deloitte powerpoint template - ctconline.org - ca n. c... · ca n.c. hegde 16 january 2016. ... •...

TRANSCRIPT

1

Capital GainsDeeming Fictions Under

Capital Gains – Section 50,

Section 50B, Section 50C and

Section 50D of the Act

CA N.C. Hegde

16 January 2016

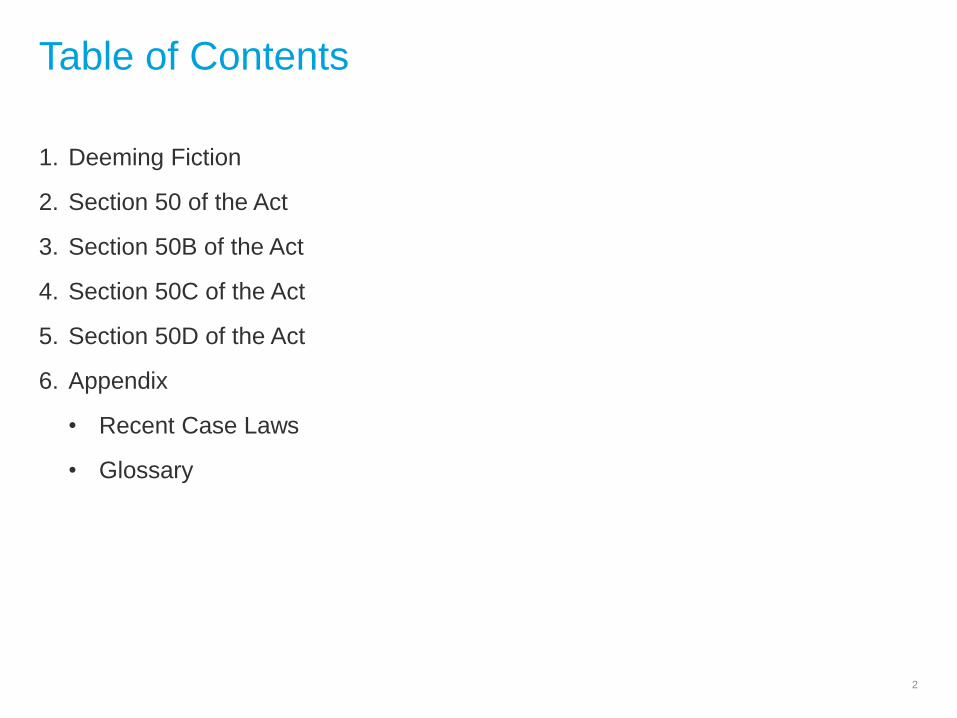

Table of Contents

1. Deeming Fiction

2. Section 50 of the Act

3. Section 50B of the Act

4. Section 50C of the Act

5. Section 50D of the Act

6. Appendix

• Recent Case Laws

• Glossary

2

Deeming Fiction

3

Interpretation of Certain Specific Provisions

Deeming Provisions and Legal Fictions

4

The word “deemed” is intended to

enlarge the meaning of a

particular word - the matter

included may or may not fall

within the provision

It includes, what is

obvious, uncertain

and in the ordinary

sense, impossible

A legal fiction is normally

to be given full effect and

carried to its logical

conclusion - It should

therefore be extended to

the consequences and

incidents that follow

However, legal fiction should

operate only within the filed of

the definite purpose for which

the fiction is created - It should

not be so interpreted to create

injustice

East End Dwellings Co. Ltd. v. Finsbury Borough Council [1952] AC 109 - The statute says that you

must imagine a certain state of affairs. It does not say that having done so, you must cause or permit

your imagination to boggle when it comes to the inevitable corollaries of that state of affairs

Section 50 of the Act

5

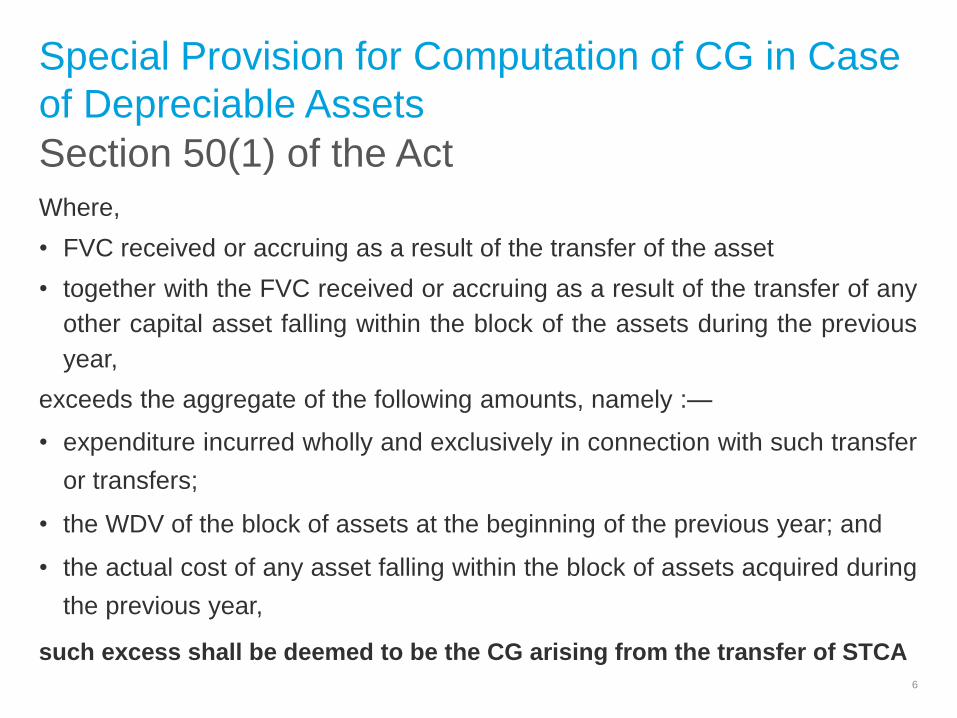

Section 50(1) of the Act

Special Provision for Computation of CG in Case

of Depreciable Assets

6

Where,

• FVC received or accruing as a result of the transfer of the asset

• together with the FVC received or accruing as a result of the transfer of any

other capital asset falling within the block of the assets during the previous

year,

exceeds the aggregate of the following amounts, namely :—

• expenditure incurred wholly and exclusively in connection with such transfer

or transfers;

