depreciation recapture §1245 and §1250media.straffordpub.com › products ›...

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE PROGRAM

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

IRC Section 67(g) and Form 1041 Trust Deduction Rules:

Fiduciary Fees, State and Local Taxes, and Other MIDs

THURSDAY, JUNE 4, 2020, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality FOR LIVE PROGRAM ONLY

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

June 4, 2020

IRC Section 67(g) and Form 1041 Trust Deduction Rules

Jeremiah W. (Jere) Doyle, IV, Senior Vice President

Bank of New York Mellon

Jacqueline Patterson, Partner

Buchanan & Patterson

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

BNY Mellon Wealth Management

New Section 67(g) – Form 1041 Trust

Deduction Rules Post TCJA of 2017

Jeremiah W. Doyle IV, Esq.

Senior Vice President

BNY Mellon Wealth

Management

Boston, MA

June, 2020

Jacqueline A. Patterson, Esq.

Buchanan & Patterson, LLP

1000 Wilshire Blvd.

Suite 570

Los Angeles, CA 90017

June, 2020

BNY Mellon Wealth Management

Agenda

• History and background

• Changes made by the TCJA of 2017 – Section 67(g) and disallowance of “miscellaneous itemized deductions” for years 2018 to 2025

• Must look at other Code sections to interpret Section 67(g)

• Analysis of Sections 641(b), 67(a), 62, 63(d), 67(b), 67(e) and the final regulations under 67(e), and 642(h) to determine what are “miscellaneous itemized deductions”

• What’s deductible in years 2018-2025

• What’s not deductible in years 2018-2025

6

BNY Mellon Wealth Management

Agenda (cont.)

• Excess deductions – Post-TCJA developments: Notice 2018-61 and May 7, 2020 proposed regulations

• Reduced AMT exposure

• Surprising result – simple trust can have taxable income

7

BNY Mellon Wealth Management

Introduction

◼ New Section 67(g) disallows “miscellaneous itemized deductions” for

years 2018-2025

◼ This affects estates and trusts as well as individuals

◼ We must determine what estate and trust expenses are “miscellaneous

itemized deductions”

◼ To do so, we must review Sections 641(b), 67(a), 62, 63(d), 67(b), 67(e)

and 67(h) of the Internal Revenue Code

◼ In addition, we must be familiar with the final Section 67(e) regulations

◼ The results may be surprising

8

BNY Mellon Wealth Management

Section 67(a) – General Rule

◼ Miscellaneous itemized deductions are allowable only to the extent

they exceed 2% of the estate or trust’s adjusted gross income.

9

BNY Mellon Wealth Management

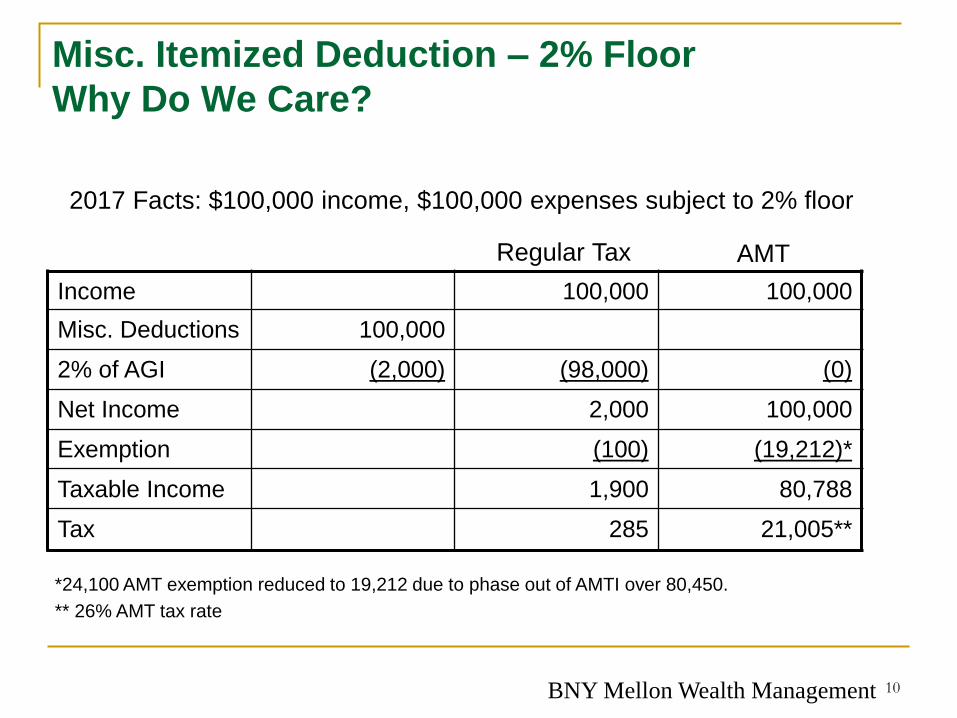

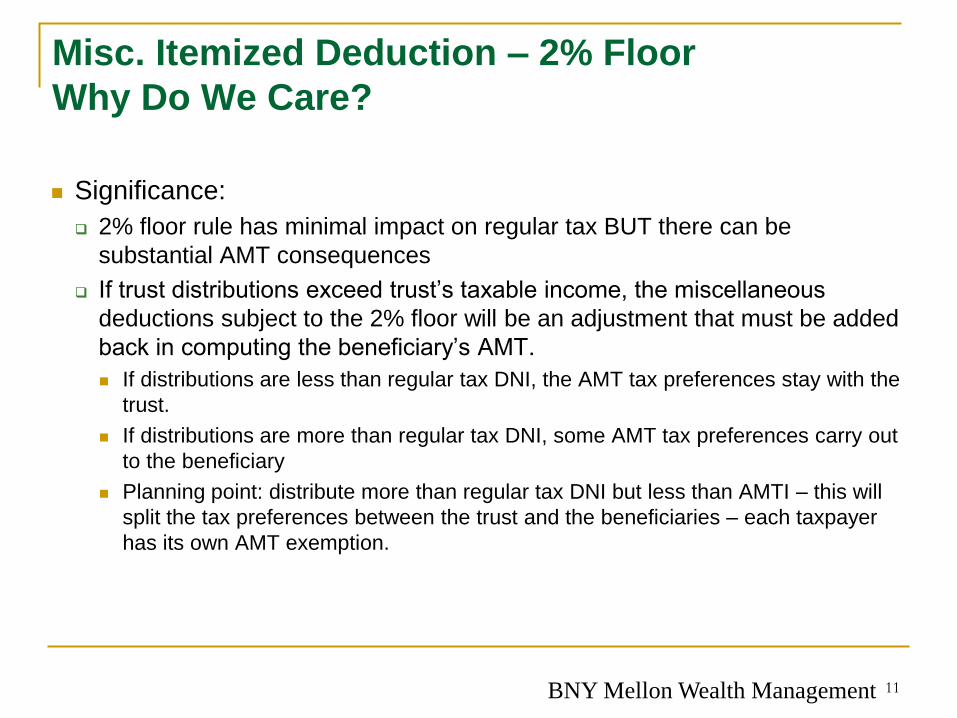

Misc. Itemized Deduction – 2% Floor

Why Do We Care?

Income 100,000 100,000

Misc. Deductions 100,000

2% of AGI (2,000) (98,000) (0)

Net Income 2,000 100,000

Exemption (100) (19,212)*

Taxable Income 1,900 80,788

Tax 285 21,005**

2017 Facts: $100,000 income, $100,000 expenses subject to 2% floor

Regular Tax AMT

*24,100 AMT exemption reduced to 19,212 due to phase out of AMTI over 80,450.

** 26% AMT tax rate

10

BNY Mellon Wealth Management

Misc. Itemized Deduction – 2% Floor

Why Do We Care?

◼ Significance:

❑ 2% floor rule has minimal impact on regular tax BUT there can be

substantial AMT consequences

❑ If trust distributions exceed trust’s taxable income, the miscellaneous

deductions subject to the 2% floor will be an adjustment that must be added

back in computing the beneficiary’s AMT.

◼ If distributions are less than regular tax DNI, the AMT tax preferences stay with the

trust.

◼ If distributions are more than regular tax DNI, some AMT tax preferences carry out

to the beneficiary

◼ Planning point: distribute more than regular tax DNI but less than AMTI – this will

split the tax preferences between the trust and the beneficiaries – each taxpayer

has its own AMT exemption.

11

BNY Mellon Wealth Management

Section 67(g) – Suspension for Taxable Years

2018 Through 2025

(g) Notwithstanding subsection (a), no miscellaneous itemized

deduction shall be allowed for any taxable year beginning after

December 31, 2017, and before January 1, 2026.

12

BNY Mellon Wealth Management

New Section 67(g) - Translated

◼ New Section 67(g) disallows “miscellaneous itemized deductions” for

years 2018-2025

◼ This affects estates and trusts as well as individuals

13

BNY Mellon Wealth Management

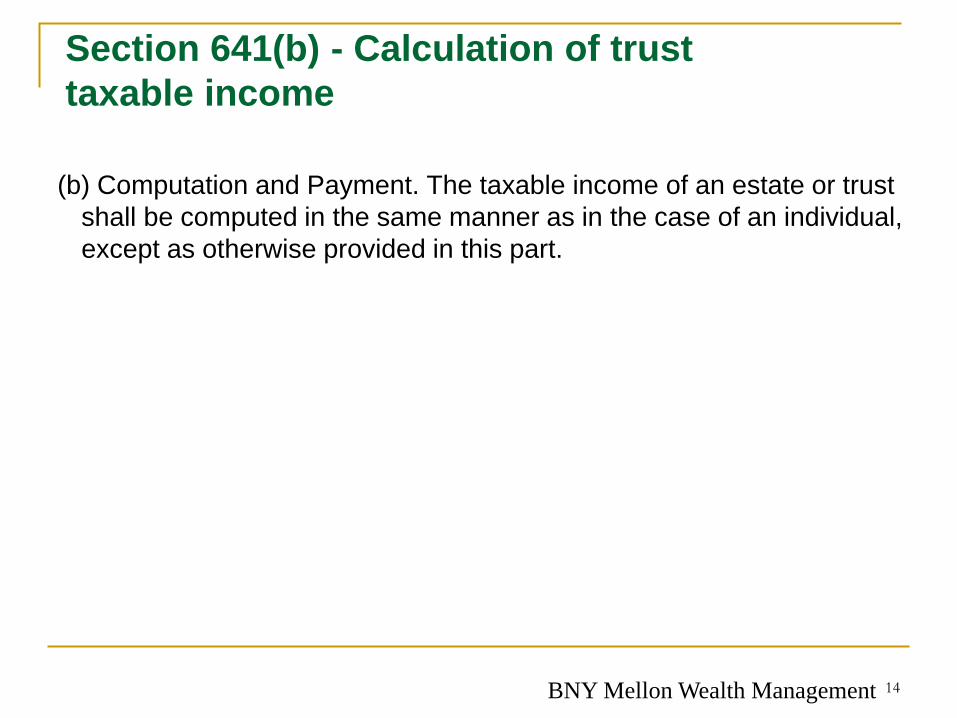

Section 641(b) - Calculation of trust

taxable income

(b) Computation and Payment. The taxable income of an estate or trust

shall be computed in the same manner as in the case of an individual,

except as otherwise provided in this part.

14

BNY Mellon Wealth Management

Section 641(b) - Translated

◼ The same rules that apply to individuals in computing taxable income

also apply to computing the taxable income of an estate or trust

unless stated otherwise.

