dissecting hotel sourcing – a well managed process · 1 dissecting hotel sourcing – a well...

TRANSCRIPT

1 1

Dissecting Hotel Sourcing – A Well Managed Process GBTA Boston July 23, 2012

Presented by: Carol Ann Salcito, CCTE President Management Alternatives, Inc. 203-849-9137 [email protected] www.mgmtalternatives.com

Jan D. Freitag

SVP STR

615-824-8664 [email protected] www.str.com

2

US Lodging Overview

Jan D. Freitag

Senior Vice President

3

www.hotelnewsnow.com

Click on “Hotel Data Presentations”

4

Agenda

• Total US Review

• Scales

• Segmentation

• 2012 / 2013 Forecast

5

Supply / Demand Drive Results. Pricing Power Is Back (?)

% Change Room Supply* 727 mm 0.3% Room Demand* 430 mm 3.5% Occupancy 59% 3.2% A.D.R. $104 4.2% RevPAR $62 7.5% Room Revenue* $45 bn 7.9%

YTD May 2012, Total US Results

* All Time High

6

YTD May 2012: Highest Demand - EVER (430 Million Rooms Sold)

7

-10

-5

0

5

1990 2000 2010

Demand ADR

ADR Rebound Trajectory Flattens Out (Too?) Early

-6.9%

-4.7%

-0.9%

-4.6%

-0.2%

-8.7%

4.0%

*Total US, ADR & Demand % Change, 12 MMA 1990 – 5/2012

8

ADR Discounting at Twice The Speed of ADR Increases

95

100

105

110

2008 2009 2010 2011

*Total US, ADR $, 12 MMA 2007 - 2011

Apr ‘10

$97

Sept ‘08

$108

Dec ‘11

$102

+4.6%

-10%

19 Months

19 Months

9

Chain Scale Review

10

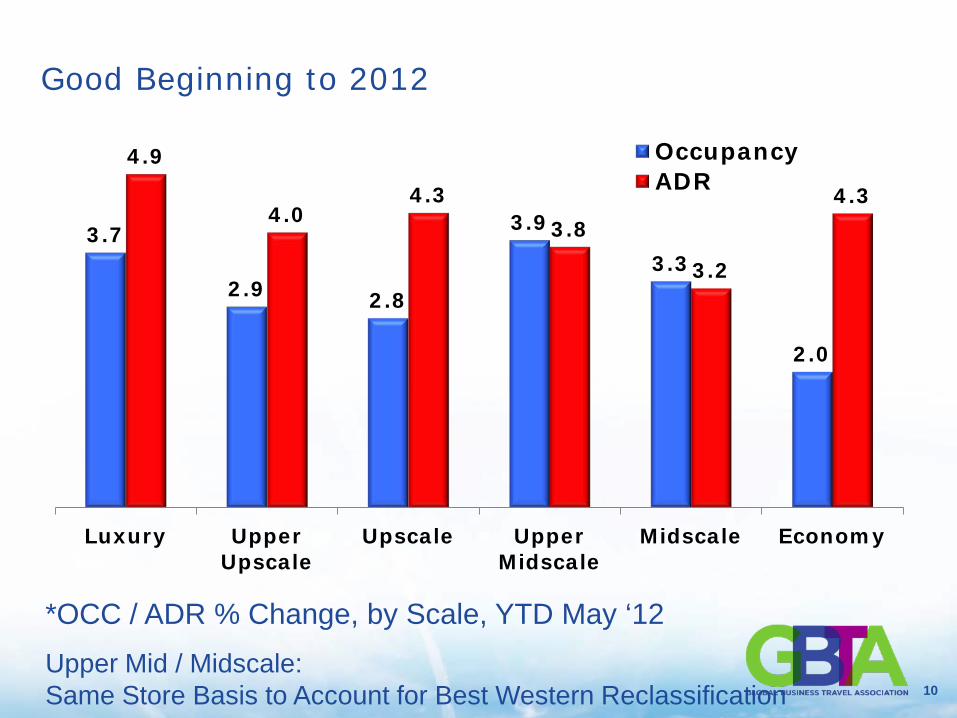

Good Beginning to 2012

3.7

2.9 2.8

3.9

3.3

2.0

4.9

4.0 4.3

3.8

3.2

4.3

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy

Occupancy ADR

*OCC / ADR % Change, by Scale, YTD May ‘12 Upper Mid / Midscale: Same Store Basis to Account for Best Western Reclassification

