developments in renewable energy storage markets in europe

TRANSCRIPT

Developments in Renewable Energy Storage Markets in Europe

2

Agenda

2. Segmentation

3. Global Hotspots

4. Key Industry Challenges

5. Market Forces

6. Emerging Technology Roadmap

7. Comparative Analysis

8. Scenario Forecasts

9. Snapshot of Key Players

10. Key Research Findings

3

Suitable Energy Storage Technologies Segmentation

Renewable Energy Storage

Centralised Decentralised

Base load Generation

Micro renewable generation

Load Levelling

Peak Shaving

Voltage Regulation

Power Quality

Renewable Energy Storage

Pumped Hydro

Flow Batteries

Electrochemical Batteries (Sodium Sulfur, Li-ion)

CAES

Thermal Energy Storage

Electrochemical Batteries (Lead Acid, Li-ion, NiCad, Sodium Nickel Chloride)

Ultra capacitors

Flywheels

Fuel CellsGrid Stabilisation

Frequency Regulation

Renewable Energy Storage Market: Segmentation (Europe), 2009

Source: Frost & Sullivan

4

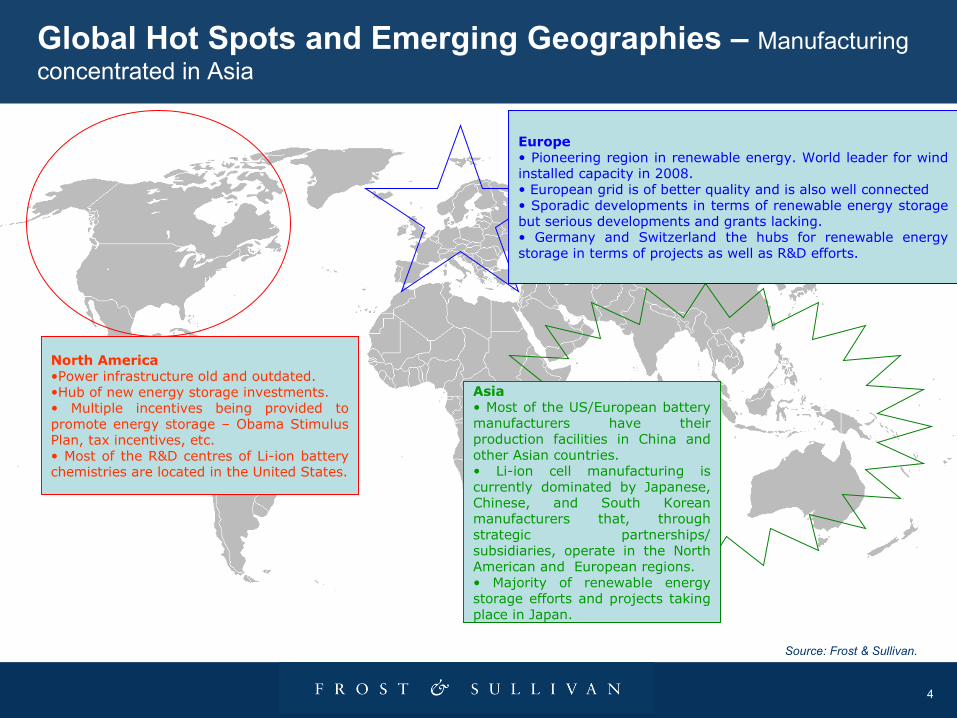

Global Hot Spots and Emerging Geographies – Manufacturing concentrated in Asia

Source: Frost & Sullivan.

North America•Power infrastructure old and outdated. •Hub of new energy storage investments.• Multiple incentives being provided to promote energy storage – Obama Stimulus Plan, tax incentives, etc.• Most of the R&D centres of Li-ion battery chemistries are located in the United States.

Asia• Most of the US/European battery manufacturers have their production facilities in China and other Asian countries. • Li-ion cell manufacturing is currently dominated by Japanese, Chinese, and South Korean manufacturers that, through strategic partnerships/ subsidiaries, operate in the North American and European regions.• Majority of renewable energy storage efforts and projects taking place in Japan.