15

BNY Mellon Wealth Management

Calculation of trust taxable income

Gross income

Less: Adjustments to gross income (§62)

Less: Section 67(e) deductions unique to a trust

Adjusted Gross Income

Less: Section 67(b) deductions (Not Misc. Itemized Deductions)

Less: Miscellaneous itemized deductions subject to 2% floor

Less: Income distribution deduction

Less: Exemption

Taxable income

Green = fully deductible

Red = not deductible 2018 -2025

16

BNY Mellon Wealth Management

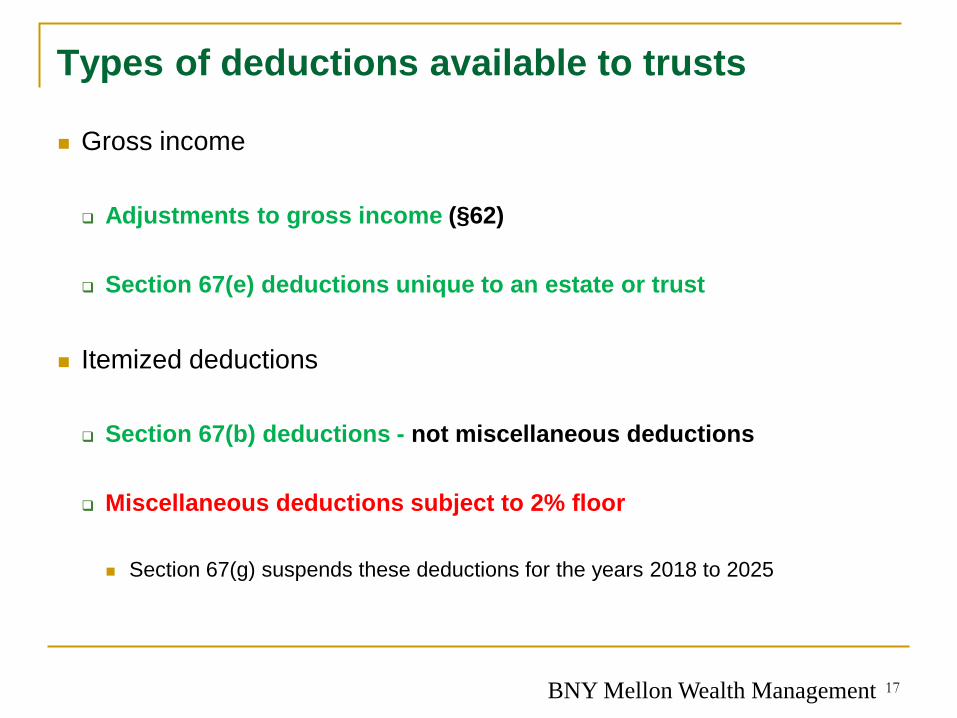

Types of deductions available to trusts

◼ Gross income

❑ Adjustments to gross income (§62)

❑ Section 67(e) deductions unique to an estate or trust

◼ Itemized deductions

❑ Section 67(b) deductions - not miscellaneous deductions

❑ Miscellaneous deductions subject to 2% floor

◼ Section 67(g) suspends these deductions for the years 2018 to 2025

17

BNY Mellon Wealth Management

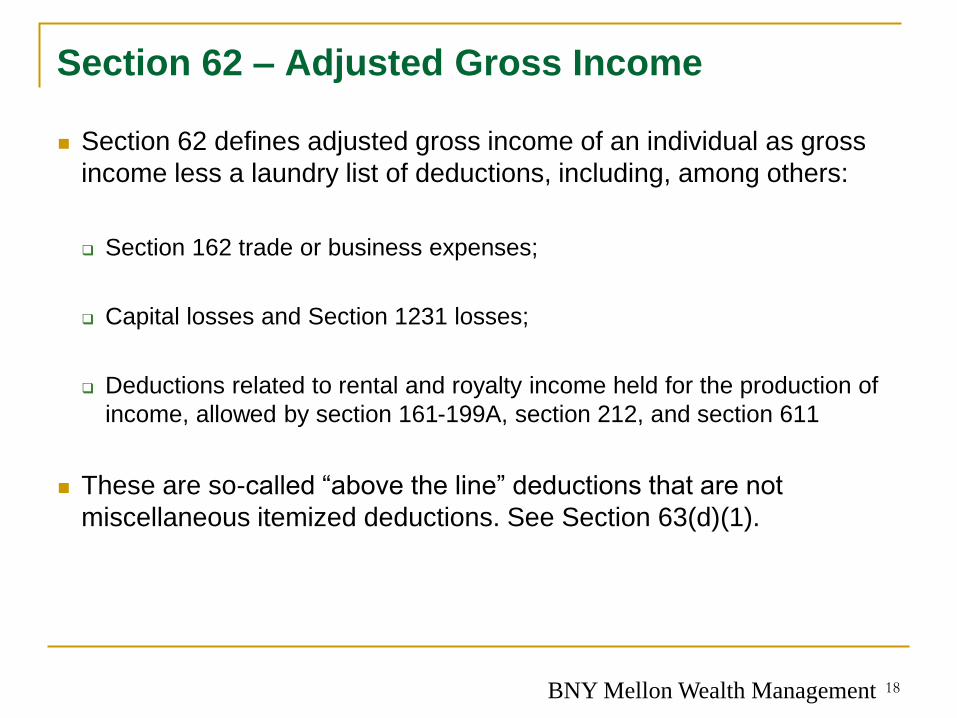

Section 62 – Adjusted Gross Income

◼ Section 62 defines adjusted gross income of an individual as gross

income less a laundry list of deductions, including, among others:

❑ Section 162 trade or business expenses;

❑ Capital losses and Section 1231 losses;

❑ Deductions related to rental and royalty income held for the production of

income, allowed by section 161-199A, section 212, and section 611

◼ These are so-called “above the line” deductions that are not

miscellaneous itemized deductions. See Section 63(d)(1).

18

BNY Mellon Wealth Management

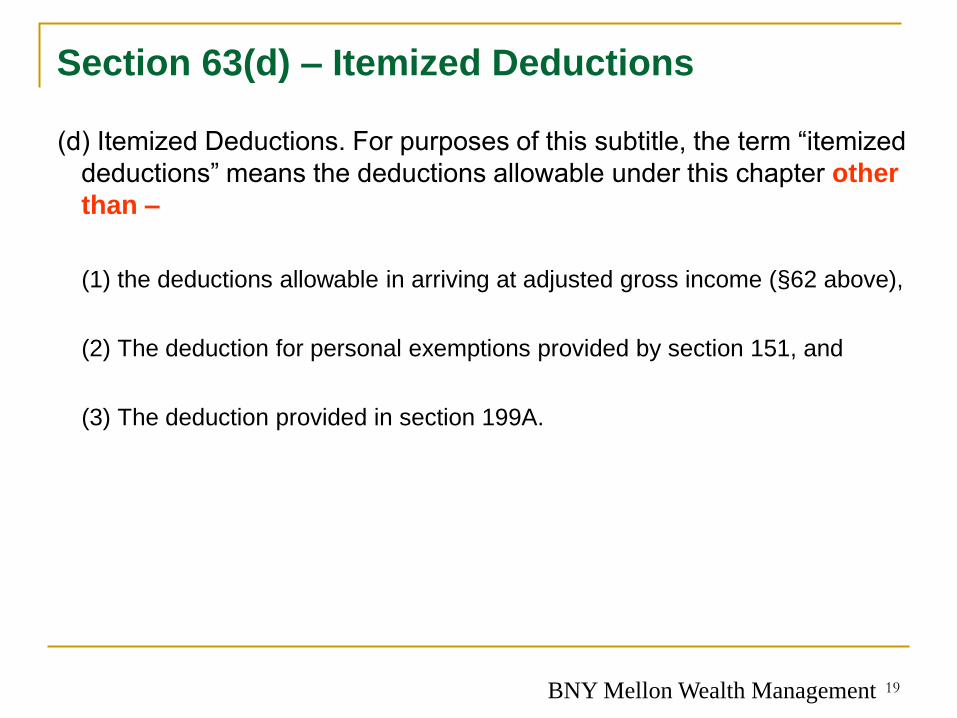

Section 63(d) – Itemized Deductions

(d) Itemized Deductions. For purposes of this subtitle, the term “itemized

deductions” means the deductions allowable under this chapter other

than –

(1) the deductions allowable in arriving at adjusted gross income (§62 above),

(2) The deduction for personal exemptions provided by section 151, and

(3) The deduction provided in section 199A.

19

BNY Mellon Wealth Management

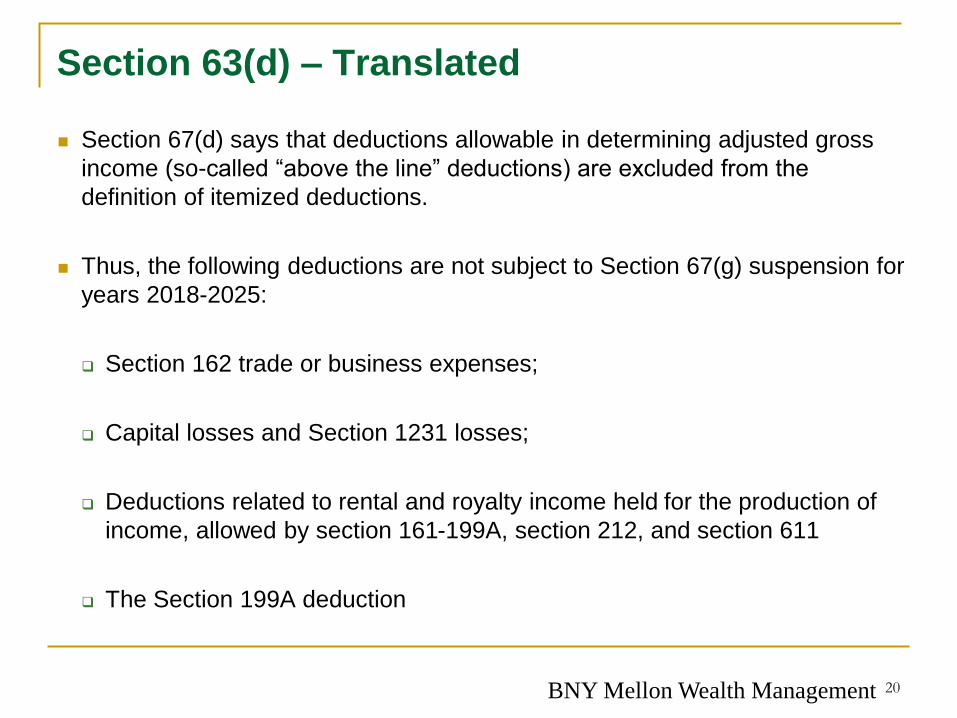

Section 63(d) – Translated

◼ Section 67(d) says that deductions allowable in determining adjusted gross

income (so-called “above the line” deductions) are excluded from the

definition of itemized deductions.

◼ Thus, the following deductions are not subject to Section 67(g) suspension for

years 2018-2025:

❑ Section 162 trade or business expenses;

❑ Capital losses and Section 1231 losses;

❑ Deductions related to rental and royalty income held for the production of

income, allowed by section 161-199A, section 212, and section 611

❑ The Section 199A deduction

20

BNY Mellon Wealth Management

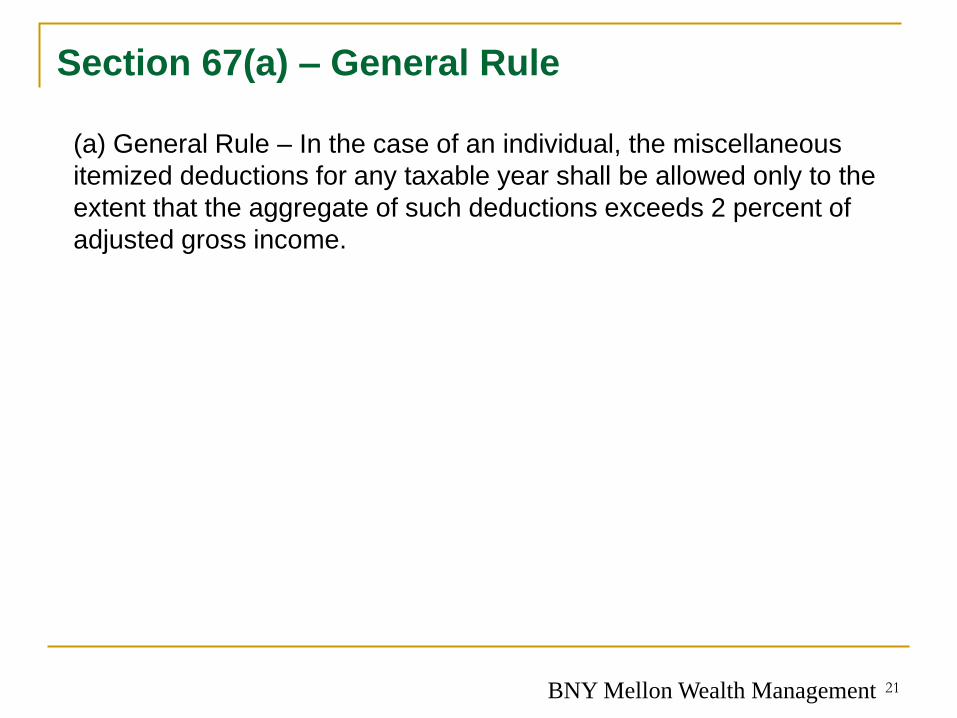

Section 67(a) – General Rule

(a) General Rule – In the case of an individual, the miscellaneous

itemized deductions for any taxable year shall be allowed only to the

extent that the aggregate of such deductions exceeds 2 percent of

adjusted gross income.

