december 2015 the nepal hartered accountant · why audit of information system is required in nepal...

TRANSCRIPT

December 2015Vol. 18 No. 2

Journal of the Institute of Chartered Accountants of Nepal

CHARTEREDCCOUNTANTA

T H E N E P A L

December 2015Vol. 18 No. 2

Global Nepal Printing Press Service Pvt. Ltd.Tel: 4102772

CA. Prakash Lamsal ChairmanCA. Mahesh Khanal Vice-ChairmanCA. Nil Bahadur Saru Magar MemberCA. Hemanta Pokharel MemberCA. Sanju Adhikari MemberCA. Shraddha Singh Shrestha MemberRA. Dev Bahadur Bohara MemberRA. Surendra Keshar Amatya MemberRA. Dharanidhar Adhikari MemberMr. Binod Prasad Neupane Secretary

Editorial 2

President's Message 3

Accounting

Challenges and Quality of Accounting Profession- CA. Paramananda Adhikari

7

The Legitimacy of International Public Sector Accounting Standards (IPSASs)- Dr. Pawan Adhikari

10

Economy

Nepal Unrest: The Fault Line- CA. Anal Raj Bhattarai

15

Managing Risks Facing the Economy- Mr. Tula Raj Basyal

18

Information Technology

Dimension of Digital Signature- CA. Mukunda Pokharel

22

Why Audit of Information System is Required in Nepal ?- CA. Gaurav Khwaunju Shrestha

27

Taxation

Taxation of Income from Long Term Contract: Need to have Clear Guidelines/Manual- CA. Kaushlendra Jha

33

Conference Material- CA. Narendra Bhattarai

38

News 45

Notices 14, 17, 52, 53, 56

Contribution

Standard Chartered Bank Nepal Ltd.

Kailash Bikash Bank Ltd.

Nabil Bank Ltd.

Rastriya Banijya Bank Ltd.

Deva Bikash Bank Ltd.

As stipulated by Nepal Chartered Accountants Act, 1997 the objective of the Institute of Chartered Accountants of Nepal (ICAN) is to play the role of a regulatory body to encourage the members to carry on accounting profession being within the extent of the code of conduct in order to consolidate and develop accounting profession as a cause for economic development of the nation. The function and duties of the Council is to monitor and regulate its members so as to ensure the compliance of Accounting Standards and Standards on Auditing developed or recommended by Accounting Standards Board and Auditing Standards Board".

Prior to the 5th amendment in Nepal Chartered Accountant Rules, 2061 ICAN has constituted a Peer Review Board in order to monitor its members with regards to practice monitoring. Institute has issued NSQC and a Statement on Peer Review with an intention to further enhance the quality of professional work of practicing CA/RA members. The Nepal Chartered Accountants Act, 1997 requires ICAN to enforce compliance with the prevailing Standards and laws by professional accountants and auditors through Disciplinary Committee. Many cases of violation of Code of Ethics (COE) and Standards are still under investigation in Disciplinary Committee. However, neither the Quality Assurance (QA) system for audit nor the practice monitoring of the members was effectively enforced. It is worth to note that ICAN has to fulfill IFAC membership obligations as a professional body and should ensure a mandatory quality assurance review program is in place for its members performing audits of financial.

In the above context, the Council feels necessary for mandatory QA system for audit firms that conduct audit of listed companies such as insurance, bank and financial institutions etc. under the direction of ICAN as well as oversight and supervision of a Board formed by ICAN.

In the view of above the 5th amendment in Nepal Chartered Accountant Rules, 2061 has been approved by the ministerial decision of 2072/08/18 of Government of Nepal empowering regulatory regime of the Institute more responsive by forming an independent Quality Assurance Review Board (QARB) comprising of 7 members. The Board will conduct inspection and monitoring independently to the accounting firms. The Board will oversee whether there exist assurance system in the accounting firms to conform the compliance with auditing standards, NSQC by accounting firms in course of performing audit.

The Board has started its functions and very soon will come up with its policy and programs on quality assurance. The function, duties and rights of the Board as specified in the Rules is to prepare policy and program for QA review, to enforce and conduct monitoring of Practice Unit pursuant to Rules as well as and as per the QA policy and program, to recommend Council to make aware about the areas of improvement revealed in course of QA review of PU (Practice Unit), to recommend council for prohibiting audit of related entity or audit of the particular sector for the errors if revealed through QA of PU. The QA Board will carry out quality assurance of accounting professional and accounting firms compulsorily for the effectiveness of accounting profession pursuant to the provision of the Rule and as its QA policy and programs.

Practice monitoring review activity is intended to ensure the quality of audit performed and audit procedures of the practicing members are in compliance with Nepal Standards on Auditing (ISAs). Therefore, we must be aware of the fact that NSQC requires that all firms including sole practitioners establish and maintain a system of quality control to be designed to provide with reasonable assurance that firm and its personnel comply with professional standards and applicable legal regulatory requirements. The Institute as a member of IFAC we are required to satisfy IFAC’s Statement of membership obligations (SMOs) with regards to quality of audit.

In recent years our members are facing many ethical dilemmas and some of them are very complex and difficult to resolve. In this context, we need to take QA Review System as an opportunity for our entire membership to demonstrate a strong sense of ethics in the conduct of our profession by bringing out our competence, knowledge and character. ICAN is determined to ensure that its members work beyond self-interest to uphold the integrity of the profession.

We have to be mindful of the fact that our failure to comply with these aspects may be challenging to retain the authority of self-regulation of the Institute. So all the members are expected to safeguard the public interest and avoid any action that would discredit the profession.

Dear Professionals,

This is my second message after assuming office as the President of ICAN. Without a doubt, the role of our profession is important as it contributes for the development of the society and the nation. Dedicational performance in the accounting profession is necessary to shape the professional activities in the changing financial scenario. Traditional practices in accounting profession have been eliminated and new practices have emerged. In this scenario, all the accounting professionals are required to be updated as prescribed by international accounting bodies to demonstrate professionalism in their performance. We feel this is our responsibility and opportunity to prepare our members more capable and result oriented. Considering the fact that the uses of relevant Accounting and Auditing Standards is very crucial while discharging the professionalism in accounting services. It is accounting professionals’ immense responsibility to provide professional services to stakeholders.

The extensive natural calamity is now becoming common in the world and Nepal is not free from such tragedy. We are still exhilarating with the catastrophic disaster of 25 April, 2015, earthquake which took more than 8000 lives, over 25000 injured leaving hundreds of thousands homeless and damaged around USD 6.6 billion worth of properties. Due to this devastation the national economy has been affected badly which adversely affected supply system leading to low economic growth. This low growth rate also affects the overall demand which highlights the current economic scenario of our country. Discouraging business environment has been rampant and investors are not ready to invest in such situation that further declines the national GDP and employment opportunities. But we are still hopeful to rebuild the nation by standing on the new Constitution, 2072 and all the people and professionals need to be united for nation building. On the above scenario, there have been direct disruptions on the supply that impacted communities and affected sector through formal business channel and there could be a number of financial reporting

issues that have emerged as a result of natural calamity. The Institute is organizing the Conference focusing on these issues on 31 January, 2016.

In the capacity of the President it’s my pleasure to share with the members and stakeholders about some achievement made as of the Journal period and upcoming program of the Institute.

Student, Education and Educational Plan

Indeed, the chartered accountancy education is the professional course carrying better future opportunities. It is said that the student in chartered accountancy course plays vital role in educational sector hence it has become the choice for deserving and meritorious student. This course is not bound only in one single sector but also covers various sectors of market.

The Institute has recently taken some reform initiatives in line with my previous message. Such initiatives include recruitment of the staff with appropriate professional qualification in order to update and revise the study materials and this activity will be continued in the coming days also. Similarly the Institute also organized interaction program between President as well as Vice President and CAP III level students so as to listen their grievances and matters related to educational activities to explore the room for further improvement in the existing professional education. We assure to organize such interaction program on regular basis with the students pursuing CA education. We hope that their comments and suggestions received will be useful for constructive improvement of the Institute.

Apart from the chartered accountancy curriculum, the institute in coordination with Kathmandu University, School of Management has conducted the GMCS training within the framework of market requirement. GMCS program has been able to raise the awareness about the

importance of dynamics of communication in a business environment and help participants to demonstrate individual communication abilities and recognize their strengths and weaknesses.