11

Upper End Sells 7 out of 10 Rooms Every Night 72.5

70.5 69.6

65.6

59.0 57.0

72.1 70.1 70.3

62.2

54.3 53.9

Luxury Upper Upscale

Upscale Upper Midscale*

Midscale* Economy

2007 12 Months end 5/12

*Absolute OCC %, by Scale, YE 2007 & 12 Months ending 5/12 Upper Mid / Midscale: Same Store Basis to Account for Best Western Reclassification

12

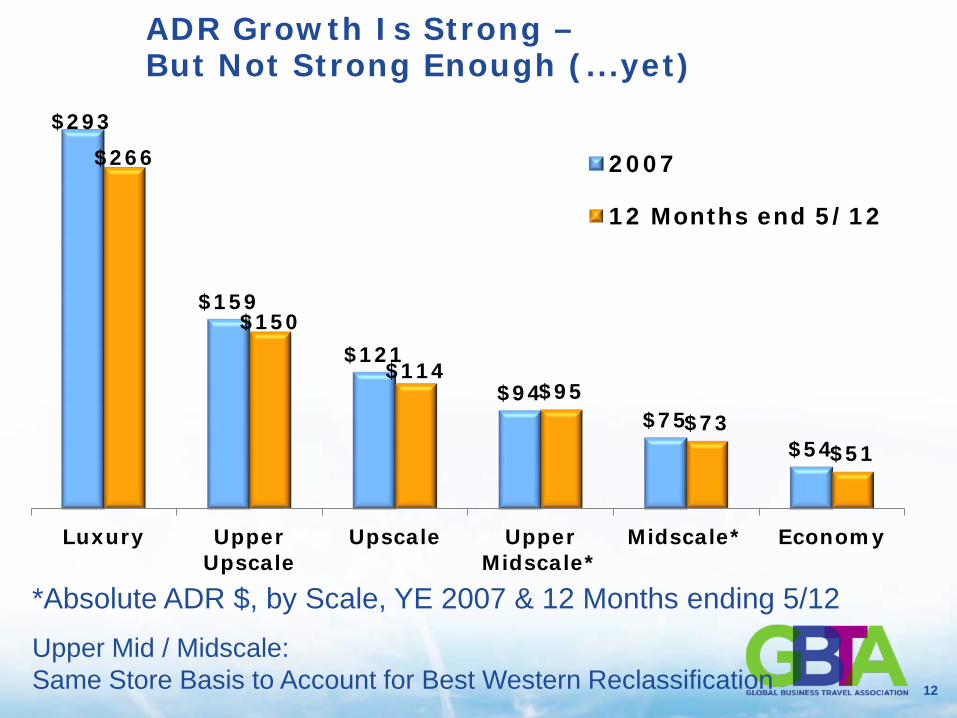

ADR Growth Is Strong – But Not Strong Enough (...yet)

$293

$159

$121

$94 $75

$54

$266

$150

$114 $95

$73 $51

Luxury Upper Upscale

Upscale Upper Midscale*

Midscale* Economy

2007

12 Months end 5/12

*Absolute ADR $, by Scale, YE 2007 & 12 Months ending 5/12 Upper Mid / Midscale: Same Store Basis to Account for Best Western Reclassification

