developing insurance markets - world bank

TRANSCRIPT

Developing Insurance Markets

Use of Financial Health and Stability Indicators

in Insurance Supervision

March 2020

Michael Hafeman

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Insurance is an important part of the financial sector. It supports broader economic and general

well‐being in developed economies in a way that is so entrenched and accepted that it is not

widely recognized. In less developed markets, insurance can remain nascent for many years and

then pick up through a dynamic development phase and reach a more mature phase. As would

be expected, many actors contribute to this development. This report is part of a larger effort

to understand the key drivers of development in insurance sectors in a range of jurisdictions

especially including the role of policy and project interventions.

This report contributes to two of the identified imperatives for development in particular.

Development has been found to be supported by more effective policy leadership, which needs

adequate and effective metrics, and by a better implemented risk‐based rather than rules‐

based approach to supervision.

The report preparation was led by Michael Hafeman, a consultant working jointly with the

Finance, Competitiveness, and Innovation (FCI) Global Practice at the World Bank and the

Monetary and Capital Markets Department at the International Monetary Fund. The author is

grateful for the active engagement of all who were involved in the discussions and in support of

the work.

The author is grateful for guidance and comments throughout the process from Jennifer Elliott

and Peter Windsor of the IMF and Fiona Stewart, Craig Thorburn, and Tetsutaro Shindo of the

World Bank. Ultimately, of course, the resulting report remains the work of the author and

does not reflect all the views of reviewers.

This material has been funded in part by the UK aid from the UK government, however the

views expressed do not necessarily reflect the UK government’s official policies. The report has

been prepared as part of a broader program of the Centre for Global Disaster Protection. For

more information on the ongoing work that is part of this project, readers may contact Craig

Thorburn at [email protected] .

Table of Contents

A. BACKGROUND ........................................................................................................................................... 1

B. SUMMARY OF KEY FINDINGS ..................................................................................................................... 4

C. ANALYSIS OF SURVEY RESULTS ................................................................................................................... 7

INSTITUTIONAL INFORMATION .......................................................................................................................................... 7 USE AND COMMUNICATION OF FHSIS .............................................................................................................................. 11 LOOKING TO THE FUTURE ............................................................................................................................................... 19 INPUT ON SPECIFIC FHSIS BY TOPIC ................................................................................................................................. 22

ANNEX 1 RESPONDENTS BY JURISDICTION ................................................................................................... 33

ANNEX 2 DETAILED RESULTS BY QUESTION .................................................................................................. 34

1. CAPITAL ............................................................................................................................................................. 44 2. ASSETS .............................................................................................................................................................. 49 3. REINSURANCE ..................................................................................................................................................... 57 4. ACTUARIAL ......................................................................................................................................................... 61 5. MANAGEMENT ................................................................................................................................................... 66 6. EARNINGS .......................................................................................................................................................... 71 7. LIQUIDITY ........................................................................................................................................................... 78 8. SUBSIDIARIES ...................................................................................................................................................... 82 9. INDUSTRY‐WIDE .................................................................................................................................................. 86

ANNEX 3 DETAILED RESULTS BY TOPIC ......................................................................................................... 90

A. USE OF FHSIS ..................................................................................................................................................... 90 B. USEFULNESS OF FHSIS ......................................................................................................................................... 93 C. GUIDANCE ON FHSIS ........................................................................................................................................... 96 D. MAPPING OF FHSIS ............................................................................................................................................. 99 E. USE OF BENCHMARKS ........................................................................................................................................ 102 F. BENCHMARKS USED ........................................................................................................................................... 105

ANNEX 4 MAPPING OF FHSIS ..................................................................................................................... 113

ANNEX 5 GUIDANCE ON FHSIS ................................................................................................................... 118

DETAILED TABLE OF CONTENTS ..................................................................................................................................... 118 1. CAPITAL ........................................................................................................................................................... 121 2. ASSETS ............................................................................................................................................................ 128 3. REINSURANCE ................................................................................................................................................... 138 4. ACTUARIAL ....................................................................................................................................................... 141 5. MANAGEMENT ................................................................................................................................................. 149 6. EARNINGS ........................................................................................................................................................ 157 7. LIQUIDITY AND ALM .......................................................................................................................................... 169 8. SUBSIDIARIES AND RELATED PARTIES ..................................................................................................................... 175 9. INDUSTRY‐WIDE ................................................................................................................................................ 180

Glossary

CU Used to describe generic “Currency Units” FHSI Financial Health and Stability Indicator FSAP Financial Sector Assessment Program IAIS International Association of Insurance Supervisors ICPs Insurance Core Principles IFRS International Financial Reporting Standards IMF International Monetary Fund RBC Risk‐Based Capital TA Technical Assistance WBG World Bank Group

Page 1

A. Background

Off‐site monitoring is an essential tool of financial sector supervision. For example, as

highlighted by Standard 9.7 of the Insurance Core Principles (ICPs) of the International

Association of Insurance Supervisors (IAIS), “The supervisor monitors and supervises insurers on

an on‐going basis, based on regular communication with the insurer, information obtained

through supervisory reporting and analysis of market and other relevant information.”

Off‐site monitoring involves both qualitative and quantitative analyses, including the calculation

of ratios and other financial health and stability indicators (FHSIs)1. Analysis of quantitative

indicators can play an important role in many aspects of supervision, including:

Market analysis for policy development;

Macroprudential risk assessment;

Microprudential risk assessment; and

Market conduct supervision.

Unfortunately, not all supervisors are using such analyses as fully and effectively as they might.

The reasons for this vary among jurisdictions, but often include one or more of the following:

Use of a less‐than‐ideal set of indicators, for example, with gaps or multiple

indicators that give the same information;

Lack of guidance on the interpretation of the indicators, including the

development and application of benchmarks;

Infrequent and inconsistent calculation of the indicators;

Gaps in the data needed to calculate some indicators; and

Insufficient capabilities among supervisory staff.

The International Monetary Fund (IMF) and World Bank Group (WBG) have collaborated on a

project to help remedy this situation. Many of their technical assistance (TA) projects over the

years have provided training and other assistance to help supervisors deal with these problems.

In the course of this work, informal tools and resources related to FHSIs have been developed.

The current project has drawn on this work. It seeks to enhance the resources through wider

input, and to make them widely available to supervisors through this report and related

documents. The project was carried out by a consultant, Michael Hafeman, in collaboration

1 The FHSIs discussed in this report include the six insurance‐related Financial Soundness Indicators (FSIs) used by the IMF in its monitoring of the soundness of the system‐wide financial sector, from a macroprudential vantage point. See 2019 Financial Soundness Indicators Compilation Guide, IMF, 2019. https://www.imf.org/en/Data/Statistics/fsi‐guide

Page 2

with the IMF and WBG and the assistance of the IAIS. The main steps of the project are outlined

below.

Preparing to seek input. Draft guidance was prepared on the interpretation of many FHSIs used

by insurance supervisors2. The FHSIs have been organized by the CARAMELS3 categories to

which they are primarily related. A separate document was prepared that mapped the FHSIs to

other risk‐assessment categories where they can be useful in informing the assessment4. A

survey questionnaire was developed, to seek input on issues such as:

The purposes for which FHSIs are being used;

Which FHSIs are currently being used;

Whether any changes to the FHSIs are being contemplated, for example, in

response to the implementation of IFRS 9 and IFRS 17;

The mapping of FHSIs to risk‐assessment categories;

Supervisory benchmarks for the FHSIs and how they were established;

How some common data and methodology issues are being dealt with; and

Suggestions for improvements to the draft interpretation guidance.

Obtaining input from insurance supervisors and others. The IAIS graciously agreed to assist in

facilitating input from the supervisory community. It sent the survey questionnaire and the

draft interpretation guidance and mapping to its members, along with a request for input. The

IMF provided an overview of the project to the IAIS Implementation and Assessment

Committee and requested its members to provide input on behalf of their own authorities, via

both the survey and the Supervisory Forum, and to encourage others to do so. The IAIS

Secretariat set up the questionnaire on its survey platform and compiled the responses. The

IMF and WBG distributed the materials to staff and external technical assistance experts and

requested their input.

Analyzing the input and preparing a paper and updated resources. The consultant analyzed

the results of the survey and prepared this paper, which reports on the results of the survey

and briefly discusses the use of FHSIs. The paper also includes resource materials, which were

updated to reflect the input obtained. They include a mapping of the FHSIs to risk assessment

categories, supervisory benchmarks (ranges being used by supervisors, not prescriptions), and

interpretation guidance. IMF and WBG staff served as peer reviewers.

2 See Interpretation of FHSIs‐2019 02 26. Earlier versions of the draft benefitted from reviews by Michael Grist (WBG, retired) and supervisors in the Eastern Caribbean (in connection with a Caribbean Regional Technical Assistance Center (CARTAC) project). 3 CARAMELS is a risk‐assessment framework used by many insurance supervisors, with the following categories: Capital; Assets; Reinsurance; Actuarial Provisions; Management; Earnings; Liquidity; and Subsidiaries (including related parties and groups). 4 See Mapping of FHSIs‐2019 02 24.

Page 3

Publishing the paper and making the resources available. The paper is being published as a

working paper by both the IMF and WBG. The paper and related resources are accessible on

both organizations’ websites.

This paper has a few main sections and several detailed annexes. Section B presents a

summary of key findings, including recommendations. Section C provides an analysis of the

survey results. It begins with a breakdown of the institutional information on the survey

respondents. This is followed by analysis of how respondents are using FHSIs and how they are

communicating with various stakeholders regarding FHSIs. Then it looks to the future, including

the progress of respondents in adapting their use of FHSIs to new financial reporting standards

and their needs for additional guidance and other resources to facilitate the use of FHSIs.

Section C concludes with an analysis of the input of respondents regarding specific FHSIs, which

has been organized by topic (rather than by CARAMELS category).

Annex 1 lists the IAIS members who responded to the survey, including breakdowns by nature

of the jurisdiction (FSB members, other OECD jurisdictions, or other) and geographic region.

Annex 2 provides the detailed results of the survey, by question. Hence, it is organized by

CARAMELS category. Annex 3 provides the same detailed results but has been organized by

topic for ease of reference. It also includes rankings of some responses not only within

CARAMELS categories but also across all FHSIs.

Annex 4 is a mapping of the FHSIs to CARAMELS and other risk assessment categories. It is an

updated version of the draft mapping provided with the survey questionnaire, which takes

account of the input provided by respondents.

Annex 5 provides guidance on the calculation and interpretation of each of the FHSIs. It reflects

input provided by respondents and includes guidance on three additional FHSIs. The guidance is

organized by CARAMELS category and Annex 5 begins with a detailed table of contents.

Page 4

B. Summary of Key Findings

IAIS members from 33 jurisdictions responded to the survey. The respondents were well‐

distributed by nature of the jurisdiction and IAIS region, except that there were no responses

from the Middle East and North Africa region. More than 80 percent of the respondents were

from high or upper middle income countries.

Respondents use FHSIs most regularly and consistently in the supervision of conventional

insurance, particularly with respect to prudential supervision. There is scope for many

authorities to make more use of FHSIs across the full range of insurance activities they

supervise and in the various aspects of supervision for which they are responsible.

Respondents typically indicated that instructions for calculating FHSIs have been documented.

However, written guidance and training on the use and interpretation of FHSIs – both in general

and in relation to specific FHSIs – is lacking at many authorities.

Overall, the extent to which respondents communicate with insurers and the general public

regarding FHSIs is limited. This includes communication regarding how FHSIs are being used,

which FHSIs are being used, and the results of calculations – both for individual insurers and

industry aggregates.

