disruptive m&a how to deal with ever-changing …...technology shifts decision relies on...

TRANSCRIPT

Disruptive M&AHow to deal with ever-changing technologies?

Disruptive M&A | Private and confidential© 2018. For information, contact Deloitte China. 2

Disruption overview

3Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Mobile phone

users

We are living in an era with significant improvement in technology

The world is changing quickly

Source: Statista, Cable UK, company websites, Deloitte analysis

Internet users

Average internet

speed

Annual e-commerce

spend

Computing costs

(cost per GFLOPS)

Storage costs

(per GB of data)

91,000kbps

USD 2.84 trillion

USD 0.03

(2017)

USD 0.02

4,570M

3,900M400M

318M

(1998)

55kbps

USD 222

USD 569

(1992)

USD 130

million (1999)

1990s 2018

28.0

22.0

18.0

14.0

12.0

7.0

4.0

4.0

3.0

3.0

1.0

iPod

YouTube

Pokemon

Telephone

0.1

Airline

Automobile

TV

Electricity

ATM

Credit Card

Computer

Cell phone

Internet

65.0

62.0

50.0

46.0

Time required to reach 50 million users (years)

4Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Non-tech Chinese buyers are more interested in tech assets and willing to enter into larger deals

Technology assets are getting more popular

41% 47%36%

51% 53%

59% 53%64%

49% 47%

2019 LTM2017

51.8

20182015 2016

54.1 54.051.6 59.5

Non-tech buyerTech buyer

636

731

0

200

400

600

800

1,000

2019 LTM20172015 2016 2018

794

413

Average size of tech-related deals involving Chinese buyers (USD million)

Shares of tech-related deals from Chinese buyers, by value

Note: (1) Announced deals with size larger than USD 100m; (2) internet companies refers to those operating in internet/e-commerce field(3) 2019 LTM refers to April 2018 to March 2019Source: Mergermarket, Deloitte analysis

= Total deal size(USD billion)

5Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Chinese market Corporate Venturing is growing rapidly

Earlier stage investments are becoming more active

260

2018

12%

2015

160

57%

29%

12%

48%

39%

Europe

North America

Others

Asia

18%

18%

29%

11%

CAGR 15-18 (%)

Note: Referring to funding invested into companies headquartered in the region/countrySource: CBInsights, SCMP, Deloitte analysis

Venture capital and corporate venture capital activities by region (USD billion)

15%

85%

20%

80%

20182015

Corporate Venturing

Venture Capital

Venture capital and corporate venture capital activities in China

6Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Chinese corporates are more likely to acquire new business capabilities than market shares