Career Counselling is the backbone to attract the deserving and meritorious student to chartered accountancy education. So considering this fact we need to step up our efforts in order to attract brightest students to the profession and increase the future prospects and opportunities in the CA education.

With the 5th amendment in Nepal Chartered Accountant Rules, 2061, the Education Committee has been replaced by the Board of Studies (BoS) to carry out all activities of Education Committee. With the formation of Board of Studies, we are hopeful to achieve further improvement in Chartered Accountancy education in future.

We have successfully conducted Chartered Accountancy, Membership and ISA examination during the Journal period. With the view of decentralisation policy and make our students facilitated we have conducted the CAP I and CAP II examination in different branches of the Institute. I would like to congratulate the students of all levels for their achievement and welcome the CAP III students those who completed all necessary requirements for obtaining membership of Institute of Chartered Accountant of Nepal. I wish all the best for their future professional career.

Formation of Quality Assurance Board

The Government of Nepal has approved the 5th amendment in Nepal Chartered Accountant Rules, 2061 by the ministerial level decision of 2072/08/18 empowering regulatory regime of the Institute further responsive by forming an independent Quality Assurance Review Board (QARB). The Board will comprise 7 members and conduct independent inspection and monitoring of

practicing accounting firms in order to oversee quality assurance system in the accounting firms.

In accordance with provision of the Rules ICAN has formed the QARB and has commenced its functions. Pursuant to Rules the function, duties and rights of the Board has been mentioned to prepare policy and program for QA review, to enforce and conduct monitoring of Practice Unit as per the QA policy and program, to recommend Council to make aware about the areas of improvement.

Members and Professional Capacity Development

We cannot deny the significant contribution of the members in the development initiatives of the Institute and acknowledge the accounting and auditing professionals as they are the pillars for the professional development. Therefore, Institute is conducting various professional development activities and keeping them well-informed of new development in the field of accounting, auditing and other related matters for the members in time to time.

We are making our membership aware about ethical practices by publishing different notices and using various other methods. Monitoring committee of the Institute is cautious to reduce any unethical activities of the members performed by them.

The Institute conducted Diploma in IFRS Certification Course in October, 2015, jointly with The Association of Chartered Certified Accountants of UK (ACCA) in Kathmandu. The Course provided in depth knowledge of International Financial Reporting Standards (IFRS). Refresh course for the previous batch was also conducted coinciding with the regular Diploma in IFRS course.

The Contemporary Issues Discussion Committee of the Institute organized workshop under the theme of Valuation Techniques to make our membership aware on

business valuation of different sectors.

The Institute organized a workshop on Nepal Financial Reporting Standards (NFRS) Implementation Status and Preparatory Work in Commercial Banks of Nepal in Kathmandu in collaboration with Nepal Rastra Bank, the Central Bank of Nepal in October 2015. The workshop was mainly targeted for the Chairperson of the Boards/Chair of the Audit Committee/ Board Members and Chief Executive Officers of the Commercial Banks.

Institutional and Human Resources

Considering the increasing volume of the work and activities of the Institute, it is felt that to some extent the existing organizational structure and manpower is overburdened to perform each and every task efficient and effectively. Therefore, to meet the organizational goal and face the new challenges, the organizational structure is being reconstructed so as to strengthen the working environment and operational efficiency of the Institute.

The 5th amendments of Nepal Chartered Accountant Rules, 2061 have been approved by the Ministerial Level decision of Nepal Government. As per the decision total 17 Rules have been either revised or added with new provision.

The Institute of Chartered Accountants of Nepal (ICAN) conducted TOT program on Nepal Public Sector Accounting Standards (NEPSAS) in October, 2015, with the joint initiatives of Financial Comptroller General Office (FCGO).

International Relation

ICAN’s relation with the International accounting bodies is now expanding gradually. In this regard, we have visited and attended the various meetings, seminars, workshops etc. organized by different national and international Accounting Bodies of different countries for

expanding the relation with those organizations. During the reporting period, we have attended the meetings in South Korea, Singapore, and Malaysia.

ICAN Officials and other member visited Bangladesh and Sri Lanka representing ICAN to attend various Committee and Board meetings.

It is my duty to inform the entire membership that the Institute has submitted the SMO Action Plan to IFAC in December 2015.

It’s my immense pleasure to bring the notice of the entire membership that I have been selected as the Board member of CAPA representing ICAN. This has been possible due to the significant contribution of past Presidents and unflinching support of my colleagues and all the members of ICAN.

I assure to keep our members and stakeholders informed about the activities of the Institute in the next issue of our Journal.

Before I conclude my message I would like to seek the support and valuable suggestions from ICAN family and past presidents for the development initiatives of the Institute.

Best wishes !

CA. Prakash LamsalPresident

The Nepal Chartered Accountant December 2015 7

ACCOUNTING

BackgroundAbout a month back, one of my fellow colleagues came to my office after a gap of couple of years. I ardently asked to him how you are doing. He softly replied that I had just started consulting work of record keeping, tax advising and other contemporary services. I was surprised and asked him that how can you provide these services without your relevant professional qualification. He simply replied that I had not audited the books of accounts of the clients. Still I had a question that though you had not audited the books of accounts but how can you provide the non-assurance services like those. Still he had throwing to me other non-tenable logic. Finally I did not want to lose my good friend through unnecessary debate and changed the topic to other non-accounting issues like the difficulties that we are passing now a days i.e. shortage of cooking gas, petroleum products, groceries items and quality of life of people of Nepal. This is not the single case practice over here. There are many more such services

carried out by the person who has no relevant qualification, experience and knowledge in the relevant field. This would be one of the biggest challenges to the regulating body to capture these types of services within the scope of accountancy.

IntroductionThe word accountancy that had a distinctive meaning in the past is now being changed as customary to suit their own purpose by the users or service providers. The meaning of accountancy embraces a number of assignments like record keeping, preparation of financial statement, audit and assurance, financial management, consultancy, taxation and so on. Now a days, person who are directly or indirectly associated with the accountancy claimed to the public that the different practice other than assurance services they are operating are not part of the accountancy profession and it’s a kind of service provided beyond the scope of accountancy. However, all over the world, accountancy is held as embracing all these disciplines and without getting valid authority

CA. Paramananda AdhikariCA. Adhikari is a Technical Director of ICAN.

He can be reached [email protected]

Challenges and Quality of Accounting Profession

The number of cases of audit failures all over the world since last one decade raise the question about the independency of auditor and their responsibilities. To win the public trust on the audit, there has obviously led the credibility question over the profession that provides justification for need of external/oversight regulation worldwide.

The Nepal Chartered Accountant December 20158

ACCOUNTING

cannot do any of the services. So, we have that great challenge to address the issue and bring those disciplines within the meaning of accountancy in our context.

Circumstances of Audit Failures The objective of audit is to get reasonable assurance rather than absolute assurance and the opinion of the auditor shall be considered persuasive rather than conclusive. Hence, auditor must obtain a high level of assurance that the conclusion expressed in management’s assessment is correct to provide an opinion. However, if we look back to the audit failures of the past across the globe, indicates that auditor fails to understand business environments, risk assessment including error in interpreting accounting principles, application of the standards and misstatements caused by client fraud are few of them. Aftermath investigation of the failures cases, it was found that in most of the cases auditors were also involved in the fraud with the management and found guilty of the professional misconduct due to concealment of facts and information. The number of cases of audit failures all over the world since last one decade raise the question about the independency of auditor and their responsibilities. To win the public trust on the audit, there has obviously led the credibility question over the profession that provides justification for need of external/oversight regulation worldwide. Probably, the oversight regulation is related to the result of the serious audit crisis and the way out of minimizing the consequences of the crisis and its reasons.