13

Segmentation Review

14

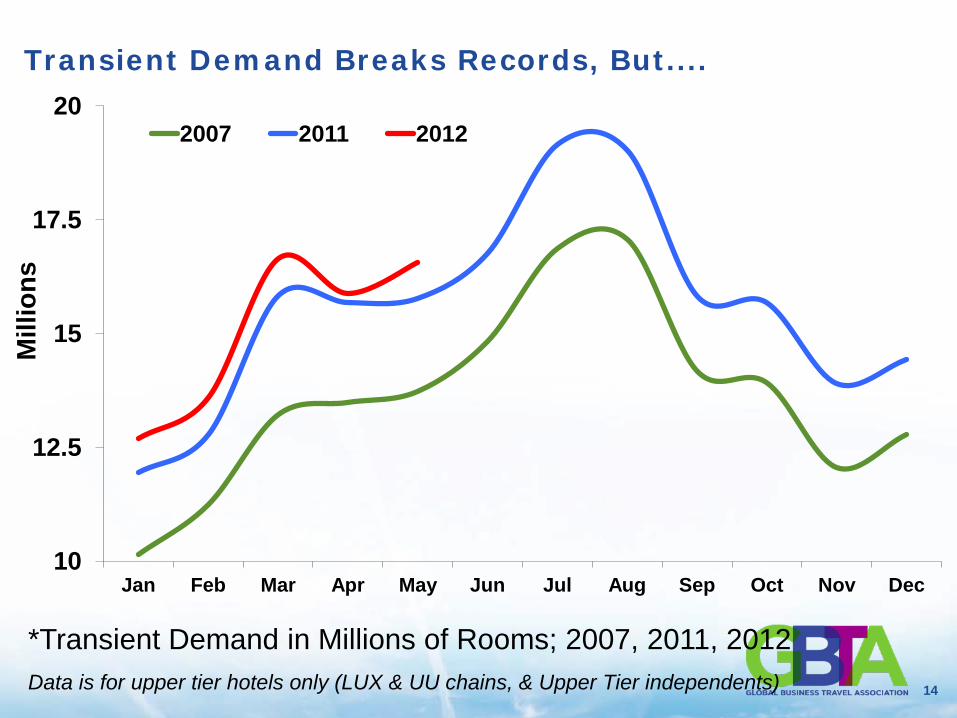

Transient Demand Breaks Records, But....

10

12.5

15

17.5

20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2011 2012

*Transient Demand in Millions of Rooms; 2007, 2011, 2012 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

Mill

ions

15

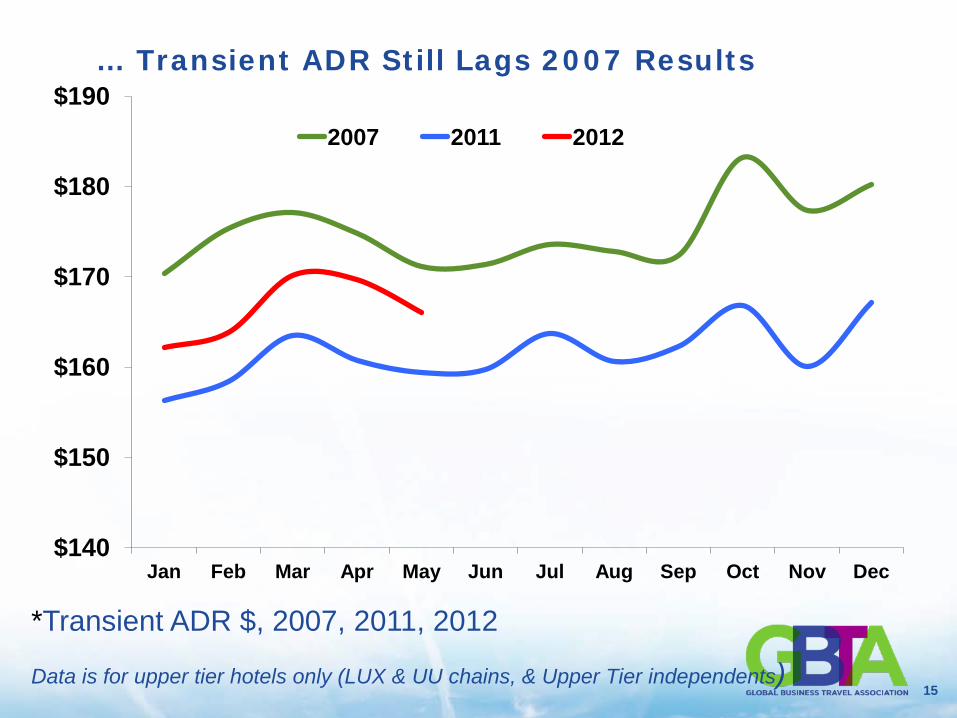

… Transient ADR Still Lags 2007 Results

$140

$150

$160

$170

$180

$190

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2011 2012

*Transient ADR $, 2007, 2011, 2012

Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

16

Group Demand Has Not Changed Over Time, But…

4

6

8

10

12

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mill

ions

2007 2011 2012

*Group Demand in Millions of Rooms, 2007, 2011, 2012 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