Chinese corporates are more open to M&As with different purposes

140 135148

159

2016 20182015 2017

Number of Top 500 Chinese Enterprises that engaged in M&A

59% 54% 50% 49%

41% 46% 50% 51%

20182015 2016 2017

Purpose of Acquisition

Acquire capabilities Acquire shares

Gaming

Payment, fintech and cloud services

Robotics and Automation

Consumer electronic

Source: Chinese Enterprise Confederation, Mergermarket, Bain, Deloitte analysis

7Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

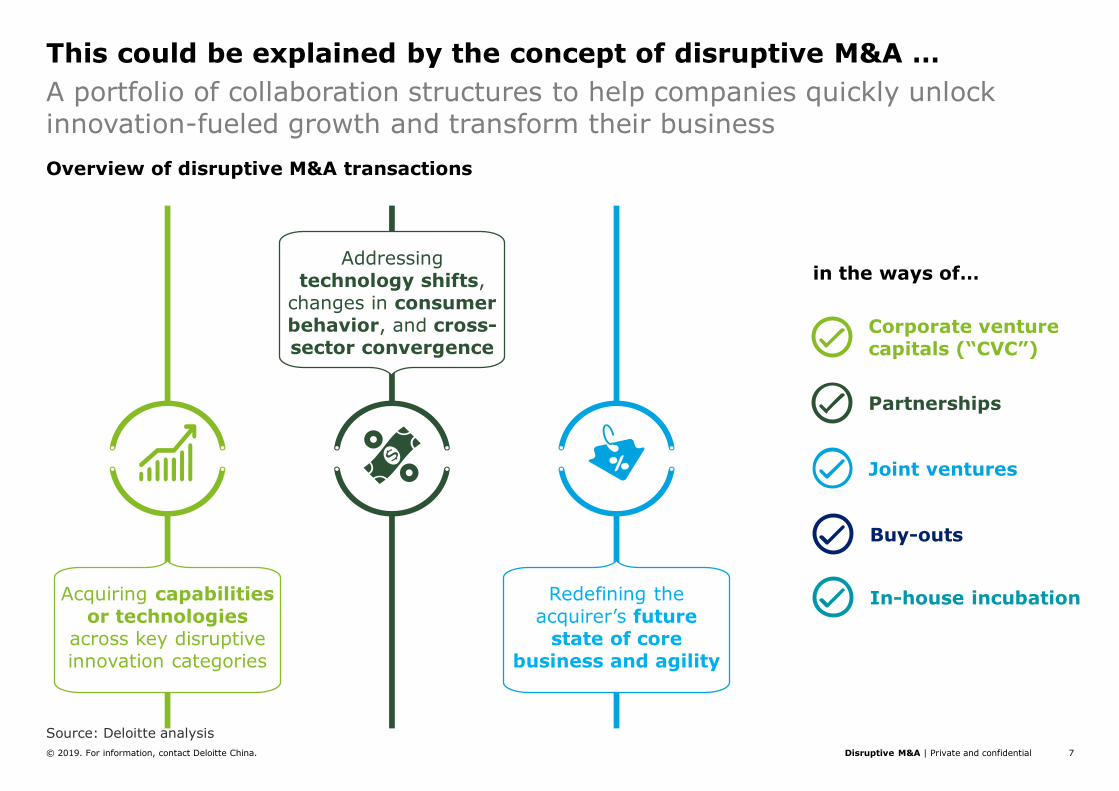

A portfolio of collaboration structures to help companies quickly unlock innovation-fueled growth and transform their business

This could be explained by the concept of disruptive M&A …

in the ways of…

Acquiring capabilitiesor technologies

across key disruptive innovation categories

Corporate venture capitals (“CVC”)

Partnerships

Joint ventures

Buy-outs

Redefining the acquirer’s future

state of core business and agility

Overview of disruptive M&A transactions

In-house incubation

Addressing technology shifts,

changes in consumer behavior, and cross-sector convergence

Source: Deloitte analysis

8Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Helping acquirers to accelerate growth at the convergence of physical and digital world in different angles

…which could be used to capture new opportunities

Improve the coreMove into an

adjacent marketCreate an entirely

new business

New product to

enhance

product

offerings

Acquire new

product

New

capabilities

such as

analytics,

digital etc. to

enhance core

business

Acquire new

capabilities

Acquiring a

new player that

is disrupting

the market but

not yet at scale

Acquire the

disruptor

Gaining entry

to adjacent

market or

category

through M&A

Disrupt

adjacent

market

Gaining

advantage

through sector

convergence

Convergence

opportunity

Transforming

the industry

and becoming

a disruptor

through

acquisition

Become a

disruptor

Common goals to be achieved by disruptive M&A

Source: Deloitte analysis

9Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

As a fundamental part of innovation strategy, providing an important conduit into external innovation ecosystem

Disruption is becoming core of global firms’ innovation strategy

of the S&P

Global 1200

companies

engaged in

disruptive

M&A/VC

Investment

during 2015-17

30%

of the M&A

deals

announced by

the S&P Global

1200

companies

during 2015-17

is related to

disruption

17%

Deal values (2015-17)

Deal volumes

(2015-17)

3,334 deals

21%

79%

USD 386 billion

76%

24%

Total S&P Global 1200 companies disruptive M&A and CVC activity

(2015-17)

CVC M&A

Source: Deloitte analysis

10Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

In-house incubation/development is also observed when building up new capabilities

Similar disruption trend is also observed in China

Improve the coreMove into an

adjacent marketCreate an entirely

new business

New product to

strengthen

current process

Acquire new

product

New functions

to enhance

core business

and stay on

par during

competition

Develop new

capabilities

Acquiring a

growing new

players that

are disrupting

the market

Acquire the

disruptor

To gain entry

to adjacent

market or

category

through M&A

Confidential

Disrupt

adjacent

market

To gain

advantage

through sector

convergence

Convergence

opportunity

To incubate

disruptors and

capture their

future potential

at early stage

Corporate

ventures

Advanced robotics

Cloud payment solutions to defend from

Alipay / WeChat

Traditional carmaker

investing on EVs

Traditional Mobility

Manufacturers partnering with hydrogen tank

producer

Tapping to O2O future retailing opportunities

Actively investing in new business

concepts

Common goals to be achieved by Chinese disruptive M&A practitioners

Source: Deloitte analysis

Disruptive M&A | Private and confidential© 2018. For information, contact Deloitte China. 11

