depreciation and depreciation accounting. copyright © 2006 pearson education canada inc. 6-2...

Post on 20-Dec-2015

214 views

TRANSCRIPT

Depreciation and Depreciation Accounting

Copyright © 2006 Pearson Education Canada Inc. 6-2

• Engineering projects often involve investment in equipment or other assets. These assets lose value, or depreciate, over time.

• The first part of Chapter 6 deals with the concept of depreciation and methods of estimating depreciation.

6.1 Introduction

Copyright © 2006 Pearson Education Canada Inc. 6-3

• Assets depreciate for a variety of reasons:

• Use related physical loss, e.g. tire wear on a car. This type of loss is usually measured as a function of units of production, miles driven, or other measures of use.

• Time related physical loss: e.g., rusting of cars. This type of loss is usually measured in units of time.

• Functional loss : e.g., style changes, changes in safety device requirements. This is usually measured in terms of the function lost.

6.2 Depreciation

Copyright © 2006 Pearson Education Canada Inc. 6-4

• Depreciation models are commonly used to model (estimate) the value of an asset at any point in time.

• The remaining value of an asset may be measured in a number of ways, depending on the circumstances:

6.2.2 Value of an Asset

Copyright © 2006 Pearson Education Canada Inc. 6-5

• Market Value: taken as the value of an asset in the open market, i.e. if it were for sale.

• Since we can only determine the market value by selling the asset, the market value usually refers to an estimate of the market value.

6.2.2 Market Value

Copyright © 2006 Pearson Education Canada Inc. 6-6

• Book value: the value of an asset calculated with a depreciation model for accounting purposes. – This value may be different from the

market value. – There may be several book values given

for the same asset, depending on the purpose. e.g. for taxation vs. shareholder reports.

• The historical cost of the asset is commonly used as its initial book value.

Book Value

Copyright © 2006 Pearson Education Canada Inc. 6-7

• Other terminology:

• Salvage Value: either the actual or estimated value of an asset at the end of its useful life (i.e. when it is sold).

• Scrap value: A special case of Salvage Value. Either the actual or estimated value of an asset at the end of its physical life (when it is broken up for parts, or sold to a recycler).

Value of an Asset

Copyright © 2006 Pearson Education Canada Inc. 6-8

• We need to estimate the value of an asset for a variety of reasons:

• Making managerial decisions: we need to know asset values. e.g., for negotiating a loan.

• Planning purposes: e.g. asset replacement decisions.

• Complying with Tax regulations: The Canadian Government regulates how much depreciation can be claimed on assets.

Why Estimate Asset Values?

Copyright © 2006 Pearson Education Canada Inc. 6-9

• To match the way in which assets depreciate and to meet regulatory requirements, several depreciation models have been developed.

• Two of the most common in Canada are:

• Straight line depreciation – simple, easy to calculate;

• Declining balance depreciation - required by Canadian tax laws.

Depreciation Models

Copyright © 2006 Pearson Education Canada Inc. 6-10

• Straight line depreciation (SLD) assumes that the rate of loss of an asset’s value is constant over its useful life.

– i.e. the value of an asset is linearly decreasing over its useful life.

P = purchase priceS = salvage value at the end of N periods.N = useful life of asset

