development of the money market, interest rates, and

TRANSCRIPT

©International Monetary Fund. Not for Redistribution

6

Development of the Money Market, Interest Rates, and

Financial Reforms in Malaysia

ZAMANI ABDUL GHANI

Over the past three decades, the Malaysian economy has achieved annual COP growth averaging about 7 percent, placing the country in the category of fast-growing Southeast Asian economies. This rapid growth has coincided with a major shift in the structure of the economy from one highly dependent on a small group of primary commodities to one in which manufacturing is the largest sector. Growth has been supported by a rise in the investmen L rate from an average of 1 4 percent of GDP in the 1960s to 33 percent in 1990. This increase was facilitated by the growing openness of Malaysia's economy, since much of the inveslll1ent came from abroad and was concentrated in export-oriented activities, and in parlicular a move toward financial liberalization.

The shift toward financial liberalization reflected, in part, the change in the philosophical underpinnings of macroeconomic policies around the world that occurred during the 1 970s. Excessive controls and regulations were increasingly viewed as detrimental to efficient resource allocation and rapid economic growth. In general, Malaysia's objectives in undertaking financial liberalization were intended to enhance efficiency through greater reliance on market forces and to improve the effectiveness of its monetary policy. The key reforms were thus aimed at liberalizing interest rates, reducing conu·ols on credit, enhancing competition and efficiency in the financial system, strengthening the supervisory framework, and promoting the growth and deepening of financial markets. The reforms were also motivated by the need for more flexible and effective policy responses to the severe external shocks experienced by Malaysia. The gradual liberalization of the domestic fi-

125

©International Monetary Fund. Not for Redistribution

126 Zamani Abdul Ghani

nancial system was accompanied by the rela.xation of restrictions on international capital flows and a shift toward more ilexible exchange rate arrangements.

Overall, financial liberalization in Malaysia has been a gradual, phased, and continuing process rather than taking place in discrete episodes of comprehensive liberalization. For instance, interest rate liberalization started in 1978, when financial institutions were allowed to freely set their deposit and lending rates; however, the base lending rate was freed from the administrative control of the central bank only in 1991. As the financial market has grown in sophistication and complexity, measures in recent years have been directed toward enhancing the market's efficiency in allocating scarce resources and ensuring the introduction of and compliance with appropriate prudential regulations.

The Financial System

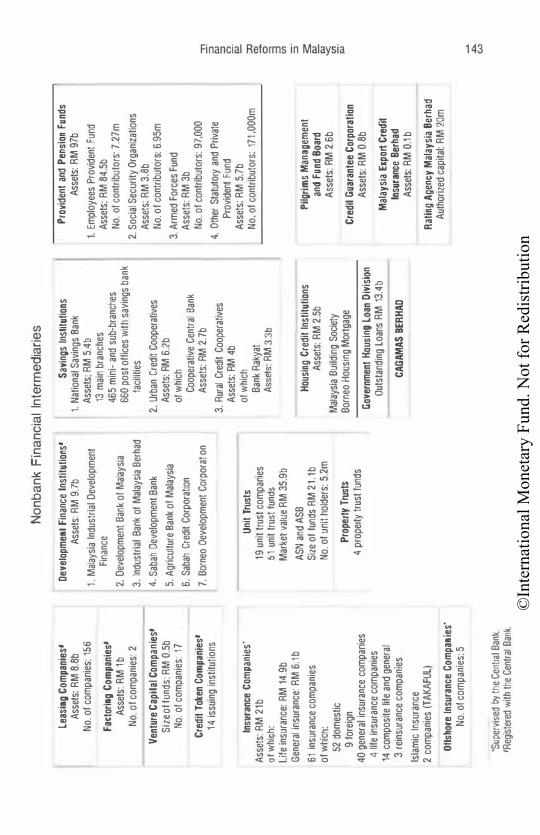

Malaysia's financial system can be divided into the banking system and nonbank financial institutions.! The entire banking system is supervised by the cenu·al bank, but of the non bank financial institutions, the insurance companies are the only ones to be supervised by the central bank.

Banking System

The banking system in Malaysia, which is the major component of the financial sector, consists of the central bank (Bank Negara Malaysia), 37 commercial banks, an lslan1ic bank, 40 finance companies, 12 merchant banks, 7 discount houses, and 8 money and foreign exchange brokers.

Currently, the institutions are differentiated on the basis of the types of deposits they are legally allowed to mobilize, the types of assets they can hold, and other regulatory constraints imposed on their operations. Since distinctions among banking institutions are increasingly blurred, such a demarcation might not prevail in the futw-e.

Commercial Banks

Commercial banks represent by far the largest component of the banking system, accounting for RM 239.2 billion of the total assets of tl1e financial system at the end of 1994, that is, 38.1 percem of the total assets of the financial system. There are 37 commer·cial banks operating

'The structure of the financial system 1n Malaysia is schematically illustrated in Appendix I.

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 127

in Malaysia, of which 2:� are domestic banks and 1 4 are foreign banks, all incorporated in Malaysia. The domestic banks operate 1 , 1 39 branches throughout the country, and the foreign banks, 144.

Commercial banks pr0\1de all normal banking services, including accepting deposits, granting loans and advances, discounting trade bills and banker's acceptances, dealing in foreign exchange, and providing business investment advisory services. Although other financial institutions in Malaysia perl()rm similar functions, commercial banks have the additional advantage of being able to offer a wider range of ancillary facilities. These institutions a� well as Bank Islam Malaysia Berhad are the only group of financial institutions in the country licensed by the central bank Lo be check-paying banks. They are also the only group authorized to deal in foreign exchange.

