dia corporate · pdf fileand not reliance on the information contained in the presentation....

TRANSCRIPT

Corporate Presentation

Legal disclaimer

This document does not constitute or form part of any purchase, sales or Exchange offer, nor is it an invitation to draw up a purchase sales or exchange offer, or advice on any stock issued by

Distribuidora Internacional de Alimentación, S.A. (“DIA” or the “Company”). Nor shall this document or any part of it form part of any offer for sale or solicitation of any offer to buy any securities

the basis of or be relied on in connection with any contract or commitment to purchase shares.

DIA cautions that this document contains forward-looking statements and information relating to DIA and include, without limitation, estimates, projections or forecast relating to possible future

trends and performance of DIA that are based on the beliefs of its management as well as assumptions made and information currently available to the Company.

Such statements reflect the current views of the Company with respect to future events and are subject to risks, uncertainties and assumptions about the Company and its subsidiaries,

including, among other things. In light of these risks, uncertainties and assumptions, the events or circumstances referred to in the forward-looking statements may not occur. None of the future

projections, expectations, estimates, guidance or prospects in this presentation should be taken as forecasts or promises nor should they be taken as implying any indication, assurance or

guarantee that the assumptions on which such future projections, expectations, estimates, guidance or prospects have been prepared are correct or exhaustive or, in the case of the

assumptions, fully stated in the presentation.

These forward looking statements speak only as of the date on which they are made and the information, knowledge and views available on the date on which they are made; such knowledge,

information and views may change at any time. Forward-looking statements may be identified by words such as “expects”, “anticipates”, “forecasts”, “estimates” and similar expressions. Current

and future analysts, brokers and investors must operate only on the basis of their own judgment taking into account this disclaimer, as to the merits or the suitability of the securities for its

purpose and only on such information as is contained in such public information having taken all such professional or other advice as its considers necessary or appropriate in the circumstances

and not reliance on the information contained in the presentation. In making this presentation available, DIA gives no advice and makes no recommendation to buy, shell or otherwise deal in

shares in DIA or in any other securities or investments whatsoever.

These analysts, brokers and investors must bear in mind that these estimates, projections and forecasts do not imply any guarantee of DIA´s future performance and results, price, margins,

exchange rates, or other events, which are subject to risks, uncertainties and other factors beyond DIA´s control, such that the future results and the real performance could differ substantially

from these forecasts, projections and estimates.

The risks and uncertainties which could affect the information provided and very difficult to anticipate and predict. DIA does not assume the obligation of publicly reviewing or updating these

statements in case unforeseen changes or events occur which could affect these statements. DIA provides information on these and other factors which could affect the business and the

results in the documents it presents to the CNMV (Comisión Nacional de Mercado de Valores) in Spain.

Accordingly, these estimates, projections and forecast must not be taken as a guarantee of future results, and the directors or managers are not responsible for any possible deviation which

could arise in terms of the different factors which influence the future performance of the company.

None of the Company nor any of its employees, officers, directors, advisers, representatives, agents or affiliates shall have any liability whatsoever (in negligence or otherwise, whether direct or

indirect, in contract, tort or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document.

Certain information contained in this presentation is based on management accounts and estimates of the Company and has not been audited or reviewed by the Company’s auditors. Recipients

should not place undue reliance on this information.

This presentation includes certain non-IFRS financial measures or expressions (gross sales under banner, comparable growth of gross sales under banner, adjusted EBITDA, adjusted EBIT, etc.)

which have not been subject to a financial audit for any period.

The information contained in this presentation does not constitute investment, legal, accounting, regulatory, taxation or other advice and the information does not take into account your

investment objectives or legal, accounting, regulatory, taxation or financial situation or particular needs. You are solely responsible for forming your own opinions and conclusions on such

matters and the market and for making your own independent assessment of the information. You are solely responsible for seeking independent professional advice in relation to the

information contained herein and any action taken on the basis of the information contained herein. No responsibility or liability is accepted by any person for any of the information or for any

action taken by you or any of your officers, employees, agents or associates on the basis of such information.

Index

02 Key Investment Highlights 8

03 Financial review 25

01 Introduction 4

04 Appendix - additional information 28

Introduction

01

DIA at a glance

A story of profitable growth in food retail

Notes

1. Excluding France, Turkey and China; 2. Ex-currency; 3. Top 100 global franchises (Franchise Direct);

4. By # of publicly published franchised stores; 5) Weight in sales of FMCG in Spain

Continued growth profile1 (#, €m) Key facts

Global and diversified footprint Discounter of reference in largest markets

1. #1 global listed proximity discounter

2. Top 20 franchisor worldwide3/ #1 in food retail in Europe4

3. Loyal customer base (+75% sales through DIA card)

4. Innovation focus (+50% private label penetration5)

SIZABLE AND UNIQUE BUSINESS MODEL…

5. EUR10.3bn gross sales under banner / EUR8.7bn net sales

6. EUR628m adjusted EBITDA (7.2% margin)

7. 19.4% ROI and 1.4x net debt / adjusted EBITDA

…FUELLED BY INDUSTRY-LEADING FINANCIAL RESULTS

DISCOUNTERS MARKET POSITION

IBERIA EMERGING

FOOD RETAIL MARKET POSITION

#1

#3

#3

#5

#1

#4

#1

#5

Source:

