diagnostic world asia - apac ivd outlook 2010

TRANSCRIPT

1N5DF-55

Opportunities and Growth Strategies for the APAC IVD Industry

2N5DF-55

Contents

Diagnostics

Industry

Briefing 3.

2.

1. APAC Market Outlook

Industry Best Practices and Growth Strategies

360 Degree Global Perspective

3

Setting the Scene Outlook for Healthcare Industry from 2010-12

Source: Frost & Sullilvan ,2010)

Global Healthcare Market : 2009

• US and Europe were impacted in a major way by global crisis

• Asia also slowed down but not as much as the West

• Valuations were low and M&A was high, many smaller Biotech companies struggled

• Major organizational restructuring occurred, along with portfolios being reassessed

Global Healthcare Market : 2010-12

• Recovery of the markets to a large extent with strong growth in Asia

• Start of major patent expiries

• M&A activity down in the West but could be important in Asia, restructuring will continue

• Asia becoming increasingly important as a market and outsourcing hub

• 5Ps to drive market: Preventive, Preemptive, Personalized, Predictive, Personal Responsibility

4

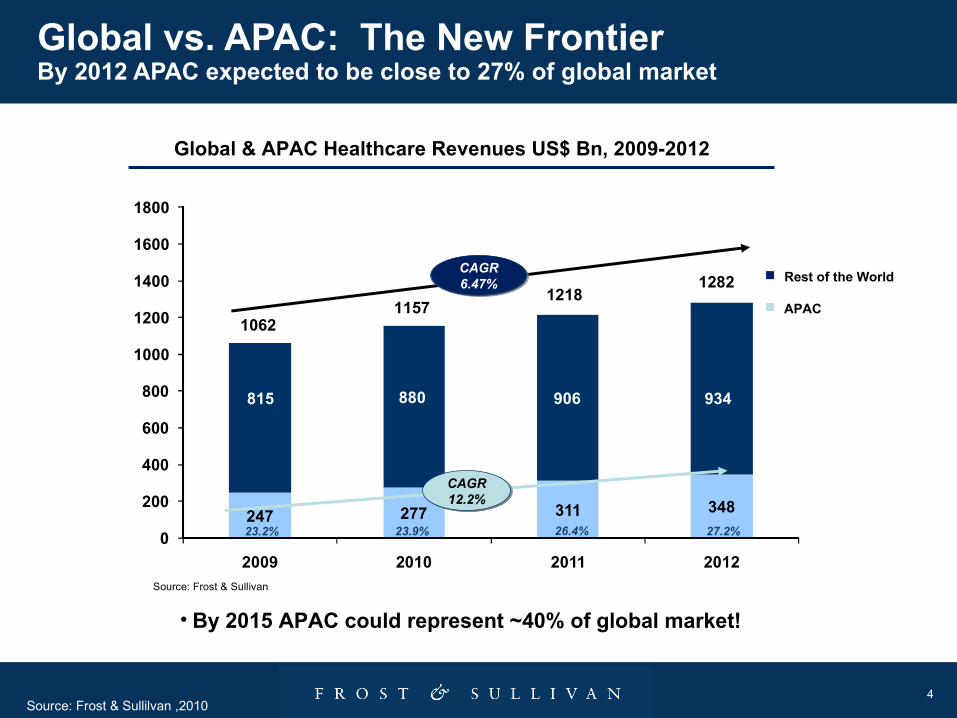

Global vs. APAC: The New FrontierBy 2012 APAC expected to be close to 27% of global market

Source: Frost & Sullilvan ,2010)

247 277 311 348

815 880 906 934

0

200

400

600

800

1000

1200

1400

1600

1800

2009 2010 2011 2012

10621157

12181282

23.9% 27.2%23.2% 26.4%

CAGR12.2%

CAGR6.47%

Global & APAC Healthcare Revenues US$ Bn, 2009-2012

• By 2015 APAC could represent ~40% of global market!

