development of ethiopian steel industries: challenges

TRANSCRIPT

FDRE, Policy Study and Research Center

Industrial Policy Study and Research Department

Development of Ethiopian Steel Industries: Challenges, Prospects, and Policy Options

(2015 –2025)

FDRE, Policy Study and Research Center - PSRC

and

Adama Science and Technology University, ASTU

By

Tesfaye G/Michael (Msc)

Moges Tufa (MA)

Niguse Assefa (Msc)

Teshome Abdo (PhD)

Jeylan Aman (PhD)

Lemi Guta (PhD)

Addis Ababa, Ethiopia

February, 2017

II

FDRE, POLICY STUDY AND RESEARCH CENTER

About PSRC FDRE, Policy Study and Research Center founded in March 2014 as a government policy and strategy research center. It is established by recognizing the need for policy related researches and knowledge based decision making process in the fast growing and transforming economy of Ethiopia. The PSRC is expected to be the major think tank center in Ethiopia that analyses policy implementation, structural and programmatic issues, and generate policy and strategy proposals. The PSRC has five major departments and one is Industrial Policy Study and Research Department (IPSRD). For more information as well as other publications by PSRC and its affiliates, go to www.PSRC.gov.et FDRE, Policy Study and Research Center P.O.Box 1072/1110 Tel: +251-11-6613767 +251-11-6610462 Fax: +251-11-6621821 E-mail: [email protected] Website: www.psrc.gov.et ABOUT THIS RESEARCH REPORTS The FDRE, policy study and research center (PSRC) research reports contain research materials from PSRC and/or its partners. The researches are circulated to the concerned Ministries and related sectors in order to stimulate discussion and critical comment. The opinions in this research are those of the authors and do not necessarily reflect that of PSRC‟s. Comments may be forwarded directly to the IPSRD and the authors through e-mail: [email protected]. Report Citation: It is cited as Industrial Policy Study and Research Department (IPSRD) and Adama Science and Technology University-ASTU. Development of Ethiopian Steel Industries: Challenges, Prospects, and Policy options (2015-2025).

III

Preface

As stipulated in the Second Growth and Transformation Plan (GTP II), Ethiopia is committed to tuning its growth direction from agriculture-led to industry-led economy. In this plan, the role of industries in general and the manufacturing sector in particular is considered as the main sector towards which the economy evolves. Today, even though the service sectors have come to dominate the economies in most of the rich countries in the west, manufacturing remains critical to the rapid economic transformation of all countries especially developing countries like Ethiopia. The Ethiopian government has recognized the importance of this sector and paid greater attention than ever.

Based on the industrial development strategy of Ethiopia, one of the priority sub-sectors in the manufacturing sector is metal and engineering industries. The study has conducted a broad investigation on Ethiopian steel industries with special emphasis on their challenges and prospects and to forwarded policy recommendations that will serve as point of departure for a medium and long-term development plan of the steel industries. It has considered technology selection, resources base, institutional arrangement, human power requirements, sources of finance, and the environment aspects for development of the sub-sector for the coming ten years and beyond.

A number of consultative and validation workshops had been done with the stakeholders and professionals which enabled us to enrich the content of the research. Moreover, important lessons have been taken from successful countries in this field like China. Some insightful lessons have been gained from the benchmarking visit such as: developing necessary human capital by establishing and expanding support institutions, continuous technology progress by investing in and buying technology (investment in R & D and acquisition of technology from advanced countries in comprehensive packages), and huge public investment in expansion of productive facilities. The study identified major policy and strategic issues such as build human resource development system, minimize heavy dependence on imports of raw materials by exploring potential local resources, improve product diversification, establishing and capacitating R&D centers, build market research capability, creating access to finance and update incentive package, upgrading infrastructure, enforcing sector-specific energy and environment policies and regulations, expanding and enhancing collaboration between industry and support institutions which would be supposed to implement for the coming ten years and beyond. The FDRE policy study and research center, Industrial policy study and research department believes that the research output of this study would help all stakeholders to acquire clear development directions for the development of specific programs and projects for further development of steel industries. Amare Matebu Kassa (PhD) Lead Researcher and Coordinator Industrial Development Policy Study and Research Section

IV

Executive Summary Ethiopia has been undergoing a rapid economic growth with a conviction of realizing the vision of

joining middle income countries by 2025. To realize this vision, it is firmly believed that growth in the

industrial sector plays a seminal role. As stipulated in the Second Growth and Transformation Plan

(GTP II), the nation is committed to tuning its growth direction from agriculture-led to industry-led

economy. In this growth and transformation plan, therefore, the role of industries in general and the

manufacturing sector in particular is extremely vital, and our industries need to align themselves

towards the attainment of this vision demanded by the economy.

There is a general consensus that the manufacturing sector is the main engine of economic growth and

structural transformation of a nation. With full recognition of the importance of manufacturing in the

socioeconomic transformation of the nation, the Ethiopian government has recently paid greater

attention than ever to this sector. The manufacturing sector comprises many subsectors including the

steel industry subsector, which has been the target of this project.

Steel industry is believed to be indispensable for a country like Ethiopia, which aspires to undergo a

rapid process of industrialization and economic transformation. Development history of most nations

demonstrates that, during their course of economic development, they relied heavily on their domestic

steel industry to meet the requirements of faster development in other industrial and non-industrial

sectors. Realizing the significance of steel industry in the development of the national economy, the

Ethiopian government has taken a number of initiatives to develop and transform the subsector.

As one of the initiatives aimed at overhauling the subsector, this project was initiated by FDRE Policy

Study and Research Center, in collaboration with Adama Science and Technology University. The

study sought to conduct a comprehensive investigation into the Ethiopian steel industries with special

emphasis on their challenges and prospects and to forward policy recommendations that will serve as

point of departure for a medium and long-term development plan of the subsector.

To realize the objectives of the project, both primary and secondary data were generated by employing

carefully designed methodology. Primary data that are needed for the purpose of the project have been

obtained through on-site observations of the existing steel industries and factories, survey

questionnaire, and in-depth interviews with key informants from selected ministries, executives and

experts from steel industries, Metal Industry Development Institute (MIDI), Ethiopian Mechanical

V

Engineering Association and other stakeholders. Secondary data were generated from both international

and national documents. The latter include the Growth and Transformation Plans (GTP I & GTP II) and

GTP I evaluations, Ethiopian Industrial Roadmap, Ethiopian Industry and City/Urban Development

Policy and Strategy Document, different steel-related studies (KOICA, JICA, MIDI) and other

documents from the Ministry of Mining, Ethiopia Power Authority, Ministry of City and Urban

Development, Ministry of Industry, Metal Industry Development Institute, Environmental Protection

Authority, Geological Survey, Planning Commission, Ethiopian Customs Authority, Ethiopian Railway

Corporation, Banks and other pertinent sources. Moreover, a visit has been made to China to

benchmark best practices of the country in steel industry.

Drawing on the data accessed from different sources, a number of key activities have been conducted to

develop the steel industry policy document. In the first place, developments in the steel industry at a

global level were addressed with particular emphasis on prominent issues such as steelmaking process

and technology, production, consumption, import and export trends. Likewise, a regional level analysis

of steel industry was conducted by taking a comprehensive look at the status of the sector in the African

continent and by focusing on issues pertaining to steel production and consumption.

The most important part of the steel industry analysis devoted itself to the assessment of the steel

industry in Ethiopia. In this analysis, the current profile of steel industries in the country and their

current performance, their production and consumption trends, and their challenges are particularly

highlighted. A review of various steel industry-related documents and studies was also conducted. From

this comprehensive analysis, it has been found out that the Ethiopian steel industry currently operates

under conditions of constrains in terms of raw materials, skilled workforce, technological capacity,

research and development, working capital, production capacity and efficiency, product diversification

and value addition, infrastructure development, market research and orientation and, above all, absence

of policy and strategic frameworks that guide the development direction of the subsector.

Useful findings were also drawn from the PESTLE and SLOC analysis of the Ethiopian steel industry.

The key findings from the PESTLE analysis indicate the presence of favorable political, economic,

social, technological, legal and environmental conditions that also serve as drivers for the development

of steel industry. Likewise, based on the SLOC analysis, some critical policy issues have been

identified for the Ethiopian steel industry development. These policy issues are:

Building a human resource skill development system that ensures the availability of required

human capital;

VI

Minimizing heavy dependence on imports of raw materials by exploring and exploiting

potential local resources;

Improving product diversification (product mix) and value addition of steel products;

Establishing and capacitating R&D centers at company and national level to imitate, improve

and create technology;

Building local and international market research capability and market information system;

Creating access to finance (bank loan, foreign currency) and updating incentive packages for

steel industries as strategic development subsector;

Upgrading and setting up infrastructure facilities and separate power transmission;

Enforcing sector-specific energy and environment policies and regulations and conducting

periodic environment and energy audit;

Expanding and enhancing collaborations between the industry and support institutions; and

Developing steel industry strategy and roadmap.