• the WDV of the block of assets at the beginning of the previous year; and

• the actual cost of any asset falling within the block of assets acquired during

the previous year,

such excess shall be deemed to be the CG arising from the transfer of STCA

Section 50(2) of the Act

Special Provision for Computation of CG in Case

of Depreciable Assets

7

Where,

• any block of assets ceases to exist - for the reason that all the assets in

that block are transferred during the previous year,

the COA of the block of assets shall be

• the WDV of the block of assets at the beginning of the previous year,

• as increased by the actual cost of any asset falling within that block of

assets, acquired during the previous year

and the income received or accruing as a result of such transfer or transfers

shall be deemed to be the CG arising from the transfer of STCA

Section 50 of the Act

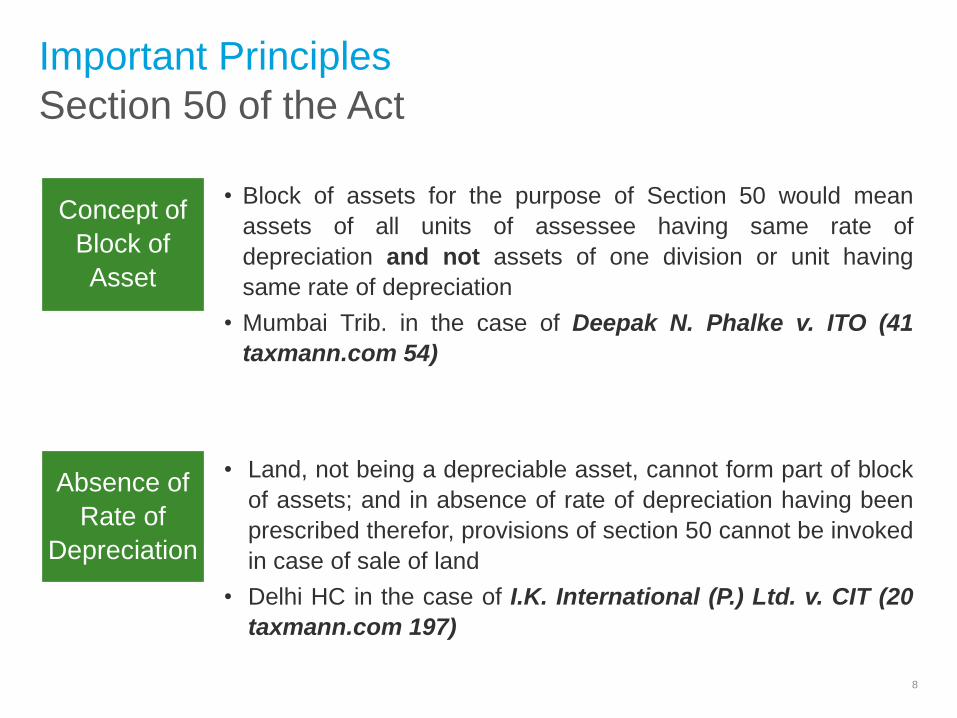

Important Principles

8

Concept of

Block of

Asset

Absence of

Rate of

Depreciation

• Land, not being a depreciable asset, cannot form part of block

of assets; and in absence of rate of depreciation having been

prescribed therefor, provisions of section 50 cannot be invoked

in case of sale of land

• Delhi HC in the case of I.K. International (P.) Ltd. v. CIT (20

taxmann.com 197)

• Block of assets for the purpose of Section 50 would mean

assets of all units of assessee having same rate of

depreciation and not assets of one division or unit having

same rate of depreciation

• Mumbai Trib. in the case of Deepak N. Phalke v. ITO (41

taxmann.com 54)

Section 50 of the Act

Important Principles

9

When to

Invoke?

• To invoke Section 50, it is necessary that the twin conditions

mentioned therein be fulfilled:

o Capital asset should be an asset forming part of block of

assets

o Depreciation should have been allowed on it under the Act

• Gujarat HC in the case of Parikh Transport Co. v. ITO (55

taxmann.com 287)

• Mumbai Trib. in the case of Divine Construction Co. v. ACIT

(16 taxmann.com 236)

Section 50 of the Act

Important Principles

10

Bifurcation

Possible?

• Set off against LTCG

• Bombay HC in the case of CIT v Manali Investments Limited

(39 taxmann.com 4)

• Rate of tax to be applied

• Mumbai Trib. In the case of Smita Conductors (152 ITD 417)

• Bifurcation of land and building into separate part for the

purpose of CG is permissible

• Section 50 does not convert LTCA into STCA

• Bombay HC in the case of Cadbury India Ltd. V. CIT (53

taxmann.com 227) based on the view taken by the Bombay

HC in ACE Builders (281 ITR 210)

No deeming

fiction

beyond

section 48

and 49?

Section 50 of the Act

Important Principles

11

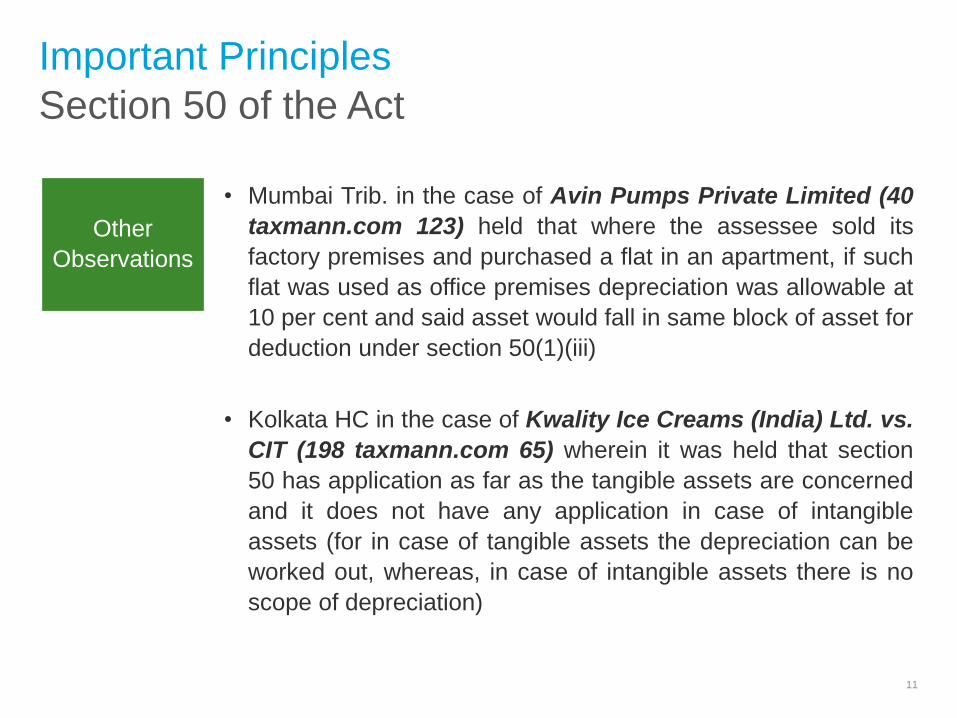

Other

Observations

• Mumbai Trib. in the case of Avin Pumps Private Limited (40

taxmann.com 123) held that where the assessee sold its

factory premises and purchased a flat in an apartment, if such

flat was used as office premises depreciation was allowable at

10 per cent and said asset would fall in same block of asset for

deduction under section 50(1)(iii)

• Kolkata HC in the case of Kwality Ice Creams (India) Ltd. vs.