Criticism Against the AuditorsBased on the above facts, there are some specific charges against auditors which includes, failed to obtain adequate business knowledge, failed to obtain sufficient appropriate audit evidence to corroborate management representations and explanations, failed to assess the risk attached with the business, failed to respond on over-valuation of assets, limiting the analytical and substantive procedures, limiting the sample selection procedures,

failed to exercise professional skepticism on unusual or related party transactions and issued unqualified opinion despite being aware of many accounting material misstatements and failures of disclosure of such facts. The auditing profession in Nepal is experiencing a period of serious havoc. Few years back from now, backing to raise the fake VAT billing and manipulation of accounting data of the clients were some of the severe criticism against the auditors not only by the government but public too. Further, there are heavy debates on the minimum audit fee issues of the accounting professionals for the services they discharged to the clients. This may bring to light the charges faced by the accounting professionals but who knows the problem actually they are facing to uphold their profession.

Practicality of Audit ServicesThe audit function is governed through the theory of agency that the owner will monitor the management activities through audit function carried out by independent professional accountant. However, in Nepal audit is mandatory for all companies incorporated under the Companies Act, 2006, despite of their size and ownership structure i.e. private or public companies. According to the provisions of sections 108 and 109 of the Act, the management of the company is responsible to maintain the accounts of the company, annual financial statements and report of the Board. Similarly, sections 110, 111 and 115 of the Act, every company incorporated under the Act needs to have its financial statements duly audited by an independent auditor. This is a mandatory provision even for the small company. The low perceived value of the audit function is challenge facing audit practitioners in Nepal. Nevertheless, the mandatory audit requirement for the companies whether large or small, the actual contribution of auditing towards its intended purposes is somehow limited. This is because significant numbers of companies in Nepal are private companies incorporated under the Act as opposed to public companies. And

The Nepal Chartered Accountant December 2015 9

ACCOUNTING

majority of these private companies are owner-managed. Hence, an audit would be worthless to most of the private companies because the directors and the shareholders are ultimately the same persons. Due to this reason, most audit clients have found an audit function as a non-value adding activity and perceive it to be a costly process to them paying money to the auditor just for signing the financial statement. They totally ignore about the responsibility taken over by the auditors on issuing the audit report. The most noticeable value of auditing for the private companies is merely adding trustworthiness to the financial statements for the purpose of tax return to the Inland Revenue Department (IRD) and for the loan applications to the bank and financial institutions to catch the credit facilities.

Quality of Audit ServicesIn contrast with the usefulness of audit services in the private companies, audit function has a more significant role for public companies since it serves the purpose of reporting to their existing shareholders and attracting further investment. However, the practical usefulness of auditing may only be pertinent to a limited group of users such as bankers, regulatory bodies, institutional investors and large stakeholders such as IRD, NRB, Office of the Company Registrar and VIP shareholders. As opposed of these, by and large public do not actually rely on the audited financial statements for their decision making purposes. As a result, over the years, it is realized that the audit has gained very little recognition from a large section of the public. Another problem underlying the audit practice in Nepal is the inability of the public to make a fair evaluation of auditors’ performance. Public do not have adequate knowledge and ability to understand the quality of an audit. Public judgment of audit quality will only come out as a result of subsequent events (situation of failing) which more often negative reporting by the media that an audit has not been performed with due care. The issue of audit quality versus audit fees has

been a major concern of the auditing profession in Nepal since many years from now. Due to this, audit quality is likely to be sacrificed by the client as a result of low audit fees and the audit clients may not be interested for higher audit quality or the audit clients may not be able to judge the audit quality as it should be.

ConclusionPerhaps, higher moral value, competency and improved qualities of services are few of the fundamental principles of profession to enhance the scope, trust and credibility of auditing profession. Educating the public and various stakeholders on the nature, objective and expected outcome from an audit that may help the public to recognize the value of auditing and the value addition made by the auditors work. Stringent regulation alone may not be only solution in promoting qualitative and better practices of auditing.

The Nepal Chartered Accountant December 201510

ACCOUNTING

1. International Public Sector Accounting Standards in Nepal

The Financial Comptroller General Office (FCGO) is in the process of extending the pilot use of Nepal Public Sector Accounting Standard (NPSAS). The NPSAS corresponds to a large extent the requirements laid down in the cash basis International Public Sector Accounting Standard (IPSAS). Twelve more centre-level agencies would be preparing their consolidated statements using the NPSAS by the end of this financial year (2015-16). It is expected that the NPSAS would be used to prepare the consolidated statement of all 44 central-level agencies within the next three years. A number of trainings are being conducted to disseminate the underlying ideas of NPSAS to government accountants at different levels and to make them capable of preparing the consolidated statements, as required by the NPSAS. Once the adoption of the NPSAS across the central-level agencies is accomplished, the FCGO intends to initiate a step towards the

accrual basis of IPSASs.

What is worth mentioning is that six years have already been passed since the government first approved the use of NPSAS by budgetary entities. Some important changes have occurred in international public sector accounting standards during these years. For instance, the International Public Sector Accounting Standards Board (IPSASB) has recently announced that it will facilitate the revision of the cash basis IPSAS following the recommendations of the Task Force, which it had established in 2010 to review the use of the standard in developing nations. In another development, the Europe Commission (EC) has clarified that the accrual-based IPSASs cannot be implemented in Europe in their present form and has put forward a proposal for developing a separate European Public Sector Accounting Standards (EPSASs) for its member states. This paper aims at providing an update of contemporary developments taking place in international public sector

Dr. Pawan AdhikariDr Pawan Adhikari is a Lecturer in

Accounting at Essex Business School. He can be reached at [email protected]

The Legitimacy of International Public Sector Accounting Standards (IPSASs)

The government/FCGO should consider an incremental approach to public sector accounting reform extending the use of modified version of cash accounting and then gradually migrating towards a simpler form of accrual accounting.

The Nepal Chartered Accountant December 2015 11

ACCOUNTING

accounting standards. This understanding might be valuable both for the government/FCGO and accounting profession in the process of implementing the NPSAS and developing a reform strategy for future public sector accounting reforms.

2. Revisiting the Cash Basis IPSASThe global accounting profession and international organisations, mainly the World Bank, are of a view that the adoption of accrual accounting cannot be an immediate solution for developing countries to improve their poorly performing public sector accounting. The challenges in implementing accrual accounting and the costs incurred in the implementation process are unfolding, as more and more European governments have moved towards the accrual basis of accounting. For instance, the European Commission (2012, 2013) has in its reports assumed that the costs of moving away from a cash-based accounting system to an accruals-based accounting system for the central government alone in a medium-sized member could reach up to EUR 50 million given the expense of putting into place the new standards, the associated IT systems, and appropriate training and education. In the same report, it is mentioned that France had spent in excess of EUR 1,500 million on articulating accrual accounting and budgeting reforms over the last decade. Given the costs incurred in the transition process, some countries have been even forced to move back and adopt a step-by-step approach to accrual accounting starting the reforms from their ministries rather covering the entire public entities.

The global accounting profession and the World Bank have therefore urged developing countries to sequence their public sector accounting reforms, beginning with the adoption of the cash basis IPSAS, with a possible move towards accrual accounting in the longer-term. The adoption of the cash basis IPSAS has, however, appeared to be a problematic in many developing nations. Certain requirements of the standard, for instance,

full consolidation, reporting external assistance and third party payments, have proved impractical in many countries (see e.g. IFAC, 2010). Wynne (2013) claims that “at least 31 governments in Africa have tried to adopt this standard, but its key requirements have not proved practical”. The PriceWaterCoopers’s (PwC) report is another illustration in this regard. It is mentioned in the report that not a single government has been able to fully implement the core requirements of the cash basis IPSAS (PwC, 2013).

Such ambiguities in implementing the cash basis IPSAS have also been acknowledged by the IPSASB, the developer of the cash basis IPSAS. In 2008, the Board had established a Task Force with a view to identifying the areas/issues within the cash basis IPSAS that have apparently become an obstacle in extending its use in developing countries. The Task Force was also assigned to make recommendations as to whether the cash basis IPSAS should be modified, or if further guidance should be provided in light of the challenges that the countries had experienced in its implementation. In its report submitted to the IPSASB in 2010, the Task Force had raised concerns over several issues, consolidation being the primacy one. In addition to the Task Force, the International Consortium on Governmental Financial Management (ICGFM), which is reckoned to be a strong supporter of the cash basis IPSAS, had also submitted detailed proposals for amending the cash basis IPSAS. Due to the issues related resource constraints, the IPSASB was not in a position until recently to address the recommendations of both the Task Force and the ICGFM.