How to be disruptive

12Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

TECHNOLOGY SHIFTS

Decision relies on analyzing technology and consumer behavior shifts, with a view toward the future landscape of their industry

Overview on strategic evaluation framework

Artificial Intelligence

IoT Robotics

Digital Fintech Big Data

Peers Over Corporate

Collaboration over

competition

Accessor over ownership

Future of consumer

Future of mobility

Future of finance

Future of manufacturing

Future of health

STRATEGIC CHOICES TO CAPTURE INNOVATION LED GROWTH

INVEST (Governance) Develop corporate venturing as a core competency to allow the organization to uncover, incubate,

and invest in new growth opportunities. This could also lead to financial gains and sign-off opportunities

COLLABORATE (Friends)Consider close collaboration with a range of eco-system partners—ranging from start-ups to cross-sector

corporates to co-innovate and develop new market offerings

BUY (Strategy)Develop a dedicated Innovation M&A strategy to acquire capabilities, products, and technologies that can unlock new sources of growth and

revenue. Cultural adoption will be a key driver for the successful integration of such deals

CONSUMER BEHAVIOR SHIFTS CONVERGENCE ACROSS SECTORS

13Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Accession over

ownership

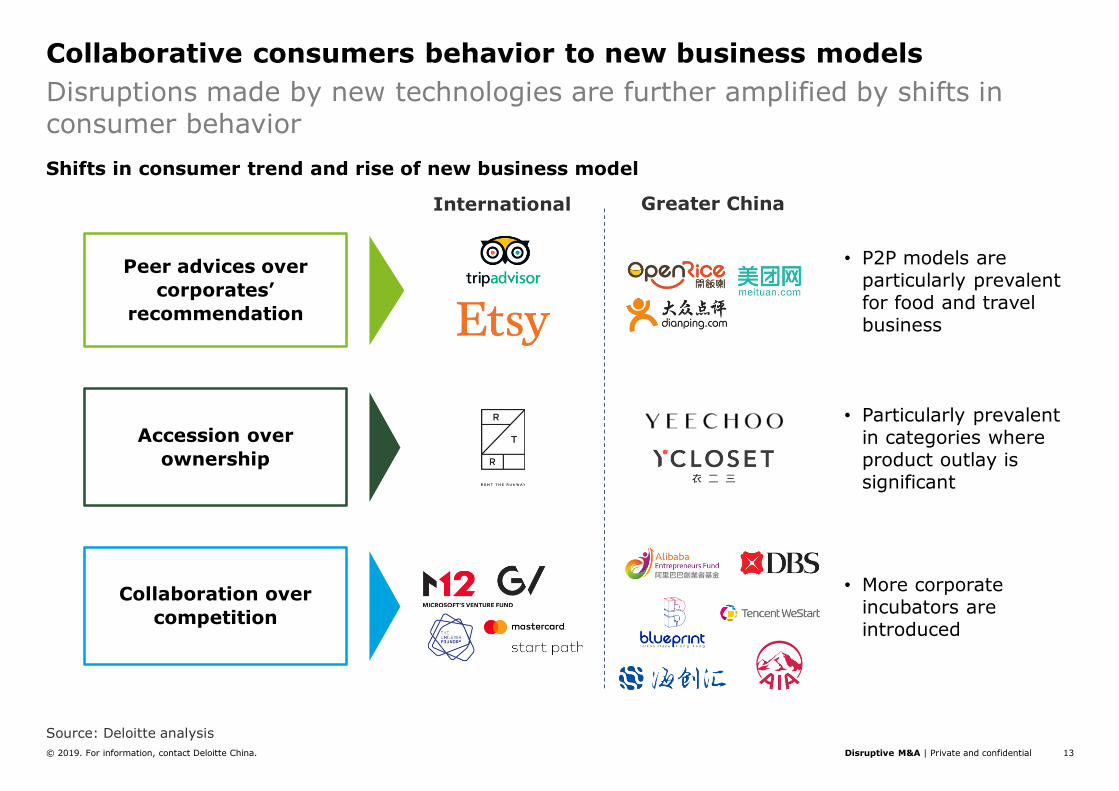

Disruptions made by new technologies are further amplified by shifts in consumer behavior