Kantar Worldpanel, Nielsen

# STORES ADJUSTED EBITDA GROSS SALES

UNDER BANNER

34%

66%

2016 EUR10.3bn

19%

81%

2016 EUR628m

26%

74%

2016 7,420

49%

51%

2016 7,420

Company-owned

Franchise

Iberia

Emerging

7,420

4,355

2016

# STORES ADJUSTED EBITDA GROSS SALES

UNDER BANNER

2011 2016 2011

10,314

7,810

628

471

2016 2011

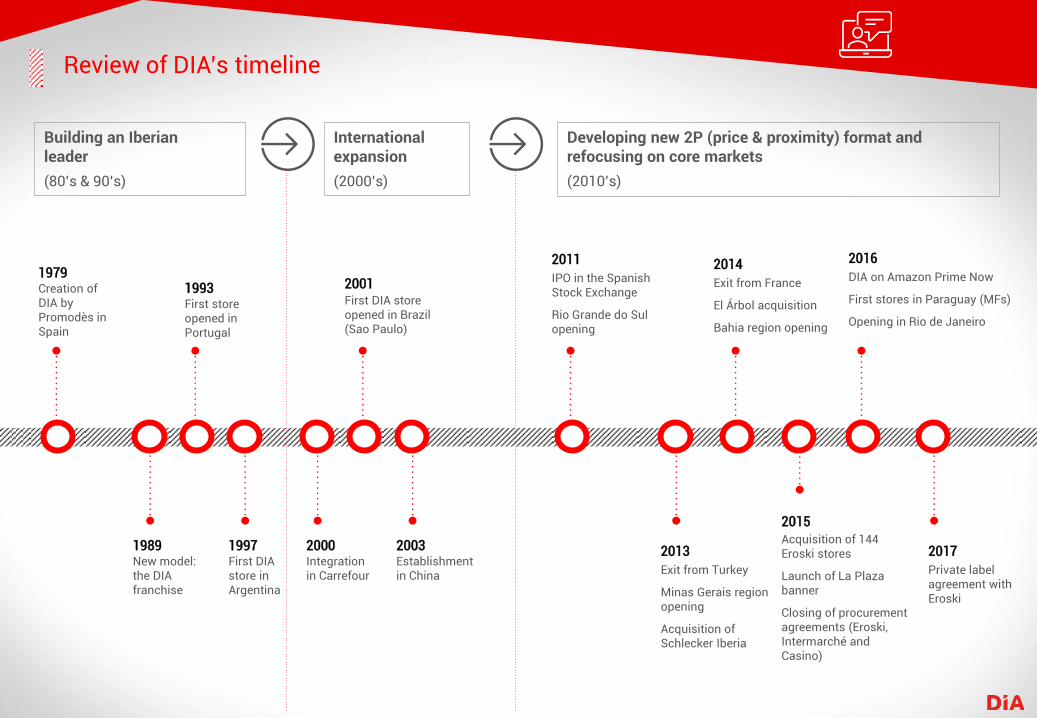

Review of DIA’s timeline

Building an Iberian leader

(80’s & 90’s)

International expansion

(2000’s)

Developing new 2P (price & proximity) format and refocusing on core markets

(2010’s)

1979 Creation of DIA by Promodès in Spain

1989 New model: the DIA franchise

1993 First store opened in Portugal

1997 First DIA store in Argentina

2000 Integration in Carrefour

2001 First DIA store opened in Brazil (Sao Paulo)

2003 Establishment in China

2011

IPO in the Spanish Stock Exchange

Rio Grande do Sul opening

2014

Exit from France

El Árbol acquisition

Bahia region opening

2013

Exit from Turkey

Minas Gerais region opening

Acquisition of Schlecker Iberia

2015 Acquisition of 144 Eroski stores

Launch of La Plaza banner

Closing of procurement agreements (Eroski, Intermarché and Casino)

2016

DIA on Amazon Prime Now

First stores in Paraguay (MFs)

Opening in Rio de Janeiro

2017

Private label agreement with Eroski

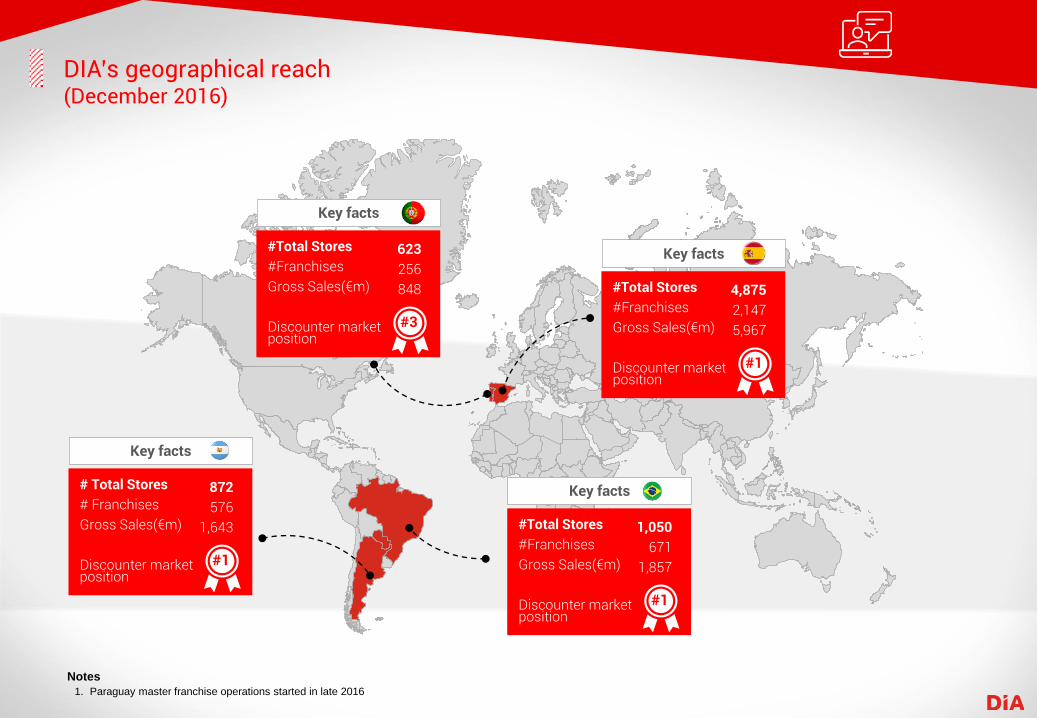

DIA’s geographical reach (December 2016)

