disclosures under basel iii · 2016-11-13 · disclosure on pillar 3 market discipline under basel...

TRANSCRIPT

2015

12/31/2015

Disclosures Under Basel III

Disclosure on Pillar 3 Market Discipline under Basel III 1

The Bank made the following detailed qualitative and quantitative disclosures in accordance with Pillar 3 Market Discipline as per Guidelines on Risk Based Capital Adequacy (RBCA) under Basel-III issued by Bangladesh Bank in 2014. The purpose of this report is to complement under Pillar 1 Minimum Capital Requirement (MCR) and Pillar 2 Supervisory Review Process (SRP) of Basel III. The following components have been disclosed hereunder as per the requirement of Risk Based Capital under Basel-III issued by Bangladesh Bank: a) Scope of Application b) Capital Structure c) Capital Adequacy d) Investment Risk e) Equities: Disclosures for Banking Book Positions f) Interest Rate Risk in the Banking Book (IRRBB) g) Market Risk h) Operational Risk i) Leverage Ratio j) Liquidity Ratio k) Remuneration These disclosures are intended for more transparent and more disciplined financial market where the participants can assess key information about the Bank's exposure in making economic decisions. A. SCOPE OF APPLICATION Qualitative Disclosure a) The name of the top corporate entity to which this framework applies: The Risk Based Capital Adequacy Framework applies to Modhumoti Bank Limited (MMBL) on ‘solo’ basis as there was no subsidiary as on the reporting date (December 31, 2015). b) Consistency and Validation: The quantitative disclosures are made on the basis of audited financial statements of the bank for the year ended December 31, 2015 prepared under relevant international accounting and financial reporting standards as adopted by the Institute of Chartered Accountants of Bangladesh (ICAB) and related circulars/instructions issued by Bangladesh Bank from time to time. c) Any restrictions, or other major impediments, on transfer of funds or regulatory capital to

subsidiaries: Not applicable for the Bank as there was no subsidiary of the Bank on the reporting date (December 31, 2015). However, the BRPD circular 05, dated 09 April 2005 and BRPD Circular No.02, dated, January 16, 2014 respectively regarding ‘Single Borrower Exposure Limit’ are being applied by the Bank in determining maximum amount of finance. Quantitative Disclosure

d) Aggregate amount of capital deficiencies: There was no capital deficiency in the financial year

2015 as there was no subsidiary of the Bank.

Pillar 3 Market Discipline

Disclosures on Risk Based Capital Adequacy (Basel III) for the year ended December 31, 2015

Disclosure on Pillar 3 Market Discipline under Basel III 2

B. CAPITAL STRUCTURE Qualitative Disclosures a) The regulatory capital under Basel-III is composed of i) Tier-1 (Going Concern Capital) and ii) Tier-

2 (Gone Concern Capital). Tier-1 Capital (Going Concern Capital) has two components of Tier 1 Capital which are Common Equity Tier 1 Capital and Additional Tier 1 Capital. It consists of highest quality capital items which are stable in nature and allows a bank to absorb losses on an ongoing basis. Common Equity Tier 1 Capital includes paid-up capital, statutory reserve, general reserve and retained earnings etc and Additional Tier 1 Capital will include perpetual bond or non-cumulative preference shares etc. Tier-2 Capital (Gone Concern Capital) lacks some of the characteristics of the going concern capital but also bears loss absorbing capacity to a certain extent. General provision on unclassified loans and advances, provision for Off-Balance Sheet items and revaluation reserve on government securities, fixed asset and equity instruments are part of Tier 2 capital. It is mentionable that revaluation reserve as of December 31, 2014 has to be phased out as per Basel III by 20% in 2015, 40% in 2016, 60% in 2017, 80% in 2018 and 100% in 2019. That means the bank cannot show revaluation reserve as capital from January 01, 2020. Compliance Status of MMBL as per Conditions for Maintaining Regulatory Capital: The Bank complied with all the requirement of regulatory capital as stipulated in the revised RBCA Guidelines by Bangladesh Bank as per following details:

Sln. Limits (Minima and Maxima)

Status of Compliance

Complied

()

Non-

complied ()

1 Common Equity Tier 1 of at least 4.5% of the total RWA

2 Tier 1 capital will be at least 6.0% of the total RWA

3 Minimum CRAR of 10% of the total RWA

4 Additional Tier 1 capital can be admitted maximum up to 1.5% of the total RWA or 33.33% of CET1, whichever is higher

5 Tier 2 capital can be admitted maximum up to 4.0% of the total RWA or 88.89% of CET1, whichever is higher

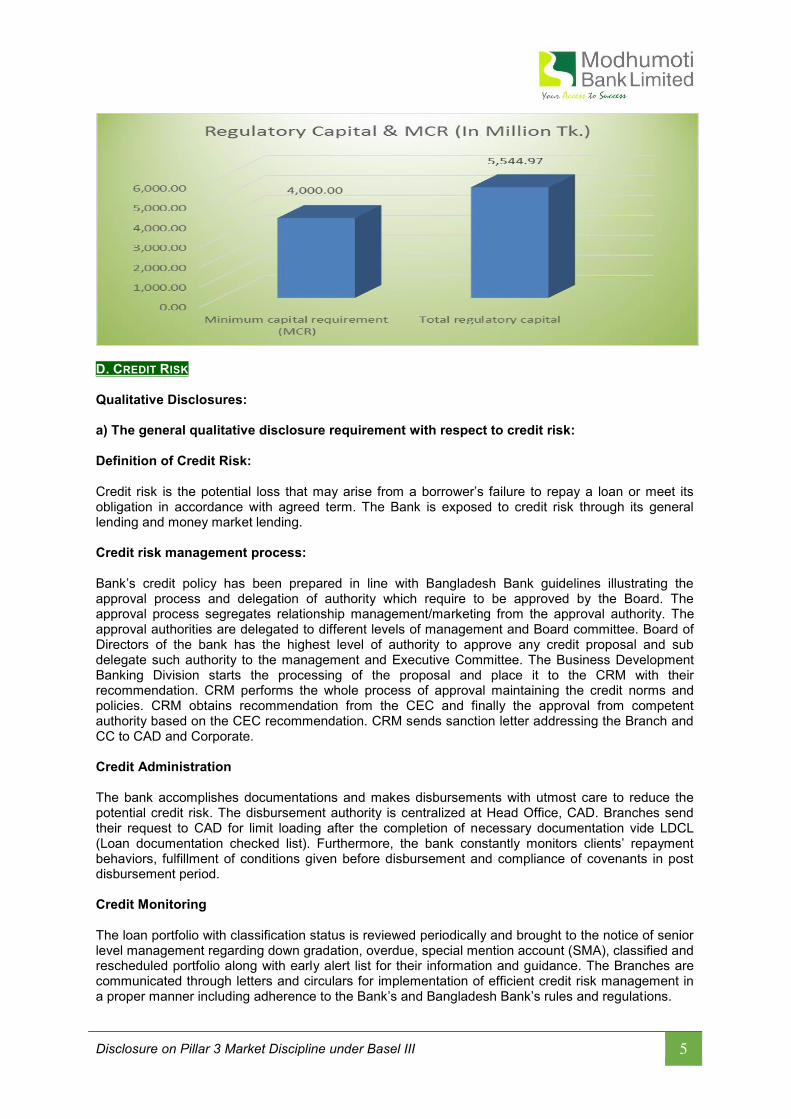

Quantitative Disclosures a) Regulatory capital of the Bank as of December 31, 2015 Tier-1 capital of the bank as of December 31, 2015 was Tk. 5,422.14 million which is 97.78% of total regulatory capital and rest 2.22% from Tier-2 capital. Tier-1 capital comprised 81.52% from paid up capital, 5.50% from statutory reserve and rest 10.77% from retained earnings of the Bank. Tier-2 capital is Tk.122.83 million which is 2.22% of total regulatory capital and the major contributors are general provision on loans and advances including Off-Balance sheet items.