Most respondents use between 25 and 74 FHSIs in total, although several use 100 or more.

Most respondents are still early in the process of revising the FHSIs to take account of

anticipated changes in financial reporting and regulatory requirements related to IFRS 9

Financial Instruments and IFRS 17 Insurance Contracts.

The survey asked several questions regarding each of nearly 100 FHSIs. Their responses indicate

that

Supervisors are using a wide variety of FHSIs, although some are used much more

frequently than others.

The FHSIs most used by supervisors, and those considered most useful, were identified.

Many respondents identified FHSIs that were surveyed that they thought would be

useful, but which they were not currently using.

The draft guidance seems largely to have achieved a good balance between being

concise but still sufficiently clear and detailed. The guidance was revised to reflect the

input provided.

Respondents were largely satisfied with the proposed mappings of the FHSIs to risk‐

assessment categories, but some additions were made in response to suggestions.

Page 5

Supervisors would be very interested in a database of benchmarks or more guidance on

the development of benchmarks. Unfortunately, very few authorities provided

quantitative responses regarding their current benchmarks for most of the FHSIs.

It is recommended that supervisors consider taking the following actions, if they are not already

doing so:

Use FHSIs to inform their analyses across the full range of insurance activities they

supervise and in the various aspects of supervision for which they are responsible.

Implement robust tools to facilitate the use of FHSIs, including databases, calculation

and reporting systems, and written guidance and training on the use and interpretation

of FHSIs – both in general and in relation to specific FHSIs.

Communicate with both insurers and the general public regarding how FHSIs are used as

part of supervisory assessments.

Communicate with both insurers and the general public, with appropriate levels of

granularity and transparency, regarding the results for specific insurers and peer groups.

Use a sufficient number of FHSIs in each risk‐assessment category to adequately inform

the risk assessments, considering the results of this survey regarding the usefulness of

specific FHSIs.

Revise the FHSIs, where necessary, to take account of anticipated changes in financial

reporting and regulatory requirements related to IFRS 9 and IFRS 17.

Page 6

Box 1 provides examples of specific steps that might be taken by supervisors in response to

these recommendations.

It is recommended that the IMF and WBG consider taking the following actions, to build on the

results of this project and help to enhance the use of FHSIs by supervisors:

Develop training programs and resources, such as regional seminars and interactive

webinars, on the use of FHSIs. This might be done in collaboration with other

organizations.

Develop and maintain a database of FHSIs being used and benchmarks established by

supervisors, starting from the information in this report. Encourage more supervisors to

provide input, particularly regarding the benchmarks.

Develop an Excel workbook to facilitate the calculation and comparison of FHSIs and

make it widely available to supervisors. Such a tool would probably be especially useful

to supervisors in developing and emerging markets.

Box 1. Examples of Specific Steps that Might be Taken

Recommendation Examples of Specific Steps

Use FHSIs to inform their analyses across the full range of insurance activities they supervise and in the various aspects of supervision for which they are responsible.

Use FHSIs in analyzing non‐conventional insurance activities, such as microinsurance and takaful.

Use FHSIs beyond prudential supervision, such as in market conduct supervision and market development.

Implement robust tools to facilitate the use of FHSIs, including databases, calculation and reporting systems, and written guidance and training on the use and interpretation of FHSIs – both in general and in relation to specific FHSIs.

Develop reporting systems that facilitate comparisons across peer groups.

Map all of the FHSIs being used to each of the relevant categories in the risk‐assessment framework.

Communicate with both insurers and the general public regarding how FHSIs are used as part of supervisory assessments.

Include on the supervisor’s website an explanation of its supervisory methodology, including how FHSIs are used, along with some examples.

Communicate with both insurers and the general public, with appropriate levels of granularity and transparency, regarding the results for specific insurers and peer groups.

Communicate to each insurer the results of key FHSIs and how such results compare with those of their peers.

Use a sufficient number of FHSIs in each risk‐assessment category to adequately inform the risk assessments, considering the results of this survey regarding the usefulness of specific FHSIs.

Select at least three FHSIs for use in each risk‐assessment category, including the 27 FHSIs considered most useful by respondents (or arithmetic transformations of them).

Revise the FHSIs, where necessary, to take account of anticipated changes in financial reporting and regulatory requirements related to IFRS 9 and IFRS 17.

Revise the FHSIs and benchmarks in response to changes in capital adequacy requirements.

Page 7

C. Analysis of Survey Results

This section provides a brief overview of the findings for each of the first 14 survey questions

separately. The findings for the remaining questions, which deal with various topics in relation

to each FHSI, are presented by topic.

The complete set of questions and corresponding data are included in Annex 2, while the

compilation of the same results by topic are included in Annex 3. Many of the tables in Annexes

2 and 3 include an index, the weights for which are shown at the top of the table; in some

cases, the index values are shown in the charts in this section. The index values can be used to

rank the items in the table, which helps in reaching conclusions. The tables in Annex 3 show

rankings both within the respective CARAMELS categories and overall.

Institutional Information

Authorities from thirty‐three jurisdictions responded to the survey. The respondents were well‐

distributed by nature of the jurisdiction and IAIS region, except that there were no responses

from the Middle East and North Africa region. Most respondents were from high (19) or upper

middle income (8) countries, although several were from low (1) or lower middle income (5)

countries. Annex 1 provides a list of the jurisdictions from which responses were received.

7

7

202

8

4

3

Respondents by IAIS Region

Asia and Oceania

Central, Eastern Europe andTranscaucasia

Latin America

Middle East and North Africa

North America

Offshore and CaribbeanIslands

Sub‐Sahara Africa

Western Europe

Page 8

Question 1. What is the institutional nature of YOUR AUTHORITY?

The institutional nature of most of the respondents (19 out of the 33) is an autonomous public

authority, with most of the others being departments in central banks or monetary authorities

Question 2. Which financial sectors are supervised by YOUR AUTHORITY? (More than one

response may be entered, where applicable.)

Very few respondents (4 out of the 33) supervise only the insurance sector. Most also supervise

other sectors, with a fairly even distribution among pensions, banking, securities and other. On

average, the respondents supervise three sectors. The average is significantly lower for the

jurisdictions that are members of the Financial Stability Board (FSB) than for the other

jurisdictions. It is lowest for jurisdictions in the North America and Asia and Oceana regions, and

highest for jurisdictions in Latin America5.

5 See Annex 2, table 2.1 for details.

10

4

19

Q1. Institutional nature of respondents

1. Department within centralbank or monetary authority

2. Department withingovernment ministry (forexample, Ministry of Finance)

3. Autonomous publicauthority

Page 9

Question 3. What types of insurance activities are supervised by YOUR AUTHORITY? (More

than one response may be entered, where applicable.)

All respondents supervise conventional insurance activities. Less than one‐half of the

respondents supervise microinsurance or offshore insurance activities, while very few supervise

takaful or microtakaful.

33

1820

17 18

0

5

10

15

20

25

30

35

1. Insurance 2. Pensions 3. Banking 4. Securities 5. Other

Q2. Financial sectors supervised by respondents

1

0

0

0

1

1

1

0

4

2

2

0

0

0

0

0

1

5

3

0

0

0

1

2

1

0

7

1

5

0

0

0

5

2

1

14

0

0

2

0

0

0

0

1

3

0% 20% 40% 60% 80% 100%

Asia and Oceania

Central, Eastern Europe and Transcaucasia

Latin America

Middle East and North Africa

North America

Offshore and Caribbean Islands

Sub‐Sahara Africa

Western Europe

Total number of respondents

Number of sectors supervised by respondents

1 Sector 2 Sectors 3 Sectors 4 Sectors 5 Sectors

Page 10

Question 4. In which aspects of regulation or supervision are YOUR AUTHORITY involved?

(More than one response may be entered, where applicable.)

Respondents are typically involved in several aspects of regulation or supervision. Most

respondents are involved in micro‐prudential, macro‐prudential, market conduct, and financial

integrity regulation or supervision. About one‐half of the respondents have responsibilities for

market development, but very few are involved in competition policy.

33

14

4

3

13

0 5 10 15 20 25 30 35

1. Conventional insurance

2. Microinsurance

3. Takaful

4. Microtakaful

5. Offshore insurance

Q3. Insurance activities supervised by respondents

0 5 10 15 20 25 30 35

1. Micro‐prudential

2. Macro‐prudential

3. Market conduct

4. Financial integrity (for example, anti‐money laundering)

5. Competition policy

6. Market development

Q4. Aspects of involvement by respondents

Page 11

Use and Communication of FHSIs

Question 5. To what extent does YOUR AUTHORITY use FHSIs in supervising each of the

following types of insurance activities?

Respondents use FHSIs most regularly and consistently in the supervision of conventional

insurance, with an index of 9.5 out of 106. Among those who supervise other insurance

activities, FHSIs are used fairly regularly in the supervision of microinsurance and microtakaful,

but less so for offshore insurance or takaful. There is scope for many authorities to make more

use of FHSIs across the full range of insurance activities they supervise.

Question 6. To what extent does YOUR AUTHORITY use FHSIs in each of the following aspects

of regulation or supervision?

Respondents use FHSIs most regularly and consistently in micro‐prudential supervision, with an

index of 9.4 out of 10, followed by macro‐prudential supervision. Among those responsible for

other aspects of regulation or supervision, FHSIs are used most regularly in the supervision of

financial integrity and least in regulation of competition. There is scope for many authorities to

6 The index for this question was calculated by applying weights of 10, 7, 4, and 1 to responses 1 through 4, respectively. For this question, and all others where a “not applicable” response was available, “not applicable” responses were omitted from the calculation of the index.

9.5

7.4

5.8 7.0 6.6

0%10%20%30%40%50%60%70%80%90%100%

Q5. Use of FHSIs by insurance activity supervised

4. Seldom if ever used

3. Used sometimes

2. Used often but notalways consistently

1. Used regularly andconsistently

Index

Page 12

make more use of FHSIs in relation to all aspects of aspects of regulation and supervision for

which they are responsible, especially those other than prudential supervision.

Question 7. To what extent does YOUR AUTHORITY have the following tools and guidance to

support the use of FHSIs?

Most respondents have tools to support their use of FHSIs, including databases, calculation

tools, and reporting systems7. However, in many cases these tools do not extend to the full

range of FHSIs being used by the authorities. The tools more frequently facilitate analysis of

trends in the FHSIs of each insurer than the comparison of FHSIs for peer groups.

Instructions for calculating FHSIs are typically documented, but written guidance and training

on the use and interpretation of FHSIs – both in general and in relation to specific FHSIs – is

lacking at many authorities.

7 For full text of the items on the horizontal axis please refer to the tables for the respective questions in Annex 2.

Page 13

a. A structured database of the data needed to calculate FHSIs

b. A supervisory reporting system that automatically calculates FHSIs for each insurer

c. Standardized spreadsheets that are used to calculate FHSIs

d. Instructions for calculating FHSIs, including the data and methodology

e. A supervisory reporting system or standardized spreadsheets that facilitate the analysis

of trends in the FHSIs for each insurer

f. A supervisory reporting system or standardized spreadsheets that facilitate the

comparison of FHSIs for peer groups of insurers

g. Supervisory benchmarks for specific FHSIs

h. Written guidance on the interpretation of specific FHSIs

i. Written guidance on the use of FHSIs, in general

j. Training on the interpretation of specific FHSIs

k. Training on the use of FHSIs, in general

Question 8. To what extent does YOUR AUTHORITY communicate with insurers regarding your

use of FHSIs?

