defining & enabling digital ecology via mobile money · defining & enabling digital ecology...

TRANSCRIPT

© 2016 TM Forum Live! 2016 | 1

Defining & Enabling DigitalEcology

via Mobile Money

© 2016 TM Forum Live! 2016 | 2

Content

11

22

33

Vodafone M-Pesa Journey

Industry Pathway To Draw A New Pattern

Realizing Vision to Build Open Payment Ecosystem

© 2016 TM Forum Live! 2016 | 3

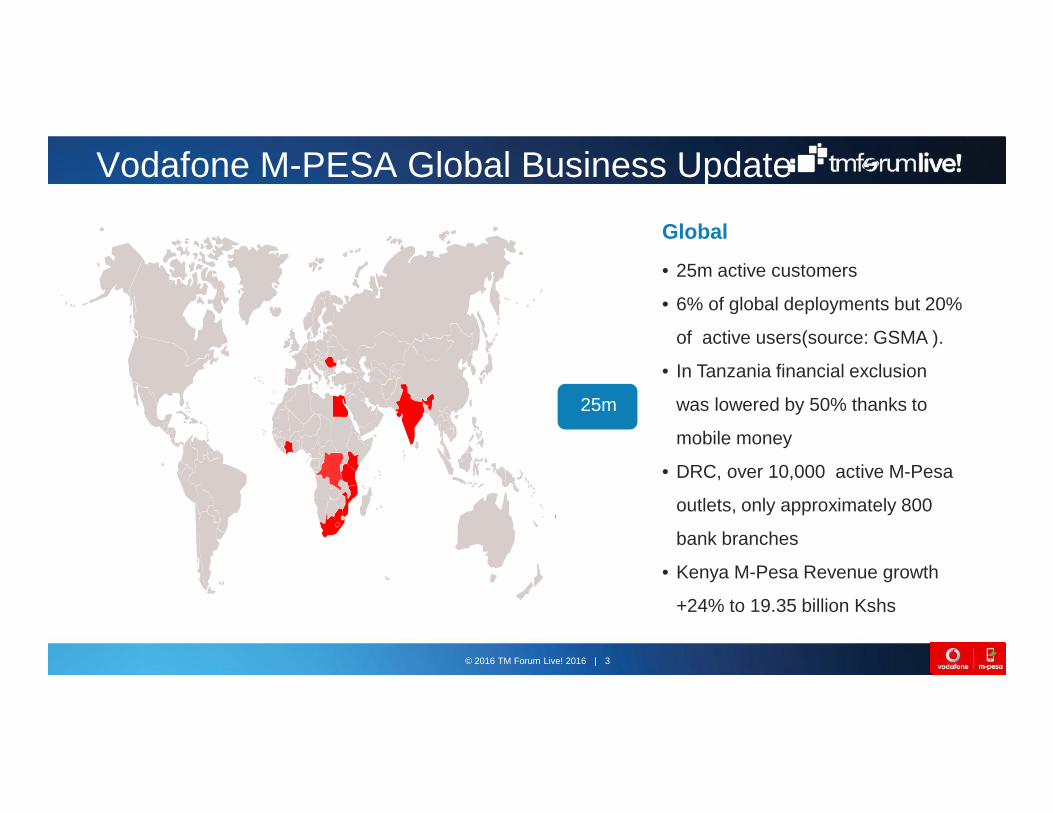

Vodafone M-PESA Global Business Update

25m

Global

• 25m active customers

• 6% of global deployments but 20%

of active users(source: GSMA ).