Source: Frost & Sullivan

Rest of the World

APAC

5

Asia is however transitioningMoving toward a Multi–Polar World Order

Source: Frost & Sullilvan ,2010)

Asia Pacific Market : 2009

• Slowing down of GDP in mature markets – Japan and Australia took a big hit

• Global consolidation left a difficult mess for integration on a local level – job losses and portfolio realignment

• Price cutting and playing the margins game

• Slow down for Medical Tourism

• Asia started to set up infrastructure for offshoring and outsourcing for US/EU companies

Asia Pacific Market : 2012

• A shift in the center of the world economically and strategically to Asia

• Asia to move from export led development to consumption led growth

• APAC the fastest growing pharma market and API production hub

• Increased government attention to primary and community based healthcare.

• Focus on building infrastructure and education: government role will be higher

• Increased use of mobile technology in healthcare service delivery

6

Note: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

APAC Clinical Diagnostics Market Shift in business model from instrumentation to service revenues

6.9 7.3 7.8 8.5

31.7 33.6 35.6 37.5

0

10

20

30

40

50

60

2009 2010 2011 2012

Rest of the World

APAC

38.640.9

43.446

17.8% 18.5%

Market Drivers

Market Restraints

Lab automation

Home care monitoring

Emphasis on early detection

High cost of genomics and proteomics tests

Mutually exclusive target customers

Reimbursement issues

Clinical Diagnostics Revenues, US$ Bn, 2009-2012

APAC Share

CAGR7.3%

CAGR6%

7

0

0APAC Molecular Diagnostics market 2010: ~US$ 700 mn; CAGR ~18%.Driven by rise in cancer, STD, thyroid disorder and other autoimmune

diseases

MolecularDiagnostics

POCT

SMBG

Top Growth Opportunities : APAC Clinical Diagnostics Market

APAC POCT market 2010 : ~US$ 539 mn; CAGR ~10.8%POCT testing focused on cardiac and diabetes care in secondary

settings

APAC SMBG market 2010 : ~US$ 1.7 bn; CAGR ~10.9% Focus on growing Asian ageing population and prevalence of diabetes

Source: Frost & Sullivan.

8

Contents

Diagnostics

Industry

Briefing 3.

2.

1. APAC Market Outlook

Industry Opportunities and Growth Strategies

360 Degree Perspective

9N5DF-55

Global Perspective

1. Reference Labs and CROs Expand Services to Developing Countries.

3. Increased R&D Outsourcing by Pharma & Biotech Companies

5. Earlier Launch of Diagnostic Tests in the Asian/European Markets

7. Changing Global Trends Drive Adoption of New Technologies.

9. Funding opportunities, primary customer base and research strengths are differentiated in the APAC region

GLOBAL

Political&

Regulatory

EmergingOpportunitiesCultural

CEO

10N5DF-55

REFERENCE LAB TESTING EXPANDING TO DEVELOPING WORLD

Advanced Markets

Reference labs based in the U.S.,such as Quest Diagnostics Inc., are looking for high growth Asian markets

India

India has growing middle class with increasing buying power and demand for better healthcare services.

China

China has a growing aging population and increasing healthcare spending.

India, China and S. Korea have some of the highest growth rates for healthcare spending in APAC and along with the growing aging population and middle class, represent attractive markets for clinical testing. Additionally, the increased prevalence of lifestyle diseases such as diabetes, cardiovascular diseases, and certain cancers contributes to the increasing need of testing.

U.S. based national reference laboratories have already taken the lead to expand into these growing markets. Global expansion of clinical lab testing is likely to be influenced by innovation, cost and readiness of the countries.

Reference Labs Expand Services to Developing Countries

11N5DF-55

High Data Output

Consolidation and Standardization

of LIMS

Outsource

to M

ultiple C

ROs

Extended Sample

Management

Independent Functional

ModulesSample

Management

Application Integration

Quality Assurance

Competency Management

Inventory Management

Increased R&D Outsourcing by Pharma and Biotech Companies

12N5DF-55

Earlier Launch of Diagnostic Tests in the Asian Markets

12

20082008 Test Development

Asian/E.U. Launch

20122012U.S. Market Launch

LEARNING, KNOW-HOW FROM TESTS LAUNCHED IN ASIA/EU CAN EXPEDITE FDA CLEARANCE AND U.S. LAUNCH

20112011

20132013

U.S.