21

BNY Mellon Wealth Management

Section 67(a) – Translated

◼ Miscellaneous itemized deductions are allowable only to the extent

they exceeds 2% of the estate or trust’s adjusted gross income.

22

BNY Mellon Wealth Management

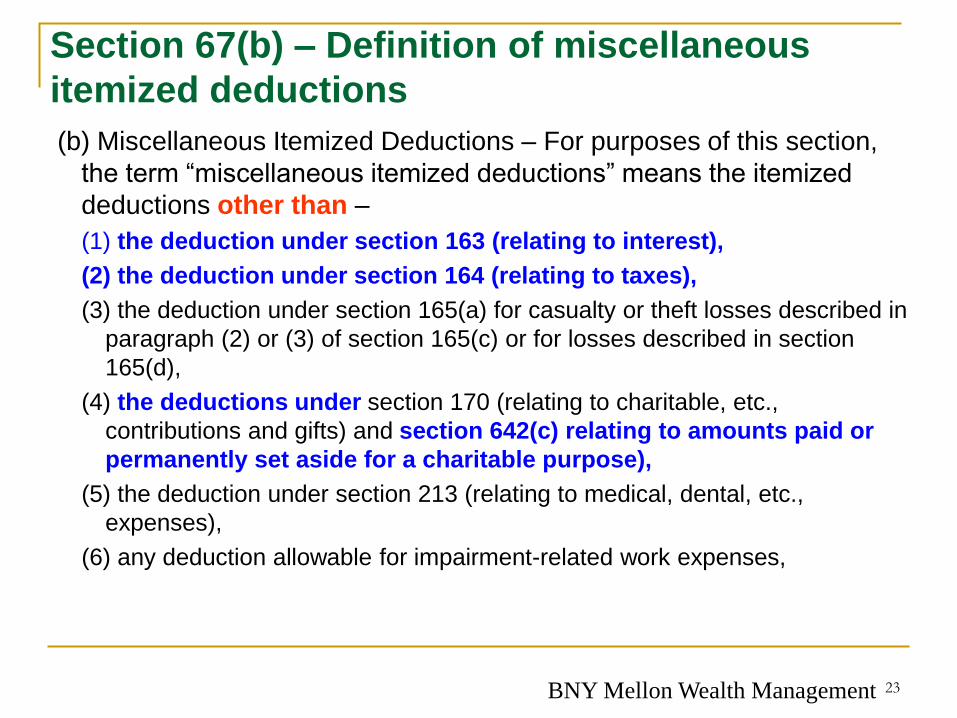

Section 67(b) – Definition of miscellaneous

itemized deductions

(b) Miscellaneous Itemized Deductions – For purposes of this section,

the term “miscellaneous itemized deductions” means the itemized

deductions other than –

(1) the deduction under section 163 (relating to interest),

(2) the deduction under section 164 (relating to taxes),

(3) the deduction under section 165(a) for casualty or theft losses described in

paragraph (2) or (3) of section 165(c) or for losses described in section

165(d),

(4) the deductions under section 170 (relating to charitable, etc.,

contributions and gifts) and section 642(c) relating to amounts paid or

permanently set aside for a charitable purpose),

(5) the deduction under section 213 (relating to medical, dental, etc.,

expenses),

(6) any deduction allowable for impairment-related work expenses,

23

BNY Mellon Wealth Management

Section 67(b) – Definition of miscellaneous

itemized deductions

(b) Miscellaneous Itemized Deductions – For purposes of this section,

the term “miscellaneous deductions” means the itemized deductions

other than –

(7) the deduction under section 691(c) (relating to deduction for estate

tax in case of income in respect of the decedent),

(8) any deduction allowable in connection with personal property used in a

short sale.

(9) the deduction under section 1341 (relating to computation of tax where

taxpayer restores substantial amount held under a claim of right),

(10) the deduction under section 73(b)(3) (relating to deduction where annuity

payments cease before investment recovered),

(11) the deduction under section 171 (relating to deduction for amortizable

bond premium),

(12) the deduction under section 216 (relating to deductions in connection

with cooperative housing corporations).

24

BNY Mellon Wealth Management

Section 67(b) - Translated

◼ Only itemized deductions not included in the above list are potentially

subject to the Section 67(a) limitation i.e., limited to the amount in

excess of 2% of the estate or trust’s adjusted gross income

◼ This excludes the items above highlighted in blue:

❑ Interest

❑ Taxes – although otherwise limited to $10,000 under TCJA of 2017 for years

2018 to 2025

❑ Section 691(c) deduction – income tax deduction for estate tax attributable to

IRD

❑ Charitable deduction under Section 642(c)

25

BNY Mellon Wealth Management

Section 67(e) – Determination of Adjusted

Gross Income in Case of Estates and Trusts

(e) Determination of Adjusted Gross Income in Case of Estates and

Trusts. For purposes of this section the adjusted gross income of an

estate or trust shall be computed in the same manner as in the case

of an individual, except that-

(1) the deduction for costs which are paid or incurred in connection

with the administration of the estate or trust and which would not have

been incurred if the property were not held in such trust or estate, and

(2) the deductions allowable under sections 642(b), 651, and 661,

shall be treated as allowable in arriving at adjusted gross income.

Under regulations, appropriate adjustments shall be made in the

application of part I of subchapter J of this chapter to take into account

the provisions of this section.

26

BNY Mellon Wealth Management

Section 67(e) - Translated

◼ Section 67(e) allows the section 651 and 661 income distribution

deduction and the section 642(b) personal exemption in computing

the adjusted gross income of an estate or trust.

❑ Thus, the Section 67(a) limitation does not apply to income distribution

deduction or the personal exemption.

❑ Section 67(a) limitation also does not apply to expenses that individuals do not

normally incur i.e., expense “unique” to an estate or trust

❑ Section 67(a) limitation applies if the cost “is included in the definition of

miscellaneous itemized deductions under section 67(b) . . . and commonly or

customarily would be incurred by a hypothetical individual holding the same

property.” Reg. 1.67-4(a).

◼ Investment advisory fees are what the IRS is concerned about

27

BNY Mellon Wealth Management

Section 67(e) - Translated

◼ Section 67(e) removes the deductions in Section 67(e)(1) and (2) from

the definition of itemized deductions under Section 63(d) and thus

from the definition of miscellaneous itemized deductions under

Section 67(b), and treats them as deductions allowable in arriving at

AGI under Section 62(a).

❑ Section 67(e)(1) – costs in the administration of an estate or trust which

would not have been incurred if the property were not held in the estate or

trust.

❑ Section 67(e)(2) – deductions allowable under Section 642(b) (personal

exemption), Section 651 and Section 661 (income distribution deduction).

28

BNY Mellon Wealth Management

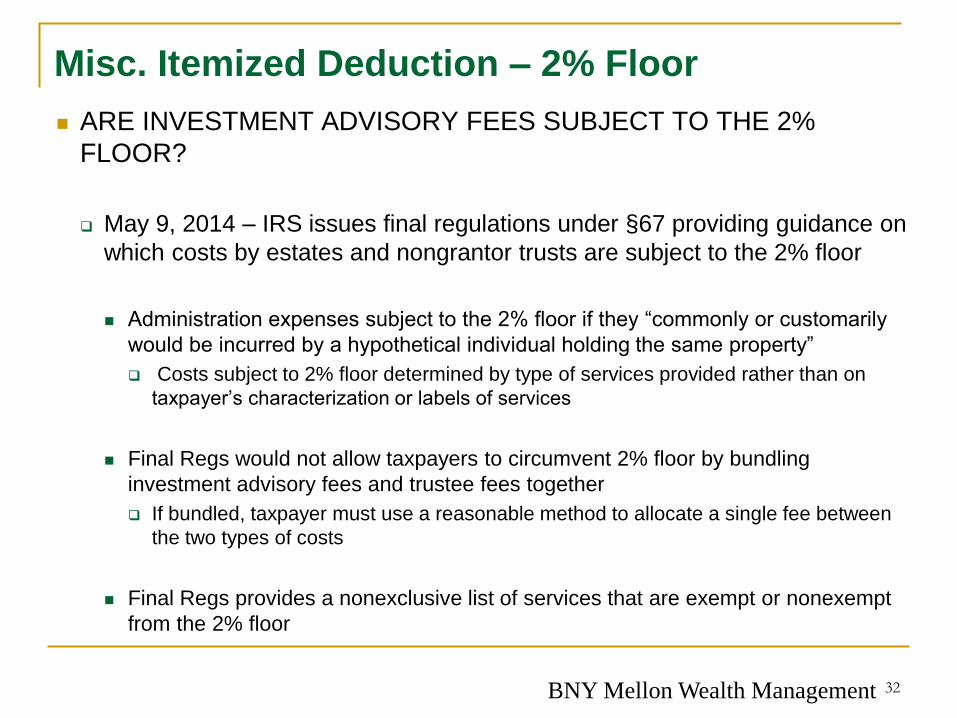

Misc. Itemized Deduction – 2% Floor

◼ ARE INVESTMENT ADVISORY FEES SUBJECT TO THE 2%

FLOOR?

❑ O’Neill – Sixth Circuit – NO

❑ Mellon – Federal Circuit – YES

❑ Scott – Fourth Circuit – YES

❑ Rudkin – Second Circuit – YES

◼ Appealed to United States Supreme Court as Knight

30

BNY Mellon Wealth Management

Section 67(e) - Misc. Itemized Deductions

Subject to 2% Floor

◼ KNIGHT v. COMMISSIONER 552 U.S. 181 (2008)

❑ §67(e) excepts from the 2% floor only those costs that it would be

uncommon (or unusual or unlikely) for an individual to incur.

❑ Specifically disavows the “could not have been incurred by an individual”

language of the Second Circuit in Rudkin and the IRS proposed regulations

31

BNY Mellon Wealth Management

Misc. Itemized Deduction – 2% Floor

◼ ARE INVESTMENT ADVISORY FEES SUBJECT TO THE 2%

FLOOR?

❑ May 9, 2014 – IRS issues final regulations under §67 providing guidance on

which costs by estates and nongrantor trusts are subject to the 2% floor

◼ Administration expenses subject to the 2% floor if they “commonly or customarily

would be incurred by a hypothetical individual holding the same property”

❑ Costs subject to 2% floor determined by type of services provided rather than on

taxpayer’s characterization or labels of services

◼ Final Regs would not allow taxpayers to circumvent 2% floor by bundling

investment advisory fees and trustee fees together

❑ If bundled, taxpayer must use a reasonable method to allocate a single fee between

the two types of costs

◼ Final Regs provides a nonexclusive list of services that are exempt or nonexempt

from the 2% floor

32

BNY Mellon Wealth Management

Misc. Itemized Deduction – 2% Floor

◼ ARE INVESTMENT ADVISORY FEES SUBJECT TO THE 2%

FLOOR?

❑ Five categories of expenses under the Section 67(e) regulations:

◼ Ownership costs

◼ Tax preparation fees

◼ Appraisal fees

◼ Certain fiduciary expenses

◼ Investment advisory fees

33

BNY Mellon Wealth Management

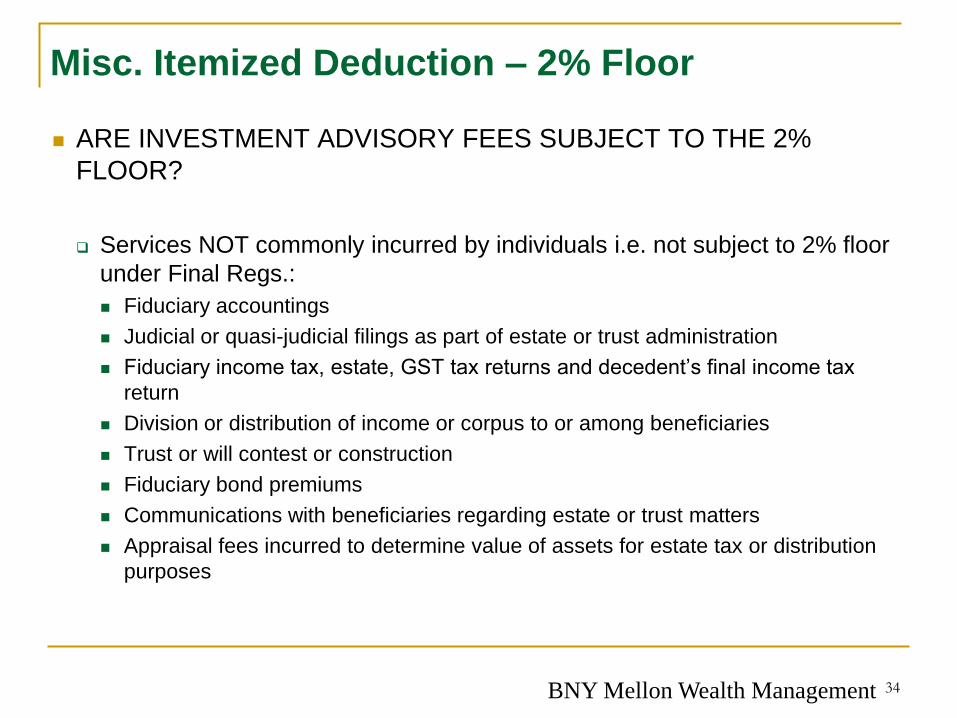

Misc. Itemized Deduction – 2% Floor

◼ ARE INVESTMENT ADVISORY FEES SUBJECT TO THE 2%

FLOOR?