• In Tanzania financial exclusion

was lowered by 50% thanks to

mobile money

• DRC, over 10,000 active M-Pesa

outlets, only approximately 800

bank branches

• Kenya M-Pesa Revenue growth

+24% to 19.35 billion Kshs

© 2016 TM Forum Live! 2016 | 4

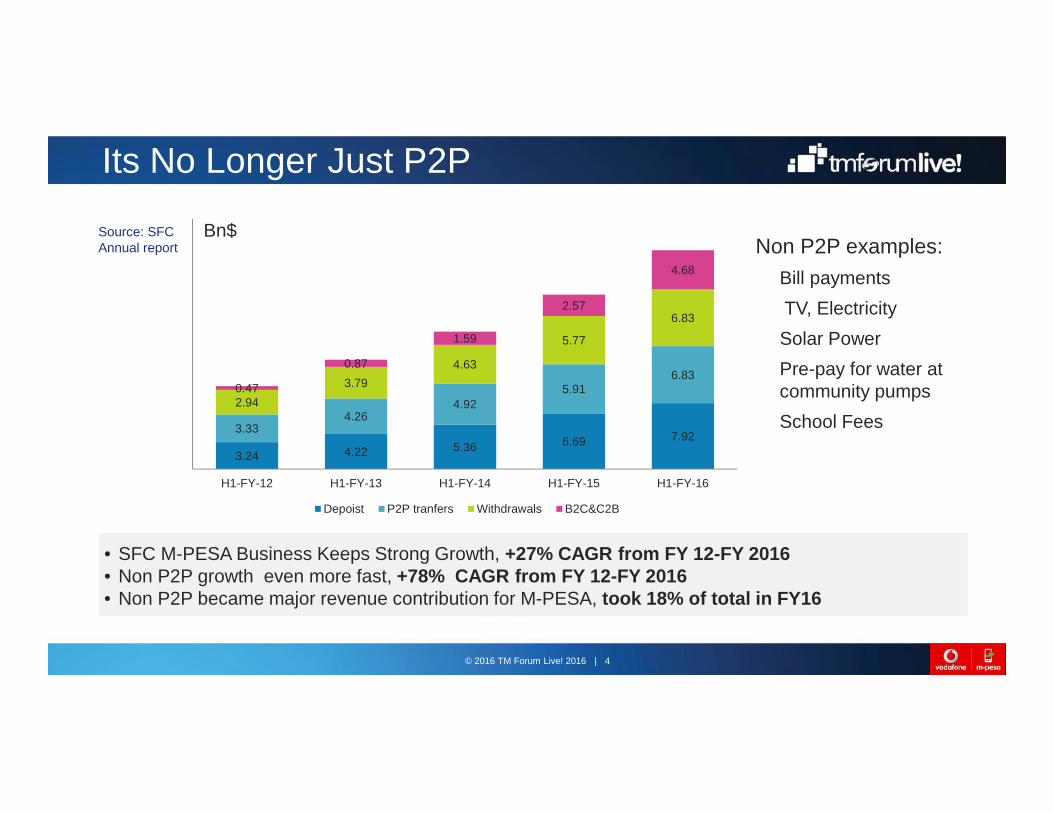

• SFC M-PESA Business Keeps Strong Growth, +27% CAGR from FY 12-FY 2016• Non P2P growth even more fast, +78% CAGR from FY 12-FY 2016• Non P2P became major revenue contribution for M-PESA, took 18% of total in FY16

Its No Longer Just P2P

• Non P2P examples:– Bill payments– TV, Electricity– Solar Power– Pre-pay for water at

community pumps– School Fees

3.24 4.22 5.36 6.69 7.923.334.26

4.925.91

6.83

2.943.79

4.63

5.77

6.83

0.47

0.87

1.59

2.57

4.68

H1-FY-12 H1-FY-13 H1-FY-14 H1-FY-15 H1-FY-16

Depoist P2P tranfers Withdrawals B2C&C2B

Bn$Source: SFCAnnual report

© 2016 TM Forum Live! 2016 | 5

1.Capture SubscribersHow to capture the subscribers financial

business?

We Still Face Business Challenge

2.Killer ServicesWhat is the 'killer service' which

will capture the market.

3. Business StrategyWhat is the business strategy to

adopt with Mobile Money?

