disclosure quality, cost of capital, and investors'...

TRANSCRIPT

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality, Cost of Capital, andInvestors’ Welfare

Pingyang Gao

Yale School of Management

March 6, 2008

Presentation atThe Wharton School

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

1 OverviewResearch QuestionsEconomic Forces and Main ResultsRelated Literatures

2 Model and EquilibriumEvents, Utility, Cash Flow Function, and InformationThe Equilibrium

3 Effects of Disclosure QualityDisclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

4 Extensions and Conclusion

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Research Questions

When disclosure changes a firm’s real decisions, how doesdisclosure quality affect cost of capital, currentshareholders’ welfare, and new shareholders’ welfare?

Under what conditions is cost of capital a sufficient statisticfor the welfare of current and/or new shareholders?

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Research Questions

When disclosure changes a firm’s real decisions, how doesdisclosure quality affect cost of capital, currentshareholders’ welfare, and new shareholders’ welfare?

Under what conditions is cost of capital a sufficient statisticfor the welfare of current and/or new shareholders?

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Motivation

Regulators and firms are concerned about the welfareimpacts of disclosure quality;

The research has focused on the relation betweendisclosure quality and cost of capital;

There is a gap between the empirical evidence and thetheoretical research;

What is the relation between cost of capital and investors’welfare?

Levitt“The truth is, high [accounting] standards lower the cost of capital.And that’s a goal we share.”

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Motivation

Regulators and firms are concerned about the welfareimpacts of disclosure quality;

The research has focused on the relation betweendisclosure quality and cost of capital;

There is a gap between the empirical evidence and thetheoretical research;

What is the relation between cost of capital and investors’welfare?

Levitt“The truth is, high [accounting] standards lower the cost of capital.And that’s a goal we share.”

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Motivation

Regulators and firms are concerned about the welfareimpacts of disclosure quality;

The research has focused on the relation betweendisclosure quality and cost of capital;

There is a gap between the empirical evidence and thetheoretical research;

What is the relation between cost of capital and investors’welfare?

Levitt“The truth is, high [accounting] standards lower the cost of capital.And that’s a goal we share.”

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Motivation

Regulators and firms are concerned about the welfareimpacts of disclosure quality;

The research has focused on the relation betweendisclosure quality and cost of capital;

There is a gap between the empirical evidence and thetheoretical research;

What is the relation between cost of capital and investors’welfare?

Levitt“The truth is, high [accounting] standards lower the cost of capital.And that’s a goal we share.”

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

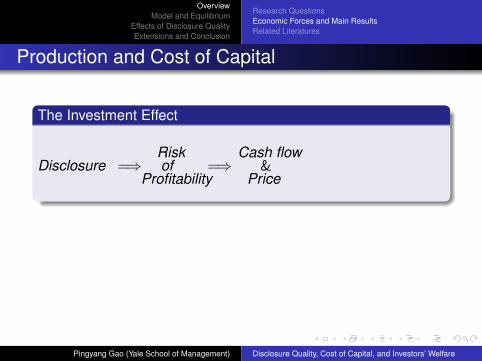

Production and Cost of Capital

The Investment Effect

Disclosure =⇒Riskof

Profitability=⇒

Cash flow&

Price

-Investment

Disclosure quality reduces cost of capital if and only if:the adjustment cost of new investment is sufficiently high,or the prior expected profitability of existing investment issufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Production and Cost of Capital

The Investment Effect

Disclosure =⇒Riskof

Profitability=⇒

Cash flow&

Price

-Investment

Disclosure quality reduces cost of capital if and only if:the adjustment cost of new investment is sufficiently high,or the prior expected profitability of existing investment issufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Production and Cost of Capital

The Investment Effect

Disclosure =⇒Riskof

Profitability=⇒

Cash flow&

Price

-Investment

Disclosure quality reduces cost of capital if and only if:the adjustment cost of new investment is sufficiently high,or the prior expected profitability of existing investment issufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