❑ Services NOT commonly incurred by individuals i.e. not subject to 2% floor

under Final Regs.:

◼ Fiduciary accountings

◼ Judicial or quasi-judicial filings as part of estate or trust administration

◼ Fiduciary income tax, estate, GST tax returns and decedent’s final income tax

return

◼ Division or distribution of income or corpus to or among beneficiaries

◼ Trust or will contest or construction

◼ Fiduciary bond premiums

◼ Communications with beneficiaries regarding estate or trust matters

◼ Appraisal fees incurred to determine value of assets for estate tax or distribution

purposes

34

BNY Mellon Wealth Management

Misc. Itemized Deduction – 2% Floor

◼ ARE INVESTMENT ADVISORY FEES SUBJECT TO THE 2%

FLOOR?

❑ Services commonly incurred by individual i.e. subject to 2% floor under

Final Regs.:

◼ Custody or management of property

◼ Advice on investing for total return

◼ Gift tax returns

◼ Defense of claims by creditors of the decedent or grantor

◼ Purchase, sale, maintenance, repair, insurance or management of nontrade or

non-business property

35

BNY Mellon Wealth Management

Misc. Itemized Deduction – 2% Floor

◼ Expenses commonly or customarily incurred by hypothetical individual

include:

❑ Cost incurred in defense of claim against the estate, the decedent, or non-

grantor trust that is unrelated to the existence, validity or administration of

the estate or trust

❑ “Ownership costs” associated with a particular assets such as a condo fee,

insurance premiums, maintenance and lawn services, automobile

registration and insurance costs

❑ Cost of individual and gift tax returns, tax return for a sole proprietorship or

a retirement plan

❑ Fees for investment advice

◼ Exception: “Special” investment advice attributable to an unusual investment

objective or need is not subject to the 2% floor.

❑ Incorporates language from the Knight decision.

36

BNY Mellon Wealth Management

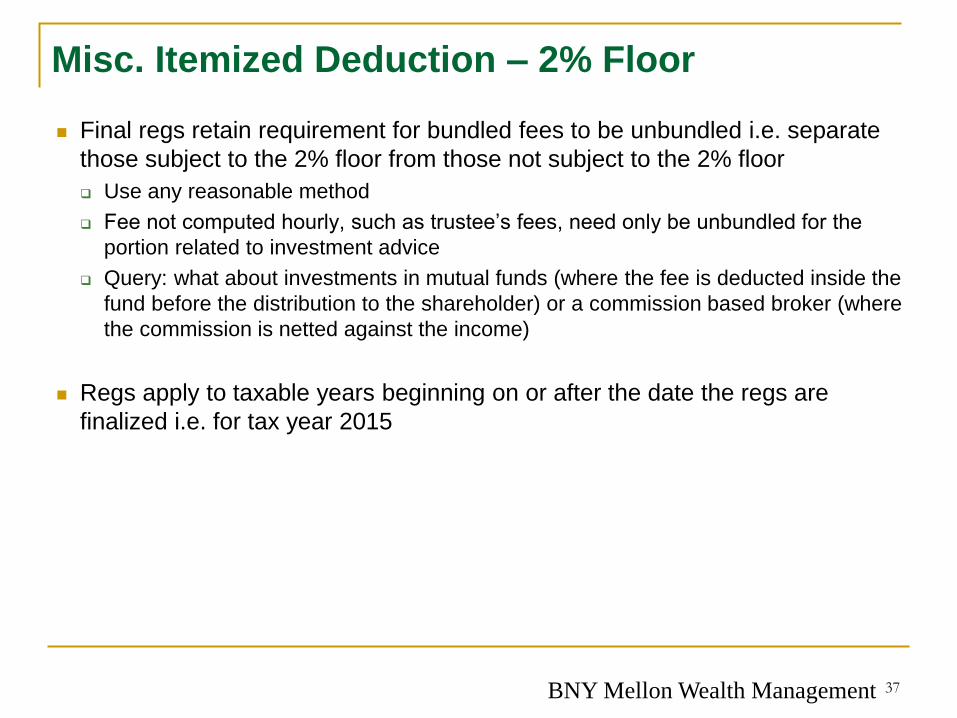

Misc. Itemized Deduction – 2% Floor

◼ Final regs retain requirement for bundled fees to be unbundled i.e. separate

those subject to the 2% floor from those not subject to the 2% floor

❑ Use any reasonable method

❑ Fee not computed hourly, such as trustee’s fees, need only be unbundled for the

portion related to investment advice

❑ Query: what about investments in mutual funds (where the fee is deducted inside the

fund before the distribution to the shareholder) or a commission based broker (where

the commission is netted against the income)

◼ Regs apply to taxable years beginning on or after the date the regs are

finalized i.e. for tax year 2015

37

BNY Mellon Wealth Management

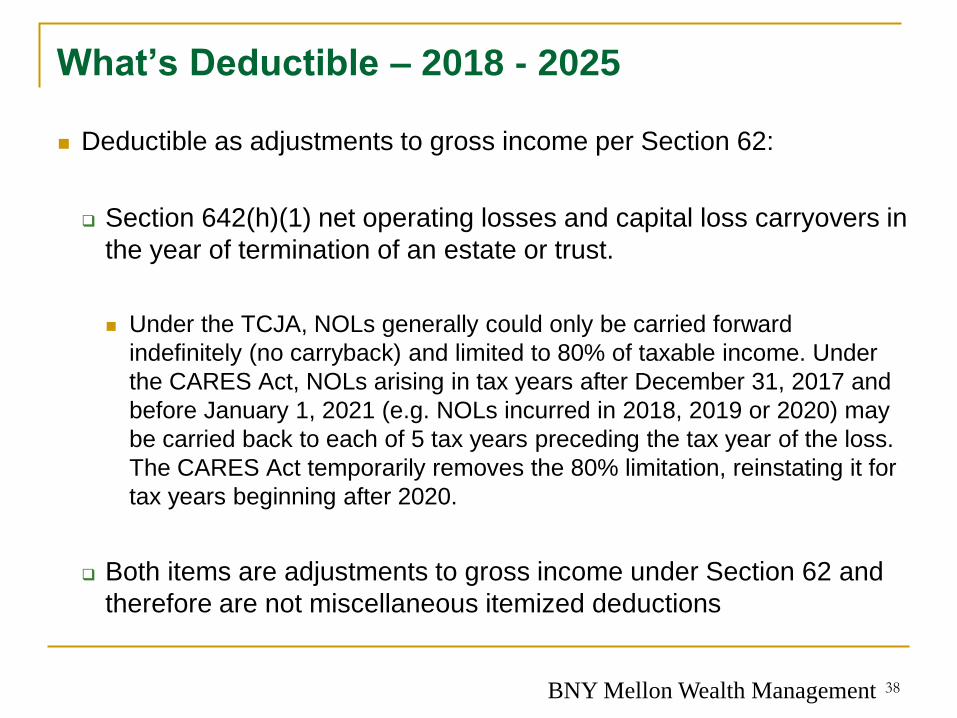

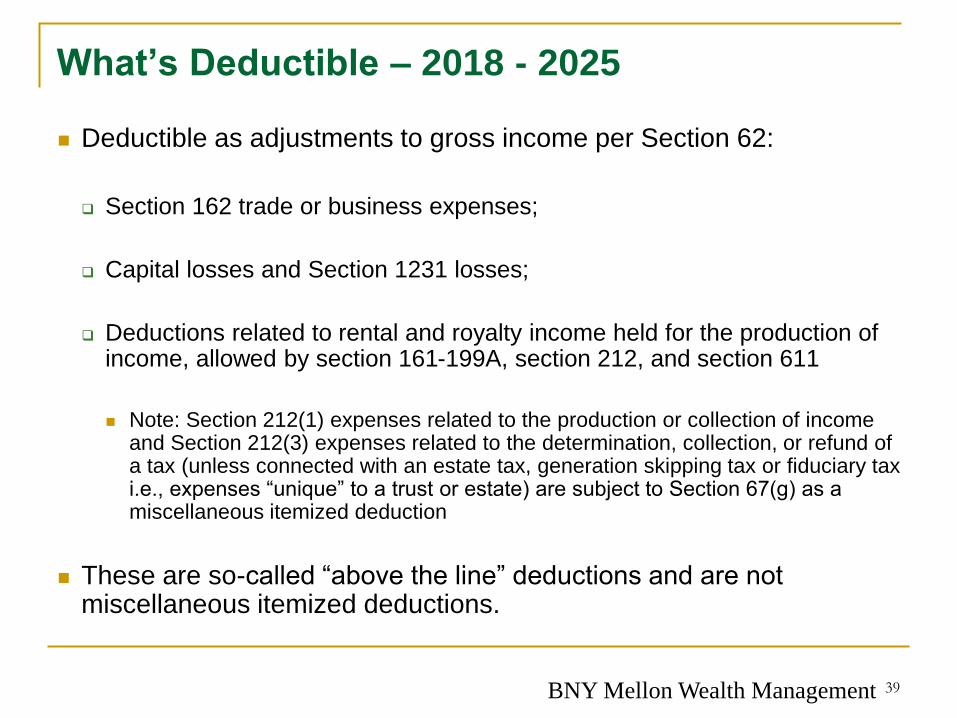

What’s Deductible – 2018 - 2025

◼ Deductible as adjustments to gross income per Section 62:

❑ Section 642(h)(1) net operating losses and capital loss carryovers in

the year of termination of an estate or trust.

◼ Under the TCJA, NOLs generally could only be carried forward

indefinitely (no carryback) and limited to 80% of taxable income. Under

the CARES Act, NOLs arising in tax years after December 31, 2017 and

before January 1, 2021 (e.g. NOLs incurred in 2018, 2019 or 2020) may

be carried back to each of 5 tax years preceding the tax year of the loss.

The CARES Act temporarily removes the 80% limitation, reinstating it for

tax years beginning after 2020.

❑ Both items are adjustments to gross income under Section 62 and

therefore are not miscellaneous itemized deductions

38

BNY Mellon Wealth Management

What’s Deductible – 2018 - 2025

◼ Deductible as adjustments to gross income per Section 62:

❑ Section 162 trade or business expenses;

❑ Capital losses and Section 1231 losses;

❑ Deductions related to rental and royalty income held for the production of income, allowed by section 161-199A, section 212, and section 611

◼ Note: Section 212(1) expenses related to the production or collection of income and Section 212(3) expenses related to the determination, collection, or refund of a tax (unless connected with an estate tax, generation skipping tax or fiduciary tax i.e., expenses “unique” to a trust or estate) are subject to Section 67(g) as a miscellaneous itemized deduction

◼ These are so-called “above the line” deductions and are not miscellaneous itemized deductions.