© 2016 TM Forum Live! 2016 | 6

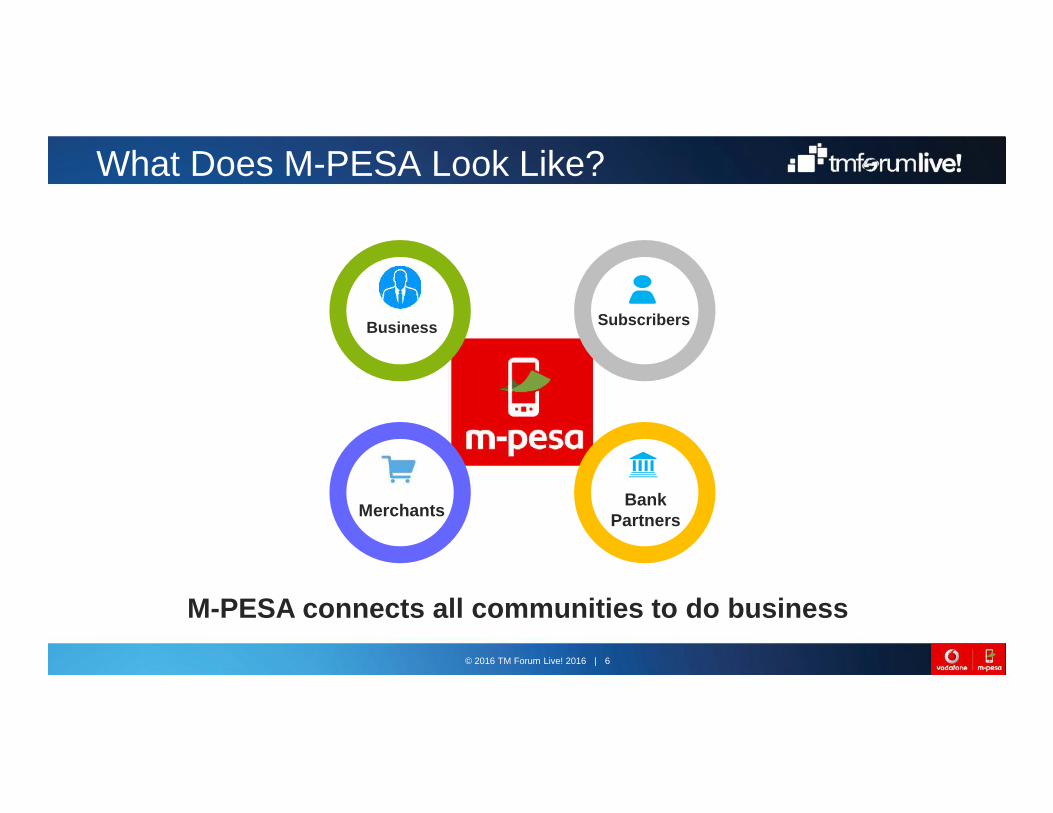

What Does M-PESA Look Like?

Merchants

Subscribers

BankPartners

M-PESA connects all communities to do business

Business

© 2016 TM Forum Live! 2016 | 7

Different Paths to Success..