Overall, the extent to which respondents communicate with insurers regarding FHSIs is limited,

with an average index of 3.0. Where information is communicated, it most commonly includes

a general explanation of how the authority uses FHSIs and the results of some FHSIs for the

specific insurer. However, on each of the aspects regarding the use of FHSIs queried, at least

some respondents do communicate extensively with insurers. This suggests that many

authorities could go further in communicating how FHSIs are used as part of their supervisory

assessments, the results for a specific insurer, and how such results compare with those of its

peers.

6.7

5.5

6.2 6.2

7.1

5.7

5.0 4.9 4.9 4.6 4.5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

a. b. c. d. e. f. g. h. i. j. k.

Q7. Availability of tools and guidance

4. Not available

3. Available for few if any FHSIs

2. Available for many FHSIs

1. Available for all or most FHSIs,where relevant

Index

Page 14

Question 9. To what extent does YOUR AUTHORITY communicate with the general public

regarding your use of FHSIs?

As might be expected, the extent to which respondents communicate with the general public

regarding FHSIs is even more limited than their communication with insurers, with an average

index of 1.8. Where information is communicated, it most commonly includes a general

explanation of how the authority uses FHSIs, descriptions of some FHSIs, and the aggregate

results of some FHSIs for peer groups of insurers or the industry. However, on each of the

aspects regarding the use of FHSIs queried, at least some respondents do communicate

extensively with the general public. This suggests that most authorities could go further in

communicating how FHSIs are used as part of their supervisory assessments and the results for

specific insurers and peer groups.

Page 15

Question 10. Which of the following categories are included in the risk‐assessment framework

used by YOUR AUTHORITY?

Almost all respondents (32 of 33) reported having a risk‐assessment framework with various

categories within which risks are assessed. The categories most commonly used are those that

are typically part of the CARAMELS framework, with the exception of the Subsidiaries category.

However, many respondents also indicate that they are using categories that are typically part

of risk‐based supervision frameworks, such as Insurance, Credit, and Market risks. This suggests

that some authorities might be applying more than one framework simultaneously (examples

of which have been seen in some TA projects) or that they might have responded affirmatively

to more categories than actually exist in their assessment frameworks (on the basis that the

other categories are “similar”). “Other” categories used by some authorities include Anti‐

Money Laundering and Combatting the Financing of Terrorism Risk, Outsourcing Risk,

Enforcement Issues, Contagion Risk, Emerging Risks, Policies and Procedures, and Shariah Non‐

compliance Risk.

Page 16

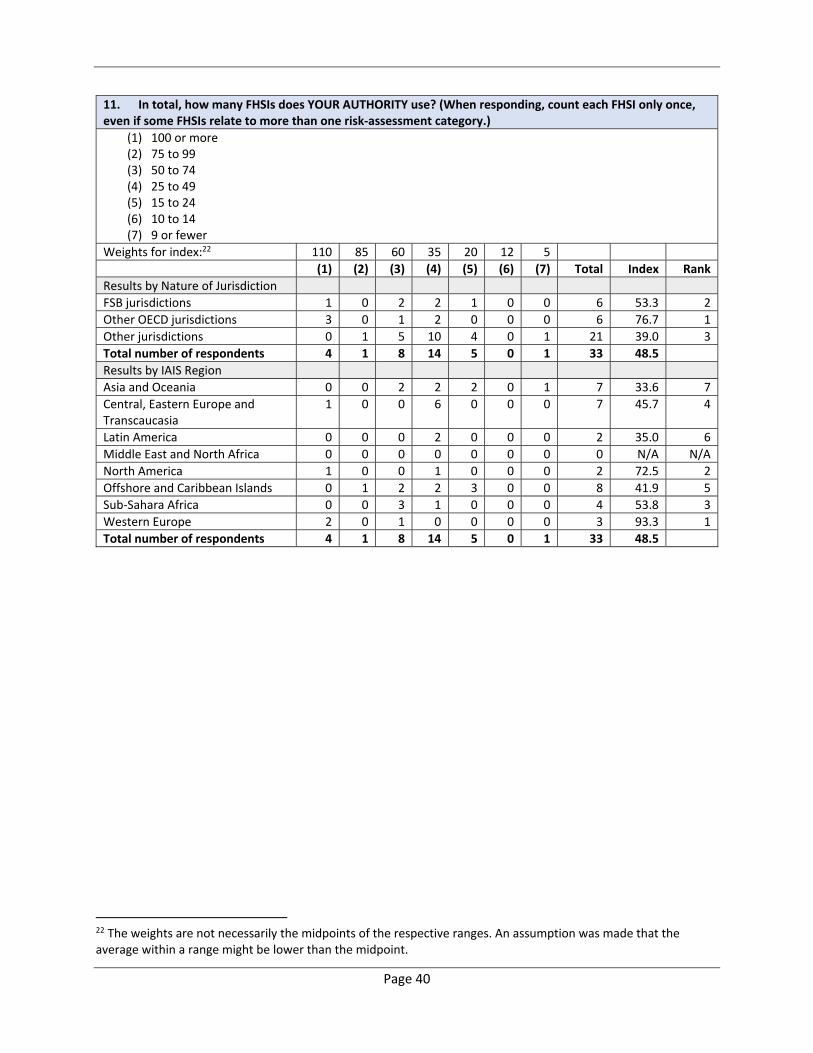

Question 11. In total, how many FHSIs does YOUR AUTHORITY use? (When responding, count

each FHSI only once, even if some FHSIs relate to more than one risk‐assessment category.)

Most respondents use between 25 and 74 FHSIs in total, although several use 100 or more. The

overall average is roughly 50, with the Western Europe and North America regions having

significantly higher averages.

Page 17

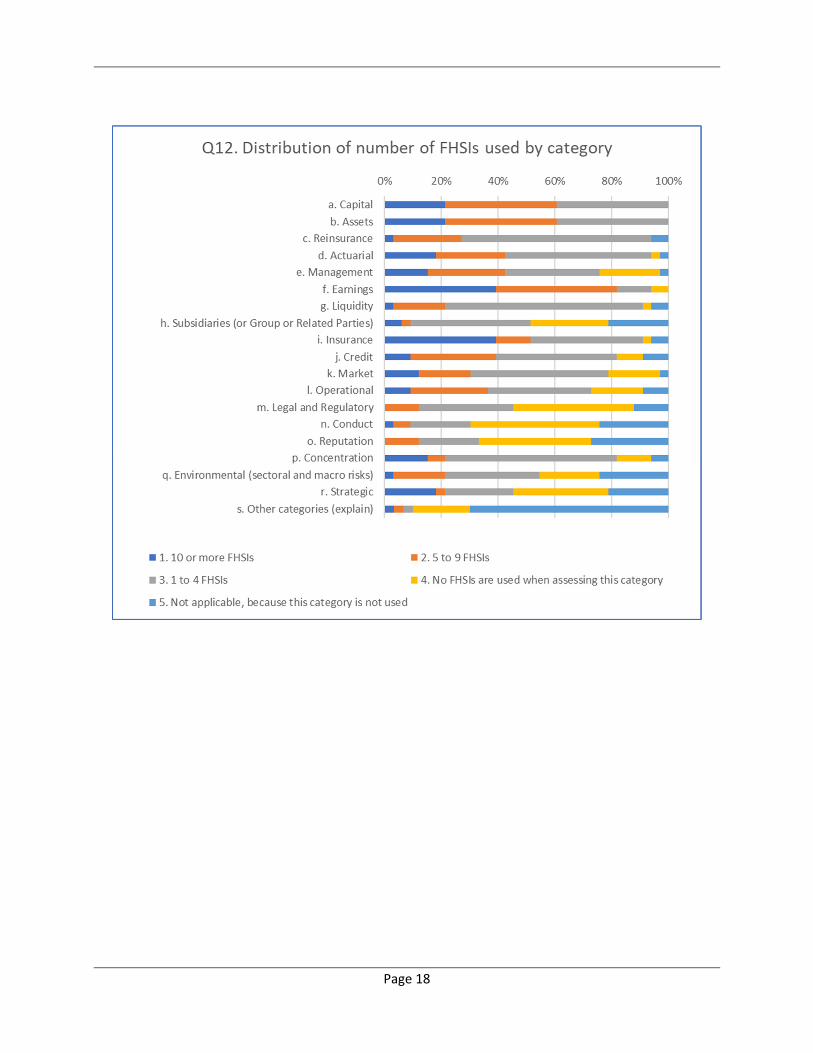

Question 12. How many FHSIs does YOUR AUTHORITY use when assessing each of the

categories in your risk‐assessment framework? (When responding, count all FHSIs mapped to

the risk‐assessment category, even if they have also been mapped other categories.)

The average number of FHSIs used by respondents when assessing the various risk‐assessment

categories varies significantly by category, around an overall average of 4.6 per category.

Unsurprisingly, the categories where the greatest numbers of FHSIs are being used are financial

in nature (Earnings, Capital, and Assets), together with Insurance Risk. Although relatively few

FHSIs are being used in assessing the more governance‐related categories, the average for

almost every category is at least two FHSIs.

0

2

4

6

8

10

12

14

16

100 or more 75 to 99 50 to 74 25 to 49 15 to 24 10 to 14 9 or fewer

Q11. Total number of FHSIs used by respondents

Number of respondents

33.6 45.7

35.0

‐

72.5

41.9 53.8

93.3

48.5

‐ 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0 100.0

0%10%20%30%40%50%60%70%80%90%100%

Distribution of total number of FHSIs used

9 or fewer

10 to 14

15 to 24

25 to 49

50 to 74

75 to 99

100 or more

Average

Page 18

Page 19

Looking to the Future

Question 13. To what extent has YOUR AUTHORITY progressed in revising the FHSIs it uses to

take account of anticipated changes in financial reporting and regulatory requirements related to

IFRS 9 and IFRS 17?

The implementation of two key International Financial Reporting Standards (IFRSs), IFRS 9

Financial Instruments and IFRS 17 Insurance Contracts, in many jurisdictions is widely expected

to result in the need to make changes in financial reporting and regulatory requirements, such

as capital adequacy requirements. Most respondents are still early in the process of revising the

FHSIs to take account of anticipated changes in financial reporting and regulatory requirements

related to IFRS 9 and IFRS 17. Nearly one‐half have yet to consider the need for revisions to

FHSIs and most of those who have considered the need for revisions have yet to make them.

The responses do not vary significantly by risk‐assessment category.

Page 20

Question 14. In addition to the resources and tools currently available (for example, the Core

Curriculum modules), to what extent would the following initiatives that might be considered by

the IMF, the WBG, or others be useful to YOUR AUTHORITY in enhancing your use of FHSIs?