39

BNY Mellon Wealth Management

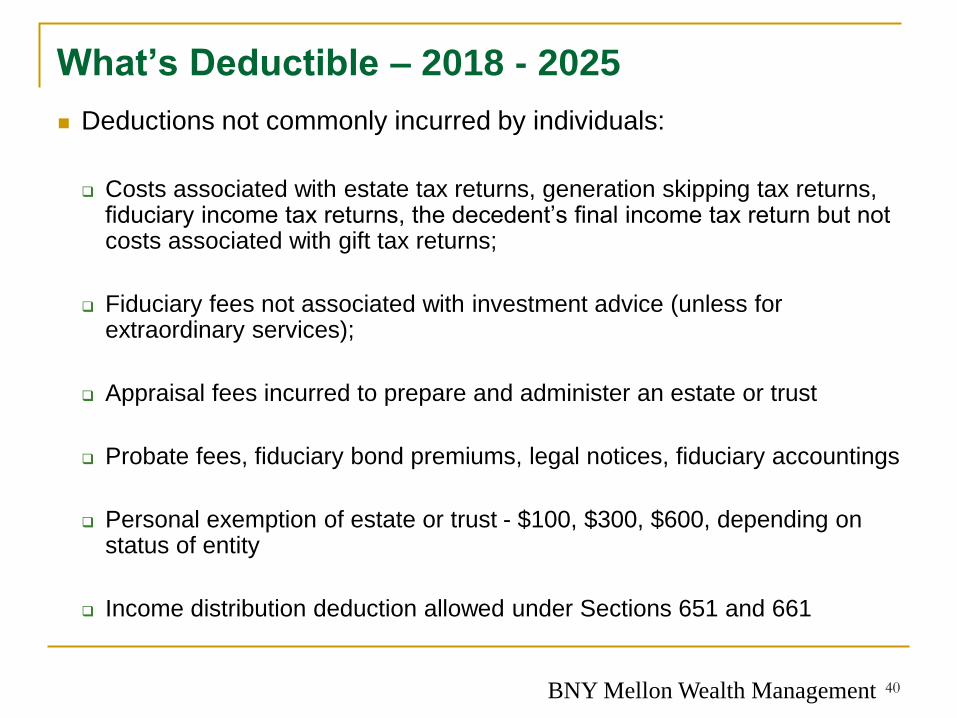

What’s Deductible – 2018 - 2025

◼ Deductions not commonly incurred by individuals:

❑ Costs associated with estate tax returns, generation skipping tax returns, fiduciary income tax returns, the decedent’s final income tax return but not costs associated with gift tax returns;

❑ Fiduciary fees not associated with investment advice (unless for extraordinary services);

❑ Appraisal fees incurred to prepare and administer an estate or trust

❑ Probate fees, fiduciary bond premiums, legal notices, fiduciary accountings

❑ Personal exemption of estate or trust - $100, $300, $600, depending on status of entity

❑ Income distribution deduction allowed under Sections 651 and 661

40

BNY Mellon Wealth Management

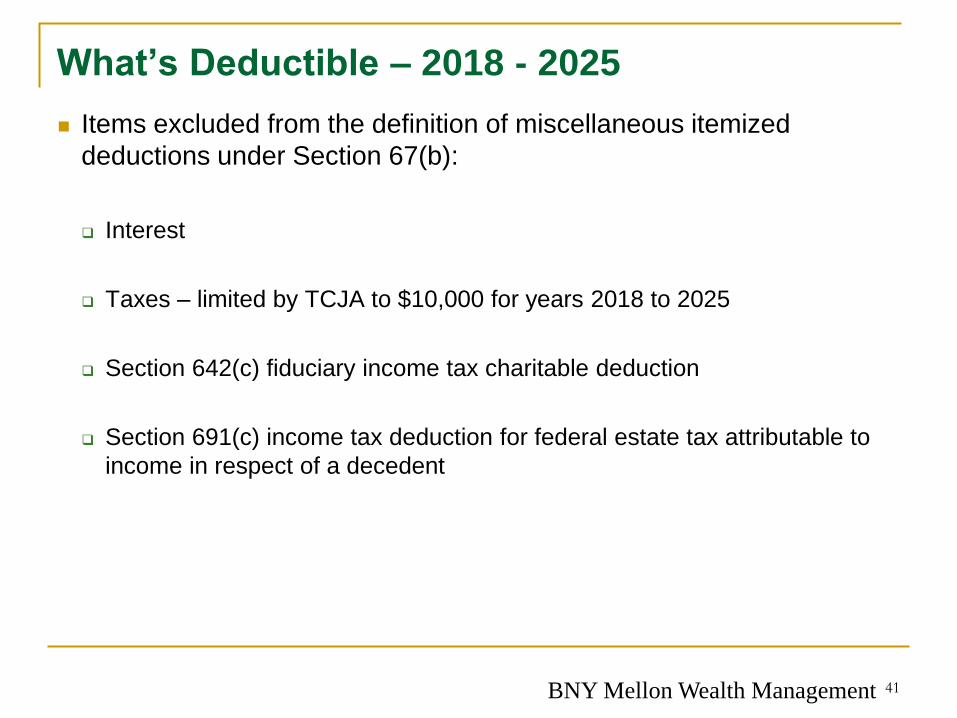

What’s Deductible – 2018 - 2025

◼ Items excluded from the definition of miscellaneous itemized

deductions under Section 67(b):

❑ Interest

❑ Taxes – limited by TCJA to $10,000 for years 2018 to 2025

❑ Section 642(c) fiduciary income tax charitable deduction

❑ Section 691(c) income tax deduction for federal estate tax attributable to

income in respect of a decedent

41

BNY Mellon Wealth Management

What’s Not Deductible – 2018 - 2025

◼ Items that constitute miscellaneous itemized deductions:

❑ Investment advisory fees (except for extraordinary expenses);

❑ Appraisal fees incurred other than in the taxation or administration of an

estate or trust;

❑ Property ownership costs not deductible as a trade or business expense;

❑ Section 212(1) expenses related to the production or collection of income

and Section 212(3) expenses related to the determination, collection, or

refund of a tax (unless connected with an estate tax, generation skipping

tax or fiduciary tax i.e., expenses “unique” to a trust or estate);

❑ Miscellaneous itemized deductions from partnerships and S corporations

42

BNY Mellon Wealth Management

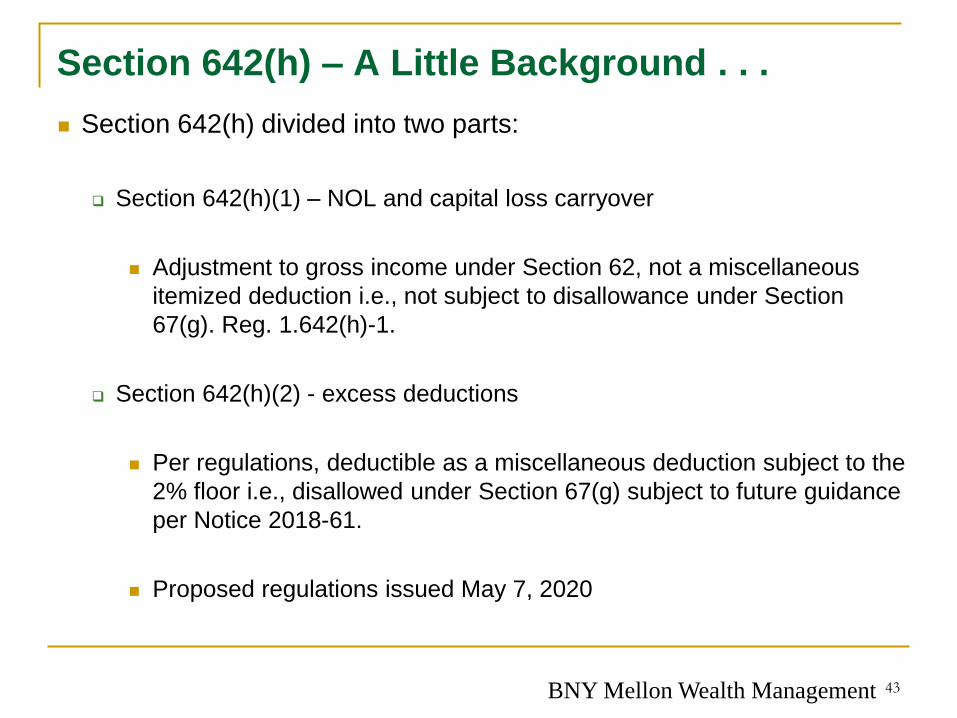

Section 642(h) – A Little Background . . .

◼ Section 642(h) divided into two parts:

❑ Section 642(h)(1) – NOL and capital loss carryover

◼ Adjustment to gross income under Section 62, not a miscellaneous

itemized deduction i.e., not subject to disallowance under Section

67(g). Reg. 1.642(h)-1.

❑ Section 642(h)(2) - excess deductions

◼ Per regulations, deductible as a miscellaneous deduction subject to the

2% floor i.e., disallowed under Section 67(g) subject to future guidance

per Notice 2018-61.

◼ Proposed regulations issued May 7, 2020

43

BNY Mellon Wealth Management

What’s Not Deductible – 2018 - 2025

◼ Items that constitute miscellaneous itemized deductions:

❑ Section 642(h)(2) excess deductions of an estate or trust

◼ Try to generate income in the final year to avoid excess deductions or better

time matching of income and deductions to avoid excess deductions

❑ The regulations treat excess deductions as miscellaneous itemized

deductions to the individuals entitled to that item. Reg. 642(h)-2(a).

❑ Thus, Section 67(g) would not allow an individual to deduct the excess

deductions for those excess deductions reported in the years 2018 to 2025.

❑ However, see Notice 2018-61 (Treasury may bifurcate excess deductions),

followed by proposed regulations issued May 7, 2020.

44

BNY Mellon Wealth Management

May 7, 2020 Proposed Regulations

◼ Confirms provisions of Notice 2018-61 - an estate or non-grantor trust

(and S portion of an ESBT) computes is AGI in the same manner as

an individual. Also, the following deductions (Section 67(e)

deductions) are allowed in arriving at AGI:

❑ Costs paid or incurred in connection with the administration of the estate or

trust which would not have been incurred if the property was not held in the

estate or trust; and

❑ Deductions allowable under Section 642(b) (personal exemption) and

Sections 651 and 661 (distribution deduction).

◼ Section 67(e) deductions are not itemized deductions under Section

63(d) and are not miscellaneous itemized deductions under Section

67(b). Therefore, Section 67(e) deductions are not disallowed under

Section 67(g).

45

BNY Mellon Wealth Management

May 7, 2020 Proposed Regulations

◼ Deduction is subject to the 2% floor and is not a Section 67(e)

deduction (1) to the extent it is included in the definition of

miscellaneous itemized deductions under Section 67(b), (2) is

incurred by an estate or non-grantor trust (including the S portion of

an ESBT) and (3) commonly or customarily would be incurred by a

hypothetical individual holding the same property. These expenses

are disallowed by Section 67(g) for the years 2018 through 2025.

46

BNY Mellon Wealth Management

May 7, 2020 Proposed Regulations

◼ Excess deductions may consist of:

❑ Deductions allowable in arriving at AGI under Section 62 and 67(e);

❑ Itemized deductions under Section 63(d) allowable in computing taxable

income; and

❑ Miscellaneous itemized deductions currently disallowed under Section

67(g).

◼ Therefore, the proposed regulations segregate excess deductions

into its components to determine the character, computation and

deductibility.

47

BNY Mellon Wealth Management

May 7, 2020 Proposed Regulations

◼ Deductions separated into three categories and its deductibility is

determined by the category to which it is assigned:

❑ Those allowable in arriving at AGI;

❑ Those that are a non-miscellaneous itemized deductions; and

❑ Those that are a miscellaneous itemized deduction.

◼ Each deduction retains its separate character in the hands of the

beneficiary that it had in the hands of the trust or estate, i.e., as an

amount in arriving at AGI, as a non-miscellaneous itemized deduction

or as a miscellaneous itemized deduction..

48

BNY Mellon Wealth Management

May 7, 2020 Proposed Regulations

◼ The proposed regulations require that the fiduciary separately state

(that is, separately identify) deductions that may be limited when

claimed by the beneficiary .

◼ In other words, the fiduciary must separately state how the deduction

is to be treated on the beneficiary’s income tax return.

◼ The deductions is to be allocated to the various classes of estate or

trust income in the year of termination as provided in Reg. 1.652(b)-3

in order to determine the character and amount of the excess

deduction.

49

BNY Mellon Wealth Management

May 7, 2020 Proposed Regulations

◼ Allocation of deductions follow the rules in Reg. 1.652(b)-3(a), (b) and

(d).

◼ Any deduction remaining after the application of Reg. 1.652-3(a), (b)

and (d) are excess deductions on termination of the estate or trust.

◼ Carryover and excess deductions to which Section 642(h) apply are

allocated among the beneficiaries succeeding to the property of the

estate or trust proportionately according to the share of each in the

burden of the loss or deduction. Reg. 1.642(h)-4.

50

BNY Mellon Wealth Management

Charging Expenses Against Items of Income

◼ Expenses entering into the calculation of DNI are charged against

items of income comprising DNI.

