distribution in china - fung group · association (ccfa) and the li & fung research centre had...

TRANSCRIPT

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

1

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Distribution in China: a perspective from leading retailers

With vast geographical span and huge regional differences, distribution1 in China has long been complicated. Often,

goods have to pass through multi-layers of distributors before reaching the hands of consumers. As China strives to

build a more consumption-driven economy, the country’s distribution sector is gaining increasing attention these days,

both from businesses and the government.

Eyeing the huge potential of the burgeoning consumer market, many manufacturers and retailers have been keen to

expand distribution network as well as to improve supply chain efficiency over the past years; urbanization and fast

development of transportation infrastructure are also rapidly changing China’s distribution sector. China’s wholesale

distribution landscape has witnessed significant transformation. Exciting changes are taking place.

Hoping to shed light on the latest development in China’s distribution sector, the China Chain Store and Franchise

Association (CCFA) and the Li & Fung Research Centre had jointly conducted a study on China’s distribution landscape

in 2009 to interview 30 prominent Chinese retailers - including convenience stores, supermarket and hypermarket

operators - on their distribution practices. We aim to have a closer look into China’s distribution sector from the

perspective of retailers.

Indeed, businesses home and abroad today are casting their eyes on China. Building demand-driven supply chains is

crucial for business success. We hope our study can help enterprises interested in expanding domestic sales.

I. Background - several observations on China’s distribution sector

1. Growing pressure of disintermediation

In the past years, we have witnessed much streamlined and shortened retail supply chains in China, thanks to more

centralized sourcing and distribution strategies of retail chain operators and the emergence of retail formats such as

manufacturer direct-sale. The bargaining power and survival of distributors, especially those traditional players serving

solely as a middleman between manufacturers and retailers without much value-added services, are under a lot of

pressure. Discussion of disintermediation, which refers to the removal of intermediaries in supply chains or “cutting out

of the middlemen”, is catching attention. 1 We refer distribution to operating activities involved as goods relayed from manufacturers to retailers; key players comprise

manufacturers, wholesalers and retailers; there may be title transfer of product ownerships during distribution.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

2

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

In fact, China’s distribution sector is highly fragmented. Competition is particularly intense in the lower spectrum of the

market and many who cannot offer higher value-added services to clients often have to resort to price-cuttings, eroding

these players’ profitability. Besides, business costs such as labor, energy, raw materials, and logistics have been rising.

Many players just manage to earn razor-thin margins.

2. Retail chain operators have gained power over their suppliers

Owing to market liberalization, retail chain operators have been rapidly expanding their influence in China in the past

decade. The total sales revenue of China’s Top 100 retail chain operators (hereafter “the Top 100s”) reached RMB

1,360 billion in 2009, up by 13.5% year-on-year (yoy). The market share of the Top 100s in the country’s total retail sales

of consumer goods has climbed from 3.8% in 2001 to 10.9% in 2009. Their total number of stores was 137,000, rising by

18.9% yoy.

Unlike in the early days of reform, product distribution today is no longer supply-driven. We witness a significant shift in

power in China’s retail supply chains. Retail chain operators in China have gained power over their suppliers because of

huge purchase volume. Indeed, many retailers have taken advantage of their strong market power – many introduce

cumbersome charges such as entrance fees, promotion and marketing charges, listing fees for new products and

launch different rebate and commission schemes to suppliers. Many wholesale players have reflected huge cost of entry

into modern trade retailers and called for more stringent regulations on retailers’ behavior - retailers introducing heavy

fees does not only eat into the profits of wholesale players, but also makes lesser-known brands harder to compete for

shelf space, limiting consumers’ choices and may lead to fraudulent activities as well.

Some retailers in China frequently extend payment of payables to suppliers, using it as a major source of funding for

working capitals. Many suppliers are wary of payment defaults. Tension between retailers and suppliers in China has

been a top industry concern.

3. Closer collaboration among supply chain partners in recent years

The mistrust among supply chain members in China has hampered information sharing in the entire value chain, leading

to bullwhip effects and has posed major barriers in enhancing supply chain efficiencies. This has hampered retailers to

react quickly to market demand. More and more retailers are now aware of the repercussions and are hoping to change

the picture.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

3

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Thanks to the concerted efforts between government, industry organizations, suppliers and retailers, retailer-supplier

relationship has shown signs of gradual improvements. Retailers now pay more attention to improve their operating

performances and seek better collaboration with their suppliers. For instance, China’s largest foreign retailer RT-Mart

has offered supports to their suppliers on areas such as logistics operations and backend information systems in order

to drive quicker responses to consumer needs. Watsons has joined hands with suppliers to co-launch advanced

information management system in an attempt to reduce inventories.