Amount in Million Tk

Sln. Regulatory Capital 2015 2014

1 Tier-1 Capital (Going Concern Capital) (2+6) 5,422.14 4,883.21

2 Common Equity Tier 1 Capital (3+4+5) 5,422.14 4,883.21

3 Paid-up capital 4,520.00 4,520.00

4 Statutory reserve 304.82 110.65

5 Retained earnings 597.33 252.56

6 Additional Tier 1 Capital - -

Disclosure on Pillar 3 Market Discipline under Basel III 3

Sln. Regulatory Capital 2015 2014

7 Tier-2 Capital (Gone Concern Capital) (8+9-10) 122.83 66.1

8 General Provision 116 57.56

9 Revaluation Reserve as on December 31, 2014 (50% of Fixed Asset & Securities & 10% of Equities)

8.54 8.54

10 Regulatory Adjustment: Revaluation Reserve for Fixed Assets, Securities & Equity Securities 20%

1.71 -

11 Total regulatory capital (1+7) 5,544.97 4,949.31

C. CAPITAL ADEQUACY Qualitative Disclosures a) Approach to assess the adequacy of capital: The bank is presently following Standardized Approach for assessing and mitigating Credit Risk, Standardized Rule Based Approach for quantifying Market Risk and Basic Indicator Approach for Operational Risk to calculate Minimum Capital Requirement (MCR) under Pillar-I of Basel-III framework as per the guidelines of Bangladesh Bank. MMBL has been generating most of its incremental capital from retained profit and statutory reserve transfer etc. MMBL has a process for assessing its overall capital adequacy in relation to the Bank’s risk profile and a strategy for maintaining its capital levels. The process provides an assurance that the Bank has adequate capital to support all risks in its business. The Bank identifies, assesses and manages comprehensively all risks that it is exposed to through sound governance and control practices, robust risk management framework and an elaborate process for capital calculation and planning. The Bank has a structured management framework in the Internal Capital Adequacy Assessment Process (ICAAP) for the identification and evaluation of the significance of all risks that the Bank faces, which may have an adverse material impact on its financial position. As per Basel III framework, the Bank faces the following material risks which are taken into consideration in assessing / planning capital:

Risks under Pillar 1 MCR Risks under Pillar 2 SRP

1 Credit Risk 1 Residual Risk

2 Market Risk 2 Concentration Risk

3 Operational Risk 3 Liquidity Risk

4 Reputation Risk

5 Strategic Risk

6 Settlement Risk

7 Evaluation of Core Risk Management

8 Environmental & Climate Change Risk

9 Other material risks

Disclosure on Pillar 3 Market Discipline under Basel III 4

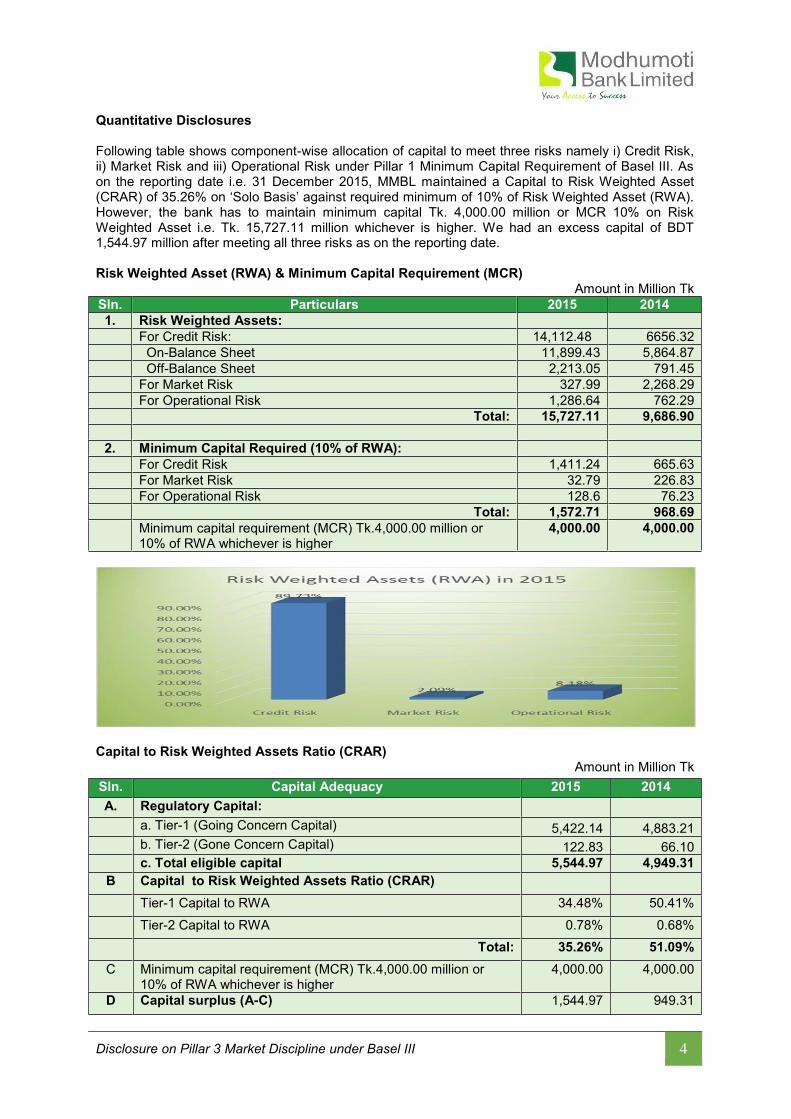

Quantitative Disclosures Following table shows component-wise allocation of capital to meet three risks namely i) Credit Risk, ii) Market Risk and iii) Operational Risk under Pillar 1 Minimum Capital Requirement of Basel III. As on the reporting date i.e. 31 December 2015, MMBL maintained a Capital to Risk Weighted Asset (CRAR) of 35.26% on ‘Solo Basis’ against required minimum of 10% of Risk Weighted Asset (RWA). However, the bank has to maintain minimum capital Tk. 4,000.00 million or MCR 10% on Risk Weighted Asset i.e. Tk. 15,727.11 million whichever is higher. We had an excess capital of BDT 1,544.97 million after meeting all three risks as on the reporting date. Risk Weighted Asset (RWA) & Minimum Capital Requirement (MCR) Amount in Million Tk

Sln. Particulars 2015 2014

1. Risk Weighted Assets:

For Credit Risk: 14,112.48 6656.32

On-Balance Sheet 11,899.43 5,864.87

Off-Balance Sheet 2,213.05 791.45

For Market Risk 327.99 2,268.29

For Operational Risk 1,286.64 762.29

Total: 15,727.11 9,686.90

2. Minimum Capital Required (10% of RWA):

For Credit Risk 1,411.24 665.63

For Market Risk 32.79 226.83

For Operational Risk 128.6 76.23

Total: 1,572.71 968.69

Minimum capital requirement (MCR) Tk.4,000.00 million or 10% of RWA whichever is higher

4,000.00 4,000.00

Capital to Risk Weighted Assets Ratio (CRAR)

Amount in Million Tk

Sln. Capital Adequacy 2015 2014

A. Regulatory Capital:

a. Tier-1 (Going Concern Capital) 5,422.14 4,883.21

b. Tier-2 (Gone Concern Capital) 122.83 66.10

c. Total eligible capital 5,544.97 4,949.31

B Capital to Risk Weighted Assets Ratio (CRAR)

Tier-1 Capital to RWA 34.48% 50.41%

Tier-2 Capital to RWA 0.78% 0.68%

Total: 35.26% 51.09%

C Minimum capital requirement (MCR) Tk.4,000.00 million or 10% of RWA whichever is higher

4,000.00 4,000.00

D Capital surplus (A-C) 1,544.97 949.31

Disclosure on Pillar 3 Market Discipline under Basel III 5

D. CREDIT RISK Qualitative Disclosures:

a) The general qualitative disclosure requirement with respect to credit risk: Definition of Credit Risk: Credit risk is the potential loss that may arise from a borrower’s failure to repay a loan or meet its obligation in accordance with agreed term. The Bank is exposed to credit risk through its general lending and money market lending. Credit risk management process: Bank’s credit policy has been prepared in line with Bangladesh Bank guidelines illustrating the approval process and delegation of authority which require to be approved by the Board. The approval process segregates relationship management/marketing from the approval authority. The approval authorities are delegated to different levels of management and Board committee. Board of Directors of the bank has the highest level of authority to approve any credit proposal and sub delegate such authority to the management and Executive Committee. The Business Development Banking Division starts the processing of the proposal and place it to the CRM with their recommendation. CRM performs the whole process of approval maintaining the credit norms and policies. CRM obtains recommendation from the CEC and finally the approval from competent authority based on the CEC recommendation. CRM sends sanction letter addressing the Branch and CC to CAD and Corporate. Credit Administration The bank accomplishes documentations and makes disbursements with utmost care to reduce the potential credit risk. The disbursement authority is centralized at Head Office, CAD. Branches send their request to CAD for limit loading after the completion of necessary documentation vide LDCL (Loan documentation checked list). Furthermore, the bank constantly monitors clients’ repayment behaviors, fulfillment of conditions given before disbursement and compliance of covenants in post disbursement period. Credit Monitoring The loan portfolio with classification status is reviewed periodically and brought to the notice of senior level management regarding down gradation, overdue, special mention account (SMA), classified and rescheduled portfolio along with early alert list for their information and guidance. The Branches are communicated through letters and circulars for implementation of efficient credit risk management in a proper manner including adherence to the Bank’s and Bangladesh Bank’s rules and regulations.

