demand, supply and price of copper – an …s3.amazonaws.com/zanran_storage/ supply and price of...

TRANSCRIPT

Demand, supply and price of copper – an exploration perspective

Eric Finlayson

Head of Exploration

Global Mining Investment Conference

London, September 30, 2009

Demand, supply and price of copper – an exploration perspective 2

This presentation has been prepared by Rio Tinto plc and Rio Tinto Limited (“Rio Tinto”) and consisting of the slides for a presentation concerning Rio Tinto. By reviewing/attending this presentation you agree to be bound by the following conditions.

Forward-Looking Statements

This presentation includes forward-looking statements. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding Rio Tinto’s financial position, business strategy, plans and objectives of management for future operations (including development plans and objectives relating to Rio Tinto’s products, production forecasts and reserve and resource positions), are forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Rio Tinto, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements.

Such forward-looking statements are based on numerous assumptions regarding Rio Tinto’s present and future business strategies and the environment in which Rio Tinto will operate in the future. Among the important factors that could cause Rio Tinto’s actual results, performance or achievements to differ materially from those in the forward-looking statements include, among others, levels of actual production during any period, levels of demand and market prices, the ability to produce and transport products profitably, the impact of foreign currency exchange rates on market prices and operating costs, operational problems, political uncertainty and economic conditions in relevant areas of the world, the actions of competitors, activities by governmental authorities such as changes in taxation or regulation and such other risk factors identified in Rio Tinto's most recent Annual Report on Form 20-F filed with the United States Securities and Exchange Commission (the "SEC") or Form 6-Ks furnished to the SEC. Forward-looking statements should, therefore, be construed in light of such risk factors and undue reliance should not be placed on forward-looking statements. These forward-looking statements speak only as of the date of this presentation.

Nothing in this presentation should be interpreted to mean that future earnings per share of Rio Tinto plc or Rio Tinto Limited will necessarily match or exceed its historical published earnings per share.

Cautionary Statement

Demand, supply and price of copper – an exploration perspective 3

1313141717192021222425262731

3841

7882

98160

0 50 100 150

Anglogold AshantiTeck Cominco

ImpalaENRC

ChalcoNewmont

NorilskAnglo Platinum

MosaicSouthern Copper

FreeportPotash Corp

GoldcorpBarrick Gold

XstrataAnglo American

Rio TintoShenhua

ValeBHP Billiton

Market capitalisation of major listed mining companies

(US$ billion)

At 1 September 09

Source: Thomson Datastream

Rio Tinto – Gross asset distribution (2008)

US, 11%Europe, 13%

Canada, 34%

Other, 7%

Australia, 35%

Demand, supply and price of copper – an exploration perspective 4

Rio Tinto – a world leader in mining

Aluminium Copper Iron Ore

Diamonds Energy Industrial Minerals

Demand, supply and price of copper – an exploration perspective 5

Key drivers for long term commodity demand growth remain intact

Sources: Global Insight, CIA Factbook

Urbanisation rates across Asia, the United States and European Union

United States

Japan

India

EU15

0

20

40

60

80

100

0 10,000 20,000 30,000 40,000 50,000

GDP per capita (US$ at PPP rates in 2006 terms)

Urb

anis

atio

n ra

te (p

erce

nt)

National averages

Chinese provinces

Urbanisation rates, income and population

Note: Size of bubble reflects total population

China

Demand, supply and price of copper – an exploration perspective 6

Sources: 1900-1928 McGraw Hill (1931), 1929-2008 CRU

Global copper consumption

• Compound Annual Growth Rate (CAGR) in demand over the last 108 years is ~ 3.4%

• China overtook the US in 2003 as the largest consumer of copper

• The proportion of global copper consumed in China will grow as per capita consumption increases