In 2015, the IPSASB, however, agreed on a project brief proposing that the cash basis IPSAS be reviewed to respond to certain recommendations of the Task Force. In its meeting which was held in Toronto in June 26, 2015, the IPSASB had on its agenda a review of the cash basis IPSAS. An entire session of the meeting

The Nepal Chartered Accountant December 201512

ACCOUNTING

was devoted to setting directions for the preparation of a first draft of an Exposure Draft (ED) identifying the potential amendments to the cash basis IPSAS. Some of the potential amendments to the standard discussed in the meeting included;

• shifting the consolidation requirements from part 1 (required) to part 2 (optional) and providing countries the option of either consolidating their financial statements or publishing them as stand-alone statements

• shifting the requirements for third-party payments from part 1 to part 2 and provide each country an option of reflecting third-party payments in their financial statements

• accommodating the requirement of external assistance in part 2 instead of part 1 so that each country will have the option of reflecting the extent of external assistance that they receive, and

• addressing the ambiguities in dealing with foreign currency and treasury single account transactions, amongst others.

An agreement was made in the meeting to action a limited scope review of the cash basis IPSAS so as to:

• propose amendments to requirements in part 1 of the cash basis IPSAS dealing with consolidation, external assistance and third party payments,

• propose limited “housekeeping” changes where necessary to ensure that the requirements remain appropriate, and

• clarify that the adoption of the cash basis IPSAS is intended as an intermediate step on the road towards accrual accounting, not an end in itself.

It is expected that this agenda of revising and simplifying the cash basis IPSAS will be endorsed in the next IPSASB meeting, which is scheduled in March, 2016.

3. The Applicability of the Accrual Basis IPSASs

As part of improving public sector governance, a large number of European countries have in the last decade adopted some degree of accrual accounting in their public sector (Ernst & Young, 2012; PwC, 2013). Organisations such as the IMF and the European Commission and the professional accounting associations and accounting firms have envisaged accrual accounting a means not only of tackling the evolving sovereign debt crisis in Europe, but also of avoiding the future financial crises. Despite the widespread use of accrual accounting, only few counties (except UK, Australia, New Zealand and Switzerland), however, have shown an interest in adopting the accrual basis of IPSASs. Mentions are made that the accrual basis of IPSASs have appeared inadequate to address the requirements of most of the central European governments in which public finance is centred around the annual budget (European Commission, 2012, 2013). For instance, countries such as Italy and Slovakia, have expressed concerns over the lack of public-sector-specific provisions in the IPSASs for recognising and measuring pension liabilities, social benefits, tax revenues and historical costs (Ernst & Young, 2012).

In a similar view, several EU member states have raised concerns over a lack of provisions in the IPSASs to address the main intangible asset inherent to the government, i.e. the power to levy taxes. The IPSASs have also come short in many counties in dealing with non-exchange transaction expenses, i.e. taxes and transfers, employee benefits, public debt and government revenues. For instance, non-exchange transaction expenses have been the main expense within many European central governments and some other public entities; there are however no IPSASs available for those expenses. In addition, IPSAS 23 has turned out be irrelevant in a number of European governments given that their revenue sources have been very broad rather than defined in the standard. Similarly,

The Nepal Chartered Accountant December 2015 13

ACCOUNTING

IPSAS 29 has appeared inapplicable in many European countries and do not have a developed system that could separate commissions and expenses for their public debt.

The significance of the IPSASB’s proposed conceptual framework has also been questioned by many EU member states. Having spent nine years and eight public consultations with the global constituency, the IPSASB has recently approved its “Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities” (Christiaens & Vandendriessche, 2015). The IPSASB claims that the framework has been developed by giving a special attention to specific public sector-related issues, and that it would provide a basis for preparing high-quality reports for both accountability and decision-making purposes. However, evidence shows that the notion of government control used in the conceptual framework has proved problematic in a range of countries. The accountability mechanisms in the European public sector are primarily focused on the use of budget appropriations and on the services provided and effects achieved from the point of ‘value for money’. This also means that the budgets statements and performance reporting, rather than the general purpose financial statements as prescribed by the IPSASs, would continue to form a basis for discharging accountability in the public sector. Furthermore, questions have been raised about the way the users of financial statements have been identified in the conceptual framework. The citizens, resource providers, legislators, and other service recipients and their representatives have been reckoned to be the key users of the financial statements in the public sector, without any actual interviews or field work having been undertaken to specify their requirements and their varied information needs (Christiaens & Vandendriessche, 2015). Countries are also of the view that the framework would have been introduced prior to the issuance of standards rather than when the standards are fully developed.

In its assessment report, the European Commission (2012) has underscored several critical issues relating to the accrual basis IPSASs, such as, the governance of the IPSASB, the relationship between the IPSASs and the European Systems of Accounts and the ‘left out of budgeting’, amongst others, and explicated that the accrual basis of IPSASs cannot be implemented in the EU member states as they currently stand. Using the IPSASs as a starting point, the European Commission (2013) has made a recommendation for the development of a set of harmonised public sector accounting and budgeting standards, i.e. the European Public Sector Accounting Standards (EPSASs) for the member states. This trend towards the EPSASs has certainly become a caveat, warning not only against the suitability of the IPSASs but also against their future adoption by EU member states.

4. Alternative Reforms to NepalThe fact that a large number of countries, both developed and developing, have referred to the IPSASs, while articulating their public sector accounting reforms, cannot be denied. However, there is no evidence that any country has fully complied with the requirements laid down in the IPSASs. The applicability and legitimacy of both the cash and accrual basis IPSASs have therefore raised concerns at a global level. Claims that a large number of countries are embarking on a move towards the IPSASs can therefore be contested. For instance, developing countries have failed to cope with several requirements of the cash basis IPSAS relating to the disclosures of third-party payment and external assistance and the preparation of consolidated statements. In a similar vein, Europe has rejected the accrual basis of IPSASs mentioning that the standards lack provisions for operating the budget, a key governance tool in the public sector and for tackling various other non-exchange transaction expenses, for instance, taxes. The Europe Commission (2012) has therefore proposed the development of a separate set of European Public Sector Accounting Standards (EPSASs)

The Nepal Chartered Accountant December 201514

ACCOUNTING

for its member states instead of adopting the accrual-based IPSASs.

Given this, concerns can therefore be raised whether it is time for Nepal to revisit its government accounting reform strategy and plans. Instead of devoting its energy and resources to implementing the NPSAS and developing consolidated accounts, it may be better to search for an alternative approach to improving the accounting practice. For example, the promotion of certain aspects of modified cash accounting could be one alternative. A large number of governments in Latin America have in recent years moved from pure cash accounting to a modified-version of cash accounting by disclosing certain aspects of receivables, payables, borrowings and other financial liabilities, non-cash assets, and accrued revenue and expenses. The paper therefore suggests that the government/FCGO should consider an incremental approach to public sector accounting reform extending the use of modified version of cash accounting and then gradually migrating towards a simpler form of accrual accounting. Only through the adoption of such approach the future federal and states governments would be able to demonstrate their financial viability and discharge their accountability to the citizens.

References:Christiaens. J., & Vandendriessche, F. (2015). IPSASs conceptual framework: a comment. CIGAR Network Newsletter, 6(2), 2.

Ernst & Young. (2012). Overview and comparison of public accounting and auditing practices in the 27 EU member states. UK.

European Commission. (2012). Public consultation – assessment of the suitability of the International Public Sector Accounting Standards for the member states. Summary of responses. Brussels: EUROSTAT.

European Commission. (2013). Towards implementing

European Public Sector Accounting Standards (EPSAS) for EU member states – public consultation on future EPSAS governance principles and structures. Public Consultation Paper. Brussels: EUROSTAT.

International Federation of Accountants (IFAC) (2010). Review of the cash basis IPSAS -Report of the task force (agenda paper 6.1). Vienna, Austria.

PWC. (2013). Towards a new era in government accounting and reporting. PWC:

PwC Global survey on accounting and reporting by central governments.

Wynne, A. (2013). International public sector accounting standards: compilation guide for developing countries, International Consortium on Governmental Financial Management. http://www.scribd.com/doc/134603499/ICGFM-Compilation-Guide-to-Financial-Reporting-by-Governments.