Collaborative consumers behavior to new business models

Peer advices over

corporates’

recommendation

Collaboration over

competition

• P2P models are particularly prevalent for food and travel business

• Particularly prevalent in categories where product outlay is significant

Shifts in consumer trend and rise of new business model

International Greater China

• More corporate incubators are introduced

Source: Deloitte analysis

14Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Established players can now compete on new markets due to disruptions made by new acquisitions

Sector convergence to bring in new competitions

Mobility

Automotive

Technology

Finance Real estate

Consumer

electronics

Manufacturing

Energy

Advanced

manufacture

Real

estate

Robotics

Source: Deloitte analysis

Examples of players engaging in new economies

Consumers

FinanceTech

Technology

SocialRetail

Food

Sportswear

Consumer

Health

Finance

Technology

Real estate

Social

Finance

Service

Automotive

Consumer

electronicsTechnology

BanksSC

Digital

Disruptive M&A | Private and confidential© 2018. For information, contact Deloitte China. 15

Case studies

16Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Notable disruptive M&A cases are selected to illustrate business development in multiple latitudes

Case study selection

Disruptive M&A Direction

Market expansion Product innovation

Double disruption

• To tackle adjacent new energy vehicle market using core technologies

• To invest in innovative and capable players; explore transformation opportunities under existing business model

• To leverage disruptors’ solution to enhance core business performance

• To further disrupt the market with large scale consolidation

Selected disruptive M&A case studies to be covered

1 2

3

Confidential

17Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

To identify and enter disrupting adjacent market using core technologies

Case study (1) – Confidential

• Subsidiary of a large foreign SOE

• Holders of several leading technologies in the hydrogen mobility industry

• Partnering with large traditional mobility (auto / truck / train)

• Exploring potential of various adjacent markets

• Identifying suitable partners in shortlisted to develop China production JV

What has been done?Who? How to disrupt?

Source: Company websites, Deloitte analysis

MobilityTech?

• Own a key piece of the technology for a future solution (5 years from mass adoption)

• Ability to enter new energy businesses – as manufacturer; component supplier and infrastructure

Confidential

18Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

!

Invest in innovative players and transform/disrupt existing business model; integration needs to be carefully executed to achieve desired synergies

Case study (2) – Deloitte

Source: Deloitte

Services

What has been done?Who? Major challenges

• Largest professional service firms globally

• More challenges from intense competition and sophisticated customer demand

• Services are on standalone basis which may create fluctuation in business planning

• Actively exploring new opportunities and offerings to diversify product portfolio

• Formed a strategic alliance with purchase rights

• Commercialise new products offerings based on Big Data

• New business models / offerings expected to be launched

− Subscription services

− Differentiated products

− Enhanced efficient delivery

A nearing commercialization

data firm

• Amazing concepts and initial results promising, but longer than expected to commercialization

• Limited time before delivering results

• Internal tensions on fit between companies

• Culture clash -conservative vs brash

• Corporate love

• Imperfect Governance Model`

19Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

To leverage disruptors’ solution to indirectly improve core business; further disruption could to be achieved through consolidation

Case study (3) – BMW

• Leading car producer in the world

• Global footprint with stable business

• Investments and development on cutting edge technologies in accessing mobility ecosystem enablers to shape global mobility

MobilityAutos

• Identification of market expansion opportunities in the parking market

• Delivered the industry’s first fully-integrated in-car mobile parking solution

• Enhanced parking experience and thus encouraging more driving activities

What has been done?Who? What’s next?

Source: Company websites

• Further disruption by joining hands with Daimler AG

• Targets to build most attractive, most comprehensive mobility solution for a better life in our connected world

Disruptive M&A | Private and confidential© 2018. For information, contact Deloitte China. 20

What can you do?

21Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Accelerated by developing capability to strengthen talents, processes and technologies, inorganically through disruptive M&A

Key questions in the disruptive journey

Do these options include investment, partnership, or acquisition components?

How do we identify and assess the available various inorganic growth options?

How should we approach and execute this ideal differently from past transactions?

6

5

4Which forces are most likely to affect my industry?

1

Do we have an adequate understanding of these forces?

2

What options do we have to get ahead of these forces?