Over the years. the role of commercial banks has evolved from the simple traditional role of mobilizing deposits and utilizing the deposits for the financing or trade and commerce to that of being agents of change in economic development. In terms of portfolio restrictions, commercial banks are not allowed to accept deposits with a maturity of less than one month. They are required, at present, to keep 1 1 .5 percent of their eligible liabilities, on which no interest is paid, as statutory reserves with Bank Negara Malaysia, and to invest an additional 1 7 percem of these liabilities in liquid assets.

Bank Islam Malaysia Berhad

A milestone in the evolution of the banking system in Malaysia was the incorporation of Bank Islam Malaysia Berhad on March 1, 1983. The purpose of sening up this bank was to provide an avenue for Malaysian Muslims who might want to benefit from the services of a modern banking system but did not want to pay or receive interest, which is forbidd<'n by Islam. The bank offers all the conventional banking services based on Islamic principles and is also required to maintain statutory reserves with the central bank (at present, the ratio is 1 1 .5 percent of its total eligible liabilities). In addition, it is also required to observe a first liquid assets ratio of 10 percent on its total eligible liabilities, excluding inn:stment account liabilities, and a ratio of 5 percent on its investment account liabilitics.2

2General and spec1al 1nvestment account liabilities are those deposits accepted under the Islamic princ1ple of Mudharabah Special Investment deposits allow the depositors to specIfy the manner 1n which the deposits are to be utilized by the bank; they are paid profits or made to bear losses from the use of the1r depos1ts. Prof1ts are paid to the general investment account holders out of the bank's revenue from its financing and investment activities. based on an agreed predetermined profit-sharing ratio.

©International Monetary Fund. Not for Redistribution

128 Zamani Abdul Ghani

After more than 10 years in operation, Bank Islam Malaysia Berhad has proved to be a viable banking institution, with its activity expanding rapidly throughout the country. The total resources of Bank Islam Malaysia Berhad increased from RM 1 7 1 million at the end of 1983 to RM 1 ,449 million at the end of June 1 989, of which deposits accounted for RM 1,272 million or 87.8 percent of total resources. Financing extended by Bank Islam Malaysia Berhad increased from only RM 41 million at the end of 1983 to RM 728 million at the end of June 1989. As at end-1994 total deposits mobilized by the Bank Islam Malaysia Berhad increased sharply to RM 2.9 billion, while financing expanded to RM 1 .2 billion.

Finance Companies

The finance companies are the second largest group of deposittaking institutions in Malaysia. They operate in the medium-term credit market and draw their resources mainly from savings and fixed deposits. They are prohibited from dealing in gold or foreign exchange and from grant.ing overdraft facilities. Loans extended by the finance companies mainly involve hire-purchase loans, leasing finance, housing loans, and loans for a variety of other purposes, particularly for the purchase and development of real estate. The finance companies are required to observe statutory reserve and liquidity requirements.

Merchant Banks

Merchant banks are licensed to operate as specialized financial intermediaries in the money and capital markets. Since their emergence in the early 1970s, merchant banks have expanded their scope of operations by providing a wide range of specialized services, including issuing-house and underwriting facililies, corporate financing, financial investment, management advice, and portfolio investment management. Other activities include money market operations, trading of money market instruments in the secondary markets, and related banking functions. At the end of December 1 994, there were 1 2 merchant banks with a total of 1 7 offices operating in the country; their total resources amounted to RM 14.6 billion. The merchant banks are required to observe statutory reserve and liquidity requirements.

Discount Houses

The role of the discount houses has changed substantially over the years. When they were first set up in the 1960s and 1970s, their role

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 129

was envisaged as that of "keepers of liquidit)'·" The overnight deposits and call money placed by the financial instillltions wilh lhe discount houses qualified as liquid assets, and this privilege enabled the discount houses to mobilize funds at below-market rates. Moreover, they were the only financial institutions allowed to accept corporate deposits of less than one-month matlllity. The funds mobilized by lhe discount houses were invested in Malaysian government paper {at least 75 percent and not mon� than 25 percent). banker's acceptances. and negotiable cerl ilicates or deposit.

Various ac1ions were taken over the years to change the role of lhe discount houses from that of mere!)' "keepers of liquidity" to that of bona fide securities dealers. Before October 1987, the discount houses had to invest at least 85 percent of their portfolios in government paper, while the permissible maximum holdings of banker's acceptances and negotiable certificates of deposit was only 1 5 percent. The ratio was changed to 75/25 in October 1987. The maximum permissible maturity of the instrumcnLs held by lhc discount houses was lengthened in January 1989 from 3 years to 5 years, and in June 1990 the maturity period was further lengthened to 1 0 years. Anot.her important change introduced in June 1990 was lhc discontinuation of the 75/25 ratio and its replacement with a risk-wcighlecl capital adequacy ratio, to provide as much nexibilit)' as possible for the discount houses to hold the permissible assets in whatever proportion they wished, subject only to the riskweighted capital adequacy constraint. The discount houses are not subject 10 1he statutorr reserve and liquidi ty requiremen ts.

Nonbank Financial Institutions

Among the nonbank linancial insLitutions, only the insurance companies arc regulated and supervised by the central bank. They comprise insurance and t·cinsurancc companies, the Islamic insurance companies, insurance brokers. and loss acUustcrs.

The other nonbank financial institutions arc supervised by government agencies other than the cenu·al bank. These institutions can be divided into four m�jor groups: the development finance inslitutions, the savings instiwtions, the provident and pension funds, and a group of olher financial intermediaries, made up of building societies, unit trusts, and several investment agencies.