1

Cash in/outP2P Transfer

2 3 4 5

Bill paymentB2C,C2B

MicroSaving/loan National remittance

HUB/IMT HUBMerchant PaymentsMobile coupon/ticket

Unbanked:e.g.Kenya

Banked:e.g.Europe

1

Cash in/outP2P Transfer

Bulk Distribution

2 3 4 5

Bill paymentInternationalRemittance

MicroSaving/loanInsurance

Interoperation

Unbanked:e.g.Kenya

MerchantPaymentsVouchers

© 2016 TM Forum Live! 2016 | 8

Content

11

22

33

Vodafone M-Pesa Journey

Industry Pathway To Draw A New Pattern

Realizing Vision to Build Open Payment Ecosystem

© 2016 TM Forum Live! 2016 | 9

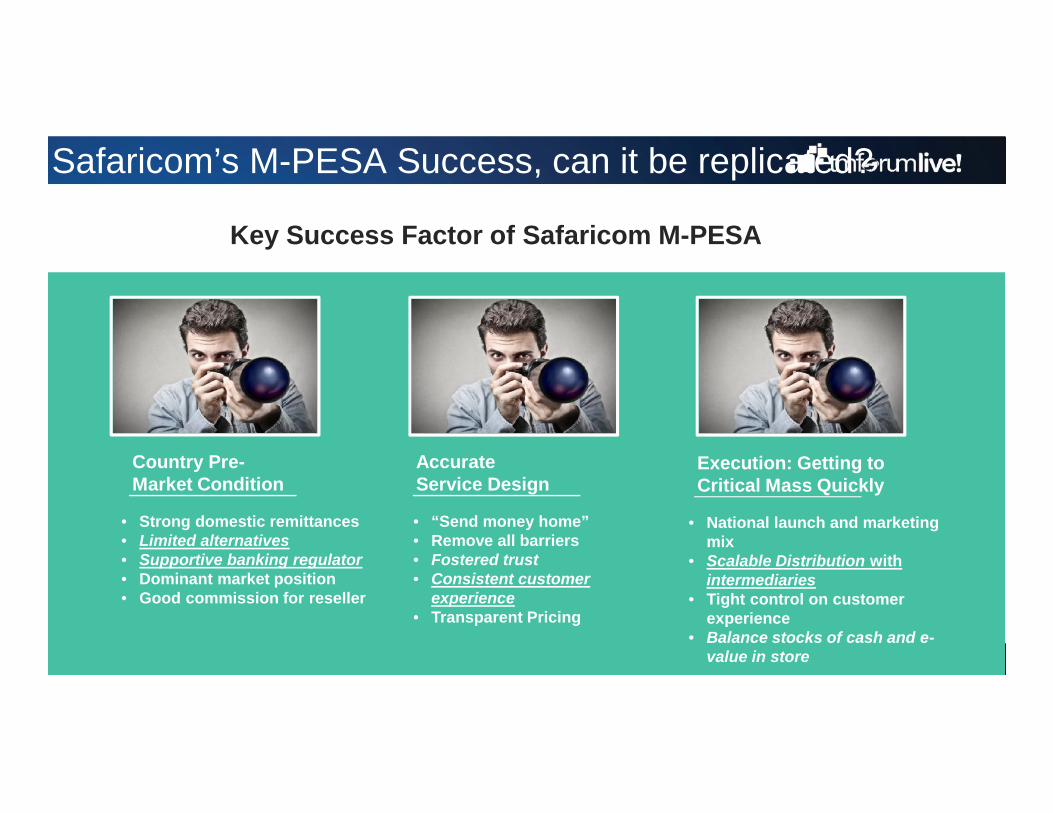

Safaricom’s M-PESA Success, can it be replicated?

Country Pre-Market Condition

• Strong domestic remittances• Limited alternatives• Supportive banking regulator• Dominant market position• Good commission for reseller