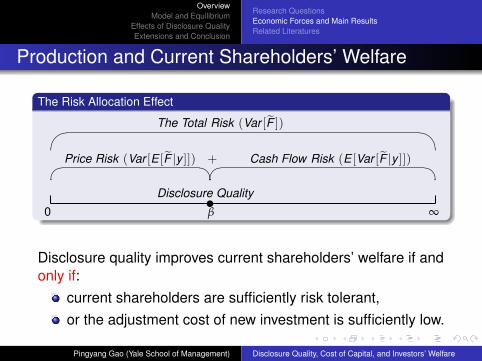

Production and Current Shareholders’ Welfare

The Risk Allocation Effect

0 ∞tβ

Disclosure Quality

The Total Risk (Var [F ])

Cash Flow Risk (E [Var [F |y ]]) Price Risk (Var [E [F |y ]]) +

Disclosure quality improves current shareholders’ welfare if andonly if:

current shareholders are sufficiently risk tolerant,or the adjustment cost of new investment is sufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Production and Current Shareholders’ Welfare

The Risk Allocation Effect

0 ∞tβ

Disclosure Quality

The Total Risk (Var [F ])

Cash Flow Risk (E [Var [F |y ]])

Price Risk (Var [E [F |y ]]) +

Disclosure quality improves current shareholders’ welfare if andonly if:

current shareholders are sufficiently risk tolerant,or the adjustment cost of new investment is sufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Production and Current Shareholders’ Welfare

The Risk Allocation Effect

0 ∞tβ

Disclosure Quality

The Total Risk (Var [F ])

Cash Flow Risk (E [Var [F |y ]]) Price Risk (Var [E [F |y ]]) +

Disclosure quality improves current shareholders’ welfare if andonly if:

current shareholders are sufficiently risk tolerant,or the adjustment cost of new investment is sufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Production and Current Shareholders’ Welfare

The Risk Allocation Effect

0 ∞tβ

Disclosure Quality

The Total Risk (Var [F ])

Cash Flow Risk (E [Var [F |y ]]) Price Risk (Var [E [F |y ]]) +

Disclosure quality improves current shareholders’ welfare if andonly if:

current shareholders are sufficiently risk tolerant,or the adjustment cost of new investment is sufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

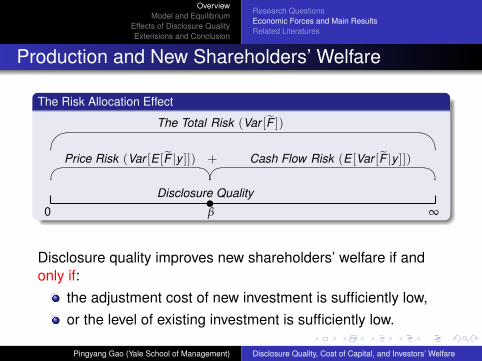

Production and New Shareholders’ Welfare

The Risk Allocation Effect

0 ∞tβ

Disclosure Quality

The Total Risk (Var [F ])

Cash Flow Risk (E [Var [F |y ]]) Price Risk (Var [E [F |y ]]) +

Disclosure quality improves new shareholders’ welfare if andonly if:

the adjustment cost of new investment is sufficiently low,or the level of existing investment is sufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Production and New Shareholders’ Welfare

The Risk Allocation Effect

0 ∞tβ

Disclosure Quality

The Total Risk (Var [F ])

Cash Flow Risk (E [Var [F |y ]]) Price Risk (Var [E [F |y ]]) +

Disclosure quality improves new shareholders’ welfare if andonly if:

the adjustment cost of new investment is sufficiently low,or the level of existing investment is sufficiently low.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Three Related Literatures

The relationship b/w disclosure quality and cost of capitalTheoretical: Easley and O’Hara (2004), Lambert, Leuz, andVerrecchia (2006, 2007), and Hughes, Liu and Liu (2007)Empirical: e.g., surveyed by Leuz and Wysocki (2007)

The welfare consequences of disclosure qualityEarly literature on Hirshleifer effect: e.g., Hirshleifer (1971),and Verrecchia (1982).Three subsequent literatures:

private information: e.g., Diamond (1985);imperfect competition: e.g., Kyle (1985);production: e.g., Kunkel (1982), Christensen and Feltham(1988), and Yee (2007).