Interest Rate Reforms

Interest rates were liberalized in 1 978, allowing financial institutions to freely set their deposit and lending rates. This led to increased com-

©International Monetary Fund. Not for Redistribution

130 Zamani Abdul Ghani

peuuon among banks and resulted in an increase in interest rates. Thereafter, from November l , 1983, all borrowing rates except those charged to the priority sectors were anchored to each bank's declared base lending rate, which was based on each bank's cost of funds after providing for the cost of stannory reserves, liquid asset requirements, and overhead costs. As the actual cost of credit to borrowers was determined by the base lending rate and an interest margin based on the borrower's credit standing, tl1is measure was intended to remove much of the banks' discretion in setting their lending rmes. The introducLion of the base lending rate was inspired by tl1e fact that when banks were allowed to decide their own lending and deposit rates, the lending rates tended to behave in an asymmetrical manner. V!'hcn the cost of funds rose, banks immediately passed it on to their customers in the form of higher lending rates. However, when tl1e cost of funds declined, banks tended to delay the adjustment in their lending rates.

In the tight liquidity environment of 1985, interest rates rose shat·ply as the financial institutions bid for funds. The high level of interest rates was inconsistent with the fact that Malaysia was in tl1e middle of its worst recession ever. Not wanting to reimpose direct controls, yet keen to resu·ain the unhealtl1y bidding up of interest rates, the central bank persuaded the commercial banks and finance companies to peg their interest rates for deposits of up to 12-month maturities to the deposit rate of the two leading domestic banks, effective October 2 1 , 1985. The maximum differential vis-a-vis the two lead banks was 0.5 percentage points for the commercial banks and 1.5 percentage points for the finance companies. Subsequently. when the economy recovered and liquidity returned to the system, the pegged interest rate arrangement was dismantled in February 1987, allowing all financial institutions once again to determine freely their deposit rates.

The central bank, however, remained concerned by tl1e fact that when deposit rates declined, the commercial banks and finance companies adjusted their base lending rates and acwal lending rates only after a long Jag. After using moral suasion several times to lower these rates, tl1e central bank issued guidelines on September 1 , 1987, limiting the base lending rate of the commercial banks to no more than 0.5 percentage points above that of the two lead banks. The margin by which lending rates could exceed the base lending rate was limited to no more than 4 percentage points, depending on the borrower's credit standing. Penalty rates on delinquent loans were not to exceed 1 percent a year. The finance companies were subject to a similar set of guidelines.

As of February 1, 1991, the base lending rate was freed from the administrative control of the central bank. Each commercial bank or finance company became free to set its base lending rate based on its own

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 131

cost of funds including the cost of holding statutory reserves and the liquid asset requirement and administrative costs but excluding the cost of provisions for bad and questionable debts. Except for interest rates on lending to certain pdority sectors, which arc still subject to cenu·al bank guidelines, all other interest rates are now freely determined by market forces. The emergence of market-oriented yield curves will benefit the future development of the capital markets, particularly the development of viable secondary markets for public and private securities.

Modernization of the Money Market

The money market, where financial institutions trade shorl-lerm funds, forms an integral pan of the Malaysian financial system. It provides a ready source of funds for market participants in need of funding, and investment outlets for those with temporary surplus funds. In Malaysia, the major financial institutions are the participants in the money market, and the development of the financial system and that of the money market are closely interrelated.

New Money Market Instruments

In May 1979, the central bank introduced negotiable certificates of deposit and banker's acceptances to increase the variety of paper available in the money market. Both these instruments proved to be popular with investors. From a mere RM 200 million at the end of 1979, the amount of outstanding negotiable certificates of deposit increased to R.J\11 9,156 million by encl-1989, whereas the outstanding amount of banker's acccpLL'U1ces increased from RM 825 million to RM 2,029 million over the same period. From February 1987, six merchant banks that met the minimum capital requirement of RM 30 million were allowed to issue negotiable certificates of deposit for the first time. The value of negotiable certificates of deposit issued by the financial institutions rose to RM 28.4 billion by May 1995.

In 1980, the central bank issued its own certificates but t11esc were not actively traded in the market as the financial institutions were required to hold them for liquidity requirements. In July 1983, nonimcrcst-bcaring Government Investment Certificates (GICs) were introduced to allow Bank Islam Malaysia Berhad and other institutions to invest t11cir liquid funds on an Islamic basis. The returns are declared by the government on the anniversary date of the issue of the certificates. The outstanding volume of these certificates increased from RM 100 million at end-1983 to RM 1 ,000 million at end-1989, and as of 1995 stood at RM 4.8 billion.

©International Monetary Fund. Not for Redistribution

132 Zamani Abdul Ghani

v\'ith the esutblishment of a national mortgage corporarion (Cagamas Berhad), mortgage-hacked bonds were first issued in Ocrober 1987. These bonds <tiT issued on an auction basis Lhrough a system of principal dealers. By June 1995, the LOtal outstanding amount of Cagamas bonds was R:vt I 0. 1 billion. f n June 1988, noating rate negotiable certificates of deposit were inLroduced. The interest rates on these cerLificates arc acUusted every three or six months based on the Kuala Lumpur interbanJ.. offered nuc. In January 1989, the cenLral bank issued guidelines to pro\'ide a framework for the growing market in corporate bonds and prombsorr notes. By the end of 1 989, the total funds raised through the issue of pri\'ate debt securities increased to RM 1 . 7 billion from RM 295 million in 1987, and as of December 1994, the issue ofpri,·ate debt securities had reached RM 8.8 billion.

On February 1993, the central bank introduced a new monetary insLrumcnt known as Bank Negara Bills. These cenLral bank bills were introduced in an effort to manage effeclively the liquidity in the (inancial system. As ofjune 1 995, the outstanding amount of Bank Negara Bills amounted to RM 3.9 billion.

The cenrral bank also took steps to develop a marker for corporate bonds. Given the objective of deepening the financial system, viable primary and secondary markets for private debt securities are necessary to provide corporations and institutional borrowers with alternative sources of funds and to gi,·e investors more avenues to invest in a wide range of financial assets. Initial sLeps to this end were taken when the central bank issued guide! i nes on the issue of private debt sccuri tics. A private credit rating agency was incoq:)orated under the name of Rating Agency Malaysia Berhad, which is privately owned; neither the governmen! nor the central bank is involved in its management or operation. The credit srancling of debt issuers is determined independenrly by I he rating agency. Market development for corporate bonds should conu·ibutc significanLly LO active primary and secondary markets for the capital and monc)' market in general.

