die billionen schuldenbombe

DESCRIPTION

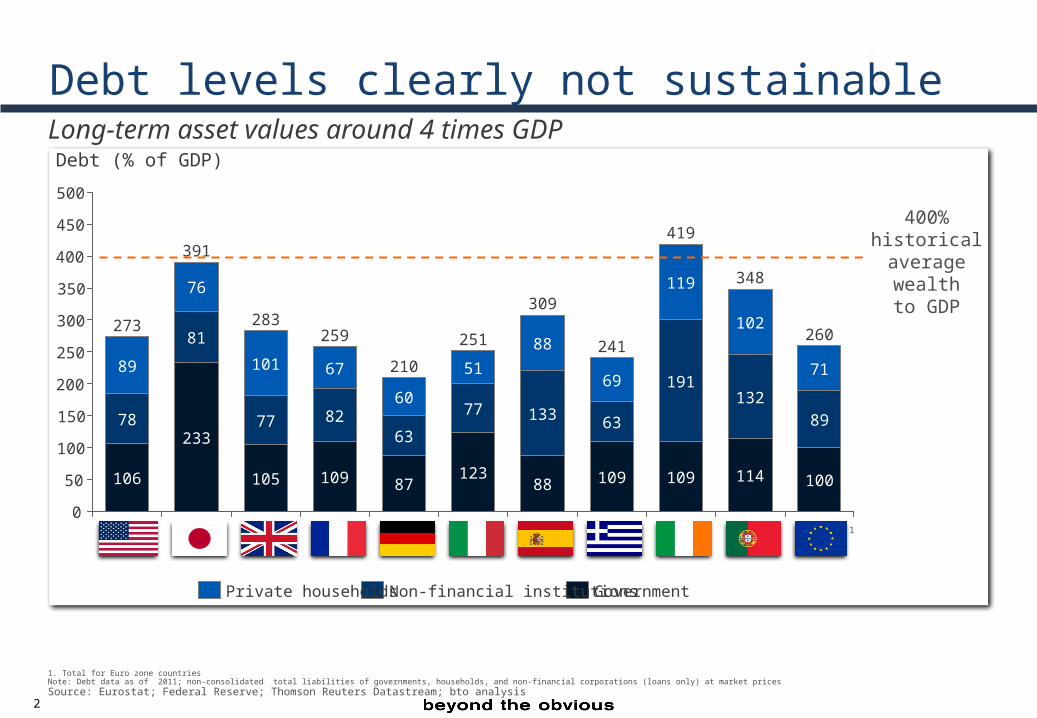

Die Billionen Schuldenbombe. Dr. Daniel Stelter. Debt levels clearly not sustainable. Long-term asset values around 4 times GDP. Debt (% of GDP). 500. 450. 419. 400% historical average wealth to GDP. 391. 400. 348. 119. 76. 350. 309. 283. 300. 102. 273. 260. 259. 81. - PowerPoint PPT PresentationTRANSCRIPT

Die Billionen Schuldenbom

beDr. Daniel Stelter

2

Debt levels clearly not sustainableLong-term asset values around 4 times GDP

1. Total for Euro zone countriesNote: Debt data as of 2011; non-consolidated total liabilities of governments, households, and non-financial corporations (loans only) at market pricesSource: Eurostat; Federal Reserve; Thomson Reuters Datastream; bto analysis

200

500

450

400

350

300

250

0

150

100

50

260

100

8960

259

109

82

67

283

105

77

101

391

233

81

69

309

88

133

88251

123

77

51210

87

63

71

348

114

132

102

419

109

191

119

241

109

63

Debt (% of GDP)

76

273

106

78

89

GovernmentNon-financial institutionsPrivate households

400% historicalaverage wealthto GDP

1

3

Not to talk about hidden liabilities …Public gross debt/GDP prediction

Source: Source: "The future of public debt: prospects and implications", BIS Working Paper, March 2010

FranceGermany

1980 2000 2020 2040

600

0

400

200

1980 2000 2020 2040

Small gradual adjustment with age-related spending held constant at level of 2011 (in % of GDP)

Small gradual adjustment (fiscal balance improves by 1 percentage point of GDP over the next 5 years)