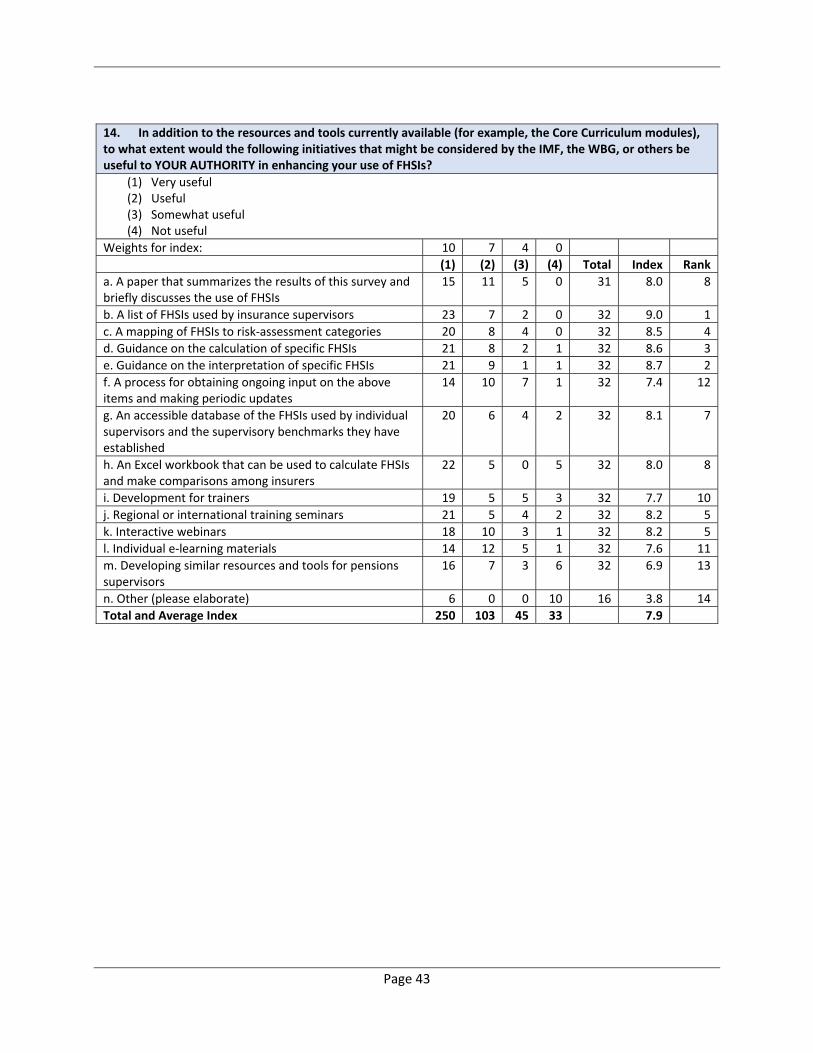

Overall, respondents indicated that each of the suggested initiatives would be useful in

enhancing the use of FHSIs. The four initiatives ranked most highly (items b, c, d, and e), along

with item a, are being dealt with by this project. Also ranked highly were several training‐

related items (items j and k), a database of FHSIs being used and benchmarks established by

supervisors, and an Excel workbook to facilitate the calculation and comparison of FHSIs.

Page 21

Page 22

Input on Specific FHSIs by Topic

A. Does YOUR AUTHORITY use the following FHSIs?8

(1) Yes, as described

(2) An arithmetic transformation is used

(3) No

The survey questionnaire asked about 95 FHSIs. The responses indicate that a wide variety of

FHSIs are being used by supervisors. In aggregate, for the 95 FHSIs queried, only 37 percent of

the responses indicated that FHSIs as described were being used, with another 5 percent

indicating that arithmetic transformations were being used. This leaves 58 percent of the

responses indicating that the FHSIs were not being used. In fact, several of the FHSIs are being

used by few, if any, of the respondents.

The table below lists the 27 FHSIs queried that are most frequently used by respondents. It

includes those FHSIs whose indices9 ranked either in the top two within the respective

CARAMELS category or in the top 20 overall.

8 Survey questions 15, 21, 27, 33, 39, 45, 51, 57, and 63. 9 The index for this question was calculated by applying weights of 10, 8, and 0 to responses 1 through 3, respectively.

Page 23

FHSIs Most Frequently Used by Respondents Index

1.06 : Cover of solvency margin 8.7

1.07 : Risk‐based capital adequacy ratios 6.5

1.08 : Growth in capital 8.6

2.02 : Real estate / total assets 5.8

2.17 : Investments: distribution by type 7.4

3.01 : Risk retention ratio 9.1

3.03 : Maximum exposure to single risk / capital 3.1

4.04 : Claims development 6.2

4.05 : Underwritten business: distribution by class of business 7.9

5.03 : Operating expenses / gross written premium 7.8

5.05 : Growth in gross written premium 9.0

5.06 : Growth in net written premium 8.4

5.07 : Growth in total assets 8.4

6.01 : Claims ratio 9.5

6.02 : Gross claims ratio 7.7

6.03 : Expense ratio 9.2

6.04 : Combined ratio [FSI Non‐Life] 9.2

6.05 : Investment income ratio 6.8

6.07 : Profitability ratio 6.7

6.12 : Return on equity (ROE) [FSI] 8.7

6.14 : Return on assets (ROA) [FSI Life] 6.8

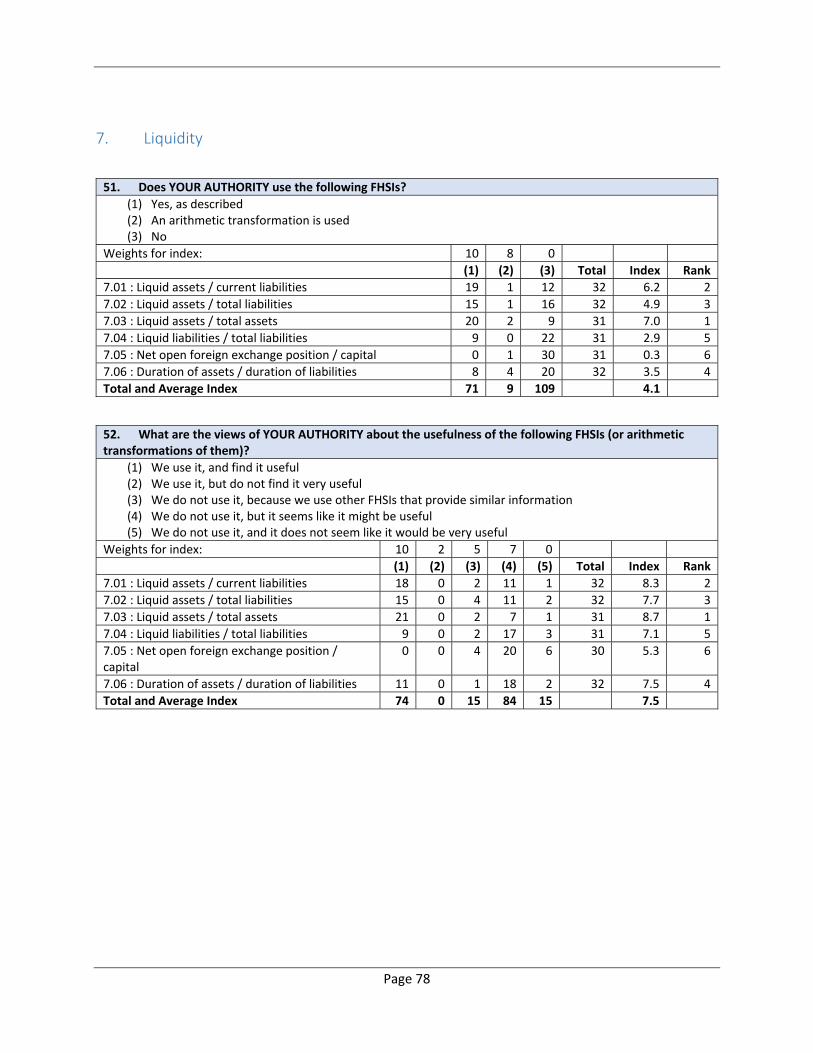

7.01 : Liquid assets / current liabilities 6.2

7.03 : Liquid assets / total assets 7.0

8.02 : Related party receivables / total assets 3.9

8.04 : (Investments in related parties + related party receivables) / total assets 3.4

9.03 : Penetration 7.5

9.04 : Density 6.0

B. What are the views of YOUR AUTHORITY about the usefulness of the following FHSIs (or

arithmetic transformations of them)?10

(1) We use it, and find it useful

(2) We use it, but do not find it very useful

(3) We do not use it, because we use other FHSIs that provide similar information

(4) We do not use it, but it seems like it might be useful

(5) We do not use it, and it does not seem like it would be very useful

The responses regarding the usefulness of the FHSIs queried were considerably more positive,

with an average index of 7.1, than those regarding use, where the average index was only 4.1.

10 Survey questions 16, 22, 28, 34, 40, 46, 52, 58, and 64.

Page 24

40 percent of the responses indicated that the FHSIs being used were useful, with only 1

percent indicating that they were not useful. Another 5 percent indicated that the FHSIs were

not being used because other FHSIs that provide similar information are being used instead. 41

percent of the responses indicated that, although they were not using the specific FHSIs, the

FHSIs seemed like they might be useful, with only 14 percent of the responses indicating that

they did not seem like they would be very useful. This suggests that many supervisors could

benefit from using additional FHSIs.

The table below lists the 27 FHSIs considered most useful by respondents. It includes those

FHSIs whose indices11 ranked either in the top two within the respective CARAMELS category or

in the top 20 overall.

FHSIs Considered Most Useful by Respondents Index

1.03 : Capital / total assets 8.6

1.06 : Cover of solvency margin 9.5

1.07 : Risk‐based capital adequacy ratios 8.3

1.08 : Growth in capital 9.5

2.11 : Equities / total assets 8.2

2.17 : Investments: distribution by type 9.0

3.01 : Risk retention ratio 9.6

3.02 : (Reinsurance recoveries + reinsurance commissions) / reinsurance ceded 7.6

3.03 : Maximum exposure to single risk / capital 7.6

4.04 : Claims development 8.9

4.05 : Underwritten business: distribution by class of business 9.3

5.05 : Growth in gross written premium 9.3

5.06 : Growth in net written premium 8.6

5.07 : Growth in total assets 9.0

6.01 : Claims ratio 9.4

6.02 : Gross claims ratio 9.0

6.03 : Expense ratio 9.4

6.04 : Combined ratio [FSI Non‐Life] 9.4

6.07 : Profitability ratio 8.3

6.12 : Return on equity (ROE) [FSI] 9.5

6.14 : Return on assets (ROA) [FSI Life] 8.5

7.01 : Liquid assets / current liabilities 8.3

7.03 : Liquid assets / total assets 8.7

8.02 : Related party receivables / total assets 7.2

8.04 : (Investments in related parties + related party receivables) / total assets 6.9

9.03 : Penetration 7.8

9.04 : Density 7.4

11 The index for this question was calculated by applying weights of 10, 2, 5, 7, and 0 to responses 1 through 5, respectively.

