deposit soup. deposit soup...e.g., chexsystems, qualifile must have a permissible purpose must send...

TRANSCRIPT

9/25/2017

1

Deposit Soup LEAH M. HAMILTON, JD

COMPLIANCE ADVISOR

CONFIDENTIAL AND PROPRIETARY

WHAT YOU WILL LEARN

Key examiner trends

FCRA reporting

ODP Watch

Freezing deposit accounts

Waiving fees

Tiered rate deposit products

Hot, hot, hot

Sales culture compliance

On the horizon

Regulation CC check collection

Prepaid cards

2

9/25/2017

2

Key examiner trends

3

ACCOUNT OPENING: FCRA

Fair Credit Reporting Act

Huh? This is deposits!

If financial institution requires any credit report or score in relation to opening deposit account, FCRA applies

e.g., ChexSystems, Qualifile

Must have a permissible purpose

Must send FCRA adverse action notice if deposit account opening declined

Modify language in credit adverse action notices

Accuracy and integrity

Dispute information

Must follow FCRA reporting rules if you identify an issue during account opening process

Compliance Bulletin 2016 – 01

The FCRA’s Requirement that Furnishers Establish and Implement Reasonable Written Policies and Procedures Regarding the Accuracy and Integrity of Information Furnished to all Consumer Reporting Agencies

Identity theft

4

9/25/2017

3

OVERDRAFT PROTECTION

Still waiting on CFPB

Will initiate a rulemaking process with goal of developing rules to make overdraft market fairer and more transparent

In the meantime …

What you need to look out for on ODP

5

ODP WATCH

Resurgence of opt-in scrutiny

Disclosures vs. advertising

Brochures highlighted free or low cost accounts appropriate for customers who had previous challenges managing accounts

Omitted information regarding costly features, particularly ODP

Balance marketing and disclosures with downsides of products and services

Timing of consent vs. when fees are charged

Be sure fees are not assessed until after valid consent and confirmation notice sent

Third party risk management

Santander Bank, NA fined $10 million for actions of its ODP telemarketer

Enrolled customers without consent, causing fees to be charged

Misled customers regarding costs and consequences

Failure to exercise appropriate oversight of third party

Prohibitions on use of a service provider to telemarket ODP, employee opt-in targets, incentives or punitive consequences

Ensure thorough due diligence on third parties

Establish complaint management system for third party actions/inactions

6

9/25/2017

4

ODP WATCH

Available balance posting

Preauthorized transactions

Account debit-hold at time of preauthorized transaction

Intervening debit transactions come through further reducing available balance

Preauthorized transaction settled, actual funds no longer available, ODP applied

Unfair practice for charging fee of OD at settlement when there were sufficient funds at authorization

Misleading advertising and disclosures

Know how your system credits/debits available amounts

Available balance vs. ledger balance

Disclosure states available balance when in fact, system calculates based on ledger balance

May not switch methods without change in terms notice

Unfair and abusive practice

Do not allow system calculation changes without change in terms notice

7

ODP WATCH

Overdrawn deposit balance added to existing loans

Customer fails to bring deposit account current

Bank adds OD amount to loan through cross-collateralization clause in loan agreement

Increase loan agreement loan amounts

Misleading and deceptive statements about the amounts owed on the loan

List amounts separately with appropriate nomenclature

Right to cure OD balances

Customer overdraws account; bank charges OD fee and daily continuous fee

Makes a check deposit to cover the OD amount

Apply Regulation CC

Credit immediately – cures the OD

Credit next business day

If check deposited on Friday, and Monday or Tuesday (if Monday holiday) is next business day, OD continuous fee applied for 2-3 days

Remember do not charge OD continuous daily fees for any day that is not a business day

If system set to assess on calendar days, change to business days

8

9/25/2017

5

FREEZING DEPOSIT ACCOUNTS

“Hard holds” to stop all activity due to suspicious activity

No deposits, no withdrawals, hold lasting up to 2 weeks

No such hold in Regulation CC

Reliance on BSA rules

UDAP/UDAAP possible

Freezing “good money”

Causing overdraft fees (both institution and vendor)

