designing a results driven digital strategy: customers and corporations’ digital journeys are just...

TRANSCRIPT

Customers and Corporations’ Digital Journeys are just Beginning…

Designing a Results Driven Digital Strategy

By Fabio Mittelstaedt

June 2017

Define Digital Vision

Change Mobile App’s Wireframe

Build Cross-

-Functional

Team Improve

Digital

Customer

Experience

Do Proof

of Concept

with Customers

Designing a Results Driven Digital Strategy

Point of View - 2

Designing a Results Driven Digital Strategy

T he common question in the market regard-ing digital strategy is if leading corporations and multinationals re-

ally need or “must have it”. However, disruptive emerging business models using digital first approach are a very clear message for the C-Level that it is not hype, it is rapidly becoming the new normal.

Remember all the innovative tech-nologies of the last two decades that seemed fragmented and more appealing for punctual process improvements and gains in isolated areas like sales, marketing, supply chain etc? CRM, BI, Big Data, Analyt-ics, Mobility, Cloud, AI, Robotics, Telematics, VR, AR are only a few examples.

It happens that the new generation driving open innovation, collabora-tive models and a fascinating new wave of startups, FinTech, InsurTech and other niches in different indus-tries, could finally connect the dots using all these available technologies in a simple, integrated and seamless way.

And how they did it? Simply reimagining or reinventing Customer’s Experiences with a holistic view of what is called to-day “Customer Journey”, mean-ing all the phases of a customer interaction with a brand, product or service in order to fulfill his needs, from the moment zero of motivation passing through re-search and comparative analysis of options in multiple channels or touchpoints (digital and physi-cal), purchasing and relationship and customer service post-sales.

Initially, disruptors attacked one strong pain point or customer

need and tried to build the ideal customer experience, the customer’s dream realized without the con-straints that large corporations and regulators tend to ignore or label as not feasible. Do an international money transfer with a few clicks paying a small fee, starting a mobile video call with a specialist doctor as a on-the-shelf service without having a health plan or previous appoint-ment, buying an auto insurance via mobile in less than two minutes that charge you for miles driven and give you back up to 50% of premium if you don’t have any incident are a proof that new game changing digital models are highly desired and ap-preciated by customers, and came to stay.

Disintermediation, unbundling products with digital challengers and simplifying customer experience are topics that most financial institutions learned to respect, developing simi-lar solutions, partnerships, accelerat-ing startups (with or without venture capital) and even acquiring players. Others are building their own Digital Innovation Labs.

Bank of America recently announced the coming launch of “erica”, a new Digital Assistant combining Artificial Intelligence, predictive analytics and cognitive messaging capabilities via voice command or text to make pay-ments, check balances and savings, pay bills, transfer money etc. Their bet is that this mobile platform, one of the first aiming to attend the retail banking focusing on mass and affluent segments, instead of wealth customers and investment capital markets, can establish a risk-taking innovation built by a huge market leader, not a FinTech competitor.

This shows that Digital Strategy is already a Top Priority in the strategic planning agenda in some industries and that executive committees already understood that it is much more than pure technology and systems, even if a company is not a tech native and deliver services or any type of goods or B2B, digital can be the catalyst to transform and join business strategy, operations and technology in one single shared vi-sion across the company.

Digital Customer Experience Maturity

Once that Digital Strategy became extremely relevant in everyday busi-ness, Banks and Retailers overall are struggling to achieve Customer

“Digital can be the catalyst to transform and join business strategy, operations and technology in one single shared vision across the company.”

“Unlike a mathematical formula that gives you certainty about the final result, Digital CX is totally about uncertainty and constant change, because it is anchored on customer’s mind, how it interacts with new technologies, products and services.”

“Unlike a mathematical formula that gives you certainty about the final result, Digital CX is totally about uncertainty and constant change, because it is anchored on customer’s mind, how it interacts with new technologies, products and services.”

Point of View - 3

Experience Maturity, recognizing that the real treasury behind it is in understanding customer’s dreams, ambitions, aspirations and daily habits and attitudes. And that all off it is transparent in the path to digital journeys, in the traces that they leave in the web, mobile apps, social networks and in the sometimes under explored in-house consumer data warehouse.

You just need a structured analytics engine and a cross-functional team of motivated strategists, UX design thinkers and Departmental Experts to reveal and envision what should be the enhanced digital customer ex-perience for all segments, from baby boomers to millennials and genera-tion Z. And for sure, do not forget the most important thing here, talk directly to your customers, despite of all your survey investments with the best research institutes.

But creating, measuring and compar-ing Digital CX Maturity is not like any regular business challenge. Corpora-tions, Consulting Firms and Research Institutes are trying to rationalize it through different methodolo-gies. The only issue is that unlike a mathematical formula that gives you certainty about the final result, Digital CX is totally about uncertainty and constant change, because it is anchored on customer’s mind, how it interacts with new technologies, products and services.

The relevance about analyzing Digital CX Maturity from different perspec-tives: Customer’s Eyes, Competi-tion Benchmarking and New Digital Comers is that it can be an effective method to quickly test and learn and bring practical insights for improve-ment in specific processes and cus-tomer journeys that your team didn’t notice before.

Some time ago, Fjord developed the “Love Index”, which aims to understand and identify how much people’s experience define the affin-ity with a product, service, company or brand and provide actionable insights for improving the design of digital CX by mapping how much

an experience is Fun, Relevant, Engaging, Social and Helpful.

Forrester delivered the “Cus-tomer Experience Index” (CX Index™), willing to help Digital Chief Officers and CX profes-sionals understand the ups and downs of CX quality over time in 18 industries. Consumers are asked how each brand or prod-uct is selected based on three dimensions: enjoyable, easy and meets needs.

Despite methodologies, the real question is: “what digital really means for your business strategy and for every single customer that your company is trying to capture or retain?”

Generic strategies or broad customer segments do not work anymore, we are living the new era of real time personalization.

Personalization is the new name of the game

Digital experts are using new expres-sions to try to distinct the natural “Digital Customer” from the more resistant segments that slowly ex-periment the benefits of life digitali-zation, from how I use my cash, how I manage macro decisions in my life and how I make the small everyday choices, what has been called micro-moments and how they can create natural personalization and customer intelligence to the daily experiences that really matters. It means that if I am searching for a new car in the web and if I just checked my avail-able credit in my mobile banking app, I can receive an instant pre-ap-proved auto loan offer for that BMW that I was dreaming off in a dealer near to my location, all in real time.