Modernization of the Payment System

Apart from encouraging greater computerization ancl modernization of bank operations. the central bank also implemented several new arrangements to improve the efficiency of Lhe financial system. The Kuala Lumpur Automared Clearing House came into operation in early 1984 to provide automated processing of checks cleared through the commercial banks. The coverage was subsequently broadened in stages throughout the counLry. The Day One Settlement System was introduced in 1986, giving same-day value to local checks deposited with the

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 133

banks. More import.ant, the Day One Scttlemen t System promoted interest rate stabilit;, as its mechanism ensured that at the end of the day, when all the checks were cleared, those banks with a net surplus would automatically lend funds on an overnight basis to banks with a deficit, at a rate equivalent to the weighted average overnight rate transacted i n the money market that day. Therefore, there was no need for banks to scramble for funds toward the end of the day, which previously had pushed interest rates up to unreasonable levels.

Toward the end of 1989, the Interbank Funds Transfet· System, an online electronic fund transfer system, was implemented to expedite daily interbank fund transfer!) and settlements among participating institutions. This was followed by the introduction of the Scripless Securities Trading System in .January 1990. This is an on-line book-enu·y system that effects and records the trading or govern ment paper and Cagamas bonds (that is, mortgage-backed bonds) between member institutions. l l is an efficient system for sculement between coun terparts, registering securities, and keeping up-to-date records of the swck in security accounts. Since scrips arc not issued, the risk of loss, destruction, and forgery or certificates has also been eliminated.

Modernization of Government Securities Market

The modernization or the government securities market has been a key clement or financial reforms in Malaysia.

Securities Issued by the Government

The governmem issues the following L)'pes of securities: treasury bills, Malaysian Government Securities. and Government Investment Certificates.

Treasury Bills

Treasury bilb are essentiall) money market insu·uments with shortterm maturities not exceeding one year. They are bearer promissory notes issued at a discount. The goverumen t started issuing treasury biUs in 1955 and, until August 1973, these were issued on demand. The rate of discount was predetermined by the government on tl1e recommendation of the central bank. Since August 20, 1973, however, treasut·y bills have been sold by regular weekly tenders in order to promote greater competition in the market and to encourage a wider range or· investors. The amount of issue generally depends on the short-term financing needs of the federal government and market demand. The

©International Monetary Fund. Not for Redistribution

134 Zamani Abdul Ghani

main investors in treasury bills arc the licensed banks, finance companies, and discount houses. The licensed banks and finance companies hold treasury bills mainly for liquidity requirements. As of June 1995, the amount of outstanding treasury bills was RM 4.3 billion.

Malaysian Government Securities

These arc essential capital market instruments with medium- to longterm maturities, ranging from 3 years up to 21 years. The Malaysian Government Securities (MGS) market is the largest component of the Malaysian capital market in terms of primary funds raised. As of the end of June 1995, the amount of MGS outstanding was RM 64.5 billion. These securities are the main vehicle used by the federal government to raise funds for longer-term development pr·ojects.

Government Investment Certificates

These certificates are non-interest-bearing bonds equivalent to MGS. The issuance of Government Investment Certificates (GIC) was necessitated by the establishment of Malaysia's first Islamic bank-the Bank Islam Malaysia Berhacl. Since the operations of an Islamic bank are based on Islamic principles, such a bank cannot, among other things, purchase or trade in MGS, treasury bills, banker's acceptances, or other financial instruments yielding a pr-edetermined fLXed rate of return, or interest. As there is, however, a real need for Islamic banks to hold liquid assets (just like conventional banks) to satisfY statutory liquidity requirements as well as to "park" temporary surplus funds, appropriate alternative financial instruments have to be developed. Even as the original purpose was to cater to the liquidity requirement for Bank Islam Malaysia Berhacl, it should be noted that there are many other Islamic institutions and Muslims in the country that could benefit from the inu·oduction of the GIG.

The crucial issues relating to the introduction of GIG were the determination of a fair rate of return for the investor and the establishment of a suitable basis for trading GTC in the secondary market. As a predetermined interest would not be in line with Islamic banking principles, the alternative would be to pay dividends to the investors. Various options were studied to determine the best basis for deciding a fair rate of return to investors. ln this regard, the Islamic Qard-ai-Hasan principle was eventually adopted, whereby the purchase of GIC by the public is considered a benevolent loan to the government to enable it to undertake projects or provide services for the benefit of the nation. The providers of the funds cannot expect any return on their loans, but they

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 135

can expect the principal amount to be returned in full at maturity. The govcrnmcm is not obliged to provide any reLUrn w the holders of GIC. However, it can, as a sign of goodwill, provide some form of return to the investors; this return on investment would be in the form of dividend<;. To implement this, a Dividend Committee was formed to advise the governmem on the appropriate rate of dividend, which is declarable on the anniversarr date of the GIC issued. Basically, the Committee takes inlO account the economic conditions of the country, the existing yield levels of other llnancial instruments, and the rate of inflation as the basis for its recommendation to the government.

Since the GIC arc intended to be liquid assets for Islamic banks, they must be marketable. Being non-in terest-bearing instruments, they cannot be traded on the conventional yield mechanism. As it is, they can only be transferable at par. To ensttre fairness lO investors, the dividends (if any) declared by the government are shared among holders, based on the period for which they have held them. The cenLral bank also decided to provide last reson facilities to GIC holders by purchasing the certificates at par. Since their introduction in 1983, the amount of GIC issued had increased significantly, from RM 100 million at end-1983 to ltlvt 4.8 billion in June 1995.