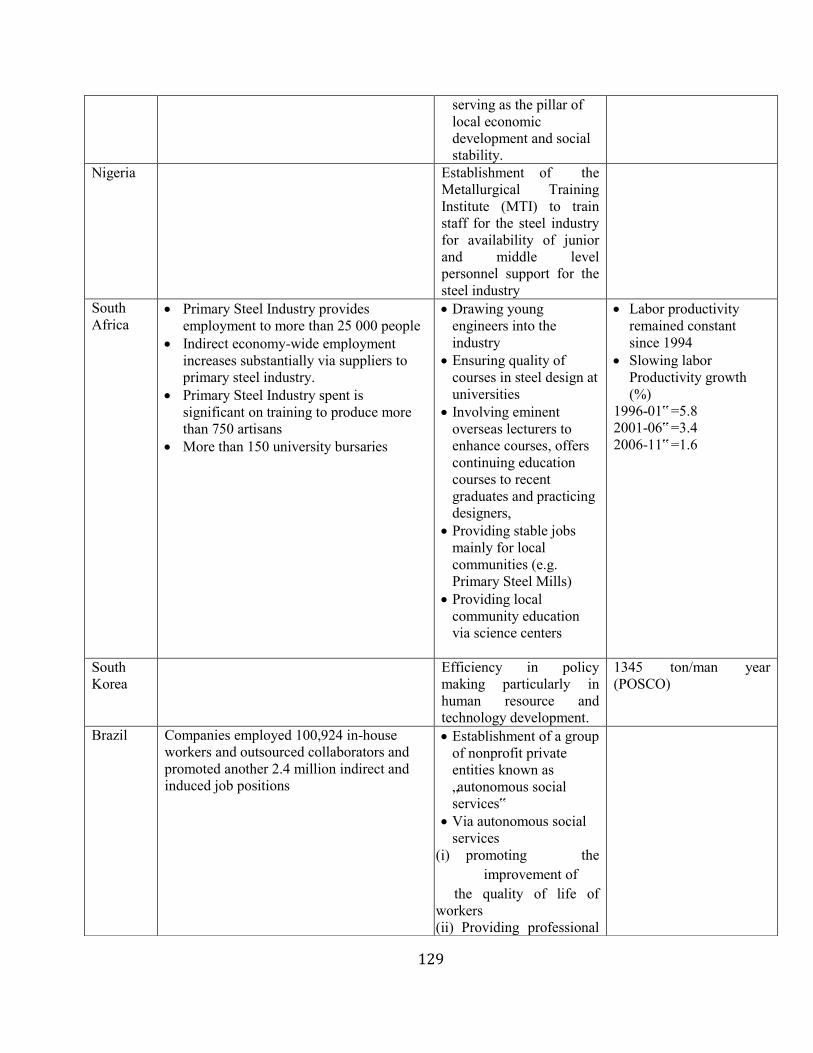

A comparative analysis was conducted by surveying the status of steel industries in selected countries

(India, China, South Korea, Brazil, South Africa, Nigeria, and Kenya), which are believed to be

exemplary for Ethiopia in the development of her steel industry. The comparison has particularly

focused on key issues pertaining to raw materials, human resource development, production,

technology, policy and regulatory frameworks, market, energy and environment. Accordingly, from the

comparative analysis made on these focus areas, some useful lessons and experiences which are

believed to be of particular importance for the Ethiopian steel industry have emerged.

As stated earlier, a benchmarking visit was also made to China by the study team to draw lessons on the

track and past trends in the development history of China‟s steel industries. Accordingly, some

insightful lessons have been gained from the benchmarking visit. Some of the critical observations are:

developing necessary human capital by establishing and expanding support institutions, continuous

technology progress by investing in and buying technology (investment in R & D and acquisition of

technology from advanced countries in comprehensive packages), and huge public investment in

expansion of productive facilities. In particular, it was found out that investing heavily on human

resource, productive capability and technology, accompanied by effective regulatory systems, makes a

significant contribution to the transformation the sector.

Drawing on inputs gained from global and regional analysis of steel industry, data obtained from the

analysis of various primary and secondary sources on Ethiopian steel industry, findings from PESTLE

and SLOC analysis, experiences gained from the comparative study and benchmarking, a National

VII

Steel Industry Policy (2015/16-2025), along with strategic objectives, strategic interventions and

implementation framework, has been proposed. The vision of the policy is to transform the Ethiopian

steel industry by exploiting locally available natural resources, importing essential resources for some

years to come, and adopting state of the art technology to ensure domestic self-sufficiency in terms of

production, consumption, quality and techno‐economic efficiency and gradually transit the industry to

export-oriented, thereby upgrading its profile to a Sub-Saharan leader by 2025.

VIII

Contents

Executive Summary ..................................................................................................................................... III

List of Tables ................................................................................................................................................... XI

List of Figures .............................................................................................................................................. XIII

1. Background of the Study .................................................................................................................... 1

1.1 Objectives of the study .................................................................................................................. 2

1.1.1 General Objective ................................................................................................................... 2

1.1.2 Specific Objectives ................................................................................................................ 2

1.2 Study Framework and Methodology ......................................................................................... 2

2. Global Analysis of Steel Industry .................................................................................................... 7

2.1. Steelmaking processes and technology .................................................................................... 8

2.1.1. Raw materials .......................................................................................................................... 8

2.1.2. Steel industry value chain ................................................................................................. 14

2.1.3. Steel production technologies .......................................................................................... 15

2.2. Global production trend of steel .............................................................................................. 18

2.2.1. Worldwide crude steel production ................................................................................. 18

2.2.2. Regional analysis of steel production ............................................................................ 19

2.2.3. Major steel-producing countries ..................................................................................... 20

2.2.4. TOP 10 steel producing companies 2014 ..................................................................... 21

2.3. Global consumption trends of steel ........................................................................................ 21

2.3.1. True steel use (finished steel equivalent) ..................................................................... 22

2.3.2. Global steel use per capita ................................................................................................ 23

2.3.3. Steel demand by end-use industry .................................................................................. 23

3. Regional Production and Consumption Analysis of Steel .................................................. 25

3.1. Steel making process and technology .................................................................................... 26

3.1.1. Raw materials ....................................................................................................................... 26

3.1.2. Steel production technologies of Africa ....................................................................... 27

3.2. Regional production trend of steel .......................................................................................... 29

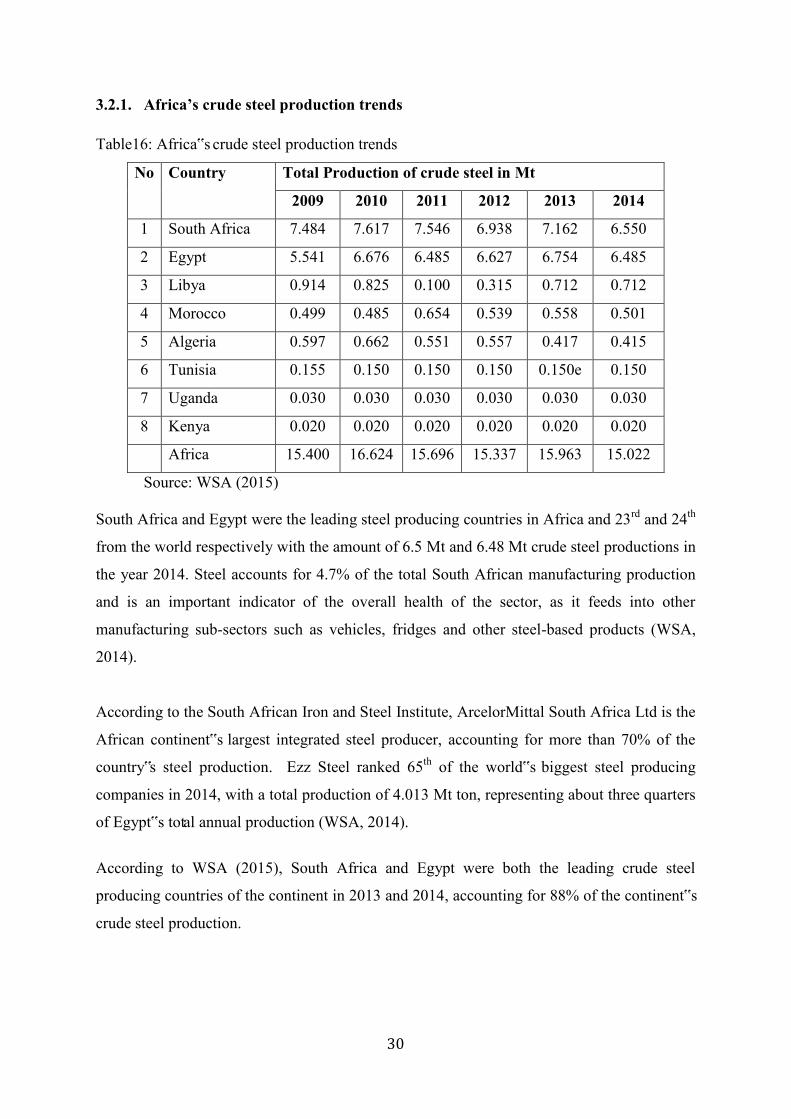

3.2.1. Africa‟s crude steel production trends .......................................................................... 30

3.3. Regional Consumption trends of steel ................................................................................... 31

3.3.1. Apparent steel use per capita (finished steel products) ............................................ 32

3.3.2. True steel use per capita (kg finished steel equivalent)............................................ 33

3.4. Analysis of regional steel trade ................................................................................................ 33

3.4.1. Leading exporters of semi-finished and finished steel products ........................... 33

3.4.2. Import of steel products ..................................................................................................... 34

3.4.3. Indirect net export of steel ................................................................................................ 35

IX

3.5. Global and regional steel demand drivers ............................................................................. 36

4. Assessment of Ethiopian Steel Industry .................................................................................... 37

4.1 Profile of Steel Industries .......................................................................................................... 38

4.1.1 The status of some selected steel industries ................................................................ 39

4.1.2 Enabling capabilities of local steel industries ............................................................. 46

4.2 An overview of performance of steel industries ................................................................. 50

4.2.1 Human resource capacity .................................................................................................. 51

4.2.2 Raw materials ....................................................................................................................... 55

4.2.3 Technological capacity ...................................................................................................... 58

4.2.4 Ethiopian steel industries value-chain ........................................................................... 61

4.3 Production trend of steel industries/firms ............................................................................. 63