Notes

1. Paraguay master franchise operations started in late 2016

Key facts

#Total Stores

#Franchises

Gross Sales(€m)

Discounter market position

623

256

848

#3

Key facts

# Total Stores

# Franchises

Gross Sales(€m)

Discounter market position

872

576

1,643

#1

Key facts

#Total Stores

#Franchises

Gross Sales(€m)

Discounter market position

1,050

671

1,857

#1

Key facts

#Total Stores

#Franchises

Gross Sales(€m)

Discounter market position

4,875

2,147

5,967

#1

Key Investment Highlights

02

Key investment highlights

1

Leading listed

discounter rightly

focused on offering

the most valuable

attributes for today’s

customers:

Price & Proximity

2

Multi-banner, multi-local,

customer-centric and

innovative business

model well-fitted to

capture digital

opportunities

3

Flexible and cost-efficient

operations levered by a

sizeable entrepreneurial

network, delivering higher

stable margins and

superior returns on

investment

4

Systematic delivery of

organic and inorganic

growth with strong

outlook

5

Experienced

management team

with a defined strategy

and strong execution

track-record

Leading listed discounter…

[#1] listed discounter worldwide, having significantly gained market share in the last few years

1

Global discounters ranking (by # stores; ‘000)

Source Company fillings; Lidl and Aldi based on latest info available (2014)

#1

#3

10,006 9,937

7,420

6,146

3,107

DIA’s market share gain in its largest geographies

#1

#1

#1

#1

#1

#1

7.1% 2011

8.6% 2016

4.8% 2011

7.0% 2016

6.0% 2011

12.4% 2016

# DIA’s discounter position Top 5 players market share

…rightly focused on core customer values: Price & Proximity

Proximity stores as the most resilient format and expected to drive global food retail growth in the mid-term

Current trends in the global food retail sector… …support DIA’s long-term strategic positioning

Mature markets Emerging markets

• Ageing population • Higher shopping frequency • Less people per home /

reduced storage capacity • Stagnation of personal income

/ value-for-money approach • Unemployment remains high

in certain geographies • More women in the workforce

• Increased weight of modern distribution

• Rising of oil and energy costs

• Increase of urban population

• Rise of middle class

• Higher personnel costs

Source Euromonitor

SPAIN BRAZIL ARGENTINA

7%

5%

2%

(8%)

(2%) (1%)

11-16 CAGR 16-21 CAGR

8%

6% 6%

(9%)

(6%)

(2%)

11-16 CAGR 16-21 CAGR

6%

(3%)

(1%)

6%

11-16 CAGR 16-21 CAGR

6% 7%

Hard discounters

Hypermarkets

Supermarkets

Department stores

Convenience

Convenience & Discount Hypermarkets Supermarkets

1

Leading price image across all geographies

Price as a differentiating feature vs. competitors

-100

-80

-60

-40

-20

0

20

40

60

80

ma

y-1

3

no

v-1

3

ma

y-1

4

no

v-1

4

ma

y-1

5

de

c-1

5

ma

y-1

6

no

v-1

6

DIA Competitor A

Competitor B Competitor C

Competitor D Competitor E

Competitor F Competitor G

-40

-20

0

20

40

60

80

100

no

v-1

3

ma

y-1

4

no

v-1

4

ma

y-1

5

de

c-1

5

ma

y-1

6

no

v-1

6

DIA Competitor ACompetitor B Competitor CCompetitor D Competitor ECompetitor F Competitor GCompetitor H