Consumption in millions of tonnes per annum

0

5

10

15

20

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

2000

Demand, supply and price of copper – an exploration perspective 7

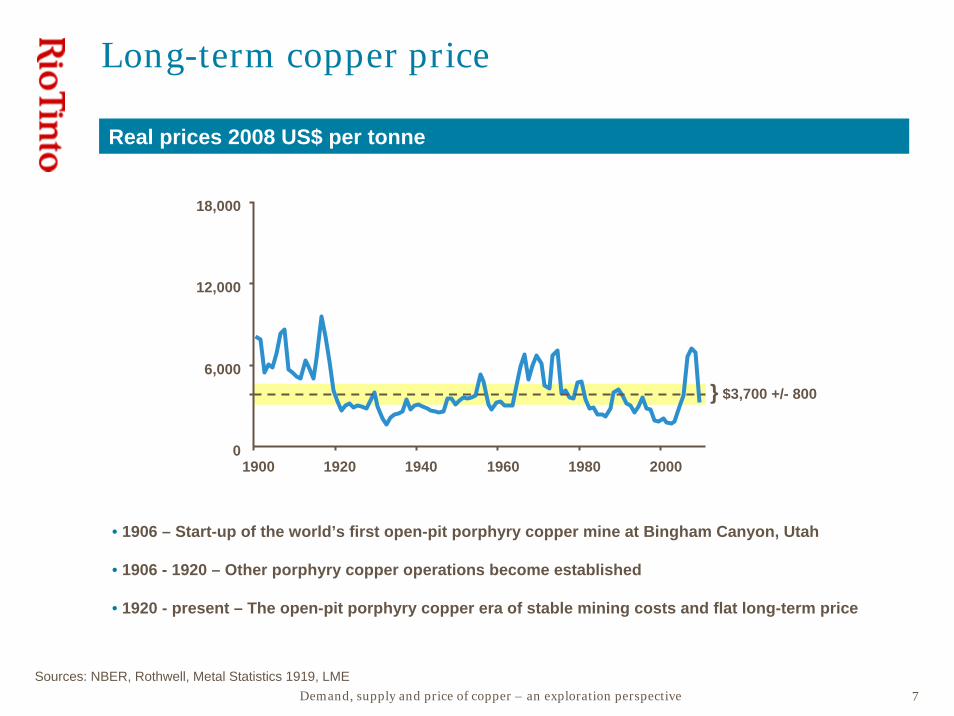

Sources: NBER, Rothwell, Metal Statistics 1919, LME

Real prices 2008 US$ per tonne

Long-term copper price

• 1906 – Start-up of the world’s first open-pit porphyry copper mine at Bingham Canyon, Utah

• 1906 - 1920 – Other porphyry copper operations become established

• 1920 - present – The open-pit porphyry copper era of stable mining costs and flat long-term price

0

6,000

12,000

18,000

1900 1920 1940 1960 1980 2000

$3,700 +/- 800}

Demand, supply and price of copper – an exploration perspective 8

Source: CRU

Production is dominated by a few operations

Grasberg/Ertsberg

Collahuasi

> 250 Other Mines

Bingham CanyonLos Bronces

AndinaBatu Hijau

MorenciCerro Verde

Antamina

Los Pelambres

Norilsk

El Teniente

Codelco Norte

Escondida

Contribution of copper mines to global copper production (2009f)

Demand, supply and price of copper – an exploration perspective 9

Source: MEG

Distribution of copper reserves and resources

•Total reserves + resources – 1.8Bt contained copper in 953 deposits•Global average grade is 0.55% copper

10%4% China

5%Australia34%

Peru

4% Mexico

3% Canada 3% Russia

3% Mongolia

3% Zambia

Others 10%3% Indonesia

2%

2%

2%

2%

2%

Philippines

KazakhstanPoland

DRC

Argentina

8%

Chile

US

Demand, supply and price of copper – an exploration perspective 10

0.770.70

0.97

0.78

1996 2000 2004 2008

24 25

45

27

1996 2000 2004 2008

Global copper reserves - years of production Average reserve grade - % copper

Source: Brook Hunt

Global copper reserves and grades are falling

• Data for 217 mines and projects

• Reserves are being mined faster than they are being replaced

• Resource conversion is falling behind production or is focusing on the high-grade parts of deposits