4.3.1 Local production by sector ............................................................................................... 63

4.4 Challenges of the sub-sector ..................................................................................................... 72

4.4.1 Challenges of Ethiopian steel industries in 2007E.C ................................................ 73

4.5 Gross value of products of iron and steel industries (public and private) ................... 74

4.6 Value added ................................................................................................................................... 75

4.7 Market trend of steel industry in Ethiopia ............................................................................ 75

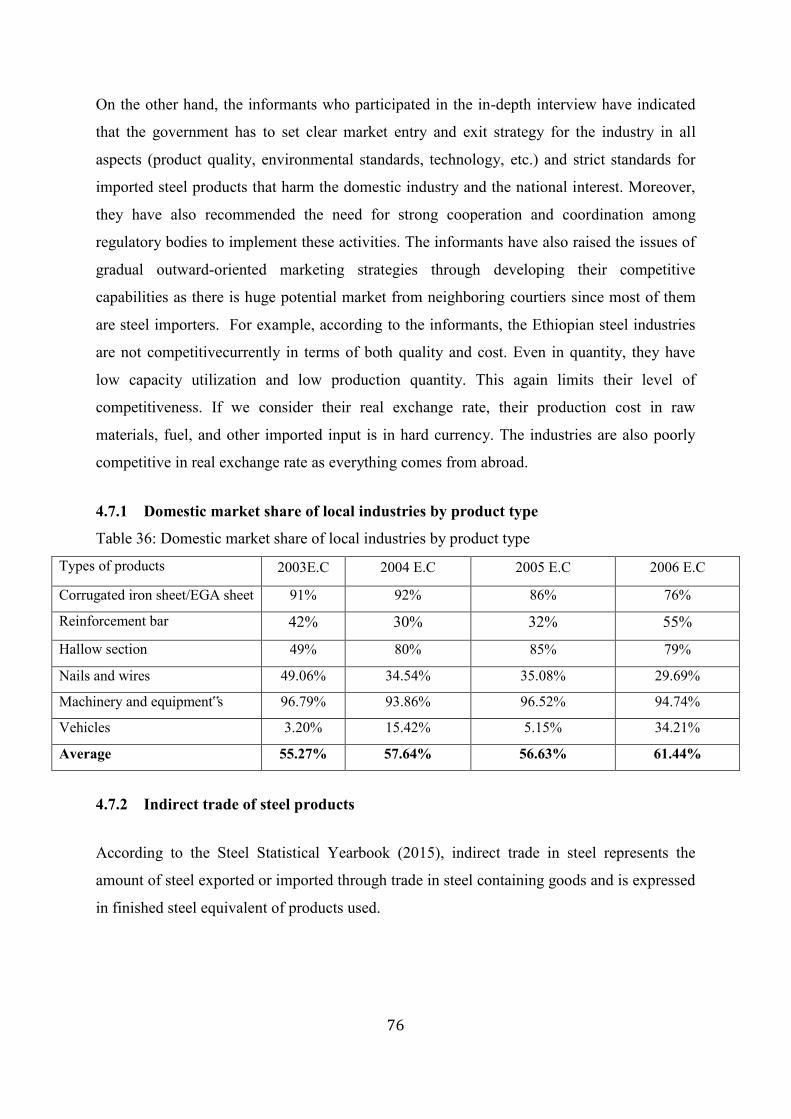

4.7.1 Domestic market share of local industries by product type .................................... 76

4.7.2 Indirect trade of steel products ........................................................................................ 76

4.8 Trends of different steel per capita consumption ................................................................ 77

4.9 Investment in the sector.............................................................................................................. 79

4.10 Potential steel demand drivers in Ethiopia ....................................................................... 79

4.11 Energy utilization..................................................................................................................... 81

4.12 Environmental standards ....................................................................................................... 82

4.13 Review of steel industry-related documents and studies.............................................. 83

4.13.1 Roles of steel industries in economic growth and development ............................ 84

4.13.2 Analysis of Ethiopian steel-related documents ........................................................... 85

4.13.3 Industry Development Strategy of Ethiopia ................................................................ 86

4.13.4 Ethiopian Industrial Roadmap ......................................................................................... 87

4.13.5 Investment incentives and regulatory frameworks .................................................... 88

4.13.6 Study conducted on Metal and Engineering Industries in Ethiopia...................... 89

4.13.7 National growth and development direction ............................................................... 90

5. PESTLE and SLOC Analysis ............................................................................................................. 93

5.1 Global and regional PESTLE analysis of the steel industry ............................................ 93

5.2 PESTLE analysis of Ethiopian steel industry ...................................................................... 94

5.3 Summary of SLOC factors ........................................................................................................ 97

X

5.4 Selected critical policy issues ................................................................................................ 102

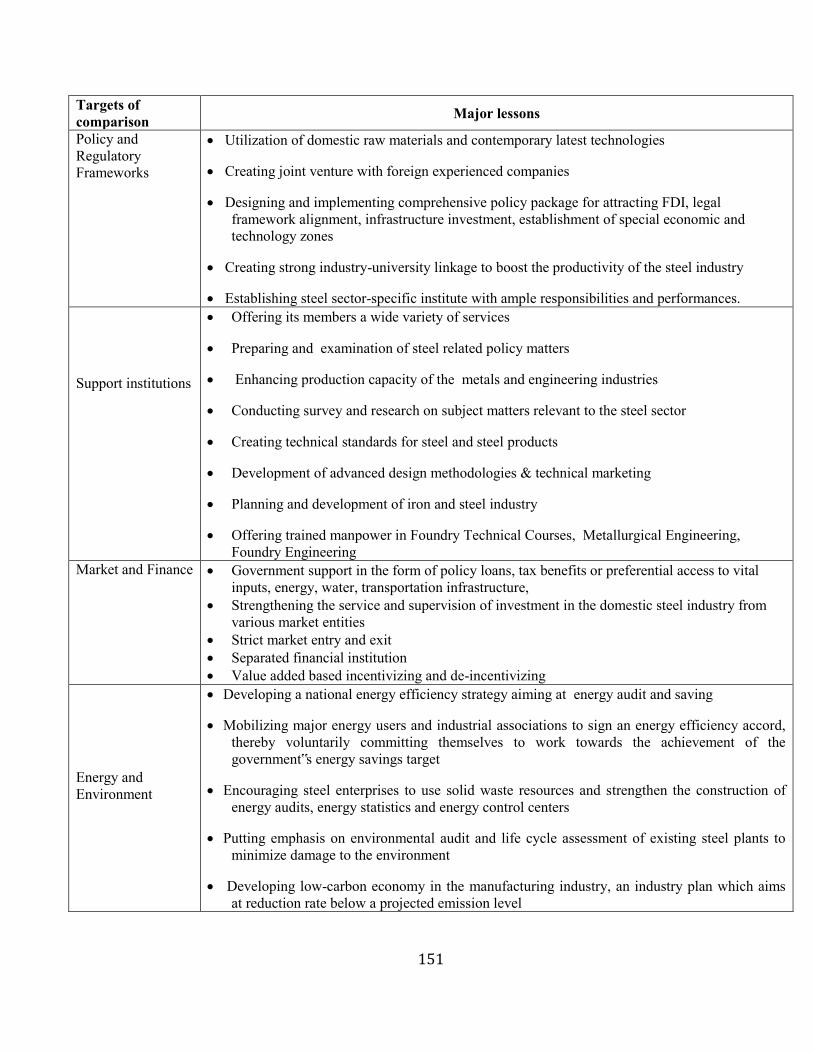

6. Comparative Analysis .................................................................................................................... 117

6.1. Raw materials ............................................................................................................................. 117

6.2. Human resource ......................................................................................................................... 122

6.3. Production ................................................................................................................................... 130

6.4. Technology ................................................................................................................................. 132

6.5. Support institutions ................................................................................................................... 135

6.6. Policy and regulatory frameworks ....................................................................................... 137

6.7. Market and finance ................................................................................................................... 145

6.8. Energy and environment ......................................................................................................... 147

7. National Steel Industry Policy: Vision, Goal, and Strategic Interventions ................ 152

8. Implementation Framework ...................................................................................................... 164

References ................................................................................................................................................... 173

Annex 1: Iron ore occurrence and deposits of Ethiopia .................................................................. 177

Annex 2: Summary of SLOC factors ................................................................................................... 178

Annex3: Experience from Benchmarking ....................................................................................... 180

XI

List of Tables

Table 1: Quality of Fe raw materials .......................................................................................................... 9

Table 2: Steelmaking raw materials, properties and application for steel product ..................... 10

Table 3: Global trend of scrap exports (Mt) .......................................................................................... 13

Table 4: Worldwide blast furnace iron production, ............................................................................. 16

Table 5: Direct reduced iron production ................................................................................................. 16

Table 6: Production of steel in electric furnace .................................................................................... 17

Table 7: Top 10 steel producing countries ............................................................................................. 20

Table 8: Top 10 steel producing companies (2014) ............................................................................ 21

Table 9: Global trends of true steel use 2009-2013 (Mt) ................................................................... 23

Table 10: iron ore export ............................................................................................................................. 26

Table 11: iron ore import ............................................................................................................................ 26

Table12: Africa‟s scrap import .................................................................................................................. 27

Table13: Iron production from blast furnace ......................................................................................... 28

Table14: Iron production from direct reduction ................................................................................... 29

Table15: Africa‟s steel production using electric furnace ................................................................. 29

Table16: Africa‟s crude steel production trends................................................................................... 30

Table 17: True steel use per capita ........................................................................................................... 33

Table 18: Export of semi-finished and finished steel products ........................................................ 34

Table 19: Distribution of major industrial by regional states (2007 E.C) ..................................... 49

Table 20: Human resource in metal and engineering subsector ...................................................... 51