According to a study conducted by Shanghai Business.net and the FMCG Research Centre, suppliers were more

satisfied with retailers in 2009. Another survey by the CCFA also showed that the supplier satisfaction index and

manufacturer satisfaction index have risen from 57% and 33% in 2008 to 82% and 62% in 2009.

4. More diversified distribution models

Many retailers have embarked on multi-channel strategy to lower operation costs and to achieve wider customer reach

in China. Online retailing, telephone retailing, television retailing and catalogues sales are becoming more popular. More

diversified distribution models now emerge in China with increasing popularity of multi-channel retailing.

For instance, among the Top 100s in China, 31 had set up their online front stores; of which, one-third had started their

online businesses in 2009 and 2010.

Not limited to the retailers, some traditional wholesalers such as Yiwu wholesale market in Zhejiang have established

online trading platforms. Merchandisers can now conduct business negotiations and transactions conveniently through

the platform.

Today, China’s distribution models are more diversified with the emergence of multi-channel retailing and wholesaling.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

4

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

II. Looking into China’s distribution sector: a perspective from leading retailers

To understand the latest development in China’s distribution sector, the CCFA and the Li & Fung Research Centre had

jointly conducted a study in 2009. The study aimed to collect first-hand quantitative information from leading retailers in

China. Our study covered 3 different retail formats: convenience stores, supermarkets and hypermarkets.

A total of 30 retailers in China, which include state-owned enterprises, solely-owned foreign enterprises, Chinese private

enterprises, joint ventures, state-invested enterprises and shareholding companies were surveyed.

25 of the retailers (83.33%) in our survey were among the Top 100s in 2008.

All retailers achieved annual sales revenue of RMB 100 million or above; of which 37.93% of the retailers achieved

annual sales revenue of RMB 10 billion or above in 2009.

See Exhibit I and 2 for the company types and sales revenue of the retailers.

Exhibit 1: Company type

Company type Number Percentage

State-owned enterprises 6 20.69%

Solely-owned foreign enterprises 5 17.24%

Chinese private enterprises 14 48.27%

Joint ventures 1 3.45%

State-invested enterprises 1 3.45%

Share-holding companies 2 6.90%

Total 29 100%

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

5

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Exhibit 2: Annual sales revenue, 2009

Annual sales revenue (RMB) Number Percentage

Below 100 million - -

100 million to 1 billion 3 10.34%

1 billion to 3 billion 5 17.24%

3 billion to 5 billion 7 24.14%

5 billion to 10 billion 3 10.34%

10 billion or above 11 37.93%

Total 29 100%

The key findings of the survey are as follows:

1. Wholesale distributors still play an indispensable role

According to the survey, more than 60% of the products in retail stores were sourced from distributors or agents while

the remaining were sourced directly from manufacturers. We also observe that the larger the scale of the retailers, the

smaller the proportion of goods they sourced from distributors or agents (the smallest share in the survey is 45%). On

the contrary, the smaller the scale of the retailers, the larger the proportion they sourced from middleman (the largest

share in the survey is 82%). Despite growing discussion about disintermediation, the findings suggest that distributors

and agents still play an important role in the supply chains.

We believe wholesale distributors will continue to play an indispensable role in China. The reasons are three-fold. Firstly,

despite rapid growth of chain operation in the past decade, China’s retail market remains highly fragmented. Second,

the vast geographical span of China offers a lot of development room for distributors, especially in some inner regions

and the rural hinterland; many companies simply do not have the skill sets and resources in developing own distribution

channels in these regions. Besides, as brands rush to sell in China like bees to honey, many do not have the know-how

in marketing and distribution and need a distribution partner. Indeed, China is both a fast-growth and high-risk market.

As brand principals seek to manage their fixed costs, there is still huge room for wholesale players to grow.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

6

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

2. Consignment sales are popular

Consignment sales� are popular in China. According to our study, 82.05% of the products were under consignment

sales arrangements, while 11.22% were bound by buy-out agreements�. For the remaining 6.28%, manufacturers/

suppliers and distributors adopt the concession model�.

Distributors bear great risks in consignment sales model as they receive no money until the goods are sold. Therefore

they must have sufficient cash flow to survive extended periods for payments of merchandise sold. Cash flow problem is

a particular challenge for smaller distributors.

3. Nearly 60% of products were distributed to retail stores by suppliers

On average, 59.56% of the products were distributed to retail stores by suppliers; 31.87% of the products were handled

by retailers’ own distribution centers; only 8.57% was handled by third-party logistics service providers.

Usually, smaller retailers would rely more on logistics services provided by suppliers; meanwhile, larger retailers are

more likely to have the goods handled by their own distribution facilities.