CIT (198 taxmann.com 65) wherein it was held that section

50 has application as far as the tangible assets are concerned

and it does not have any application in case of intangible

assets (for in case of tangible assets the depreciation can be

worked out, whereas, in case of intangible assets there is no

scope of depreciation)

Section 50 of the Act

Important Principles

12

Value of

consideration

Impact of

section 50 C

• What happens in a situation where section 50 and 50 C are

both applicable.

• Special Bench of the Mumbai tribunal in United Marine

Academy( 130 ITD 113)

There are two different fictions created into two different

provisions and going by the legislative intentions to create the

said fictions, the same operate in different fields. Harmonious

interpretation of the provisions makes it clear that there is no

exclusion of applicability of one fiction in a case where other

fiction is applicable - there is no conflict between these two

legal fictions.

• However the ITAT in Bhaidas Cursondas & Company vs.

ACIT (Mum - Trib)( 59 Taxmann.com 373) has held that this

is limited to situations where capital gains need to be

computed.

Section 50B of the Act

13

Section 50B of the Act

Special Provision for Computation of CG in Case

of Slump Sale

• Profits or gains arising from the slump sale

• effected in the previous year

• shall be chargeable to income-tax as CG arising from the transfer of LTCA and

shall be deemed to be the income of the previous year in which the transfer took

place

• Provided that any profits or gains arising from the transfer under the slump sale

of any capital asset being one or more undertakings owned and held by an

assessee for not more than thirty-six months immediately preceding the date of

its transfer shall be deemed to be the capital gains arising from the transfer of

STCA

• SC in PNB Finance vs. CIT (175 Taxman 242)

14

Definitions for Section 50B

Slump Sale

• Section 2(42C) - Slump sale means

o the transfer of one or more undertakings;

o as a result of the sale;

o for a lump sum consideration;

o without values being assigned to the individual assets and liabilities in such

o sales

• Undertaking includes any part of an undertaking, or a unit or division of an undertaking or a business activity taken as a whole” but does not include "individual assets or liabilities or any combination thereof not constituting a business activity”

• Determination of the value of an asset or liability for the sole purpose of payment of stamp duty, registration fees or other similar taxes or fees shall not be regarded as assignment of values to individual assets or liabilities

15

Computation Under Section 50B

Slump Sale

16

Capital Gains – Section 48 r.w. Section 50B

Particulars Amount (in INR)

Full value of consideration (FVC) 100

Less: Net worth of undertaking 75

Taxable Capital Gains 25

Net Worth – Explanation 1 and 2 to Section 50B

Particulars Amount (in INR)

Income-tax WDV of depreciable assets 50

Add: Book value of non-depreciable assets

(excluding revaluation)

100

Total 150

Less: Book value of liabilities (excluding revaluation) 75

Net Worth 75

Section 50B of the Act

Slump Sale

• Profit on slump sale will have to be included in book profit for MAT purposes

• Unlike demergers / mergers, slump sale is not subject to approval from HC

• No enabling provision for transfer of losses / unabsorbed depreciation to

purchaser

17

Section 50B of the Act

Important Principles

18

Does Sale

Include

Exchange?

• Slump sale is for lump sum consideration

• It is nothing but a transfer of a whole or a part business

• For slump sale, transfer has to be by way of sale

• The Bombay HC in the case of Bharat Bijlee Limited vs. CIT

(46 taxmann.com 257) upheld the decision of the Mumbai

tribunal that the transfer of a business undertaking as a going

concern against bonds/ preference shares issued was not a

sale, but an exchange – therefore, Section 2(42C) and Section

50B of the Act relating to the computation of the capital gains

were not applicable to such a transfer

• The Delhi HC ruling of SREI Infrastructure Finance Limited

(Writ petition no. 1592 of 2012), was distinguished as the

consideration was in terms of money and shares, and the

transfer could therefore be not termed as exchange

Section 50B of the Act

Important Principles

19

If Separate

Deeds

Entered?

• Sale of trademarks, assets, technical know-how, copyrights

and goodwill pertaining to business being carried out by

assessee; if found to be part of one transaction - would be a

slump sale

• Mumbai Trib. in the case of Mahindra Engineering &

Chemical Products Ltd. V. ITO (20 taxmann.com)

Section 50B of the Act

Important Principles

20

Concept of

Negative

Networth

• Negative net worth cannot be considered as NIL – it has to be

added to the sale consideration

• Mumbai Trib. in the case of DCIT v. Summit Securities Ltd.

(135 ITD 99)

Sale Consideration 100 100 100

Net Worth Calculation

Depreciable Assets 20 20 20

Book Value – Other Assets 30 30 30

Total Assets 50 50 50

Book Value – Liabilities 30 80 80

Net Worth 20 (30) -

Capital Gains 80 130 100

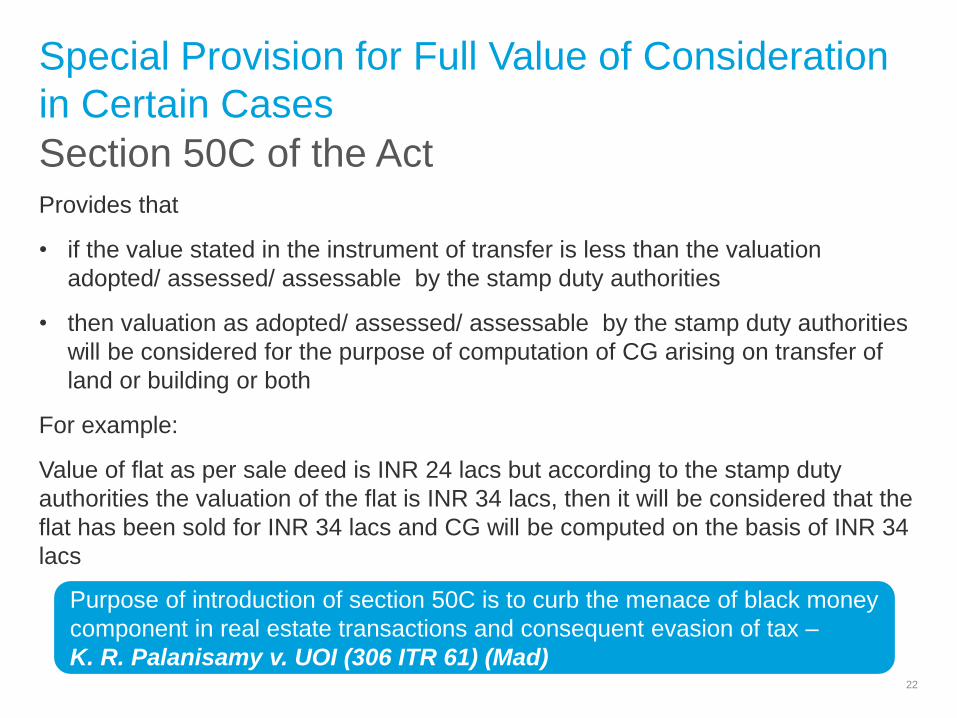

Section 50C of the Act

21

Section 50C of the Act

Special Provision for Full Value of Consideration

in Certain Cases

Provides that

• if the value stated in the instrument of transfer is less than the valuation

adopted/ assessed/ assessable by the stamp duty authorities

• then valuation as adopted/ assessed/ assessable by the stamp duty authorities

will be considered for the purpose of computation of CG arising on transfer of

land or building or both

For example:

Value of flat as per sale deed is INR 24 lacs but according to the stamp duty

authorities the valuation of the flat is INR 34 lacs, then it will be considered that the

flat has been sold for INR 34 lacs and CG will be computed on the basis of INR 34

lacs

22

Purpose of introduction of section 50C is to curb the menace of black money

component in real estate transactions and consequent evasion of tax –

K. R. Palanisamy v. UOI (306 ITR 61) (Mad)

Section 50C of the Act

Important Principles

23

Valuation

When

Challenged

• Valuation of capital asset should be done under section 50C(2)

of the Act, when taxpayer makes an objection to adopt the

market value under section 50C(1) of the Act

• Madras HC in the case of Appadurai Vijayaraghavan vs.

JCIT (369 ITR 486).

• The Madras HC in the case of N. Meenakshi v. ACIT [2010]

326 ITR 229 held that once the assessee applies to AO for

making reference to the DVO under section 50C, "may"

becomes "shall“

• The valuation by the DVO is required to avoid miscarriage of

justice – AO duty bound even when no prayer made

• Mumbai Trib. in the case of Reshma Daryanani vs. ITO -

(166 TTJ 22) and Sunil Kumar Agarwal .v. CIT (372 IT 83)

• In the case of Jitendra Mohan Saxena (117 TTJ 974), held

that both the remedies under section 50C are alternative.

Challenge the guideline value before the AO only if he has not

challenged the same before stamp valuation authority – Also

Mohd. Shoib v. Dy. CIT (127 TTJ 459)

Section 50C of the Act

Important Principles

24

Variation

Applicability

• Consideration received on sale of a capital asset by stamp

duty valuation is applicable only in case of a seller

• Gujarat HC in the case of CIT vs. Sarjan Realities Ltd. (20

taxman 112)

• If difference between valuation for the purpose of stamp

duty and the sale consideration actually received by the

assessee is 10% or less, then the value actually received by

the assessee should be adopted for the purpose of computing

LTCG

• Kolkata Trib. in the case of M/s LGW Limited vs. I.T.O. (ITA

No. 267/Kol/2013) keeping in view the decision of the Hyd.

Trib. in ACIT vs. Suvarna Rekha (ITA No.743/Hyd/2009)

• Pune Trib. in the case of Rahul Construction Co. vs. ITO (51

SOT 192)

Section 50C of the Act

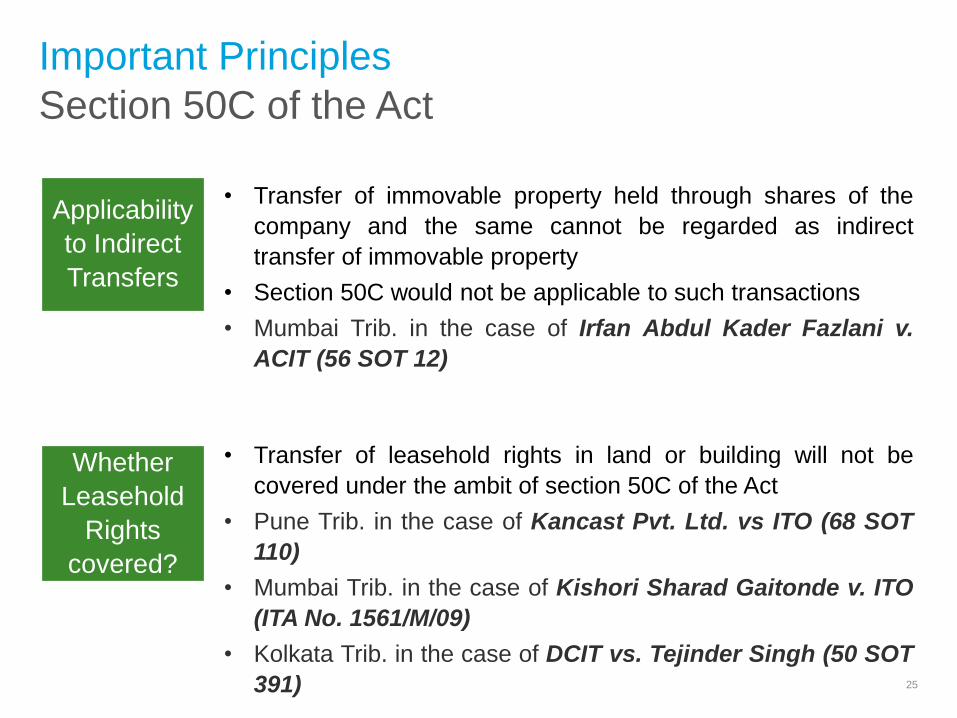

Important Principles

25

Applicability

to Indirect

Transfers

Whether

Leasehold

Rights

covered?

• Transfer of leasehold rights in land or building will not be

covered under the ambit of section 50C of the Act

• Pune Trib. in the case of Kancast Pvt. Ltd. vs ITO (68 SOT

110)

• Mumbai Trib. in the case of Kishori Sharad Gaitonde v. ITO

(ITA No. 1561/M/09)

• Kolkata Trib. in the case of DCIT vs. Tejinder Singh (50 SOT

391)

• Transfer of immovable property held through shares of the

company and the same cannot be regarded as indirect

transfer of immovable property

• Section 50C would not be applicable to such transactions

• Mumbai Trib. in the case of Irfan Abdul Kader Fazlani v.