Page 25

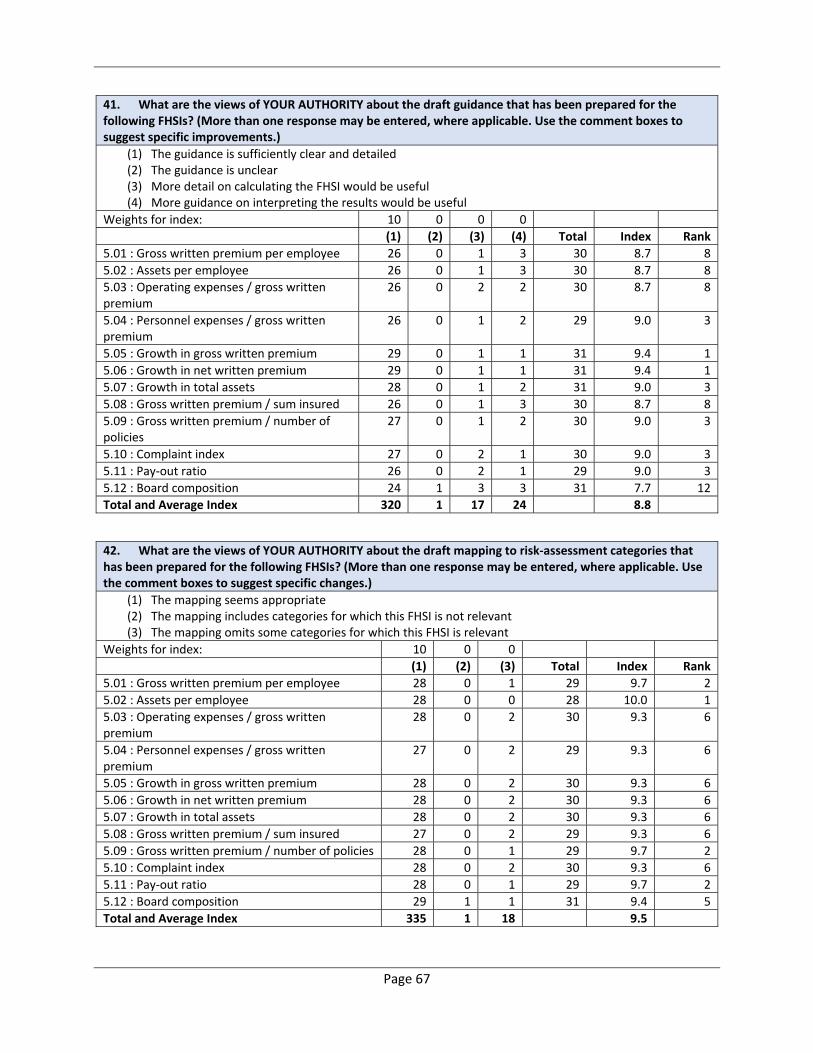

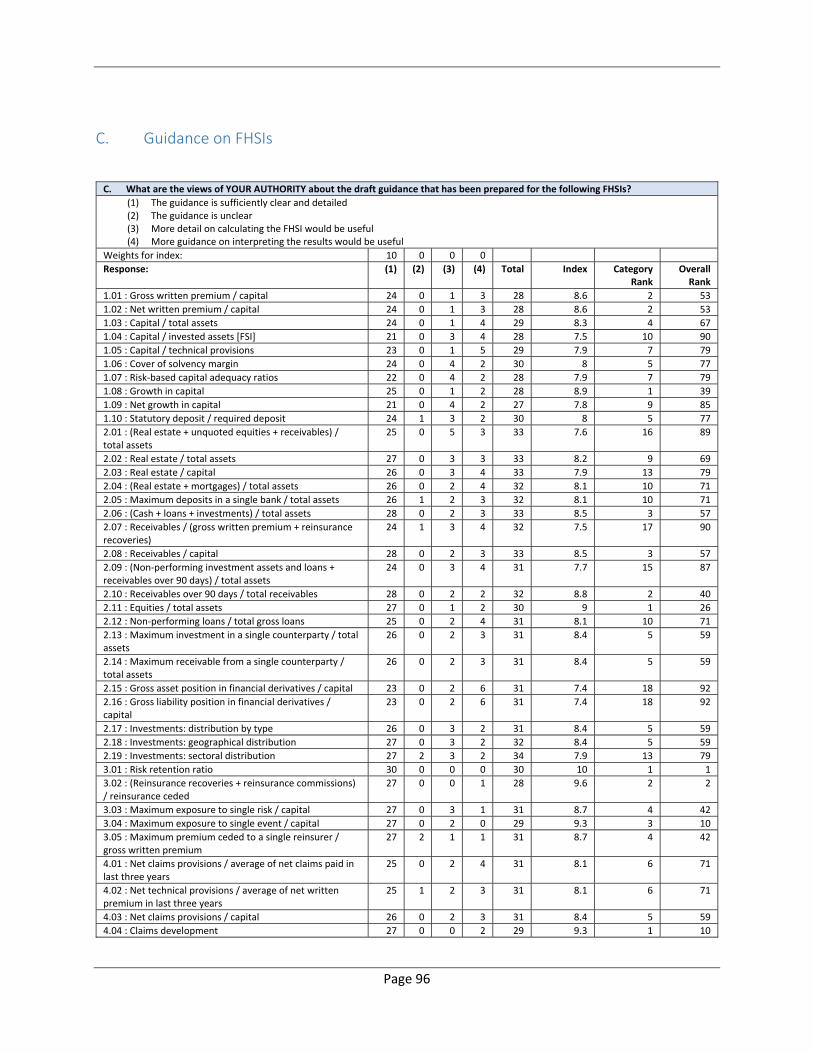

C. What are the views of YOUR AUTHORITY about the draft guidance that has been prepared

for the following FHSIs?12

(1) The guidance is sufficiently clear and detailed

(2) The guidance is unclear

(3) More detail on calculating the FHSI would be useful

(4) More guidance on interpreting the results would be useful

The draft guidance seems largely to have achieved a good balance between being concise but

still sufficiently clear and detailed, with response 1 accounting for 86 percent of the responses

and response 2 for only 1 percent. However, respondents were able to enter more than one

response; some did so, for example, combining response 1 with response 3 or 4. Response 3

accounted for 6 percent of the responses and response 4 for 8 percent. A few respondents

offered explicit suggestions for improving the guidance, which were particularly appreciated.

The responses to this question have been carefully considered in the preparation of the

guidance included in Annex 5.

D. What are the views of YOUR AUTHORITY about the draft mapping to risk‐assessment

categories that has been prepared for the following FHSIs?13

(1) The mapping seems appropriate

(2) The mapping includes categories for which this FHSI is not relevant

(3) The mapping omits some categories for which this FHSI is relevant

Respondents were largely satisfied with the draft guidance mappings of the FHSIs to risk‐

assessment categories, with response 1 accounting for 96 percent of the responses.

Respondents were able to enter more than one response, and some did so. Response 2

accounted for only 1 percent of the responses and response 3 for 4 percent. The responses to

this question have been carefully considered in the preparation of the mapping included in

Annex 5. Although none of the mappings in the draft guidance were deleted, most of the

additions suggested by respondents have been included. Also, the comments inspired further

consideration of the mappings, which resulted in some additions that were not explicitly

suggested by respondents.

12 Survey questions 17, 23, 29, 35, 41, 47, 53, 59, and 65. 13 Survey questions 18, 24, 30, 36, 42, 48, 54, 60, and 66.

Page 26

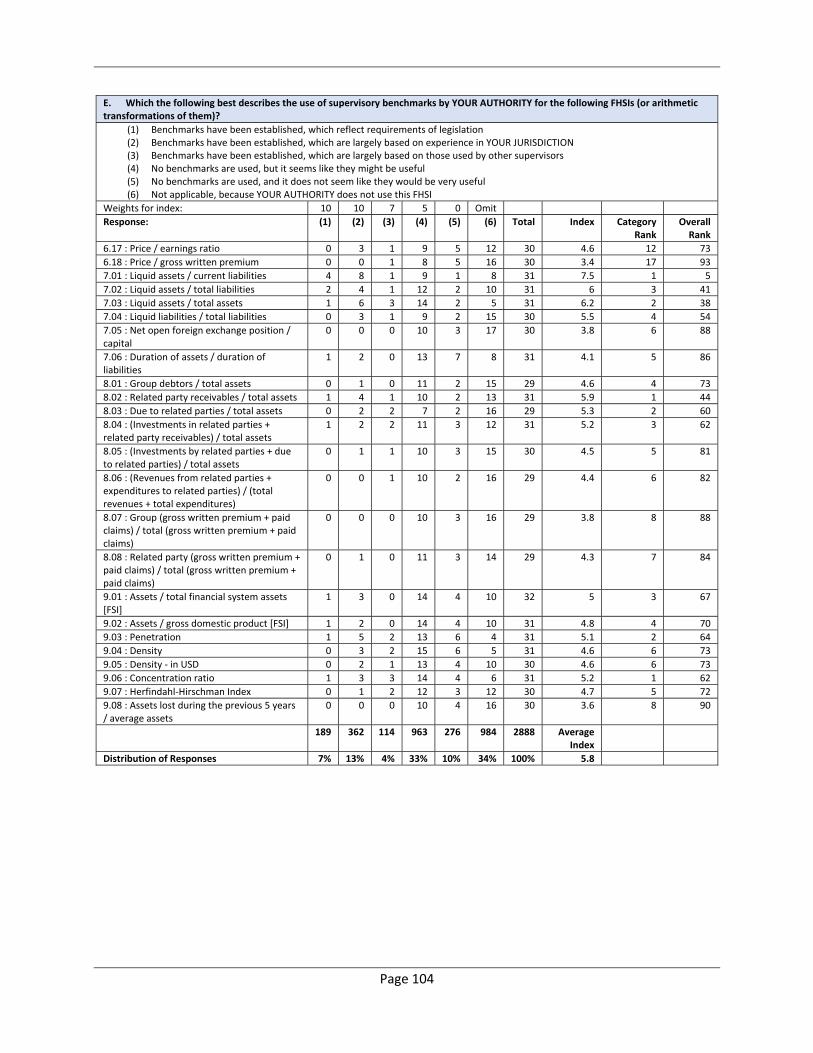

E. Which the following best describes the use of supervisory benchmarks by YOUR AUTHORITY

for the following FHSIs (or arithmetic transformations of them)?14

(1) Benchmarks have been established, which reflect requirements of legislation

(2) Benchmarks have been established, which are largely based on experience in YOUR

JURISDICTION

(3) Benchmarks have been established, which are largely based on those used by other

supervisors

(4) No benchmarks are used, but it seems like they might be useful

(5) No benchmarks are used, and it does not seem like they would be very useful

(6) Not applicable, because YOUR AUTHORITY does not use this FHSI

In TA projects, supervisors often express interest in having benchmarks against which to assess

the FHSIs of their insurers. However, as noted by some respondents, many FHSIs do not lend

themselves to fixed, internationally applicable benchmarks. In some cases, benchmarks are

appropriate, but will need to vary to reflect factors such as conditions in the local insurance

market or the economy. In some other cases, FHSIs are used primarily to help achieve a better

understanding of an insurer’s business and how it is changing over time, so it might be

inappropriate to establish benchmarks for “good” or “bad” levels of an FHSI.

The chart below shows the distribution of responses, from those authorities using the queried

FHSIs, regarding their use of benchmarks and the sources of the benchmarks that are being

used. The questions also sought views on the potential usefulness of benchmarks for those

FHSIs for which benchmarks are not currently being used. The results confirm the above

observation regarding the level of interest in having benchmarks, with only 14 percent of the

responses relating to cases where benchmarks would not be considered useful. However, only

35 percent of the responses indicated cases where benchmarks are currently in place. The

results suggest that supervisors would be very interested in a database of benchmarks or more

guidance on the development of benchmarks, which is consistent with the response to item g

of question 14.

14 Survey questions 19, 25, 31, 37, 43, 49, 55, 61, and 67.

Page 27

The table below lists the 32 FHSIs for which benchmarks might be most useful. It includes those

FHSIs whose indices15 ranked either in the top two within the respective CARAMELS category or

in the top 20 overall.

15 The index for this question was calculated by applying weights of 10, 10, 7, 5, and 0 to responses 1 through 5, respectively. Those who responded 6 were omitted from the calculation.