Payments and deposits rejected

Use less drastic measures

Consider process similar to Federal Benefit look-back process

Is it one transaction vs. new account with all transactions

Communicate, communicate, communicate

Promptly notify customer

Clearly and consistently explain the situation

Ongoing status

9

A FEW MORE TO WATCH OUT FOR OR REVISIT …

Misrepresentation of monthly service fees

Waiving fees “if qualifications are met”

Deceptive practice if

Make X# of payments from the account per cycle vs. Make X# debit card transactions

Posted, cleared

Know your system and validate against advertisements and disclosures

Regulation E error resolution

Closing an investigation and denying claims because customer failed to provide more documentation than institution needs to make a valid determination

Failure to provide provisional credit

Informing customer that they need to provide a subpoena to review the institution’s Reg E materials relied up to make determination

10

9/25/2017

6

REGULATION DD: TIERED RATE PRODUCTS

Advertisement for tiered rate account that states an APY

must also state the APY for each tier, and

corresponding minimum balance requirements

in close proximity and with equal prominence

Any interest rates stated must appear in conjunction with the applicable APYs for each tier

3.0% APY for balances over

$25,000

11

3.0% APY

for balances over $25,000

METHOD B TIERED-RATE PRODUCTS

Method B is where you pay x interest on different balances

If I have $60,000 in my account, I will earn 1.75% on the first $50k,

Then, I earn a rate of 0.5% on the next $10k

APY for this second tier is a range x% to y%

Tiered-rate Method B model language

An interest rate of .50% will be paid only for that portion of your [daily balance/average daily

balance] that is greater than $50,000.00. The annual percentage yield for this tier will range

from ?% to ?_%, depending on the balance in the account.

An interest rate of __% will be paid only for that portion of your [daily balance/average daily

balance] that is greater than $__. The annual percentage yield for this tier will range from __%

to __%, depending on the balance in the account.

12

9/25/2017

7

METHOD A VS. METHOD B TIERED RATE PRODUCTS

Method A

The rate is specified for each tier

Depending on the balance, rate applies to the entire balance

Tier 1 $0.01-$10,000 1.00%

Tier 2 $10,001-$25,000 2.00%

Tier 3 > $25,001 3.00%

If the balance is $22,500, 2.00% APY applies to the entire balance.

Method B

The rate or range of rates are specified for each tier

Depending on the balance, rate applies to the corresponding balance

Tier 1 $0.01-$10,000 1.00%

Tier 2 $10,001-$25,000 2.00%

Tier 3 > $25,001 3.00%

If the balance is $22,500, 1.00% applies to the first $10,000 and 2.00% applies to the remaining $12,500, which creates a range (1.01% - 2.61% APY)

13

DEPOSIT PRODUCT LIFE CYCLE

UDAP/UDAAP focus

Key Considerations

Product Features

System capabilities

Advertising / Marketing

Disclosures

Training

Engage compliance early in development

Keep compliance engaged

What’s wrong with this picture?

14

9/25/2017

8

Sales Culture Compliance Hot, hot, hot

15

SALES CULTURE COMPLIANCE

Unsafe and unsound banking practices

Impacts both safety and soundness examinations and compliance examinations

Triggering event

Improper sales practices

Opening and manipulation of customer accounts without the customer’s authorization

16

9/25/2017

9

OCC LESSONS LEARNED FROM WF FINDINGS

Findings

OCC did not take timely and efficient supervisory actions after the bank and the OCC identified significant issues with complaint management and sales practices

Untimely and ineffective supervision of complaints and whistleblower cases

Untimely and ineffective supervision of incentive sales program

Ineffective MRA communication and follow-up

Noncompliance with OCC guidance

Unclear supervisory records

Lessons learned (that the OCC must do)

Implement processes to ensure periodic, comprehensive analysis of complaints and whistleblower cases that includes testing, root cause analysis and appropriate follow-up

Ensure effective and timely supervision by improving controls

Ensure institution’s governance processes evaluation systemic root causes of reputational risk reflects shift from moderate to high and take appropriate supervisory action

Ensure effective communication, follow-up and validation of MRAs

Develop enterprise-wide whistleblower process and protocols

Improve collaboration processes between teams on multi-discipline issues

Improve processes to include earlier collaboration outside LOB

Ensure follow-through to effective corrective action

Although lessons learned focused on large bank supervisions, community banks should take note