Disclosure on Pillar 3 Market Discipline under Basel III 6

Credit Risk Assessment and Grading Know Your Client (KYC) is the first step to analyze any credit proposal. Banker-Customer relationship is established through opening of CD/SB accounts of the customers. Proper introduction, photographs of the account holders/ signatories, passports etc., and all other required papers as per Bank’s policy are obtained during account opening. Physical verification of customer address is done prior to credit appraisal. At least three Cs, i.e., Character, Capital & Capacity of the customers are confirmed. Credit Appraisals include the details of amount and type of loan(s) proposed, purpose of loan (s), result of financial analysis, loan Structure (Tenor, Covenants, Repayment Schedule, Interest), security arrangements. The bank follows the CRG manual of Bangladesh Bank circulated on December 11, 2005 through BRPD circular no. 18. Borrowers are assigned risk grades based on the qualitative and quantitative factors of their business. There are 8 grades based on the marks obtained in qualitative and quantitative factors. The grades and quantitative factors of CRG:

Grading Short Name Marks Number

Superior SUP Fully cash secured by Govt. 1

Good GD 85+ 2

Acceptable ACCPT 75-84 3

Marginal/Watch list MG/WL 65-74 4

Special Mention SM 55-64 5

Sub-standard SS 45-54 6

Doubtful DF 35-44 7

Bad & Loss BL <35 8

Risk weight of principal risk components:

Quantitative and quantitative factors/ principal risk components

Weight

Financial Risk 50%

Business/Industry Risk 18%

Management Risk 12%

Security Risk 10%

Relationship Risk 10%

Credit Risk Mitigation Potential credit risks are mitigated by taking primary and collateral securities. There are other risk mitigates like netting agreements, credit insurance and other guarantees. The recognition of credit risk mitigation is subject to a number of considerations, including ensuring legal certainty of enforceability and effectiveness, ensuring the valuation and liquidity of the collateral is adequately monitored, and ensuring the value of the collateral is not materially correlated with the credit quality of the obligor. Collateral types which are eligible for risk mitigation include:

cash;

residential, commercial and industrial property;

assets such as motor vehicles, plant and machinery;

marketable securities & commodities;

bank guarantees; and letters of credit. Collateral is valued by independent third party surveyor in accordance with the credit policy and procedures.

Disclosure on Pillar 3 Market Discipline under Basel III 7

Past Due and Impaired Credit A claim that has not been paid as of its due date is termed as past due claim. Payment may be for repayment/renewal/rescheduling or as an installment of a loan. For loan classification and maintenance of specific and general provision Bank follows BRPD circular No-14 and 19 of 2012 and 05 of 2013, and advice of Bangladesh Bank from time to time. Approaches followed for specific and general allowances:

Particulars Short Term Agri Credit

Consumer Financing

SMEF Loans to

BHs/MBs/SDs All other

Credit Other than

HF, LP HF LP

UC 5% 5% 2% 2% 0.25% 2% 1%

SMA - 5% 2% 2% 0.25% 2% 1%

SS 5% 20% 20% 20% 20% 20% 20%

DF 5% 50% 50% 50% 50% 50% 50%

B/L 100% 100% 100% 100% 100% 100% 100% NB: CF=CONSUMER FINANCING, HF=HOUSING FINANCE, LP=LOANS FOR PROFESSIONALS TO SET UP BUSINESS, UC=UNCLASSIFIED, SMA=SPECIAL MENTION ACCOUNT, SS=SUBSTANDARD, DF=DOUBTFUL, B/L=BAD/LOSS, BHs/ MBs,/SDs= LOANS TO BROKERAGE HOUSES/MERCHANT BANKS/STOCK DEALERS.

Eligible Collateral: The following collateral is included as eligible collateral in determining base for provision:

100% of deposit under lien against the loan

100% of the value of government bond/savings certificate under lien

100% of the value of guarantee given by Government or Bangladesh Bank

100% of the market value of gold or gold ornaments pledged with the bank.

50% of the market value of easily marketable commodities kept under control of the bank

Maximum 50% of the market value of land and building mortgaged with the bank

50% of the average market value for last 06 months or 50% of the face value, whichever is less, of the shares traded in stock exchange.

Base for Provision: Provision is maintained at the stated rates mentioned above on the base for provision. Base for provision is calculated deducting interest suspense and the value of eligible collateral as followings:

Deposit with the same bank under lien against the loan

Government bond/savings certificate under lien,

Guarantee given by Government or Bangladesh Bank. For all other eligible collaterals, the provision will be maintained at the stated rates mentioned above on the balance calculated as the greater of the following two amounts:

Outstanding balance of the classified loan less the amount of Interest Suspense and the value of eligible collateral; and

15% of the outstanding balance of the loan. Interest treatment of classified account:

Sln. Status Interest to be credited to If recovered

1 SS Interest Suspense Account, instead of crediting the same to Income Account

First the interest charged and accrued but not charged is to be recovered from the said deposit and the principal to be adjusted afterwards

2 DF

3 BL Charging of interest in the same account will cease

Disclosure on Pillar 3 Market Discipline under Basel III 8

Subjective/Qualitative Judgment for Loan Classification Considering the nature and performance of a loan, the bank can also classify a particular loan on the basis of subjective judgment taking into consideration the factors such as uncertainty or doubt of repayment, continuous loss of capital, adverse situation, decrease of value of securities, legal suit etc. Condition for Qualitative Judgment:

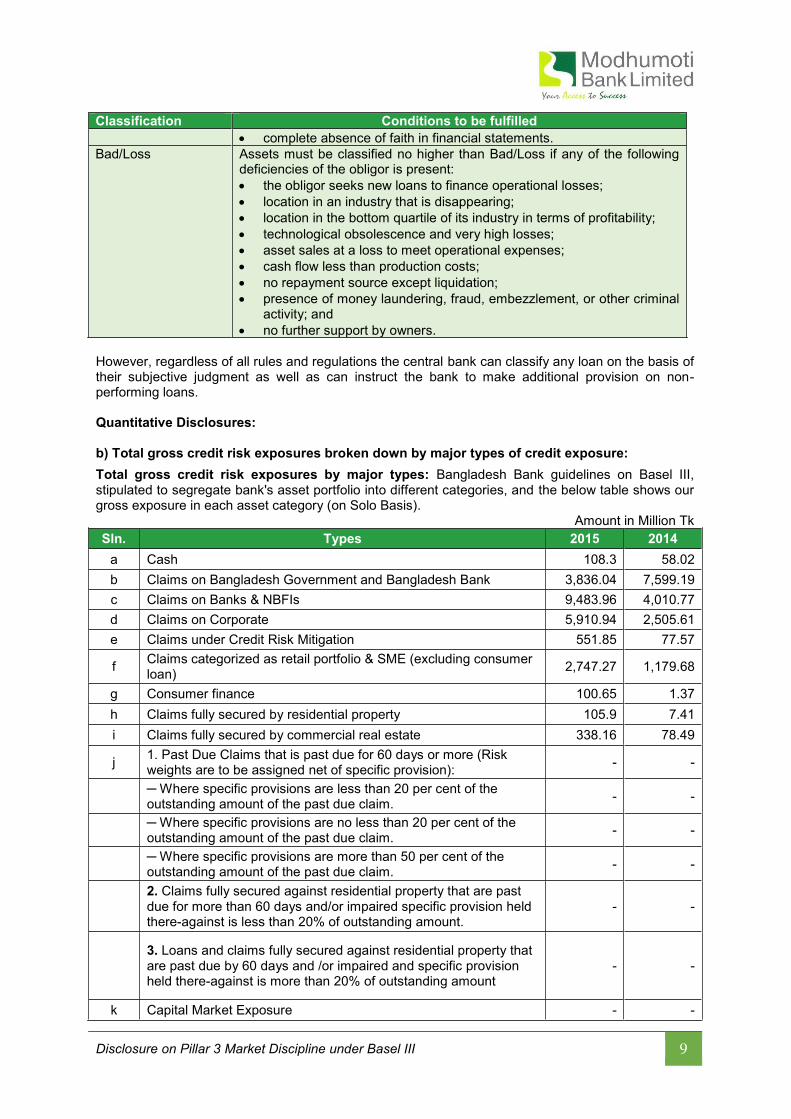

Classification Conditions to be fulfilled

Special Mention i. i) Assets must be classified no higher than Special Mention if any of the following deficiencies of bank management is present:

the loan was not made in compliance with the bank’s internal policies; failure to maintain adequate and enforceable documentation; or

poor control over collateral

ii. ii) Assets must be classified no higher than Special Mention if any of the following deficiencies of the obligor is present:

occasional overdrawn within the past year,

below-average or declining profitability;

barely acceptable liquidity;

problems in strategic planning.