Europe• Pioneering region in renewable energy. World leader for wind installed capacity in 2008.• European grid is of better quality and is also well connected • Sporadic developments in terms of renewable energy storage but serious developments and grants lacking.• Germany and Switzerland the hubs for renewable energy storage in terms of projects as well as R&D efforts.

5

Key Industry ChallengesGrid Scale Energy Storage is Limited in Europe Due to Lack of a Suitable Technology

Lack of a suitable energy storage

technology

Need for greater power, lifecycle and reliability

Cost of energy storage

technology

Lack of visibility on who will bear

the charges

Customer awareness about

various chemistries & technologies

Unfair Pricing of Fossil Fuels

Source: Frost & Sullivan

Recycling Issue Key Challenges

Renewable Energy Storage Market: Industry Challenges (Europe), 2009-2020

6

Drivers

Constraints

Drivers

Constraints

Intermittent Nature of Renewable

Energy

Rising Share of Renewable

Energy

Economic Downturn Affecting Investment

in R&D and Commercialization

Timeline

Smart Grid Development

High Cost of Energy Storage

Market ForcesRising Share of Renewable Energy and its Intermittent Nature Driving Demand for Energy Storage

Cost Effective for Solving Peak Power or Load

Levelling Issues

Solves the Issue of Accurate

Demand-Supply Forecast

Deters Expensive

Grid Upgrades

Rise in cost of renewable

electricity to customers

Renewable Energy Storage Market: Drivers and Restraints (Europe), 2009-2020

Short term

Medium termLong term Source: Frost & Sullivan

7

2010 2011 20122009 2013

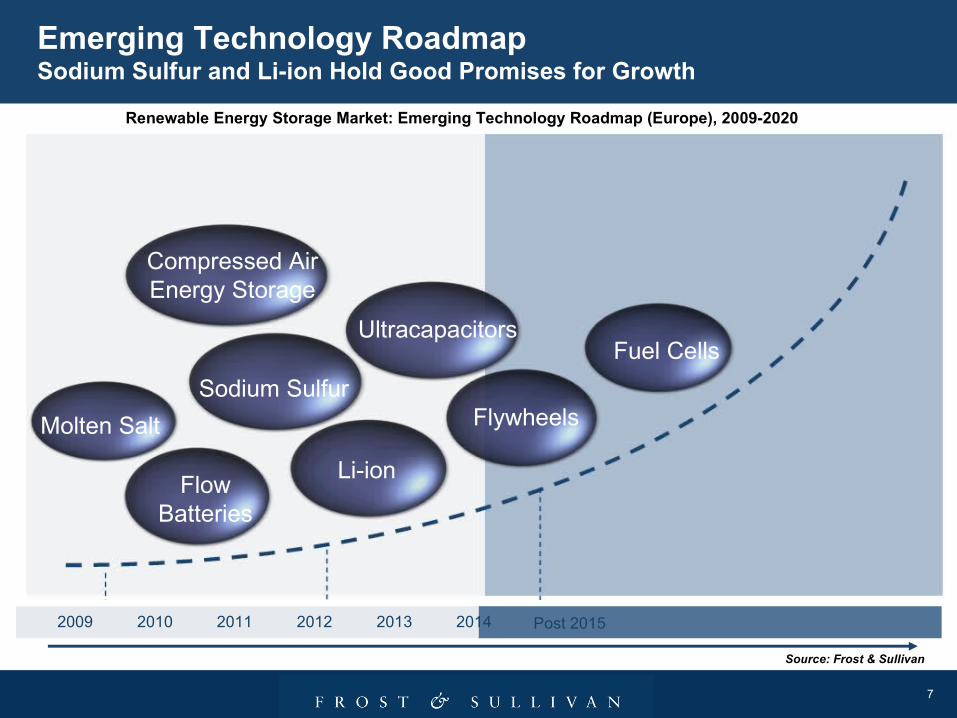

Emerging Technology RoadmapSodium Sulfur and Li-ion Hold Good Promises for Growth

2014 Post 2015

Source: Frost & Sullivan

Molten Salt

Li-ion

Ultracapacitors

Flow Batteries

Sodium Sulfur

Compressed Air Energy Storage

Fuel Cells

Flywheels

Renewable Energy Storage Market: Emerging Technology Roadmap (Europe), 2009-2020

8

Comparative Analysis – Centralized StorageDepending on the Grid Requirements, Different Storage Chemistries are Suitable