Table 21: Comparison of local and expatriate employees (2003-2006 EC) ................................ 53

Table 22 Coal and limestone distribution ............................................................................................... 56

Table 23 Comparison of local and imported raw materials (ton) .................................................... 57

Table 24: Imported spare parts (ton) from 2002-2006 ....................................................................... 58

Table 25: Local construction sub-sector products ............................................................................... 64

Table 26: Design production capacity and actual production of major rebar producers .......... 65

Table 27: design capacity and capacity utilization of rebar producing industries ...................... 65

Table 28: Major local engineering and machinery products (2003-2007) .................................... 67

Table 29: Comparison of local and imported products of engineering machinery .................... 68

Table 30Vehicle and agricultural products ............................................................................................ 69

Table 31: Steel industry products of motor vehicle and agricultural equipment sector ............ 70

XII

Table 32 Comparison of local &imported products of motor vehicle &agricultural equipment70

Table 33 Aggregate expenditure on imported raw materials and steel products ........................ 71

Table 34 gross value of products of iron and steel industries (public and private) .................... 74

Table 35: Value added to national income ............................................................................................. 75

Table 36: Domestic market share of local industries by product type ........................................... 76

Table 37: Indirect imports and exports of steel (2004-2013) ........................................................... 77

Table 38: Growth of steel per capita consumption during GTP I ................................................... 77

Table 39: Apparent steel use ..................................................................................................................... 78

Table 40: True steel use (2004−2013) ..................................................................................................... 78

Table 41: Investment in the subsector ..................................................................................................... 79

Table 42: List of licensed metal/steel investment ................................................................................ 79

Table 43: Steel demand projection by 2025 .......................................................................................... 81

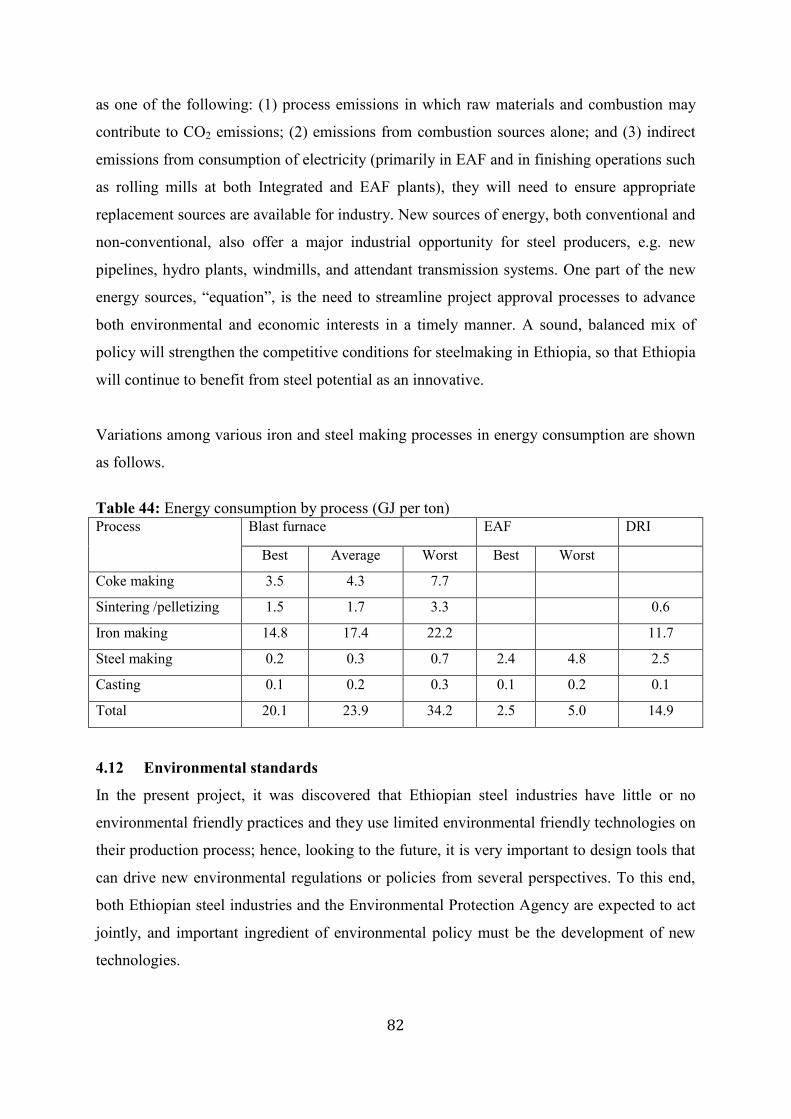

Table 44: Energy consumption by process (GJ per ton) .................................................................... 82

Table 45: Emission of iron and steel making technologies ............................................................... 83

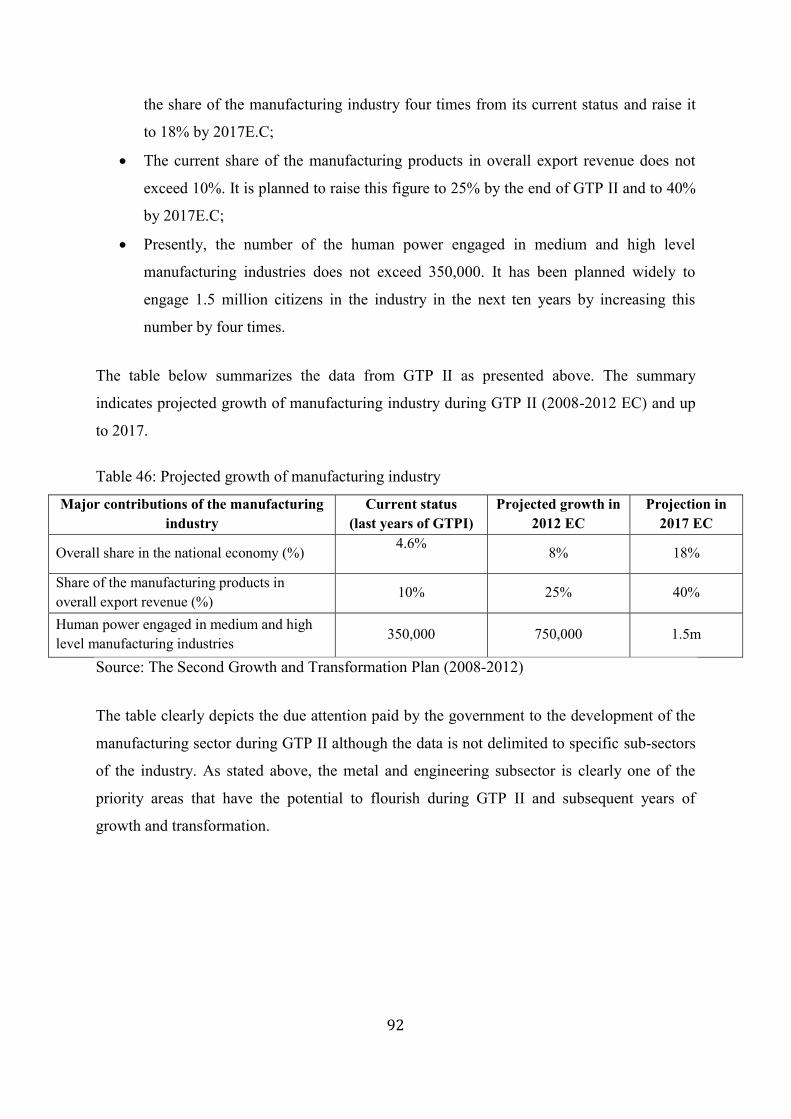

Table 46: Projected growth of manufacturing industry ...................................................................... 92

Table 47: List of strengths (S) and limitations (L) .............................................................................. 97

Table 48: List of opportunities (O) and challenges (C) ...................................................................... 98

Table 49: SLOC analysis matrix ............................................................................................................... 99

Table 50: Automobile emission standards .......................................................................................... 113

Table 51: Raw materials ........................................................................................................................... 122

Table 52: Human resource related information ................................................................................. 128

Table 53: Steel production ....................................................................................................................... 131

Table 54: Technology................................................................................................................................ 132

Table 55: Support institutions ................................................................................................................. 135

Table 56: Major lessons from comparative analysis ........................................................................ 149

Table 57: Analysis of strategic interventions and policy issues ................................................... 164

Table 58: Evolving of techno-economic indexes of China steel industry ................................. 184

XIII

List of Figures

Figure 1: Production, consumption, import and export of iron ore ................................................ 11

Figure 2: Regional base production, consumption, import and export of iron ore ..................... 11

Figure 3: Region base import, export and net import of scrap in 2014 ......................................... 13

Figure 4: Value chain of steel making ..................................................................................................... 15

Figure 5: Crude steel production trend from 2007-2014 ................................................................... 19

Figure 6: Steel production by geographical distribution 2004 and 2014 ...................................... 20

Figure 7: World steel consumption .......................................................................................................... 22

Figure 8: World steel demand by end products .................................................................................... 24

Figure 9: Share of Africa‟s crude steel production in 2013 & 2014............................................... 31

Figure 10: Share of crude steel consumption 2013 & 2014 ............................................................. 32

Figure 11: Share of crude steel consumption 2013 & 2014 .............................................................. 32

Figure 12: Indirect net export of steel ..................................................................................................... 35

Figure 13: Indirect import of steel (by commodity groups) .............................................................. 35

Figure 14: Steel use by sector .................................................................................................................... 37

Figure 15: 2006 E.C industrial distributions of steel industries ....................................................... 50

Figure 16: Comparison of local and imported products of construction sector in Mt ............... 66

Figure 17: Steel industry products of engineering and machinery sector ..................................... 68

Figure 18:local and imported products of motor vehicle and agricultural equipment .............. 70

Figure 19: Challenges of steel industries of Ethiopia ......................................................................... 72

Figure 20: Challenges of Ethiopian steel industries in 2007E.C ..................................................... 73

XIV

Acronym

BF Blast Furnace

BOF Basic Oxygen Furnace

BRICS Brazil, Russia, India, Chinaand South Africa

CSA Central Statistical Agency

CIS Belarus, Kazakhstan, Russia, Ukraine

DRI Direct Reduced Iron

EAF Electric Arc Furnace

ECA Ethiopian Customs Authority

GDP Gross Domestic Product

IF Induction Furnace

IoTs Institute of Technologies

MIDI Metal Industry Development Institute

Mt Million ton

NAFTA Canada, Mexico, USA

SSPI Sustainable Steel Policy and Indicators

SSY Steel Statistical Yearbook

STU Science and Technology Universities

WSF World Steel Figure

1

1. Background of the Study The Ethiopian government has been designing and implementing strategies and plans to

manage the overall development endeavors of the country and to achieve the key objective of

eradicating poverty and ensuring broad-based, accelerated, and sustained economic growth.