Source DIA and Kantar

-30

-20

-10

0

10

20

30

40

50

60

70

Ma

y-y

y

No

v-y

y

Ma

y-y

y

No

v-y

y

Ma

y-y

y

De

c-y

y

Ma

y-y

y

No

v-y

y

DIA Competitor A

Competitor B Competitor C

Competitor D Competitor E

1 M

ay

-13

No

v-1

3

Ma

y-1

4

No

v-1

4

Ma

y-1

5

No

v-1

5

Ma

y-1

6

No

v-1

6

Ma

y-1

3

No

v-1

3

Ma

y-1

4

No

v-1

4

Ma

y-1

5

No

v-1

5

Ma

y-1

6

No

v-1

6

No

v-1

3

Ma

y-1

4

No

v-1

4

Ma

y-1

5

No

v-1

5

Ma

y-1

6

No

v-1

6

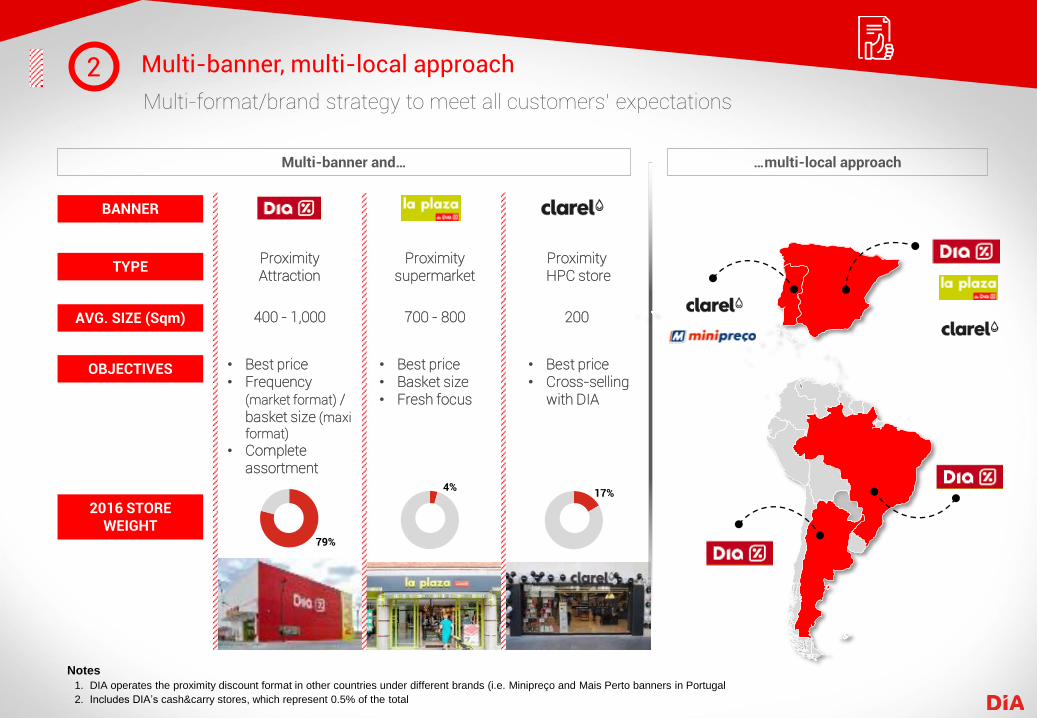

Multi-banner, multi-local approach

Multi-format/brand strategy to meet all customers’ expectations

2

Notes

1. DIA operates the proximity discount format in other countries under different brands (i.e. Minipreço and Mais Perto banners in Portugal

2. Includes DIA’s cash&carry stores, which represent 0.5% of the total

Multi-banner and… …multi-local approach

BANNER

TYPE

AVG. SIZE (Sqm)

Proximity Attraction

Proximity supermarket

Proximity HPC store

400 - 1,000 700 - 800 200

OBJECTIVES • Best price • Frequency

(market format) / basket size (maxi format)

• Complete assortment

• Best price • Basket size • Fresh focus

• Best price • Cross-selling

with DIA

2016 STORE WEIGHT

79%

4%17%

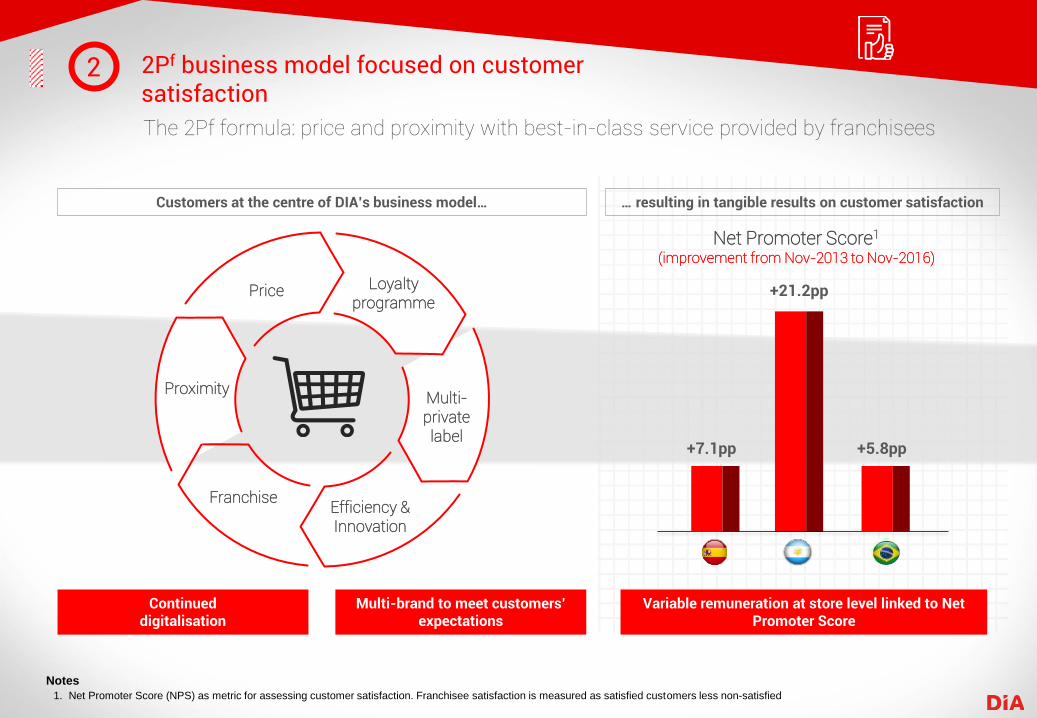

2Pf business model focused on customer satisfaction

The 2Pf formula: price and proximity with best-in-class service provided by franchisees

2

Customers at the centre of DIA’s business model… … resulting in tangible results on customer satisfaction

Notes

1. Net Promoter Score (NPS) as metric for assessing customer satisfaction. Franchisee satisfaction is measured as satisfied customers less non-satisfied

Variable remuneration at store level linked to Net Promoter Score

Net Promoter Score1

(improvement from Nov-2013 to Nov-2016)