Sub-standard i. i) Assets must be classified no higher than Sub-standard if any of the following deficiencies of the obligor is present:

recurrent overdrawn,

low account turnover,

competitive difficulties,

location in a volatile industry with an acute drop in demand;

very low profitability that is also declining;

inadequate liquidity;

cash flow less than repayment of principal and interest;

weak management;

doubts about integrity of management;

conflict in corporate governance;

unjustifiable lack of external audit; and

pending litigation of a significant nature.

ii. ii) Assets must be classified no higher than Sub-standard if the primary sources of repayment are insufficient to service the debt and the bank must look to secondary sources of repayment, including collateral.

iii. Iii) Assets must be classified no higher than Sub-standard if the banking organization has acquired the asset without the types of adequate documentation of the obligor’s net worth, profitability, liquidity, and cash flow that are required in the banking organization’s lending policy, or there are doubts about the validity of that documentation.

Doubtful Assets must be classified no higher than Doubtful if any of the following deficiencies of the obligor is present:

permanent overdrawn;

location in an industry with poor aggregate earnings or loss of markets;

serious competitive problems; failure of key products; operational losses;

illiquidity, including the necessity to sell assets to meet operating expenses;

cash flow less than required interest payments; very poor management;

non-cooperative or hostile management;

serious doubts of the integrity of management;

doubts about true ownership; and

Disclosure on Pillar 3 Market Discipline under Basel III 9

Classification Conditions to be fulfilled

complete absence of faith in financial statements.

Bad/Loss Assets must be classified no higher than Bad/Loss if any of the following deficiencies of the obligor is present:

the obligor seeks new loans to finance operational losses;

location in an industry that is disappearing;

location in the bottom quartile of its industry in terms of profitability;

technological obsolescence and very high losses;

asset sales at a loss to meet operational expenses;

cash flow less than production costs;

no repayment source except liquidation;

presence of money laundering, fraud, embezzlement, or other criminal activity; and

no further support by owners.

However, regardless of all rules and regulations the central bank can classify any loan on the basis of their subjective judgment as well as can instruct the bank to make additional provision on non-performing loans. Quantitative Disclosures: b) Total gross credit risk exposures broken down by major types of credit exposure:

Total gross credit risk exposures by major types: Bangladesh Bank guidelines on Basel III, stipulated to segregate bank's asset portfolio into different categories, and the below table shows our gross exposure in each asset category (on Solo Basis).

Amount in Million Tk

Sln. Types 2015 2014

a Cash 108.3 58.02

b Claims on Bangladesh Government and Bangladesh Bank 3,836.04 7,599.19

c Claims on Banks & NBFIs 9,483.96 4,010.77

d Claims on Corporate 5,910.94 2,505.61

e Claims under Credit Risk Mitigation 551.85 77.57

f Claims categorized as retail portfolio & SME (excluding consumer loan)

2,747.27 1,179.68

g Consumer finance 100.65 1.37

h Claims fully secured by residential property 105.9 7.41

i Claims fully secured by commercial real estate 338.16 78.49

j 1. Past Due Claims that is past due for 60 days or more (Risk weights are to be assigned net of specific provision):

- -

─ Where specific provisions are less than 20 per cent of the outstanding amount of the past due claim.

- -

─ Where specific provisions are no less than 20 per cent of the outstanding amount of the past due claim.

- -

─ Where specific provisions are more than 50 per cent of the outstanding amount of the past due claim.

- -

2. Claims fully secured against residential property that are past due for more than 60 days and/or impaired specific provision held there-against is less than 20% of outstanding amount.

- -

3. Loans and claims fully secured against residential property that are past due by 60 days and /or impaired and specific provision held there-against is more than 20% of outstanding amount

- -

k Capital Market Exposure - -

Disclosure on Pillar 3 Market Discipline under Basel III 10

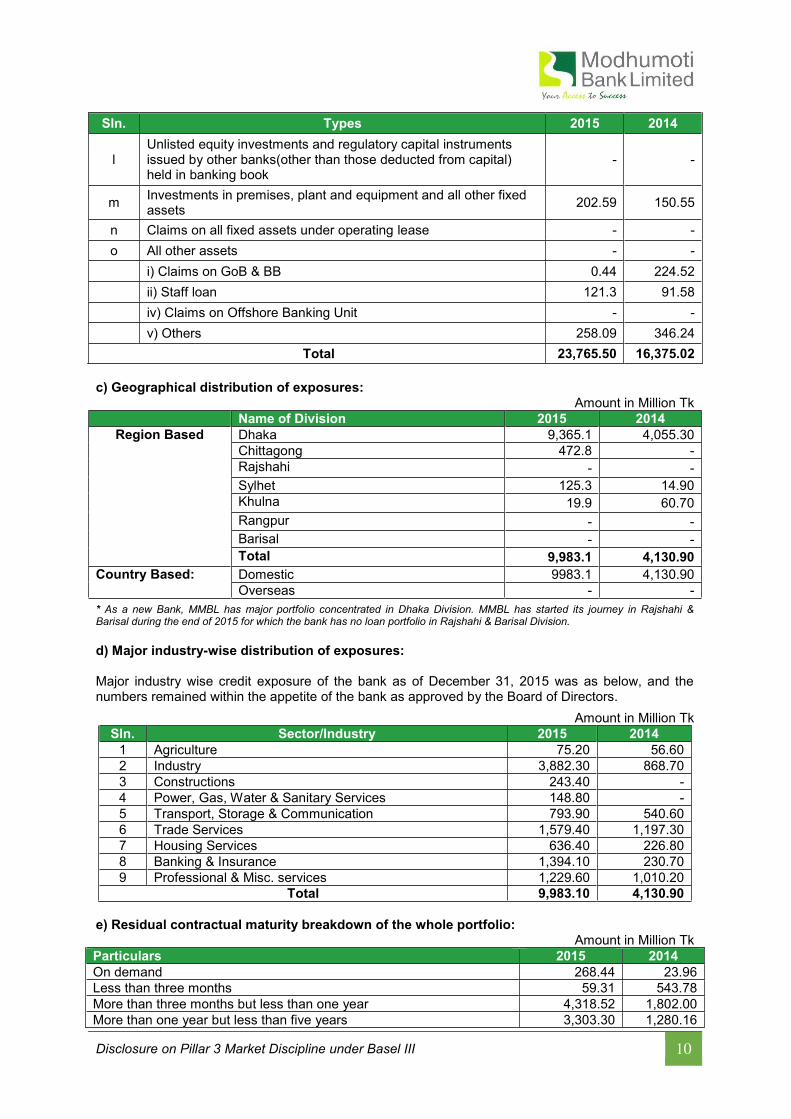

Sln. Types 2015 2014

l Unlisted equity investments and regulatory capital instruments issued by other banks(other than those deducted from capital) held in banking book

- -

m Investments in premises, plant and equipment and all other fixed assets

202.59 150.55

n Claims on all fixed assets under operating lease - -

o All other assets - -

i) Claims on GoB & BB 0.44 224.52

ii) Staff loan 121.3 91.58

iv) Claims on Offshore Banking Unit - -

v) Others 258.09 346.24

Total 23,765.50 16,375.02

c) Geographical distribution of exposures:

Amount in Million Tk

Name of Division 2015 2014

Region Based Dhaka 9,365.1 4,055.30

Chittagong 472.8 -

Rajshahi - -

Sylhet 125.3 14.90

Khulna 19.9 60.70

Rangpur - -

Barisal - -

Total 9,983.1 4,130.90

Country Based: Domestic 9983.1 4,130.90

Overseas - -

* As a new Bank, MMBL has major portfolio concentrated in Dhaka Division. MMBL has started its journey in Rajshahi & Barisal during the end of 2015 for which the bank has no loan portfolio in Rajshahi & Barisal Division.

d) Major industry-wise distribution of exposures: Major industry wise credit exposure of the bank as of December 31, 2015 was as below, and the numbers remained within the appetite of the bank as approved by the Board of Directors.