3

Source: Deloitte analysis

22Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Three key elements to support corporates to create a “controlled disruptions” environment

Making disruption a success

Controlleddisruption

Own the customer

• Collaborative customers behavior requires more effort on servicing

• Customer stickiness will be key advantage on future competition

• Business models is thus expecting to shift from product to customer-centric

Execute diligently

• More complex deal execution due to significant difference in operations

• Smooth transition and integration will be more important on realizing value of disruption

• Monitoring and evaluation framework is also needed to support and trace synergies realization

Monitor opportunities

• More common to encounter opportunities on acquiring new capabilities due to technological advancement

• Screening, identifying and managing the right targets systematically will be crucial for future success

Steps to manage disruption

Source: Deloitte analysis

23Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

To define corporate’s vision and visualize an ecosystem that can capture target customers demand

From “owning the product” to “owning the customers”

Big Data

New retail

mi.com

MIUI

Mi Home

ProductsInternetservices

Big Data

Big Data

Communication Music

App store

Theme shop Browser

Virtual reality

Ninebot

Luggage

Smartphone

Smartlight

• Disruptive business model are more consumer-centric rather than product-specific

− Using different products to enhance experiences and user stickiness

• Taking Xiaomi as an example, the company has developed a ecosystem linked up by big data and user interfaces:

− Products to capture consumers day-to-day usage scenarios

− Services to address consumption behavior

− Retail network to bridge online and offline service gaps

Xiaomi’s example to own customers

Source: Company disclosure, Deloitte analysis

24Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

To develop a complete venturing lifecycle, create and capture value in innovative ecosystem

Monitor and execute through venture mechanism

Corporates

5. Design venturing options

Design and evaluate your immediate and long-term venturing options and model the business case

4. Identify, validate and connect

Employ data-driven search and proven methodology to identify, validate and connect to target’s leadership

6. Execution

Structure the deal, determine partnership principles, due diligence, legal contracting, and deal close

1. Develop venturing & M&A growth strategy

Reason from your assets & capabilities, identify growth domains and develop your strategy

2. Position for venturing

Position your venturing and innovation instruments as a strategic portfolio with alignment and collaboration between teams

3. Explore innovative growth domains

Understand the impact of new technologies, as well as dynamics and drivers in relevant ecosystems