Exhibit 3: Product distribution methods

59%

32%

9%

Logistics servicesprovided by suppliers

Through retailers' owndistribut ion centers

Through third-partylogistics serviceprovders

2 Consignment (

���, ��������� ) occurs when suppliers (the consignor) provide goods to a reseller (the consignee) for sale

within a period agreed upon by both parties. There is no title transfer of product ownerships and the consignee has the right to return any products that are unsold. 3 There is title transfer of product ownerships in buy-out ( ��� ) transactions. Payment has to be settled immediately when the retailers receive merchandise. Retailers cannot return the products unless there are quality problems. 4 Retailers/ distributors lease the retail sites to suppliers/ manufacturers and offer relevant management expertise and guidelines in return for rental income and commission fee. Meanwhile, suppliers and manufacturers will send sales representatives to the retail sites, and are responsible for merchandising, pricing, logistics, promotion activities and after-sale services. Retailers/ distributors typically will not purchase any goods from the suppliers and manufacturers.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

7

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

4. Online retailing strategy is increasingly popular, bringing new changes to distribution landscape

Online retailing has been increasingly popular in China, especially among the tech-savvy and young population.

According to iResearch, China’s online transaction value reached RMB 263 billion in 2009, representing a stellar

year-on-year growth of 105.2%. Eyeing the huge market potential, a number of retailers have embarked on

click-and-mortar strategy.

According to our survey, 12 out of the 30 retailers (40%) had established their online retailing platforms. And most of the

online stores were developed and run independently. Another 27% of the retailers had planned to develop their online

retailing platforms in the next few years.

Exhibit 4: Launching online retailing platforms

33%

27%

40%No online platform withno plan to build oneNo online platform; butwith plan to build oneHave online retailingplatform

We are positive on the long-term growth prospect of e-commerce in China. Online platform is today an effective

doorway to tap China’s growing number of online shoppers. Nevertheless, logistics and fulfillment remain one of the

challenges. China’s online retailers have invested huge sums of money to improve these areas. Growing popularity of

the bricks-and-clicks model is quickly transforming China’s distribution landscape.

5. Retailers said relationship with suppliers is satisfactory

Retailer-supplier relationship is crucial for the healthy development of the retail sector. Better collaboration between

retailers and suppliers is a key element in building demand-driven supply chains.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

8

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

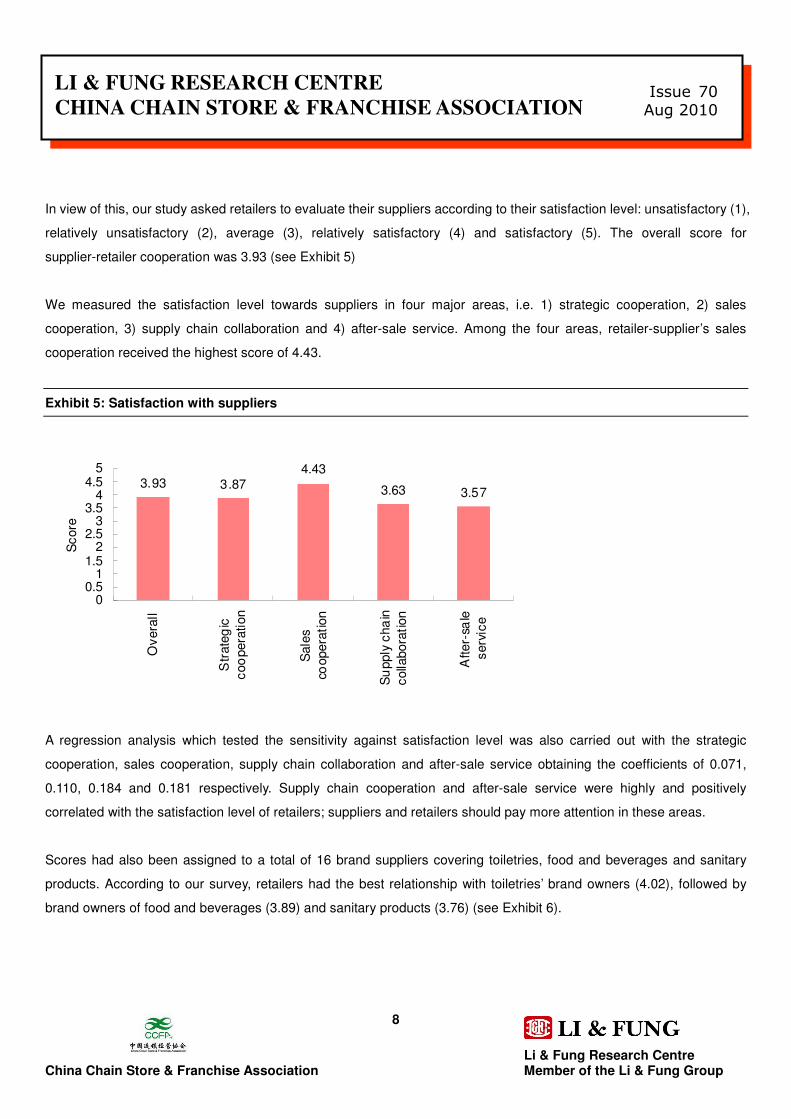

In view of this, our study asked retailers to evaluate their suppliers according to their satisfaction level: unsatisfactory (1),

relatively unsatisfactory (2), average (3), relatively satisfactory (4) and satisfactory (5). The overall score for

supplier-retailer cooperation was 3.93 (see Exhibit 5)