Continued digitalisation

Multi-brand to meet customers’ expectations

Proximity

Price Loyalty programme

Franchise Efficiency & Innovation

Multi-private label

+21.2pp

+7.1pp +5.8pp

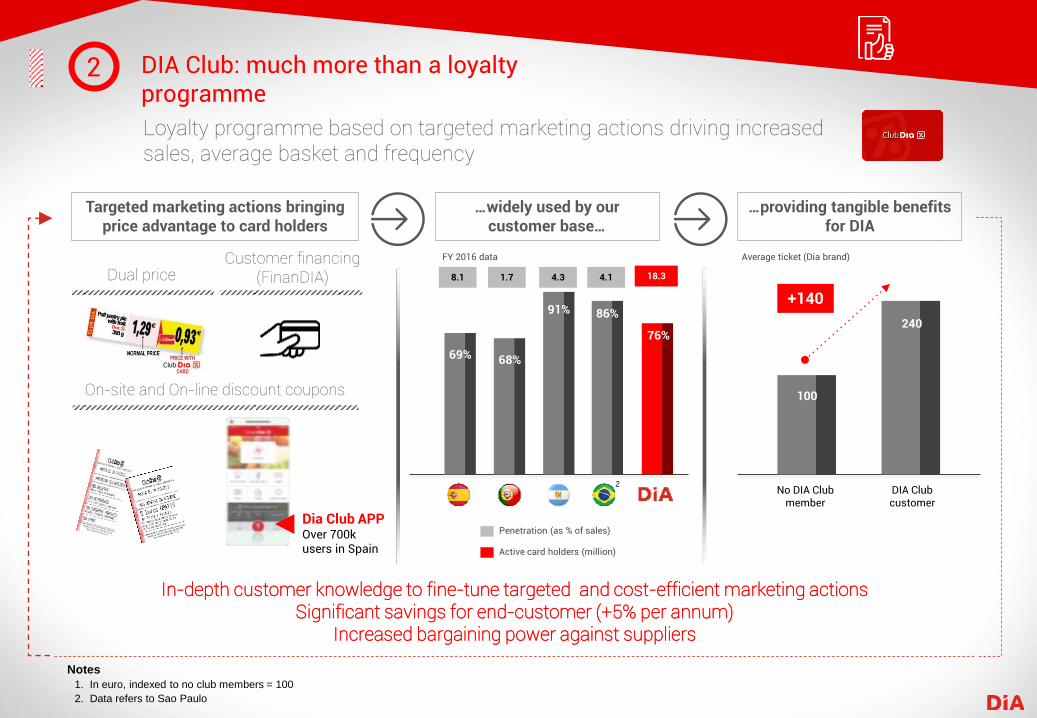

DIA Club: much more than a loyalty programme

Loyalty programme based on targeted marketing actions driving increased sales, average basket and frequency

2

Notes

1. In euro, indexed to no club members = 100

2. Data refers to Sao Paulo

Targeted marketing actions bringing price advantage to card holders

…widely used by our customer base…

…providing tangible benefits for DIA

In-depth customer knowledge to fine-tune targeted and cost-efficient marketing actions Significant savings for end-customer (+5% per annum)

Increased bargaining power against suppliers

Dual price

On-site and On-line discount coupons

Customer financing (FinanDIA)

Dia Club APP Over 700k users in Spain

69% 68%

91% 86%

76%

2

FY 2016 data

8.1 1.7 4.3 4.1 18.3

Penetration (as % of sales)

Active card holders (million)

Average ticket (Dia brand)

100

240

No DIA Club member

DIA Club customer

+140

Outstanding private label proposition backed-by strong innovation

Successful implementation of DIA’s private label in all countries driving superior price and quality image

2

A continued and cost-efficient innovation funnel… … with proven track record

Selection of base products

Testing

Manufacture

Finished products

• Choice and distribution of product • Description of quality specifications

Notes

1. Weight in Fast Moving Consumer Good sales

• Over 3,000 panel tests per year for validation and control

• Sourcing (selection of suppliers) • Logistics • Display • Multi-lingual packaging

• Systematic quality control at DIA warehouse labs

• Additional controls in external laboratories

Penetration1 of DIA’S private label vs. overall market (as a % of sales)

+44% SALES IN 2016 Latest launches

39%

53%

32%

54%

7% 5%

37% 35%

DIA PL share (%) Market PL share (%)

DIA poised for digital transformation

New measures have been implemented with a strong focus on improving operations for the 3 main pillars of the Company: customers, stores and local partners

2

Notes

1. Source Nielsen (Measured as satisfied less non-satisfied)

Customers Store management Franchisees

Digital transformation

> EUR120m sales in Spain in 2020 (x6 vs 2016)

Greater streamlining of tasks and improved quality of procedures

+ 9 pp improvement in franchise satisfaction1

• Store management: price, checks, offers

• Inventory: stock control, generation of files

• Logistic/Transport service: daily monitoring of service frequency and fleet

• Shopping list • Access to digitalised

discount coupons • Monthly expense control • Digital loyalty card • +3,000 Click&Collect points

• Franchisee App • Smart tracking of deliveries • Direct contact line with

Regional Centres

Franchise model: a fundamental pillar of the business

Unique franchise proposition supporting a flexible and efficient operation

3

Top 20 franchisor worldwide1/ #1 in food retail in Europe2 Well balanced store mix

…leading to a sustainable business model in the long run Continued increase of the franchising activity…

Notes

1. Top 100 global franchises (Franchise Direct); 2. By # of publicly published franchised stores; 3. Excludes China)

% of owned and franchised stores by segment

56%

44%

5,498

35% 65%

1,922

% Owned % Franchised

• Profitable capillarity

• Day-to-day management flexibility

• Efficient management of operational expenses

• Reduced personnel expenses

• Higher control of shrinkage

• Lower rotation of personnel vs. owned stores

• Higher commitment / top service

• Better knowledge of customers

Top franchise ranking by geography and years of experience in the country

#1

#1

Over 37 years retail and 27

franchising track-record

Over 23 years retail and 20

franchising track-record

#1

#1

Over 19 years retail and 15

franchising track-record

Over 15 years retail and 14

franchising track-record

#1

Weight of franchises (# stores)3

34% 34%

40% 40% 44% 44% 42%

52%

42%

55%

47%

60%

49%

61%

2011 2012 2013 2014 2015 2016 2010

DIA banner stores Total stores

Integrated and cost-efficient business model

Fully integrated and cost-effective supply chain based on our proprietary IT infrastructure resulting in recurrent industry-leading productivity and return on investment