The Nepal Chartered Accountant December 2015 15

ECONOMY

The current economic difficulties and shortage of essential goods are the result from non-economic activities. Major factors of current crisis are political mistrust, border unrest and blockade. Political instability has significant impact on the economic growth as the market always negatively respond to Non-economic turmoil.

The political implications for the market are as important as the economic effects. The collapse of the supply system further amplified anger at ground level, sending a wide ramification throughout the Nepalese population. It was further accelerated by opportunists who want to fulfil their political dream and translate them into political benefits.

We stand at movement of great challenge and great opportunity. We are facing worst economic crises in generation, in part because of complex political situation. These difficult times are not a result of accident of history. There are a number of composite political

and legal issues which were not handled prudently. To be sure, some of these problems are results of unprecedented political development that could have been easily avoided. The recent turmoil does not condone our mistake!

Due to various reason price of daily necessitates from groceries to fuel had been skyrocketed. Many of us are worry about whether we will be able to raise our kids in safety and security and give them a better life. It is easy to feel as if that dream of boundless opportunity that should be right of all Nepalese is slipping away. Our country needs to provide economic opportunities to the people to fulfil their dream. We need to provide economic security to private sector with continual spread of benefit to the general public.

Economic policy need to protect the interest of the working families that are backbone and the engine of our economic growth. It is a complex phenomenon which not merely concerns the national policy or behaviour of political leaders

CA. Anal Raj BhattaraiCA. Bhattarai is a Fellow Member of ICAN.

He can be reached at [email protected]

Nepal Unrest: The Fault Line

Every institutions who are responsible for bringing current situation has been adversely affected by the crisis but, the general public has been affected the worst. The reasons for these failures can be clearly understood, it happened apparently because lead players had miscalculated the effects.

The Nepal Chartered Accountant December 201516

ECONOMY

but also touches upon the very structure of our country. We must create bottom-up growth that empowered hardworking families to climb the ladder of success and raise their children with security, opportunity, and hope for better future. These hopes are at the heart of Nepalese people. Yet despite of the resilience, optimism, and hard work of Nepalese people, their dreams too often have been frustrated.

In difficult times, there's less room for ambiguity in defining goals. To meet our challenge, we must summon our common faith in our values - "the sense of who we are, and what is our limits". We are at critical juncture of time, to lead Nepal at this critical moment in history, we require more rational judgements. We cannot simply look backward for finding solution to the complex economic problems.

Today’s political crisis needs to be analysed very carefully. Constitution promulgated by Nepalese Constitution Assembly may or may not be able to address concerns of all sections of the society but it has been able to emphasise on freedom of economic activities, unquestioned right to properties, smooth and free flow of goods and services etc. To encourage investment activities government must guarantee uninterrupted supply system. The demand, production, trade and transport are the major basis of market selection. We learnt our lesson.

When the economy takes a downturn, wise market player usually respond by changing their financial behaviour. Even though constitution has secured economic rights of all, Corporate Investors do not blend with political instability as a result of which they will book profits and go to another country. Further, crisis like today definitely encourage investors to make larger and riskier investments during the upswing of the business cycle and to cut back in their investments during the downturn, increasing rather than damping the instability of the financial markets and the volatility of the underlying

real economy.

The integrity of political system and the public’s trust in those system are essential to the economic well-being of a nation. The soundness and the sustained prosperity of the country depends on the notions of fair dealing, responsibility, and transparency. Unfortunately—there has been cases of mistrust and confusion—we witnessed an erosion of standards of responsibility and ethics that exacerbated the political crisis. The Political system has been thus suffering from mistrust (lax governance, falling confidence, ownership and slow acceptance) through the fault in its own inabilities. The problem that we are facing is unique to our country. Though, the constitution has been able to address legitimate demands of various sections of societies, the political system has not been able to take venerable section in confidence. Serious flaws exist in the short-term vision of our political players.

Considering the situation in various part of country our political system should have taken some rational steps to deal with them so that they could have easily avoided those elements which can disintegrate country. They should have played a role to consolidate all Nepalese in to one roof. The political turmoil, when it appeared in some section of societies, or more precisely, in the Tarai regions but now the ramifications of turmoil had wider effect which crossed the Nation and had crossed maximum economic losses The problems we faced are not only political but it has rather affected the survival of people. This has had negative impacts on investment activities therefore the government must guarantee an uninterrupted supply system and support free market.

Every institutions who are responsible for bringing current situation has been adversely affected by the crisis but, the general public has been affected the worst. The reasons for these failures can be clearly understood, it happened apparently because lead players had miscalculated the effects.

The Nepal Chartered Accountant December 2015 17

ECONOMY

Under present condition, reconciliation with each one is necessary to remove the mistrust. If this continues, we expect that, the entire system, may become incapable of carrying out even the simplest of steps involved in the conversion of savings into investment or the financing of home building, personal consumption, or development.

There is a deep fault in our approach both politically, economically and diplomatically, we are not been able to design proper solution for current crisis. Further the crisis had not been managed smoothly. It seems our Political System does not process information efficiently, or well. Any solution must take account of the socio-economic costs of the crisis as its starting point, because these are disproportionally affecting the country economy as well as the poor and labour more generally.

Assuming that our political system cannot be fully reformed, measures must be taken to place a ring around the system’s core called “politic”. A stable political system is a means to an end, not an end in itself, and the ends that matter are social justice and economic development. The merit of the political system should not be judged merely in terms of the stability that it promotes or in terms of the growth, innovation, and investment that it may encourage. The political arrangements should also be judged in terms of how effectively they promote social justice.

We must analyse the magnitude of the impact of current crisis and its impact on social harmony and loss of businesses confidence. We need an emergency economic plan to jump-start the economy and get our economy back in track. We must adept our policies that can triggered a fundamental changes in the economy and create wide spread opportunity and economic prosperity; we need to make commitment towards future generations, so that, they know, we care:-

1. To move beyond the bitterness,

2. To arrive at consensus,

3. Fulfil our responsibility for the Nation,

4. To start the path for economic development and reconstruct our Nation.

We know, once we overcome with our political difference, other complex economic and legal issues can be easily resolved to ensure sustainable economic development. We are confident on our abilities and we must look forward, do work efficiently and maintain good relation with our neighbouring countries.

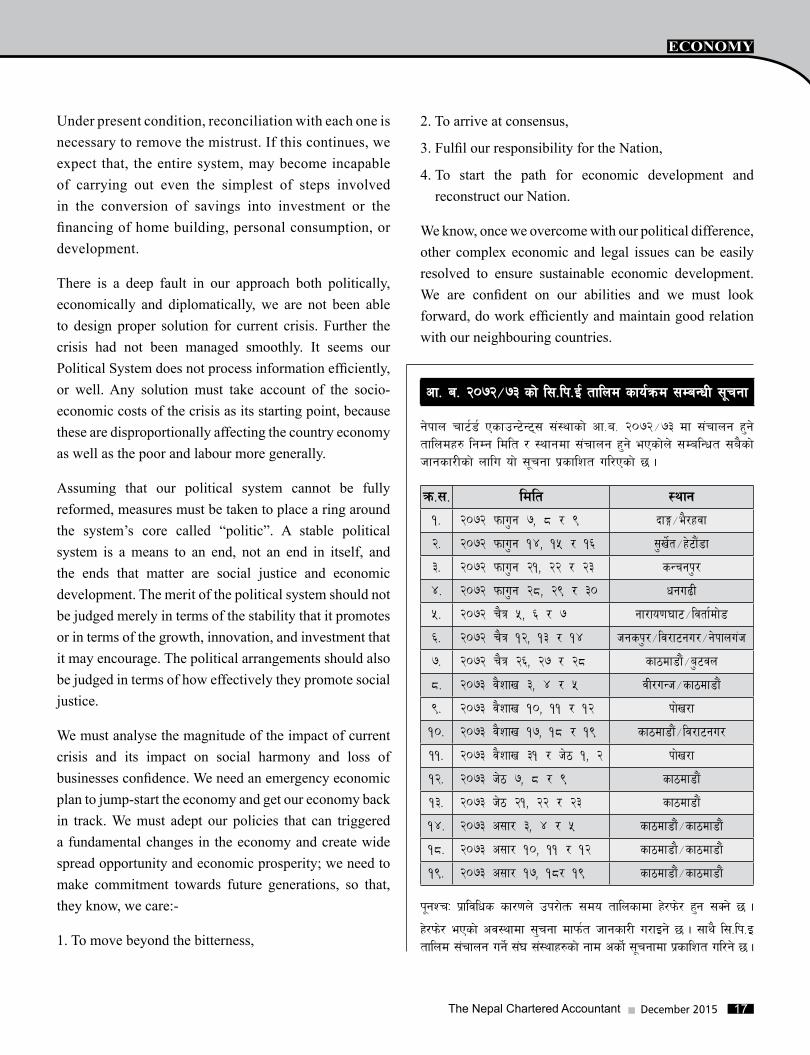

cf= a= @)&@÷&# sf] l;=lk=O{ tflnd sfo{qmd ;DaGwL ;"rgf

g]kfn rf6{8{ PsfpG6]G6\; ;+:yfsf] cf=a= @)&@÷&# df ;+rfng x'g] tflndx? lgDg ldlt / :yfgdf ;+rfng x'g] ePsf]n] ;DalGwt ;a}sf] hfgsf/Lsf] nflu of] ;"rgf k|sflzt ul/Psf] 5 .