AccurateService Design

• “Send money home”• Remove all barriers• Fostered trust• Consistent customer

experience• Transparent Pricing

Execution: Getting toCritical Mass Quickly

• National launch and marketingmix

• Scalable Distribution withintermediaries

• Tight control on customerexperience

• Balance stocks of cash and e-value in store

Key Success Factor of Safaricom M-PESA

© 2016 TM Forum Live! 2016 | 10

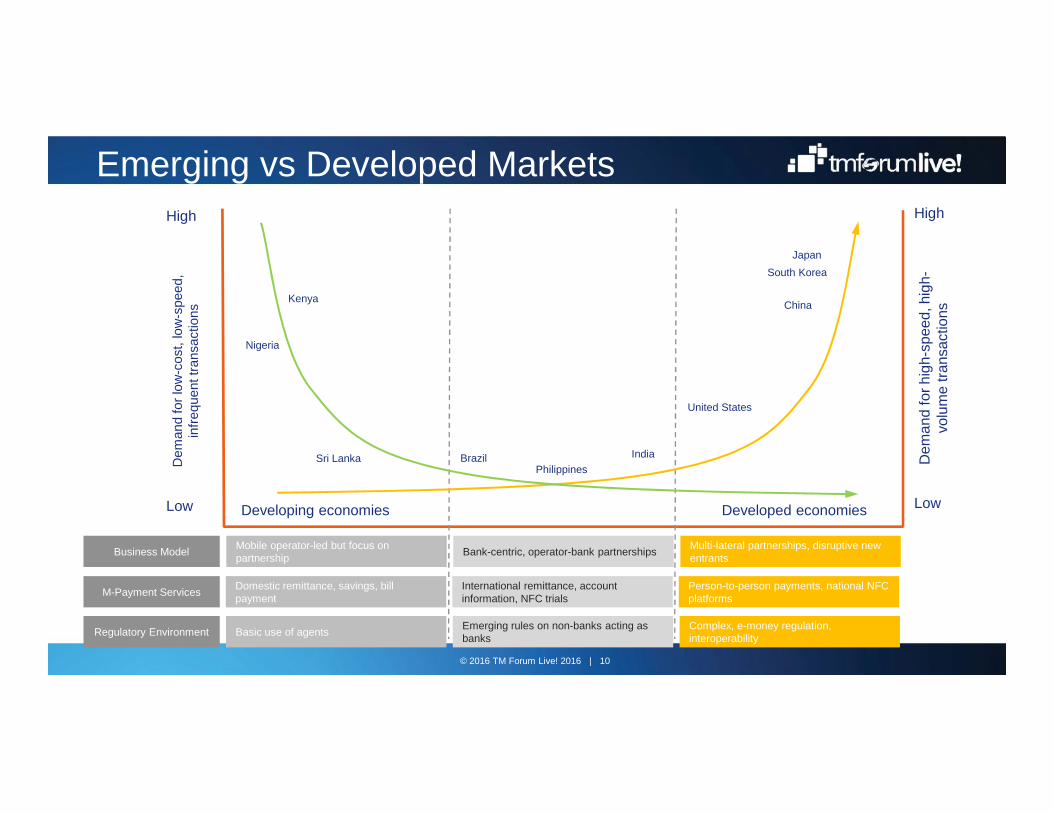

Emerging vs Developed Markets

Business Model

M-Payment Services

Regulatory Environment

Mobile operator-led but focus onpartnership

Domestic remittance, savings, billpayment

Basic use of agents

Bank-centric, operator-bank partnerships

International remittance, accountinformation, NFC trials

Emerging rules on non-banks acting asbanks