The real effect of accounting disclosure in capital markete.g., Kanodia (1980, 2007).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Three Related Literatures

The relationship b/w disclosure quality and cost of capitalTheoretical: Easley and O’Hara (2004), Lambert, Leuz, andVerrecchia (2006, 2007), and Hughes, Liu and Liu (2007)Empirical: e.g., surveyed by Leuz and Wysocki (2007)

The welfare consequences of disclosure qualityEarly literature on Hirshleifer effect: e.g., Hirshleifer (1971),and Verrecchia (1982).Three subsequent literatures:

private information: e.g., Diamond (1985);imperfect competition: e.g., Kyle (1985);production: e.g., Kunkel (1982), Christensen and Feltham(1988), and Yee (2007).

The real effect of accounting disclosure in capital markete.g., Kanodia (1980, 2007).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Research QuestionsEconomic Forces and Main ResultsRelated Literatures

Three Related Literatures

The relationship b/w disclosure quality and cost of capitalTheoretical: Easley and O’Hara (2004), Lambert, Leuz, andVerrecchia (2006, 2007), and Hughes, Liu and Liu (2007)Empirical: e.g., surveyed by Leuz and Wysocki (2007)

The welfare consequences of disclosure qualityEarly literature on Hirshleifer effect: e.g., Hirshleifer (1971),and Verrecchia (1982).Three subsequent literatures:

private information: e.g., Diamond (1985);imperfect competition: e.g., Kyle (1985);production: e.g., Kunkel (1982), Christensen and Feltham(1988), and Yee (2007).

The real effect of accounting disclosure in capital markete.g., Kanodia (1980, 2007).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

1 OverviewResearch QuestionsEconomic Forces and Main ResultsRelated Literatures

2 Model and EquilibriumEvents, Utility, Cash Flow Function, and InformationThe Equilibrium

3 Effects of Disclosure QualityDisclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

4 Extensions and Conclusion

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

Time Line of Events and Utility Functions

t = 1The firm discloses a signalaccording to a stipulated

disclosure quality .

t = 2The firm makes new investmentand the current owner sellsthe firm to the new owner .

t = 3Investment pays off ;The new ownerconsumes.

Both the current and new owners have CARA utilityfunctions.

U(Wi) = −exp(−Wi

τi), i ∈ c, n

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

Time Line of Events and Utility Functions

t = 1The firm discloses a signalaccording to a stipulated

disclosure quality .

t = 2The firm makes new investmentand the current owner sellsthe firm to the new owner .

t = 3Investment pays off ;The new ownerconsumes.

Both the current and new owners have CARA utilityfunctions.

U(Wi) = −exp(−Wi

τi), i ∈ c, n

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

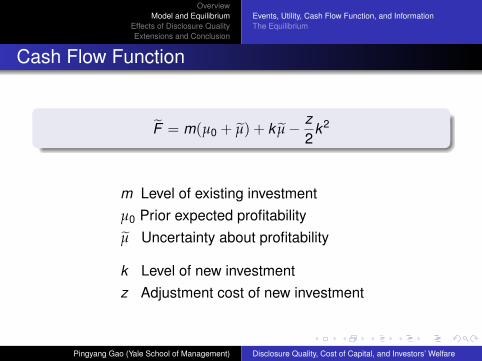

Cash Flow Function

F = m(µ0 + µ) + k µ− z2

k2

m Level of existing investmentµ0 Prior expected profitabilityµ Uncertainty about profitability

k Level of new investmentz Adjustment cost of new investment

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

Cash Flow Function

F = m(µ0 + µ) + k µ− z2

k2

m Level of existing investmentµ0 Prior expected profitabilityµ Uncertainty about profitability

k Level of new investmentz Adjustment cost of new investment

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

Cash Flow Function

F = m(µ0 + µ) + k µ− z2

k2

m Level of existing investmentµ0 Prior expected profitabilityµ Uncertainty about profitability

k Level of new investmentz Adjustment cost of new investment

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

The New Owner’s Information

µ: the source of uncertainty

Disclosure is a garbling of µ

y = µ + ε, ε ∼ N(0,1β)