And that your food requests through voice command for AI ChatBots like Siri, Alexa, Jarvis or Google Assistant can be crossed with data from wear-ables like Jawbone body media and fitness trackers and next time you try to order a meal online, you will receive a personalized diet advice about the type of food, proteins and

calories that you should eat in order to have a balance in your nutrition and health.

But what this kind of thing has to do with digital banking and finan-cial services? Everything. Your daily habits in life and how you manage your money are fully connected. And digital is the link that is building the bridges for a more integrated experience. Ideally in a near future I shouldn’t need thousand different apps for shopping, payment, learn-ing, travelling etc. The one-stop-shop is not a new concept, but only now we have available all the digital, analytics, mobility, omnichannel and artificial intelligence capabilities that will make it possible.

Your mobile Banking platform becomes an intelligent and per-sonalized retail marketplace for all customer needs, integrating several providers with secure APIs in the Banking as a Service platform. This complete Mobile Banking Mall would be frictionless, meaning that there is no data duplication, it is pre-populated in the background every time you want to buy a new service from another financial services partner sharing this open platform, generating revenues for incumbent Banks and FinTech Startups. A Digital Win-Win.

Point of View - 4

Designing a Results Driven Digital Strategy

Big data collects data from your financial history, social networks, last purchased products, preferred channels, demographic data, fam-ily household profile, geolocation and can use predictive analytics to model your personal context in the customer life cycle. Thus, Artificial In-telligence just built your persona and now can instantly send you personal-ized offers.

That could go from an investment advice coming from a robot advisor to an insurance product to a cheaper air flight ticket for a frequent travel that you do monthly to visit your parents in another state.

Moven’s Mobile banking app, is a very well know digital case, but not everybody knows that besides all basic personal financial management features (very similar to Simple and GuiaBolso) depending on the analy-sis of your spending behavior, Moven can automatically increase your savings volume sending you simple personalized recommendations via a specialized debit card linked with your app.

Case: BBVA, Personalized Mobile Videos

Personalization in Digital banking does not mean the apps features only, but using digital and customer data analytics to generate higher adoption and contribution margin on products online. BBVA and Allianz are using Uses Personalized Mobile Video to Drive Pensions and Digital Banking with Idomoo. They created a Future Self video from the perspec-tive of their future retired customer. The videos are further customized to each individual viewer, showing them the specific amount that they currently contribute, how much they can save if they increase the average contribution, their rates and end of term savings they could see based on their current financial status and activity what would be the monthly pension income after retirement. In the same digital platform, just swap-ping a bar in the mobile bank app,

customers could adjust their pension plans for best future cost vs benefit. In the case of BBVA, 40% of target customers (selected automatically via analytics campaign engine) saw the personalized video, resulting in a 78% increase in retirement savings.

Regarding mobile banking personal-ization, there are many aspects that do not add too much value for cus-tomer engagement like design and photo personalization or basic things like using geoloca-tion to find the nearest ATM. What is really interesting about personalization is when a bank use three things in a smart way: intelligent data analytics person-alization, real time automated personalized advice and artificial intelligence managing it all and interacting with the customer in a less robot style and more hu-man appeal.

Case: Tangerine Bank, Personal Finance Summary

For the first aspect Tangerine

Bank (previously ING Direct, a Retail Bank from Toronto, Canada and part of the Scotia Bank group) has a very nice way to show customer’s financial data summary in one small screen, showing what you have, what you owe, interest earned and fees saved since you became a client and the rest is the typical informa-tion that most mobile banks have.

Point of View - 5

Case: Finie, AI Digital Powered Banking with Natural Language

And there is a mobile innovation that intends to join the three points mentioned before: Finie (meaning Financial Genie), which is an AI App for Digital Bank Account. Created by professors at the University of Michigan who assembled a small start-up named Clinc, Finie is a voice-powered AI platform based on deep neural networks, an innovative way to interact with a banking account using natural language queries (as opposed to a very limited set of rule-based commands as most rob advisors in the market do). This is a game changing AI technology, more advanced than Siri and Alexa for instance.

And what else is different about Finie comparing to other AI platforms?

Finie is a Banking expert! Its remark-able natural language processing engine has specifically trained its ap-plications with a deeper knowledge of the financial and banking industry. Finie is like a fast machine learning, expanding knowledge and improving results with every interaction.

Instead of being limited to robotic boring commands such as, “Show me my credit card balance”, you can freely talk to Finie in your own words asking for instance: “Do I have enough money to travel to Caribe next holiday with my family for one week, spending around US$ 8,000?” or “Did I spend more on groceries this month than last?”

Finie is integrated within a banks’ mobile banking application, acting as “a voice-activated intelligent person-al assistant” that is able to answer financial questions unique to each individual user, offering personalized spending advice.

This new level of digital banking per-sonalization may take digital custom-er experience to a totally different quality and satisfaction high stan-dard. A few Banks in Canada like ATB Financial and Royal Bank of Canada

are trying it, but with the more basic AI platforms. ATB launched the digi-tal assistant “Pepper” which pretty much a customer service robot, since it does not make transactions. Royal Bank of Canada Canada’s is offer-ing e-transfers for its customers via voice-command with Siri, Apple’s virtual assistant.

Case: L’Oréal, Digital Beauty Personalization integrated with m-Commerce

Going outside financial services world, there is a digital personaliza-tion innovation in beauty prod-ucts retail that I particularly like because the idea is simple, the customer need was latent but nobody could implement a so user friendly and intelligent digital platform before: the Make Up Genius from L’Oréal, launched by 2015. It is an augmented reality app which allows customers to virtually try on 4,500 of the cosmetic brand’s catalogue of products using their smartphone or tablet.

The Makeup Genius applies bronzer, eyeshadow, lip gloss, and eyeliner in real time using facial recognition technology, enabling the virtual make up to stay in place as you move your face. The technology captures 64 facial data points and 100 differ-ent facial expressions to accurately place the make up. The app scans your face, and then allows you to try out different products or entire make up looks.

Depending on the context and event: going to a marriage during the day or a night dinner or party, the app can recommend and apply instantly dif-ferent looks in your virtual face. You can then save your selfie, share it on social media, and the app automati-cally select the products needed for your make up, add to your mobile

basket, you pay directly through the app and receive it at home. It means “really” a seamless and integrated digital customer experience.

And one lesson learned for seasoned executives should be: pay attention

to digital best cases from different industries that do not belong to your comfort zone. You need to be creative and open mind when talking about digital innovation and try to adapt the best of each idea and join the pieces in a new original innova-tion that will work for you market context and type of customer.