ACIT (56 SOT 12)

Section 50C of the Act

Important Principles

26

Exemptions

Under

Section 54

• While computing exemption under section 54, actual sale

consideration is to be taken into consideration and not the

stamp duty valuation under section 50C of the Act

• Jaipur Trib. in the case of Nand Lal Sharma vs. ITO (61

taxmann.com 271)

Section 50C of the Act

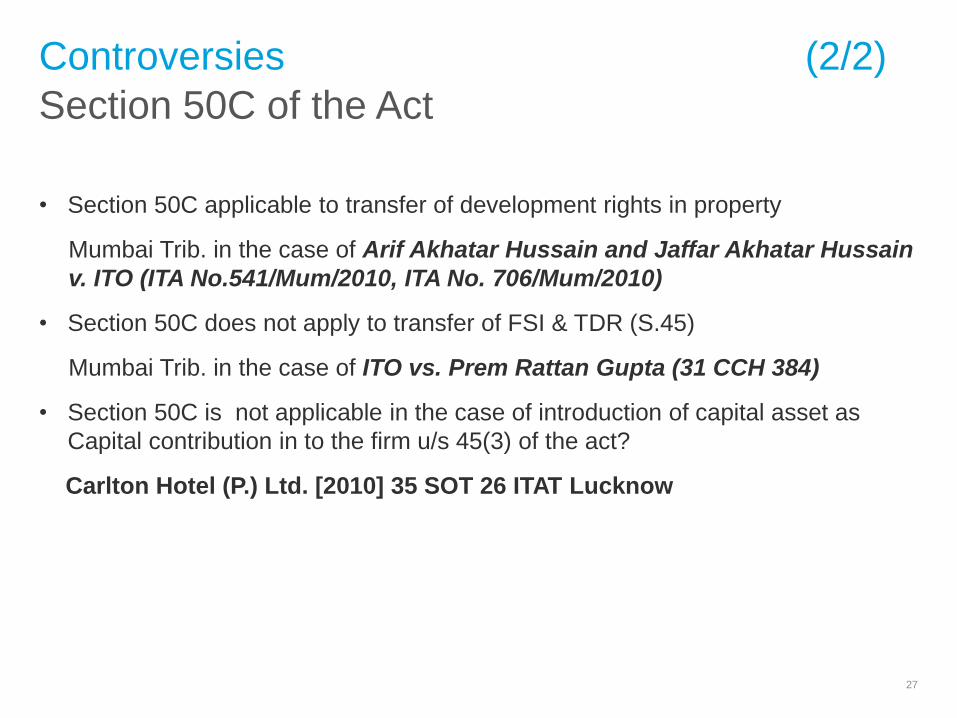

Controversies (2/2)

• Section 50C applicable to transfer of development rights in property

Mumbai Trib. in the case of Arif Akhatar Hussain and Jaffar Akhatar Hussain

v. ITO (ITA No.541/Mum/2010, ITA No. 706/Mum/2010)

• Section 50C does not apply to transfer of FSI & TDR (S.45)

Mumbai Trib. in the case of ITO vs. Prem Rattan Gupta (31 CCH 384)

• Section 50C is not applicable in the case of introduction of capital asset as

Capital contribution in to the firm u/s 45(3) of the act?

Carlton Hotel (P.) Ltd. [2010] 35 SOT 26 ITAT Lucknow

27

Section 50C of the Act

Controversies (1/2)

• Transfer of assets under a family arrangement does not attract the provisions of

Section 2(47) - As the provisions of Section 45 are not attracted, Section 50C is

also not applicable

Mumbai Trib. in the case of Shirish S. Maniar v. ITO (167 Taxmann 81)

• Section 50C applies only to capital asset and does not apply to assets held as

stock-in-trade

Mumbai Trib. in the case of Inderlok Hotels (P.) Ltd. V. ITO (32 SOT 419)

• Where land or building sold or otherwise transferred, such transfer shall be

deemed to have taken place only after the stamp duty has been assessed by

the State Government, because it is on the valuation made for the purpose of

stamp duty that the tax is payable - The assessee cannot contend that section

50C would not be applicable merely because the Deed of Conveyance had not

at that time been executed or registered

Kolkata HC in the case of Bagri Impex (P.) Ltd. v. ACIT (214 Taxman 305)28

Section 50D of the Act

29

Section 50D of the Act

Fair Market Value Deemed to be FVC in Certain

Cases

Where

• the consideration received or accruing as a result of the transfer of a capital

asset by an assessee is not ascertainable or cannot be determined,

then,

• for the purpose of computing income chargeable to tax as CG, the FMV of the

said asset on the date of transfer shall be deemed to be the FVC received or

accruing as a result of such transfer

30

Section 50D of the Act

Introduction

• Finance Act, 2012 inserted a new section 50D w.e.f. AY 2013-14, in order to get

over the argument of the taxpayer that no CG (machinery provision) failed when

consideration received for assets transferred was unascertainable

• Intending to undo Hyd. Trib. in the case of Ms. K Radhika vs. DCIT (2012-

TIOL-90)

• Made prospective

• Observations of SC in George Henderson [1967] 66 ITR 622 reversed - Value

of incoming asset - The consideration for the transfer of the capital asset is what

the transferor receives in lieu of the asset he parts with, namely, money or

money's worth, and therefore, the very asset transferred or parted with cannot

be the consideration for the transfer

31

Appendix

32

Recent Case Laws

33

41 taxmann.com 54

Deepak N. Phalke vs. ITO (Mum-Trib) (1/2)

Facts of the case:

• Assessee owned three properties namely, 'S', 'E' and 'A'

• He maintained the financial statements and the depreciation schedules for each

of these three proprietary concerns separately

• However, at the time of filing the ROI he consolidated all the financial statements

and the depreciation schedules of these three concerns

• During the year under consideration, he sold a factory building of concern 'S',