β is the disclosure quality.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

The New Owner’s Information

µ: the source of uncertainty

Disclosure is a garbling of µ

y = µ + ε, ε ∼ N(0,1β)

β is the disclosure quality.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

Lemma 1: the Equilibrium

The new owner’s demand function:

D = τnE [F |Ω]− p(Ω)

Var [F |Ω], Ω = (y , k)

The price function:

p(Ω) = E [F |Ω]− 1τn

Var [F |Ω]

The firm’s optimal investment function:

k(y) =E [µ|y ]

z + 2τn

Var [µ|y ]−

2τn

Var [µ|y ]

z + 2τn

Var [µ|y ]m

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

Lemma 1: the Equilibrium

The new owner’s demand function:

D = τnE [F |Ω]− p(Ω)

Var [F |Ω], Ω = (y , k)

The price function:

p(Ω) = E [F |Ω]− 1τn

Var [F |Ω]

The firm’s optimal investment function:

k(y) =E [µ|y ]

z + 2τn

Var [µ|y ]−

2τn

Var [µ|y ]

z + 2τn

Var [µ|y ]m

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Events, Utility, Cash Flow Function, and InformationThe Equilibrium

Lemma 1: the Equilibrium

The new owner’s demand function:

D = τnE [F |Ω]− p(Ω)

Var [F |Ω], Ω = (y , k)

The price function:

p(Ω) = E [F |Ω]− 1τn

Var [F |Ω]

The firm’s optimal investment function:

k(y) =E [µ|y ]

z + 2τn

Var [µ|y ]−

2τn

Var [µ|y ]

z + 2τn

Var [µ|y ]m

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

1 OverviewResearch QuestionsEconomic Forces and Main ResultsRelated Literatures

2 Model and EquilibriumEvents, Utility, Cash Flow Function, and InformationThe Equilibrium

3 Effects of Disclosure QualityDisclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

4 Extensions and Conclusion

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Cost of Capital and the Variance-mean Ratio

E [R] =EF − P

P=

1τnV

FE

F

− 1

Lemma 2As disclosure quality improves,

EF increases monotonically;VF increases if and only if the adjustment cost of newinvestment is sufficiently low (V ′

F> 0 ⇐⇒ z < z∗).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Cost of Capital and the Variance-mean Ratio

E [R] =EF − P

P=

1τnV

FE

F

− 1

Lemma 2As disclosure quality improves,

EF increases monotonically;VF increases if and only if the adjustment cost of newinvestment is sufficiently low (V ′

F> 0 ⇐⇒ z < z∗).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Proposition 1

Proposition 1: Disclosure Quality and Cost of Capital

Disclosure quality increases cost of capital if and only if:the adjustment cost is sufficiently low (z < z∗), andthe prior expected profitability of existing investment issufficiently high (µ0 > µ∗0).

-

6

β

The Pure Exchange Economy

EF or VF

EF

VF(VFEF

)pe = Var [µ|y ]µ0 β-

6EF or VF

The CRTS Economy

EF

VF

(VFEF

)crts = τn2+ mµ0τn

Vcrts

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Proposition 1

Proposition 1: Disclosure Quality and Cost of Capital

Disclosure quality increases cost of capital if and only if:the adjustment cost is sufficiently low (z < z∗), andthe prior expected profitability of existing investment issufficiently high (µ0 > µ∗0).