Multi-lateral partnerships, disruptive newentrants

Person-to-person payments, national NFCplatforms

Complex, e-money regulation,interoperability

Dem

and

for l

ow-c

ost,

low

-spe

ed,

infre

quen

t tra

nsac

tions

High

Low

Dem

and

for h

igh-

spee

d, h

igh-

volu

me

trans

actio

ns

High

LowDeveloped economiesDeveloping economies

Sri Lanka

Kenya

Nigeria

BrazilPhilippines

India

United States

South Korea

China

Japan

© 2016 TM Forum Live! 2016 | 11

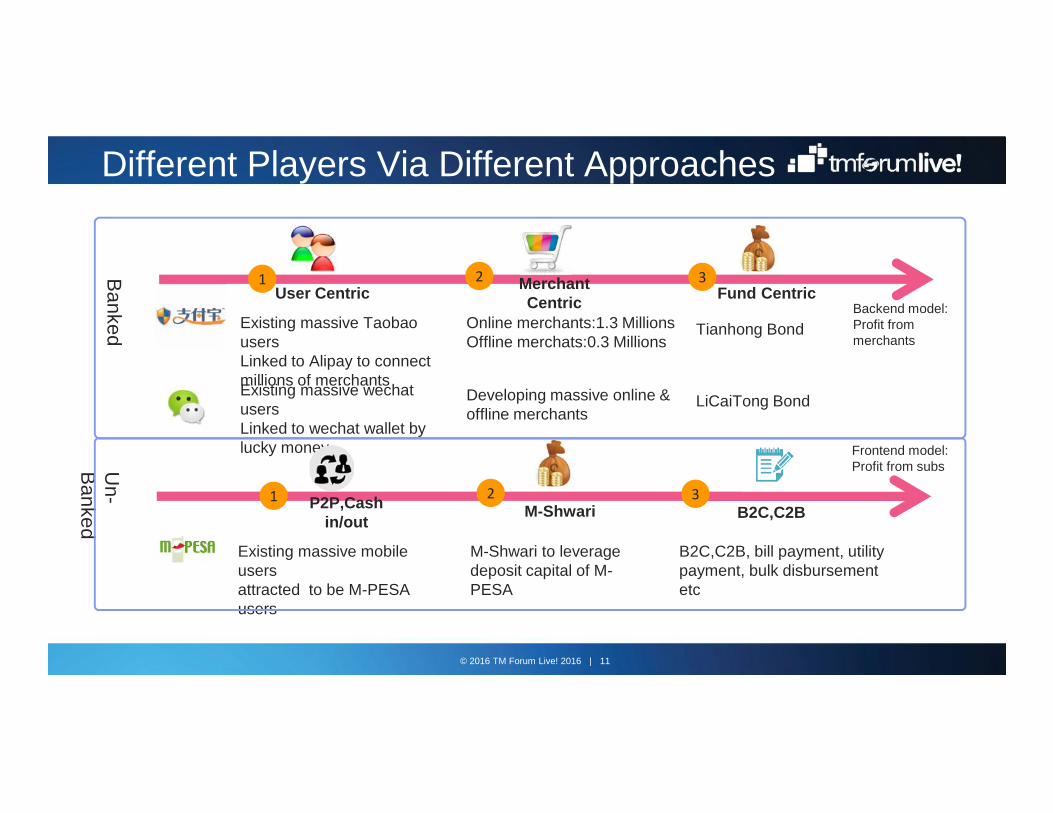

Different Players Via Different Approaches

1User Centric Merchant

Centric2 3

Fund Centric

Online merchants:1.3 MillionsOffline merchats:0.3 Millions

Tianhong BondExisting massive TaobaousersLinked to Alipay to connectmillions of merchantsExisting massive wechatusersLinked to wechat wallet bylucky money