Source: Deloitte analysis

25Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

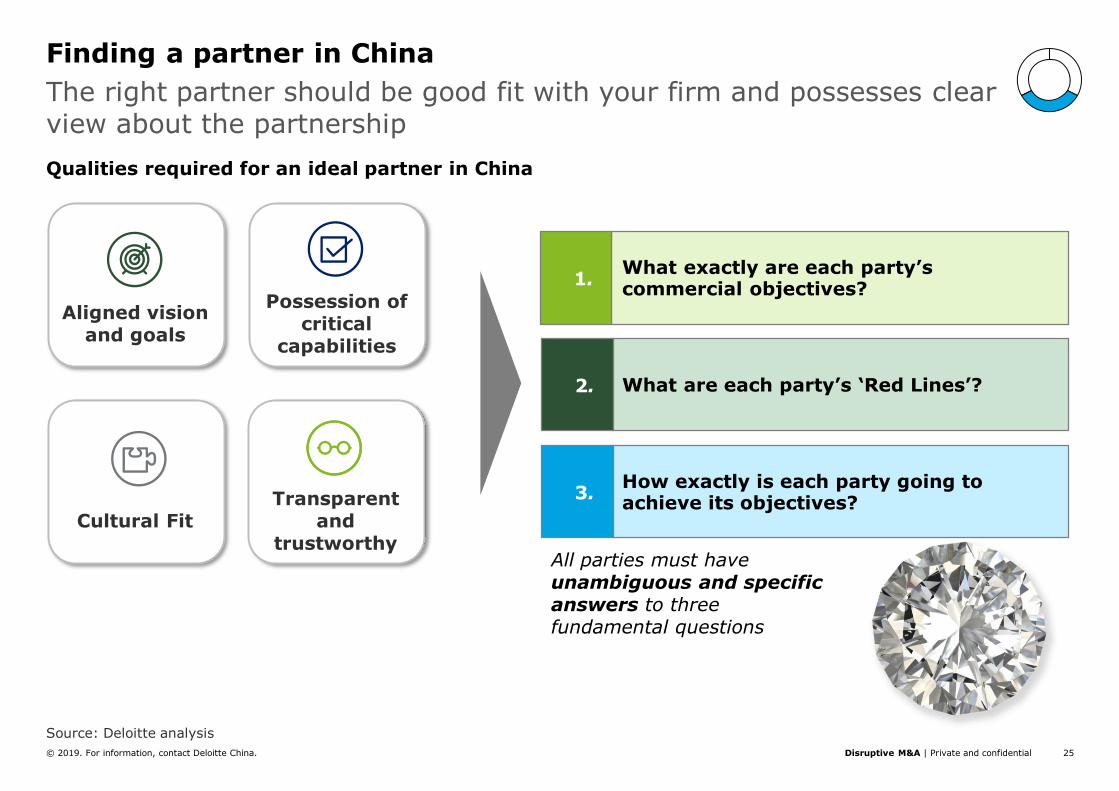

The right partner should be good fit with your firm and possesses clear view about the partnership

Finding a partner in China

Aligned vision and goals

Possession of critical

capabilities

Cultural FitTransparent

and trustworthy

What exactly are each party’s commercial objectives?

1.

What are each party’s ‘Red Lines’?2.

How exactly is each party going to achieve its objectives?

3.

Qualities required for an ideal partner in China

All parties must have unambiguous and specific answers to three fundamental questions

Source: Deloitte analysis

26Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Be upfront and to the point right from the beginning. If the deal premises do not exist, let it fail – fast!

Disruptive M&A / Partnering in China

Scope Business Define success ControlPartner

contribution

Exclusivity Compliance GovernanceNegotiation

timeline

Product & operationalfocus?

Revenue and margin aspirations? Other

definition?

Control needed over IPR, management, consolidations, etc.

What are each partner bringing to

the table?

Exclusivity (geography, product, other)? Negotiation?

Which laws and standards apply?

Organization and entity structures? Board Structures?

Controls?

When, what needs to be completed by

whom?

Basic principles of forming a Partnership in China

Source: Deloitte analysis

27Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Deloitte has also produced various materials to guide you further on this topic

Future of the Deal: Winds of

change

Disruptive M&A: Are you

ready to define your future?

Fueling growth through

innovation: Deloitte M&A

Index

Fintech acquisitions:

Integrations are a different

adventure

Insurance: Life Sciences and

Health Care

Digital Transformation in Oil,

Gas & Chemicals

Retail Banking: Digital

Transformation Network

Retail & Consumer Products:

Digital Transformation

Network

Accelerating Digital

Ecosystem Development

through Strategic Alliances

Automotive: Digital

Transformation Network

Insurance: Digital

Transformation Network

Disruptive M&A | Private and confidential© 2018. For information, contact Deloitte China. 28