Among such plans, GTP I (2010-2015) and GTP II (2015-2020) are the most significant

development and transformation plans the country has ever seen. GTP I is unique as

compared to the past development plans of the country due to its high economic growth and

comprehensive development targets (11.2-14.9%). It was a plan that has cleared the ground

and paved the way for the desired transformation of Ethiopia into the status of a middle-

income country within 15 years, that is, by 2025.

Likewise, the ongoing GTP II is believed to move the nation into a historically new direction.

During the GTP II, the country strives to tune its growth direction from agricultural-led to

industry-led economy. In this development direction, the role of industries is, thus, extremely

desirable. This entails the need for industrial transformation, and our industries are expected

to align themselves towards the attainment of this vision demanded by the economy. When it

comes to the specific component of industry, the role of manufacturing comes to the fore

front of the development and transformation agenda.

Steel industry is one of the manufacturing industries that have been given due attention by the

government with the target of increasing the per capita of steel products and gradually

substituting imported products of this industry. In addition, steel industries are planned to

support other industries such as Leather, Textile, Cement, Agro-industries, Construction,

Vehicle and other industries by supplying them with spare parts and necessary products.The

implication of all of these is that steel industries will have many- fold impacts on the national

economy and that overhauling these industries requires the design of better polices and

strategies.

The purpose of this study was, therefore, to conduct national level in-depth investigation on

the development of Ethiopian steel industries with special emphasis on their challengesand

prospects in terms of their economic viabilities, human and material resources, technology,

environmental effects and the like. In the light of this, the study has drawn on primary data

2

generated through both quantitative and qualitative methods. The study has also utilized

secondary data by reviewing the existing national strategy documents on steel industries and

the experiences of the nations with success stories (South Korea, China, India, Brazil and

South Africa) as best practices, and eventually has come up with a policy option that will be

used as frame of reference for the next medium-term development plan of the country.

1.1 Objectives of the study

1.1.1 General Objective

The main objective of the study is to examine economic viability, technology transfer,

human and material resources, and financial sources of steel industries in Ethiopia with a

view to enriching and expanding steel industries to the desired level of development and

proposing ideas for policy decision and the way forward.

1.1.2 Specific Objectives

Based on the main objective, the specific objectives of the study are to:

identify problems, gaps, and stumbling blocks of steel industries and forward

policy recommendations;

pinpoint the economic viability of steel industries in the Ethiopian context and

examine the support system needed for their expansion and reinforcement;

based on local and international experiences, investigate into the kind of

technology transfer, human and material resources, and financial sources that

would enable the Ethiopian steel industries to expand and flourish to the required

level of development.

1.2 Study Framework and Methodology

1.2.1 Data Collection Methods

Primary Data

Primary data that are needed for the purpose of this study have been obtained through on-site

observations of production system/processes and products of the existing steel

industries/factories, survey questionnaire, and in-depth interviews with selected ministries,

Metal Industry Development Institute (MIDI), steel industry executives, steel experts,

Ethiopian Mechanical Engineering Association and others.

3

Secondary Data

Secondary data were obtained from both international and national documents. The national

documents consulted for the purpose of this study include the Growth and Transformation

Plans (GTP I & GTP II) and GTP I evaluations, Ethiopian Industrial Roadmap, Ethiopian

Industry and City/Urban Development Policy and Strategy Document, different steel-

related studies (KOICA, JICA, MIDI) and other documents from the Ministry of Mining,

Ethiopia Power Authority, Ministry of City and Urban Development, Ministry of Industry,

Metal Industry Development Institute, Environmental Protection Authority, Geological

Survey, Planning Commission, Ethiopian Customs Authority, Ethiopian Railway

Corporation, Banks and other pertinent sources.

Benchmarking

The main objective of benchmarking is to draw lessons on the track and past trends of best

performing countries in the development of the steel industries in order to formulate better

policy options. In this regard, the focus of the benchmarking is exploring how backward

and forward linkages (inputs and output markets analysis) are identified. Further,

production process efficiency and technologies, application areas, environmental issues,

supply, distribution, downstream value chain and other factors will be considered. In

addition, the overall development and current situation of the steel industry in terms of

consolidation, production, capacity, consumption, employment and major macro-level

overhauls such as vertical integration, management and organization will be explored. For

this purpose, a visit was be made to China to benchmark the best practices in the steel

industry.

4

1.2.2 Approach and Methodology

Team Formation & Detail Design Contract and Kickoff

Instrument Development Prel

imin

ary

Act

iviti

es

Mile

ston

e -1

: Situ

atio

nal

Ana

lysis

Data Collection

Primary Data On-site visit Questionnaires In-depth Interview FGD

Secondary Data Document

Analysis

Benchmarking China

SLOC & PESTL Analysis

Vision & Policy Option Objectives

Selection of Policy Options Mile

ston

e -2

: Fo

rmul

atio

n of

Pol

icy

Opt

ions

Drafts, Validation & Submission

Mile

ston

e -3

: V

alid

atio

n &

Su

bmis

sion

5

1.2.3 Project Activities

The following tasks are the constituents of the key activities of this project.

I. Preliminary Activities

Contract and Kickoff:

Contractual agreement for the project was prepared and signed by official representatives of

FDRE-Policy Study and Research Center and ASTU. A kickoff workshop had been

conducted before the actual project commenced. In the workshop, the core project team

members presented their understanding of the assignment and how they intended to

undertake the project. The inception workshop was meant to provide opportunity for all

stakeholders to know the general objectives and methodology of the project. The timetable

for the project and the different milestones in the different phases of the project were

presented. On the workshop, concerned stakeholders actively participated and provided the

necessary feedback and guidance and announced their acceptance on the plan.

Instrument Development

Questionnaires, interview questions, focus group discussion guides, and observation

checklists were developed from both primary and secondary sources.

Detailed Design and Team Formation

After the kickoff workshop, the core team prepared a detailed design of the project and

formed working teams based on division of assignments.

II. Milestone -1: Situation Analysis

On-site visits of production system/processes and products, observation of the

existing steel industries, and in-depth interviews with experts and sector

representatives.

Root cause analysis and assessment of the competitive position of the Ethiopian

steel industries. This was done by considering several indicators and through 5

“W” and 1 “H” approach to know the level of their competitiveness such as

business conditions, various input indicators (e.g. raw materials, energy

efficiency), which can be assumed to affect the competitive performance of the

6

steel industries, as well as process, output and performance indicators (i.e.,

quantity, quality, etc.). Moreover, focus was made on the trend of demand for

steel products and market prospects.

Analysis and assessment of relevant framework conditions for the

competitiveness of the Ethiopian steel industries, focusing primarily on the

regulatory conditions affecting the industries, that is, environmental regulations,

industry specific standards, competition policy, labor market, health and safety

regulations, and so on.

Data Collection: Using the instruments developed, data were collected from

groups identified as respondents for the purpose of developing this steel industry

policy options and strategies and by benchmarking steel industries of one

country.

Assessment on an extensive literature review and available statistical data to

explore strategic and policy options outlook for the Ethiopian steel industry,

focusing on likely developments, strengths, weaknesses and opportunities, threats

of the sector, and possible policy options.

II. SLOC & PESTL Analysis: Based on data obtained from identified respondents,

strengths, limitations, opportunities, and challenges of Ethiopian steel industry have

been identified. In addition, the political, economic, social and technological

environments of Ethiopian steel industry have been assessed. Therefore, both the

SLOC and PEST analyses have been done to identify key issues in strategic and

policy options of Ethiopian steel industry.

III. Milestone -2: Formulation of Policy Option

Based on the findings of the study,policy vision, goal, strategic objectives and

interventions have been formulated for the Ethiopian Steel Industry.

IV. Milestone -3: Validation & Submission

The first draft of the policy options document was prepared and presented on a

workshop that was organized for validation.

The final draft of policy option document was prepared based on the feedback

from the validation workshop and benchmark and submitted to FDRE-Policy

Study and Research Center.

7

2. Global Analysis of Steel Industry

Introduction

Steel is and will remain the most important engineering and construction material in the

modern world and it is at the core of a green economy in which economic growth and

environmental responsibility exist as a mutually beneficial partnership that serves the entire

globe.

Steel is vital to a sustainable development of economic growth and innovation. In 2014,

according to World Steel Reports, the annual revenue of the steel industry was 980 billion

USD. The industry invested 7.5% of revenue in new processes and products, and it

distributed 954 billion USD to society directly and indirectly, including 120 billion USD in

tax contributions and 8 million people worked for the steel industry (SSPI 2015).

