAC is circumventing margin funding structure through this

method of distribution and, in doing so, undermining the Supply Chain.

6.2.6. New entrants / low barriers to entry

New Zealand’s full-line wholesalers, like those internationally, are under pressure from new entrants

that choose to only stock higher margin OTC products. These new entrants do not have customers

that are required to meet the service obligations associated prescription-only medicines.

OTC products are now available in supermarkets (both progressive and foodstuffs). Wholesalers

have historically cross subsidised ethicals with OTC but this may be limited in future if the OTC

competitive landscape heats up.

6.3. DHB perspectives and implications

We also interviewed a number of DHB representatives to canvas their perspectives on the current

supply chain.

A common theme in our discussions with DHB representatives was that there is a lack of clarity over

what the drug margin is intended to cover. Pharmacy and wholesalers interviewed were under the

impression that dispensing fees should not cross-subsidise procurement and stock-holding activities.

DHB interviewees disputed this interpretation as, in their view, it is not well defined when supply chain

activities stop and when dispensing activities commence.

Environmental Scan Regarding Drug Margins – January 2015 28

Another common theme was that DHBs believed that the number of community pharmacies is

currently too high in some areas. The interviewees believed that concerns from pharmacy and

wholesalers over the sustainability of the current model should be placed in the context of the over-

provision of pharmacies in some areas. It is suspected that pharmacies of scale and those closer to

primary health facilities were not at risk under the current funding mechanism.

DHBs did acknowledge that small rural pharmacies have a unique set of challenges that result in

higher risks and costs related to procurement and stock-holding.

Other perspectives voiced by DHBs included:

Concern that DHBs have little influence or transparency over costs that are incurred in the

supply chain. Wholesalers in New Zealand distribute products via a number of channels and

do not disclose costs exclusively related to Community Pharmacy;

DHBs are supportive of initiatives that have increased distribution of medicines directly to the

patient as this is considered the most efficient delivery method; and

DHBs are not confident that the current mechanism encourages innovation in the distribution

of medicines. Examples cited included increased use of robotics and delivery methods that

circumvent the current funding mechanism.

The overall perception of interviewees both in New Zealand and Australia was that New Zealand’s

supply chain is very efficient by international standards.

However, there is a high degree of concern in the sector that the current funding for pharmaceutical

margins is unsustainable. This perception is strengthening as PHARMAC continues to successfully

reduce prices for pharmaceuticals and invests its budget outside of Community Pharmacy.

A robust supply chain is crucial to cost-effective delivery of medicines in New Zealand.

Internationally, Manufacturers have acknowledged the valuable role that wholesalers and pharmacy

play in distributing pharmaceuticals to patients. Wholesalers that are capable of assuming the

working capital risk of full-line stock-holding are crucial to ensure that pharmacy can supply to the

requirements of the CPSA.

Environmental Scan Regarding Drug Margins – January 2015 29

Appendix 1

Interviews

Mike Rhodes - CDC Pharmaceutical Limited

Anna Mickell - Pharmacy Retailing (NZ) Limited

David Bullen – Green Cross Health

Lee Hohaia – Pharmacy Guild New Zealand

Stephen Armstrong – Pharmacy Guild of Australia

David Mitchell – Pharmacy Partners

Johnny Louie – Bay of Plenty District Health Board

Ken Orr – Pharmacy Guild New Zealand

Michael James- Canterbury District Health Board

Matthew Wood – Canterbury District Health Board

Tim Wood – Waitemata District Health Board

Helene Carbonatto - Service Integration and Development Unit at Capital & Coast District Health

Board

Sandra Williams - Service Integration and Development Unit at Capital & Coast District Health Board

Steffan Crausaz – Chief Executive, PHARMAC

Grant Short – 2TEN Consultants

Kiusiang Tay-Teo Ph.D – Associate Director, Health Economics and Social Policy, Deloitte Australia

Environmental Scan Regarding Drug Margins – January 2015 30

Documents

Burden of Disease Epidemology, Equity and Cost-Effective Programme, Costing of Pharmaceuticals

in New Zealand for Health Economic Studies: Backgrounder and Protocol for Costing, Technical

Report: Number 6, September 2011

Commerce Commission, Section 66: Notice Seeking Clearance for the Proposed Merger of CDC and

PWL Central (Public Version), June 2014

European Medicines Information Network, The Pharmaceutical Distribution Chain in the European Union: Structure and Impact on Pharmaceutical Prices, March 2011

New Zealand Ministry of Health, Medicines in New Zealand: Contributing to good health outcomes for

all New Zealanders, December 2007

Environmental Scan Regarding Drug Margins – January 2015 31

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee,

and its network of member firms, each of which is a legally separate and independent entity. Please

see www.deloitte.com/nz/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu

Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning

multiple industries. With a globally connected network of member firms in more than 140 countries, Deloitte

brings world-class capabilities and deep local expertise to help clients succeed wherever they operate. Deloitte’s

approximately 169,000 professionals are committed to becoming the standard of excellence.

Deloitte New Zealand brings together more than 900 specialists providing audit, tax, technology and systems,

strategy and performance improvement, risk management, corporate finance, business recovery, forensic and

accounting services. Our people are based in Auckland, Hamilton, Wellington, Christchurch and Dunedin, serving

clients that range from New Zealand's largest companies and public sector organisations to smaller businesses

with ambition to grow. For more information about Deloitte in New Zealand, look to our website

www.deloitte.co.nz.

Confidential – this document and the information contained in it are confidential and should not be used or

disclosed in any way without our prior consent.

© 2015 Deloitte. A member of Deloitte Touche Tohmatsu Limited.