No change in fiscal policy and age-related spending

US Japan UK

1980 2000 2020 2040

600

0

400

200

1980 2000 2020 2040 1980 2000 2020 2040

4

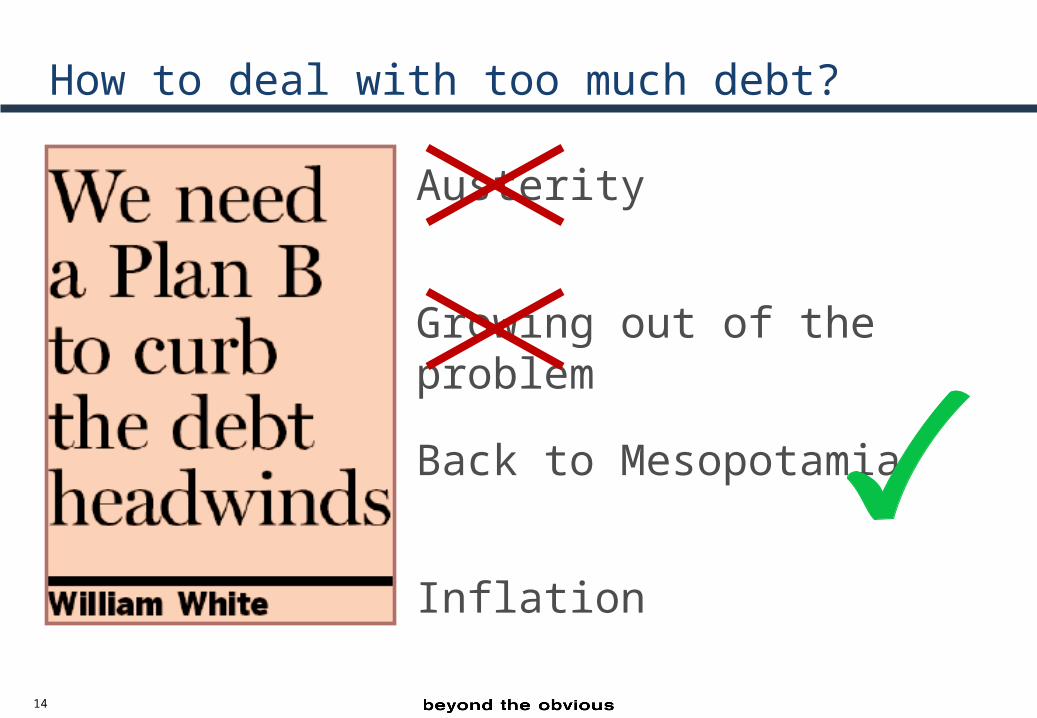

How to deal with too much debt?

Austerity

5

Austerity at workGreece in numbers

1. Forecasted nominal value (market value is used in all other analyses) 2. Before repurchase of government bonds in January 2013Source: National Statistical Service of Greece; Eurostat; Greek Ministry of Finance (Public Debt Bulletin June 2012); Eurostat; Transparency International; Wall Street Journal;

Bloomberg; bto analysis

First110

Second

130

First110

Second

130

Debtrelief107

233

4265

88

186

240

108

345356

NominalGDP

(2008)

NominalGDP

(2011)

Publicdebt

(2011)1

Publicdebt

(2012)2

Bailouts(so far)

Publicexpenditures

(2011)

Publicrevenue(2011)

Blackmarket(2009)

Deposit flight(Aug 2011—

Jul 202)

0

100

200

300

400

in billion €

A significant part of the economy is not counted in

official statistics and does not bring tax revenues

5

Public revenues shrink faster than

expenditures

4

Two bailouts have already been

necessary

3

Debtrelief107-47

-11

-20

Shrinking GDP makes debt re-payment even

more difficult

1

Even a 30% debt relief does not

really help

2

The population tries to rescue their

savings

6

6

How to deal with too much debt?

Austerity

Growing out of the problem

7

Note: Historical estimates of World Population estimates reflect "lower estimates" of US Census Bureau. Data by 2009 from US Census Bureau, starting 2010 from UN World Population ProspectsSource: US. Census Bureau, Historical Estimates of World Population, 2012; United Nations, Department of Economic and Social Affairs, Population Division (2011). World Population Prospects: The 2010 Revision; Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315, http://www.nber.org/papers/w18315

The growth formula is brokenEconomic growth = workforce × productivity

Population evolution …

Highest growth from 1950–2000 of ~1.75% p.a.