Developing massive online &offline merchants

LiCaiTong Bond

1 P2P,Cashin/out M-Shwari

2 3B2C,C2B

Existing massive mobileusersattracted to be M-PESAusers

B2C,C2B, bill payment, utilitypayment, bulk disbursementetc

M-Shwari to leveragedeposit capital of M-PESA

Backend model:Profit frommerchants

Frontend model:Profit from subs

BankedU

n-Banked

© 2016 TM Forum Live! 2016 | 12

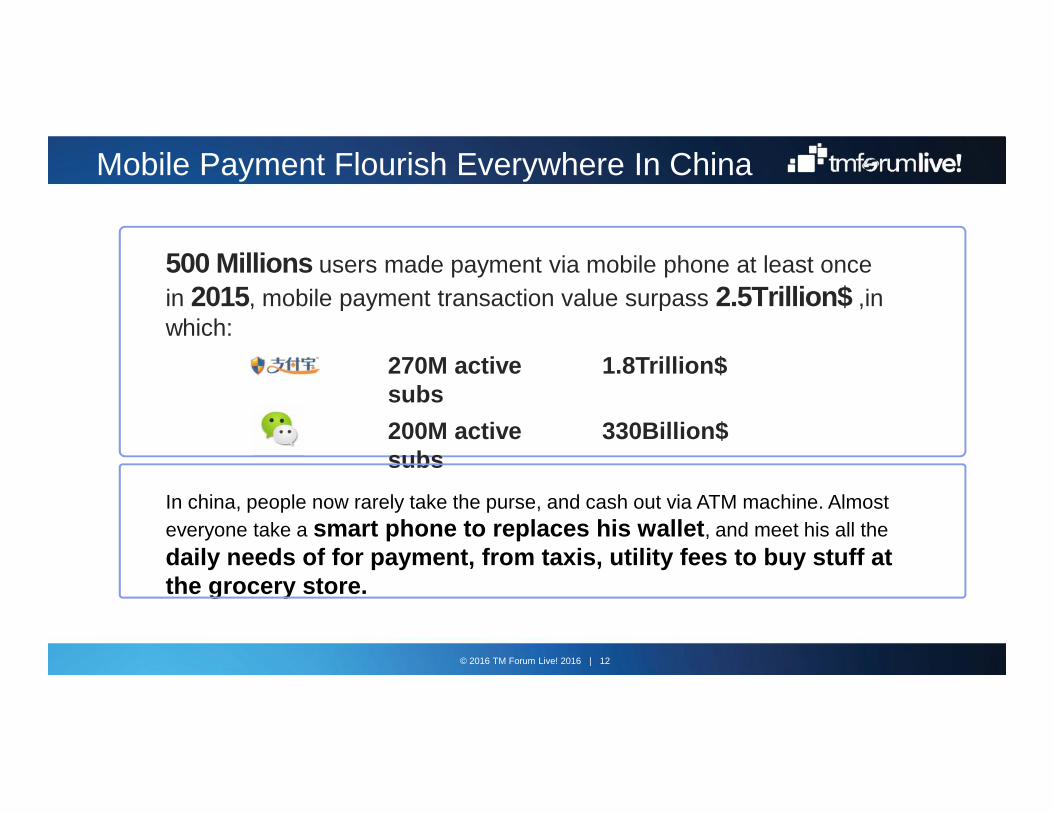

270M activesubs200M activesubs

1.8Trillion$

330Billion$

Mobile Payment Flourish Everywhere In China

In china, people now rarely take the purse, and cash out via ATM machine. Almosteveryone take a smart phone to replaces his wallet, and meet his all thedaily needs of for payment, from taxis, utility fees to buy stuff atthe grocery store.

500 Millions users made payment via mobile phone at least oncein 2015, mobile payment transaction value surpass 2.5Trillion$ ,inwhich:

© 2016 TM Forum Live! 2016 | 13

① Bank Partners② Online Merchant

③ Offline Merchants

The Eco-Centric Business Shall Be The Next Move

© 2016 TM Forum Live! 2016 | 14

Interconnected Services Signal New OpportunitiesMobile Marketing

Mobile Banking and Payments

Mobile Shopping

Core Competency: Customer Relationship

Core Competency: Customer Experience

Core Competency: Financial & Payment Service

• Data analytics• Service and product advertising and

marketing (location based)• Loyalty and other promotions

• Product and service search and discovery• Social location shopping• Price comparison shopping• Support, customer care• Orders and delivery

• Point-of-sale payments e.g. NFC/barcode• Mobile wallets• Device-based credit card processing

solution• Direct carrier billing• Salary payments• Microfinance• Insurance services• Investment services• International remittance• Domestic remittance• Mobile web payments• Utility bill payments

Led by financial, mobile operators and technology Led by Technology, marketing and retailers

Hig

h se

rvic

e m

atur

ityLo

w s

ervi

ce m

atur

ity

© 2016 TM Forum Live! 2016 | 15

Content

11

22

33

Vodafone M-Pesa Journey

Industry Pathway To Draw A New Pattern

Realizing Vision to Build Open Payment Ecosystem

© 2016 TM Forum Live! 2016 | 16

Huawei for Eco-Centric Based Platform Is Ready

SystemSecurity

SystemRobustness

ServiceExperience

SystemOpenness

System Agility

•Mobile APP•QR code/NFC•Self care

•PlatformVirtualization•Platform Elasticity•2000 TPS/node

•HSM encryption•Anti virus n•AML

•Generic API•Merchant toolkit•NFC integration

•80% requirement forlocal configuration•TTM to days

© 2016 TM Forum Live! 2016 | 17

Eco-centric Services Layouts @ Huawei Platform

01

02

03

05

04

Financial services:Savings, Loan, Donation, Stock, Insurance…

Life Assistance services:Buy airtime, gas,water,electricity, TV bill payment…

Personal & Group services:P2P transfer, Credit card repay, AA payment, red envelop…