17

… Group ADRs Still Depressed (& Could Dampen Future Absolute ADRs)

$130

$140

$150

$160

$170

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 2011 2012

*Group ADR $, 2008, 2011, 2012 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

18

Forecast 2012 / 2013

19

Total United States Forecast 2012 / 2013 Key Performance Indicator % Change

2012 Forecast

2013 Forecast

Supply 0.5% 1.1%

Demand 2.0% 1.8%

Occupancy 1.5% 0.7%

ADR 4.0% 4.6%

RevPAR 5.5% 5.4%

20

2012 Chain Scale Forecast

Chain Scale Occupancy

(% chg) ADR

(% chg) RevPAR (%chg)

Luxury +2.6% +5.1% +7.9% Upper Upscale +1.5% +4.2% +5.7%

Upscale +2.3% +4.6% +7.1%

Upper Midscale +1.4% +4.0% +5.5% Midscale +2.8% +1.4% +4.3% Economy +1.4% +3.1% +4.5%

Independent +0.5% +3.5% +4.0% Total United States 1.5% 4.0% 5.5%

21 21

Best in Class Sourcing Strategy, Formation and Data Analysis Carol Ann Salcito, CCTE

22

23

Topics • Sourcing Strategy Simplified

• Hotel Data

• Data-driven Insights

• Chain Wide Deals

• Travel Policy & Negotiations • Savings & Reporting Methods • Compliance & Performance Tracking • Meetings & Events Management

24

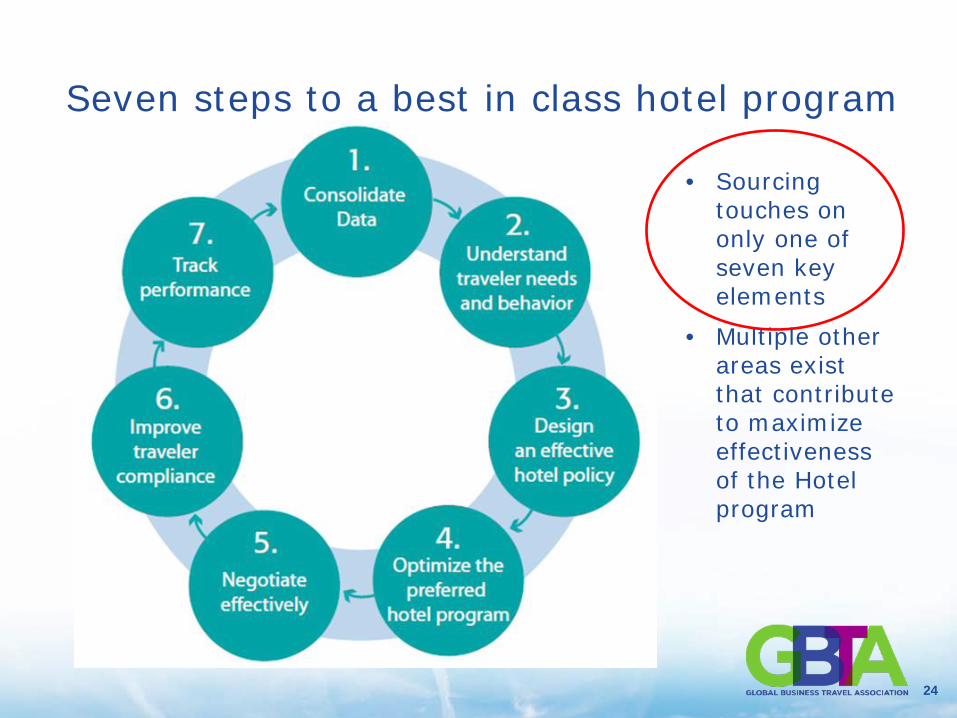

Seven steps to a best in class hotel program

• Sourcing touches on only one of seven key elements

• Multiple other areas exist that contribute to maximize effectiveness of the Hotel program

25

Best in Class Approaches for Navigating 2012 RFP Season

•Consolidate all data available (agency, charge card, expense system, supplier data)

•Focus on bids in top markets

•Benchmark for competitiveness

•Analyze total cost of stay

•Avoid program dilution caused by choosing too many preferred hotels

•Audit frequently

•Communicate purposefully around greatest opportunities.