◼ Deductions cannot reduce any item of income below zero because a

fiduciary cannot distribute a negative amount to a beneficiary.

◼ Expenses are classified as either: (1) direct expenses or (2) indirect

expenses

51

BNY Mellon Wealth Management

Charging Expenses Against Items of Income

◼ Direct expenses

❑ All deductible items directly attributable to one class of income must be

charged against that class of income.

❑ For example, in determining the rental income comprising DNI, real estate

repairs, real estate taxes and other deductible expenses directly attributable

to rental property are charged against the rental income.

❑ If deductions directly attributable to a particular class of income exceed the

amount of that income, the excess is generally charged against other

classes of income in the same manner as indirect expenses. However, if the

expense is directly related to a class of ordinary income, then no portion of

the expense needs to be charged against tax-exempt income. Reg.

1.652(b)-3(d) says that such excess can be charged against other items of

taxable income, notwithstanding the general rule concerning indirect

expenses. Similarly, excess deductions directly attributable to tax-exempt

income cannot offset any other class of income.

52

BNY Mellon Wealth Management

Charging Expenses Against Items of Income

◼ Indirect expenses

❑ Tax deductions not directly attributable to a specific class of income may be

charged against any item of income included in DNI, but a pro rata portion

must be allocated against tax-exempt interest

53

BNY Mellon Wealth Management

Charging Expenses Against Items of Income

◼ Charging indirect expenses against tax-exempt income

❑ Section 265 prohibits taking a deduction for expenses allocated to tax-

exempt income

❑ Reg. 1.652(b)-3(b) requires that a portion of indirect expenses incurred by a

trust or estate be allocated against tax-exempt income.

❑ One method of allocation to tax-exempt income is to do a pro-rata allocation,

i.e., tax-exempt income/all items of gross income entering into DNI x

expense.

◼ This method has been accepted by the courts in Manufacturer’s Hanover Trust Co.

v. United States, 312 F.2d 785 (1963); Tucker v. Commissioner, 322 F.2d 86 (2d

Cir. 1963; Rev. Rul, 77-355, 1977-2 C.B 82..

54

BNY Mellon Wealth Management

Charging Expenses Against Items of Income

◼ Charging indirect expenses against tax-exempt income

❑ However, the above method is not mandatory. The fiduciary may use any

method of allocation that he can justify as reasonable. See, e.g. Wittemore v.

United States, 383 F.2d 824 (8th Cir. 1967 (trustee’s termination fee was

allocated based on ratio of taxable to nontaxable income over the life of the

trust).

❑ However, state income taxes are deductible in full despite the existence of

tax-exempt interest. Why? Because Section 164 specifically allows a

deduction for taxes. Section 265 applies to Section 212 expenses which are

allowed for expenses relating to the production of income. Rev. Rul. 61-86,

1961-1 C.B. 41.

55

BNY Mellon Wealth Management

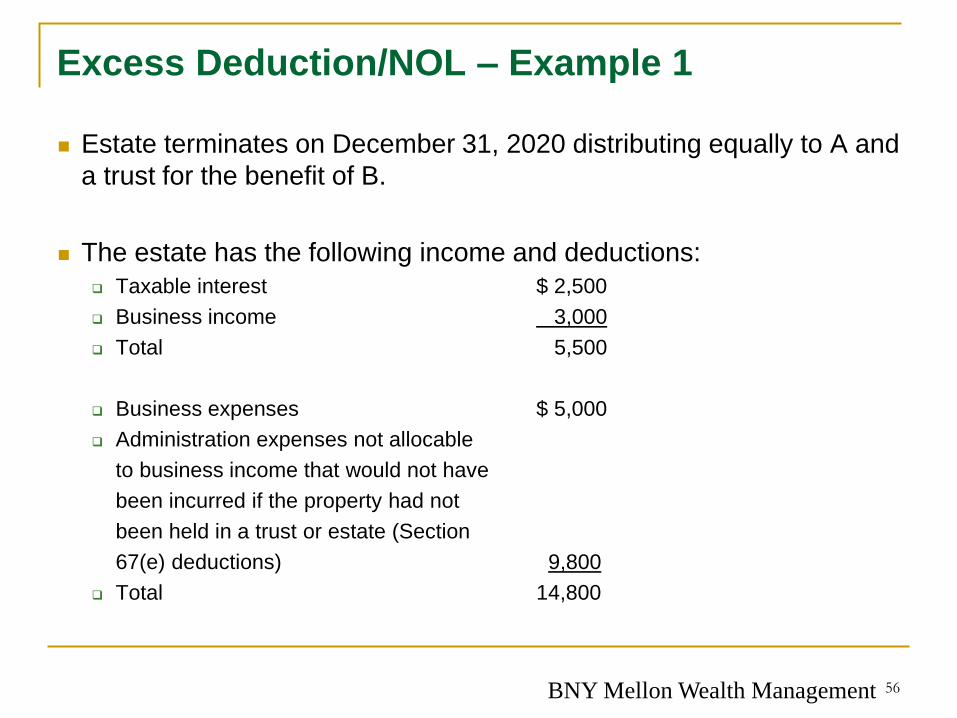

Excess Deduction/NOL – Example 1

◼ Estate terminates on December 31, 2020 distributing equally to A and

a trust for the benefit of B.

◼ The estate has the following income and deductions:

❑ Taxable interest $ 2,500

❑ Business income 3,000

❑ Total 5,500

❑ Business expenses $ 5,000

❑ Administration expenses not allocable

to business income that would not have

been incurred if the property had not

been held in a trust or estate (Section

67(e) deductions) 9,800

❑ Total 14,800

56

BNY Mellon Wealth Management

Excess Deduction/NOL – Example 1

57

Interest

Business

Income Total

Income $2,500 $3,000 $5,500

Direct

Expense (5,000) (5,000)

Indirect

Expense (9,800) (9,800)

(7,300) (2,000) (9,300)

Section 67(e)

Excess Deduction

NOL

BNY Mellon Wealth Management

Excess Deduction/NOL – Example 1

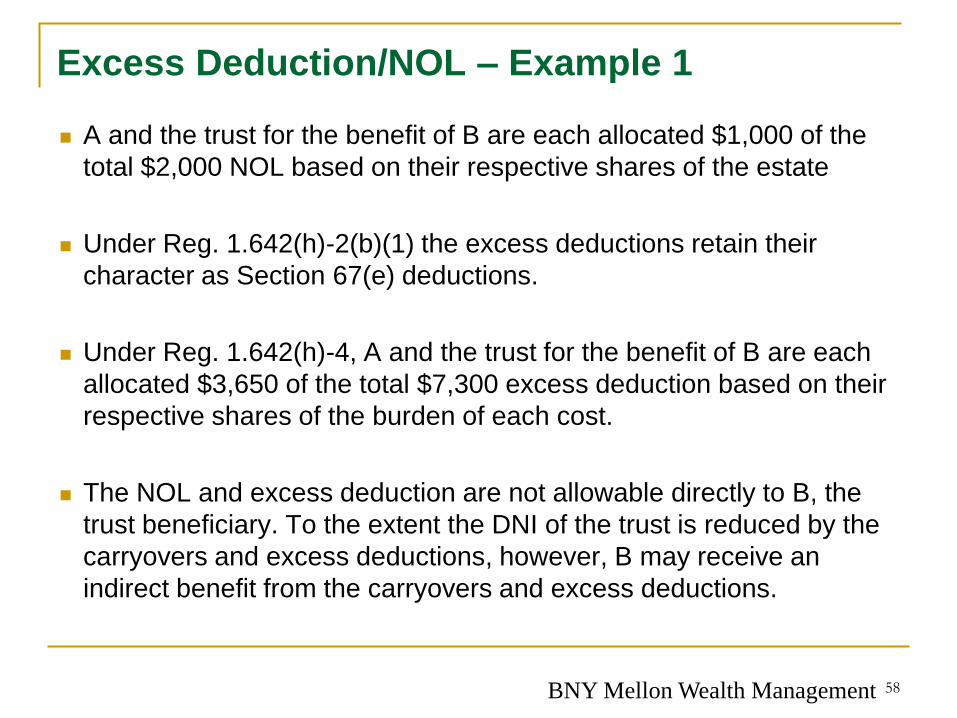

◼ A and the trust for the benefit of B are each allocated $1,000 of the

total $2,000 NOL based on their respective shares of the estate

◼ Under Reg. 1.642(h)-2(b)(1) the excess deductions retain their

character as Section 67(e) deductions.

◼ Under Reg. 1.642(h)-4, A and the trust for the benefit of B are each

allocated $3,650 of the total $7,300 excess deduction based on their

respective shares of the burden of each cost.

◼ The NOL and excess deduction are not allowable directly to B, the

trust beneficiary. To the extent the DNI of the trust is reduced by the

carryovers and excess deductions, however, B may receive an

indirect benefit from the carryovers and excess deductions.

58

BNY Mellon Wealth Management

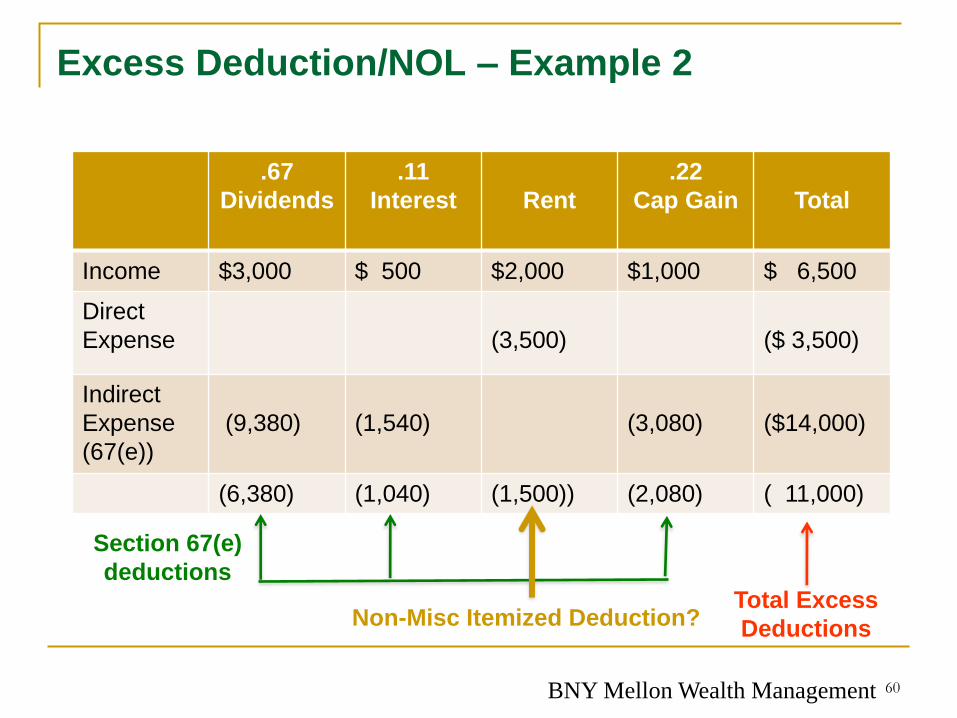

Excess Deduction/NOL – Example 2

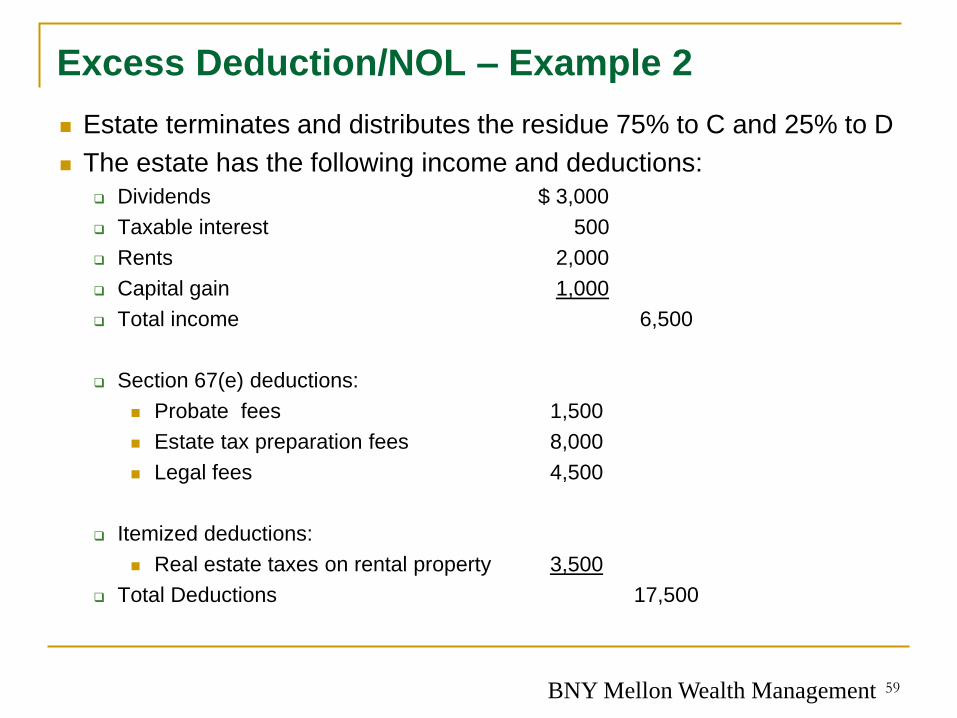

◼ Estate terminates and distributes the residue 75% to C and 25% to D

◼ The estate has the following income and deductions:

❑ Dividends $ 3,000

❑ Taxable interest 500

❑ Rents 2,000

❑ Capital gain 1,000

❑ Total income 6,500

❑ Section 67(e) deductions:

◼ Probate fees 1,500

◼ Estate tax preparation fees 8,000

◼ Legal fees 4,500

❑ Itemized deductions:

◼ Real estate taxes on rental property 3,500

❑ Total Deductions 17,500

59

BNY Mellon Wealth Management

Excess Deduction/NOL – Example 2

60

.67

Dividends

.11

Interest Rent

.22

Cap Gain Total

Income $3,000 $ 500 $2,000 $1,000 $ 6,500

Direct

Expense (3,500) ($ 3,500)

Indirect

Expense

(67(e))

(9,380) (1,540) (3,080) ($14,000)

(6,380) (1,040) (1,500)) (2,080) ( 11,000)

Total Excess

Deductions

Section 67(e)

deductions

Non-Misc Itemized Deduction?

BNY Mellon Wealth Management

Excess Deduction/NOL – Example 2

◼ Pursuant to Reg. 1.642(h)-2(b)(2), the character and amount of the

excess deductions is determined by allocating the deductions among

the estate’s items of income as provided in Reg. 1.652(b)-3.

◼ Under Reg. 1.652(b)-3(a), $3.500 of real estate taxes is a direct

expense of producing rental income so it is allocated directly to the

$2,000 of rental income, leaving $1,500 excess deduction.

◼ In exercising the executor’s discretion pursuant to Reg. 1.652(b)-3(b)

and (d), the executor allocates remaining indirect expenses to the

remaining classes of income pro-rata.

◼ The result is excess deductions on termination totaling $11,000,

consisting of $9,500 of Section 67(e) deductions and $1,500 of non-

miscellaneous itemized deductions.

61

BNY Mellon Wealth Management

Excess Deduction/NOL – Example 2

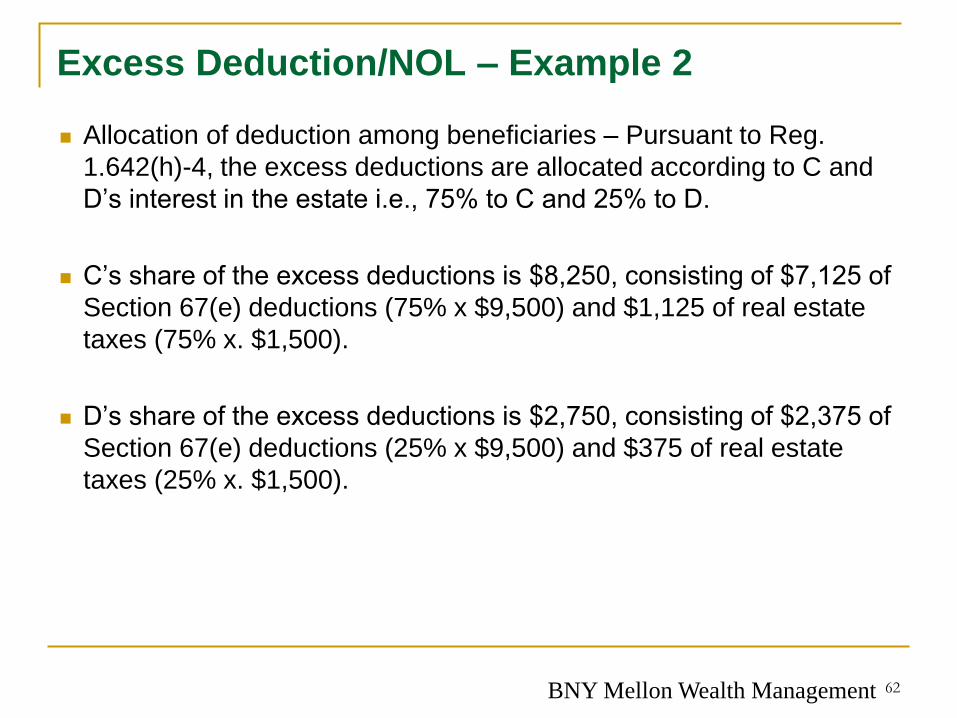

◼ Allocation of deduction among beneficiaries – Pursuant to Reg.

1.642(h)-4, the excess deductions are allocated according to C and

D’s interest in the estate i.e., 75% to C and 25% to D.

◼ C’s share of the excess deductions is $8,250, consisting of $7,125 of

Section 67(e) deductions (75% x $9,500) and $1,125 of real estate

taxes (75% x. $1,500).

◼ D’s share of the excess deductions is $2,750, consisting of $2,375 of

Section 67(e) deductions (25% x $9,500) and $375 of real estate

taxes (25% x. $1,500).

62

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ The big questions is how are these excess deductions reported on the

beneficiary’s income tax return – the 1040 or 1041?

◼ Example 2 in the proposed regulation is taken almost exactly from the

Example in Reg. 1.642(h)-5, which was written 63 years ago before

we had Section 67(a), the passive activity loss rules and Section

67(e).

◼ The regulations say the excess deductions retain the same character

in the hands of the beneficiary as they had in the hands of the estate

or trust.

64

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ So, the excess deduction could be (1) a deduction to get from gross

income to adjusted gross income (an above-the-line deduction under

Section 62, 63(d) or 67(e)), a non-miscellaneous itemized deduction

under 67(b), or a miscellaneous itemized deduction disallowed under

Section 67(g). In addition, the excess deduction could result in a loss

being classified as a passive activity loss (PAL).

◼ If the excess deduction is an itemized deduction and the beneficiary

takes the standard deduction – as many will because of the increase

in the standard deduction – the beneficiary will lose the benefit of the

excess deduction.

◼ On the other hand, if it is an above-the-line deduction, the beneficiary

will get the benefit of the excess deduction. But where would you

report it on the tax return?

65

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ First, how does it get reported out to the beneficiary?

❑ Schedule K-1, Box 11 – should attach an explanation of the type of excess

deduction i.e., above-the-line (e.g., Section 67(e) deduction), a non-

miscellaneous itemized deduction, a miscellaneous itemized deduction or

a passive activity loss which is added to the cost basis of the relevant

asset..

❑ The IRS could include a code box alongside Box 11 with codes to identify

the type of excess deduction similar to what is currently used, e.g., Code

A-1 – Section 67(e) or other deduction from gross income to arrive at

adjusted gross income, Code A-2 – non-miscellaneous itemized

deduction, Code A-3 – miscellaneous itemized deduction subject to

Section 67(g), and Code A-4 – passive activity loss, add to basis of

distributed property (see instructions). The instructions would instruct the

taxpayer to determine what property is subject to the basis adjustment.

66

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ Second, where does the above-the-line Section 67(e) deduction get

taken?

❑ Form 1040 – Schedule E, Part III, Income or Loss from Estates and

Trusts. Alternatively, Schedule 1 could be amended by adding a line

“Other Deductions.”

❑ Alternatives for Form 1041: (1) Line 15a – Other Deductions (including

Section 67(e) deductions, or (2) Schedule E, Part III, Income or Loss from

Estates and Trusts – with an attached explanation of the type of excess

deduction.

❑ The IRS has given no guidance on this issue – the above are possibilities

67

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ In Example 2, there is rental income of $2,000 and a $3,500 direct

expense of real estate taxes allocated to the rental income resulting in

a $1,500 loss.

◼ First issue: normally, the income and expense would be reported on

Schedule E and be an above-the-line deduction. However, the

proposed regulation classifies it as an itemized deduction.

❑ If taken as an itemized deduction and the beneficiary takes the standard

deduction, the benefit of the excess deduction is lost.

❑ If it retains its character as an above-the-line deduction, the beneficiary

would benefit from the excess deduction whether he itemizes or takes the

standard deduction.

68

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ Second issue: the $1,500 loss on the rental income is a passive loss.

◼ If the real estate is distributed by the estate to the beneficiary, the loss

would be added to the basis of the distributed asset and “such losses

shall not be allowable as a deduction for any taxable year.” Section

469(j)(12). Thus, the $1,500 loss in Example 2 would not qualify as an

excess deduction.

69

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ If the real estate, instead of being distributed, is sold by the estate in

the year of termination to an unrelated party in a fully taxable

transaction, the loss would be recognized. Section 469(a)(1).

❑ If the property is sold at a gain, the $1,500 loss would probably offset the

gain and not be an excess deduction.

❑ If sold at a loss, the $1,500 would not be a passive loss and would

probably be a net operating loss and not an excess deduction. Section

469(g)(1). In that case, the NOL would carry out to the beneficiary under

Section 642(h)(1).

❑ If not a fully taxable transaction or sold to a related party, Section

469(g)(1) does not apply, the loss is a passive loss and should be an

excess deduction – but is it deductible as an itemized deduction or an

above-the-line deduction?

70

BNY Mellon Wealth Management

Excess Deduction/NOL – Where’s It Go?

◼ If a Section 643(e) election is made to recognize gain on the sale of

the real estate at the entity level, the $1,500 loss, being passive,

should not be allowable because the trust and beneficiary would be

related parties under Section 267 and Section 469(g)(1) is

inapplicable to sales between related parties. Section 469(g)(1)(A),

(B). What happens to the $1,500 loss?

◼ If the decedent was an active participant in the rental activity prior to

his death, the $1,500 loss (subject to a $25,000 limit which is phased

out based on the estate’s AGI) would not be a passive loss for an

estate’s tax year ending less than two years after the decedent’s

death. That loss would probably be a NOL.

❑ The same rule would apply to a “qualified revocable trust” making the

Section 645 election.

71

BNY Mellon Wealth Management

Can You Do This?

◼ Reg. 1.652(b)-3(a) (last sentence) and Reg. 1.652(b)-3(d) (second full

sentence) allows the allocation of the excess of direct expenses over

the income to which those expenses are related to other classes of

income.

◼ It seems that those excess direct expenses, like the $1,500 excess in

Example 2, could be allocated to the other classes of income (except

you don’t have to allocated any of the excess direct expenses to tax-

exempt income) increasing the excess deduction for those classes of

income, and eliminating the $1,500 loss from rental income.

◼ That would avoid the issue of whether the excess of $1,500 direct

expense otherwise allocated to rental income is an itemized

deduction, a NOL, a PAL etc.

72

BNY Mellon Wealth Management

Proposed Regulation Effective Date

◼ Apply to taxable years beginning after the date they are published as

final regulations in the Federal Register.

◼ However, estates, non-grantor trusts and their beneficiaries may rely

on these proposed regulations under Section 67 for taxable years

beginning after December 31, 2017, and on or before the date these

regulations are published as final regulations in the Federal Register.

◼ Taxpayers may also rely on the proposed regulations under Section

642(h) for taxable years of beneficiaries beginning after December 31

2017, and on or before the date these regulations are published as

final regulations in the Federal Register in which an estate or trust

terminates.

73

BNY Mellon Wealth Management

Surprising Results – 2018 - 2025

◼ Alternative minimum tax

❑ Miscellaneous itemized deductions will not be an adjustment for AMT

purposes from 2018 to 2025 for an estate or trust.