whose WDV was INR 7 lakhs, for a consideration of INR 21 lakhs

• Out of the sale consideration of INR 21 lakhs, the assessee invested a sum of

INR 13 lakhs and purchased another office premises, which fell into the same

block of assets, in the name of another proprietary concern 'E‘

• In his ROI, the assessee sought adjustment of the said block of assets

• AO rejected the claim stating that since the assessee maintained the books of

account for each of the proprietary concerns separately - when the businesses

are different, no such adjustments should be made to the block of assets34

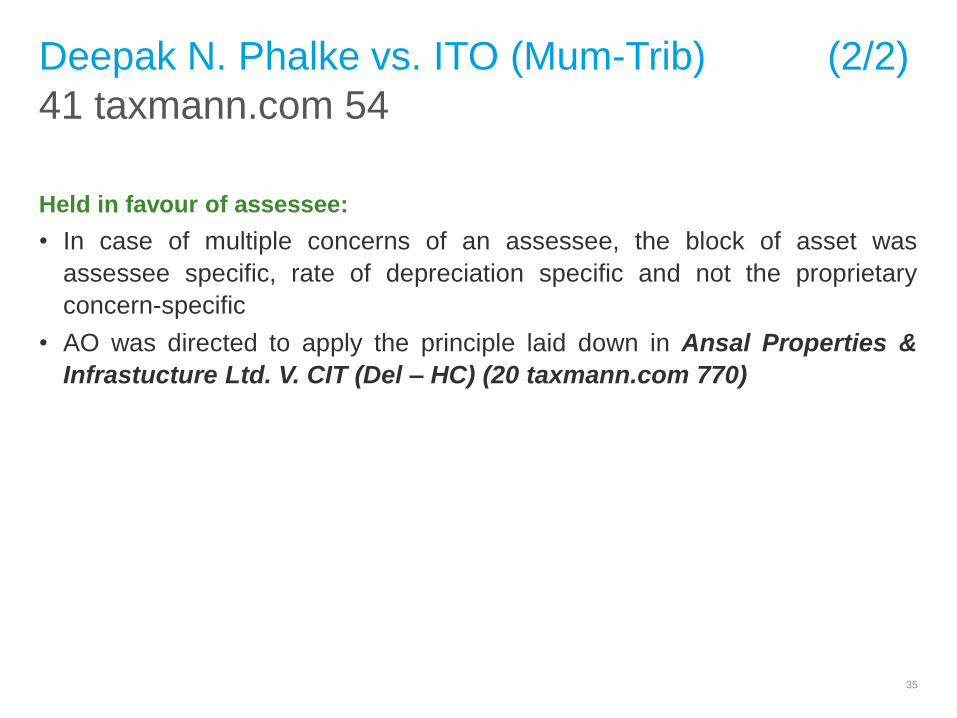

41 taxmann.com 54

Deepak N. Phalke vs. ITO (Mum-Trib) (2/2)

Held in favour of assessee:

• In case of multiple concerns of an assessee, the block of asset was

assessee specific, rate of depreciation specific and not the proprietary

concern-specific

• AO was directed to apply the principle laid down in Ansal Properties &

Infrastucture Ltd. V. CIT (Del – HC) (20 taxmann.com 770)

35

53 taxmann.com 227

Cadbury India Ltd. vs. CIT (Bom – HC) (1/1)

Facts of the case:

• During the year under consideration the assessee transferred land and building

and computed LTCG separately in respect of land and in respect of building and

claimed exemption under section 54EC of the Act

• AO found that bifurcation of property was made only in instant year

• He computed STCG under section 50, which came to nil

• Was held that there was no CG and hence no question of allowing deduction

under section 54EC arose

Held in favour of assessee:

• Section 50 makes it clear that the deeming fiction created in sub section (1) &

(2) is restricted only to the mode of computation of CG contained in Section 48 &

49

• Section 50 does not convert LTCA into STCA

36

198 taxmann.com 65

Kwality Ice Creams (India) Ltd. vs. CIT (Kol - HC)

(1/2)

Facts of the case:

• Assessee carried on the business of manufacturing and marketing of ice creams

• Marketing undertaking of the assessee comprised of

o Physical depreciable assets - cabinets, vans, pushcarts, etc.;

o Entire dealership network built over several years - management and non-

management employees with complete marketing data and know-how also

developed by the assessee over the years;

o Vending licenses, sales contracts and relationship with franchisees

• During the year under consideration, the assessee entered into an agreement

with BBL under which it transferred its marketing undertaking as a going concern

to BBL for a sum of INR 3 crores

• AO held that the entire sum of INR 3 crores received pursuant to the agreement

for transfer of the marketing undertaking would attract the provisions of section

50(1) and would be taxed as a STCG after deducting the WDV of the marketing

assets appearing in the books of account37

198 taxmann.com 65

Kwality Ice Creams (India) Ltd. vs. CIT (Kol-HC)

(2/2)

38

Held in favour of assessee:

• Precondition for pressing in section 50 for computation is that the capital asset

must be an asset forming part of block asset, in respect of which the

depreciation has been allowed under the Act

• Section 50 has application as far as the tangible assets are concerned and

it does not have any application in case of intangible assets (for in case of

tangible assets the depreciation can be worked out, whereas in case of

intangible assets there is no scope of depreciation)

• Depreciation is allowed in the Act in case of tangible assets

• Hence, AO had erroneously clubbed the intangible assets with the tangible

assets for holding the entire consideration amount as capital gain

46 taxmann.com 257

Bharat Bijlee Limited vs. CIT (Bom – HC) (1/2)

Facts of the case:

Assessee T Ltd.

Transfer of its lift division

(under a scheme of arrangement*)

Consideration disbursed by way of allotment/ issue of

bonds/ preference shares

• The AO disallowed the claim of the assessee that the transfer of its lift

division is an exchange and not a sale

• AO opined that transfer of lift division was a slump sale, and therefore,

taxable in terms of Section 50B of the Act

*by invoking Section 391 r.w.s Section 394 of the Companies Act, 195639

46 taxmann.com 257

Bharat Bijlee Limited vs. CIT (Bom – HC) (2/2)

Held in the favor of the assessee:

• The scheme of arrangement approved by the Court cannot be considered as

the ‘sale’ of lift division or undertaking by the assessee

• Transfer of the undertaking took place in exchange of issue of preference

shares/ bonds - This was a case of exchange and not sale

• For slump sale, the transfer has to be by way of sale

• Tribunal held that the transfer of lift division comes within the purview

of Section 2(47) of the Act, but cannot be termed as slump sale

• No substantial question of law raised and hence, case

dismissed by the HC

40

ITA No. 267/Kol/2013

M/s LGW Limited vs. I.T.O. (Kol - ITAT) (1/1)

Facts of the case:

• During the year under consideration the assessee sold property for INR

60,00,000

• AO after taking note of the provisions of section 50C computed LTCG by

adopting sale consideration at INR 61,22,330

Held in favour of assessee:

• Although Section 50C does not speak of any variation in terms of percentage

between value adopted for the purpose of stamp duty registration and the actual

consideration received on transfer, keeping in view the decision of the Hyd. ITAT

in ACIT vs. Suvarna Rekha (ITA No.743/Hyd/2009), it was held that since the

difference between the actual consideration received on transfer and the stamp

duty valuation is less than 2%, Section 50C of the Act should not be invoked

41

20 Taxman 112

CIT vs. Sarjan Realities Ltd. (Gujarat - HC) (1/1)

Facts of the case:

• AO invoked the provisions of

section 50C of the Act on the

basis of difference in

valuation of land and treating

the same as unexplained

investment

• CIT(A) upheld the order of

AO

• Tribunal deleted the said

addition and dismissed the

order of CIT(A)

Held in favor of the

assessee:

• HC held that, section 50C

will only be applicable to

the seller as section 50C

of the Act states,

consideration received by

the assessee on sale of

capital asset

• HC upheld the decision of

the ITAT

42

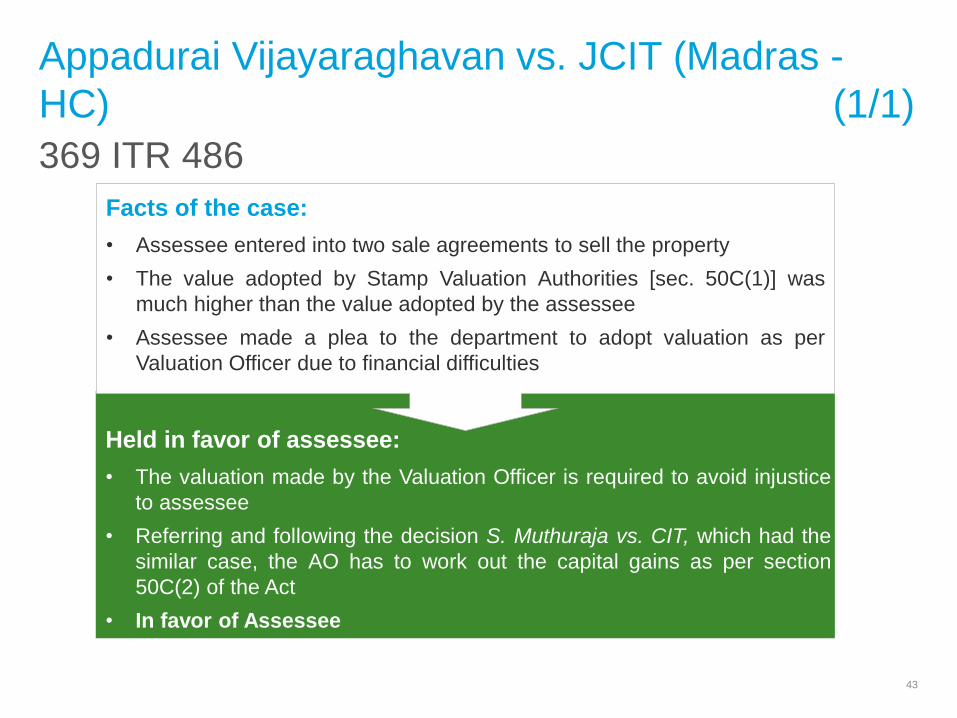

369 ITR 486

Appadurai Vijayaraghavan vs. JCIT (Madras -

HC) (1/1)

Held in favor of assessee:

• The valuation made by the Valuation Officer is required to avoid injustice

to assessee

• Referring and following the decision S. Muthuraja vs. CIT, which had the

similar case, the AO has to work out the capital gains as per section

50C(2) of the Act

• In favor of Assessee

Facts of the case:

• Assessee entered into two sale agreements to sell the property

• The value adopted by Stamp Valuation Authorities [sec. 50C(1)] was

much higher than the value adopted by the assessee

• Assessee made a plea to the department to adopt valuation as per

Valuation Officer due to financial difficulties

43

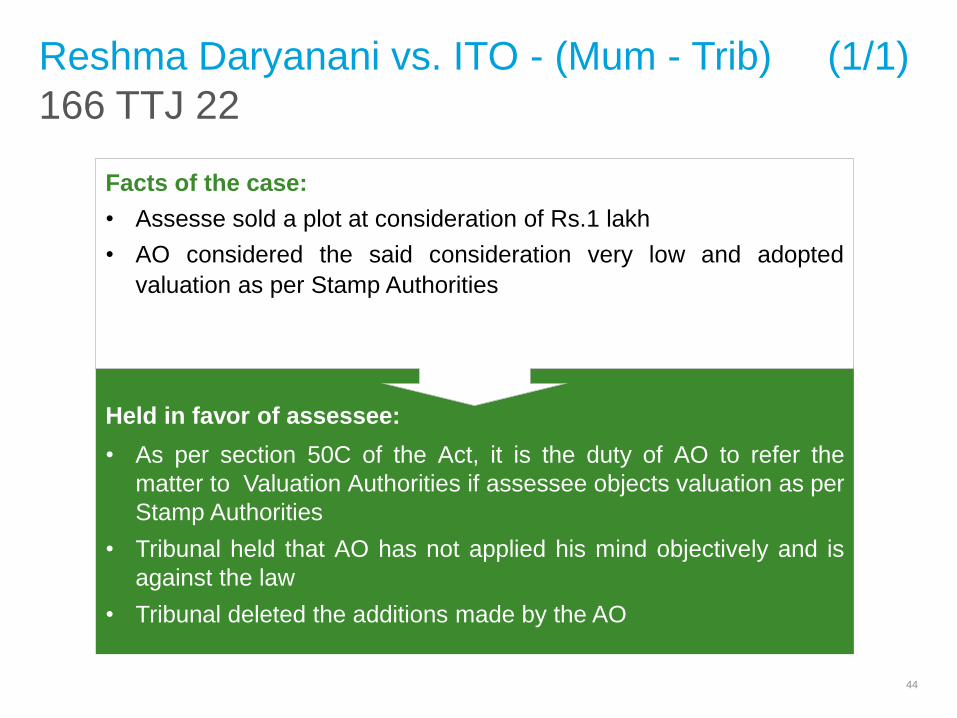

166 TTJ 22

Reshma Daryanani vs. ITO - (Mum - Trib) (1/1)

Held in favor of assessee:

• As per section 50C of the Act, it is the duty of AO to refer the

matter to Valuation Authorities if assessee objects valuation as per

Stamp Authorities

• Tribunal held that AO has not applied his mind objectively and is

against the law

• Tribunal deleted the additions made by the AO

Facts of the case:

• Assesse sold a plot at consideration of Rs.1 lakh

• AO considered the said consideration very low and adopted

valuation as per Stamp Authorities

44

68 SOT 110

Kancast Pvt. Ltd. vs. ITO (Pune - Trib) (1/1)

Held in favor of assessee:

• Going by the words of section 50C, it states that it would be applicable only to a capital

asset, being land or building or both

• Tribunal held that section 50C does not come into picture because transfer here is only

of leasehold rights in land

• Leasehold rights in land is a capital asset but section 50C will not be in operation when

transfer takes place

Facts of the case:

• Assessee transferred leasehold right in factory land, building and shed; and declared

the said transfer as LTCG

• AO, on the basis of Section 50C of the Act, took the value adopted by Stamp

Authorities for the said transfer of rights in land and accepted the value of

consideration taken by assessee for transfer of building

Issue involved:

• Whether section 50C will be applicable for the said transfer of leasehold rights in land?