Page 28

FHSIs for Which Benchmarks Might Be Most Useful Index

1.01 : Gross written premium / capital 7.0

1.02 : Net written premium / capital 7.4

1.03 : Capital / total assets 7.1

1.04 : Capital / invested assets [FSI] 7.1

1.06 : Cover of solvency margin 9.0

1.07 : Risk‐based capital adequacy ratios 8.7

1.08 : Growth in capital 6.9

1.10 : Statutory deposit / required deposit 8.2

2.01 : (Real estate + unquoted equities + receivables) / total assets 7.3

2.04 : (Real estate + mortgages) / total assets 7.1

2.05 : Maximum deposits in a single bank / total assets 7.2

2.08 : Receivables / capital 7.2

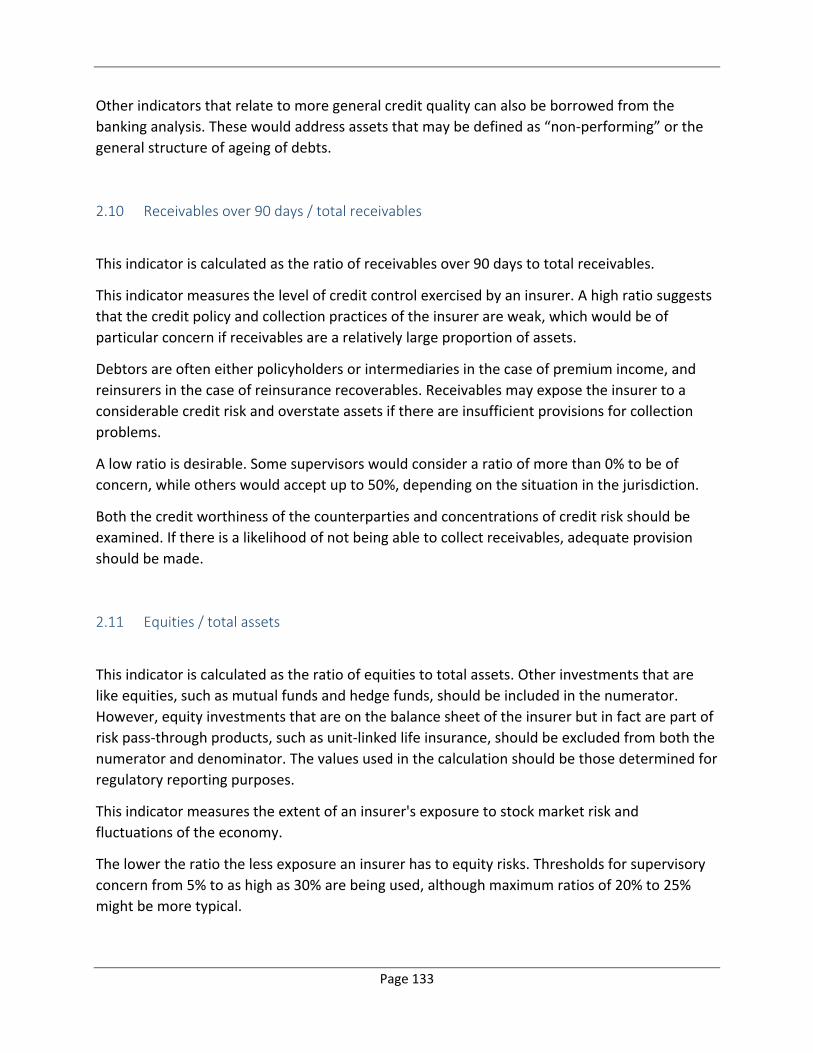

2.10 : Receivables over 90 days / total receivables 7.6

2.13 : Maximum investment in a single counterparty / total assets 7.1

2.14 : Maximum receivable from a single counterparty / total assets 7.3

2.17 : Investments: distribution by type 7.0

3.01 : Risk retention ratio 6.3

3.03 : Maximum exposure to single risk / capital 6.3

3.05 : Maximum premium ceded to a single reinsurer / gross written premium 6.3

4.01 : Net claims provisions / average of net claims paid in last three years 5.9

4.08 : Actuarial assumption: short‐term interest rate 5.9

4.09 : Actuarial assumption: long‐term interest rate 6.3

5.03 : Operating expenses / gross written premium 7.0

5.12 : Board composition 7.2

6.03 : Expense ratio 6.8

6.04 : Combined ratio [FSI Non‐Life] 7.4

7.01 : Liquid assets / current liabilities 7.5

7.03 : Liquid assets / total assets 6.2

8.02 : Related party receivables / total assets 5.9

8.03 : Due to related parties / total assets 5.3

9.03 : Penetration 5.1

9.06 : Concentration ratio 5.2

Page 29

F. If YOUR AUTHORITY has established benchmarks for the following FHSIs, what benchmarks

are used for conventional insurance activities?16

1. Minimum for non‐life insurance

2. Maximum for non‐life insurance

3. Minimum for life insurance

4. Maximum for life insurance

Authorities were asked to provide the benchmarks being used for the FHSIs for which they had

established benchmarks. Unfortunately, very few authorities provided quantitative responses

for most of the FHSIs. For 41 of the 95 FHSIs queried, none of the respondents provided

benchmarks. Among the FHSIs that attracted few or no quantitative responses would be those

that do not lend themselves to the use of benchmarks. However, this still leaves considerable

scope for gathering more data on the benchmarks being used by supervisors.17

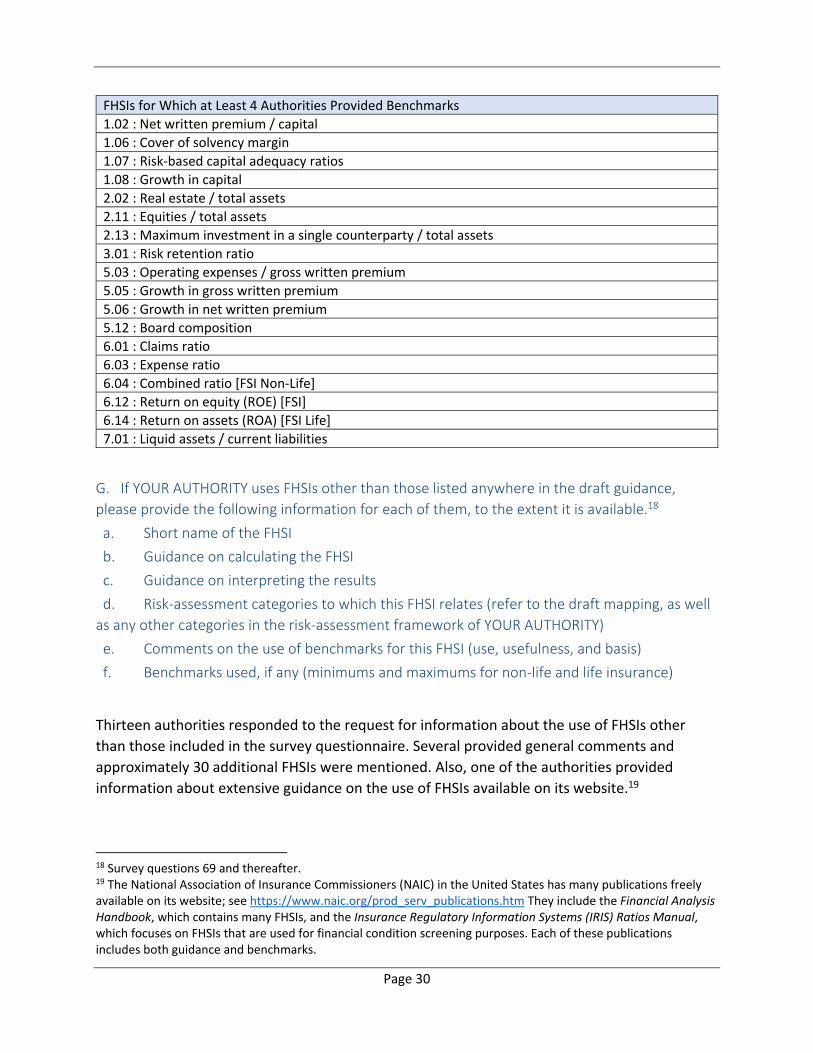

The table below lists the 18 FHSIs for which at least 4 authorities provided quantitative

responses.

16 Survey questions 20, 26, 32, 38, 44, 50, 56, 62, and 68. 17 The survey questionnaire allowed free‐form entry of responses regarding the benchmarks used. Perhaps, a more structured format, such as the entry of specific percentages or selection from ranges of percentages, would elicit more quantitative data.

Page 30

FHSIs for Which at Least 4 Authorities Provided Benchmarks

1.02 : Net written premium / capital

1.06 : Cover of solvency margin

1.07 : Risk‐based capital adequacy ratios

1.08 : Growth in capital

2.02 : Real estate / total assets

2.11 : Equities / total assets

2.13 : Maximum investment in a single counterparty / total assets

3.01 : Risk retention ratio

5.03 : Operating expenses / gross written premium

5.05 : Growth in gross written premium

5.06 : Growth in net written premium

5.12 : Board composition

6.01 : Claims ratio

6.03 : Expense ratio

6.04 : Combined ratio [FSI Non‐Life]

6.12 : Return on equity (ROE) [FSI]

6.14 : Return on assets (ROA) [FSI Life]

7.01 : Liquid assets / current liabilities

G. If YOUR AUTHORITY uses FHSIs other than those listed anywhere in the draft guidance,

please provide the following information for each of them, to the extent it is available.18

a. Short name of the FHSI

b. Guidance on calculating the FHSI

c. Guidance on interpreting the results

d. Risk‐assessment categories to which this FHSI relates (refer to the draft mapping, as well

as any other categories in the risk‐assessment framework of YOUR AUTHORITY)

e. Comments on the use of benchmarks for this FHSI (use, usefulness, and basis)

f. Benchmarks used, if any (minimums and maximums for non‐life and life insurance)

Thirteen authorities responded to the request for information about the use of FHSIs other

than those included in the survey questionnaire. Several provided general comments and

approximately 30 additional FHSIs were mentioned. Also, one of the authorities provided

information about extensive guidance on the use of FHSIs available on its website.19

18 Survey questions 69 and thereafter. 19 The National Association of Insurance Commissioners (NAIC) in the United States has many publications freely available on its website; see https://www.naic.org/prod_serv_publications.htm They include the Financial Analysis Handbook, which contains many FHSIs, and the Insurance Regulatory Information Systems (IRIS) Ratios Manual, which focuses on FHSIs that are used for financial condition screening purposes. Each of these publications includes both guidance and benchmarks.

Page 31

Some of the FHSIs mentioned by respondents were the same as those queried but employed

different terminology. Some of the others would facilitate more detailed analyses by focusing

on the composition of various elements of financial results, such as the composition of available

or required capital, or particular types of expenses or claims. Still others were suggestions of

information that could be analyzed, but were not themselves FHSIs, such as exceedance

probability curves.

The responses were greatly appreciated, and the information provided has been used in various

ways, as summarized in the following table. This includes the addition of three new FHSIs to the

guidance: capital in excess of minimum required / average annual loss (“burn rate”), highest

quality liquid assets / claims, and inclusion.

FHSI Categories Disposition

Composition of available capital by tier

Capital Discussed in guidance for FHSIs 1.06 and 1.07

Retained earnings or accumulated losses / paid‐up capital

Capital Discussed in guidance for FHSIs 1.06 and 1.07

Impact of long‐term guarantee measures20

Capital Jurisdiction‐specific

Composition of required capital by risk category

Capital Discussed in guidance for FHSIs 1.06 and 1.07

Capital in excess of minimum required / average annual loss

Capital, Legal and Regulatory New FHSI 1.11

Structured finance investments / total investments

Assets Discussed in guidance for FHSIs 2.01 and 2.17

Assets with counterparty risk / total assets

Assets Discussed in guidance for FHSIs 2.13, 2,14 and 2.17

Debt securities / total assets Assets Discussed in guidance for FHSIs 2.13, 2,14 and 2.17

Growth in claims paid Actuarial Discussed in guidance for FHSI 4.01

Growth in technical provisions Actuarial, Management, Insurance, Legal and Regulatory, Operational, Conduct, Strategic

Discussed in guidance for FHSIs 4.02 and 5.07

Surrender values / technical provisions [for relevant life classes of business]

Actuarial Discussed in guidance for FHSI 4.02

20 The long‐term guarantees measures were introduced in the Solvency II Directive to ensure an appropriate treatment of insurance products that include long‐term guarantees. The long‐term guarantees measures are the following: the extrapolation of risk‐free interest rates; the matching adjustment; the volatility adjustment; the extension recovery period in case of non‐compliance with the Solvency Capital Requirement; the transitional measure on the risk‐free interest rates; the transitional measure on technical provisions.