74

BNY Mellon Wealth Management

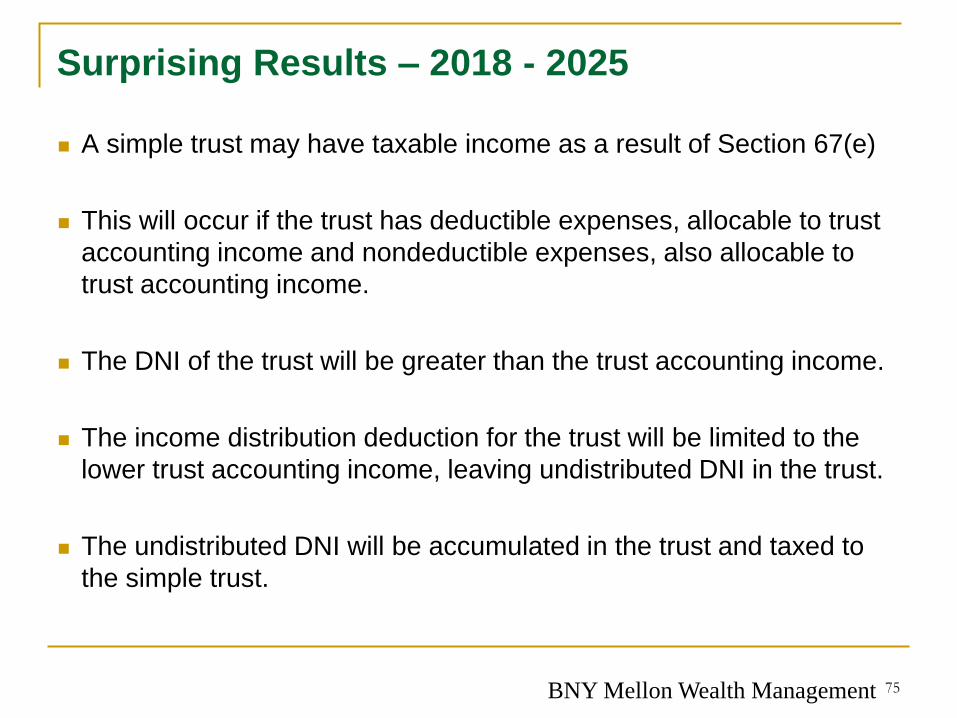

Surprising Results – 2018 - 2025

◼ A simple trust may have taxable income as a result of Section 67(e)

◼ This will occur if the trust has deductible expenses, allocable to trust

accounting income and nondeductible expenses, also allocable to

trust accounting income.

◼ The DNI of the trust will be greater than the trust accounting income.

◼ The income distribution deduction for the trust will be limited to the

lower trust accounting income, leaving undistributed DNI in the trust.

◼ The undistributed DNI will be accumulated in the trust and taxed to

the simple trust.

75

BNY Mellon Wealth Management

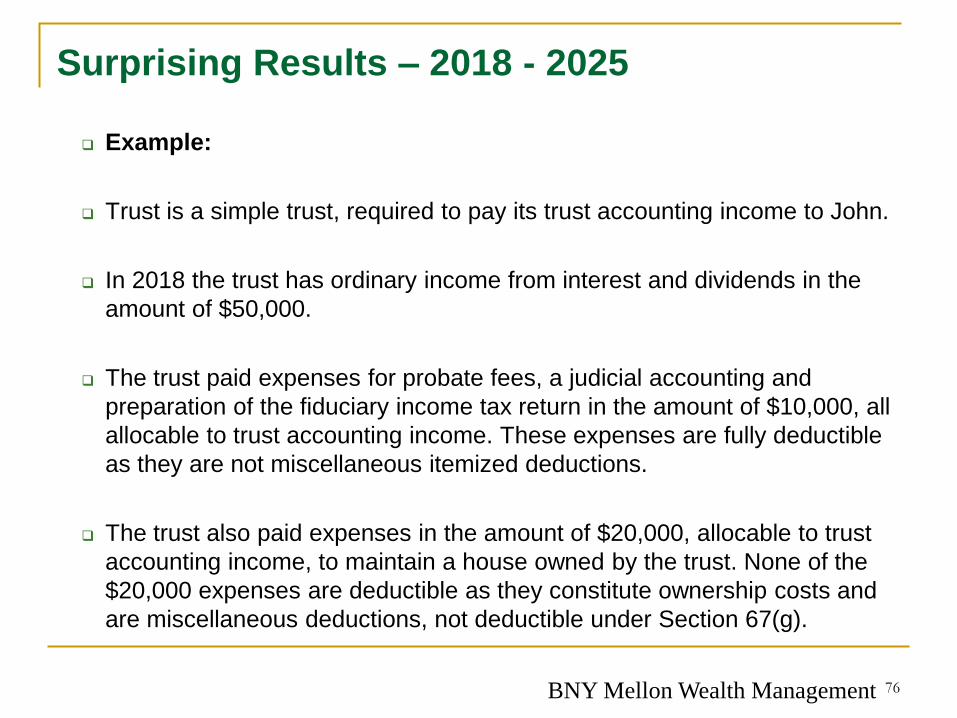

Surprising Results – 2018 - 2025

❑ Example:

❑ Trust is a simple trust, required to pay its trust accounting income to John.

❑ In 2018 the trust has ordinary income from interest and dividends in the

amount of $50,000.

❑ The trust paid expenses for probate fees, a judicial accounting and

preparation of the fiduciary income tax return in the amount of $10,000, all

allocable to trust accounting income. These expenses are fully deductible

as they are not miscellaneous itemized deductions.

❑ The trust also paid expenses in the amount of $20,000, allocable to trust

accounting income, to maintain a house owned by the trust. None of the

$20,000 expenses are deductible as they constitute ownership costs and

are miscellaneous deductions, not deductible under Section 67(g).

76

BNY Mellon Wealth Management

Surprising Results – 2018 - 2025

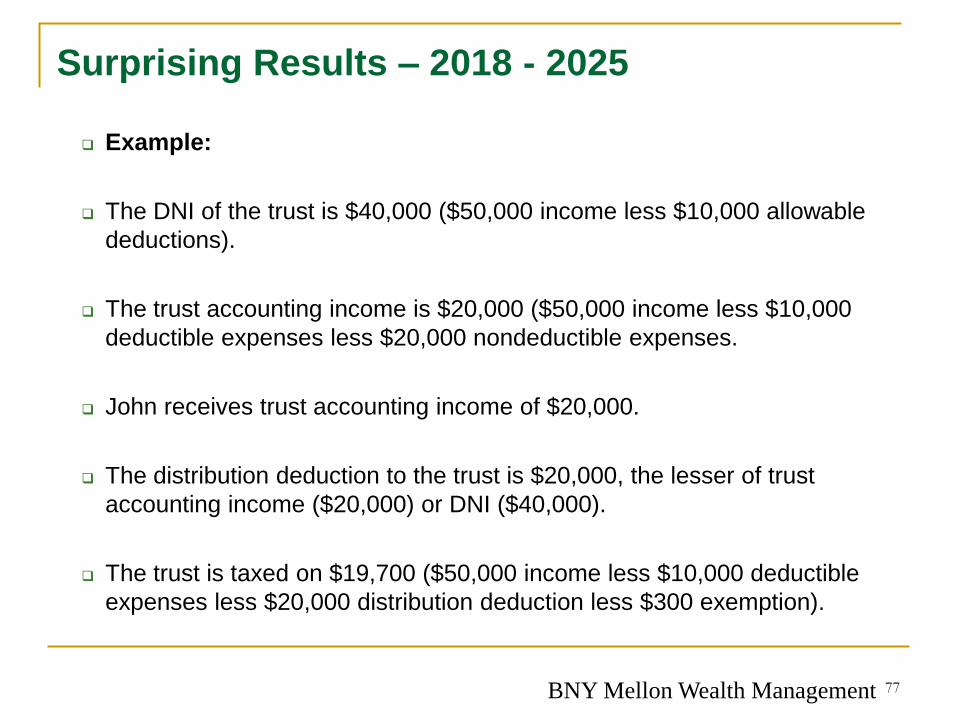

❑ Example:

❑ The DNI of the trust is $40,000 ($50,000 income less $10,000 allowable

deductions).

❑ The trust accounting income is $20,000 ($50,000 income less $10,000

deductible expenses less $20,000 nondeductible expenses.

❑ John receives trust accounting income of $20,000.

❑ The distribution deduction to the trust is $20,000, the lesser of trust

accounting income ($20,000) or DNI ($40,000).

❑ The trust is taxed on $19,700 ($50,000 income less $10,000 deductible

expenses less $20,000 distribution deduction less $300 exemption).

77

BNY Mellon Wealth Management

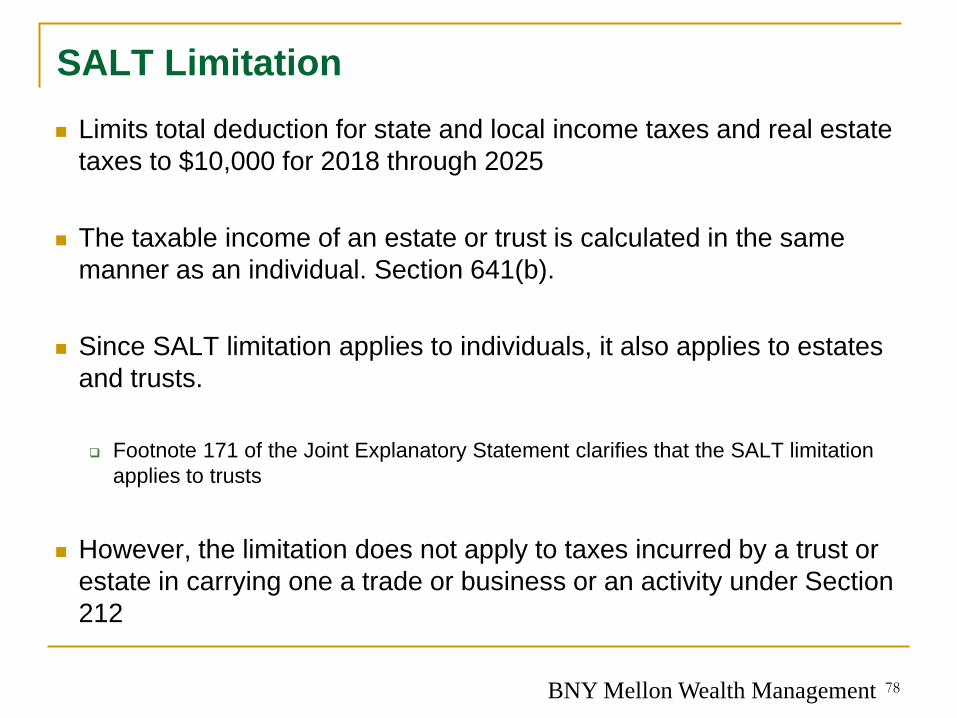

SALT Limitation

◼ Limits total deduction for state and local income taxes and real estate

taxes to $10,000 for 2018 through 2025

◼ The taxable income of an estate or trust is calculated in the same

manner as an individual. Section 641(b).

◼ Since SALT limitation applies to individuals, it also applies to estates

and trusts.

❑ Footnote 171 of the Joint Explanatory Statement clarifies that the SALT limitation

applies to trusts

◼ However, the limitation does not apply to taxes incurred by a trust or

estate in carrying one a trade or business or an activity under Section

212

78

BNY Mellon Wealth Management

Surprising Results – 2018 - 2025

❑ Example:

❑ Trust is a simple trust, required to pay its trust accounting income to John.

❑ In 2018 the trust has ordinary income from interest and dividends in the amount of $50,000.

❑ The trust also paid real estate taxes in the amount of $16,000 which are all allocable to trust accounting income. Only $10,000 of the $16,000 expenses are deductible under the SALT limitation.

79

BNY Mellon Wealth Management

Surprising Results – 2018 - 2025

❑ Example:

❑ The DNI of the trust is $40,000 ($50,000 income less $10,000 allowable deduction of real estate taxes).

❑ The trust accounting income is $34,000 ($50,000 income less $16,000 real estate taxes allocated to income).

❑ John receives trust accounting income of $34,000.

❑ The distribution deduction to the trust is $34,000, the lesser of trust accounting income ($34,000) or DNI ($40,000).

❑ The trust is taxed on $5,700 ($50,000 income less $10,000 deductible real estate taxes less $34,000 distribution deduction less $300 exemption).

80

BNY Mellon Wealth Management

Conclusion

◼ New Section 67(g) disallows miscellaneous itemized deductions for

years 2018-2025

◼ This affects estates and trusts

◼ We must determine what estate and trust expenses are “miscellaneous

itemized deductions”

◼ To do so, we must review Sections 641(b), 67(a), 62, 63(d), 67(b),

67(e) and 642(h) of the Internal Revenue Code

◼ In addition, we must be familiar with the final Section 67(e) regulations

◼ The results may be surprising

81

BNY Mellon Wealth Management

Thank You!

82