Diagnostics assay development done at a U.S. R&D facility is likely to benefit from clinical data generated from use of tests in APAC countries.

India

Large market, low operating costs, and excellent local skills allow for low set up costs and ease of technology adoption leading to high revenues.

China

Tests launched in China and clinical data generated from them can be used to improve standardization of tests.

13N5DF-55

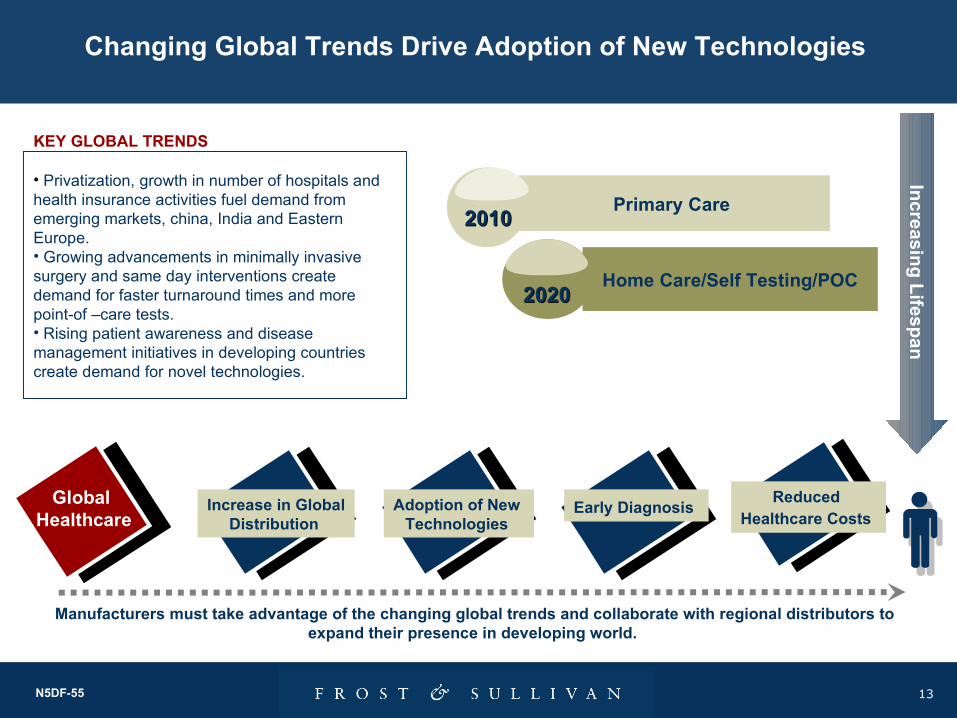

Changing Global Trends Drive Adoption of New Technologies

Primary Care 20102010

Home Care/Self Testing/POC20202020

Global Healthcare

Reduced Healthcare Costs

Increase in GlobalDistribution

Early Diagnosis Adoption of New Technologies

Increasin

g L

ifespan

Manufacturers must take advantage of the changing global trends and collaborate with regional distributors to expand their presence in developing world.

• Privatization, growth in number of hospitals and health insurance activities fuel demand from emerging markets, china, India and Eastern Europe. • Growing advancements in minimally invasive surgery and same day interventions create demand for faster turnaround times and more point-of –care tests. • Rising patient awareness and disease management initiatives in developing countries create demand for novel technologies.