-

6

β

The Pure Exchange Economy

EF or VF

EF

VF(VFEF

)pe = Var [µ|y ]µ0

β-

6EF or VF

The CRTS Economy

EF

VF

(VFEF

)crts = τn2+ mµ0τn

Vcrts

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Proposition 1

Proposition 1: Disclosure Quality and Cost of Capital

Disclosure quality increases cost of capital if and only if:the adjustment cost is sufficiently low (z < z∗), andthe prior expected profitability of existing investment issufficiently high (µ0 > µ∗0).

-

6

β

The Pure Exchange Economy

EF or VF

EF

VF(VFEF

)pe = Var [µ|y ]µ0 β-

6EF or VF

The CRTS Economy

EF

VF

(VFEF

)crts = τn2+ mµ0τn

Vcrts

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

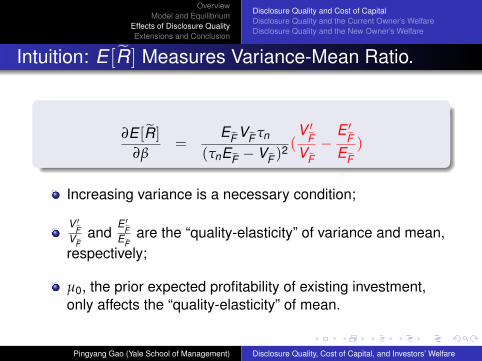

Intuition: E [R] Measures Variance-Mean Ratio.

∂E [R]∂β

=EF VF τn

(τnEF − VF )2 (V ′

FVF

−E ′

FEF

)

Increasing variance is a necessary condition;

V ′F

VFand

E ′F

EFare the “quality-elasticity” of variance and mean,

respectively;

µ0, the prior expected profitability of existing investment,only affects the “quality-elasticity” of mean.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: E [R] Measures Variance-Mean Ratio.

∂E [R]∂β

=EF VF τn

(τnEF − VF )2 (V ′

FVF

−E ′

FEF

)

Increasing variance is a necessary condition;

V ′F

VFand

E ′F

EFare the “quality-elasticity” of variance and mean,

respectively;

µ0, the prior expected profitability of existing investment,only affects the “quality-elasticity” of mean.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: E [R] Measures Variance-Mean Ratio.

∂E [R]∂β

=EF VF τn

(τnEF − VF )2 (V ′

FVF

−E ′

FEF

)

Increasing variance is a necessary condition;

V ′F

VFand

E ′F

EFare the “quality-elasticity” of variance and mean,

respectively;

µ0, the prior expected profitability of existing investment,only affects the “quality-elasticity” of mean.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: E [R] Measures Variance-Mean Ratio.

∂E [R]∂β

=EF VF τn

(τnEF − VF )2 (V ′

FVF

−E ′

FEF

)

Increasing variance is a necessary condition;

V ′F

VFand

E ′F

EFare the “quality-elasticity” of variance and mean,

respectively;

µ0, the prior expected profitability of existing investment,only affects the “quality-elasticity” of mean.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Empirical Implications: Part 1

Disclosure quality increases the cost of capital when theadjustment cost of new investment is sufficiently low andthe general economic outlook is optimistic;

Disclosure quality increases the risk of a firm’s cash flowwhen the adjustment cost of new investment is sufficientlylow;

More empirical research on how disclosure quality affectsthe firm’s investment decisions could facilitate the tests(e.g., Verdi (2006)).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Empirical Implications: Part 1

Disclosure quality increases the cost of capital when theadjustment cost of new investment is sufficiently low andthe general economic outlook is optimistic;

Disclosure quality increases the risk of a firm’s cash flowwhen the adjustment cost of new investment is sufficientlylow;

More empirical research on how disclosure quality affectsthe firm’s investment decisions could facilitate the tests(e.g., Verdi (2006)).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Empirical Implications: Part 1

Disclosure quality increases the cost of capital when theadjustment cost of new investment is sufficiently low andthe general economic outlook is optimistic;

Disclosure quality increases the risk of a firm’s cash flowwhen the adjustment cost of new investment is sufficientlylow;

More empirical research on how disclosure quality affectsthe firm’s investment decisions could facilitate the tests(e.g., Verdi (2006)).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Definition and Results

The current owner’s welfare is her expected utility beforedisclosure.