qm=;= ldlt :yfg1= 2072 kmfu"g 7, 8 / 9 bfé÷e}/xjf

2= 2072 kmfu"g 14, 15 / 16 ;"v]{t÷x]^f}+*f

3= 2072 kmfu"g 21, 22 / 23 sGrgk"/

4= 2072 kmfu"g 28, 29 / 30 wgu(L

5= 2072 r}q 5, 6 / 7 gf/fo)f#f^÷ljtf{df]*

6= 2072 r}q 12, 13 / 14 hgsk"/÷lj/f^gu/÷g]kfnu+h

7= 2072 r}q 26, 27 / 28 sf&df*f}+÷a"^jn

8= 2073 j}zfv 3, 4 / 5 jL/uGh÷sf&df*f}+

9= 2073 j}zfv 10, 11 / 12 kf]v/f

10= 2073 j}zfv 17, 18 / 19 sf&df*f}+÷lj/f^gu/

11= 2073 j}zfv 31 / h]& 1, 2 kf]v/f

12= 2073 h]& 7, 8 / 9 sf&df*f}+

13= 2073 h]& 21, 22 / 23 sf&df*f}+

14= 2073 c;f/ 3, 4 / 5 sf&df*f}+÷sf&df*f}+

18= 2073 c;f/ 10, 11 / 12 sf&df*f}÷sf&df*f}+

19= 2073 c;f/ 17, 18/ 19 sf&df*f}+÷sf&df*f}+

k"gZrM k|fljlws sf/0fn] pk/f]tm ;do tflnsfdf x]/km]/ x'g ;Sg] 5 .

x]/km]/ ePsf] cj:yfdf ;'rgf dfkm{t hfgsf/L u/fOg] 5 . ;fy} l;=lk=O tflnd ;+rfng ug]{ ;+3 ;+:yfx?sf] gfd csf]{ ;"rgfdf k|sflzt ul/g] 5 .

The Nepal Chartered Accountant December 201518

ECONOMY

1. Past GrowthOn an annual basis, Nepal’s growth for the last four decades (1975/76-2014/15) averaged at a lower single digit of 4.2 percent. Population growth during the period averaged at 1.8 percent. So, Nepal’s per capita gross domestic product (GDP) growth during the four decades averaged at 2.3 percent. However, talking about our neighbors, the average per capita GDP growth during the 34-year period (1980-2015) was 9.0 percent in China and 4.5 percent in India, according to World Economic Outlook Database (IMF, October 2015). According to GDP figures published by the Central Bureau of Statistics of Nepal, the pre-democracy period (1975/76-1989/90) recorded an average growth of 3.9 percent while the post-democracy period (1990/91-2014/15) experienced an average growth of 4.4 percent. The highest growth rates recorded were in 1983/84 (9.7 percent), 1993/94 (8.6 percent), 1980/81 (8.3 percent), 1987/88 (7.7 percent), and 1990/91 (6.4 percent). During the three years,

namely, 1984/85, 1999/00, and 2007/08, the growth rate recorded in each of these years was 6.1 percent. The growth rates were 5.3 percent each in 1995/96 and 1996/97, 5.6 percent in 2000/01, and 5.4 percent in 2013/14. Rest of the 28 years witnessed growth rates below five percent. During the last nine years (2006/07-2014/15), the growth rate averaged 4.4 percent. During the current fiscal year 2015/16, the economy is heading for negative growth on account of so called economic blockade. Two previous blockades imposed by India were in (a) 1969 and (b) 1988/89 and 1989/90. The growth rate then was not negative. Actually, the growth rates recorded in 1988/89 and 1989/90 were positive 4.3 percent and 4.6 percent respectively. During the last four decades, there were previously two episodes of negative growth occasioned by large negative agricultural growth—in 1979/80 and 1982/83. The negative growth recorded in these two years was 2.3 percent and 3.0 percent respectively. In 2001/02, almost nil growth was recorded yet the growth (0.1 percent)

Mr. Tula Raj BasyalMr. Basyal is a Former Executive Director of

Nepal Rastra Bank.He can be reached at

Managing Risks Facing the Economy

Increasing and managing wider and deeper interrelationships with the global economy would be essential for enhancing the efficiency and effectiveness of the economies in the modern world. Globalization means increasingly integrating with the world economy through introducing facilitative changes and arrangements so that the benefits of the associated openness, competition, reform, and restructuring are available to the stakeholders at a faster pace and rising scale.

The Nepal Chartered Accountant December 2015 19

ECONOMY

was positive. We can, therefore, observe that the negative growth during this year will be the first such evidence in 33 years.

2. Effects of BlockadeThe effects of so called blockade now continuing for over four months are evident throughout daily lives of people and in every sector of the economy. The immediate and short-term costs of the blockade are catastrophic. The long-term costs of the blockade are even hard to guess. The shortage of fuel, food, medicine, other essential commodities, and industrial raw materials has hardest hit the people’s lives. Transportation in the country has been paralyzed. The Terai Bandha has crippled normal life. Closure of educational institutions has created uncertainty about the future of the children. Closure of about 2,200 industrial establishments and disruption of business activities has resulted in colossal loss in terms of lost output and employment. Blockade near the border points has severely affected Nepal’s transit facilities and resulted in revenue loss worth billions of rupees. The supply chain associated with domestic and foreign trade has been disrupted. As a result, scarcities and price rise of essential commodities have been the normal occurrence. The size and reach of Informal economy has been on the rise. Development projects in the public sector and investment activities in the private sector have been disturbed. On the whole, the economy’s consumption, investment, and external trade have been affected. Business confidence and competitiveness of the economy have declined. Unemployment has been on the rise. Consequently, the ratio of population living below the poverty line must have increased by a couple of percentage points more. Therefore, the 13th Plan (2013/14-2015/16) target of reducing the population below the poverty line to 18 percent by 2015/16 from 23.8 percent at the end of 2012/13 is unlikely to be attained. Nor will there be favorable outcome in the goal of elevating Nepal to the status of developing country by 2022 from the present

status of LDC. Other targets of the 13th Plan are also likely to be unmet.

3. Globalization as the Present TrendGlobalization is defined as the process of enhanced economic interdependence and integration among nations. Increasing integration is seen today in the dramatic growth in the flows of goods, services, and finance across national borders. Goods, services, finance, and even manpower markets across the globe are being liberalized, becoming more competitive and getting increasingly integrated. The restrictions in their transactions are being reduced through implementation of rule-based institutional arrangements, both at the regional and international levels. Institutions and fora like the Bretton Woods institutions; WTO, BIMSTEC, Group of Twenty, regional trading arrangements like the South Asia Free Trade Area, etc. are supporting this process. Increasing and managing wider and deeper interrelationships with the global economy would be essential for enhancing the efficiency and effectiveness of the economies in the modern world. Globalization means increasingly integrating with the world economy through introducing facilitative changes and arrangements so that the benefits of the associated openness, competition, reform, and restructuring are available to the stakeholders at a faster pace and rising scale. In fact, globalization is the process of expanding and intensifying the transactions and interrelationships with the global economy so as to make the domestic economies efficient, productive, and competitive.