We measured the satisfaction level towards suppliers in four major areas, i.e. 1) strategic cooperation, 2) sales

cooperation, 3) supply chain collaboration and 4) after-sale service. Among the four areas, retailer-supplier’s sales

cooperation received the highest score of 4.43.

Exhibit 5: Satisfaction with suppliers

3.93 3.874.43

3.63 3.57

00.5

11.5

22.5

33.5

44.5

5

Ove

rall

Str

ateg

icco

ope

ratio

n

Sal

esco

oper

atio

n

Su

pply

cha

inco

llabo

ratio

n

Afte

r-sa

lese

rvic

e

Sco

re

A regression analysis which tested the sensitivity against satisfaction level was also carried out with the strategic

cooperation, sales cooperation, supply chain collaboration and after-sale service obtaining the coefficients of 0.071,

0.110, 0.184 and 0.181 respectively. Supply chain cooperation and after-sale service were highly and positively

correlated with the satisfaction level of retailers; suppliers and retailers should pay more attention in these areas.

Scores had also been assigned to a total of 16 brand suppliers covering toiletries, food and beverages and sanitary

products. According to our survey, retailers had the best relationship with toiletries’ brand owners (4.02), followed by

brand owners of food and beverages (3.89) and sanitary products (3.76) (see Exhibit 6).

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

9

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Exhibit 6: Scores given by retailers for suppliers of different products

4.02

3.89

3.76

3.63.65

3.73.753.8

3.853.9

3.95

44.05

Toiletries Food and beverages Sanitary products

Sco

re

6. Degree of cooperation among supply chain partners

To understand the degree of cooperation between supply chain partners, retailers were asked to assign a score from 1

to 5 on areas including strategic cooperation, sales cooperation and supply chain collaboration with suppliers (“1”

represents no cooperation; “5” represents very close cooperation). The scores were relatively high at 4.21, 4.22 and

4.26 respectively (see Exhibit 7).

Exhibit 7: Degree of cooperation with suppliers

4.214.22

4.26

4.184.2

4.22

4.244.264.28

Strategiccooperation

Salescooperation

Supply chaincollaboration

Sco

re

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

10

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Exhibit 8 details the degree of cooperation in 3 major areas.

Exhibit 8: degree of cooperation in 3 major areas

Cooperation

areas Indicators

Degree of

cooperation

Importance

weight (%)

Average

Score

1. Understanding the business strategy of

your company with regular high-level

meetings

4.27 12.82

2. Formulating business plan with your

company with quality business evaluation 4.30 28.21

3. Launching projects jointly with your

company in areas such as consumer

behavior analysis, joint sales promotion,

supply chain optimization and loss

prevention

4.17 15.38

4. Taking initiatives to increase profitability

of both parties and maximizing common

interest

4.07 17.95

5. Embarking on different sales strategies

according to different retail format

operations of your company

4.10 7.69

Strategic

cooperation

6. Providing products and services

according to your company’s needs;