3

Notes

1. DIA based on 2016 figures; Peers’ data based on 2015 figures; employees on a FTE basis

2. ROI as EBITDAR / Avg. invested capital; Avg. invested capital = Avg total assets exc cash + Avg D&A Avg account payables – Avg accrued liabilities + x5 Rent adjustment

3. Carrefour, Casino, Jeronimo Martins,, Metro, Morrison, Sainsbury, Sonae and Tesco

EBITDA per employee (k€)1 Efficient and integrated supply chain

Return on investment 2016 (%)1,2

Strong franchise platform Strict capital allocation process

14.7

10.2 Average peers3

+44%

19.4%

11.9% Average peers3

+750bps

Streamlined, fully integrated retail capabilities

Proprietary management system

End-to-end scope

Supplier

Warehouse

Transport

Owned Store /

Franchise

Efficient store portfolio management

Active store portfolio management to adapt to evolving customer requirements

3

Active Store Portfolio

Management

Continued rent negotiation

Refurbishment plans

Active store network

optimisation

Disciplined and smart capex allocation Rental flexibility

Continued effort towards sustainability Active network right-sizing

+1,400 transfers from COCO to COFO stores since 2011

+2,650 openings and

+1,300 closures

cumulated since 2011

• 90% Lease-hold

• Significant lessor

atomisation

• Contract flexibility < 1 year

commitment on average

• 7.0% rental per square

meter reduction in

2011-16 period

Notes

1. Includes rental costs related to property and equipment and revenue from lease agreements; Rents / AVG sqm Company owned company

operated + company owned franchise operated

Superior, resilient and consistent financial profile

4

Notes

1. Ex-currency

2. Defined as Net debt / Adjusted EBITDA

Gross sales under banner evolution (EURm) Stores (#)

Net debt & leverage2 evolution (EURm) Adjusted EBITDA (EURm)

2011 2012 2013 2014 2015 2016

4,355 4,617

6,102 6,938

7,337 7,420

2011 2012 2013 2014 2015 2016

7,810 8,587

9,096 9,199 10,306 10,314

2011 2012 2013 2014 2015 2016

466 529

581 589 614 628

2011 2012 2013 2014 2015 2016

576 629 651 533

1,132 878

1.2x 1.2x 1.1x 0.9x

1.9x

1.4x

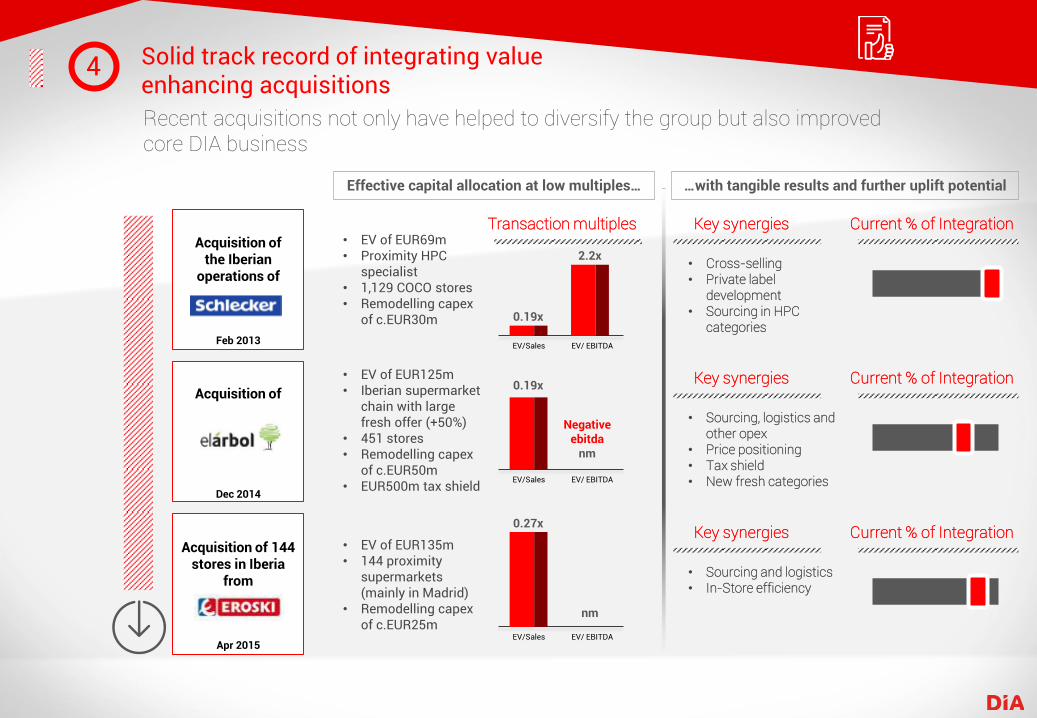

Solid track record of integrating value enhancing acquisitions

Recent acquisitions not only have helped to diversify the group but also improved core DIA business

4

Acquisition of the Iberian

operations of

Feb 2013

Acquisition of

Dec 2014

Acquisition of 144 stores in Iberia

from

Apr 2015

Effective capital allocation at low multiples… …with tangible results and further uplift potential

• EV of EUR69m • Proximity HPC

specialist • 1,129 COCO stores • Remodelling capex

of c.EUR30m

• EV of EUR125m • Iberian supermarket

chain with large fresh offer (+50%)

• 451 stores • Remodelling capex

of c.EUR50m • EUR500m tax shield

• EV of EUR135m • 144 proximity

supermarkets (mainly in Madrid)