• Selective conversion and mining of high-grade is an unsustainable practice

Demand, supply and price of copper – an exploration perspective 11

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

100,000,000

Kam

oto

JVK

onko

laTe

nke

Fung

urum

eG

logo

wN

kana

Cha

mbi

shi

KG

HM

Mt I

saO

lym

pic

Dam

Ayn

akU

doka

nsko

eG

aisk

y C

ompl

exTi

ntay

aA

ntam

ina

Gra

sber

gE

l Ten

ient

eZh

ezka

zgan

Com

plex

Col

lahu

asi

And

ina

Div

isio

nE

scon

dida

Sal

obo

Lum

wan

aC

huqu

icam

ata

Sar

ches

hmeh

Sun

gun

Los

Pel

ambr

esR

adom

iro T

omic

Que

llave

coS

alva

dor D

ivis

ion

Rio

Bla

nco

Esp

eran

zaTo

rom

ocho

Cua

jone

Los

Bro

nces

Alm

alyk

Com

plex

Oyu

Tol

goi

Agu

a R

ica

Ray

Com

plex

Bin

gham

Can

yon

Dex

ing

Com

plex

San

to T

omas

Que

brad

a B

lanc

aE

l Abr

aG

aby

Bal

khas

h C

ompl

exM

onyw

aB

atu

Hija

uB

or B

asin

Saf

ford

Cer

ro V

erde

Toqu

epal

aC

anan

eaB

agda

dM

oren

ciS

ierri

taLa

Car

idad

Con

tain

ed C

u

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Cu

Gra

de (%

)

Sources: MEG; FCX 2008 Form 10-K

Mined grades will continue to fall

Reserves – Deposits with >4Mt contained copper Resources – Deposits with >4Mt contained copper

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

100,000,000

T intaya

Konkola Nor th

Tenke Fung urumKamoto JVNkanaRe solu tionLim amayo

Lo s Su lfatos

W ind y Cra ggy

Zhezka zga n CompleKonkolaOyu To lgoi

M t Isa

Yulong

La s Bambas

Qulo ngAntam ina

O lymp ic DamCo lla huas i

K alum bilaJunin

Lo okout Hill

Sungu n

Ce rro C oloradNokom isPanan tza

A ndina D iv isio

San Manue l Div isioLumw anaTampakan

Tuw u-YandonE l Pachon

Fried a RiveEscondid a

M irad orGra sbe rg

Lo s Azules

Santa Cru z

Rio B lanco

Lo s Pe lam bres

Ak-Sug

E l A rcoE l Ten iente

La G ranjaPetaquilla

Que brad a Blan cRe ko D iq

Ch uquicam ata

Galo re Cre ekSafford

E rdm in SxewGale no

B ingham CanyoQue lla veco

Co bre de S ono r

We stern Coppe

Tok i C lu ster

Le tpa daung

B alkhash C omple

A lma lyk C omple

S ierra Go rda

Lo s Bronces

ToromochoA idarlyE l Abra

Salvador D

iv isio

V izcach itasA gua Rica

PebbleE spe ran za

Bor BasinGab y

Santo TomasMonywa

Ce rro Verd eB agda dMore nci

S ierritaBatu H ijau

Zangezu r

Cont

aine

d C

u

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Cu G

rade

(%)

Weighted average grade: 0.88% copper

Total contained copper: 457Mt

Weighted average grade: 0.68% copper

Total contained copper: 909Mt

Demand, supply and price of copper – an exploration perspective 12

0

10

20

30

40

50

60

190

6

1910

1914

1918

192

2

192

6

193

0

193

4

193

8

194

2

194

6

195

0

195

4

195

8

196

2

196

6

1970

1974

1978

198

2

198

6

199

0

199

4

199

8

20

02

20

06

Mil

lio

ns

Met

ric

To

nn

es

Ore Mined

View of the open pit

• Tier 1 deposits – the largest and highest quality in the world – are geologically rare and confer sustainable competitive advantage