•Manage program throughout the year

“Don’t let your hotel program sit on the shelf”

26

Typical sourcing timeline

27

Goal: Maximize convenience and savings, subject to the Frame

• Framing the “should cost” • The Framework is: ‒ Travel Policy

‒ LOCATION

‒ Convenience

‒ Tier

‒ Market

‒ Current Workload

‒ Company Culture for change (traveler and management)

‒ Supplier relationships

28

Hotel Data

29

Sources of Hotel data

• TMC Bookings • charge Cards • Buyer’s preferred program rates • Suppliers - but data varies wildly • Automated Expense Reporting Tools are best… ‒ But require adjustment - entry filters

‒ Even with corporate card feed!

• Manually-entered expense reports are unreliable • E-folio data may be more than time permits!

30

Data-driven Insights

31

Volume Leverage

• You know each market’s room nights

‒ Realistic and actionable opportunity for bidders

• Becomes a much more practical basis for negotiations

• Can show realistic available room nights to each brand and chain by rolling up markets

‒ Cities, metro areas, states, regions and countries – all from bottom-up detail

32 32

Optimizing Hotel Spend: Travel Policy & Negotiations

33

“Surprising how quickly we wrapped up negotiations after I ate that liverwurst and onion sandwich for lunch”

34

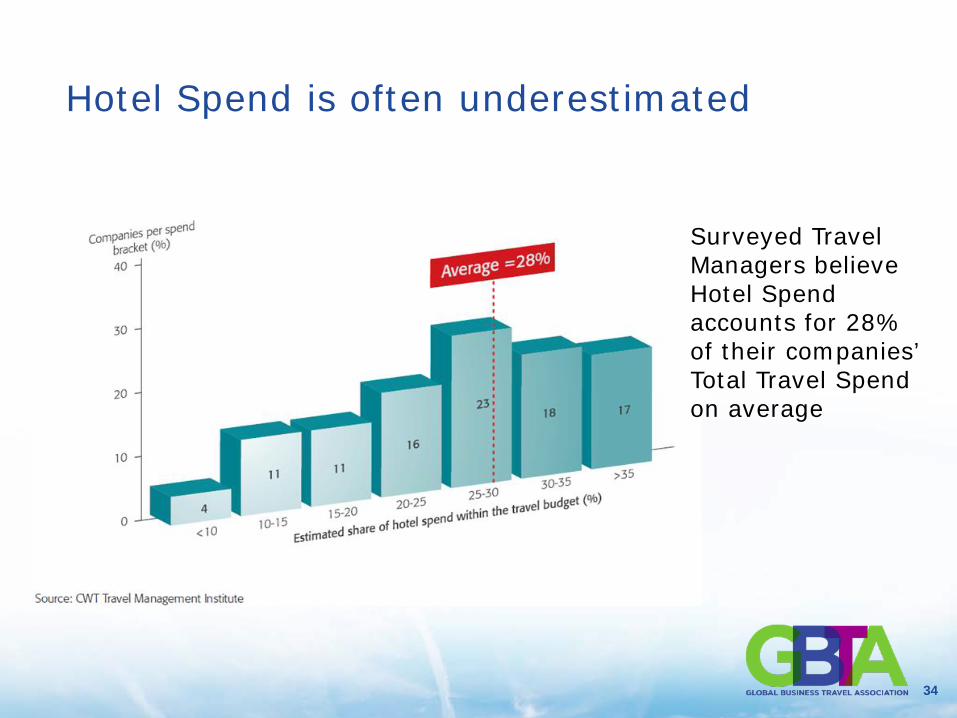

Hotel Spend is often underestimated

Surveyed Travel Managers believe Hotel Spend accounts for 28% of their companies’ Total Travel Spend on average