Globally, steel is the backbone of manufacturing and is a strategic industry essential for

socioeconomic growth and stability. One of the specialties of steel industry is its global

leader in job creation; for example, in 2013 the steel industry directly employed more than

two million people worldwide, plus two million contractors and four million people in

supporting industries such as construction, transport, and energy. In short, the steel industry is

a source of employment for more than 50 million people (WSF, 2014).

Moreover, the global steel production and consumption have continued to grow at a rapid

pace, with emerging economies coming to the fore, in recent years. According to World Steel

Association (2015), in 1970 and 2014, steel production was 595 Mt and 1,665 Mt

respectively. The average growth of the steel production was 1.6% from 1970-1975 and 6.2%

from 2000-2005 but it dropped to 3.8% from 2010-2014 (WSF, 2015).

Global apparent steel consumption on the previous six years increased by 386.6 Mt (in 2009

it was 1,150.7 Mt but in 2014 it reached 1537.3Mt). On top of that, according to Global Steel

Market Outlook 2015, global consumption was forecasted to be increased by 0.5% and it

would reach 1544 Mt in 2015. For instance, the global average apparent steel use per capita

was 185.24 Kg in 2008 and 216.6 Kg in 2014 respectively(WSA,2015).

8

The production process for manufacturing steel is energy-intensive and requires a large

amount of natural resources. Energy constitutes a significant portion of the cost of steel

production, up to 40% in some countries. Thus, increasing energy efficiency is the most cost-

effective way to improve the environmental performance of this industry. To address these

issues, there has been significant investment in new products, plants, technologies and

operating practices. The result has been a dramatic improvement in the performance of steel

products, and a related reduction in the consumption of energy and raw materials in their

manufacture (SOCAT, 2010).

With this brief background, this chapter focuses on some of the prominent global issues such

as steelmaking process and technology, production, consumption, import and export trends.

2.1. Steelmaking processes and technology

Steel is the most complex and widely used engineering material. It is the pillar of

manufacturing and strategic industry essential for socioeconomic growth and stability. Due

to its versatile properties, it is everywhere in our lives such as construction, automotive,

machinery and equipment, energy supply, transportation system, urban centers, clean water

and safe food supply, defense and home security, appliance and others.

Steel making is the process of removing impurities such as sulfur, phosphorus, and excess

carbon from iron and adding alloying elements such as manganese, nickel, chromium, and

vanadium to produce the exact steel required. Its technology continues to evolve, but the

changes are incremental rather than fundamental. The main processes of crude steel

production have narrowed over many years and now only electric steelmaking is used based

on scrap and molten pig iron as basic inputs (SOCAT, 2010; Danish Technological Institute,

2008).

2.1.1. Raw materials

Steel industry is reliant on a number of raw materials, particularly iron ore, coal (coke),

ferrous scrap and various alloying elements for the steelmaking process. Iron ore provides the

ferrous content for steel, and is used almost exclusively by the steel industry. Coking coal is

used to produce coke, which is an essential element that provides heat and the carbon

required to remove oxygen from the ore. Ferrous scrap is the key ingredient in the electric-arc

furnace (EAF) route, where recycled steel is melted and subsequently rolled into new steel

products. Scrap is also used along with iron in basic oxygen steel furnaces (BOF), to reduce

9

levels of heat in the furnace. The amount and quality of iron (Fe) influences the selection of

specific furnaces for production of steel in addition to energy sources.

The details of iron ore with its specific iron (Fe) are summarized in Table 1 below

Table 1: Quality of Fe raw materials

No Name of iron ore Formula %Fe

1. Hematite Fe2O3 69.9

2. Magnetite Fe3O4 74.2

3. Goethite/Limonite HFeO2 ~ 63

4. Siderite FeCO3 48.2

5. Chamosite (Mg,Fe,Al)6(Si,Al)4 (OH)8 29.61

6. Pyrite FeS 46.6

7. Ilmenite FeTiO3 36.81

Source: Geological Survey of Ethiopia, 2010

For example, if the iron content of iron ore is above 65%, it is advisable to use DRI steel

production process from productivity point of view in which case Hematite and Magnetite

iron ore types are typical examples.

On the other hand, technically it is possible to improve the quality of steel products by adding

other additives to the scrap or pig iron as per required standards. Some of these additives and

properties are summarized as follows:

10

Table 2: Steelmaking raw materials, properties and application for steel product

No Raw material Properties in steel Steel industries share of use

1. Iron ore Provides the ferrous content in the steel 98%

2. Coking coal Produce coke, heat source and reducing

agent in BF >80%

3. Ferrous scrap

Main elements for EAF-steel, combined

with iron in BOF to reduce levels of heat 100%

4. Manganese

Desulpherises and as alloying element for

strength 90%

5. Silicon Used to de-oxidize steel 60%

6. Nickel

Anti-corrosion (nickel content in stainless

steel 8-10%) 60%

7. Chromium

Anti-corrosion (in stainless steel, average

content 18%) 75%

8. Zinc

Used to galvanize steel (enhance corrosion

resistance) 60%

9. Tin Brings protective coating to steel 20%

10. Molybdenum Resistance to heat, corrosion 60%

11. Vanadium Brings extreme hardness to steel 85%

12. Tungsten Brings extreme hardness to steel 20%

Source: OECD (2014).

Steel is an alloy; as the result, as indicted in Table 2, additives are essential for producing

steel products to have different properties which can be applicable for multipurpose; for

instance, if we add Molybdenum, the product will have a capability to resist heat and

corrosion.

2.1.1.1. Iron ore

The demand and supply of iron ore has been fluctuating from time to time. For example

during the first half of 2014, Australia was the largest iron ore exporter in the world, with

outward shipments amounting to 353 Mt, followed by Brazil with 157 Mt, South Africa with

33 Mt, Canada with 19 Mt and India with 8 Mt of iron ore exports.

During the first six months of 2014, the major iron ore importers were China (457 Mt), the

EU (68 Mt), Japan (65 Mt) and Korea (37 Mt), according to OECD 2014.

11

Furthermore, the production, consumption, import and export of iron ore of some selected

countries in 2013 (Mt) is given in the figure below.

Figure 1: Production, consumption, import and export of iron ore

Source: World Steel Association 2014

When it comes to the regional pattern of iron ore production, consumption, import and

export, the Asian countries take the lion‟s share as depicted in the following figure.

Figure 2: Regional baseproduction, consumption, import and export of iron ore

Source: World steel Association, 2014

12

2.1.1.2. Scrap

Scrap consists of recyclable materials left over from product manufacturing and

consumption, such as parts of vehicles, building supplies, and surplus materials.

Unlike waste, scrap has monetary value; especially, recovered metals, and non-metallic

materials are also recovered for recycling.

Recycling involves processing used materials into new products in order to prevent wastage

of potentially useful materials by reducing consumption of raw materials and energy usage,

by lowering air pollution, water pollution and greenhouse gas emissions as compared to

virgin production. Steel is the world‟s most recycled material; for example, according to

WSA (2015),650 Mt of steel are recycled every year, avoiding over 900 Mt of CO2

emissions.

According to a study by US Environmental Protection Agency, inrecycling scrap metals in

place of virgin iron ore, every ton of new steel made from scrap steel saves 1,115 kg of iron

ore, 625 kg of coal and 53 kg of limestone.Furthermore, recycling scrap metals in place of

virgin iron ore can yield 75% savings in energy, 90% savings in raw materials used, 86%

reduction in air pollution, 40% reduction in water use, 76% reduction in water pollution and

97% reduction in mining wastes. (http://www.norstar.com.au/, UnitedStates Environmental

Protection Agency)

2.1.1.3. Trade in ferrous scrap

In 2012, China and the European Union were the largest scrap generators, generating

approximately 125 Mt and 107 Mt of ferrous scrap respectively. In 2013, China‟s scrap

generation grew to 143 Mt, according to data from the Japanese Ferrous Raw Materials

Association (2014).

The figure below summarizes the regional import, export and net imports of scrap in 2014.

13

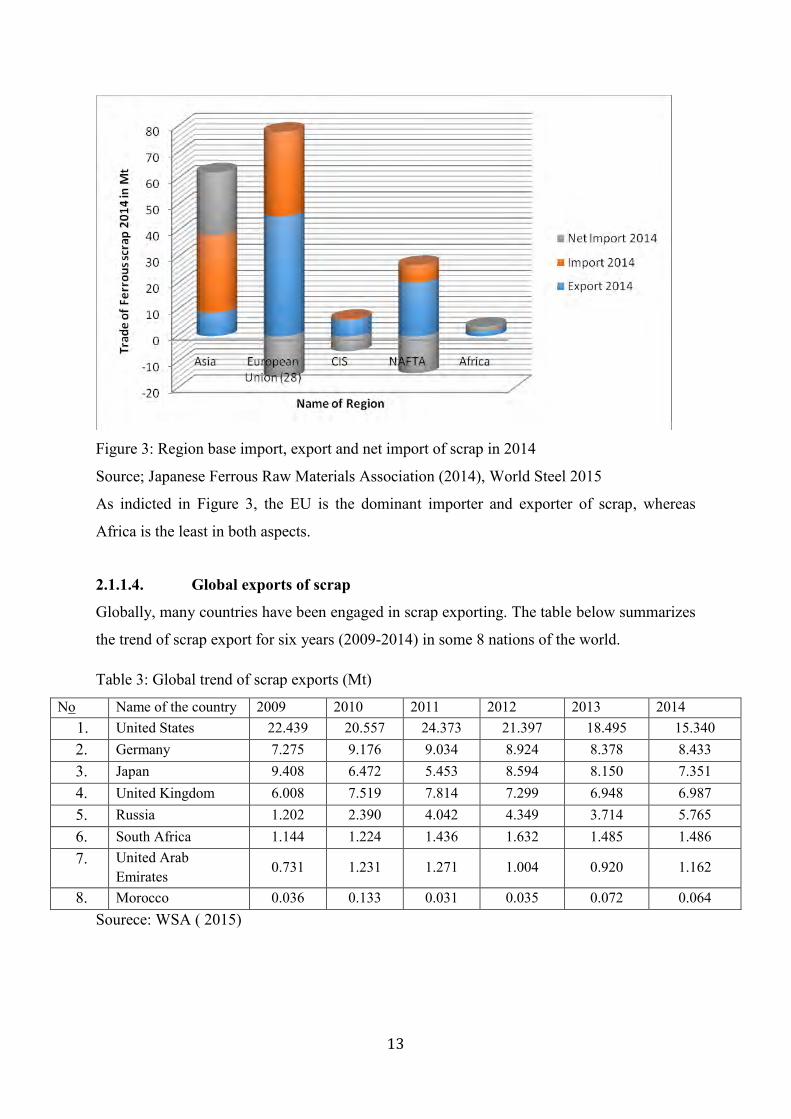

Figure 3: Region base import, export and net import of scrap in 2014

Source; Japanese Ferrous Raw Materials Association (2014), World Steel 2015

As indicted in Figure 3, the EU is the dominant importer and exporter of scrap, whereas

Africa is the least in both aspects.