Proposition 2: Disclosure Quality and Current Owner’s WelfareDisclosure quality makes the current owner worse off if andonly if:

the current owner is sufficiently risk averse relative to thenew owner (τc < τn

2 ), andthe adjustment cost of new investment is sufficiently high(z > z∗c ).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Definition and Results

The current owner’s welfare is her expected utility beforedisclosure.

Proposition 2: Disclosure Quality and Current Owner’s WelfareDisclosure quality makes the current owner worse off if andonly if:

the current owner is sufficiently risk averse relative to thenew owner (τc < τn

2 ), andthe adjustment cost of new investment is sufficiently high(z > z∗c ).

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: Trade-off of the Dual Effects

Welfare of the Risk Allocation Effect

CEc = P − 12τc

Var [p(y)]

= µ0 −1τn

Var [µ|y ]︸ ︷︷ ︸Cash Flow Risk

− 12τc

Var [E [µ|y ]]︸ ︷︷ ︸Price Risk

= µ0 −1

2τc

1α

+ (1

2τc− 1

τn)

1α + β

Welfare of the Investment Effect

E [U(Wc)] = − 1√1 + 1

2τcP

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: Trade-off of the Dual Effects

Welfare of the Risk Allocation Effect

CEc = P − 12τc

Var [p(y)]

= µ0 −1τn

Var [µ|y ]︸ ︷︷ ︸Cash Flow Risk

− 12τc

Var [E [µ|y ]]︸ ︷︷ ︸Price Risk

= µ0 −1

2τc

1α

+ (1

2τc− 1

τn)

1α + β

Welfare of the Investment Effect

E [U(Wc)] = − 1√1 + 1

2τcP

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

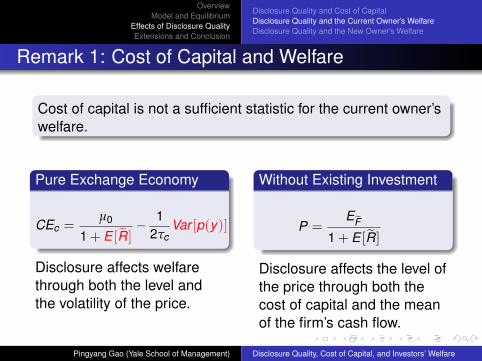

Remark 1: Cost of Capital and Welfare

Cost of capital is not a sufficient statistic for the current owner’swelfare.

Pure Exchange Economy

CEc =µ0

1 + E [R]− 1

2τcVar [p(y)]

Disclosure affects welfarethrough both the level andthe volatility of the price.

Without Existing Investment

P =EF

1 + E [R]

Disclosure affects the level ofthe price through both thecost of capital and the meanof the firm’s cash flow.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Remark 1: Cost of Capital and Welfare

Cost of capital is not a sufficient statistic for the current owner’swelfare.

Pure Exchange Economy

CEc =µ0

1 + E [R]− 1

2τcVar [p(y)]

Disclosure affects welfarethrough both the level andthe volatility of the price.

Without Existing Investment

P =EF

1 + E [R]

Disclosure affects the level ofthe price through both thecost of capital and the meanof the firm’s cash flow.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Remark 1: Cost of Capital and Welfare

Cost of capital is not a sufficient statistic for the current owner’swelfare.

Pure Exchange Economy

CEc =µ0

1 + E [R]− 1

2τcVar [p(y)]

Disclosure affects welfarethrough both the level andthe volatility of the price.