200018001600140012001000800600400110000

World population in million 10,000 BC–2100 AD –2100 AD

10,000

5,000

0

+0.9%

+0.5%

+0.1% CAGR

… GDP growth per capita

Actual UK

Actual US

2.5

Percent p.a.3.0

2000

2.0

1.5

1.0

0.5

0.021001900180017001600150014001300

8

Headwinds for further productivity gain

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315, http://www.nber.org/papers/w18315

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315, http://www.nber.org/papers/w18315

Innovation with less impact on productivity than in the past

The West is falling behind on education

Intensified international competition increases labor cost pressure

Efforts to reduce CO2/the end of cheap resources

Underinvestment in assets by public and private sector

Increased income inequality

3.0

2.5

2.0

1.5

1.0

0.5

0.01300 1400 1500 1600 1700 1800 1900 2000 2100

Percent per year

Actual UK

Actual US

Hypothetical path

9

Debt above 90% of GDP leads to lower growth rates

1. GOV = public debt (gross liabilities) 2. NFC = Non financial corporations (total liabilities less shares and other equity) 3. HH = household debt (gross liabilities)Note: All data as of 2011SSource: BIS; Eurostat; national central banks; Thomson Reuters Datastream; bto analysis

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315, http://www.nber.org/papers/w18315

GOV

Total

71–100% debt/GDP >100% debt/GDP0–70% debt/GDP

HH

NFC

10

How to deal with too much debt?

Austerity

Growing out of the problem

Back to Mesopotamia

11

1. Total for Euro zoneNote: Debt data as of 2011Non-consolidated total liabilities of governments, households, and non-financial corporations (loans only) at market pricesSource: Eurostat; Federal Reserve; Thomson Reuters Datastream; bto analysis

Back to Mesopotamia?

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315, http://www.nber.org/papers/w18315

Including haircut

7661,568 1,122 1271,367287380 7,388 10,810 1,8619,936

Debt overhang (B€)

0

50

100

150

200

250

300

350

400

450

500Debt (% of GDP)

180% threshold

1

100

71

260

89

114

102

348

132

123

51

251

77

109

69

63

241

88

88

309

133

106

89

273

78233

76

391

81

109

119

191

419

105

101

77

283

109

67

259

82

87

60

63

210

GovernmentNon-financial institutionsPrivate households

12

1. Total for Euro zoneNote: Debt data as of 2011Non-consolidated total liabilities of governments, households, and non-financial corporations (loans only) at market pricesSource: Eurostat; Federal Reserve; Thomson Reuters Datastream; bto analysis

Significant hit for savers

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315, http://www.nber.org/papers/w18315

125

100

75

50

25

0

-25

53

47

100

-23

72

28

61

39

84

16

48

52

69

31

61

39

19

81

26

74

-22

100

Remaining household financial assetsHousehold financial assets needed for debt reduction

Japan's and

Ireland's househol

d financial assets

less than necessar

y for debt

reduction

Including haircut

7661,568 1,122 1271,367287380 7,38810,810 1,8619,936

Necessary debt reduction and remaining HH financial assets (%)

Debt overhang (B€)

1

13

Cyprus = Mesopotamia

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315, http://www.nber.org/papers/w18315

Source: Financial Times, 26 March 2013, Economist "The Cypriot deal: Second time unlucky", 30 March 2013