helping your company increase sales and

profitability

4.27 17.95

4.21

7. Providing regular analysis on

consumption behavior; assisting your

company to understand consumer’s need

4.30 22.86

8. Working closely with your company on

category management 4.03 14.29

Sales cooperation

9. Sharing market data with your company

and providing recommendations

accordingly

4.00 17.14

4.22

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

11

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

10. Frequently updating with your

company on new product launch, pricing

changes and promotion plans; making

sales forecasts and formulating promotion

strategy with your company

4.30 22.86

11. Providing recommendations on how to

improve customer traffic and consumer

loyalty; launching joint promotion

4.27 11.43

12. Providing training to salespersons and

helping your company reduce human

resources and management cost

4.33 11.43

13. Sharing with your company on the

operations of its supply chain as well as

core performance indicators; setting

common targets in areas of inventory

turnover, out-of-stock ratio and logistic

cost

4.33 25.00

14. Making sales forecast with your

company 4.23 19.44

15. Providing updated, accurate and

comprehensive market data for your

company to enhance information flow in

the supply chain

4.13 11.11

16. Delivering the right quantities of

products to the right place at the right

time

4.40 13.89

17. Offering solutions to your company

should there be supply problems 4.27 25.00

Supply chain

collaboration

18. Taking measures to prevent loss and

damages in daily operations; formulating

loss prevention scheme with your

company

3.80 0

4.26

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

12

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

19.Increasing logistics efficiency by

continuous improvement of technology

and data management

3.97 5.56

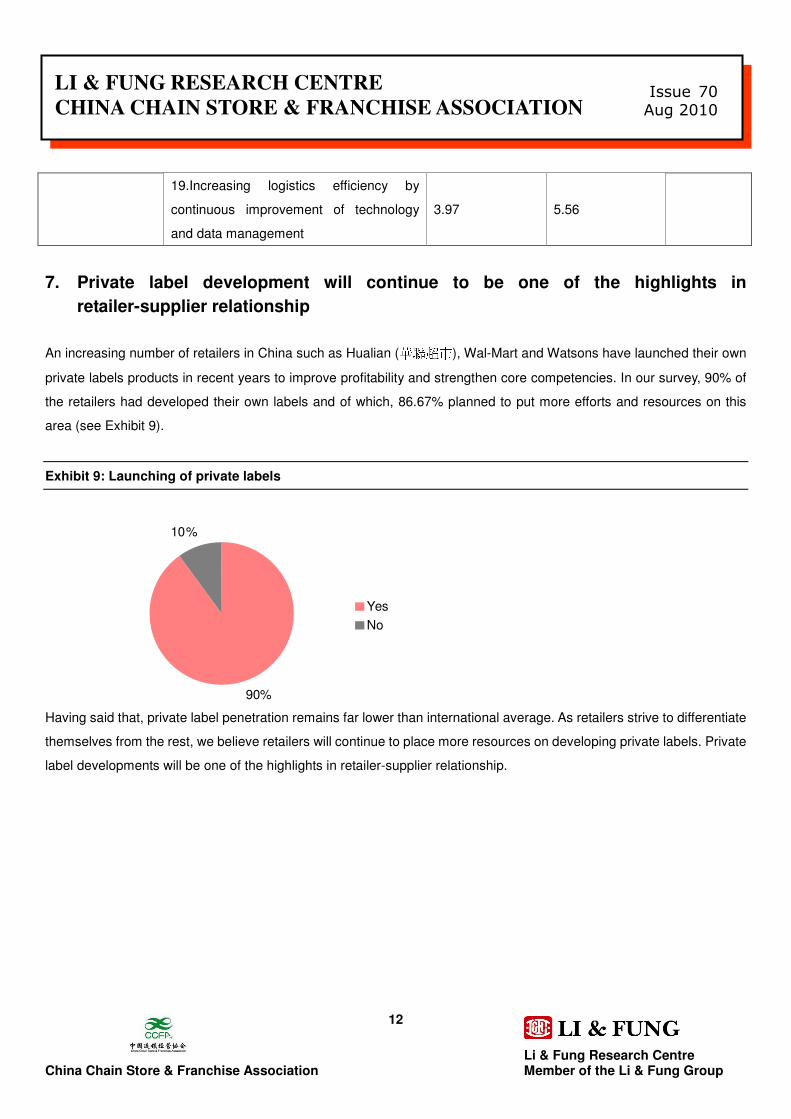

7. Private label development will continue to be one of the highlights in retailer-supplier relationship

An increasing number of retailers in China such as Hualian ( ������� ), Wal-Mart and Watsons have launched their own

private labels products in recent years to improve profitability and strengthen core competencies. In our survey, 90% of

the retailers had developed their own labels and of which, 86.67% planned to put more efforts and resources on this

area (see Exhibit 9).

Exhibit 9: Launching of private labels

90%

10%

YesNo

Having said that, private label penetration remains far lower than international average. As retailers strive to differentiate

themselves from the rest, we believe retailers will continue to place more resources on developing private labels. Private

label developments will be one of the highlights in retailer-supplier relationship.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

13

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Special highlight: China’s export-oriented enterprises embarking on domestic sales – a distribution challenge

The financial crisis that swept through the globe since the later half of 2008 has brought synchronized recession in major

economies and tremendous changes in international trade dynamics. Many retailers in the United States and Europe

have suffered from softening retail sales and tightening credit lines. On the other hand, many retailers in China are

fortunate enough to witness strong market resilience. China’s ever-expanding domestic market is gaining increasing

attention from the country’s many export-oriented manufacturers. More and more manufacturing enterprises now

employ a twin-pronged strategy or so-called walking on two legs, by engaging in both domestic and foreign trade

sectors.

Having said that, “selling to the source” is no easy task. Many export-oriented enterprises lack the experience,

know-how, and resources tapping the domestic potential. Selling to the source is particularly difficult for traditional

processing trade factories (TFPs), as most of them have for a long time been engaged chiefly in original equipment

manufacturing (OEM) activities, earning a razor-thin margin. Many have little, if not no experience in design, product

development, branding, selling, and marketing. Without much market recognition of their products, tapping the already

crowded domestic retail scene is a huge challenge.