KEY GLOBAL TRENDS

14N5DF-55

Singapore and Korea are building up

strong government

supported public sector research

Australia and Malaysia

encouraging private sector

research

Genomics Hot-spots

Oncology Hot-Spots

Manufacturers should invest in implementation and provide multiple financing options

Increased implementation of new technologies requires more training programs andstreamlining workflow

Low manufacturing costs in APAC

increases pricingcompetition within Western countries

Differentiated Funding Opportunities, Primary Customer Base and Research Strengths in the APAC Region Shape Implementation Strategies

Australia

Japan

Singapore

Korea

15N5DF-55

Integrated Industry Perspective

FluctuatingRaw Material

Levels

Material Costs

Maintain Capital

SupplierRelationships

CEO

INTEGRATED INDUSTRY

Secure Capital

2. Key Areas Spurs Integration of Pharmaceutical and Diagnostic Companies

4. Incorporation of Information Technology is the New Business Model.

6. The vertical alignment trend in the healthcare sector is affecting the clinical diagnostic sector as well, and will strongly impact the healthcare industry as a whole.

16N5DF-55

Integration of Pharmaceutical and Diagnostic Companies is the Next Move

TargetQualification

CompoundScreening

LeadOptimization

Pharma/toxAnalysis

Clinical Phase FDA Post-Market

BiomarkerIdentification

AssayDevelopment FDA

Assay LaunchStandardization& Validation

$9.5 Million-------------$14.5 Million------------$12.0 Million-----------$ 40Million Diagnostic/Device R&D Costs (U.S.) 2008, ~$40 million/Test

Tech-PlatformOptimization

Average Drug Development Cost = $1.2 Billion/ drug

Average Diagnostic Development Cost = $40 million/test

Four areas that will integrate pharmaceutical and diagnostic manufacturers arepharmacogenomics, development of biomarker assays, comprehensive disease

management programs and more applied, focused clinical trials

17N5DF-55

Incorporation of Information Technology is the New Business Model

2010

Next Generation Integrated Systems

20152015

Broader Data

Management

Tools

Patient Support

Tools

Shareable Personal Health Records

Web Portalsto EHR Systems

Electronic Management

of Sample Transport

Reduced Cost of

Logistics

Essential Part of Clinical Diagnostics

Business

18N5DF-55

The Vertical Alignment in the Healthcare Sector Impacts Clinical Diagnostics

Diagnostic Labs

Hospital and Clinics

Healthcare Insurance Company

Ver

tica

l Ali

gn

men

t

Diagnostic Labs

Hospital and Clinics

Healthcare Insurance Company

Interoperability

Healthcare Insurance Company

Hospital and Clinics Diagnostic Labs

Increasing Opportunities for Suppliers and IT Infrastructure Providers

19N5DF-55

Technology Perspective

NewApplications

DisruptiveTechnologies

TECHNOLOGYEmerging

Technology

CEO

• Clinical Sample Management Will Take Center Stage.

• Non-invasive Testing and Pre-natal diagnostics Will be High Priority

6. Changing market demands from R&D Sites

20N5DF-55

Clinical Sample Management Will Take Center Stage

Efficient storage systems

to aid testoutsourcing

Use of non-invasiveCollection methods

With degree of sophistication in clinical sample handling, clinical diagnostics will witness

growth in developing countries

Use of chemical techniques

to store samples

Use of nanofluidics to improve workflow

Use of non-invasivecollection methods

ClinicalSample

Volume optimization

Transportation

Storage

Collection

21N5DF-55

Non-invasive Testing and Prenatal Diagnostics Drive Growth

MicroarrayM

Icro

flu

idic

s/N

ano

dia

gn

ost

ics

Non-invasive

technologies

Biomarker Discovery

Improved Sample

Management and Workflow

Point-of-Care Diagnostics

Low Cost Multiplexing

Capabilities

Prenatal Genetic Testing

Technologies Thrust Areas

MicroarrayM

Icro

flu

idic

s/N

ano

dia

gn

ost

ics

Non-invasive

technologies

22N5DF-55

Current Market Scenario Future Market Scenario

Automation

Multiplex

Lab-On-Chip

Integration

Fragment Based

Manual Handling

Immunoassays

Large Footprints

High Throughput Screening

Stand-alone

Changing Market Demands from R&D Sites

Faster, Easier, Automated

23N5DF-55

ECONOMIC

Country Risk

Economic Trends &Issues

EconomicThreats

Economic Trends

CEO

Economic Perspective

• Impact of Economic Downturn

• Increase in M&A Activities

24N5DF-55

Under-developed Economies Access to clinical testing facilities is a big challenge. More emphasis on

developing easy to use cheaper POC tests.