Amount in Million Tk

Sln. Sector/Industry 2015 2014

1 Agriculture 75.20 56.60

2 Industry 3,882.30 868.70

3 Constructions 243.40 -

4 Power, Gas, Water & Sanitary Services 148.80 -

5 Transport, Storage & Communication 793.90 540.60

6 Trade Services 1,579.40 1,197.30

7 Housing Services 636.40 226.80

8 Banking & Insurance 1,394.10 230.70

9 Professional & Misc. services 1,229.60 1,010.20

Total 9,983.10 4,130.90

e) Residual contractual maturity breakdown of the whole portfolio:

Amount in Million Tk

Particulars 2015 2014

On demand 268.44 23.96

Less than three months 59.31 543.78

More than three months but less than one year 4,318.52 1,802.00

More than one year but less than five years 3,303.30 1,280.16

Disclosure on Pillar 3 Market Discipline under Basel III 11

More than five years 2,033.51 481.00

Total 9,983.10 4,130.90

f) Major industry type amount of impaired loans:

Amount in Million Tk

Particulars 2015 2014

Agriculture - -

Large and Medium Scale Industries - -

Small and Cottage Industry - -

Exports - -

Commercial Lending - -

Finance to NBFIs - -

Real Estate - -

Retail Banking - -

Transport & Communication - -

Credit Card - -

Others - -

Total - -

*The bank had no impaired loans as of December 31, 2015. g) Gross Non Performing Assets (NPAs)

Amount in Million Tk

Particulars 2015 2014

Gross Non Performing Assets (NPAs) - -

Nonperforming assets to outstanding loans and advances - -

Movement of Non-Performing Assets (NPAs): - -

Opening balance - -

Additions - -

Reductions - -

Closing balance - -

Movement of specific provisions for NPAs: - -

Opening balance - -

Provision made during the period - -

Write off - -

Write back of excess provisions - -

Closing balance - -

*The bank had no impaired loans as of December 31, 2015. E. EQUITIES: DISCLOSURES FOR BANKING BOOK POSITIONS Qualitative Disclosures: a) Banking book positions consist of those assets which are bought for holding until they mature.

The bank treats unquoted equities as banking book assets. Unquoted equities are not traded in the bourses or in the secondary market, they are shown in the balance sheet at cost price and no revaluation reserve is created against these equities.

Quantitative Disclosures: b) Values of investments as disclosed in the Balance Sheet:

Amount in Million Tk

Particulars Solo

Cost Price Market Price

Unquoted Share - -

Quoted Share - -

*The bank had no equity investment as of December 31, 2015.

Disclosure on Pillar 3 Market Discipline under Basel III 12

For Banking Book Equity

Amount in Million Tk

e) Capital Requirement

Amount in Million Tk

Particulars Solo (Bank)

Unquoted Share -

Quoted Share -

F. INTEREST RATE RISK IN THE BANKING BOOK (IRRBB) Qualitative Disclosures: a)

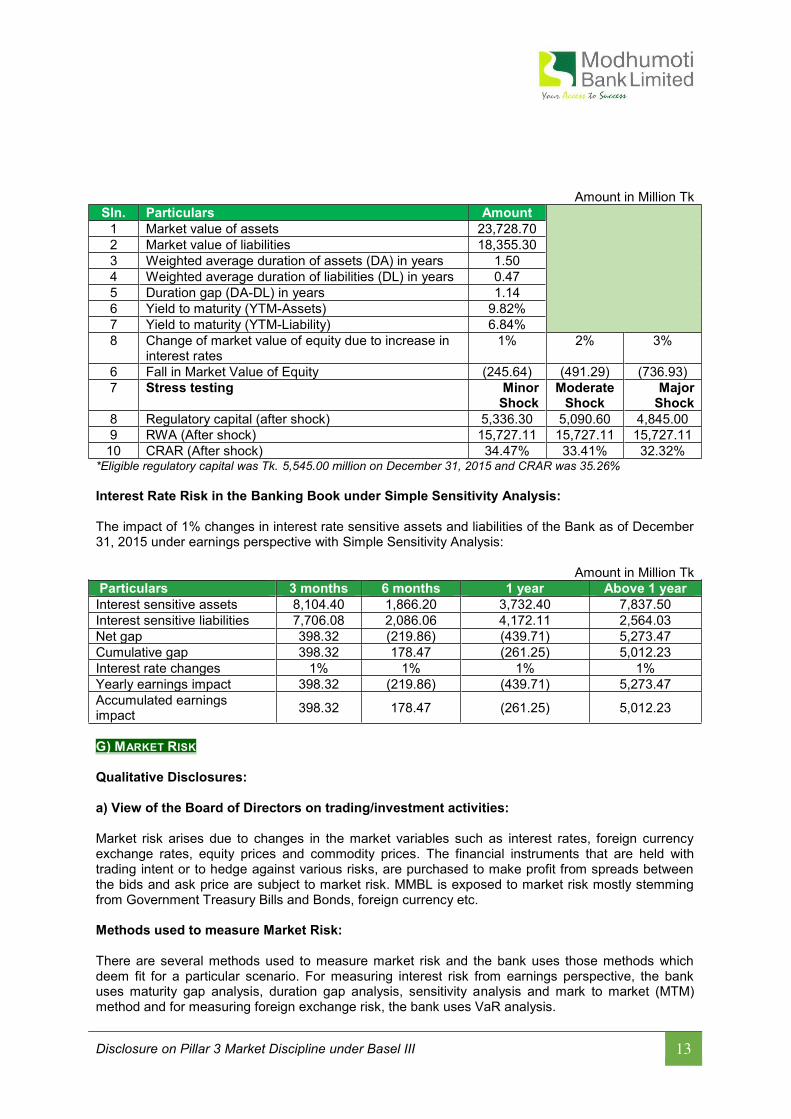

Interest rate risk affects the bank’s financial condition due to adverse movements in interest rates of interest sensitive assets and liabilities. Interest Rate Risk is managed through use of Gap analysis of rate sensitive assets and liabilities and monitored through prudential limits and stress testing. The IRRBB is monitored in movements/changes on a monthly basis and the impact on Net Interest Income is assessed. Interest rate risk is the risk where changes in market interest rates might adversely affect a bank's financial condition.

Changes in interest rates affect both the current earnings (earnings perspective) as well as the net worth of the bank (economic value perspective).

Re-pricing risk is often the most apparent source of interest rate risk for a bank and is often gauged by comparing the volume of a bank’s assets that mature or re-price within a given time period with the volume of liabilities that do so. The short-term impact of changes in interest rates is on the bank’s Net Interest Income (NII). In a longer term, changes in interest rates impact the cash flows on the assets, liabilities and off-balance sheet items, giving rise to a risk to the net worth of the bank arising out of all re-pricing mismatches and other interest rate sensitive position. The ALCO formulates the policy and strategy depending on the market conditions to maximize Net Interest Income.

Quantitative Disclosures: Gap analysis: Duration Gap

The duration gap tells how cash flows for assets and liabilities are matched. A positive duration gap is when the duration of assets exceeds the duration of liabilities (which means greater exposure to rising interest rates). If rates go up by 1% the price of assets fall more than the price of liabilities. A negative duration gap is when the duration of assets is less than the duration of liabilities (which means greater exposure to declining interest rates). If rates go down by 1%, the price of assets goes up less than the price of liabilities.