The new digital salesforce models launched by products industry are a good example that could be adapted to rationalize costs with huge struc-tures of sales representatives in the financial services industry.

Digital Experience is omnichannel, but Mobile will Prevail

When defining a digital strategy, omnichannel is much more than an operational decision. Ideally a Bank should put available 100% of all func-tionalities, products and services in digital channels, while keeping them connected with traditional channels, allowing customers to go forward and back through channels without struggling and have to restart the

Point of View - 6

Designing a Results Driven Digital Strategy

process when switching touchpoints. Citi Card’s Digital Lead, Alice Milligan, recently declared that made around 85% of services available on mobile app so far, and will hopefully move quickly to 100%.

But the main point here is that we can’t choose what channels cus-tomers will use in their non-linear journey. Depending on the indus-try, digital channels can handle the full experience from research and purchase to aftersales service or play the typical role of decision support and the purchase will be done on physical channels, like the car buying experience. A research from Google and Luth says that even before going to a car dealer, customers explore from 6 to 14 brands online, do on average 139 google searches, see 14 youtube videos with technical details about the desired car in sites like cars.com and more. 71% of these online activities are performed on mobile. In addition to that more than 60% of customers use the digital car configurator tool and more than 40% simulate auto finance online. Only after all this digital research, or in between, customer visit car dealers in order to do the test drive, negoti-ate and close the deal.

This seems complex, right? As a mat-ter of fact, native digital customers already do it intuitively. That is why mapping and improving a customer journey is something that you can’t do only with common sense inside

your company.

Coming back to Banks, it is easy to notice that they offer multiple chan-nels, from branch to social network, call center, chat, video call, e-mail,

apps, ATM and others. Definitely it is a very rare situation when you really start experiencing true omnichannel integration.

Take as an example what every bank is trying to do now: implement a fully digital new checking account opening experience. After FinTech players like mBank, IGaranti and others showed the treasure map, most leading banks put this available with steps and technologies that are becoming a standard like digital sign-in, face recognition, photo capture and OCR documents, fingerprint login etc. And most of these apps are really great.

The reality is, if you have any issue post-digital account opening and contact another channel, typically there is no context transfer and customer’s interactions detail his-tory with data transposed from one platform to another. That is why

“Your daily habits in life and how you manage your money are fully connected. Digital is the link that is building the bridges for a more integrated experience.

Your mobile Banking becomes an intelligent and personalized retail marketplace for all customer needs, integrating several providers with secure APIs in the Banking as a Service platform. A complete Mobile Banking Mall.”

Point of View - 7

backoffice and customer service are the most complicated Achilles’ heel when integrating omnichannel and delivering new end-to-end digital banking journeys.

The good news is that there is a lot of digital technology available to improve this experience and more flexible business models disrupt-ing the market, taking advantage of business inefficiencies of established market leaders.

This is the case of Lemonade, a New York-based insurer for homeowners and renters. It looks like a peer-to-peer insurer, this is because they disintermediated the market by eliminating brokers from the process, what made the InsurTech community call them the “Uber of Insurance”. They use a artificial intelligence bot named Maya, that interacts with cus-tomers through chat, with the value proposition to get insured through mobile in 90 seconds and in case of claims, pay customer on average in 3 minutes. No stress, when you start a claim in the app, you just answer a few questions and record a video

telling the details about the incident and a few minutes later the money is in your account.

An article published by March 2017 at The Economist web site, described a real customer claim and told the science behind it: “Late last year a customer called Brandon claimed for a stolen coat. He answered a few questions on the app and recorded a report on his iPhone. Three sec-onds later his claim was paid—a world record, says Lemonade. In those three seconds “A.I. Jim”, the firm’s claims bot, reviewed the claim, cross-checked it with the policy, ran 18 anti-fraud algorithms, approved it, sent payment instructions to the bank and informed Brandon.”

Another good case of linking mobile app and other channels seamless in the customer journey is cardless ATM withdrawal, not thinking only about the convenience when you forget your debit card at home, but also aiming a less risk and quick operation without identity theft situation. The discussion here is not if ATMs will die or survive, it is about

giving real functional technological examples of omnichannel, consider-ing that this topic sometimes is too much theoretical.

In the last months, many Banks and Credit Card Companies announced cardless ATM withdrawal, but one of the first to develop it was Akbank, from Turkey, using beacons (tiny Bluetooth 4.0-based devices).

Wells Fargo is going one step ahead of competition in this area. Their in-novation team is close to launch the mobile capability to use Apple Pay to withdraw cash from ATMs without a card (5,000 NFC enabled ATMs out of its 13,000 total network). After you click on Apple Pay app you will just need to enter your card PIN to finish the transaction. Simple like that.

In all these examples, there is something in common, even in a omnichannel scenario, digital mobile is always taking the lead as main platform. It is absolutely clear and natural for any Digital Strategist that omnichannel integration is a key element of customer success’ path.

“Mobile-First Approach and Apps are the first thought when teams start a project to digitize customer journeys. By 2016 more than 90% of time spent on mobile was in apps and only 10% on browser, and daily web consumption per user is getting almost equal in the mobile and laptop.”

“Mobile-First Approach and Apps are the first thought when teams start a project to digitize customer journeys. By 2016 more than 90% of time spent on mobile was in apps and only 10% on browser, and daily web consumption per user is getting almost equal in the mobile and laptop.”

Point of View - 8

Designing a Results Driven Digital Strategy

There are significant signals that digital channels are gaining preference and that the internet access through Desktop and Laptop is losing share for the Mobile platform. That is why Mobile-First Approach and Apps are the first thought when teams start a project to digitize customer journeys. By 2016 more than 90% of time spent on mobile was in apps and only 10% on browser, according to Flurry and comScore.

Daily web consumption per user is getting almost equal in the mobile and laptop in emerging markets like China (3h03m mobile, 3h29m laptop) and Brazil (4h48m mobile, 5h36m laptop), while in mature markets web access via laptop continues much higher. France shows only 1h32 minutes of daily web access on mobile and the triple in laptop (3h57m). Surprisingly, mobile web access in USA is close to half of the volume in Brazil, with 2h37 minutes.

By 2017, mobile banking may reach incredible 60% of usage in Asia Pacific and 54% in Latin America. Europe and North America, despite the fact that they are regions with strong mobile banking technology R&D investments, will show an average range from 42% to 45% of mobile usage. One possible explanation is that both continents have older aging inhabitants, more resistant to innovative technologies. Millenials share of population are much larger in emerging markets for instance, and all surveys shows that they are the early adopters and promoters of new digital banking technologies, along with generation X.