Indeed, there are huge differences between domestic and foreign trade engagements in terms of method of payment,

mode of operation, business registration, applicable regulations, and so on. Exhibit 10 summarizes the major

differences. Foreign orders are typically larger in size with product specifications provided by clients. Payments are

better secured and TFPs are exempt from paying value-added tax (VAT) and tariffs. This explains why some exporters

still adopt a wait-and-watch approach in tapping the domestic market potential. Tapping the domestic market, to many, is

in itself a distribution challenge.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

14

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

As chain retailers expand their scale in China, it is suggested that chain retailers could have a bigger role to play by

introducing the made-to-export products to the Chinese consumers. It is true that the order volume involved in domestic

trade is typically much smaller than their overseas counterparts, but chain retailers can increase the purchase volume

through central sourcing.

In fact, some leading retailers have launched a series of initiatives in the past two years to help export-oriented

Exhibit 10: Domestic trade vs. foreign trade

Domestic trade Foreign trade

Order volume Smaller order volume, but orders are

generally placed in a more frequent

manner.

Larger order volume

Method of payment Case by case for each manufacturer.

Usually late payments by clients.

Use the letter of credit, which is

internationally accepted. Buyers usually

pay a deposit in advance and pay in full

upon delivery of products.

Operation Buyers require the manufacturers to

produce the products first and then

determine the order volume after

examining the products. It increases

risks such as excessive inventory to

the manufacturers.

Buyers provide the manufacturers with

designs and other technical

requirements when placing orders.

Marketing & after-sale

services

Buyers require the manufacturers to

work together for better sales

performance by asking them to take

part in promotion and advertising,

which involves manpower and

financial resources.

Manufacturers are not involved in

aspects such as marketing and after-sale

services.

Source: Compiled by Li & Fung Research Centre

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

15

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

enterprise sell to the source. For instance, since April 2009, Wal-Mart has partnered with local governments to launch

the “Program Supporting Export-oriented Enterprises in Developing Domestic Market (PSEE)” in Guangdong, Jiangsu,

Zhejiang, Fujian and other regions where export-oriented enterprises are concentrated. It has sponsored 7 PSEE

activities and took part in 9 related exhibitions and symposiums organized by central and local governments. More than

1,000 enterprises attended PSEE trainings, and over 60 enterprises have successfully signed contracts with Wal-Mart to

put their products on the retail shelves, driving total sales of over RMB 50 million. Some other domestic retailers in China

such as Wumart ( ��� ), Hunan Better Life Commercial ( ��������� ), and Shandong Liqun Group ( � ��!�"�#%$ ) have

also taken measures to facilitate the domestic sales of export products, for instance, sourcing from the factory backlog

and employing the idle production facilities of the factory to develop and manufacture private label products for their

chains. Besides, some shopping mall operators such as Solana ( &�'�(�) ) in Beijing have also held sales fairs selling

the made-to-export products.

As mentioned, difference in payment methods has been a major concern as well. Today, the payment period for China’s

domestic sales can be up to two to three months. There are high incidences of payment defaults as well, adding to the

risks of suppliers. On the contrary, for exporters engaging in foreign trade activities, payments are better secured by

Letter of Credits and different exports insurance. These have deterred China’s export-oriented enterprises from selling

domestically. Attempts are being made to ease the financial pressures of suppliers. It is reported that some retailers,

suppliers and banks have worked together in pilot supply chain financing projects – in which retailers in China will act as

guarantors and banks will pay the suppliers some of the money for the merchandise first; retailers will later pay the

parties the proceeds from sales minus charges such as commission, service fees, etc.

The efforts are much appreciated; however, many measures launched are short-term without truly addressing the

historical legacy problem of separation of domestic and foreign trade sectors in China. To boost China’s domestic

private consumption, as well as to help millions of exporters expand their domestic sales, some longer-term mechanism

to facilitate domestic distribution of export products will be needed.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

16

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

III. Outlook 1. Growing calls for the government to improve the distribution sector

Boosting domestic private consumption today tops the agenda of the Chinese government. Apart from initiatives that

help boost domestic demand, e.g., accelerating income redistribution and improving social security system, there are

growing calls that the Chinese government should eliminate bottlenecks that hamper efficient and low-cost product

delivery in order to improve distribution in China, so that both businesses and consumers can benefit from more

responsive supply chains. We will introduce several major suggestions for the government to improve the country’s

distribution sector.

In fact, it is widely anticipated that the Chinese government will seek to improve the distribution sector in the forthcoming

Twelve Five-Year Plan.