Sln. Particulars Solo (Bank)

c) The cumulative realized gains (losses) arising from sales and liquidations in the reporting period

-

d) Total unrealized gains(losses) -

Total latent revaluation gains (losses) -

Any amounts of the above included in Tier 2 capital -

Disclosure on Pillar 3 Market Discipline under Basel III 13

Amount in Million Tk

Sln. Particulars Amount

1 Market value of assets 23,728.70

2 Market value of liabilities 18,355.30

3 Weighted average duration of assets (DA) in years 1.50

4 Weighted average duration of liabilities (DL) in years 0.47

5 Duration gap (DA-DL) in years 1.14

6 Yield to maturity (YTM-Assets) 9.82%

7 Yield to maturity (YTM-Liability) 6.84%

8 Change of market value of equity due to increase in interest rates

1% 2% 3%

6 Fall in Market Value of Equity (245.64) (491.29) (736.93)

7 Stress testing Minor Shock

Moderate Shock

Major Shock

8 Regulatory capital (after shock) 5,336.30 5,090.60 4,845.00

9 RWA (After shock) 15,727.11 15,727.11 15,727.11

10 CRAR (After shock) 34.47% 33.41% 32.32% *Eligible regulatory capital was Tk. 5,545.00 million on December 31, 2015 and CRAR was 35.26%

Interest Rate Risk in the Banking Book under Simple Sensitivity Analysis: The impact of 1% changes in interest rate sensitive assets and liabilities of the Bank as of December 31, 2015 under earnings perspective with Simple Sensitivity Analysis:

Amount in Million Tk

Particulars 3 months 6 months 1 year Above 1 year

Interest sensitive assets 8,104.40 1,866.20 3,732.40 7,837.50

Interest sensitive liabilities 7,706.08 2,086.06 4,172.11 2,564.03

Net gap 398.32 (219.86) (439.71) 5,273.47

Cumulative gap 398.32 178.47 (261.25) 5,012.23

Interest rate changes 1% 1% 1% 1%

Yearly earnings impact 398.32 (219.86) (439.71) 5,273.47

Accumulated earnings impact

398.32 178.47 (261.25) 5,012.23

G) MARKET RISK Qualitative Disclosures: a) View of the Board of Directors on trading/investment activities: Market risk arises due to changes in the market variables such as interest rates, foreign currency exchange rates, equity prices and commodity prices. The financial instruments that are held with trading intent or to hedge against various risks, are purchased to make profit from spreads between the bids and ask price are subject to market risk. MMBL is exposed to market risk mostly stemming from Government Treasury Bills and Bonds, foreign currency etc. Methods used to measure Market Risk: There are several methods used to measure market risk and the bank uses those methods which deem fit for a particular scenario. For measuring interest risk from earnings perspective, the bank uses maturity gap analysis, duration gap analysis, sensitivity analysis and mark to market (MTM) method and for measuring foreign exchange risk, the bank uses VaR analysis.

Disclosure on Pillar 3 Market Discipline under Basel III 14

We use standardized (Rule Based) method for Calculating capital charge against market risks for minimum capital requirement of the Bank under Basel-III. Market Risk Management System: The Bank has its own Market Risk Management System which includes Asset Liability Risk Management (ALM) and Foreign Exchange Risk Management under the core risk management guidelines. Asset Liability Management (ALM): The ALM policy specifically deals with liquidity risk management and interest rate risk management framework. Foreign Exchange Risk Management: Foreign exchange risk arises when the bank is involved in foreign currency transactions. These include foreign currency exchange, placement, investments, loans, borrowings and different contractual agreements. We use different hedging techniques to mitigate foreign exchange risks exposed to the bank. Policies and processes for mitigating market risk

Risk Management and reporting is based on parameters such as Maturity Gap Analysis, Duration Gap Analysis, VaR etc, in line with the global best practices.

Risk Profiles are analyzed and mitigating strategies/ processes are suggested by the Asset Liability Committee (ALCO).

Foreign Exchange Net Open Position (NOP) limits (Day limit / Overnight limit), deal-wise trigger limits, Stop-loss limit, Profit / Loss in respect of cross currency trading are properly monitored and exception reporting is regularly carried out.

Holding equities is monitored regularly so that the investment remains within the limit as set by BB.

ALCO analyzes market and determines strategies to attain business goals.

Reconciliation of foreign currency transactions. Quantitative Disclosures: b) The capital requirements:

Amount in Million Tk

H. OPERATIONAL RISK Qualitative Disclosures:

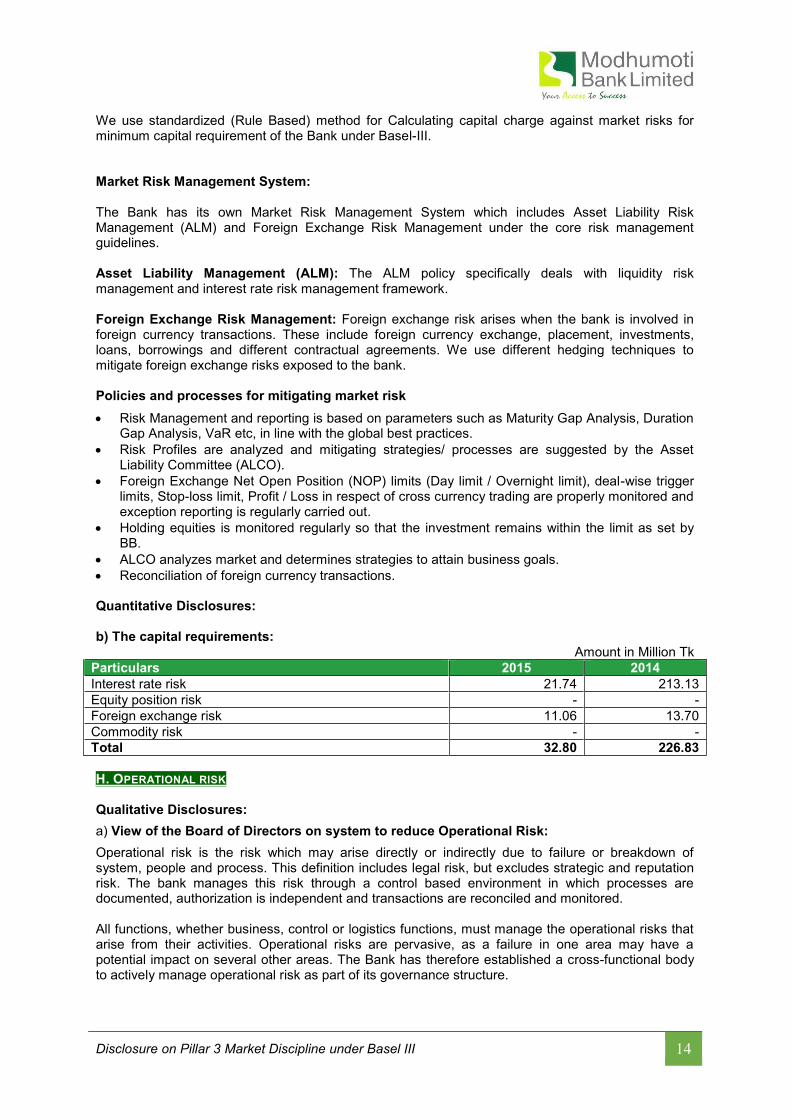

a) View of the Board of Directors on system to reduce Operational Risk:

Operational risk is the risk which may arise directly or indirectly due to failure or breakdown of system, people and process. This definition includes legal risk, but excludes strategic and reputation risk. The bank manages this risk through a control based environment in which processes are documented, authorization is independent and transactions are reconciled and monitored. All functions, whether business, control or logistics functions, must manage the operational risks that arise from their activities. Operational risks are pervasive, as a failure in one area may have a potential impact on several other areas. The Bank has therefore established a cross-functional body to actively manage operational risk as part of its governance structure.

Particulars 2015 2014

Interest rate risk 21.74 213.13

Equity position risk - -

Foreign exchange risk 11.06 13.70

Commodity risk - -

Total 32.80 226.83

Disclosure on Pillar 3 Market Discipline under Basel III 15

The foundation of the operational risk framework is that all functions have adequately defined their roles and responsibilities. The functions can then collectively ensure that there is adequate segregation of duties, complete coverage of risks and clear accountability. The practice is supported by a periodic process conducted by ICCD, and monitoring external operational risk events, which ensure that the bank stays in line with the international best practices. Performance Gap of Executives and Staffs: The bank believes that training and knowledge sharing is the best way to reduce knowledge gap. Therefore, it arranges trainings on a regular basis for its employees to develop their expertise. The bank offers competitive pay package to its employees based on performance and merit. It always tries to develop a culture where all employees can apply his/her talent and knowledge to work for the organization with high ethical standards in order to add more value to the company and for the economy. Policies and processes for mitigating operational risk: The Bank has adopted policies which deal with managing different Operational Risks. Bank strongly follows KYC norms for its customer dealings and other banking operations. The Audit & Inspection Unit of Internal Control and Compliance Division of the Bank, the inspection teams of Bangladesh Bank and External Auditors conduct inspection of different branches and divisions at Head Office of the Bank and submit reports presenting the findings of the inspections. Necessary control measures and corrective actions have been taken on the suggestions or observations made in these reports. Approach for calculating capital charge for operational risk: The bank applies ‘Basic Indicator Approach’ of Basel II as prescribed by BB in revised RBCA Guidelines. Under this approach, banks have to calculate average annual gross income (GI) of last three years and multiply the result by 15% to determine required capital charge. Gross Income is the sum of ‘Net Interest Income’ and ‘Net non-interest income’ of a year or it is ‘Total Operating Income’ of the bank with some adjustments as followings:

Be gross of any provision (e.g. for unpaid interest),

Be gross of operating expenses, including fees paid to outsourcing service providers,

Exclude realized profits/losses from sale of securities held to maturity in the banking book, Exclude extraordinary or irregular items,

Exclude income derived from insurance and

Include lost interest i.e. interest suspense on SMA and classified loans.