• Remodelling capex of c.EUR25m

Key synergies Current % of Integration

• Cross-selling • Private label

development • Sourcing in HPC

categories

Key synergies Current % of Integration

• Sourcing, logistics and other opex

• Price positioning • Tax shield • New fresh categories

Key synergies Current % of Integration

• Sourcing and logistics • In-Store efficiency

Transaction multiples

EV/Sales EV/ EBITDA

0.19x

2.2x

EV/Sales EV/ EBITDA

0.19x

Negative ebitda

nm

EV/Sales EV/ EBITDA

0.27x

nm

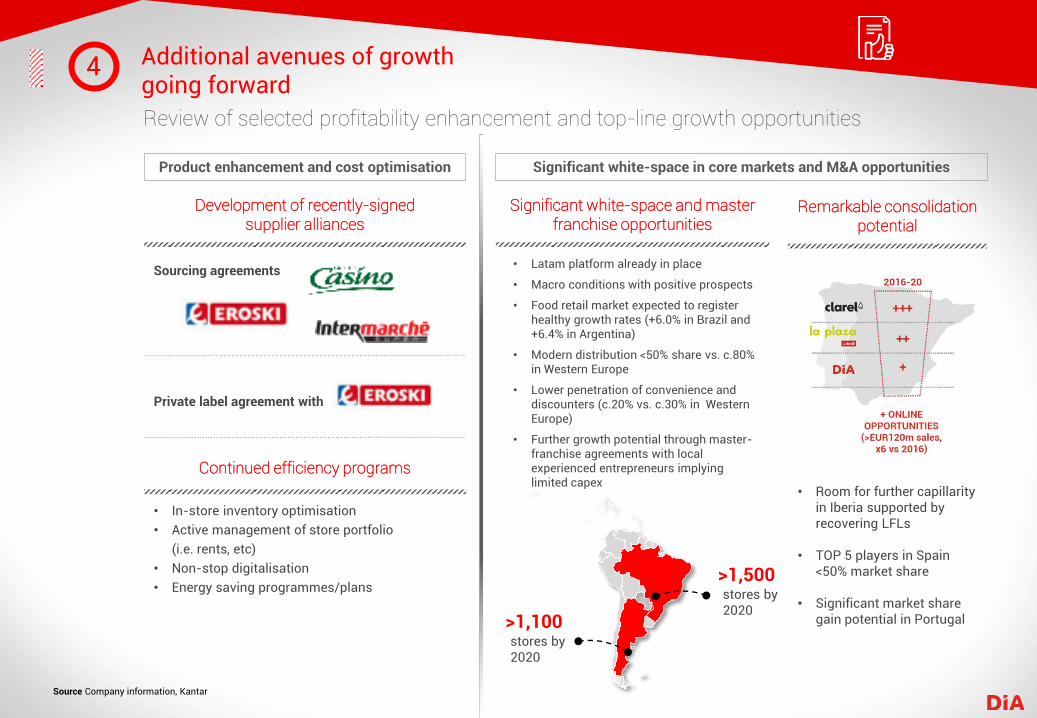

Additional avenues of growth going forward

Review of selected profitability enhancement and top-line growth opportunities

4

Source Company information, Kantar

Product enhancement and cost optimisation Significant white-space in core markets and M&A opportunities

Development of recently-signed supplier alliances

Sourcing agreements

Private label agreement with

Continued efficiency programs

• In-store inventory optimisation

• Active management of store portfolio

(i.e. rents, etc)

• Non-stop digitalisation

• Energy saving programmes/plans

Significant white-space and master franchise opportunities

Remarkable consolidation potential

• Latam platform already in place

• Macro conditions with positive prospects

• Food retail market expected to register healthy growth rates (+6.0% in Brazil and +6.4% in Argentina)

• Modern distribution <50% share vs. c.80% in Western Europe

• Lower penetration of convenience and discounters (c.20% vs. c.30% in Western Europe)

• Further growth potential through master-franchise agreements with local experienced entrepreneurs implying limited capex

• Room for further capillarity in Iberia supported by recovering LFLs

• TOP 5 players in Spain <50% market share

• Significant market share gain potential in Portugal >1,100

stores by 2020

>1,500 stores by 2020

Worked at P&G and Schweppes

Founder and CEO of Openbank and Director at British American Tobacco

Marketing manager at Cadbury Schweppes, Chairman & CEO of RJR Nabisco and Parques Reunidos

Worked at P&G for 33 years

Currently board member of Zinkia Entertainment

CEO at Dufry AG

Worked at TNT Leisure and Aldeasa

Worked at P&G , Ahold, Digsa, CEO of Toys R Us

Currently board member of Pascual

General Manager of Santander , CEO of Sabadell and VP and CEO of Caixabank

Current Board member of Société Générale

Worked at Cadbury, Coca Cola Schweppes, Debenhams and The Original Factory Shop

Currently board member of Brown Group

Worked at Bain, CEO of Microsoft Iberia and VP for EMEA of Microsoft Business solutions

Experienced management team supported by an industry-leading Board

DIA’s governing bodies as an example of the highest corporate governance standards

5

Key management Independent/External Directors of the Board

NAME

Ricardo Currás CEO

31 31

Diego Cavestany Chief Executive New Business DIA Spain Officer

29 29

Antonio Coto Executive Manager for Latin America and Partnerships

30 30

Juan Cubillo Business & Merchandise Executive Manager

23 23

Javier Lacalle Chief Resources Officer & China Executive

32 32

Amando Sánchez Chief Services Officer & Portugal Executive

5 20

Faustino Dominguez Chief Executive DIA Banner Spain Officer

26 26

YEARS AT DIA

YEARS OF INDUSTRY EXP.