44

45

42

54

60

32

38

43

43

52

Africa/MiddleEast

NorthAmerica

Europe

LatinAmerica

AsiaPacific

MobileBankingBasicServicesUsageandIntentionByRegion

2016Actual 2017Forecast

Source:TheNielsenMobileShopping,Banking&PaymentsSurvey2016,analysisFabioMittelstaedt.

MobileBankingAdoptionGrowthwillbehigherinAsiaPacificandLatinAmericaas atrendfornextyears,stronglypushedbyemergingmarketslikeIndia,Singapore,China,Brazil,ArgentinaandColombia.

2.37

1.32

3.03

4.484.48

3.57 3.29

5.36

USA France China Brazil

Webconsumption peruserviaMobileandLaptop(HoursperDay)

Mobile Laptop

Source: Statista Digital Market Outlook, April 2017, analysis Fabio Mittelstaedt.

Point of View - 9

52% of millennials will be doing payments through mobile banking by 2017, with 47% from generation X. These are really aggressive numbers, considering that many innovative payment apps from FinTech Startups and even incumbents, still have security issues to be solved in the mobile architecture, which is relatively new comparing to other systems like web and branch front office solutions. Here some of the key motivations is the offer of more user friendly and simple apps and lower fees. Above all, younger digital users like to experiment and have no attachments or loyalty with financial services providers. They just use it because they like the experience and there is no bureau-cracy in new Digital “FinTech like” models.

The current usage and future intention to use mobile apps for financial services and personal finance management is a trend that is not going to decline anytime like in a product lifetime curve that people learn in marketing and admin-istration courses, because it is changing people lifestyle and making it easier and more dynamic. This trend is becom-ing a solid reality that is being materialized (or saying better digitized) in the last 8 or 10 years. Proof of that is the incredible number of finance mobile apps available at Apple Store by March 2017: 49,060 apps, and with the poten-tial power to consolidate apps from other industries and segments as cash and daily life needs converge naturally, as you need to buy and pay for goods and services. We will show in this point of view one of the best examples of this digital converge with “Ant Financial / Alipay’s Digital Strategy Case”.

Building a Strategic Digital Customer Experience Road-map

The first step to build your Digital CX Roadmap is to forget about technol-ogy. The temptation to use the most advanced and appealing digital and mobile technologies shouldn’t be part of your Experience Strategy upfront. Super Sex Digital Features like Location Based Services, Aug-mented Reality, Artificial Intelligence Avatar, Smart Robo Advisors for In-vestments, Gamification… All of this can used, if they make sense for the storyline of your customer and for the value proposition that your busi-

ness strategy is aiming to achieve and design.

Start from the basics, talk to your customer, apply user experience research techniques, do the typi-cal design thinking workshops with a multidisciplinary team, and test hypothesis again with your customer, even before prototype and minimum viable product phase.

Try to understand the non-linear path of CX in the omnichannel environment and do exercises to simplify the experience and create shortcuts in the value chain, using digital innovations, existing and new ones to be developed. That is when

big data analytics show its power, because the customer won’t tell you everything, but you can consolidate behaviors of common segments and prioritize some personas that make sense for your business and your ap-plication design.

And don’t underestimate backoffice processes. Sometimes digitizing a process may be more important to a lean experience than a sophisticated personal finance management dash-board, and can make the difference in critical moments as purchase and customer service, when trying to fix a pain point in the customer journey.

Put a limit in the complexity of your

Point of View - 10

Designing a Results Driven Digital Strategy

UX strategy, a few products, a few clicks and a killer design that facili-tate customer’s interaction making intuitive screens and buttons, just like Steve Jobs envisioned when inspired the programmers to create the Mac interface, yes old school of design still works a lot…

But the real test of success is when the empathy with the customer is achieved and in your next focus group you listen testimonials like: “it seems that they guessed what I wanted, easy and fast, without push-ing products that I don’t want”.

At this point of the CX Strategic Blueprint, the CMO, CDO and CIO are probably satisfied with the prelimi-nary results of the initial sprints of your agile development. And then the CFO asks about the projected ROI, Revenues Generation, Estimated Customer Acquisition Curve in the first year of operation, Costs Amor-tization, Potential Churn and other important quantitative and financial elements to sustain the business case, that is the value creation part, for the customer and for the busi-ness, it must be a Digital Win-Win in

the Customer Experience and Bal-ance Sheet.

The “Digital Strategy Roadmap” explain in a simple way the basic steps to build and implement your strategy in a high-level vision. This model is complemented next in this point of view with the “Digital Strat-egy Framework”, that brings further detail organized by structural points that should be evaluated when de-signing your digital strategy.

The Roadmap steps are based on the most advanced techniques of open innovation, design thinking, agile,

scrum and traditional strategy and management consulting methodolo-gies.

The steps are intuitive and not nec-essarily sequential: understanding the digital market context, the com-petitive scenario (including disrup-tive startups and FinTech), technol-ogy trends etc makes total sense when starting any digital project.

But your digital team may choose to start from the step 2, which is map-ping digital customer needs and pain points and trying to transform them

in strong hypothesis for value cre-ation opportunities and innovative business models, that is step 3.

Or you could jump from customer assessment directly to the design thinking customer journey vision-ing (step 4) and only after that think about revenue models and how your digital idea has the potential to be-come the next US$ 1 billion unicorn.

The Digital Transformation Strategy (step 5) is a broad step, because here you need to have more than the stra-tegic vision at this point: a structured business case, sales projections and

all the operational, technological, human and cultural changes needed to make the transformation happen, and before that, engage the board and the all company with the digital vision.

The agile implementation (step 6), based on quick sprints and test & learn is self-explanatory. Using open innovation working model, APIs, intense collaboration of cross-func-tional teams to create a continuous digital innovation cycle.

And finally, the Agile Project Man-

Point of View - 11

agement is a gradual evolutionary concept, totally based on lessons learned in large digital transforma-tion projects. For instance, in a lead-ing Bank, I have spent a significant time first preparing the field, what I call Digital Building Blocks, in order to make the organization ready to develop the most advanced digital innovation ideas. In some customer journeys it means basic things like digitizing processes, going paper-less, integrating digital channels with branches’ front end and other actions.

Some organizations like Deutsche Bank are many steps ahead of that, and already established their own in-novation lab and made several waves of internal transformation to make their digital strategy a real success.