Emerging Economies (BRIC) Growing middle-class population with better income and access to

private insurances have increasing purchasing power

Developed Economies Keen in developing state-of-the art

market tests. Less budgetary constraints for new technologies

Diverse Global Economies Impact Product Development and Marketing Strategies

EQUILIBRIUM BETWEEN COST EFFECTIVENESS AND CLINICAL EVIDENCE WILL BE A PRIMARY ECONOMIC DRIVER FOR NEW PRODUCT DEVELOPMENT AND ADOPTION.

25N5DF-55

Test Kit Providers

(Diagnostic Companies)

Sample Processing Platform

Manufacturers

Test Service Providers

(Laboratories)

Molecular Diagnostics

Inte

grat

ed te

st

kit a

nd p

latfo

rm

deve

lopm

ent

Novel

molecular

test

development

Quest Diagnostics Licenses Epigenetic Biomarker for

Prostate Cancer from Epigenomics Inc to Develop and

Market the Diagnostic Test

Beckman Coulter to Acquire Lab Based

Diagnostics Business from Olympus Corporation

Increase in M&A Activities Impacts Market Dynamics

26N5DF-55

Competitive Perspective

In-Direct

Competition

Competitive

Strategy

Competitive

Benchmarking

Emerging

Competition

COMPETITIVE

CEO

• Diagnostic Potential of New Diseases Increases Competition.

• Vendors Offer Competitive Workflows

27N5DF-55

Diagnostic Potential of New Diseases Increases Competition

2012

BENCH BED SIDE

Multiplex Detection

Panels for Cancer

Differentiated Product

Development

2005

2011

Incr

easi

ng

Co

mp

etit

ion

2020

Target miRNAs important

in cell differentiation

Multiplex Detection Panels

for Cardiac and Diabetes

Incr

easi

ng

Dia

gn

ost

ic

Tes

ts

Differentiate between

Chronic & Life Style

Diseases

28N5DF-55

Large up-front costs, Quality disparities

Mergers & Acquisitions Maintain ‘best-in-class’ rep

Vendors Offer Complete Workflows to Remain Competitive

Validation

• RNAi• Antisense

oligonucleotides• Mimics and inhibitors• shRNA

Sample Preparation Functional Analysis

• Sample collection• Nucleic acid

purification• Protein purification• Automated liquid

handling

• Microarray• Multiplex assay• Sequencing • High content screening• Cell based assays

Detection and Quantification Analysis

• qRT-PCR• ELISA• Mass spectrometry• Western blotting

Wor

kflo

wT

echn

olog

ies

Validation

Strategies to Fill Workflow ChallengesBenefits

Revenues sharingAlliances Align with top provider

Large R&D costs In-house Development Easy integration

29N5DF-55

Customer Perspective

CEOCUSTOMER

NonCustomer

Demo-graphics

BehaviorCompetitor’sCustomers

1. Types of testing in Hospital and Physician Owned Labs

3. R&D Sites Prefer Walk Away Solutions

30N5DF-55

Endocrinologists, Family practitioners & Internists are

leading adopters of these testing methods in POLs

OB/GYN, Pediatricians, and Cardiologists are leading in adoption for pregnancy, infectious

disease, and coagulation tests, respectively

FOBT and urinalysis are commonly used in many

specialties

0%

20%

40%

60%

80%

100%

Glu

cose

han

dhel

dm

ete

rs HbA

1c

Ch

oles

tero

l/Lip

id

Che

mis

try

anal

yzer

s

Imm

unoa

ssay

anal

yzer

s

Dru

gs o

f Ab

use

rapi

d te

st k

its

Infe

ctio

us

Dis

ease

rapi

d te

st k

its

Pre

gnan

cy/F

ertil

ityra

pid

test

kits

Hem

ato

logy

ana

lyze

rs

He

mos

tasi

sC

oagu

latio

nsy

ste

ms

Car

dia

cB

iom

ark

ers

Fec

al O

ccul

tB

lood

Tes

ts

Urin

alys

is s

yste

ms

The current utilization pattern of tests in physician office laboratories illustrates high utilization for glucose handheld meters, fertility test kits, fecal occult blood tests, and urinalysis systems.