Energy

Density

Temperature/

Safety

Operating

Cost Efficiency Lifecycle

Capital

Cost Development Stage Total

Pumped HydroMost widely used form of

storage21

Flow Batteries

Commercialised but only very

few projects implemented in

Europe

15

Lithium-ion Research stage 16

CAES

Commercialised. 2 plants in

operation globally – Germany

and US

19

Thermal

Storage

Molten salt widely used for

CSP plants20

Lead Acid Widely used 14

Sodium Sulfur

165 MW installed capacity in

Japan. No projects as yet in

Europe

22

Sodium Nickel

Chloride

Been in existence for over 20

years. MES-DEA only

company in Europe

manufacturing these batteries

17

Very HighAttractiveness = 5

High Attractiveness = 4 Source: Frost & Sullivan

ModerateAttractiveness = 3

Low Attractiveness = 2

Very LowAttractiveness = 1

Total Renewable Energy Storage Market: Comparative Analysis of Storage Technologies (Europe), 2009

9

Comparative Analysis – Decentralized StorageUltra-Capacitors though not widely used today are highly suitable for Grid Stabilization and Grid Storage

10

Scenario ForecastsEnergy Storage Installed Capacity Forecasts

• In the base case scenario the energy storage installed capacity is expected to grow at a CAGR of 64% from 2010 to 2020

• For the purpose of calculation, the forecast looks only at storage of onshore wind and solar

• The growth rate is expected to become faster post 2015 with further developments in smart grids, electric and plug-in hybrid electric vehicles (PHEVs) and availability of suitable storage technologies with the desired features of high energy density, efficiency, reliability and competitive cost.

11

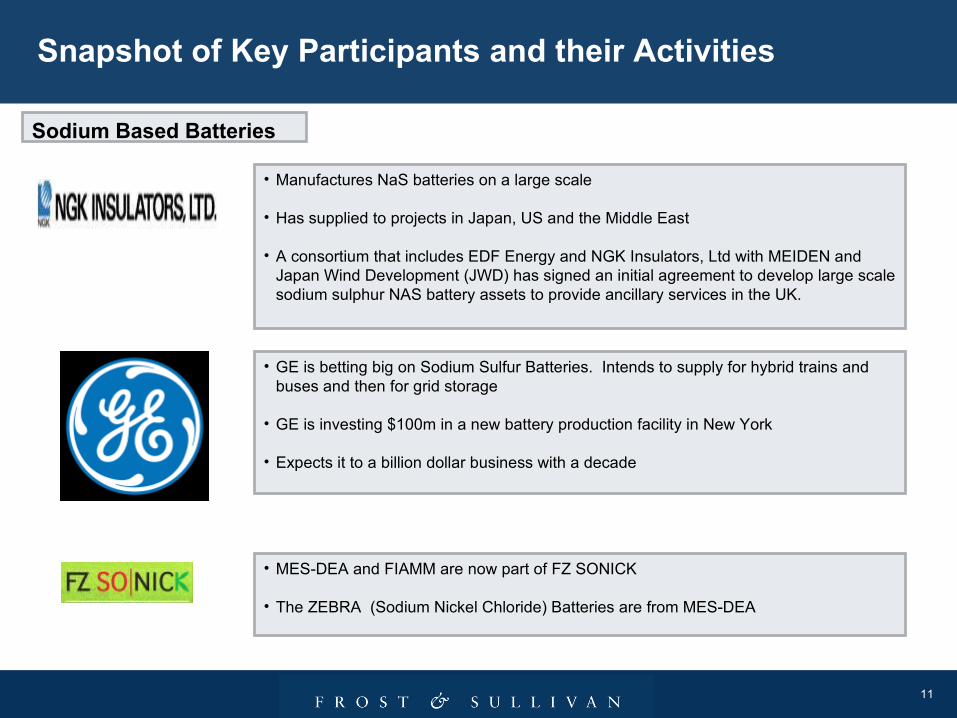

Snapshot of Key Participants and their Activities

• GE is betting big on Sodium Sulfur Batteries. Intends to supply for hybrid trains and buses and then for grid storage

• GE is investing $100m in a new battery production facility in New York

• Expects it to a billion dollar business with a decade

• Manufactures NaS batteries on a large scale

• Has supplied to projects in Japan, US and the Middle East

• A consortium that includes EDF Energy and NGK Insulators, Ltd with MEIDEN and Japan Wind Development (JWD) has signed an initial agreement to develop large scale sodium sulphur NAS battery assets to provide ancillary services in the UK.