A Digital Roadmap requires flexibility and agility. You need to constantly learn and adapt your digital strategy, and be bold in your digital thinking, allowing mistakes and understand-ing that quickly test, try and improve can lead you to a huge success very soon, if you go fast. So it is not about finishing a great Digital Strategy Roadmap and in the next day starting

developing a revolutionary mobile app that will change your business. Even small startups commonly don’t do it this way. Imagine big corpora-tions that have their cash cow and star products that generate great profits for decades. It is always a phased approach, going forward and back again, and educating employees with a different digital mentality, like if everyday you challenged yourself to create a new business or replace your own product portfolio.

Digital Transformation is about Reinventing the Business

Typically, most large incumbent Banks launch fancy new mobile apps, but ignore completely the toughest customer pain points, that would re-quire a strong change management effort in the governance model, com-pany culture, core banking and CRM systems, internal processes, paper elimination, digitalization and auto-mation, backoffice workflow rules, new training for branches, salesforce reorganization and even revision of

contact center outsourcing contracts.

It means that digital transformation can’t be a cosmetic change in the design of your digital channels and investing heavily in digital marketing and mass advertising to convince your customer that you are the best digital bank.

Must be a new attitude, culture and rethink strategically the business model, value proposition, revenues model, core costs, segmentation, product portfolio and the new profile of your needed digital talent work-force. Smart Bots don’t implement digital roadmaps.

FinTech and InsurTech Startups do not have a millionaire cash flow and a broad customer base and the terabytes of big data about customer behavior as leading financial institu-tions possess, but they bring two lost assets in large corporations: simplicity and true customer centricity.

“A Digital Roadmap requires flexibility and agility. You need to constantly learn and adapt your digital strategy, and be bold in your digital thinking, allowing mistakes and understanding that quickly test, try and improve can lead you to a huge success very soon, if you go fast.”

Designing a Results Driven Digital Strategy

Point of View - 12

Results & Insights: Continu-ously Improving Experience

If in your digital strategy you had to choose one first priority KPI, certain-ly it should be something new and broad like “digital customer journey success”, meaning that along all the journey and steps interacting with a brand, how the typical most stress-ful pain points simply disappear in the design of your enhanced digital experience, and as a result of that you do not need to call the contact center, do not need to go to a branch and do not need to email your bank-ing account manager to handle the top list of issues affecting customer satisfaction in the sales and after-sales stages of the relationship with a financial service provider.

Example of Best Digital Mobile Ex-perience: Blocking a Credit or Debit Card

One of the most common examples is the urgent need to block a credit or debit card, when minutes can make a difference when you lost your card or when it has been stolen. Imagine you are travelling for vaca-tions with the family and your card was theft. Great probability that you

do not have a laptop close to your hands, but almost 100% chance that your smartphone is with you. This way, the mobile app experience should be the focus of any Bank for this critical task. Santander Mobile App, for instance, offer one of the most simple and intuitive experienc-es to block a card: you just login with fingerprint, click on cards and then on block card. Three clicks with no screen scroll, no unnecessary infor-mation, data fields are all pre-popu-

lated in the background and the call to action buttons and icons are clear and easy to find in the screen. The same is not true for other Competi-tor Banks offering the same function-ality in their mobile app. The main issues noticed in these other banks are multiple screens, buttons and process is not clear in the application and when you finally find the right place after trial and error, a lot of information is requested like details explaining why you are blocking your card, security questions, if you wish or not to receive another card etc.

“Mobile Banking Sell? Or it is just about a better experience?”

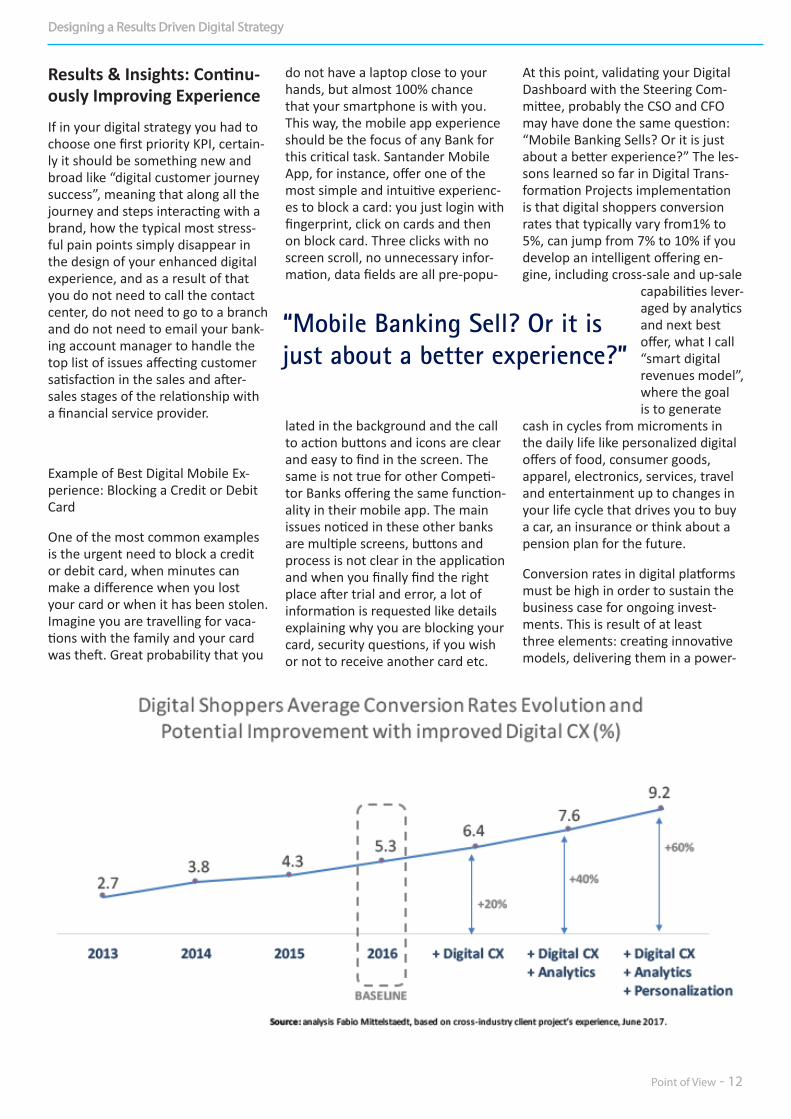

At this point, validating your Digital Dashboard with the Steering Com-mittee, probably the CSO and CFO may have done the same question: “Mobile Banking Sells? Or it is just about a better experience?” The les-sons learned so far in Digital Trans-formation Projects implementation is that digital shoppers conversion rates that typically vary from1% to 5%, can jump from 7% to 10% if you develop an intelligent offering en-gine, including cross-sale and up-sale

capabilities lever-aged by analytics and next best offer, what I call “smart digital revenues model”, where the goal is to generate

cash in cycles from microments in the daily life like personalized digital offers of food, consumer goods, apparel, electronics, services, travel and entertainment up to changes in your life cycle that drives you to buy a car, an insurance or think about a pension plan for the future.