One major component of globalization is the steady increase in the international trade as a share of GDP. Globalization is supported by a continuous drop in the transportation and associated costs along with declining tariffs and barriers to trade. Essentially, globalization reflects an extension of specialization and division of labor to the entire world. Global integration of goods and financial markets has produced impressive gains from

The Nepal Chartered Accountant December 201520

ECONOMY

trade in the form of lower prices, increased innovation, and more rapid economic growth. However, these gains have sometimes been accompanied by adverse side-effects. One consequence of economic integration is the unemployment and lost profits that occur when low-cost foreign producers displace domestic production. To address such interests, some arrangement of protectionism in the form of tariffs and quotas on international trade is sometimes advocated. Globalization could raise many new issues for policymakers as it has both positive and negative connotations. A prudent step would be to strive to make globalization a better instrument for a country’s prosperity. Inability to do so would only reflect ones ignorance in skillfully managing the dynamics of the domestic economy in the face of rising currents of the process of globalization. Inability on the part of national authorities to manage successfully the process of globalization due to lack of vision and failure to introduce necessary enabling and mitigating measures should not be viewed as the demerits and defects of the globalization itself. Are the gains from trade worth the domestic costs in terms of social disruption and dislocation? Does integration lead to greater income inequality? The policymakers with the responsibility to deal with globalization have to think about such questions.

4. Neighbors’ Wrong Policies in the PastNepal realized the importance and appreciated the virtues of increasing economic interrelationships with the world economy six decades ago and, consequently, adopted liberal trading regime, private sector-friendly investment climate, and other conducive policy arrangements. However, the control-based policies of the neighbors exerted pressure on Nepal to abandon the liberal regime and start pursuing the control-fostering policies, thereby dismantling from the roots Nepal’s vision and quest for rapid economic transformation. Our neighboring countries then loved and glorified the system of licenses, permits, quota, and inspection raj as the means for

economic transformation under the popularized slogan of creating socialistic society. Under the hangover of centuries of colonialism, they intentionally forced people to wrongly believe that economic liberalization was another form of colonization. They showed that they hated everything foreign and also discouraged growth of domestic private sector entrepreneurship and investment for their real fear that the domestic capitalists could snatch the politicians’ new-found luxury of controlling and exploiting the economy and the masses. However, they forced the masses to believe that all these controls were meant for making them rich and increasing their welfare. The policies adopted by the politicians penalized people who wanted to pursue prosperity and happiness through their hard work, enterprise, innovation, and efficiency. In the process, the politicians succeeded in amassing personal wealth and transformed themselves into a highly prosperous lot. They turned their economies into the most underdeveloped ones and pushed their countrymen into the abject poverty, misery, squalor, decline, and decay. The economies became most unproductive and the people became the most under-privileged. They were successful in making South Asia the abode of highest number of poor and destitute. The wrong policies succeeded in not only producing massive scale of poverty, unemployment, and underdevelopment but also transmitting the negative spill-over effects on the countries neighboring them. The only beneficiaries of this drama of incompetent handling of the economic management were none other than the whole lot of new political masters who falsely championed the cause of socialism to serve their real object of themselves becoming the biggest capitalists. When people finally woke up to the fallacies of such wrong tactics perpetrated by the politicians, many precious decades were already lost for the people and the economy. When the control-loving politicians also sensed that the drama of deception and cheating so far orchestrated would not become sustainable, they were forced to review it and introduce hesitatingly the liberal regime which they

The Nepal Chartered Accountant December 2015 21

ECONOMY

thought would widen the economic inequality. Since the adoption of these policies 25 years ago, substantial changes have occurred in these neighboring economies. The positive effects of liberal economic regime based on increased foreign direct investment (FDI), fostered productive domestic investment, and adoption of prudent macroeconomic and sectoral policies have been evident in these countries. Due to good policies, the previously poverty-producing economies have thus started creating wealth and prosperity. People have started to believe that they can become rich through hard work and enterprise instead of dishonesty.

5. Globalization Benefits for NepalNepal immensely benefitted from globalization. Sectoral areas of investment and economic activities have widened and deepened. Financial sector, civil aviation, mass communication, transportation, hotels and restaurants, cooperatives, NGOs, social infrastructure like educational and health institutions, etc. are fast progressing. Rising public resources and their more productive and equitable distribution have fostered better allocation of resources. Literacy and health indicators have improved. The ratio of population falling below the poverty line also came down fast. However, the current blockade is a vain attempt to deny Nepal the benefits of liberalization and globalization policy hitherto adopted by Nepal.

6. Assumptions behind Adopted Policy Regime

In the era of globalization and deregulation where each country is interlinked to the global economy, it is assumed that countries will foster, and not inhibit, the transit and border trade. It is assumed that the landlocked countries are offered unrestricted transit facility and the provisions of WTO, other international conventions like the UN Convention on Transit Trade of Landlocked States (Vienna Convention, 1965) and UN Convention on the Law of the Seas (1973), and also the bilateral agreements are respected. The minimum assumption for choosing

and pursuing any policy regime are the continuation of the status-quo by the external environmental factors. For close neighborly country with open border, the validity of such assumption becomes far greater. However, such assumptions get violated by bigger neighbors and no corrective mechanism for enforcing them is presently in sight.

7. Conclusion and SuggestionsTo minimize the risks and overcome the negative consequences of the so called blockade, the following measure should be adopted:

* For more agricultural production and productivity, Government should introduce policy reforms and support increased investment in agriculture, forestry, and fishing

* More investment should be channeled towards mining and quarrying with focus on extracting gas

* Government should introduce policy reforms and support increased investment in hydro-power and other sources of power

* Policy of prioritizing the regulated development of financial intermediation area should be continued

* Focus on real estate, renting, and business activities

* Enhance the capacity utilization of hotels, restaurants, and other tourism-related activities

* Prioritize development of education and health sector

* Focus on promoting community and social activities

* Manufacturing industries with indigenous raw materials and components should deserve priority

* Government should introduce policy reforms and support increased investment in construction

* To the extent possible, consumption and investment should be based on domestic products.

The Nepal Chartered Accountant December 201522

INFORMATION TECHNOLOGY

Contextual Background During the past few years, we have seen an increasing move from paper documents to electronic documents. With ever growing adoption of electronic transactions, there needs to be a mechanism to trust those digital documents at a level of signed paper documents or better. The major factor that determines the trustworthiness and legal enforceability of digital documents or electronic transactions is the ability and easy mechanism to establish that the transaction has been initiated by the party in question, that the document is not-altered before it reaches the recipient and when needed it can be validated and proved in the court that the document was signed and sent by the party in question.

It has been long since we have benefited from digital signature, knowing or unknowingly. For instance, when you download some update from Microsoft, the update is digitally signed and you can verify that the update is indeed sent by Microsoft and not by any bad party who wants to send some

spyware to your computer disguised as a genuine Microsoft update. Major software vendors release their software and updates digitally signed so that you can verify and be assured that the files received are not viruses or spywares.

Similarly, when you fill a form to apply for passport or file an income tax return with the document or message digitally signed by you (this will happen in near future), the passport or income tax office should be able to verify that the document was really send by you; and on the other hand, when you receive a notice from income tax office, bank or court, you should be able to verify that the document was really sent by the respective office and it is not a con to deceive you and steal your information.

A digital signature scheme offers a cryptographic analogue of handwritten signatures that provides much stronger security guarantee. Digital signatures serve as a powerful tool and are now accepted as legally binding in many countries

CA. Mukunda PokharelCA. Pokharel is a Member of ICAN

He can be reached [email protected]

Dimensions of Digital Signature

Digital Signatures provide a viable solution for creating legally enforceable electronic records, closing the gap in going fully paperless by completely eliminating the need to print documents for signing. Digital signatures enable the replacement of slow and expensive paper-based approval processes with fast, low-cost, and fully digital ones.

The Nepal Chartered Accountant December 2015 23

INFORMATION TECHNOLOGY

including Nepal. They can be used for certifying contracts, notarizing docu ments, filing returns or for authentication of individuals or corporations.