17

SALES PRACTICE PITFALLS

Culture

High pressure sales

Failure to promote escalation while minimizing issues

Sales performance measurements focus on units for totality

Disproportional regional sales targets

Constant monitoring and ranking of sales performance metrics in competitive manner rather than compliance

Quantity over quality

Vision and values inconsistent with sales strategy

Organizational structure

Inhibit authority and independence of lines of defense

Strong deference to front line management

Lack of compliance authority

Incomplete escalation processes and board reporting

Aggregate view

Looking to individual performance and root cause vs. enterprise-wide

Failure to view customer harm

Failure to connect risk indicators

Failure to recognize, acknowledge or act on trends and correlations

18

9/25/2017

10

SALES CULTURE GOVERNANCE

Accountability

Board

Senior management

Risk management

Human resources

Who is responsible for sales culture compliance and governance?

19

DEPARTMENT OF JUSTICE GUIDANCE

DOJ issued New Corporate Compliance Guidelines

Outlines criteria for the DOJ’s Criminal Division’s Evaluation of Corporate Compliance Programs

11 broad sample topics and questions in checklist format

Not new or novel, but this is the DOJ

Issued just months after WF consent orders published

Sample topics

Analysis and remediation of underlying conduct

Senior and middle management

Compliance autonomy and resources

Policies and procedures

Risk assessment

Training and communication

Confidential reporting and investigation

Incentive and disciplinary measures

Continuous improvement, periodic testing and review

Third party management

Mergers and acquisitions

20

9/25/2017

11

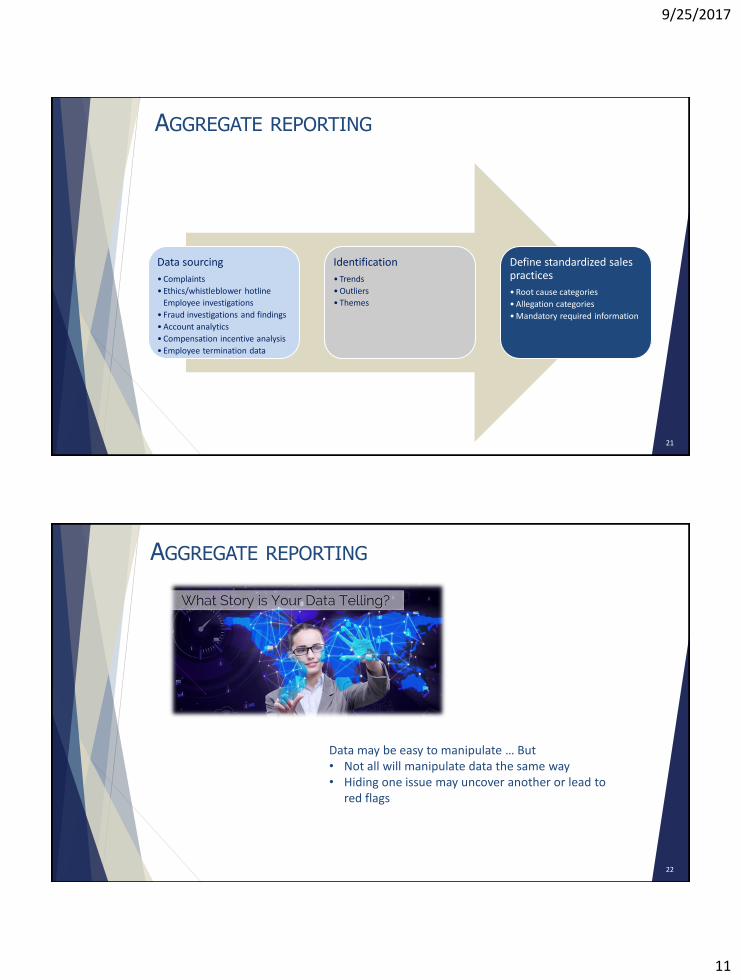

AGGREGATE REPORTING

Data sourcing

• Complaints

• Ethics/whistleblower hotline

Employee investigations

• Fraud investigations and findings

• Account analytics

• Compensation incentive analysis

• Employee termination data

Identification

• Trends

• Outliers

• Themes

Define standardized sales practices

• Root cause categories

• Allegation categories

• Mandatory required information

21

AGGREGATE REPORTING

Data may be easy to manipulate … But • Not all will manipulate data the same way • Hiding one issue may uncover another or lead to

red flags

22

9/25/2017

12

TAKEAWAYS

If the regulators are going to beef up their internal supervisory programs, such processes will have an impact on how thorough they conduct their examinations