Conversion rates in digital platforms must be high in order to sustain the business case for ongoing invest-ments. This is result of at least three elements: creating innovative models, delivering them in a power-

Point of View - 13

ful digital & omnichannel experi-ence and bringing to the customer’s awareness an attractive value propo-sition, that goes beyond pure pricing discounts, establishing a positive relationship with the brand.

Understanding the new all day con-nected on multiple devices reality is something that is not responsibility of design thinkers and marketers only, but of all executives, because they allow you to enter in customer’s digital life through the front door. Thinner light Ultrabooks, the latest iPhone or Samsung Galaxy or a re-versible tablet/notebook. The device doesn’t matter so much. Screens of all these devices are getting bigger, since user research experience shows that customers need to see high quality product images, videos, in-tuitive screens and easy simulations and secure environ-ment to enter pay-ment information. If your mobile app delivers all these features, conversion rates can increase by 20% or higher. If you add analytics intelligence, per-sonal and context based interactions, it can move up to 60% or more, tak-ing your conversion rate from 3%-5% range to 7%-10%.

This is valid for large corporations going digital. Sure, for startups and FinTech the metrics are different: number of app downloads, people using the app and making transac-tions on the digital platform. Other KPI’s like average value spent online continue the same. This is the output of innovation, not the input or mo-tivators that can explain why some digital players become unicorns and others not. The level of disruption in the digital business model, easi-ness of digital customer experience, lower prices and fees due to disin-termediation and lower overhead, are some common factors, but can’t summarize all the key digital success elements.

Case: Ant Financial / Alipay’s Digital Strategy

The largest FinTech Unicorn by 2017 is Ant Financial (controlled by Ali-baba Executive Chairman Jack Ma), valued at US$ 60 Billion, owner of Alipay, which manages almost 60% of all China’s payments through digital channels and that have many other integrated digital ventures like the mobile bank called “MyBank”.

And coming back to original ques-tion: Why Ant Financial / Alipay is the most succesfull unicorn in the world?

The answer is not just because they are based in China, where is located

the largest population in the world: 1.4 Billion (but sure it helped them to get 450 million users, being in-clusive both for the average citizen, unbanked, and for the small and medium enterprises). It is because Ant Financial / Alipay is extremely customer centric in the heart of their digital strategy and financial services strategy.

Their vision and ambition was to build an entire digital ecosystem to cover all Chinese Customer’s Finan-cial Needs, and also all other every-day habits where you need cash or a robust digital wallet, as some define in the market. Or a “Lifestyle app”, as Alipay define itself. And the position-ing slogan makes sense, because they are much more than a Digital Wallet.

If you look at Apple iTunes’Alipay page at https://itunes.apple.com/us/app/alipay-makes-life-easy/id333206289?mt=8, it is impressive

to see the list features that the Digi-tal Platform deliver to users:

1. Send/Receive money from your peers;

2. Transfer money to friends or split the bill at your favorite restaurant;

3. Card free payment at millions of merchants;

4. Top up your mobile phone and pay your utility bills;

5. Place and track orders in Taobao and TMall;

6. Order food from local restaurants or book a taxi;

7. Manage your money with wealth management products;

8. Free off-site cross-bank transfer / credit card repayment and loans;

9. Scan & Pay – Scan & use the QR code to pay at your local stores;

10. Book Air/Rail/Movie Tickets, at ease;

11. Enjoy hundreds of discounts and promotions from various merchants;

12. Group account facility to manage expenses within family and friends circle;

13. Donate/Participate in walkathons along with your friends.

Designing a Results Driven Digital Strategy

Point of View - 14

For instance, an incumbent Bank wants to deliver a new Mobile Wal-let for Millenials or Digital Checking Account for Mass Segment. In order to deliver a full digital experience in the Customer’s standpoint on the opening account / onboarding journey, many changes must hap-pen, from eliminating paper con-tracts and physical signatures, to automating backoffice routines and doing customer data analytics in real time. In the meantime, the bank will probably need to review the role, profile (and eventually the sizing) of salesforce and front office advisors at branch and call center.

In the end of the day, to obtain the best cost reduction while reengi-neering processes and creating new digital experience models outside for customers and workflows inside for employees, it is unavoidable to combine advanced digital technology and analytics with structural changes

Despite all these exciting features, Alipay’s Design and Digital Customer Experience is highly friendly, easy to use and effective for all types of cus-tomers. Probably they have the most impressive social payments network globally. And also, the most practical digital payments solution for un-banked and low-income users.

Another integration that Alipay did and is amazing is between their giant e-Commerce platform composed of Alibaba and Marketplace Mobile App Taobao, facilitating the shopping experience. Taobao’s social media features in some aspects are bringing innovation lessons for the estab-lished leader Facebook. Keep people connected and buying is the dream of every retailer in the world. But despite their aggressive online sales strategy, Alipay didn’t forget the physical shopping experience: you can use the QR Code Reader feature in Alipay’s app and instantly read a code and pay a product, enabling a frictionless customer journey.

The range of Alipay allows Ant Financial to capture an incredible amount of customer data. This data is not static as a trophy in a data center. They really have a Big Data Strategy and can generate actionable insights with a very specific goal, engage customers online, creating a phenomenon that digital experts are labeling as “social media commerce”. And how it works?

They analyze customer’s online buy-ing patterns, which means millions of data points and automatically invite users, during their navigation online in the web and mobile platforms, to join custom interest groups, which from special algorithms, suggest higher affinity topics according to each individual’s profile, much more than a segmentation.

While exchanging views and opin-ions about products and brands, this social experience makes shopping more frequent and engaging. The re-sult is fantastic leading to an average 7 visits/day/user to Taobao’s mobile commerce app. The average ticket per unique user/year is greater than US$ 1,200.