Without Existing Investment

P =EF

1 + E [R]

Disclosure affects the level ofthe price through both thecost of capital and the meanof the firm’s cash flow.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Proposition 3: Disclosure Quality and New Owner’s WelfareAs disclosure quality increases, the new owner is worse off ifand only if m and z are in the blank area.

0 0

β < α β > α

m∗n m∗

n

s sz∗n z∗n ss

sz∗∗n

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

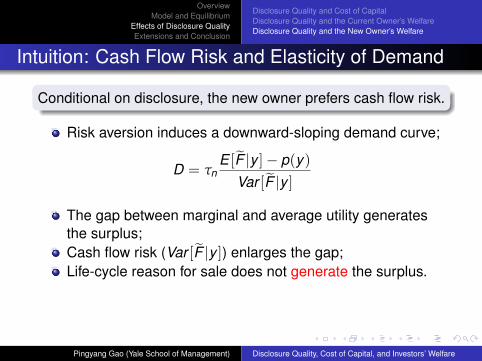

Intuition: Cash Flow Risk and Elasticity of Demand

Conditional on disclosure, the new owner prefers cash flow risk.

Risk aversion induces a downward-sloping demand curve;

D = τnE [F |y ]− p(y)

Var [F |y ]

The gap between marginal and average utility generatesthe surplus;Cash flow risk (Var [F |y ]) enlarges the gap;Life-cycle reason for sale does not generate the surplus.

Before disclosure, the new owner is also averse to the volatilityin his conditional utility.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: Cash Flow Risk and Elasticity of Demand

Conditional on disclosure, the new owner prefers cash flow risk.

Risk aversion induces a downward-sloping demand curve;

D = τnE [F |y ]− p(y)

Var [F |y ]

The gap between marginal and average utility generatesthe surplus;Cash flow risk (Var [F |y ]) enlarges the gap;Life-cycle reason for sale does not generate the surplus.

Before disclosure, the new owner is also averse to the volatilityin his conditional utility.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: Cash Flow Risk and Elasticity of Demand

Conditional on disclosure, the new owner prefers cash flow risk.

Risk aversion induces a downward-sloping demand curve;

D = τnE [F |y ]− p(y)

Var [F |y ]

The gap between marginal and average utility generatesthe surplus;

Cash flow risk (Var [F |y ]) enlarges the gap;Life-cycle reason for sale does not generate the surplus.

Before disclosure, the new owner is also averse to the volatilityin his conditional utility.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: Cash Flow Risk and Elasticity of Demand

Conditional on disclosure, the new owner prefers cash flow risk.

Risk aversion induces a downward-sloping demand curve;

D = τnE [F |y ]− p(y)

Var [F |y ]

The gap between marginal and average utility generatesthe surplus;Cash flow risk (Var [F |y ]) enlarges the gap;

Life-cycle reason for sale does not generate the surplus.

Before disclosure, the new owner is also averse to the volatilityin his conditional utility.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: Cash Flow Risk and Elasticity of Demand

Conditional on disclosure, the new owner prefers cash flow risk.

Risk aversion induces a downward-sloping demand curve;

D = τnE [F |y ]− p(y)

Var [F |y ]

The gap between marginal and average utility generatesthe surplus;Cash flow risk (Var [F |y ]) enlarges the gap;Life-cycle reason for sale does not generate the surplus.

Before disclosure, the new owner is also averse to the volatilityin his conditional utility.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Intuition: Cash Flow Risk and Elasticity of Demand

Conditional on disclosure, the new owner prefers cash flow risk.

Risk aversion induces a downward-sloping demand curve;

D = τnE [F |y ]− p(y)

Var [F |y ]

The gap between marginal and average utility generatesthe surplus;Cash flow risk (Var [F |y ]) enlarges the gap;Life-cycle reason for sale does not generate the surplus.

Before disclosure, the new owner is also averse to the volatilityin his conditional utility.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Remark 2: Cost of Capital and Welfare

Cost of capital is not a sufficient statistic for the new owner’swelfare, either.