• MES-DEA and FIAMM are now part of FZ SONICK

• The ZEBRA (Sodium Nickel Chloride) Batteries are from MES-DEA

Sodium Based Batteries

12

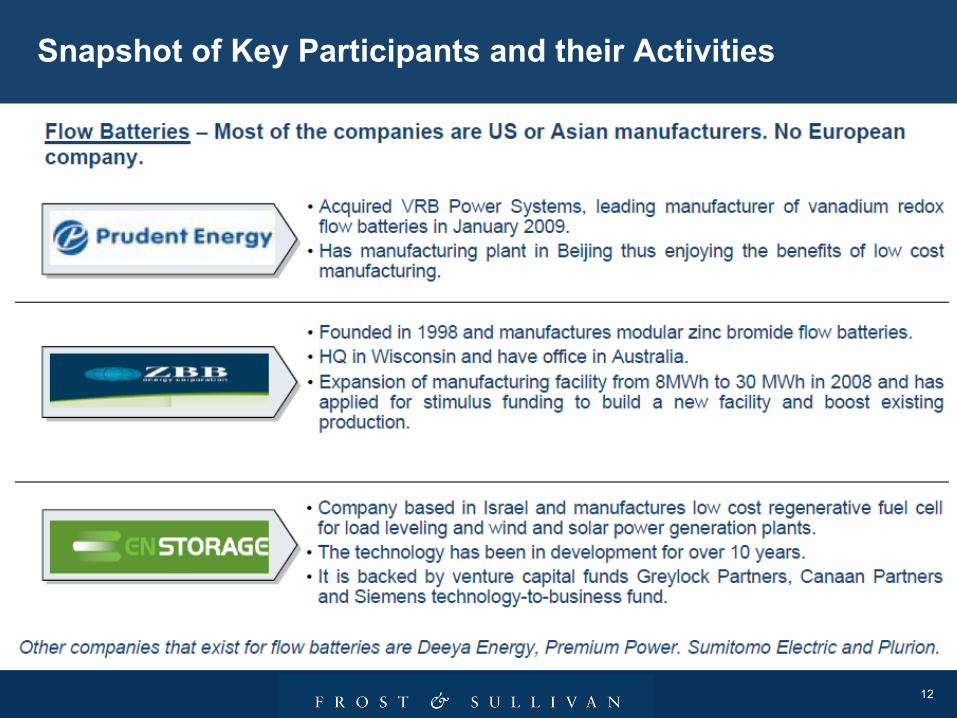

Snapshot of Key Participants and their Activities

13

Snapshot of Key Participants and their Activities

14

Snapshot of Key Participants and their Activities

Rechargeable Lithium: Quite a few European manufacturers. Majority of them have their manufacturing facility in Asia. Manufacturers developing various types of Li rechargeable batteries that have high energy density, better safety and lifecycle.

15

Key Research Findings

Rise in renewable energy generation along with its intermittent nature is driving the demand for energy storage technologies

For centralised storage consisting of large scale generation and load leveling activities sodium sulfur batteries present an attractive option while for decentralised applications, ultracapacitors and even flow batteries could be the preferred technologies

The installed capacity for energy storage technologies and batteries in particular is expected to witness a CAGR of around 65% from 2010-2020 in the Frost & Sullivan forecast scenario.

Growth in demand for energy storage is expected to rise post 2015 with smart grid development picking up pace and growth in EVs and HEVs.

There are quite a few European based lithium battery and ultracapacitor manufacturers but for other technologies many of them are Asian or US based companies.

Cost of energy storage technologies such as flow batteries ($2000/KW for vanadium redox) and Li-ion (more than $1100/KWh) remains a challenge and needs to come down substantially for widespread adoption

11

2

3

4

5

6