NAME

Ana María Llopis Non-Executive Chairwoman

Mariano Martín Second Vice Chairman

Antonio Urcelay Board member

Juan María Nin Board member

Angela Spindler Board member

Richard Golding First Vice Chairman

Julián Díaz Board member

SELECTED PROFESSIONAL EXPERIENCE

María Garaña Board member

Former CFO at Inditex and El Corte Inglés Purchase Manager Borja de la Cierva Board member

Financial review

03

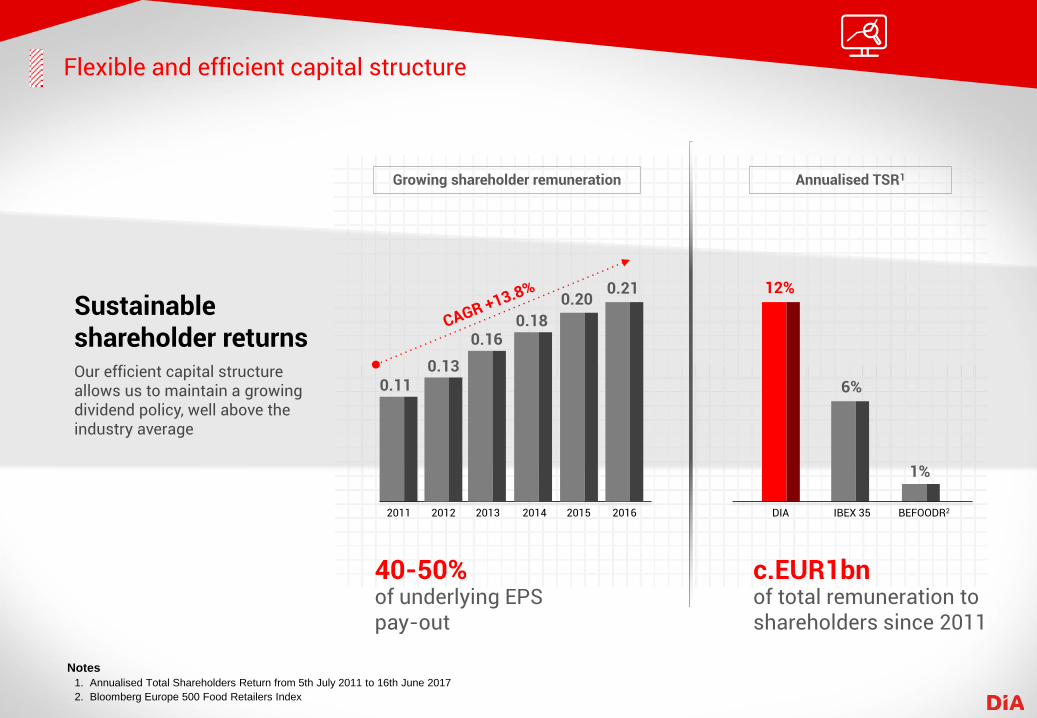

Flexible and efficient capital structure

Notes

1. Annualised Total Shareholders Return from 5th July 2011 to 16th June 2017

2. Bloomberg Europe 500 Food Retailers Index

Sustainable shareholder returns Our efficient capital structure allows us to maintain a growing dividend policy, well above the industry average

Growing shareholder remuneration Annualised TSR1

40-50% of underlying EPS pay-out

c.EUR1bn of total remuneration to shareholders since 2011

12%

6%

1%

DIA IBEX 35 BEFOODR2

0.11

2011 2012 2013 2014 2015 2016

0.13

0.16 0.18

0.20 0.21

Best-in-class financial metrics

DIA enjoys industry leading returns on investment and above average remuneration levels while maintaining a more conservative approach towards leverage than its peers

Notes

1. Return on Investment defined as EBITDAR/Average Invested Capital. Average Invested Capital defined as Equity + Net debt + 5x Rent adjustment + Accumulated D&A

2. Dividend yield based on current share price (as of April 24th 2017) and includes potential share buy backs already communicated to the market

3. Market average defined as the average for Carrefour, Casino, Jeronimo Martins, Metro, Morrisons, Sainsbury, Sonae and Tesco

2016 Return on Investment (ROI) (%)1

19.4%

11.9%

INDUSTRY AVERAGE3

DIA

+750bps

2016 Leverage (Net debt / Adjusted EBITDA)

1.9x

1.4x

INDUSTRY AVERAGE3

DIA

(0.5x)

2016 Expected dividend yield2 (%)

4.1%

2.9%

INDUSTRY AVERAGE3

DIA

+1.2%

Appendix Additional information

04

Definition of Alternative Performance Measures (APM)

• Gross sales under banner: total turnover value obtained in stores, including indirect taxes (sales receipt value) in all the company’s stores, both owned and franchised.

• Net sales: sum of the net sales generated in our integrated stores and sales to franchises.

• LFL sales growth under banner: growth rate of gross sales under banner at constant currency of the stores that have been operating for more than thirteen months under the same business conditions.

• Adjusted EBITDA: operating profit after adding back non-recurring costs, impairments, re-estimation of useful life and gains/losses arisen on the disposal of assets and depreciation and amortization of fixed assets.

• Adjusted EBIT: operating profit after adding back non-recurring costs, impairment and re-estimation of useful life and gains/losses arisen on the disposal of assets.

• Underlying net profit: net income calculated on net profit attributable to the parent company, excluding non-recurring items (restructuring costs, impairment and re-estimation of useful life, gain/losses on disposal of assets, tax litigations, exceptional financial expenses and equity derivatives), discontinued operations and the corresponding tax impact.

• Underlying EPS: fraction of the company’s profit calculated as underlying net profit divided by the weighted average number of shares.

• Cash From Operations (CFO): adjusted EBITDA less non-recurring cash items less capex on an organic basis.

Corporate Presentation