And in order to enable the health and credibility of its financial ser-vices and eCommerce apps growth, Ant Financial developed too the first credit agency in China, named “Sesame Credit”, which an intel-ligent automated credit-scoring that leverages big data (online and offline), purchasing history, social media presence and digital customer behavior to build a strong analytics machine that provides the group the capability to make credit available to Chinese Consumers and Small Entrepreneurs.

Higher Revenues and Customer Satis-faction are undoubtedly the most de-sired targets of digital strategy proj-ects. On the other hand, we should not forget cost reduction, with an important parameter: reduce costs while increasing satisfaction and revenues, what implies in profound changes in corporations’ businesses and processes.

“Digital Strategy is not only about digitizing processes and customer journeys, it is about creating a more lean and efficient operating model, that reflects a new culture of doing business.”

Point of View - 15

in the organization and high levels of automation. The combined ben-efits, considering direct and indirect levers, can be extremely attractive, going from 5% to 35% reduction, depending on your strategic plan and execution.

So, Digital Strategy is not only about digitizing processes and customer journeys, it is about creating a more lean and efficient operating model, that reflects a new culture of doing business.

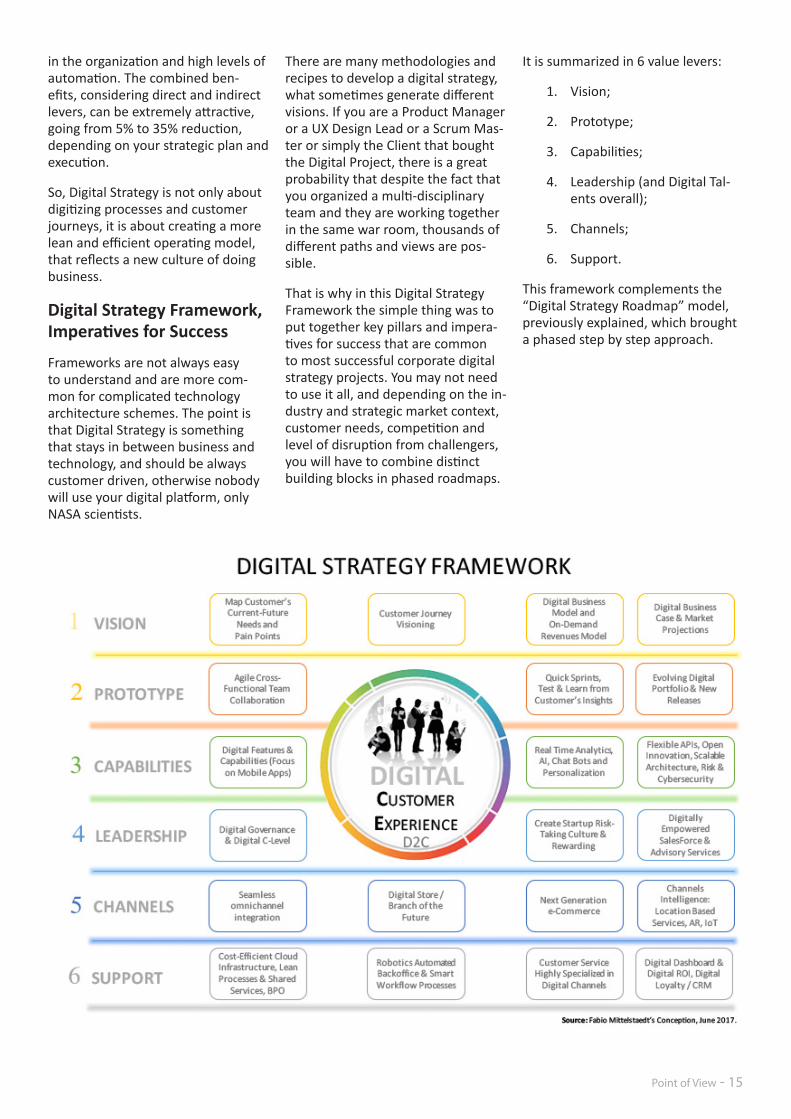

Digital Strategy Framework, Imperatives for Success

Frameworks are not always easy to understand and are more com-mon for complicated technology architecture schemes. The point is that Digital Strategy is something that stays in between business and technology, and should be always customer driven, otherwise nobody will use your digital platform, only NASA scientists.

There are many methodologies and recipes to develop a digital strategy, what sometimes generate different visions. If you are a Product Manager or a UX Design Lead or a Scrum Mas-ter or simply the Client that bought the Digital Project, there is a great probability that despite the fact that you organized a multi-disciplinary team and they are working together in the same war room, thousands of different paths and views are pos-sible.

That is why in this Digital Strategy Framework the simple thing was to put together key pillars and impera-tives for success that are common to most successful corporate digital strategy projects. You may not need to use it all, and depending on the in-dustry and strategic market context, customer needs, competition and level of disruption from challengers, you will have to combine distinct building blocks in phased roadmaps.

It is summarized in 6 value levers:

1. Vision;

2. Prototype;

3. Capabilities;

4. Leadership (and Digital Tal-ents overall);

5. Channels;

6. Support.

This framework complements the “Digital Strategy Roadmap” model, previously explained, which brought a phased step by step approach.

Designing a Results Driven Digital Strategy

Point of View - 16

Some final thoughts with imperatives for success about Designing a Results Driven Digital Strategy:

1. Start your Digital Strategy always with the Customer perspective, be open to hear and change from a product feature and pain point up to the entire business model;

2. Use Big Data and predictive analytics to anticipate and envision future customer needs and create real inno-vation that is a combination of rich insights;

3. Don’t rush to go after the most complex digital innova-tion like embedding AI on your mobile app, first make sure that you are delivering a consistent Digital Customer Journey;

4. Agile methodologies aside, do not forget to make the time investment to gener-ate your Digital Strategy Roadmap and engage all the organization with the same

vision, otherwise your plan may be too tactical and with a narrow vision;

5. More important than tech-nology, think first how you will attract the best digital talent and transform all your workforce and C-Level on Digital First Thinkers and Executers;

6. In the beginning of your Digital Strategy implementa-tion, make sure that you will simultaneously do the quick wins to gain the organiza-tion’s confidence and at same time deliver digital cost reduction to internally fund your big Digital Innova-tion Bets. It means that your organization will be more efficient, with a lean oper-ating model, high levels of automation and new digital revenues streams sustaining business growth;

7. Put a big target around digital personalization of-fering through mobile and

omnichannel. The Digital winners will be who use ana-lytics and real time context to make personalized offers and specialized advisory to Customers and also B2B Clients;