• They grow with exploration and commonly have other Tier 1 deposits nearby

• Their capacity to support production expansions delivers optionality and value growth

• Output from these deposits dominates global copper production

The challenge for exploration – discovery of new Tier 1 copper deposits

Production by year 1906 - 2008

Bingham Canyon, USA

Demand, supply and price of copper – an exploration perspective 13

Date Name Commodity Country Date Name Commodity Country

1947 Lac Allard Ilmenite Canada 2000 Potasio Rio Colorado Potash Argentina

1952 Weipa Bauxite Australia 2002 Resolution Copper USA

1962 Tom Price Iron Ore Australia 2004 Simandou Iron Ore Guinea

1963 Kirka Borates Turkey 2005 La Granja Copper Peru

1971 Paragominas Bauxite Brazil 2009 Jadar Borates Serbia

1965 Panguna Copper PNG 2005 Caliwingina Iron Ore Australia

1967 Ok Tedi Copper PNG 2008 Sulawesi Nickel Indonesia

1968 Rossing Uranium Namibia 2008 Mutamba Ilmenite Mozambique

1979 Argyle Diamond Australia

1982 Kaltim Prima Coal Indonesia

1983 Lihir Gold PNG

1985 QMM Ilmenite Madagascar

1990 Century Zinc Australia

1991 Corumba Iron Ore Brazil

1994 Diavik Diamond Canada

1995 Orissa Iron Ore India

In evaluation

In operation

Divested/suspended

Rio Tinto Tier 1 discoveries

• A discovery is a deposit handed over to a Product Group pre-feasibility study team

Demand, supply and price of copper – an exploration perspective 14

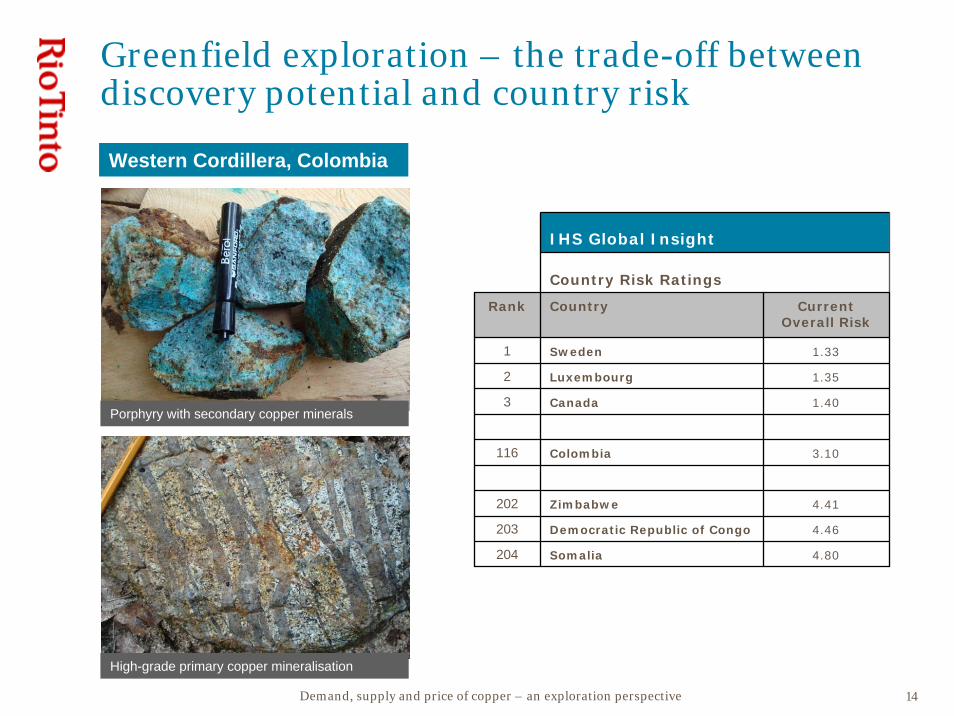

Greenfield exploration – the trade-off between discovery potential and country risk