35

Hotel spend represents an avg of 39% of total travel spend

36

Source: CWT Travel Management Institute

Based on transaction data

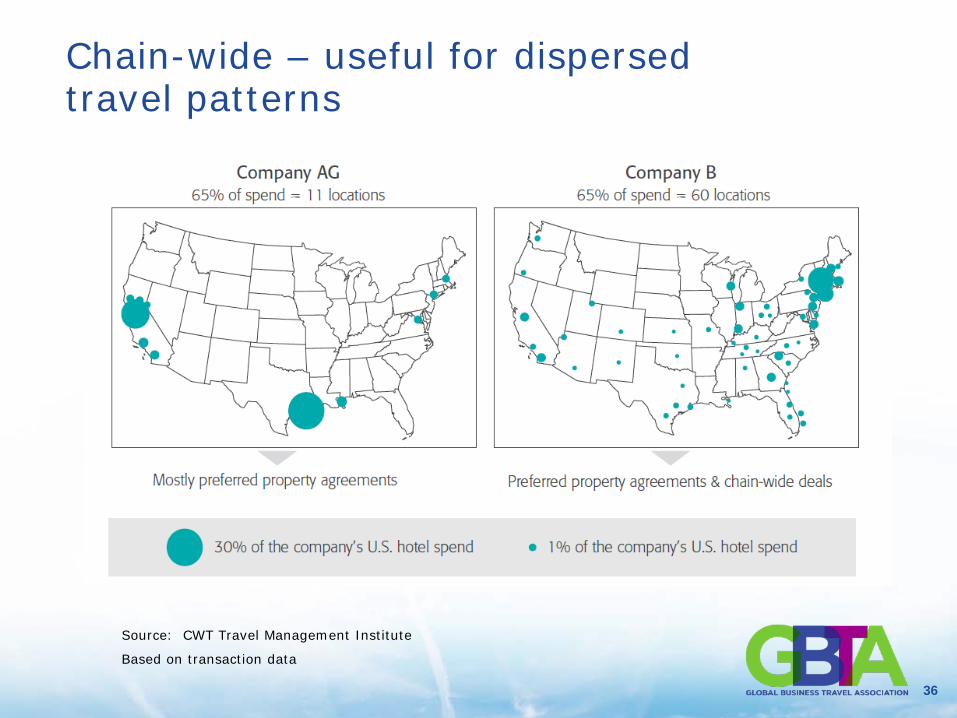

Chain-wide – useful for dispersed travel patterns

37

Key: High/Easy Medium Low / Difficult

What are the negotiation decision points?

Decision Point Impact Ease to Implement Accessibility

Volume at hotel

Year-over-year

Amenity inclusions

City volumes

Competitor benchmark

Relationship

Market conditions

Length of stay

Arrival pattern

Advanced booking

-

38

What is the best value?

Hotel A Hotel B

$182 $180

$0 $0

$15 $15

$0 $12

$165 $155

39 39

Measurements Savings and Reporting Methods

40

Testing the Value of Measuring and Reporting Savings

• Credible (can be audited, pass the CFO test) • Relevant (to company culture and in the right

language) • Predictable (for budgets and forecasts) • Accountable (linked to specific efforts)

41

Which Rates for Benchmarks?

Which undiscounted rate? • Published or Best Available (BAR)

‒ BAR gets a better grade from CFOs

Which rate used by travelers?

• Negotiated* • Booked (ABR) • Paid

*(a.k.a. corporate or program)

CFO’s Rank Low

OK

Best

TM’s Rank

Low

OK

Best

42 42

What is Happening? Traveler Compliance & Performance Tracking

43

Understand why travelers book out of policy is key to improving compliance

44

Actions to Improve Compliance

• Publish the program to web directory and communicate

• Implement clear mandate policies

• Check online booking tool configuration

• Require air w/hotel booking

• Empower TMC to enforce compliance

• Investigate reasons for non-compliance reasons and follow-up

• Explain the stakes

45

FUTURE

GBTA SOURCING WORKSHOPS

• Air Sourcing

– October 9, 2012 – Denver, Colorado

• Go “Beyond” Hotel Sourcing

– November 14, 2012 – Scottsdale, Arizona

46

Don’t Forget! We Want to Hear From You!

Please take a moment now to complete an evaluation.

Go Green! Complete your evaluation from the mobile app or http://m.gbta.org.

Paper surveys can be turned in to the

GBTA room volunteer upon exit.