2.1.1.4. Global exports of scrap

Globally, many countries have been engaged in scrap exporting. The table below summarizes

the trend of scrap export for six years (2009-2014) in some 8 nations of the world.

Table 3: Global trend of scrap exports (Mt)

No Name of the country 2009 2010 2011 2012 2013 2014 1. United States 22.439 20.557 24.373 21.397 18.495 15.340 2. Germany 7.275 9.176 9.034 8.924 8.378 8.433 3. Japan 9.408 6.472 5.453 8.594 8.150 7.351 4. United Kingdom 6.008 7.519 7.814 7.299 6.948 6.987 5. Russia 1.202 2.390 4.042 4.349 3.714 5.765 6. South Africa 1.144 1.224 1.436 1.632 1.485 1.486 7. United Arab

Emirates 0.731 1.231 1.271 1.004 0.920 1.162

8. Morocco 0.036 0.133 0.031 0.035 0.072 0.064 Sourece: WSA ( 2015)

14

2.1.2. Steel industry value chain

The steel industry value chain includes all the processes required to transform raw materials

(mainly coal, iron ore, and scrap) into finished steel products. Steel industry value chain

would include upstream stockholders (the suppliers of raw materials), downstream,

intermediaries (service centers, stockholding companies, and so on) and final customers

(producers of steel end products).

Based on the degree of vertical integration, steel making plants can be broadly classified in

two different groups, i.e. integrated plants and mini-mills.

I. Integrated steelmaking

The two most common routes are a blast furnace in combination with a Basic Oxygen

Furnace (BOF), commonly referred to as “integrated” steelmaking, and a principally scrap

based Electric Arc Furnace (EAF), commonly referred to as the “mini-mill” (SOACT,2010).

II. Mini-mill steelmaking

The direct smelting of iron-containing materials such as scrap is usually performed in electric

furnaces, known as mini-mills, which play an important and increasing role in modern

steelworks concepts. The major feedstock for the EF is ferrous scrap, which may comprise of

scrap from inside the steelworks, from steel product manufacturers (e.g. vehicle builders) and

capital or post-consumer scrap (e.g. end of life products).

Mini-mills utilize electric furnaces and mainly rely on scrap, and only partially on raw iron,

which is usually purchased as processed input. Nonetheless, some mini-mills are moving

toward upstream vertical integration, by adopting new iron-making technologies (e.g. direct

reduction iron making, smelting reduction) requiring relatively limited capital investment and

characterized by a minimum efficient scale lower than traditional blast furnaces. For

developing countries which are rich in scraps, it is recommendable to use electric furnace and

direct reduced iron instead of blast furnace.

15

Globally, the value chain of steel making process can be represented pictorially as shown in

figure 5.

Figure 4: Value chain of steel making

2.1.3. Steel production technologies

Selecting state of the art technology is crucial for producing high quality and diversified

products, taking into consideration the environment and energy. Among those technologies,

the types and capacity of furnaces used in steel production are decisive. The most common

furnace types are:

2.1.3.1. Blast furnace iron (BFI) production

A blast furnace is a shaft-like unitthat operates according to thecountercurrent principle. Iron

ore, coke,heated air and limestone or other fluxesare fed into the blast furnace. All iron

orecarriers contain oxygen, which has to beremoved through reduction in the blastfurnace by

using carbon as a reducing agent.

16

Table 4: Worldwide blast furnace iron production,

N0 Country Blast furnace iron production, 2009-2013 (In Mt) 2009 2010 2011 2012 2013

1. China 568.634 595.601 645.429 670.102 708.970 2. Japan 66.943 82.283 81.028 81.405 83.849 3. India 38.233 39.560 43.624 47.987 51.359 4. Russia 43945 47934 48.117 50.529 50.111 5. South Africa 4.444 5.429 4.604 4.599 4.960 6. Egypt 0.800 0.600 0.600 0.550 0.550

Source: WSF (2015)

2.1.3.2. Direct reduced iron (DRI) production

Direct reduction processes require a reducing gas to remove the oxygen from the iron

containing material in a solid state. The reducing gas is in the form of CO and/or H2. It

involves the reduction of iron ore to metallic iron in the solid state at process temperatures

less than 1000°C. DRI is a new process which uses gas rather than coke as a fuel, and it is

particularly cheap in countries with access to low-cost natural gas. DRI facilities are less

capital-intensive than traditional integrated plants and are efficient at smaller production

volumes.

Table 5: Direct reduced iron production

Source: Steel Statistics Year Book, 2015

As indicated in Table 6, India was by far the leading producer of steel using DRI from 2009

to 2014. From Africa, Egypt is a country with better experience in producing steel by using

this technology.

No Country Direct reduced iron production, 2009-2014 In Mt

2009 2010 2011 2012 2013 2014

1. India 22.030 23.420 21.970 20.050 16.893 20.366

2. Iran 8.099 9.350 10.368 11.582 14.458 14.551

3. Mexico 4.147 5.368 5.854 5.586 6.100 5.976

4. Russia 4.600 4.700 5.200 5.125 5.329 5.350

5. Egypt 3.051 2.965 2.932 3.068 3.432 2.882

6. South Africa 1.340 1.120 1.414 1.493 1.295 1.560

7. Libya 1.077 1.270 0.165 0.508 0.956 0.998

17

Additionally, crude steel can also be produced by using Open Hearth Furnace, but this

technology is not popular like the other technologies.

2.1.3.3. Electric furnaces

Steel production in an EAF typically occurs by charging 100 percent recycled steel scrap,

which is melted using electrical energy imparted to the charge through carbon electrodes and

then refined and alloyed to produce the desired grade of steel.

The Electric Arc Furnace (EAF) is a completely different technology for steel-making; it is

usually adopted in mini-mills. The main inputs for the EAF are scrap and electricity.

Electrodes installed within the furnace melt scrap through the heat created by an electric arc.

Limestone and other flux are added in the EAF to remove impurities from molten steel.

The size of EAFs ranges from very small units of 50 ton of capacity per cycle, to large

facilities that can charge up to 200 ton. An EAF processing only scrap uses 10% of the

energy needed by blast furnaces and BOFs, not accounting for the different inputs used in the

two routes. New technologies are enabling further reduction in energy consumption by pre-

heating scrap with recovered hot gases.

EAFs are economic and efficient at relatively small volumes of production compared to

BOFs, in particular because they can be easily shut down and restarted.

The summary of selected countries using Electric Furnaces is given in the following table.

Table 6: Production of steel in electric furnace

No Country Production of steel in electric furnace in Mt

2009 2010 2011 2012 2013 2014

1 Italy 14.036 17.163 18.843 17.939 17.295 17.200

2 Germany 11336 13.215 14.204 13.789 13.459 13.062

3 Spain 11.270 12.503 11.660 10.216 10.042 10.042

4 France 5.164 5.601 6.128 6.102 5.491 5.498

5 Egypt 4.700 6.075 5.940 6.100 6.215 5.970

6 South Africa 3.530 3.250 3.555 3.034 2.947 2.819

Source: SSY (2015)

18

2.2. Global production trend of steel

The global steel production and consumption have continued to grow at a rapid pace, with

emerging economies coming to the fore, in recent years. For instance, steel production in

1970, 2000, 2013 and 2014 was 595 Mt, 850 Mt, 1649 Mt and 1665 Mtrespectively.

Similarly, the average growth of the steel production was 1.6%, from 1970-1975 and 6.2%

from 2000-2005 although it dropped to 3.8% from 2010-2014. With regard to geographical

distribution, in 2014, 49.4% of the world‟s crude steel production was covered by China,

whereas the share of Africa was only 0.9%.

In 2014, the Middle East, the smallest region for crude steel production, had the most robust

growth. Crude steel production in the EU (28), North America and Asia grew modestly in

2014 compared to 2013, while in the C.I.S. and South America it decreased.

According to geographical distribution, in 2013and 2014, the crude steel production of China

was 48.5% and 49.4% respectively, but the ratio of Africa in 2013 and 2014 was only 1% and

0.9% respectively.

Thus, over the last couple of decades, increased demands are observed from emerging

economies, with Asia (mainly China and India) and United States accounting for more than

half of the world‟s consumption. Population and GDP growth continue to be the drivers for

consumption in these regions with steel demand directly linked to population growth as it

spurs demand for urbanization and infrastructure.