Digital Signatures provide a viable solution for creating legally enforceable electronic records, closing the gap in going fully paperless by completely eliminating the need to print documents for signing. Digital signatures enable the replacement of slow and expensive paper-based approval processes with fast, low-cost, and fully digital ones. The purpose of a digital signature is the same as that of a handwritten signature. Instead of using pen and paper, a digital signature uses digital keys (public-key cryptography). Like the pen and paper method, a digital signature attaches the identity of the signer to the document and records a binding commitment to the document. However, unlike a handwritten signature, it is considered impossible to forge a digital signature the way a written signature might be. In addition, the digital signature assures that any changes made to the data that has been signed cannot go undetected. Digital signatures calculate the hash or digest of the complete document and a small change in the document will result in big change in the hash which will make the digital signature verification fail.

After about 9 years of passing the Electronic Transaction Act, 2063, the Digital signature service has been officially launched in Nepal on Mangsir 16, 2072. This has a lots of potential regarding electronic transactions and document exchange in government services and banking services among other sectors.

What is Digital Signature?A digital signature is a mathematical scheme for demonstrating the authenticity of a digital document. A valid digital signature gives the recipient reason to believe that the message was created by a known sender in a way that they cannot deny sending it and that the message was not altered in transit.

A digital signature scheme is typically used by a signer and a set of potential ver ifiers. The signer possesses a pair of keys - public key and private key (or secret key). The private and public keys are mathematically related and it is not possible to compute the private key from public key. The signer then publicizes its public key so that any potential verifier is in possession of (or can obtain) an authentic copy of the public key associated with the signer.1

There is a public directory linking signers to their public keys, and this directory is administered in such a way that it is not possible for someone to reg ister a public key in someone else’s name. There will be many signers, each with their own public key, and so any potential verifier must know not only the set of valid public keys, but also which of these public keys belongs to the signer whose signature he is interested in verifying.

Once a signer has established a public key, digital sig-nature schemes allow the signer to “certify” (or “sign”) a message in such a way that any other party who knows public key can verify that the message originated from the signer and has not been modified in any way.

How Digital Signature Works?Let’s see how this works with an example.

Ram is sending a document to Sita. Sam wants to send the document in such a way that:

• Ram wants Sita to know that the document really came from him

• Ram wants to assure Sita that the document has not been changed in the way

• And if needed, Sita can prove that the sender of the document was Ram and not anyone else

1 Jonathan Katz, Digital Signatures (Advances in Information Security),

The Nepal Chartered Accountant December 201524

INFORMATION TECHNOLOGY

Using digital signature scheme, Ram will send the document to Sita as follows:

• Ram creates the document to be sent in electronic form like word, pdf or excel (also possible with email message)

• He also creates a hash (also called fingerprint or digest)2 of the message using a special software tool

• He then encrypts the hash with his private key• The encrypted hash becomes the digital signature of

the document and the signature is appended to the document using the software tool

• This becomes the signed document which Ram sends to Sita

On Sita’s part, she verifies the message as follows:

• Sita receives the document• To be sure it came from Ram unchanged; first, she

creates a hash of the document she received using some software tool.

• The signing and verifying tools are part of digital signature certificate issuance. The software tool may be in the form of web application or software supplied to the user in USB tokens or some other similar way.

• Then, she decodes the encrypted document hash using Ram’s public key which was attached to the message as well.

• In this process the software tool provided for digital signature checks the validity of the certificate by asking the Certificate Status Provider where all the valid and revoked certificates are listed.

• At this point, Sita compares the two hashes • If they match, the document came from Ram and has

not been tampered with. If they do not match, digital signature verification fails and the document cannot be trusted.

2 Message digest, also known as the hash of a message, is a small piece of data that is generated by applying a mathematical calculation (hashing function) on the message.

Diagrammatic representation of sending and verification process. Image adopted from Wikipedia

The Nepal Chartered Accountant December 2015 25

INFORMATION TECHNOLOGY

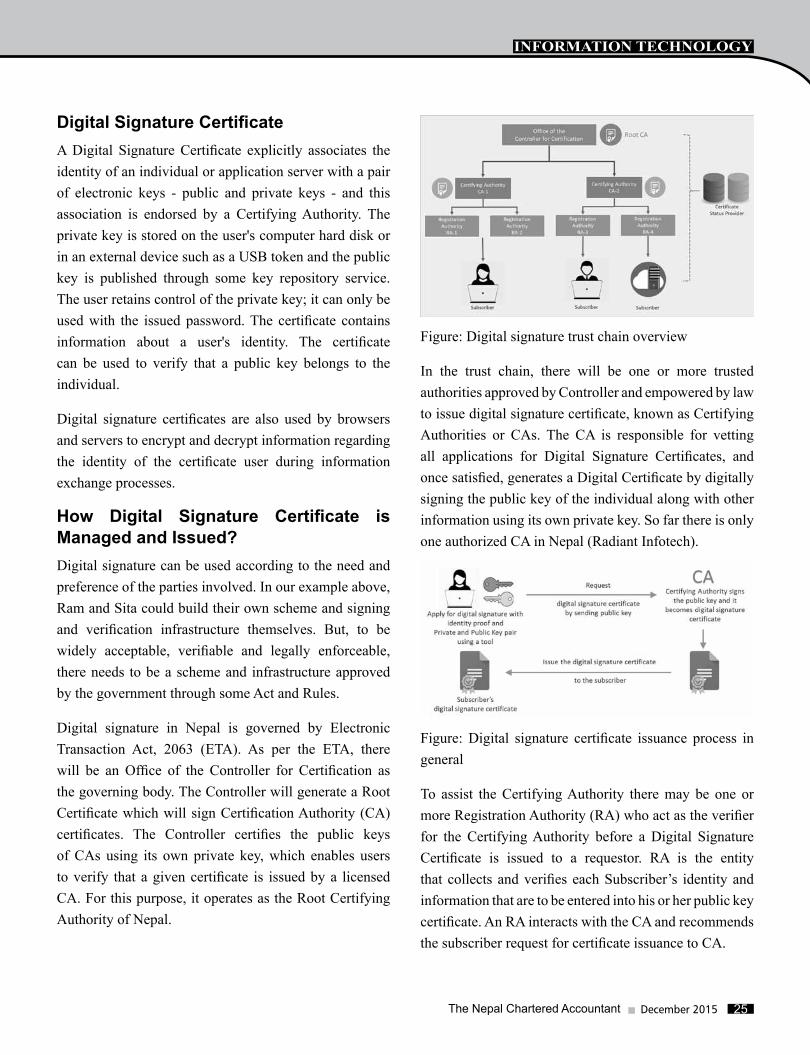

Digital Signature CertificateA Digital Signature Certificate explicitly associates the identity of an individual or application server with a pair of electronic keys - public and private keys - and this association is endorsed by a Certifying Authority. The private key is stored on the user's computer hard disk or in an external device such as a USB token and the public key is published through some key repository service. The user retains control of the private key; it can only be used with the issued password. The certificate contains information about a user's identity. The certificate can be used to verify that a public key belongs to the individual.

Digital signature certificates are also used by browsers and servers to encrypt and decrypt information regarding the identity of the certificate user during information exchange processes.

How Digital Signature Certificate is Managed and Issued?Digital signature can be used according to the need and preference of the parties involved. In our example above, Ram and Sita could build their own scheme and signing and verification infrastructure themselves. But, to be widely acceptable, verifiable and legally enforceable, there needs to be a scheme and infrastructure approved by the government through some Act and Rules.

Digital signature in Nepal is governed by Electronic Transaction Act, 2063 (ETA). As per the ETA, there will be an Office of the Controller for Certification as the governing body. The Controller will generate a Root Certificate which will sign Certification Authority (CA) certificates. The Controller certifies the public keys of CAs using its own private key, which enables users to verify that a given certificate is issued by a licensed CA. For this purpose, it operates as the Root Certifying Authority of Nepal.

Figure: Digital signature trust chain overview

In the trust chain, there will be one or more trusted authorities approved by Controller and empowered by law to issue digital signature certificate, known as Certifying Authorities or CAs. The CA is responsible for vetting all applications for Digital Signature Certificates, and once satisfied, generates a Digital Certificate by digitally signing the public key of the individual along with other information using its own private key. So far there is only one authorized CA in Nepal (Radiant Infotech).

Figure: Digital signature certificate issuance process in general