Development of Malaysian Government Securities Market

Until the mid-l950s, the amount of MGS issued was insignificant, mainl}' reflecting the small financing needs of the government at that time. The achievement of independence by Malaysia in 1957 and the subsequent emphasis on economic development based on the economic diversification and industrialization strategy required the government to spend massive sums of money to develop the infrastructural base.

To raise funds, the government issued MGS. The following measures were adopted to ensure that MGS were attractive to investors: transactions in MGS were exempted fwm stamp duty; MGS could be tendered as payment for estate dul)' at par value: a higher commission was paid to brokers for facilitating MGS than for other trading; and interest income earned by individual holders of MGS was exempted from income tax.

At the same time, a captive market was created by requiring certain institutions to hold MGS as a mandalOry investment. The aim of this requirement was to ensure some diversification of investors and to secure a stable source of funds for the government's budgetary requirements.

The Employee Provident Fund-the largest provident fund in the country-is J"Cquirecl to invest 70 percent of its total assets in MGS. The National Savings Bank's minimum investment in MGS is set at 65 percent of its lOtal assets. Licensed banks and finance companies, which are re-

©International Monetary Fund. Not for Redistribution

136 Zamani Abdul Ghani

quired to hold a minimum amount of liCJuicl a')seL'>. were encouraged to hold MGS to satisfy this requirement as MGS were designated as liCJuid assets irrespect i"e or their maturity and no cap was imposed on the amount of MGS that could be held and be cotmted as liguid assets. Discount houses were set up to an as keepers of liquidity for government paper.

The buildup of the \'Olume of MCS in the primary issue market in the period 1950-80, however, did not give;' rise tO an active secondary market This was partly due to the imposition of the above mandatory investment requirements on the various institutions, which meant that they tended to keep their MGS until mawrity, and partly because the macroeconomic conditions during the period were not conducive to secondary market transaCLions. Until 1978, interest rates in the deposit market were regulated to the extent that there was l iu le market movement. Yields of MGS in turn remained steady, with very infrequent changes. There was, therefore, little room f()r risk-taking activities.

The inertia in the developmenL or the MCS market was even wally broken in the mid-1980s. The country's public finance deficit had risen b)' 1982 LO an untenable level of 17.9 percenL of GNP, or RM 10.7 billion.

This led the government to ··e,'icw its financial management. The squeeze on the government's resources brought in to focus important issues related to the ov<'rall domestic financial system, including its allocative efficiency, ability to mobilize domestic financial resources, and risk-taking capaci ty. After the deregulation of interest rates in 1978, a serious distortion began LO develop in the system. The yields on MGS were generall)' below those of comparable nongovernmenL financial assets. The differential yield became particularly pronounced in the 1980s. as increased competition for funds in the pt·ivate senOt· resulted in higher commercial lending and deposit rates. One factor contributing to this siwalion was the crowding-out effect of the huge public sector borrowing requirements.

The state of the MGS market after the 1978 deregulation or interest rates ga,·e rise to the following live areas of concern:

l . It discouraged the development or an active secondary market in MGS, thereby limiting the g•·owth of this important segment of the overall capital market. The yields on MGS were regulated and not market determined. ln conu·ast, deposit rates were allowed to be set by the banks after Oetobcr 1978. Previously, deposit rates (like the MGS yields) were determined by the central bank in consultation with the banks. Furlhennore, the bulk of MGS was held in the portfolios of linancial institutions and the b:mployee Provident Funds to satisfy their statutory minimmn requirements, which reduced the availability of MGS in the trading market;

2. It limited the ability of the central bank to regulate and conu·ol the moner suppl)' and credit through active open market operations,

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 137

given that the bulk (more than 80 percent) of MGS were held to meet statutory requirements;

3. The mandatory legal requirements squeezed and "crowded out" the supply of risk capital to private sector corporations, by directing trust institutions to invest in MGS, thereby increasing the premium charged on the more risky corporate obligations. Longterm funds were made available to the public sector at a much cheaper price than shorter-term funds to the private sector;

4. It distorted the interest rate structure of the financial system as financiaJ intermediaries attempted to pass the implicit "tax" on holding MGS partly to borrowers, through higher lending rates, and partly to depositors, through lower deposit rates; and

5. It underestimated the full impact of budget deficits, thereby delaying fiscal adjustment. This is particularly so wherever the rate of interest of MGS is lower than the perceived market rate, which was often the case in Malaysia. The interest charged on the government's borrowing was correspondingly lower, so that the real cost of the deficits was not clearly identified in the budget.

ft was immediately recognized that the yield structure of MGS should be market related to correct the inefficient allocation of scarce funds in the system . Market-determined MGS yields would provide investors with a more accurate assessment of portfolio choices and an appropriate interest rate benchmark for other debt securities of similar maturities. The implication for the government was that it would have to compete with the private sector for funds. Il was aJso clear that tailored measures had to be taken to develop the secondary market.

A plan to develop the MGS market was conceived with the understanding that the successful development of an active secondary market in MGS would simultaneously require: ( I ) appropriate changes in the operating procedures of monetary management in order to increase the role of the market in providing liquidity for the MGS market; (2) reduction of the scope of captive markets in MGS by progressively modifying the statutory requirements and revising related regulations; and (3) modifications in the government's debt-management strategy with a view to moving toward market-related pricing in primary issues, to facilitate secondary u·ading.

The following actions have been taken so far to allow the market to determine MGS rates:

1. Supportive linanciaJ reforms were inu·oduced in 1986 and 1987, including the uppegging of interest rates on deposits; aJiowing the ban king system to maintain its liquidity ratio and statutory reserves ratio on an average basis; expanding the number of money market participants by aJlowing well-capitaJized finance companies to par-

©International Monetary Fund. Not for Redistribution

138 Zamani Abdul Ghani

uc1pate in the interbank money market; using the Kuala Lumpur interbank offered rate as an official indicator of the conditions in the money market; realigning in stages the statutory reserve ratio of the commercial banks, finance companies, and merchant banks to bring about greater competition (this was completed in May 1989); and establishing the Day One Settlement System, under which banks are required to give Day One value for all local checks and other items deposited by customers into their accounts.