Quantitative Disclosures: a) Capital requirement for operational risk

Amount in Million Tk

Particulars Solo

2015 2014

The capital requirements for operational risk 128.66 76.23

Calculation of Capital Charge for Operational Risk: Basic Indicator Approach

Amount in Million Tk

Year Gross Income (GI) Average GI 15% of Average GI

2013 209.97

2014 806.40 857.76 128.66

2015 1,556.90

Total 2,573.29 857.76 128.66

I. LIQUIDITY RATIO Qualitative Disclosures:

Disclosure on Pillar 3 Market Discipline under Basel III 16

Views of BOD on system to reduce liquidity Risk

Liquidity risk is the risk of probability to be unable to meet short term financial demands by the

bank. This may occur due to the inability to convert a security or fixed asset to cash without a loss of capital and/or income in the process. Banks today are facing a myriad of challenges; most of them triggered by new regulatory requirements. To maintain a profitable business, however, it is not enough for a bank to simply comply with new regulatory requirements: it must also optimize its business model within regulatory constraints. To do so, the bank has already been introduced regulatory ratios (as per Basel III), the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR), top- down from the Board of Directors of the Bank.

In order to reduce the liquidity risk, the Board of Directors of the Bank has formed Asset Liability Committee (ALCO) and All Risk Committee at management level as per guidelines of Bangladesh Bank. ALCO regularly monitors the maintenance of the liquidity position of the Bank. The management decided to concentrate on retail or individual (small) deposits instead of large corporate deposits. The Bank also draws up contingency plans to deal with extraordinary conditions of Liquidity Risk after comprehensive scenario analysis. Methods used to measure Liquidity risk

Liquidity mismatch profile

The primary tool of monitoring liquidity risk is the maturity mismatch analysis, which presents the profile of future expected cash flows under pre-defined scenarios. The bank conduct liquidity mismatch profiling on an ongoing basis which is ultimately monitored by Treasury, ALCO, Core Risk Management Division and All Risk Committee of Management. Stress testing

The bank undertook stress testing and scenario analysis periodically to determine the stress situations on the liquidity of the Bank and ultimate impact of the liquidity risk on the fund management of the Bank.

Liquidity Coverage Ratio (LCR): LCR aims to ensure the maintenance of an adequate level of unencumbered, high-quality liquid assets that can be converted into cash to meet its liquidity needs for 30 calendar days. It measures the need for liquid assets in a stressed environment, in which deposits and other sources of funds (both unsecured and secured) run off, to various extents, and unused credit facilities are also drawn down in various magnitudes.

LCR= Stock of high quality liquid assets ≥100

Total net cash outflows over the next 30 days Stock of high quality liquid asset (SHQLA):

The following components are included in the computation of SHQLA -

1. Cash on hand (Lcy + Fcy) 2. Balance with BB (Lcy+ Fcy, excluding lien) 3. Un-encumbered approved securities (excluding lien) Net Stable Funding Ratio (NSFR): The NSFR aims to limit over-reliance on short-term wholesale funding during times of abundant market liquidity and encourage better assessment of liquidity risk across all on- and off-balance sheet items. The minimum acceptable value of this ratio is 100 percent, indicating that available stable funding (ASF) should be at least equal to required stable funding (RSF).

NSFR= Available amount of stable funding (ASF) ≥100 Required amount of stable funding (RSF)

Liquidity risk management system

Liquidity risk management is a key banking function and an integral part of the asset and liability management process. The fundamental role of banks is the maturity transformation of short-term

Disclosure on Pillar 3 Market Discipline under Basel III 17

deposits (liabilities) into long-term loans (assets) and this makes banks inherently vulnerable to liquidity risk. The transformation process creates asset and liability maturity mismatches on a bank’s balance sheet that must be actively managed with available liquidity. This is the process known as liquidity risk management. The primary role of liquidity-risk management is to (1) prospectively assess the need for funds to meet obligations and (2) ensure the availability of cash or collateral to fulfill those needs duly by coordinating the various sources of funds available to the institution under normal and stressed conditions. Policies and processes for mitigating liquidity risk The Bank has contingency funding plan and Treasury Policy as a policy support to combat liquidity risk. The Board and the management implement the following processes in the bank for superior liquidity risk management:

Liquidity risk tolerance: Bank set liquidity risk tolerance like Maximum Cumulative Outflow (MCO) at 20% as per guidelines of BB;

Maintaining adequate levels of liquidity considering the average daily withdrawal by the customers;

Identification and measurement of contingent liquidity risks arising from unseen scenarios.

Contingency funding plan: Contingency funding plans incorporate events that could rapidly affect the bank’s liquidity arising from sudden inability to call back long-term loans and advances, or the loss of a large depositor or counterparties.

Public disclosure in promoting market discipline under Pillar 3 of Basel III. Quantitative Disclosures:

Amount in Million Tk

*LCR and NSFR come into effect from March 31, 2015 as per RBCA Guidelines.

J. LEVERAGE RATIO Qualitative Disclosures: Views of BOD on system to reduce excessive leverage

Excessive leverage by banks is widely believed to have contributed to the global financial crisis in 2008. To address this, the international community has proposed the adoption of a non-risk-based capital measure, the leverage ratio, as an additional prudential tool to complement minimum capital adequacy requirements. Accordingly, leverage ratio has been introduced under Basel III. Leverage ratio is the relative amount of Tire 1 capital to total exposure of the Bank (not risk-weighted) which has been set at minimum 3%. Under Basel III, a simple, transparent, non-risk based regulatory leverage ratio has been introduced to achieve the following objectives:

constrain leverage in the banking sector, thus helping to mitigate the risk of the destabilizing deleveraging processes which can damage the financial system and the economy

introduce additional safeguards against model risk and measurement error by supplementing the risk-based measure with a simple, transparent, independent measure of risk

The Board Risk Management Committee regularly reviews the leverage ratios and advice the management to strictly monitor the ratio in addition to the Pillar 1 Minimum Capital Requirement.

Particulars 2015 2014*

Liquidity Coverage Ratio (LCR) 500.68% NA

Net Stable Funding Ratio (NSFR) 175.55% NA Stock of High quality liquid assets 3,944.27 NA

Total net cash outflows over the next 30 calendar days 787.78 NA Available amount of stable funding 19,617.52 NA

Required amount of stable funding 11,111.33 NA

Disclosure on Pillar 3 Market Discipline under Basel III 18

Policies and processes for managing excessive on and off- balance sheet leverage The bank reviews its leverage position as per the Guidelines on Risk Based Capital Adequacy (revised regulatory capital framework for banks in line with Basel III). In addition, the bank has Risk Appetite as per Credit Risk Management Policy and Risk Appetite Framework of the Bank. Bank also employ Annual Budget Plan and Capital Growth Plan for managing excessive on and off-balance sheet leverage. Approach for calculating exposure

The bank calculates the exposure under standardized approach as per the Guidelines on Risk Based Capital Adequacy (revised regulatory capital framework for banks in line with Basel III).