Page 32

FHSI Categories Disposition

Technical provisions for unit‐linked business / assets backing unit‐linked business

Actuarial Discussed in guidance for FHSI 4.02

Non‐guaranteed distributions to policyholders / distributions to policyholders illustrated at time of sale

Management, Insurance, Legal and Regulatory, Conduct, Reputation, Strategic

Discussed in guidance for FHSI 5.10

Growth in market share Management, Insurance, Legal and Regulatory, Operational, Conduct, Strategic

Discussed in guidance for FHSIs 5.05, 5.06, and 5.07

Catastrophe claims / total claims Earnings, Actuarial, Insurance Discussed in guidance for FHSIs 6.01 and 6.02

Catastrophe claims / catastrophe premiums [average over a period of years]

Earnings, Actuarial, Insurance Discussed in guidance for FHSIs 6.01 and 6.02

Surrenders / total claims Earnings, Actuarial, Insurance Discussed in guidance for FHSIs 6.01 and 6.02

Commission expense ratio Earnings, Insurance, Operational, Conduct

Discussed in guidance for FHSI 6.03

Investment income / profits Earnings Discussed in guidance for FHSIs 6.06 and 6.07

Composition of profits by component [underwriting, investment income, unrealized capital gains]

Earnings Discussed in guidance for FHSIs 6.06 and 6.07

Premium persistency Earnings, Liquidity, Insurance, Conduct

Discussed in guidance for FHSI 6.15

Highest quality liquid assets / claims Liquidity, Insurance New FHSI 7.07

(Investments in related parties + related party receivables) / capital

Subsidiaries, Capital, Assets, Liquidity, Credit, Reputation, Concentration

Discussed in guidance for FHSIs 8.01, 8.02, 8.03, and 8.04

Inclusion [number of people with at least one insurance policy / population]

Management, Reputation, Environmental, Strategic

New FHSI 9.07

Page 33

Annex 1 Respondents by Jurisdiction

Nature of Jurisdiction Income Level21 IAIS Region

IAIS Member

FSB

Other OEC

D

Other

Low In

come

Lower M

iddle

Income

Upper M

iddle

Income

High In

come

Asia an

d Ocean

ia

Central, Eastern

European

d

Latin America

Middle East an

d

NorthAfrica

North America

Offshore and

CaribbeanIslands

Sub‐Sah

ara Africa

Western Europe

Albania x x x

Austria x x x

Bahamas x x x

Belgium x x x

Belize x x x

Bermuda x x x

British Virgin Islands x x x

Canada ‐ OSFI x x x

Cayman Islands, BWI x x x

China, Hong Kong x x x

Chinese Taipei x x x

Colombia x x x

Croatia (Republic of ) x x x

Gibraltar x x x

Hungary x x x

India x x x

Lithuania x x x

Malaysia x x x

Maldives (Republic of ) x x x

Namibia x x x

Nigeria x x x

Pakistan x x x

Philippines x x x

Portugal x x x

Rwanda x x x

Slovakia x x x

Slovenia x x x

South Africa x x x

Turkey x x x

Turks & Caicos BWI x x x

Uruguay x x x

USA, NAIC x x x

Vanuatu x x x

Jurisdictions of respondents by category 6 6 21 1 5 8 19 7 7 2 0 2 8 4 3

Total number of respondents 33

21 World Bank classification

Page 34

Annex 2 Detailed Results by Question

0. Distribution of respondents by nature of jurisdiction and IAIS region

FSB jurisdictions

Other OECD jurisdictions

Other jurisdictions

Total

Asia and Oceania 2 0 5 7

Central, Eastern Europe and Transcaucasia 1 3 3 7

Latin America 0 0 2 2

Middle East and North Africa 0 0 0 0

North America 2 0 0 2

Offshore and Caribbean Islands 0 0 8 8

Sub‐Sahara Africa 1 0 3 4

Western Europe 0 3 0 3

Total number of respondents 6 6 21 33

1. What is the institutional nature of YOUR AUTHORITY?

(1) Department within central bank or monetary authority (2) Department within government ministry (for example, Ministry of Finance) (3) Autonomous public authority (for example, Financial Services Authority)

(1) (2) (3) Total

Results by Nature of Jurisdiction

FSB jurisdictions 1 1 4 6

Other OECD jurisdictions 3 0 3 6

Other jurisdictions 6 3 12 21

Total number of respondents 10 4 19 33

Results by IAIS Region

Asia and Oceania 2 2 3 7

Central, Eastern Europe and Transcaucasia 3 1 3 7

Latin America 1 0 1 2

Middle East and North Africa 0 0 0 0

North America 0 0 2 2

Offshore and Caribbean Islands 1 1 6 8

Sub‐Sahara Africa 2 0 2 4

Western Europe 1 0 2 3

Total number of respondents 10 4 19 33

Page 35

2. Which financial sectors are supervised by YOUR AUTHORITY? (More than one response may be entered, where applicable.)

(1) Insurance (2) Pensions (3) Banking (4) Securities (5) Other

(1) (2) (3) (4) (5) Total

Results by Nature of Jurisdiction

FSB jurisdictions 6 3 2 0 1 6

Other OECD jurisdictions 6 5 4 4 2 6

Other jurisdictions 21 10 14 13 15 21

Total number of respondents 33 18 20 17 18 33

Results by IAIS Region

Asia and Oceania 7 2 3 2 4 7

Central, Eastern Europe and Transcaucasia 7 7 3 5 2 7

Latin America 2 2 2 2 2 2

Middle East and North Africa 0 0 0 0 0 0

North America 2 1 1 0 0 2

Offshore and Caribbean Islands 8 2 7 5 5 8

Sub‐Sahara Africa 4 2 2 1 3 4

Western Europe 3 2 2 2 2 3

Total number of respondents 33 18 20 17 18 33

2.1 Number of financial sectors supervised.

1 2 3 4 5 Total Average number supervised

Results by Nature of Jurisdiction

FSB jurisdictions 2 2 2 0 0 6 2.00

Other OECD jurisdictions 0 2 0 3 1 6 3.50

Other jurisdictions 2 1 5 11 2 21 3.48

Total number of respondents 4 5 7 14 3 33 3.21

Results by IAIS Region

Asia and Oceania 1 2 3 1 0 7 2.57

Central, Eastern Europe and Transcaucasia 0 2 0 5 0 7 3.43

Latin America 0 0 0 0 2 2 5.00

Middle East and North Africa 0 0 0 0 0 0 ‐

North America 1 0 1 0 0 2 2.00

Offshore and Caribbean Islands 1 0 2 5 0 8 3.38

Sub‐Sahara Africa 1 0 1 2 0 4 3.00

Western Europe 0 1 0 1 1 3 3.67

Total number of respondents 4 5 7 14 3 33 3.21

Page 36

3. What types of insurance activities are supervised by YOUR AUTHORITY? (More than one response may be entered, where applicable.)

(1) Conventional insurance (2) Microinsurance (3) Takaful (4) Microtakaful (5) Offshore insurance

(1) (2) (3) (4) (5) Total

Results by Nature of Jurisdiction

FSB jurisdictions 6 2 0 0 1 6

Other OECD jurisdictions 6 1 0 0 1 6

Other jurisdictions 21 11 4 3 11 21

Total number of respondents 33 14 4 3 13 33

Results by IAIS Region

Asia and Oceania 7 6 3 3 3 7

Central, Eastern Europe and Transcaucasia 7 0 0 0 0 7

Latin America 2 1 0 0 1 2

Middle East and North Africa 0 0 0 0 0 0

North America 2 0 0 0 0 2

Offshore and Caribbean Islands 8 2 0 0 7 8

Sub‐Sahara Africa 4 4 1 0 1 4

Western Europe 3 1 0 0 1 3

Total number of respondents 33 14 4 3 13 33

4. In which aspects of regulation or supervision are YOUR AUTHORITY involved? (More than one response may be entered, where applicable.)

(1) Micro‐prudential (2) Macro‐prudential (3) Market conduct (4) Financial integrity (for example, anti‐money laundering) (5) Competition policy (6) Market development

(1) (2) (3) (4) (5) (6) Total

Results by Nature of Jurisdiction

FSB jurisdictions 5 5 4 4 0 3 6

Other OECD jurisdictions 6 6 5 6 0 1 6

Other jurisdictions 20 20 18 20 5 13 21

Total number of respondents 31 31 27 30 5 17 33

Results by IAIS Region

Asia and Oceania 6 6 6 7 1 6 7

Central, Eastern Europe and Transcaucasia 6 7 7 7 1 2 7

Latin America 2 2 2 2 0 1 2

Middle East and North Africa 0 0 0 0 0 0 0

North America 2 1 1 0 0 0 2

Offshore and Caribbean Islands 8 8 6 7 1 4 8

Sub‐Sahara Africa 4 4 3 4 2 3 4

Western Europe 3 3 2 3 0 1 3

Total number of respondents 31 31 27 30 5 17 33

Page 37

5. To what extent does YOUR AUTHORITY use FHSIs in supervising each of the following types of insurance activities?

(1) Used regularly and consistently (2) Used often but not always consistently (3) Used sometimes (4) Seldom if ever used (5) Not applicable, because YOUR AUTHORITY has no responsibility for this type of insurance activity

Weights for index: 10 7 4 1 omit

(1) (2) (3) (4) (5) Total Index Rank

a. Conventional insurance 28 5 0 0 0 33 9.5 1

b. Microinsurance 9 1 1 3 19 33 7.4 2

c. Takaful 2 1 0 2 28 33 5.8 5

d. Microtakaful 2 0 0 1 30 33 7.0 3

e. Offshore insurance 6 4 2 3 18 33 6.6 4

Total and Average Index 47 11 3 9 95 8.1

6. To what extent does YOUR AUTHORITY use FHSIs in each of the following aspects of regulation or supervision?

(1) Used regularly and consistently (2) Used often but not always consistently (3) Used sometimes (4) Seldom if ever used (5) Not applicable, because YOUR AUTHORITY has no responsibility for this aspect of regulation or

supervision

Weights for index: 10 7 4 1 omit

(1) (2) (3) (4) (5) Total Index Rank

a. Micro‐prudential 28 3 0 1 1 33 9.4 1

b. Macro‐prudential 22 7 2 2 0 33 8.5 2

c. Market conduct 15 6 5 4 3 33 7.2 4

d. Financial integrity 19 7 1 4 2 33 8.0 3

e. Competition policy 2 1 2 4 24 33 4.3 6

f. Market development 9 5 5 3 11 33 6.7 5

Total and Average Index 95 29 15 18 41 7.8

Page 38

7. To what extent does YOUR AUTHORITY have the following tools and guidance to support the use of FHSIs?

(1) Available for all or most FHSIs, where relevant (2) Available for many FHSIs (3) Available for few if any FHSIs (4) Not available