2. The central bank also made its ftrst move to issue MCS with market-related coupon rates with effect from 1989, and initiated trading by way of "nudging" operations.3

3. Given the above supportive reforms and the conducive macroeconomic environment, a number of major reforms were introduced in January 1989 to bring about a more effective secondary market for government papers: • A principal dealership system for government securities was in

troduced on January 1 , 1989. A total of ] 8 principal dealers were appointed, consisting of 4 commercial banks, 7 merchant banks, and 7 discount houses. These dealers underwrite the primary issues of MGS and are obliged to provide two-way quotations in the secondary market;

• At the same time, an auction system for the shorter-maturity MGS primary issues (maturities of 10 years and less) was also implemented. Howe\'er, the longer-dated issues are still offered on a subscription basis; and

• The size of the weekly treasury bill offering was standardized at RM lOO million per issue. The same principal dealers system was also introduced for the auction of the treasury bills.

To further refine the method of creating an MCS market attuned to real market forces, the central bank altered the basis of submission of bids by the principal dealers. Under the auction system for MGS issues instaJled in early 1989, the central bank would fix the coupon rate of the issue based on the prevailing market yield curve. The principal dealers would submit their bids on a price basis. The cutoff price below which bids wc•·e not accepted was determined by the bids received and by tJ1e amount of MGS the government wanted to issue. As the central bank had set the coupon rate in advance, a change in the market rates during the interval between the announcement of the issue and the actual auction elate would result in bid prices being different from the par value of the MCS. The government therefore faced uncertainty in the

3'"Nudging·· operations are transactions undertaken by the central bank to buy and sell securiltes w1th the hnanc1al 1nshtutions in order to activate secondary market trading aCtivities.

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 139

amount of funds that it could receive. Another problem with the fixing of the coupon rates was that the market tended to move toward the announced coupon rate, thet·eby disturbing the market. To ensure that the government obtained the funds in the quantity that was required, and to allow the market to determine the price of capital, it was decided that from October 1990, principal dealers would be required to submit their bids on a yield basis. The coupon rate for the MGS issue would be determined by the yield bids submitted. Competition among the principal dealers would therefore be also enhanced.

Flexibility of operation is important to the securities dealers. In recognition of this, the central bank freed the discount houses from rigid portfolio restrictions. Previously, the discount houses were required to maintain al least 75 percent of their investments in government paper and Cagamas bonds. This restriction was lifted in June 1990. Discount houses are now free to decide their own portfolio structure. This flexibility is a prerequisite for the effective transformation of the discount houses from their keepers-of-liquidity role to that of true securities dealers. At the same time, discount houses have also been allowed to invest in paper with original maturities of up to ten years, up from the previous limit of five years.

Given all the above reforms, the MGS market seems poised to develop into a truly efficient and liquid market in the years ahead. This scenario is more conceivable now than a few years ago. The major challenge in the near future is to formulate and implement measures that will progressively reduce the size of the captive market. One way to do this is to regularize the issuance of MGS. In time, the MGS market should become more professional, and the central bank could conduct open market operations more effectively. The measures and reforms already undertaken will be continued, and additional in novations ,.yjJl be introduced. Moreover, once the cash market is sufficiently deep, the setting will be appropriate for the introduction of financial futures.

MGS Market Development and Monetary Policy

The most important institutional reform was the appointment of a panel of principal dealers with whom the central bank could conduct its open market operations on its own initiative. A total of 18 financial institutions ( 4 commercial banks, 7 merchant banks, and 7 discount houses) were originally appointed as principaJ dealers for MGS. Another 5 commercial banks were accorded principal dealer status in 1990, bringing to 23 the total number of principal dealers for government securities.

In June 1990, the principal dealer system for treasury bills was also extended to the commercial banks and merchant banks, which are the

©International Monetary Fund. Not for Redistribution

140 Zamani Abdul Ghani

principal dealers for MGS. Previously, only the seven discount houses were principal dealers for treasury bills. The main responsibilities of the principal dealers are to underwrite new issues of MGS and provide twoway quoLations in the secondary market for selected issues. Only the principal dealers have access to the central bank's discount ""indow. Moreover, the central bank's open market operations woulcl be conducted only through these dealers. As such, the central bank's role in the money market has changed from one of responding to the needs of each individual institution to one of maintaining liquidity in the financial system as a whole. Individual institutions-other than principal dealersthat have excess liquidity or are short of funds will now have to cover their positions in the market, and no longer with the central bank.

Unlike the past practice of accepting advance subscriptions from all institutions, issues of MGS with maturities of up to l 0 years are now auctioned through the principal dealers, except in the cases of the Employee Provident Funds and the National Savings Bank. Longer-dated issues are still offered on a subscription basis for these two institulions. To fully integrate the primary issues market into a completely marketbased system, the next step would obviously be to introduce auctions of MGS for all maturitics. Once the auction system is wholl)' established, the longer-term rate structure should improve. When this happens, the undistorted MGS rates could act as true benchmarks for rationalizing longer-term bond rates in the private sector.

Before the introduction of the Day One Settlement System, the overnight rate for interbank funds could be highly volatile. One of the preconditions required for the development of an active secondary market is interest rate stability, although not to the extent that the rates do not move at all over long periods. The Day One Settlemem System introduced in 1986 promoted interest rate stabili ty, as already mentioned.

To further improve the operational efficiency of funds and securities transfers and thus enhance monetary policy transmission, the cenu·al bank established a "scripless" book-e!1lry securities trading and funds transfer system known as SPEEDS. This system comprises an Interbank Funds Transfer System to effect and record transfers of funcls between the central bank and the participating institutions, and among the participating institutions themselves; and a Scripless Securities Trading System to effect and record the trading of MGS, u·easury bills, GIC, Bank Negara Bills, and Cagamas bonds, collectively known as SSTS securities.