45

56 SOT 12

Irfan Abdul Kader Fazlani vs. ACIT (Mum - Trib)

(1/1)

Facts of the case:

• Assessee was a shareholder of a company which owned two flats

• Assessee and other shareholders sold all the shares of the company and

declared the income from sale of shares as LTCG

• AO concluded that there was indirect transfer of immovable property through

transfer of shares and provisions of Section 50C of the Act were applied

Held in favor of assessee:

• The expression ‘transfer’ under section 2(47) of the Act has to be a direct

transfer

• In this case assessee had transferred shares and not the immovable properties

• Assessee did not have the full ownership of the flats

• Transfer of shares cannot come under the ambit of section 50C

• Tribunal held that, AO’s decision to apply section 50C to the tax planning

adopted by the assessee is not correct

• Section 50C would not be applicable to the above transaction46

49 taxmann.com 513

Appadurai Vijayaraghavan vs. JCIT (OSD -

Chennai) (1/1)

Facts of the case:

• Assessee agreed to sell two properties ( land + Building)

• Assessee had raised loan from SIPCOT against collateral securities of

aforesaid assets

• Sale deed was executed on 17/05/06

• AO rejected the explanation and concluded the registration of sale deed as

sale date therefore computed capital gains escaped assessment.

Held in favor of assessee:

• Section 50C would be applicable to the above transaction.

• As per section 50C(2) of the Act, it is the duty of AO to refer the matter to

Valuation Authorities if assessee objects valuation as per Stamp Authorities

with regards to distress sale.

• Even if assessee made objection for invoking section 50C(1) the AO should

have referred the matter to VO as per section 50(2). 47

59 taxmann.com 373

Bhaidas Cursondas & Company vs. ACIT (Mum -

Trib) (1/1)

Facts of the case:

• Assessee sold assets forming part of the block “building”

• AO considered stamp duty as per section 50C, recomputed opening WDV

of the relevant assets and allowing reduced depreciation accordingly

Held in favor of assessee:

• Section 50C would be applicable to depreciable assets being assessee’s

claim in immovable assets

• But application of section 50C is limited for computing CG

• WDV would necessarily be computed as per section 43(6) and section 50C

has no application

48

61 taxmann.com 362

Fleurette Marine Novelle Hatam (Mum - Trib)

(1/1)

Facts of the case:

• Assessee filed his return computing LTCG on transfer of tenancy rights

• Computation not accepted by AO, who was of the firm belief that provisions

of section 50C were clearly applicable, and therefore the Stamp Duty value

should have been considered as the full value of consideration

Held in favor of assessee:

• Undisputedly tenancy right is a capital asset

• However, perusal of section 50C suggests that it is only for the limited

purpose of computing capital gain in respect of sale of land and building

• Accordingly, provisions of section 50C are not applicable on the transfer

of tenancy right

49

52 taxmann.com 330

CIT vs. Fortune Hotels and Estates (P.) Ltd.

(Bombay - HC) (1/1)

Held in favor of assessee:

• Tribunal held that registered sale was there and consideration was mentioned

• Clarification and findings of tribunal does not raise substantial question of law thus

revenues appeal dismissed

Facts of the case:

• Assessee sold office premises for INR 2 crores

• AO, on the basis of Section 50C of the Act, took the value adopted by Stamp

Authorities INR 3.72 crores

• Assessee insisted the matter be referred to DV - the amount submitted by VO was INR

2.70 crores

• AO passed penalty order for inaccurate particulars of income which was set aside by

tribunal

Issue involved:

• Whether penalty could be imposed on addition to deemed income under section 50C of

the Act?

50

38 taxmann.com 195

Neelkamal Realtors & Errectors India (P.) Ltd. vs.

DCIT (Mum - Trib) (1/1)

Facts of the case - Issue 1:

• Assessee was engaged in real estate - sold flats for INR 3.63 crores under

the head PGBP

• AO made addition to the income of INR 4.45 crores for variation in the price

charged

• CIT(A) applied provisions of Section 50C and considered SDV, making

addition of INR 8.53 crores

Held in favor of assesse - Issue 1:

• As per section 50C(2)(a) of the Act, it is the duty of AO to refer the matter to

the Valuation Officer if assessee claimed that stamp valuation exceeded the

FMV of property

51

47 taxmann.com 88

Raj Kumari Agarwal vs. DCIT (Agra – Trib.) (1/1)

Facts of the case – Issue 1:

• Assessee sold land for INR 1,64,000 (SDV – Rs. 2,58,000)

• He considered the sale value as consideration (as the land was situated in

underdeveloped area and due to other economic factors)

• AO rejected assessee’s contention and applied section 50C (FMV).

Held in favor of assesse – Issue 1:

• As per section 50C(2)(a) of the Act, it is the duty of AO to refer the matter to

Valuation Authorities if assessee claimed that Stamp valuation exceeded

the FMV of property

• Tribunal set aside the orders and directed AO to complete the assessment

on valuation by DVO

52

64 taxmann.com 265

ACIT vs. Rakesh Narang (Delhi - Trib) (1/1)

Facts of the case 2:

• Assessee purchased property for INR 34 lakhs

• FMV INR 83.15 lakhs as per DVO

• AO made additions of INR 49.15 lakhs U/s 69B

Held in favor of assesse 2:

• Prerequisite for applicability of section 69B are, AO must have substantiveevidence that actual amount invested by assesse is more then the amountrecorded in books of accounts

• Valuation of DVO is mere estimate cost of construction and not price finallybargained

• Section 50C will only be applicable to the seller as section 50C of the Actstates, consideration received by the assessee on sale of capital assets

• Section 56(2)(vii) is applicable to individual or HUF who receivesimmovable property on or after 01.10.09

53

50 taxmann.com 269

R. Bhoopathy vs. JCIT (Chennai - Trib) (1/1)

Facts of the case:

• Assessee engaged in real estate business.

• Sold property to wife for INR 20 lakhs in normal course of business.

• AO applied section 50C thus considered guideline value of INR 29 lakhs

(increase in business income by INR 9 lakhs)

Held in favor of assessee:

• Section 50C of the Act, is special provision applying only to CG, does not

apply to computation of business income

• There is no general proposition that business transaction cannot take place

between husband and wife

• Principle of duality is applied to all other transaction unless otherwise

specified

54

Glossary

55

Glossary

CG – Capital gains

COA – Cost of Acquisition

FMV – Fair market value

FCV – Full value of consideration

SDV – Stamp duty value

STCG – Short term capital gain

STCL – Short term capital loss

LTCG – Long term capital gain

LTCL – Long term capital loss

AO – Assessing officer

ITO – Income-tax officer

CIT – Commissioner of income-tax

DVO – Departmental valuation officer

HUF – Hindu undivided family56

Thank You

57

The information contained in this document is intended to provide general information on a particular subject or subjects and is not exhaustive treatment of such subject(s).The contents of this document are for general information and the presenter by means of this document is not rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This document is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your finances or your business.Before making any decision or taking any action that may affect your finances or business, you should consult a qualified professional advisor.The presenter shall not be responsible for any loss, whatsoever, sustained by any person who relies on this document.