Weights for index: 10 7 2 0

(1) (2) (3) (4) Total Index Rank

a. A structured database of the data needed to calculate FHSIs 12 14 2 5 33 6.7 2

b. A supervisory reporting system that automatically calculates FHSIs for each insurer

9 12 4 8 33 5.5 6

c. Standardized spreadsheets that are used to calculate FHSIs 10 14 3 6 33 6.2 3

d. Instructions for calculating FHSIs, including the data and methodology

11 12 5 5 33 6.2 3

e. A supervisory reporting system or standardized spreadsheets that facilitate the analysis of trends in the FHSIs for each insurer

12 16 1 4 33 7.1 1

f. A supervisory reporting system or standardized spreadsheets that facilitate the comparison of FHSIs for peer groups of insurers

8 14 5 6 33 5.7 5

g. Supervisory benchmarks for specific FHSIs 8 9 11 5 33 5.0 7

h. Written guidance on the interpretation of specific FHSIs 6 13 6 8 33 4.9 8

i. Written guidance on the use of FHSIs, in general 7 11 7 8 33 4.9 8

j. Training on the interpretation of specific FHSIs 5 12 9 7 33 4.6 10

k. Training on the use of FHSIs, in general 6 10 9 8 33 4.5 11

Total and Average Index 94 137 62 70 5.6

8. To what extent does YOUR AUTHORITY communicate with insurers regarding your use of FHSIs?

(1) Communicated for all or most FHSIs, where relevant (2) Communicated for many FHSIs (3) Communicated for a few FHSIs (4) Not communicated

Weights for index: 10 7 2 0

(1) (2) (3) (4) Total Index Rank

a. General explanation of how FHSIs are used 5 9 6 13 33 3.8 1

b. Descriptions of the FHSIs used 4 6 7 16 33 2.9 3

c. Supervisory benchmarks for specific FHSIs 2 5 8 18 33 2.2 5

d. Results of calculations of specific FHSIs for the insurer 3 9 13 8 33 3.6 2

e. Aggregate results of calculations of specific FHSIs for peer groups of insurers or the industry

3 7 4 19 33 2.6 4

Total and Average Index 17 36 38 74 3.0

Page 39

9. To what extent does YOUR AUTHORITY communicate with the general public regarding your use of FHSIs?

(1) Communicated for all or most FHSIs, where relevant (2) Communicated for many FHSIs (3) Communicated for a few FHSIs (4) Not communicated

Weights for index: 10 7 2 0

(1) (2) (3) (4) Total Index Rank

a. General explanation of how FHSIs are used 4 5 4 20 33 2.5 1

b. Descriptions of the FHSIs used 4 4 5 20 33 2.4 2

c. Supervisory benchmarks for specific FHSIs 2 3 5 23 33 1.5 4

d. Results of calculations of specific FHSIs for specific insurers, with the insurers identified

1 3 4 25 33 1.2 5

e. Results of calculations of specific FHSIs for specific insurers, but with the insurers not identified

0 2 5 26 33 0.7 6

f. Aggregate results of calculations of specific FHSIs for peer groups of insurers or the industry

2 6 9 16 33 2.4 2

Total and Average Index 13 23 32 130 1.8

10. Which of the following categories are included in the risk‐assessment framework used by YOUR AUTHORITY?

(1) Included in the framework (2) A similar category is included (explain) (3) Not included (4) Not applicable, because YOUR AUTHORITY has no risk‐assessment framework

Weights for index: 10 7 0 omit

(1) (2) (3) (4) Total Index Rank

a. Capital 28 4 0 1 33 9.6 2

b. Assets 27 5 0 1 33 9.5 3

c. Reinsurance 26 4 2 1 33 9.0 7

d. Actuarial 28 2 2 1 33 9.2 4

e. Management 26 4 2 1 33 9.0 7

f. Earnings 31 1 0 1 33 9.9 1

g. Liquidity 28 2 2 1 33 9.2 4

h. Subsidiaries (or Group or Related Parties) 19 5 7 2 33 7.3 15

i. Insurance 27 3 2 1 33 9.1 6

j. Credit 26 3 3 1 33 8.8 9

k. Market 26 2 4 1 33 8.6 11

l. Operational 24 4 4 1 33 8.4 12

m. Legal and Regulatory 25 3 3 2 33 8.7 10

n. Conduct 15 6 9 3 33 6.4 17

o. Reputation 17 5 8 3 33 6.8 16

p. Concentration 22 4 4 3 33 8.3 13

q. Environmental (sectoral and macro risks) 14 6 9 4 33 6.3 18

r. Strategic 21 2 7 3 33 7.5 14

s. Other categories (explain) 6 1 13 13 33 3.4 19

Total and Average Index 436 66 81 44 8.3

Page 40

11. In total, how many FHSIs does YOUR AUTHORITY use? (When responding, count each FHSI only once, even if some FHSIs relate to more than one risk‐assessment category.)

(1) 100 or more (2) 75 to 99 (3) 50 to 74 (4) 25 to 49 (5) 15 to 24 (6) 10 to 14 (7) 9 or fewer

Weights for index:22 110 85 60 35 20 12 5

(1) (2) (3) (4) (5) (6) (7) Total Index Rank

Results by Nature of Jurisdiction

FSB jurisdictions 1 0 2 2 1 0 0 6 53.3 2

Other OECD jurisdictions 3 0 1 2 0 0 0 6 76.7 1

Other jurisdictions 0 1 5 10 4 0 1 21 39.0 3

Total number of respondents 4 1 8 14 5 0 1 33 48.5

Results by IAIS Region

Asia and Oceania 0 0 2 2 2 0 1 7 33.6 7

Central, Eastern Europe and Transcaucasia

1 0 0 6 0 0 0 7 45.7 4

Latin America 0 0 0 2 0 0 0 2 35.0 6

Middle East and North Africa 0 0 0 0 0 0 0 0 N/A N/A

North America 1 0 0 1 0 0 0 2 72.5 2

Offshore and Caribbean Islands 0 1 2 2 3 0 0 8 41.9 5

Sub‐Sahara Africa 0 0 3 1 0 0 0 4 53.8 3

Western Europe 2 0 1 0 0 0 0 3 93.3 1

Total number of respondents 4 1 8 14 5 0 1 33 48.5

22 The weights are not necessarily the midpoints of the respective ranges. An assumption was made that the average within a range might be lower than the midpoint.

Page 41

12. How many FHSIs does YOUR AUTHORITY use when assessing each of the categories in your risk‐assessment framework? (When responding, count all FHSIs mapped to the risk‐assessment category, even if they have also been mapped other categories.)

(1) 10 or more FHSIs (2) 5 to 9 FHSIs (3) 1 to 4 FHSIs (4) No FHSIs are used when assessing this category (5) Not applicable, because this category is not used

Weights for index:23 12 7 3 0 omit

(1) (2) (3) (4) (5) Total Index Rank

a. Capital 7 13 13 0 0 33 6.5 3

b. Assets 7 13 13 0 0 33 6.5 3

c. Reinsurance 1 8 22 0 2 33 4.3 9

d. Actuarial 6 8 17 1 1 33 5.6 5

e. Management 5 9 11 7 1 33 4.9 6

f. Earnings 13 14 4 2 0 33 8.1 1

g. Liquidity 1 6 23 1 2 33 4.0 12

h. Subsidiaries (or Group or Related Parties)

2 1 14 9 7 33 2.8 15

i. Insurance 13 4 13 1 2 33 7.2 2

j. Credit 3 10 14 3 3 33 4.9 6

k. Market 4 6 16 6 1 33 4.3 9

l. Operational 3 9 12 6 3 33 4.5 8

m. Legal and Regulatory 0 4 11 14 4 33 2.1 17

n. Conduct 1 2 7 15 8 33 1.9 19

o. Reputation 0 4 7 13 9 33 2.0 18

p. Concentration 5 2 20 4 2 33 4.3 9

q. Environmental (sectoral and macro risks)

1 6 11 7 8 33 3.5 14

r. Strategic 6 1 8 11 7 33 4.0 12

s. Other categories (explain) 1 1 1 6 21 30 2.4 16

Total and Average Index 79 121 237 106 81 4.6

23 The weights are not necessarily the midpoints of the respective ranges. An assumption was made that the average in the “1 to 4” category might be higher than the midpoint, because the use of only a single indicator for a category is not often seen in practice.

Page 42

13. To what extent has YOUR AUTHORITY progressed in revising the FHSIs it uses to take account of anticipated changes in financial reporting and regulatory requirements related to IFRS 9 and IFRS 17?

(1) Revisions were needed and have already been made (2) No revisions were considered necessary (3) Revisions will be needed, but have not yet been made (4) The need for revisions has not yet been considered (5) Not applicable, because this category is not used (6) Not applicable, because IFRS is not used by insurers in YOUR JURISDICTION

Weights for index: 10 9 5 0 omit omit

(1) (2) (3) (4) (5) (6) Total Index Rank

a. Capital 3 2 12 12 0 0 29 3.7 2

b. Assets 3 3 11 12 0 0 29 3.9 1

c. Reinsurance 3 2 9 15 0 0 29 3.2 11

d. Actuarial 4 1 10 14 0 0 29 3.4 6

e. Management 1 3 10 15 0 0 29 3.0 12

f. Earnings 3 2 10 14 0 0 29 3.4 6

g. Liquidity 2 2 11 13 1 0 29 3.3 9

h. Subsidiaries (or Group or Related Parties)

1 0 12 12 3 0 28 2.8 16

i. Insurance 4 1 11 12 0 0 28 3.7 2

j. Credit 1 3 11 12 1 0 28 3.4 6

k. Market 1 2 10 14 0 0 27 2.9 13

l. Operational 1 4 9 12 1 0 27 3.5 4

m. Legal and Regulatory 2 3 9 14 0 0 28 3.3 9

n. Conduct 2 3 8 12 3 0 28 3.5 4

o. Reputation 1 2 9 14 2 0 28 2.8 16

p. Concentration 1 2 10 15 0 0 28 2.8 16

q. Environmental (sectoral and macro risks)

1 1 10 12 4 0 28 2.9 13

r. Strategic 1 2 10 14 1 0 28 2.9 13

s. Other categories (explain) 0 0 3 5 9 0 17 1.9 19

Total and Average Index 35 38 185 243 25 0 3.2

Page 43

14. In addition to the resources and tools currently available (for example, the Core Curriculum modules), to what extent would the following initiatives that might be considered by the IMF, the WBG, or others be useful to YOUR AUTHORITY in enhancing your use of FHSIs?

(1) Very useful (2) Useful (3) Somewhat useful (4) Not useful

Weights for index: 10 7 4 0

(1) (2) (3) (4) Total Index Rank

a. A paper that summarizes the results of this survey and briefly discusses the use of FHSIs

15 11 5 0 31 8.0 8

b. A list of FHSIs used by insurance supervisors 23 7 2 0 32 9.0 1

c. A mapping of FHSIs to risk‐assessment categories 20 8 4 0 32 8.5 4

d. Guidance on the calculation of specific FHSIs 21 8 2 1 32 8.6 3

e. Guidance on the interpretation of specific FHSIs 21 9 1 1 32 8.7 2

f. A process for obtaining ongoing input on the above items and making periodic updates

14 10 7 1 32 7.4 12

g. An accessible database of the FHSIs used by individual supervisors and the supervisory benchmarks they have established

20 6 4 2 32 8.1 7

h. An Excel workbook that can be used to calculate FHSIs and make comparisons among insurers

22 5 0 5 32 8.0 8

i. Development for trainers 19 5 5 3 32 7.7 10

j. Regional or international training seminars 21 5 4 2 32 8.2 5