Next steps – panel session

29Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

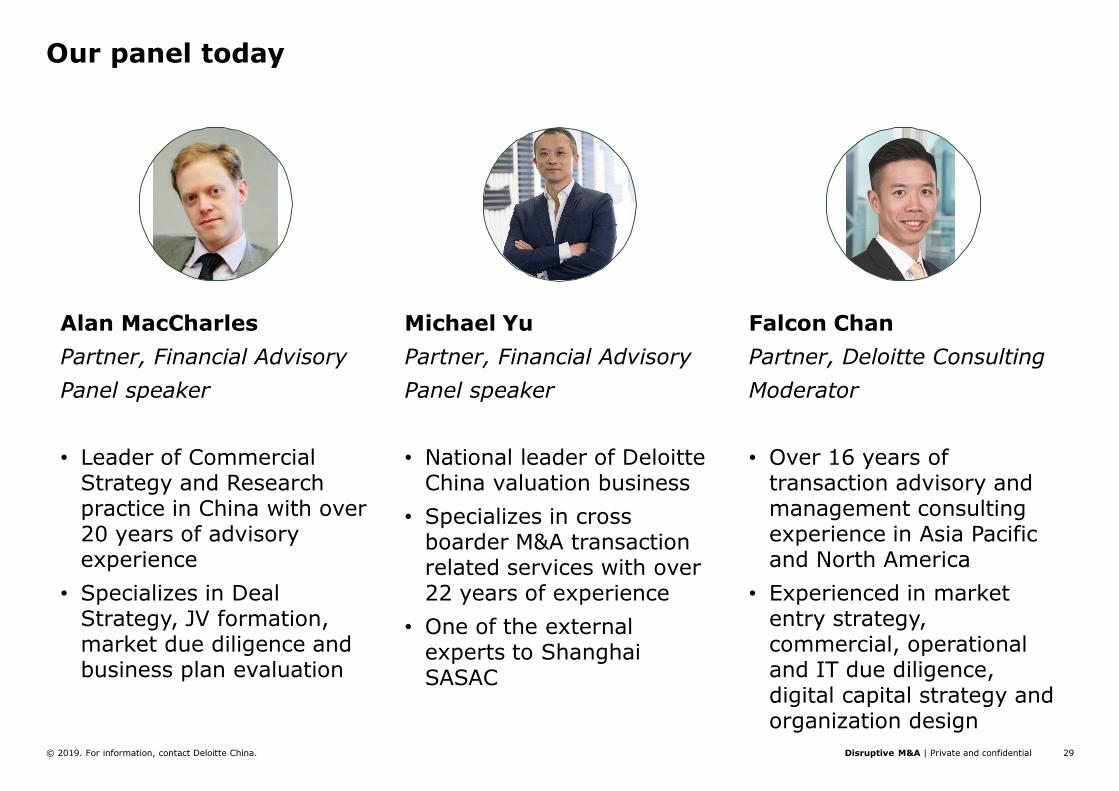

Our panel today

Alan MacCharles

Partner, Financial Advisory

Panel speaker

• Leader of Commercial Strategy and Research practice in China with over 20 years of advisory experience

• Specializes in Deal Strategy, JV formation, market due diligence and business plan evaluation

Michael Yu

Partner, Financial Advisory

Panel speaker

• National leader of Deloitte China valuation business

• Specializes in cross boarder M&A transaction related services with over 22 years of experience

• One of the external experts to Shanghai SASAC

Falcon Chan

Partner, Deloitte Consulting

Moderator

• Over 16 years of transaction advisory and management consulting experience in Asia Pacific and North America

• Experienced in market entry strategy, commercial, operational and IT due diligence, digital capital strategy and organization design

About Deloitte Global Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about to learn more about our global network of member firms.

Deloitte provides audit & assurance, consulting, financial advisory, risk advisory, tax and related services to public and private clients spanning multiple industries. Deloitte serves nearly 80 percent of the Fortune Global 500® companies through a globally connected network of member firms in more than 150 countries and territories bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges. To learn more about how Deloitte’s approximately 263,900 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

About Deloitte ChinaThe Deloitte brand first came to China in 1917 when a Deloitte office was opened in Shanghai. Now the Deloitte China network of firms, backed by the global Deloitte network, deliver a full range of audit & assurance, consulting, financial advisory, risk advisory and tax services to local, multinational and growth enterprise clients in China. We have considerable experience in China and have been a significant contributor to the development of China's accounting standards, taxation system and local professional accountants. To learn more about how Deloitte makes an impact that matters in the China marketplace, please connect with our Deloitte China social media platforms via www2.deloitte.com/cn/en/social-media.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively the “Deloitte Network”) is by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2018. For information, contact Deloitte China.

31Disruptive M&A | Private and confidential© 2019. For information, contact Deloitte China.

Corporates need to select “right” tools to fuel future business growth

Combination of technologies to deliver desired results

Artificial intelligence IoT Robotics

Digital Fintech Big data

The confluence of advances in deep-learning algorithms, chip manufacturing technologies and cognitive computing have spurred investments in AI which is

on the cusp of a revolution in applications in both the consumer and enterprise segments

The Internet of Things (IoT) is about making intelligent digitally-enabled and connected products. The falling costs of key infrastructure and the proliferation of

consumer and enterprise user applications have proven a catalyst

Significant advances in new materials, computing and battery power as well as the rapid growth in both industrial and consumer applications is stimulating

investment in robotics. These investments range from industrial automation and drones to service process automation

The digitization of industries is leading to the development of cross channel digital and social business models and investments in new segments such as E-

Commerce, On-Demand services and digital healthcare business models

The wide range of opportunities presented by Fintech means there has been significant growth in investment from non-financial service sectors such as

telecoms, software and media

Companies have been investing heavily to harness the potential of Big Data as advances in sensing applications provide practical business insights and

applications. In recent years the key areas of investments include cloud-based analytics, enterprise software, cyber-security risk and cognitive analytics