Hospital and Physician-owned Laboratories Lead Routine TestingP

erce

nta

ge

of

Ph

ysic

ian

s U

tili

zin

g T

est

Internal Medicine Pediatrics OB/GYN Family Practice/GP Cardiology Endocrinology

Test Types

Utilized Testing byPhysician Specialty

31N5DF-55

Top Reasons for Satisfaction

(% of respondents, N=298)

Genomic Technology

Usefulness/ relevance to

research

Easy to use

High accuracy

Well integrated with existing technologies

High specificity/ selectivity

PCR/Thermal cycling 21 43 5 7 12

Gel Based (Northern/ Southern) 16 28 16 4 11

Multiplex assay 16 6 15 4 3

qPCR/RT-PCR 24 15 20 3 28

CE sequencing 14 14 23 6 8

Next Generation sequencing 20 13 13 13 --

Microarray 28 14 6 10 7

Automated liquid handling 10 6 6 12 4

SMD platforms 20 15 20 10 20

DNA/RNA isolation & purification 19 29 5 6 2

RNA interference 47 15 6 6 16

Transfection 33 38 2 9 3

Ease-of-use features and technology integration are critical for customer satisfaction in the fast-paced and demanding end-user community for drug discovery technologies.

R&D Sites Prefer Easy-to-use Walk-away Solutions

Secondary Reason for SatisfactionPrimary Reason for Satisfaction

32N5DF-55

Contents

Diagnostics

Industry

Briefing 3.

2.

1. APAC Market Outlook

Industry Opportunities and Growth Strategies

360 Degree Perspective

33N5DF-55

Opportunities in the Clinical Diagnostics Market

Clinical Chemistry

Coagulation

HematologyImmunoassay

Microbiology

Molecular Diagnostics

POCT

SMBG

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

CA

GR

%

Infancy Early Growth Late Growth Maturity

Bubble size indicates the relative projected revenues of different segments in Yr 2010

Market Age Vs. CAGR of Diagnostics Market (Global), 2006-2010.

• The market growth of Molecular diagnostics is driven by the Majority of population with Sexually transmitted diseases, growing popularity of Thyroid & other Autoimmune diseases, Usage of molecular tests in drug discovery clinical trials and Need for quantitative, real-time monitoring of viral loads.

• Technological advancement in whole blood analyzer would spur the growth in coagulation/Hemostasis market.

• Most of the segments are expected to grow fairly due to emerging focus on preventative medicines in Asia.