Essentially SPEEDS is a "paperlcss" transfer system, whereby paper documents have been r·eplaccd by electronic transfers through computers located on the premises of all the participating instiLUtions. The system provides a book-entry method for the confirmation, transfer, recording, and settlement of u·ade in SSTS securities. Previously, tracl-

©International Monetary Fund. Not for Redistribution

Financial Reforms in Malaysia 141

ing in these <;ecurities required the exchange of letters, movement of papa securities for registration of new ownership, and the issue of payment instructions. The new system enhances the ease of trading and the speed at which it can be effected, and another important advantage is that large denominations of securities are no longer a hindrance to small-time investors, because the book-entry system allows the large denominations to be split into smallct· amounts, thereby significantly broadening the potential investor base for the SSTS securities.

Concluding Remarks

Since the establishment of Bank Negara Malaysia in 1958 as the nation's monetary authority, the Malaysian financial system has evolved into one of the more developed and liberal systems in the region, able to service the needs of the expanding and changing structure of the Malaysian economy.

During the past 35 years, the Malaysian economy has undergone profound structural changes, evolving from a primary commodity producer into an increasingly diversified and broad-based economy witl1 an expanding industrial base. The changes in the economy have been most marked in the last five years, which also saw the most intense development of the financial system. The banking system has matured. The deregulation of the financial system, which was stalled by the recession of the late 1980s, resumed and intensified, with the aims of increased competition, increased depth in the money market, and further development of the capital market, particularly the secondary market for MGS.

To a large extent, this prog1·ess reflected the conduct of macroeconomic policies and strategies geared toward the industrialization and modernization of the economy and the effective implementation of a market-oriented and outward-looking economic system. More important was tl1at these policies were implemented in a pragmatic and flexible manner, with a willingness by the government to change policies quickly, and that these policies became market based.

Concomitant with the inslilLllional reform, structural reform of the monetary system proceeded with vigor. The most important step was the complete deregulation of tlle interest rate regime in February 1991, when the base lending rate of the banking institutions was completely freed from the administrative control of the cen u·al bank. This reform measure created a new in terest rate regime, whereby i nterest rates were determined by the dictates of market forces. This important step means mat Malaysia is now one of the few financial markets in the region witll an interest rate ,-egime free of government control.

©In

tern

atio

nal M

onet

ary

Fund

. Not

for R

edis

tribu

tion

I I

Mer

chan

t Ban

ks*

Dis

coun

t H

ouse

s•

Ass

ets:

RM

23.

6b

Asse

ts: R

M 9

.3b

Depo

sits

: RM

14.

6b

Loan

s: R

M 11

.6b

7 di

scou

nt h

ouse

s

12 m

erch

ant

bank

s 17

bra

nche

s

Ap

pen

dix

I

Str

uc

ture

of

the

Ma

lay

sia

n F

ina

nc

ial

Sy

ste

m

(As

at D

ecem

ber 3

1, 1

994)

The

Ba

nkin

g I

nstit

utio

ns

Cen

tral

Ban

k ol

Mal

aysi

a As

sets

: RM

92.

8b

of w

hich

Ex

tern

al r

eser

ves:

RM

68.2

b 12

bra

nch

offic

es

I I

Isla

mic

Ban

k*

Com

mer

cial

Ban

ks•

Fina

nce

Com

pani

es•

Asse

ts: R

M 3.

3b

Asse

ts: R

M 23

9.2b

As

sets

: RM

73.

5b

D epo

sits

: RM

2.9b

De

posit

s: RM

160.

3b

Dep

osits

: RM

57.

3b

Loan

s: R

M 1

.2b

Loan

s: R

M 1

34.2

b Lo

ans:

RM

50.1

b

No.

of b

ranc

hes:

60

37 b

anks

40

fin

ance

com

pani

es

of w

hich

: 86

0 fin

ance

com

pany

23

dom

estic

of

fices

(to

tal a

sset

s: R

M 1

84.7

b)

14 fo

reig

n (to

tal a

sset

s: R

M 54

.9b)

1,28

3 ba

nk b

ranc

hes

of w

hich

: 1,

139

dom

estic

ban

ks

144

fore

ign

bank

s

I Fo

reig

n Ba

nks

Rep

rese

ntat

ive

Off

ices

•

33 o

ffic

es

l O

ffsh

ore

Ban

ks

(lab

uan

IOFC

)*

35 o

ffsh

ore

bank

s

N

llJ

3

llJ

::I

©In

tern

atio

nal M

onet

ary

Fund

. Not

for R

edis

tribu

tion

Leas

ing

Com

pani

es•

Ass

ets:

RM

8.8

b N

o. o

f co

mp

anie

s: 1

56

Fact

orin

g C

ompa

nies

• A

sset

s: R

M 1

b N

o. o

f co

mpa

nies

: 2

Ven

ture

Cap

ital

Com

pan

ies•

S

ize

of f

unds

: RM

0.5

b N

o. o

f co

mpa

nies

: 17

Cre

dit T

oken

Com

pani

es•

14 is

suin

g in

stitu

tions

Insu

ranc

e C

ompa

nies

' A

sset

s: R

M 2

1 b

of

whi

ch:

Life

insu

ranc

e: R

M 1

4.9

b G

ener

al in

sura

nce:

RM

6.1

b

61 i

nsur

ance

com

pani

es

of w

hich

: 52

dom

estic

9

fore

ign

40 g

ener

al in

sura

nce

com

pani

es

4 li

fe in

sura

nce

com

pani

es

14 c

ompo

site

life

and

gen

eral

3

rei

nsur

ance

co

mpa

nies

Isla

mic

Insu

ranc

e 2

com

pani

es (

TAKA

FUL)

Off

shor

e In

sura

nce

Co

mpa

nies

' N

o. o

f com

pan

ies:

5

'Sup

ervi

sed

by th

e Ce

ntra

l Ban

k.