Look for gaps in your CMS and sales culture

Add sales culture compliance monitoring and reporting to your schedule

Frequent reporting

Monitor sales incentive pay-outs

Review incentive plans

Not just loan originator compensation plans

Branch and call center incentives

Pay on use vs. opening

Contests, rankings

Whistleblower policy and procedures

Follow through

Reporting

Analytics

Mystery shop high risk areas or rotate to test all areas

23

On the horizon

24

9/25/2017

13

REGULATION CC: PROPOSALS AND FINALS

FRB March 2011 proposal to cover both notices and check collection

http://www.gpo.gov/fdsys/pkg/FR-2011-03-25/pdf/2011-5449.pdf

Under Dodd-Frank, the Reg CC notices section (section B) is now joint with FRB and CFPB

Proposal dragged on and on and on

No changes to the hold notices at this time

FRB proposed check collection amendment in 2014

Final rule issued

Effective date: 7/1/2018

Evolution of largely paper-based check system to one that is virtually all electronic

Creates a framework for electronic check collection and return

Creates new warranties for electronic checks to provide consistency in the warranty chain regardless of the check's form

Parties still may, by mutual agreement, vary the effect of the amendments' provisions as they apply to electronic checks and electronic returned checks

Modify the expeditious-return and notice of nonpayment requirements to create incentives for electronic presentment and return

New proposed FRB rule

Proposed amendments to address situations involving a dispute about whether portions of an electronic check have been altered or whether the item is a forgery

In cases where original paper check is not available, for purposes of determining burden of proof, it would be assumed that the item has been altered rather than forged

Comments were due 8/1/2017

25

REGULATION CC FINAL RULE

Impact

Modifies current check return requirements by requiring that all returned checks, both paper and electronic, be returned by 2:00 p.m. (depositary bank local time) on the second business day following the banking day on which the check was presented to the paying bank and eliminating the “forward collection” option

Adds a condition that the depositary bank must have arrangements to accept returned checks electronically in order to make a claim for damages due to a late return

If a paying bank determines not to pay a check in the amount of $5000 or more (increased from $2500), it must provide a notice of nonpayment such that the notice would normally be received by the depositary bank not later than 2 p.m. (depositary bank local time) on the second business day following the banking day on which the check was presented to the paying bank

Revised the content of the notice of nonpayment

Revised the notice in lieu of return with clarification that the account number of the depositing customer, the branch name or number of the depositary bank from its indorsement, and the name of the paying bank is not required

Clarifying examples of when notice in lieu of return is permissible

Applies return requirements to electronic images of checks, including images that are not derived from a paper check (i.e., electronically-created items)

Creates new indemnities for losses caused by unauthorized or duplicate electronically-created items

Adds new indemnity that indemnifies a depositary bank that received a deposit of an original paper check if the item is returned unpaid after being deposited using a remote deposit capture service

26

9/25/2017

14

PREPAID CARD RULE

Effective date of 10/1/2017 delayed to 4/1/2018

10/31/2018 submission deadline to submit agreements to CFPB unchanged

Broad scope

Regulation E to cover “prepaid accounts”

Regulation Z to treat overdrafts on prepaid cards as credit cards

Special pre-acquisition disclosures

Alternative disclosure to periodic statements

Greater error resolution rights for “registered cards” when customer has completed ID verification

60-day period begins when consumer access electronic account history reflecting the error or when written history sent to consumer

How is your system going to track this?

Alternative is to limit rights by giving consumer 120-day period to report errors after error occurs

Unregistered cards still have protections

Account agreements posted publicly and submitted to CFPB

If required to submit to CFPB, must publicly post agreement or provide copy to consumer within 5 business days of consumer request

Special rule for remittances funded by prepaid account

27

Questions?

28