34N5DF-55

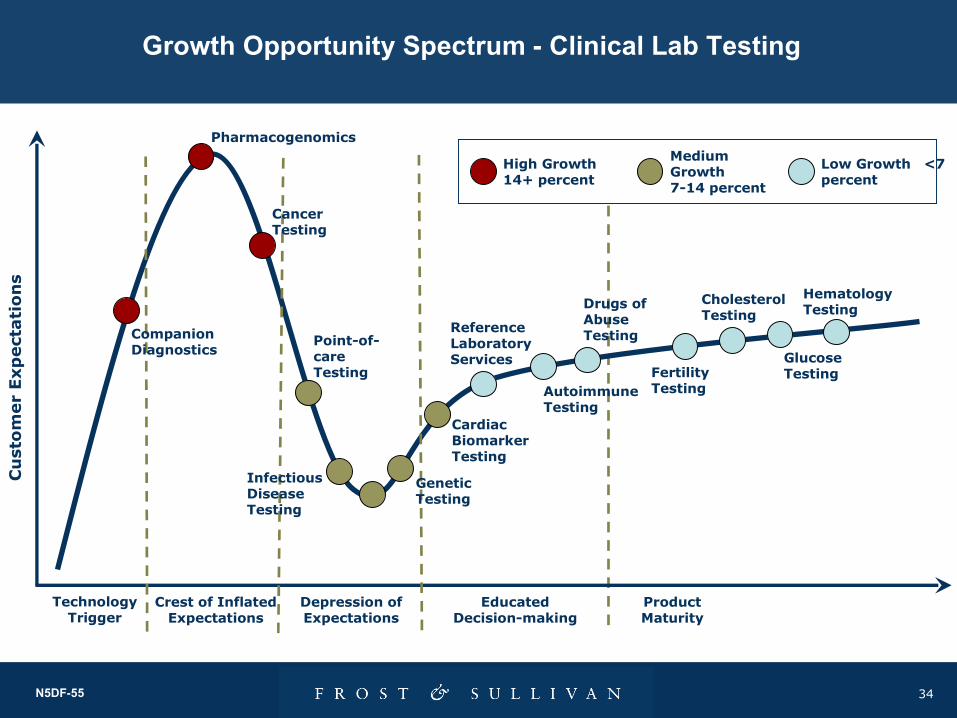

Growth Opportunity Spectrum - Clinical Lab Testing

High Growth 14+ percent

Medium Growth 7-14 percent

Low Growth <7 percent

Technology Trigger

Crest of Inflated Expectations

Depression of Expectations

Educated Decision-making

Product Maturity

Pharmacogenomics

Companion Diagnostics

Cancer Testing

Point-of-care Testing

Genetic Testing

Infectious Disease Testing

Cardiac Biomarker Testing

Reference Laboratory Services

Autoimmune Testing

Drugs of Abuse Testing

Glucose TestingFertility

Testing

Cholesterol Testing

Hematology Testing

Cu

sto

mer

Exp

ect

ati

on

s

35N5DF-55

Response from Service Providers

36N5DF-55

Focus by Disease Areas

37N5DF-55

Technology Trigger Crest of Inflated Expectations

Depression of Expectations

Educated Decision-making

Product Maturity

High Growth 14+ percent

Medium Growth 7-14 percent

Low Growth <7 percents

Declining Market

ELISA

Next Generation Sequencing

Microfluidic Chip Technology

Capillary Electrophoresis DNA Sequencing

Nucleic Acid Isolation and Purification

DNA Microarray

Automated Liquid Handling

Protein Interaction Analysis Technology

Protein Arrays

High Content Screening and Analysis

Multiplex Assay Technology

Cell Culture

Proteomics Sample Preparation

Protein Electrophoresis

Western Blotting

Cell Based Assays

RNAi Technology

MicroRNA Technology

Growth Opportunity Spectrum - Research & Development Testing

38N5DF-55

2/3

1/3Academic and

Govt. LabsPharma/Biotech

CompaniesClinical Labs

Limited equipment funds

Mostly unlimited equipment funds

Very limited equipment funds

Price often directs purchases

Large account bargaining power

Seek reagent rental programs

Technology Compliance

Legislative Compliance

Growth Strategy – R&D Testing

39N5DF-55

Growth Strategies- Research & Development Testing

0.0

20.0

40.0

60.0

80.0

100.0

Affym

etrix

Milli

pore Pall

Sigma-

Aldrich

Qiagen

Life

Techn

ologie

s

Therm

o Fish

er S

cient

ific

Illum

ina

Perkin

Elmer

Seque

nom

Agilen

t Tec

hnolo

gies

Wat

ers

Bruke

r

Est

imat

ed P

rod

uct

Mix

(P

erce

nt)

Instrumentation Reagents & Consumables

0.0

20.0

40.0

60.0

80.0

100.0

Affym

etrix

Milli

pore Pall

Sigma-

Aldrich

Qiagen

Life

Techn

ologie

s

Therm

o Fish

er S

cient

ific

Illum

ina

Perkin

Elmer

Seque

nom

Agilen

t Tec

hnolo

gies

Wat

ers

Bruke

r

Est

imat

ed P

rod

uct

Mix

(P

erce

nt)

Instrumentation Reagents & Consumables

Estimated Revenue by Product Mix for SelectDrug Discovery Technologies Companies (2008)

Aggregate Product Mix forSelect Drug Discovery Technologies

Companies (2008)

Instrumentation33.8%

Reagents &Consumables

66.2%

Technology applications that require excessive optimization slow the “burn rate” of high-profit reagents and consumables. Moreover, complex workflows with excessive optimization often necessitate technology centralization, which further limits reagents and consumables-related business.