Porphyry with secondary copper minerals

High-grade primary copper mineralisation

IHS Global Insight

Country Risk Ratings

Rank Country CurrentOverall Risk

1 Sweden 1.33

2 Luxembourg 1.35

3 Canada 1.40

116 Colombia 3.10

202 Zimbabwe 4.41

203 Democratic Republic of Congo 4.46

204 Somalia 4.80

Western Cordillera, Colombia

Demand, supply and price of copper – an exploration perspective 15

-200

0

200

400

600

800

1000

1200

14001850 1870 1890 1910 1930 1950 1970 1990 2010

Approximate year of discovery

App

roxi

mat

e de

pth

to to

p of

dep

osit

Copper discoveries showing depth of deposits with >4Mt contained copper

Deeper discoveries are starting to appear

Resolution

Hugo Dummett

Pebble East

Heruga

Kalamazoo

EscondidaGrasberg

Chuquicamata

El Teniente Andina

Olympic Dam

Los Sulfatos

Source: MEG

Demand, supply and price of copper – an exploration perspective 16

• Deep Molybdenum Zone to date only partially delineated by drilling (D664 only recently completed)

• Annular body of mineralisation extending >2,000m downwards beneath current open pit

• Current Exploration Target of 500-600Mt @ 0.1 – 0.15% Mo (pre-D664) is likely to significantly expand with further drilling

Bingham Canyon – Deep Molybdenum Zone

Brownfield exploration – high potential for discovery in an established operating environment

Demand, supply and price of copper – an exploration perspective 17

Bingham Canyon – an emerging mineral district

Bingham Canyon – tip of the iceberg

• New geophysical data have traced the Bingham Canyon ore body to depth

• Nearby unroofed intrusions identified for 2009/2010 drilling

• Potential for additional major discoveries within the Bingham Canyon mineral district

Demand, supply and price of copper – an exploration perspective 18

Notes: 1 - Existing mines and funded projects

Source: Brook Hunt

Increasing depth . . . . . . means higher mining costs?

Underground production1 - % of global production Average 2007 C1 composite costs - (c/lb)

26%

40%

2008 2025

63

102

Open Pit Underground

Copper mining methods and costs

Demand, supply and price of copper – an exploration perspective 19

Cu >0.75% drill intercepts

Technology and innovation – unlocking the value of lower-grade mineral deposits

View looking south

La Granja, Peru

• 2,770Mt @ 0.51% Cu, 0.1% Zn

• Deposit remains open

• Amenable to dump leaching of copper and zinc

• Major new mineralised porphyry found immediately to the north-west – currently under evaluation

Demand, supply and price of copper – an exploration perspective 20

Source: MEG

Global exploration expenditures

• Cyclicity of exploration spend is normal

• The current economic downturn will have no lasting impact on copper exploration & development

0

2

4

6

8

10

12

14

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

US$

(bill

ions

)

Demand, supply and price of copper – an exploration perspective 21

• Global copper reserves and resources are sufficient for several decades. Ongoing exploration will continue to deliver new resources

• Reserve and resource grades are progressively declining due to depletion of supergene-enrichment blankets in the major producing districts

• Greenfield exploration in under-explored countries offers some potential to reverse this trend through new surface copper discoveries. However, the full potential of these countries to support major production may be undermined by sovereign risk factors

• Deeper discoveries are appearing in known districts as we explore around surface deposits. Some of these brownfield discoveries have unusually high copper and by-product grades

• Innovation in mining and processing technology may reduce the costs of production from lower-grade surface resources

• Given forecast future demand, future copper prices will depend on the relative success of greenfield discovery, brownfield discovery and innovation in mining and processing

Summary