6.2.3 Straight Line Depreciation

Copyright © 2006 Pearson Education Canada Inc. 6-11

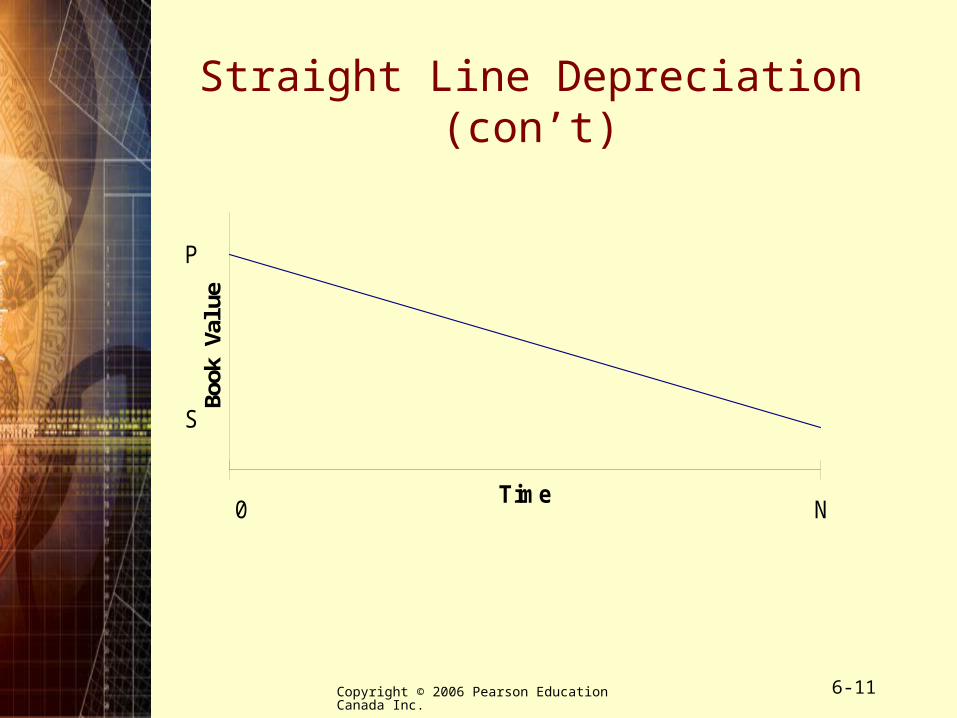

Straight Line Depreciation (con’t)

Time

Boo

k Va

lue

P

S

N0

Copyright © 2006 Pearson Education Canada Inc. 6-12

• Depreciation in period n using SLD:

• Book value of the asset at the end of period n:

• Accumulated Depreciation at the end of period n:

)(N

SPnslD

NSP

nPnBVsl )(

)(

NSP

nnBVP sl

Straight Line Depreciation (con’t)

Copyright © 2006 Pearson Education Canada Inc. 6-13

• An asset was purchased 7 years ago for $10 000. It was estimated to have a 10 year service life and a salvage value of $2000 at the end of its service life.

• If SLD is a good model of asset value, what its book value today?

Example 6-1: (important)

Copyright © 2006 Pearson Education Canada Inc. 6-14

• Given : n = 7, P = $10 000, N = 10, S = $2000

• SLD estimates the book value of the asset at $4400

Example 6-1: Answer

4400. =

800 *7- 000 10 =

102000-000 10

7- 000 10 =

)7(

NSP

nPBVsl

Copyright © 2006 Pearson Education Canada Inc. 6-15

• SLD’s advantage is that it is easy to calculate and understand.

• The main problem with SLD is that many assets do not, in fact, depreciate at a constant rate.

• Thus, market values often differ from book values when SLD is used.

Comments on the Straight Line Depreciation Method:

Copyright © 2006 Pearson Education Canada Inc. 6-16

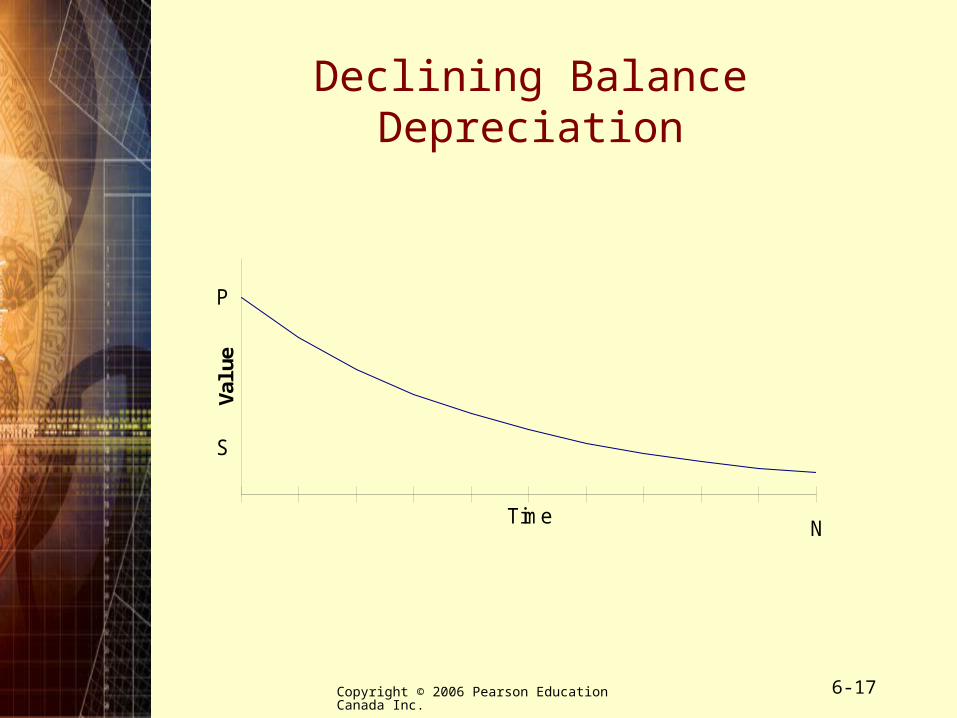

• The declining balance method of depreciation models the loss in value of an asset in a period as a constant proportion of the asset’s current value.

• DBD often matches the decline in value of an asset well.

• DBD must be used for reporting depreciation expenses under Canadian Tax law.

6.2.4 Declining Balance Depreciation

Copyright © 2006 Pearson Education Canada Inc. 6-17

Declining Balance Depreciation

Time

Val

ue

P

S

N

Copyright © 2006 Pearson Education Canada Inc. 6-18

• d = depreciation rate• P = purchase price

• Initial book value:

• Book value at the end of period n using DBD

• Depreciation in period n using DBD

Declining Balance Depreciation

)0( PBVdb

)1()( dnBVnD dbdb

)1()( ndb dPnBV

Copyright © 2006 Pearson Education Canada Inc. 6-19

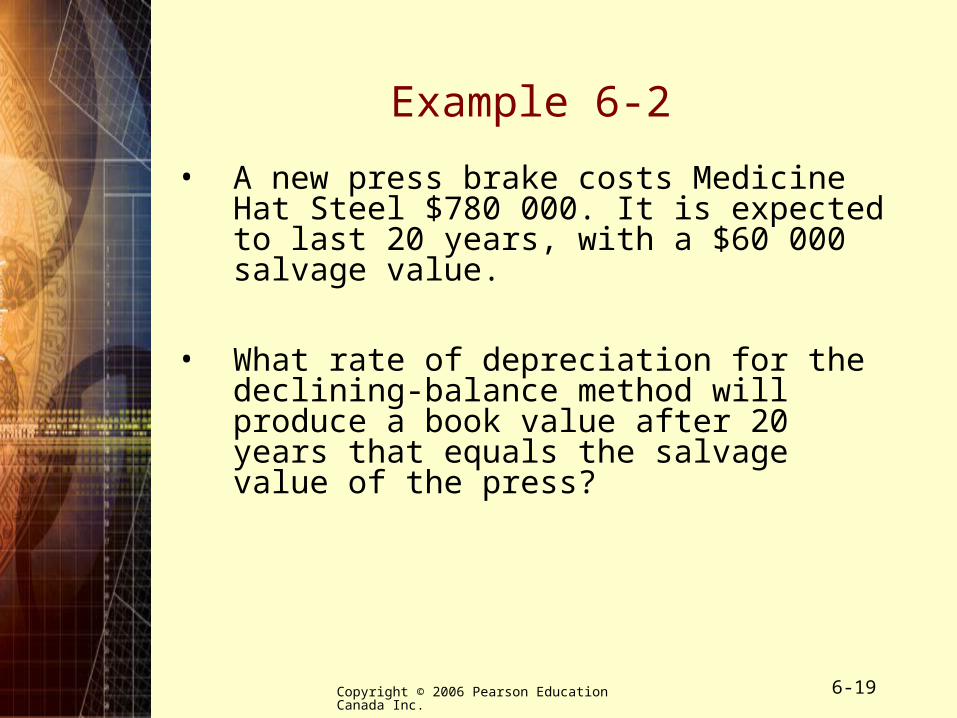

• A new press brake costs Medicine Hat Steel $780 000. It is expected to last 20 years, with a $60 000 salvage value.