Table 2: Effects of Disclosure Quality on Cost of Capital and Welfare

Cost of Current Owner ′s New Owner ′sEconomies Capital Welfare Welfare

General Economy Increase /Decrease♥ Increase/Decrease♣ Increase/Decrease♠

Pure Exchange Decrease Increase/Decrease Decrease

No Endowment Decrease Increase Increase/Decrease

CRTS Increase Increase Increase

Note: Conditions of ♥, ♣, and ♠ differ from and do not subsume each other.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Remark 2: Cost of Capital and Welfare

Cost of capital is not a sufficient statistic for the new owner’swelfare, either.

Table 2: Effects of Disclosure Quality on Cost of Capital and Welfare

Cost of Current Owner ′s New Owner ′sEconomies Capital Welfare Welfare

General Economy Increase /Decrease♥ Increase/Decrease♣ Increase/Decrease♠

Pure Exchange Decrease Increase/Decrease Decrease

No Endowment Decrease Increase Increase/Decrease

CRTS Increase Increase Increase

Note: Conditions of ♥, ♣, and ♠ differ from and do not subsume each other.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Empirical Implications: Part 2

Be careful to infer prescriptive suggestions from the resultsabout the relationship between disclosure quality and costof capital;

Firms commit to high disclosure quality if the adjustmentcost of new investment is sufficiently low or current ownersare sufficiently risk tolerant;

Exchanges and legal regimes with differential disclosurerequirements could attract distinct clienteles.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Empirical Implications: Part 2

Be careful to infer prescriptive suggestions from the resultsabout the relationship between disclosure quality and costof capital;

Firms commit to high disclosure quality if the adjustmentcost of new investment is sufficiently low or current ownersare sufficiently risk tolerant;

Exchanges and legal regimes with differential disclosurerequirements could attract distinct clienteles.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Disclosure Quality and Cost of CapitalDisclosure Quality and the Current Owner’s WelfareDisclosure Quality and the New Owner’s Welfare

Empirical Implications: Part 2

Be careful to infer prescriptive suggestions from the resultsabout the relationship between disclosure quality and costof capital;

Firms commit to high disclosure quality if the adjustmentcost of new investment is sufficiently low or current ownersare sufficiently risk tolerant;

Exchanges and legal regimes with differential disclosurerequirements could attract distinct clienteles.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Extensions

The model could survive diversification;

Other definitions of cost of capital do not affect the mainresults;

The main conclusions still hold if disclosure reducesinformation asymmetry among new investors.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Extensions

The model could survive diversification;

Other definitions of cost of capital do not affect the mainresults;

The main conclusions still hold if disclosure reducesinformation asymmetry among new investors.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Extensions

The model could survive diversification;

Other definitions of cost of capital do not affect the mainresults;

The main conclusions still hold if disclosure reducesinformation asymmetry among new investors.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Conclusion

Disclosure quality could increase cost of capital in thepresence of the investment effect;

There are plausible conditions under which disclosurequality reduces the welfare of both current and newshareholders;

Cost of capital is not a sufficient statistic for the welfare ofeither current or new shareholders in the analysis of theeconomic consequences of disclosure quality.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Conclusion

Disclosure quality could increase cost of capital in thepresence of the investment effect;

There are plausible conditions under which disclosurequality reduces the welfare of both current and newshareholders;

Cost of capital is not a sufficient statistic for the welfare ofeither current or new shareholders in the analysis of theeconomic consequences of disclosure quality.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare

OverviewModel and Equilibrium

Effects of Disclosure QualityExtensions and Conclusion

Conclusion

Disclosure quality could increase cost of capital in thepresence of the investment effect;

There are plausible conditions under which disclosurequality reduces the welfare of both current and newshareholders;

Cost of capital is not a sufficient statistic for the welfare ofeither current or new shareholders in the analysis of theeconomic consequences of disclosure quality.

Pingyang Gao (Yale School of Management) Disclosure Quality, Cost of Capital, and Investors’ Welfare