40N5DF-55

Critical Success Factors for the Diagnostics Industry

41N5DF-55

Value system

Educate

IntegrateInnovate

Invest

To provide cost

effective solution

To gain competitive

edge

To frame winning

strategies

To create brand loyalty

Invest in technology to develop cost

effective scalable solutions with high

robustness

Develop innovative esoteric tests with

high clinical relevance for

existing diseases

Integrate novel testswith existing

platforms to provide comprehensive test

menu

Provide educationalawareness to promote novelpredictive tests

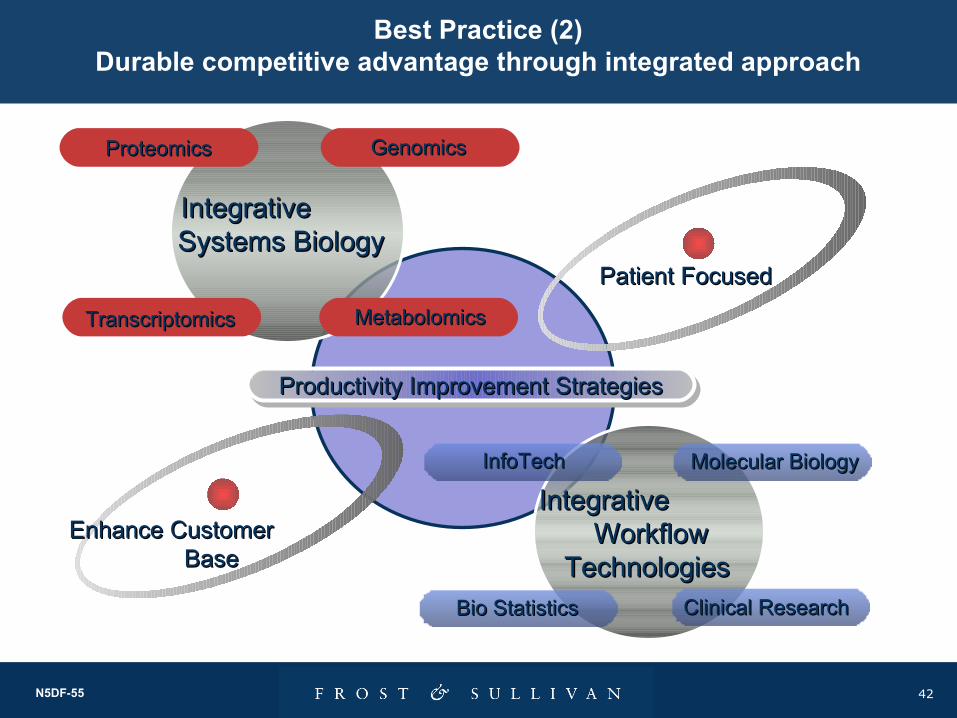

Best Practice (1) Durable Competitive Advantage Drives Growth

New Technology meets a market need and valueN Reduction in mortality ratesR Reduction in disease burdenR Reduction in disease management cost

42N5DF-55

Patient FocusedPatient Focused

Productivity Improvement StrategiesProductivity Improvement Strategies

Integrative Integrative Systems BiologySystems Biology

ProteomicsProteomics

TranscriptomicsTranscriptomics

GenomicsGenomics

Integrative Integrative Workflow Workflow

TechnologiesTechnologies

InfoTechInfoTech

Enhance Customer Enhance Customer BaseBase

MetabolomicsMetabolomics

Bio StatisticsBio Statistics Clinical ResearchClinical Research

Molecular BiologyMolecular Biology

Best Practice (2)Durable competitive advantage through integrated approach

43N5DF-55

Thank You!