• What rate of depreciation for the declining-balance method will produce a book value after 20 years that equals the salvage value of the press?

Example 6-2

Copyright © 2006 Pearson Education Canada Inc. 6-20

• P = $780 000, N = 20 years, S = $60 000

780 000(1 – d)20 = 60 000

(1 – d)20 = 1/13

d = 1 – (1/13)1/20 = 1 – 0.8796 = 0.1204

• A depreciation rate of about 12% will produce a book value in 20 years equal to the salvage value of the press.

Example 6-2: Answer

Copyright © 2006 Pearson Education Canada Inc. 6-21

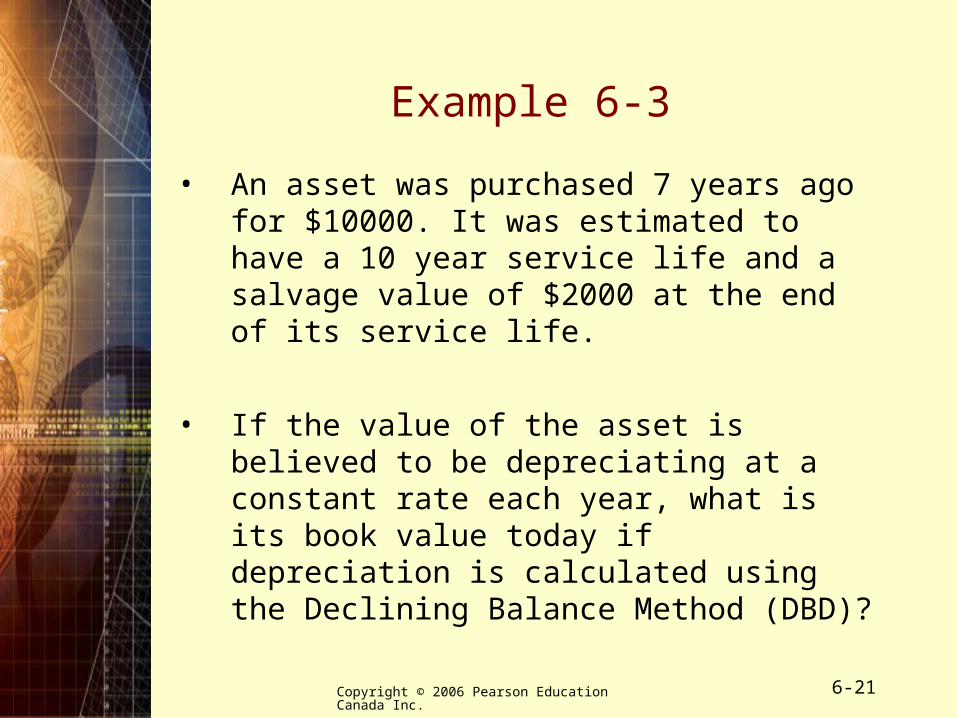

• An asset was purchased 7 years ago for $10000. It was estimated to have a 10 year service life and a salvage value of $2000 at the end of its service life.

• If the value of the asset is believed to be depreciating at a constant rate each year, what is its book value today if depreciation is calculated using the Declining Balance Method (DBD)?

Example 6-3

Copyright © 2006 Pearson Education Canada Inc. 6-22

BVdb(n) = P(1-d)n

BVdb(10) = 10,000(1-d)10 = S

S = 10,000(1-d)10

2000 = 10,000(1-d)10

d = 1- (2000/10000)1/10

d = 0.1487 or 14.87% (approx)

At the end of 7 years:

BVdb(7) = 10,000(1-.1487)7

BVdb(7) = $3240 (approx)

Example 6-3: Answer

Copyright © 2006 Pearson Education Canada Inc. 6-23

• Depreciation and Depreciation Accounting– Reasons for Depreciation– Value of an Asset– Straight Line Depreciation– Declining Balance Depreciation

Summary