Enhancing retail industry developments In the past decades, retail industry in China has witnessed impressive growth. However, retailers in China still lag far

behind their overseas counterparts in many areas such as management, branding, and information technology

applications. As retailers gained power over suppliers, many have transferred excessive risks or unexpected costs onto

their suppliers; unscrupulous practices are common.

Retailers relying heavily on slotting fees or harsh sales terms on suppliers is detrimental to the health of China’s

distribution sector, and is not sustainable in the long run. To boost the developments of China’s distribution sector, the

Chinese government should promote better regulatory environment for domestic distribution. The government has

launched The Management Rules on Fair Transaction between Retailers and Suppliers ( *�+�,�-�.�,�/�021�3 4�5267

) in 2006 and the Credit Management Technical Specification for Commercial Enterprises ( ,�8�9�:<;2=�4�5�>�?�@�A )

in 2008. However, there remains much improvement room on enforcement fronts. Relevant authorities should

strengthen its monitoring on industry players. Strengthening distribution in rural areas

The relatively underdeveloped distribution network and logistics infrastructure has hampered the distribution in the rural

areas. This does not only hurt the livelihood of rural households but also put consumption safety at risks. The Chinese

government has strived to improve distribution efficiency in rural areas in the past years.

Launched by the Ministry of Commerce (MOFCOM) in 2006, the Agricultural Produce Wholesale Market and

Distribution Company Development Project ( B�C���D�E�F ) aims to facilitate the distribution of agricultural produce to

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

17

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

markets through restructuring large-scale modern agricultural produce wholesale markets as well as nurturing

large-scale agricultural produce distribution enterprises. The MOFCOM has selected 100 agricultural produce wholesale

markets with extensive distribution coverage and helped them modernize and upgrade their logistics and information

system, warehouse facilities, quality assurance and food recall mechanism. It has also chosen another 100 large-scale

agricultural produce distribution enterprises and trained the operators to modernize their operation and cold storage

system, as well as ways to market to various modern retail channels.

It is suggested that the government should further utilize the platforms and expand the scope of the project to cover

categories not limited to agricultural produce but also the consumer products.

Promoting direct-farm sourcing to shorten retail supply chains

Retailer direct-farm sourcing is increasingly popular in China. First introduced in the country by Carrefour in 2007, many

foreign retailers such as Wal-Mart, Tesco, Lotus and RT Mart soon embarked on similar initiatives to save logistics and

merchandising cost by streamlining distribution.

Retailer direct-farm sourcing has significant implications in China. It benefits farmers, retailers and consumers; and

helps promote sustainable developments in the long run. China’s agricultural development is lagging behind. Many

small-scale farm producers have long relied on layers upon layers of middlemen to sell their products; distribution cost is

high. As the agricultural product supply chains are shortened, farmers will likely be benefited from higher purchasing

price. Besides, establishing long-term stable contractual relationship with retailers helps farmers improve sales and

facilitate future planning. Rural households sharing better profits will promote healthy developments of China’s

agricultural sector. Government efforts to further promote retailer direct-farm sourcing will be much appreciated.

Accelerating the integration of domestic and foreign trade sectors As mentioned, enterprises engaged in China’s domestic and foreign trade sectors are governed by differential policies;

the later is often said to enjoy more favorable government treatments, such as export tax rebates. Enterprises selling to

domestic markets also need to pay VAT. To help reduce the country’s reliance on exports, the Chinese government may

consider adjusting its trade policies to offer more incentives for enterprises switching to domestic sales. Initiatives

include also financial supports to the developments of online and offline wholesale platforms, and providing financial

incentives to export-enterprises engaging in domestic sales.

Enhancing the competitiveness of China’s wholesale distributors can help facilitate the integration of domestic and

foreign trade sectors as well. For instance, the government may encourage wholesale distributors with strong domestic

networks to play a more active role in helping export-oriented enterprises tap the domestic market, for example, by

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

18

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

offering advice on the latest consumer trends and alleviating capital or communication bottlenecks.

Indeed, facilitating domestic sales of made-to-export products can enrich the merchandise variety and mix in China,

benefiting the Chinese consumers. This is conducive to China to build a more consumption-led economy.

The central government can leverage on the close connection and proximity of the Pearl River Delta Region with Hong

Kong and use it as a testing ground of new policies to facilitate export-oriented enterprises engaging in domestic sales.

For example, the Guangdong and Hong Kong governments can work together to put in place a mutual recognition and

information-sharing mechanism in testing and certification services to the effect that test reports issued by accredited

testing and certification agencies of the China National Accreditation Service for Conformity Assessment and the Hong

Kong Accreditation Service can be recognized by regulatory authorities of the two places.5 This will greatly reduce the

enterprises’ costs and enhance efficiency. It can also ensure that the mainland standards are aligned with the

international ones.

Further, the Chinese government can consider establishing long-term mechanisms to facilitate domestic sales.