2.2.1. Worldwide crude steel production

Crude steel is defined as steel in its first solid (or usable) form: ingots, semi-finished products

(billets, blooms, slabs sheet metals, rolled coil…), and liquid steel for castings. The following

graph shows the global trend of crude steel production and growth rate from 2007 to 2014.

19

Figure 5: Crude steel production trend from 2007-2014

Source: World Steel Association 2015, Global Iron and Steel Market (Deloitte, September

2015)

The average growth rate of crude steel production has been fluctuating over the last more

than 40 years. For example, there had been steady decline in the growth of crude steel

production from 1970-1990, while it showed dramatic increase from 1995-2005. However,

this growth has begun to fall sharply since 2005.

2.2.2. Regional analysis of steel production

When we compare the crude steel production across regions, we can clearly observe the

dramatic shift of production capacity from EU to China between 2004 and 2014 as shown in

Figure 9.

20

Figure 6: Steel production by geographical distribution 2004 and 2014

Source: WSA, 2015

2.2.3. Major steel-producing countries

As can be observed from Table 7, China, Japan, United States and India were the leading

steel producing countries in 2013 and 2014.

Table 7: Top 10 steel producing countries

No Country 2013 2014 Rank 1. China 822 822.7 1 2. Japan 110.6 110.7 2 3. United States 86.9 88.3 3 4. India 81.3 83.2 4 5. South Korea 66.1 71 5 6. Russia 69.0 70.7 6 7. Germany 42.6 42.9 7 8. Turkey 34.7 34 8 9. Brazil 34.2 33.9 9 10. Ukraine 32.8 27.2 10

11. South Africa 7.2 6.5 23 12. Egypt 6.8 6.5 24

Source:World Steel Figure, 2015

21

2.2.4. TOP 10 steel producing companies 2014

International companies which have production capacity of more than 3 Mt are outlined

below.

Table 8: Top 10 steel producing companies (2014)

Rank Name of the company Name of own country

2010(Mt) 2011(Mt) 2012(Mt) 2013(Mt) 2014(Mt)

1. ArcelorMittal Luxembourg 98.2 97.248 93.575 96.096 98.088

2. Nippon Steel and Sumitomo Metal Corporation

Japan 35.0 33.388 47.858 50.128 49.3

3. Hebei Steel Group China 44.36 42.84 45.786 47.094

4. Baosteel Group China 37.0 43.34 42.7 43.908 43.347

5. POSCO South Korea 35.4 39.118 39.875 38.261 41.428

6. Shagang Group China 23.2 31.92 32.31 35.081 35.332

7. Ansteel Group China 22.1 29.75 30.23 33.687 34.348

8. Wuhan Steel Group China 16.6 37.68 36.42 39.311 33.051

9. JFE Steel Corporation Japan 31.1 29.902 30.409 31.161 31.406

10. Shougang Group China 14.9 30.04 31.42 31.523 30.777

Source: WSF (2014, 2015)

2.3. Global consumption trends of steel Global apparent steel consumption increased by 386.6 Mt over the last six years (from 2009-

2014). Particularly, it was 1,150.7Mt in 2009 and 1537.3 Mt in 2014. Out of the global

consumption, China accounted for 46.2% of world steel consumption with 710.8 Mt (Mt) in

2014, while the United States of America took the second rank by consuming 106.9 Mt (Mt)

in the same year.

From regional perspective, Asian countries were the leading consumers of steel by

consuming 1008.2 Mt, followed by EU, which accounts for 146.8 Mt. When it comes to

22

Africa, the annual consumption of steel was only 36.9 Mt (Mt), which accounts only for 2.4%

in 2014.

On the other hand, the world average steel use per capita was 185.24 Kg, 193 Kg, 217.8 Kg

and 216.6 Kg in 2008, 2010, 2013 and 2014 respectively (WSA,2015).From 2009-2014,

apparent steel use of countries was different from year to year, sometimes increasing and

other times decreasing.

Globally, the consumption trendsof steel and its growth ratecan be observedfrom the

following figure.

‟

Figure 7: World steel consumption

Source: WSA (2015), Global Iron and Steel Market (Deloitte, September 2015)

The forecast for steel consumption over the next two years will be expected to increase with

1.02 and 1.03 percent.

2.3.1. True steel use (finished steel equivalent)

True steel use (TSU) is obtained by subtracting net indirect exports of steel from apparent

steel use (ASU). The following table illustrates the trends of true steel use of some selected

countries of the world.

23

Table 9: Global trends of true steel use 2009-2013 (Mt)

No Name of the country 2009 2010 2011 2012 2013

1. Czech Republic 2.576 3.330 3.590 3.167 3.028

2. Germany 22.242 29.876 32.760 28.618 28.286

3. Italy 14.727 17.342 19.103 16.404 17.052

4. Russia 28.110 42.777 50.540 52.382 52.254

5. Turkey 16.182 22.320 25.908 27.115 29.80

6. Brazil 19.113 28.076 28 128 28 513 30 378

7. China 515.746 537.434 583.375 603.471 680.438

8. Japan 36.729 42.971 43.767 44.022 48.113

9. South Korea 29.085 33.768 35.555 35.133 35.587

10. Ethiopia 29.085 33.768 35.555 35.133 35.587

Source: SSY (2015)

2.3.2. Global steel use per capita

Growth in Gross Domestic Product (GDP) per capita, a measurement of the average national

standard of living, can be a contributing factor to steel demand. According to Global Steel

and world steel issue, increased industrialization caused by economic expansion has a

tendency to drive corresponding increases in steel consumption.

According to World Steel Association (2015), South Korea was the leading country by using

1118.8 Kg of finished steel per capita worldwide and Egypt was the leading in Africa by

using 113.7 Kg of finished steel per capita in 2014. Worldwide finished steel consumption

per capita was 217.8 and 216.9 in 2013 and 2014 respectively, but Africa was using only 31.6

and 31.9 Kg of finished steel per capita in the same year. Furthermore, according to WSA

(2015), globally, United Arab Emirates was the leading country in 2014 by using 1052.0 Kg

of true steel per capita and Algeria was the first from Africa with 198.0 Kg in the same year.

2.3.3. Steel demand by end-use industry

The majority of steel products are used by construction sub-sector followed by mechanical

engineering.

24

Figure 8: World steel demand by end products

Source: WSA (2014)

25

3. Regional Production and Consumption Analysis of Steel

Introduction

With the exception of South Africa and some countries in North Africa like Egypt, the steel

industry in the other African countries is still in a state of slumber. South Africa has a fully

developed steel industry and most of the generalisations that apply to most other African

countries would be out of place when one is referring to South Africa. At best, the industry

can be described as being in its infancy.

According to African Iron and Steel Association (2002), Africa‟s steel industry is scrap-based

steelmaking, which is dominated by very small steelmakers each with 0.040-0.050 Mt steel

capacity mainly producing small rebar, but no special steel are produced.

Moreover, African crude steel production has been increased from 13.827 Mt in the year

2000 to 15.022 Mt in the year 2014. Africa‟s share of crude steel production accounts only

for 0.89 % of the world in the same year (WSA, 2015).

Consumption of steel products follows the trend of economic activity in individual countries.

There is a clear trend for high levels of consumption of steel products at certain stages of

economic development, which are associated with rapid urbanization and construction,

combined with industrialization and the growth of manufacturing industry. Africa‟s share of

apparent finished steel use in the year 2004 was 1.6% of the world and it has increased to

1.8% in the year 2014, which accounts for 36.9 Mt (WSA, 2015).

26

3.1. Steel making process and technology

3.1.1. Raw materials

A healthy global steel industry needs widely available and freely traded raw materials,

because there is no self-sufficient country in producing all raw materials.

Table 10: iron ore export

No Country Export of iron ore in Mt

2009 2010 2011 2012 2013 2014

1 South Africa 44.559 47.971 53.343 54.002 62.763 64.799

2 Mauritania 10.296 11.109 11.484 12.255 13.076 14.599

3 Sierra Leone - - 0.051 3.961 11.996 19.190

4 Liberia - - 0.072 2.038 4.295 5.034

Africa 54.855 59.080 64.950 72.255 92.129 103.623

Source: SSY (2015)

African countries could play a key role in the coming years, because of their large mining

potential. South Africa takes the lion‟s share of producing and exporting raw materials for

steel making; the country accounted for 60.8% of Africa‟s total production of iron ore and

62.53% of its export of iron ore in 2013 (WSA, 2015).

Table 11: iron ore import

No Country Import of iron ore in Mt

2009 2010 2011 2012 2013 2014

1 Egypt 4.583 4.178 4.343 4.235 3.824 3.249

2 Libya 1.304 2.257 0.063 0.844 1.819 1.377

3 South Africa 0.352 0.401 0.417 0.558 0.476 0.479

4 Algeria 0 0.117 0.011 0.026 0 0

5 Other Africa 0 0.001 0.085 0.012 0.167 0.371

Africa 6.239 6.953 4.918 5.675 6.287 5.476

Source: SSY (2015)

In the year 2014, Egypt‟s import of iron ore covered 59.33% of Africa‟s import which ranked

the top from Africa followed by Libya and South Africa that accounted for 3.249 Mt, 1.377

27

Mt, and 0.479 Mt respectively. Both Egypt and Libya are net importers of iron ore, but the

continent is a net exporter.

3.1.1.1. Scrap

Ferrous scrap remains a dominant steel making raw material in many parts of Africa. The net

import of scrap in Africa was 1.2 Mt in 2014. In the same year, South Africa exported 1.486

Mt of scrap that makes it the leading exporter in the continent followed by Morocco,

Zimbabwe, Ghana, and Egypt which accounted for 0.064 Mt, 0.037 Mt, 0.032 Mt, and 0.023

Mt respectively (WSA, 2015).