'Reg

iste

red

with

the

Cen

tral

Ban

k.

No

nb

an

k F

ina

ncia

l In

term

ed

iari

es

Deve

lopm

ent

Fin

ance

Ins

titu

tion

s•

Ass

ets:

RM

9.7

b

1. M

alay

sia

Indu

stri

al D

evel

opm

ent

Fina

nce

2. D

evel

opm

ent

Ban

k of

Mal

aysi

a

3. I

ndus

tria

l Ba

nk o

f M

alay

sia

Ber

had

4. S

abah

Dev

elop

men

t B

ank

5. A

gric

ultu

re B

ank

of M

alay

sia

6. S

abah

Cre

dit

Corp

orat

ion

7. B

orne

o D

evel

opm

ent

Corp

orat

ion

Uni

t Tr

usts

19

uni

t tr

ust

com

pani

es

51

unit

trus

t fu

nds

Mar

ket v

alue

RM

35.

9b

AS

N a

nd A

SB

S

ize

of f

unds

RM

21.

1b

No.

of

unit

hol

ders

: 5.2

m

Pro

pert

y Tr

usts

4

pro

perty

tru

st fu

nds

Sav

ings

lns

lltut

ions

1.

Nat

iona

l Sav

ings

Ban

k A

sset

s: R

M 5

.4b

13

mai

n br

anch

es

465

min

i· a

nd s

ub-b

ranc

hes

660

post

off

ices

wit

h s

avin

gs b

ank

faci

litie

s

2. U

rban

Cre

dit

Coop

erat

ives

A

sset

s: R

M 6

.2b

of w

hich

Co

oper

ativ

e Ce

ntra

l Ban

k A

sset

s: R

M 2

. 7b

3. R

ural

Cre

dit

Coop

erat

ives

A

sset

s: R

M 4

b of

whi

ch

Ban

k R

akya

t A

sset

s: R

M 3

.3b

Hou

sing

Cre

dit

Inst

itut

ions

A

sset

s: R

M 2

.5b

Mal

aysi

a B

uild

ing

Soci

ety

Born

eo H

ousi

ng M

ortg

age

Gov

ernm

ent

Hou

sing

Loa

n D

ivis

ion

Out

stan

ding

Loa

ns R

M 1

3.4

b

CA

GA

MA

S B

ERH

AD

Pro

vide

nt a

nd P

ensi

on F

unds

A

sset

s: R

M 9

7b

1. E

mpl

oyee

s P

rovi

dent

Fun

d A

sset

s: R

M 8

4.5

b N

o. o

f con

trib

utor

s: 7

.27

m

2. S

oci

al S

ecur

ity

Org

aniz

atio

ns

Ass

ets:

RM

3.8

b N

o. o

f co

ntri

buto

rs: 6

.95m

3. A

rmed

For

ces

Fund

A

sset

s: R

M 3

b N

o. o

f co

ntri

buto

rs: 9

7,00

0

4. O

ther

Sta

tuto

ry a

nd P

rivat

e P

rovi

dent

Fun

d A

sset

s: R

M 5

.7b

No

. of

cont

ribu

tors

: 17

1 ,O

OOm

Pilg

rim

s M

ana

gem

ent

and

Fun

d B

oard

A

sset

s: R

M 2

.6b

Cre

dit

Gua

rant

ee C

orpo

rati

on

Ass

ets:

RM

0.8

b

Mal

aysi

a E x

port

Cre

dit

Insu

ranc

e Be

rhad

A

sset

s: R

M 0

.1 b

Rat

ing

Age

ncy

Mal

aysi

a B

erha

d A

utho

rize

d ca

pita

l: R

M 2

0m

©International Monetary Fund. Not for Redistribution

144 Zamani Abdul Ghani

Appendix 11

Statutory and Liquidity Requirements

Statuwry and liquidity requirements are important policy instruments used by the central bank to achieve its monetary objectives. The trend has been to ease the burden of carrying reserves by allowing the financial institutions more flexibility in meeting the requirements. As of February 1987, the commercial banks, finance companies, and merchant banks were allowed to observe the minimum liquidity requirement on a two-week average basis, subject to a maximum daily \radation of 2 percentage points above or below the requirement. Previously, this requirement had to be met daily. In addition to lowering the costs of operations of the financial institutions, the measure was also intended to dampen the volatility in the interbank market interest rates caused by banks seeking funds lO meet the daily ,·equirements. Similarly, from January 1989, the banking institutions were allowed lO observe an average statuwry reserve ratio within a 0.5 percentage point band over a two-week period. The statutory reserve ratio for the banking institutions was realigned so that all of them had a common ratio, thus placing them on a more even footing and p1·omoting greater competition. The pdmary liquidity ratios of the finance companies and commercial banks wc1·e abolished in January 1989 and June 1990, respectively.

Reginning July I , I 990, the commercial banks, finance companies, and merchant banks were required to observe the statuto1·y 1·eserve ratio and the mini

mum liquidity requirement by averaging eligible liabilities instead using a single base day. To illusu·ate, the statutory reserve ratio and minimum liquidity requirement observed dlllingJuly 1-15, 1990, were computed based on the av

erage daily amount of eligible liquidities in the base period June 1-15, 1990. The statutory reserve ratio and minimum liquidity requi1·ement for July 18-31, 1990, were based on the average daily amount of eligible liabilities in the base period June 1 6-30, 1990. With the avei-aJ;,ring of eliJ;,rible liabilities, the computation of both statutory reserve ratio and minimum liquidity requirement now have a common base period. At present, the stawtory reserve ratio stands at 1 1 .5 percent of the eligible liabilities base of the linancial institutions.