Previously, export processing enterprises intending to transform into “foreign-invested enterprises”, which can operate

business of domestic sale, needed to go through very complicated and time-consuming formalities. At present,

individual cities have introduced more simplified measures, including provision of “all-in-one” services, to speed up the

processing time. It is hoped that more similar measures can be provided.

Besides, city governments such as Shenzhen and Dongguan have organized a number of trade fairs after the financial

tsunami to promote domestic sales. The two places also implemented a trial practice of “taxation after sale”, which was

widely welcomed by enterprises and brought immense business opportunities to both cities. In view of this, the Chinese

government should study the possibility of extending similar measures in other cities and provinces.

2. Retailers in China will pay more attention to improve operations

China’s retail competition is fierce. To win the hearts of increasingly discerning Chinese consumers, growing numbers of

retailers in China now hope to break away from current operating model by offering more innovative product and

services. They are now paying increasing attention to improve different aspects of their operations. These have

profound implications on China’s distribution sector.

5 Under the new arrangements of CEPA 7, accredited testing organizations in Hong Kong are allowed to cooperate with designated Mainland organizations to undertake testing of selected products listed in the China Compulsory Certification (CCC) Catalogue and processed in Hong Kong. This arrangement which is considered as a breakthrough could facilitate HK enterprises’ entry into the Mainland domestic market. .

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

19

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

For instance, retailers are spending greater efforts to improve their retailing brand image to win consumer preference.

The lack of sophisticated retail merchandise knowledge is taking its toll on retailers – many have resorted to price cuts

as competition intensifies. Retailers growingly recognize that they should improve differentiation and brand

management, such as through unique product assortment and the launch of private labels to enhance shopping

experiences. Some are trying to take a more active role in merchandising practices. However, inventory risks, heavy

initial capital outlays and the lack of experience in sourcing remain common concerns. In this regard, retailers may

explore new profit- and risk-sharing schemes to work with suppliers or other professional supply chain companies to

improve merchandising.

And as mentioned, more and more retailers have embarked on bricks-and-clicks strategy. To improve time to market

response, many retailers have invested large sums of money in areas such as information technology, logistics and

fulfillment. We believe distribution efficiency in China to continue to increase.

3. Export-oriented enterprises will put more resources on domestic sales The trend for export-oriented enterprises to employ a twin-pronged strategy will continue, as the purchasing power of

Chinese consumers increases. Growing number of enterprises are now trying to move up the value ladder and have put

more resources on brand building and sales and marketing. Nevertheless, the cost of getting into the domestic channels

is likely to remain high; we expect online sales portals will be one of the most popular channels for these enterprises to

test the water in China.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

20

���������

�������

LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION

About the Organizations

The China Chain Store & Franchise Association ��������������������������������

Founded in 1997, the China Chain Store & Franchise Association (CCFA) is an official representative of the retailing and

franchise industry in China. Currently, there are 900 enterprise members with 160,000 outlets, including domestic &

overseas retailers, franchisers, suppliers, and relevant organizations. The total sales of China’s “Top 100 retail chain

operators”, which are part of the members of the CCFA, exceeded RMB 1.36 trillion in 2009, with more than 137,000

stores in total.

CCFA participates in policymaking and coordination, safeguards the interests of industry and members, provides a

series of professional trainings and industry information and data for its members and establishes platforms for

exchange and cooperation.

Li & Fung Group � � � � � � � �

The Li & Fung Group is a Hong Kong-based multinational company with three distinct core businesses: export sourcing,

distribution and logistics, and retailing. Founded in Guangzhou in 1906, the Li & Fung Group achieved an annual

turnover of around US$16.0 billion in 2009. Today, the Li & Fung Group operates in some 40 countries and regions and

employs over 33,000 people worldwide. One of its core competencies is “Supply Chain Management” (SCM).

Li & Fung Research Centre � �� � �� � �� � ��

Li & Fung Research Centre is the research institute of the Li & Fung Group. It serves as a knowledge bank on China's

economy, industries, logistics and distribution sector, with its research scope covering the whole spectrum of the entire

supply chain, from ideas, production, distribution, retailing to consumers. It also offers research analyses and consulting

services to colleagues and clients to assist them in their day-to-day decision-making.

© Copyright 2010 Li & Fung Research Centre and the China Chain Store & Franchise Association (CCFA). All rights reserved.

Though Li & Fung Research Centre and CCFA endeavor to have information presented in this document as accurate and updated as possible, it accepts no responsibility for any error, omission or misrepresentation. Li & Fung Research Centre, CCFA and/or their associates accept no responsibility for any direct, indirect or consequential loss that may arise from the use of information contained in this document. Reproduction or redistribution of this material without Li & Fung Research Centre and CCFA’s prior written consent is prohibited.