Quantitative Disclosures: Amount in Million Tk

*Leverage ratio come into effect from March 31, 2015 as per RBCA Guidelines. K. REMUNERATION

Qualitative Disclosures:

a) Information relating to the bodies that oversee remuneration

Name, composition and mandate of the main body overseeing remuneration The Board of Directors of the Bank oversee the remuneration of the employees and members of the Board of the Bank. The bank has no separate committee in the Board to look after the remuneration issues of the Bank. The Board set competitive salary and bonuses for the employees of the Bank. However, the Board allows the remuneration to its members as per the guidance of Bangladesh Bank. The remuneration strategy is designed to reward competitively the achievement of long-term sustainable performance and attract and motivate the very best people who are committed to maintaining a long-term career with the bank and performing their role in the long-term interests of our shareholders. To achieve this objective, the bank believes that effective governance of our remuneration practices is a key requirement. Governance of remuneration principles and oversight of its implementation by the Board ensures what we pay our people is aligned to our business strategy and performance is judged not only on what is achieved over the short and long term but also importantly on how it is achieved, as we believe the latter contributes to the long-term sustainability of the business. External consultants for remuneration process There is no external consultant in the bank for setting remuneration for its employees of the Bank. Scope of the bank’s remuneration policy The Board formulate different policies e.g HR Policy, Increment Policy, Promotion Policy, Provident Fund Policy and Gratuity Fund Policy which eventually supplement the remuneration of the employees. However, the HR Policy is yet to finalize. The board periodically reviews the adequacy and effectiveness of the bank’s remuneration policy and ensures that the policy meets the commercial requirement to remain competitive, is affordable, allows flexibility in response to prevailing circumstances and is consistent with effective risk management.

Particulars 2015 2014*

Leverage Ratio 21.17% NA

On balance sheet exposure 23,765.50 NA Off balance sheet exposure 1,853.80 NA Total exposure 25,619.30 NA

Disclosure on Pillar 3 Market Discipline under Basel III 19

Types of employees considered as material risk takers and as senior managers There are 19 employees is considered as material risk takers which include the Managing Director & CEO, Additional Managing Director, Head of Operations, Head of Treasury and Head of Business Development & Marketing Division and 15 branch managers. Apart from that SVP and above employees can be considered as senior managers who eventually perform management role in achieving the organization’s goal. Accordingly the bank has 7 senior managers working in different areas of the bank including HO and different branches. b) Information relating to the design and structure of remuneration processes Overview of the key features and objectives of remuneration policy Key features of the remuneration policy and the structure of remuneration process of the Bank are noted below:

Fixed pay : The purpose of the fixed pay is to attract and retain employees by paying market competitive pay for the role, skills and experience required for the business. This includes salary, fixed pay allowance, cash in lieu of pension and other cash allowances in accordance with local market practices These payments are fixed and do not vary with performance.

Benefits : The bank provides benefits in accordance with the industry practice of the country. This includes but is not limited to the provision of provident fund, gratuity fund, medical allowances, transport loan and house building loan etc.

Annual incentive

: The banks provide annual incentive based on the achievement of the business and profit target of the Bank. The bank provide performance based incentive to its employees.

Bonus paid based on the last basic salary of the employee of the Bank. However, bonus for MD & CEO has maximum limit of Tk.10.00 lac pa as per guidance of Bangladesh Bank.

Only cash, and cash equivalent remuneration shall be permitted – no equity or equity linked payments are permitted in the bank. Objectives of remuneration policy The main objectives of the remuneration policy are to attract, retain and reward talented staff and management, by offering compensation that is competitive within the industry, motivates management to achieve the bank’s business objectives and encourage high level of performance and aligns the interests of management with the interests of shareholders. Whether the remuneration committee reviewed the firm’s remuneration policy during the past year, and if so, an overview of any changes that were made The board ratified the bonus (incentive) policy of the bank during 2015. The policy outlined the eligibility to receive annual incentive. Whether risk and compliance employees are remunerated independently of the businesses they oversee The bank has no separate policy for the risk and compliance employees. c) Description of the ways in which current and future risks are taken into account in the

remuneration processes Overview of the key risks that the bank takes into account when implementing remuneration measures

Disclosure on Pillar 3 Market Discipline under Basel III 20

The bank’s policy is to ensure that the level and composition of remuneration is appropriate and fair having regard to competitive forces and the interests of the bank, its shareholders, and that its relationship to performance is clear in present and future environment. The bank considers the general inflation, industry (banking) pay structure and national pay-scale in determining the salary structure of the employees. If the pay structure cannot be competitive then good employees may leave the organization i.e. employees turnover will increase which may negatively impact the business of the bank. Overview of the nature and type of the key measures used to take account of these risks, including risks difficult to measure The management proposes competitive remuneration and other non-financial benefits like promotion, training etc. so that employees turnover ratio can be kept under tolerable limit. Sometimes few issues are difficult to measure relating to employees e.g. creativity, helpfulness to customers, commitment risk etc. In such cases, management need to apply qualitative judgment for determining the remuneration especially annual incentive or bonuses. A discussion of the ways in which these measures affect remuneration Qualitative judgment may affect the remuneration as there is no direct way to determine the remuneration. A discussion of how the nature and type of these measures has changed over the past year and reasons for the change, as well as the impact of changes on remuneration. No visible changes have been made in respect to the nature and type of the measures used regarding the key risks take into account when implementing remuneration. d) Description of the ways in which the bank seeks to link performance during a performance

measurement period with levels of remuneration An overview of main performance metrics for bank, top-level business lines and individuals Staff are subject to performance management reviews annually. Remuneration, including bonuses, are in alignment with the outcome of these reviews. The reviews are being done based on the annual performance appraisal including the business performance of the employees. A discussion of how amounts of individual remuneration are linked to bank-wide and individual performance Remuneration is based on bank-wide business performance of the Bank including achievement of profit target, loans and advances target etc. These are assessed individually on a rating scale overseen by the individuals’ supervisor or committee. Remuneration increases will only take place if the bank’s overall performance is positive, and the individuals’ performance is considered to be exceeding expectations. A discussion of the measures the bank will in general implement to adjust remuneration in the event that performance metrics are weak If the performance of the bank found weak, then no increases in remuneration may take place despite personal achievements of employees. However, the management will take initiative to improve the overall business performance and individual performance so that remuneration of the employees cannot be hampered for prolonged period. e) Description of the ways in which the bank seek to adjust remuneration to take account of

longer-term performance.

Disclosure on Pillar 3 Market Discipline under Basel III 21

A discussion of the bank’s policy on deferral and vesting of variable remuneration and, if the fraction of variable remuneration that is deferred differs across employees or groups of employees, a description of the factors that determine the fraction and their relative importance The bank provides Provident Fund contribution and Gratuity Fund contribution for the employees as deferred payment. The bank does not provide any deferred variable remuneration.

A discussion of the bank’s policy and criteria for adjusting deferred remuneration before vesting and (if permitted by national law) after vesting through clawback arrangements.

The bank has no clawback arrangements after providing deferred remuneration (PF, GF etc.). However, in case of special cases, the management may clawback the deferred remuneration vested to the employees.

f) Description of the different forms of variable remuneration that the bank utilizes and the

rationale for using these different forms.

An overview of the forms of variable remuneration offered (i.e. cash, shares and share-linked instruments and other forms)

The board may declare general annual incentive, if the bank achieves its business target. However, employees who exceeds expected performance can get variable remuneration. All remuneration are paid in cash only.

A discussion of the use of the different forms of variable remuneration and, if the mix of different forms of variable remuneration differs across employees or groups of employees, a description the factors that determine the mix and their relative importance.

The most common forms of variable pay are bonuses and incentives. The contractual employees will not be considered for variable remuneration.

Quantitative Disclosures: g) Meetings of main body overseeing remuneration and remuneration paid to its member

during 2015 Amount in Million Tk.

Particulars Number Amount

Number of meetings held 3 -

Remuneration paid - 0.27

h) Variable remuneration, bonuses and other payments during 2015

Amount in Million Tk

Particulars Number Amount

Employees having received a variable remuneration award - 20.00

Guaranteed bonuses awarded 2 16.88

Sign-on awards made - -

Severance payments made - -

i) Deferred remuneration in 2015

Amount in Million Tk

Particulars Amount

Disclosure on Pillar 3 Market Discipline under Basel III 22

Total amount of outstanding deferred remuneration:

Cash 46.48

Shares -

Share-linked instruments & others -

Total amount of deferred remuneration paid out in 2015 19.34

j) Breakdown of amount of remuneration

Amount in Million Tk

Particulars Amount

Breakdown of amount of remuneration:

Fixed 166.55

Variable 20.00

Deferred 19.34

Non-deferred -

Different forms used

Cash 205.89

Shares -

Share-linked instruments & others -

l) Quantitative information about employees’ exposure to implicit (eg fluctuations in the

value of shares or performance units) and explicit adjustments (eg clawbacks or similar reversals or downward revaluations of awards) of deferred remuneration and retained remuneration:

Amount in Million Tk

Particulars Amount

Total amount of outstanding deferred remuneration and retained remuneration exposed to ex post explicit and/or implicit adjustments

-

Total amount of reductions during 2015 due to ex post explicit adjustments -

Total amount of reductions during 2015 due to ex post implicit adjustments -