14

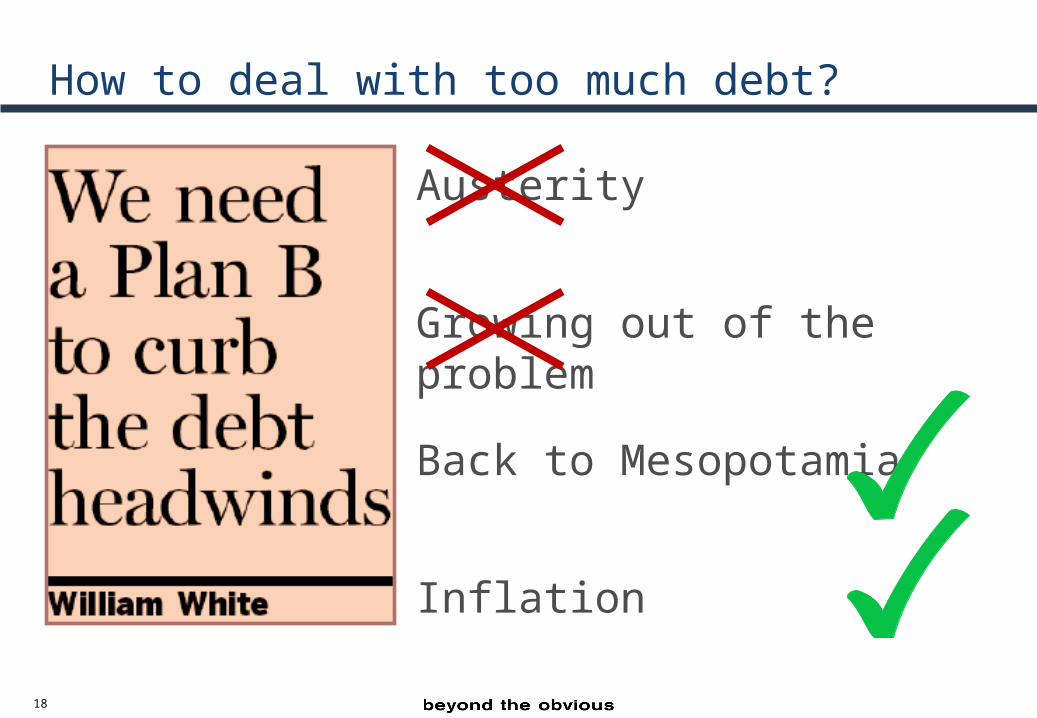

How to deal with too much debt?

Austerity

Growing out of the problem

Back to Mesopotamia

Inflation

15

Financial repression?

Note: 2011 data, Portugal interest paid as of 2010Non-consolidated total liabilities of governments, households, and non-financial corporations (loans only) at market pricesSource: OECD; bto analysis

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315,

http://www.nber.org/papers/w18315

Number of years to reach 180% threshold

-0.60.3 1.02.1 5.91.4-0.9-0.6-0.6

Interest rate – GDP growth = -5 Interest rate – GDP growth = -1

Actual 2011Interest rate– GDP growth

0

20

40

60

80

100

16

The idea of helicopter money is gaining popularity

Source: The Economist; Financial Times; Irish Times; bto analysis

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315,

http://www.nber.org/papers/w18315

Let us suppose that one day a helicopter flies over this community and drops an additional $1000 in bills from the sky, which is, of course hastily collected by members of the community …Milton FriedmanThe Optimum Quantity of Money, Chapter 11969

Today I will argue for a different approach and suggest that the Bank of Japan cooperate temporarily with the government to create an environment of combined monetary and fiscal ease to end deflation and help restart economic growth in Japan.

Ben BernankeSpeech before the Japan Society of Monetary EconomicsTokyo, May 31, 2003

… in some extreme circumstances— those in which there is a simultaneous and significant fall in both the price level and real output—it is unambiguously clear that OMF would be the best policy, and in some circumstances may be the only policy available to prevent continual deflation.

Adair Turner Financial Services Authority Chairman, Lecture at the Cass Business School, London, February 6, 2013

17

Just retire the QE debt?

Source: Financial Times, 11 March 2012, page 9

Source: Robert Gordon, "Is U.S. economic growth over? Faltering innovation confronts the six headwinds", NBER Working Paper 18315,

http://www.nber.org/papers/w18315

After buying £325B of debt from the market, the public

sector (the Treasury) is paying interest to itself (the BoE) on debt that it owes to itself.

Instead of selling the debt back into the market, theBoE can retire the debt. At a stroke, £325bn of UK

government debt disappears. If the US follows suit, about $1.5T of US government debt will be retired.

The main obstacle to retiring the debt lies with themarkets and credit rating agencies. They may see this as

a slide towards Weimar Republic economics: monetary financing of government debt by printing money. Consequently, both the BoE and the Treasury cannot be seen to advocate retiring QE-acquired debt at this stage.

18

How to deal with too much debt?

Austerity

Growing out of the problem

Back to Mesopotamia

Inflation

Die Billionen-SchuldenbombeWie die Krise begann und warum sie noch lange nicht zu Ende ist