8. Do not underestimate the level of effort and energy that you will have to put in change management for the backoffice and customer service support areas, most new digital business models do not rise or do not get cus-tomer’s adoption because the digital experience in only good in the appearance, but many service and logistics dissatisfaction points con-tinue to exist;

9. Integration is the hardest technological challenge that you will face to execute with mastery your digital strategy. If you are a leading incumbent, this is 100% true. Integrate new digital chan-nels with traditional chan-nels, integrate core banking

Digital

Imperatives

for Success

Point of View - 17

systems, integrate different data marts to enable digital analytics and many other aspects. Before investing a lot of time and money on this odyssey of integration, consider the possibility to rethink from scratch your old IT Architecture (that works pretty well but is not a competitive advantage for the future) into a completely new “Digital Architecture”. Define graduals cycles of change tied to benefits for the business through digital innovation. And meanwhile, while the architecture transformation is happening maybe you will need assem-ble temporary digital units for new businesses, other-wise you could stop innova-tion process. An example of that are incumbents launch-ing digital neobanks with independent structure and cost centers. Sure, without a minimum integration with core systems nothing works, but some technological flex-ibility is crucial to make not just your IT department, but the entire company an agile machine;

10. Find the right equilibrium between risk management, cybersecurity and simple and seamless customer experi-ence of your digital platform. If you increase too much the security measures on mobile apps, you may reduce fraud risk, but make the experi-ence hard for users. Fast sign-in through biometrics, voice or face recognition are a good example. Even today the mobile app of some incumbent banks requires several steps, tokens and passwords to access your mobile banking app. For every transaction, the same concept may apply, with two or three clicks maximum and no screen scroll, a customer should finish an action on

mobile. That is why it is so important that experts in cybersecurity, compliance, regulations and legal par-ticipate in digital cross-func-tional teams in all key digital innovation projects and agile teams;

11. Pricing and Fees are a very important issue of your Digital Business Model. Many incumbents launched Digital Mobile Banking apps with exactly the same pric-ing structure from standard business model and physical channels. The point is not about doing a price war with startups and FinTech, that have lower structural costs, but using all the key ele-ments of digital like analytics and artificial intelligence to increase your share of wal-let through more effective digital cross-sale, up-sale and new models like digital subscription, on demand services and others, enabling you to have a digital pricing intelligence and flexibility;

12. Measure the success of Digi-tal Customer Journeys and how they will bring higher profits to the stakeholders is highly difficulty, turn your digital ROI measure into a top priority, automate KPI’s analysis in real time building a robust Digital Dashboard;

13. Define a hybrid digital orga-nization, with a dream team of cross-functional experts and executives fully dedi-cated to digital transforma-tion and a matrix structure with focal points for digital in all areas of the organization, unifying common goals and objectives. For those more aggressive on digital invest-ment, you may think about establishing your own inno-vation lab or design center;

14. Make innovation and bench-marking an obsession in your

company, you need to be aggressively agile mapping innovation in the market, adapting and creating your own digital innovation, with a dynamic go to market lead time, keeping you one step ahead of competition. And don’t forget to look at Digital Innovation lessons cross-industry. There are always some aspects that you can incorporate in your own in-novation model;

15. Foster open innovation and increase your value network constantly. It is not just opening APIs or sharing cus-tomer data like some bank-ing regulations in Europe are defining, but letting business partners participate actively in the digital innovation cycles and sprints. Remem-ber, this includes your cus-tomers providing you direct feedback, not just through research institutes;

16. Develop new analytics risk score models for your digital innovation models in bank-ing, retail and any other rev-enues based business online. In some markets, selective FinTech players are testing more broad risk models that include not just stan-dard quantitative data from credit institutions, includ-ing secondary demographic data, online behavior, social media habits and network, purchase history etc. The Chinese FinTech Unicorn Ant Financial is one Company doing this more complete and flexible scoring analysis with the ultimate goal to be more inclusive for target segments like the unbanked and millennials starting their careers. On demand services that do not require signing annual contracts with loy-alty restriction are another solution that Startups are bringing to change the risk

Designing a Results Driven Digital Strategy

Point of View - 18

score paradigm. A good example is the Oscar Digital Health Platform, which allow customers that do not have a health plan to buy separated services like a mobile video call with a specialized doctor without previous appoint-ment, you just pay online with your credit or pre-paid card or other tools like pay-pal, and you get the immedi-ate service. You can later pay for a complementary face to face appointment with the doctor if needed and do the required health exams, using the online appointment tool;

17. CRM and analytics are not optional items in your Digital Strategy. For instance, a Mo-bile Banking app without any analytics intelligence is just one more channel. Analytics gives you the capability to recognize individual cus-tomer’s profile and needs, do personalized offers in the right moment for the right model and pricing, provide services in a more intimate way, knowing the history and personality of your cus-tomer. Analytics together with CRM will make your digital platform a live organ-ism that learn everyday like a machine learning system, not something static, and will bring effectiveness for your customer’s acquisition, cross-sell & up-sell, reten-tion and loyalty strategies. And finally, big data real time streaming analytics (not just predictive analytics) is a key component to make this CRM + Analytics equation work with perfection, giving you the ability to anticipate customer needs and act right when opportunities happen, instead of analysis based on past behaviors, which are good to minimize customer churn, but not so adequate for the speed of the digital customer;

18. Complementing the point above you need to have a super expert digital market-ing team in order to make your digital strategy effec-tive. This team will not do the marketing advertising in the old way, putting all your eggs in TV Media. FinTech players were naturally forced to become masters in digital marketing, because they did not have budget for mass ad-vertising. And they got mil-lions of downloads and new digital customers this way. So, your new digital mar-keting team need to build and use proficiently capa-bilities like SEO, online Lead Management, Social Media Marketing, Personalized Push Mobile Offers, Location Based Services, Campaign analytics and others, with a focus on marketing ROI. Do not delegate all this change and responsibilities for your Advertising or Digital Agency, you need to have an in-house digital marketing governance body;

19. Your Company should have a Venture Capital and M&A mindset. Digital innovation is spread in the market, in the Small & Medium Enterprises, early stage Startups, that competitor that you never paid too much attention, smart ideas from emerging markets and more. Keep an strategic eye on all Digital players and rapidly make decisions about investing, acquiring, accelerating, in-cubating or just establishing strategic alliances strength-ening your ecosystem. This can speed up your rhythm of digital innovation and future growth of your business.

Point of View - 19

Author: Fabio Mittelstaedt

Innovation and Digital Strategist

June 2017