Online payment services:ebay,Amazon,Taobao online merchant payment…

Offline payment services:Cinema, Taxi, Restaurant, hotel, coupon, Loyalty,promotion…

© 2016 TM Forum Live! 2016 | 18

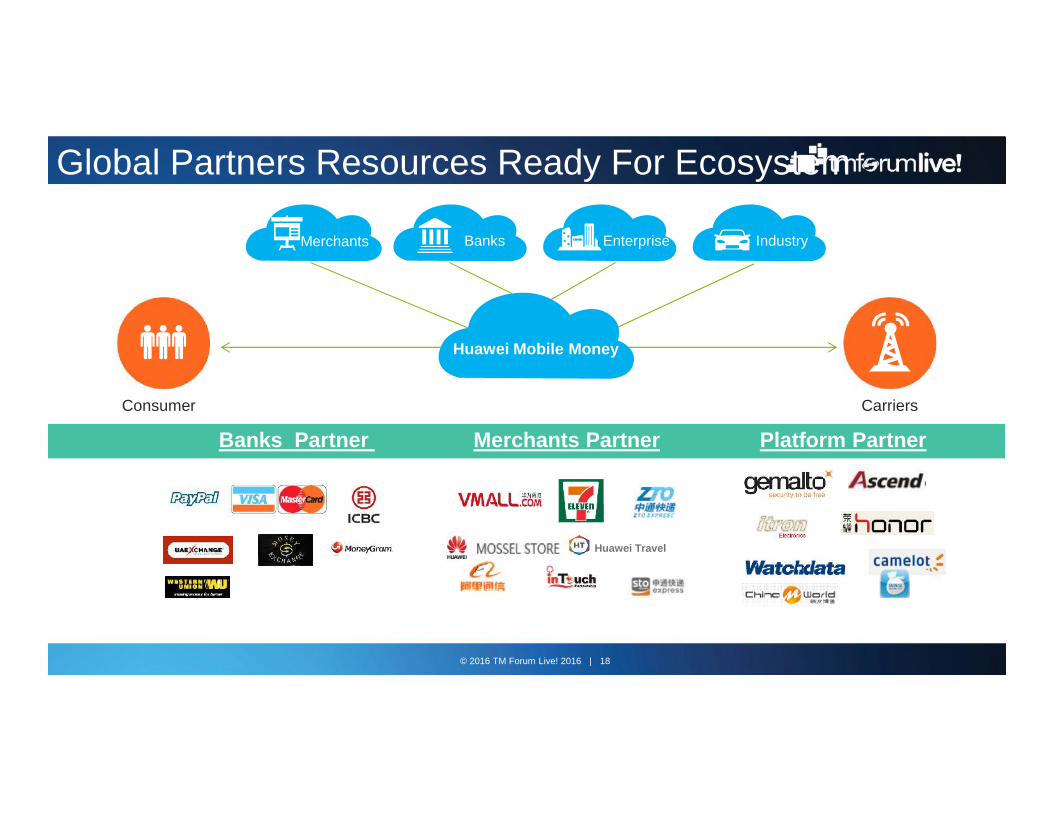

Global Partners Resources Ready For Ecosystem

Consumer

Banks Partner Merchants PartnerCarriers

IndustryEnterpriseBanks

Huawei Mobile Money

Merchants

Huawei Travel

Platform Partner

© 2016 TM Forum Live! 2016 | 19

© 2016 TM Forum Live! 2016 | 20Copyright©2016 Huawei Technologies Co., Ltd. All Rights Reserved.