dec 2012 uncertainties cloud market opportunities derek yung senior managing director...

TRANSCRIPT

Dec 2012

Uncertainties Cloud Market Opportunities

Derek Yung

Senior Managing Director

AllianceBernstein Investment Taiwan Limited

AllianceBernstein Investments Taiwan Limited is the Master Agent of AllianceBernstein fund in Taiwan. AllianceBernstein Investments Taiwan Limited 57F-1, No.7, Sec. 5, Xing Yi Rd., Taipei City 110, Taiwan R.O.C. 02-8758-3888 AllianceBernstein Investments Taiwan Limited is a separate entity and operated business independently.Since investing involves risk to principal, positive results and the achievement of an investor’s goals are not guaranteed. There are no assurances that any investment will be profitable. No information contained in the results should be construed as investment advice. Please consult your Financial Advisor for personalized financial guidance. The information contained herein reflects, as of the date hereof, the views of AllianceBernstein and sources believed by AllianceBernstein to be reliable. No representation or warranty is made concerning the accuracy of any data compiled herein. In addition, there can be no guarantee that any projection, forecast or opinion in this article will be realized. The views expressed herein may change at any time subsequent to the date of issue hereof. This article is provided for informational purposes only and under no circumstances may any information contained herein be construed as investment advice.

©2012AllianceBernstein L.P.

AllianceBernstein.com

Returns in US Dollars

Markets Performed Better than They Felt…

3Q 2012 Returns

Japan Gov’t

Global High Yield

US Gov’t

Euro Gov’t

Emerging Market Debt

Global Corp

Europe

World

Japan

Equities

Credit

Gov’tBonds

Commodities

Alternatives

US

2

Emerging Markets

YTD 2012 Returns

Global Real Estate Investment Trusts

Treasury Inflation Protected Securities

28 Feb 2009 – 30 Sep 2012 Annualized Returns

Past performance does not guarantee future results.As of 30 September 2012Global High Yield, Global Corp, Japan Gov’t and Euro Gov’t in hedged USD terms. All other non-US returns in unhedged USD terms.An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Please see the end of the presentation for index definitions. Source: Barclays Capital, DJ-UBS, FactSet, FTSE, MSCI, Standard & Poor’s and AllianceBernstein

AllianceBernstein.com

…Because of Real Economic and Capital-Market Uncertainties…

3

BofA: ‘Fiscal Cliff’ Becomes Top Investor Concern for September

Italy slashes growth forecast for 2012. Rome expects 2.4% contraction while eurozone PMI falls.

Fearing an Impasse in Congress, Industry Cuts Spending

Asia Trade Data Show Weakening Demand

Spain, Italy 10-Year Bonds Drop; Spanish Yield Rises to

6.46%

Greek Leaders Struggle With Spending Reductions

September 18, 2012

August 28, 2012

September 19, 2012

September 20, 2012

August 5, 2012

September 10, 2012

China, euro-zone PMI data highlight global fears

US inflation fears rise after QE3September 17, 2012

September 20, 2012

BUSINESS

WORLD

AllianceBernstein.com

We Expect Modest Global Growth to Continue

…and highly stimulative fiscal and monetary policies…

Tension between uncertainties’ cumulative effect on global growth…

…should culminate in a slightly better 2013

Global Purchasing Managers’ Index (PMI)

PMI through August 31, 2012; official rates and GDP forecasts as of September 30, 2012Source: JPMorgan Chase, Markit and AllianceBernstein

Official Rates (Percent)

Emerging Markets

Developed Markets

AllianceBernstein Real GDP Growth Forecasts (Percent)

4

AllianceBernstein.com

Attractive Equity Potential Tempered by Volatility

5

Long-TermExpected Return (%)

Near-TermExpected Global

Equity Volatility (%)

Long-Term Average15.5

14.6Normal

Asset Allocation

Our View of Equity Allocation: Long-Term 60/40 Investors

Equ

ity A

lloca

tion

(%)

60

50

40

70

Global S

tock Index

Historical analysis and current forecasts do not guarantee future results.Data do not represent past performance and are not a promise of actual results or range of future results.As of 1 October 2012Global sovereign bonds are represented by global, developed, sovereign, seven-year constant-maturity nominal bonds; global stocks by a universe similar to MSCI World. Both are reported in and hedged into US dollars. *As of 30 September 2012. Equity here refers to 70% US equity (MSCI USA) and 30% international equity (25% MSCI EAFE, 5% MSCI EM). **Represented by the MSCI All Country World Index.An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Please see end of presentation for index definition.Source: MSCI and AllianceBernstein

AllianceBernstein.com

Market Environments Inform Portfolio Strategy

As of 30 September 2012There is no guarantee that the portfolio strategies presented would yield positive results, or that the market environments presented will occur.Source: AllianceBernstein

Financial Crisis/Recession

Risk On/Risk Off Recovery/Normalization

Economic Outlook Negative real growth Fears of deflation

1%–2% global GDP growth Fears shift between inflation

and deflation

3%–5% global GDP growth Healthy reflation

Market Volatility High and sustainedFrequent shifts between high and low volatility

Low and sustained

Market Return Negative Modest High

Investment Focus Preservation Income Appreciation

Bonds Governments Credits High-beta credit

Real Assets TIPS Real estate Commodities

Equities Defensives US

Stability Global

Cyclical Non-US EM

Currencies Hedged Partial hedge Unhedged/carry exposure

Potential Market Environments and Portfolio Strategies

6

AllianceBernstein.com

Maintaining Our Corporate Exposure

Issuance and leverage as of June 30, 2012; spreads through September 30, 2012*US-dollar investment-grade, high-yield and emerging-market corporates, mortgage-backed securities, commercial mortgage-backed securities, asset-backed securities (including card, student loan and manufactured home) and collateralized loan obligations**Gross Leverage = Total Debt/EBITDA; Net Leverage = (Total Debt – (Cash + Cash Equivalents))/EBITDA; both metrics are for the Barclays Capital US Investment-Grade Corporate IndexSource: Barclays Capital and JPMorgan Chase

Nongovernment Debt:* Net Issuance

Lack of supply is generally supportive of nongovernment debt, including corporates

Valuations are fair

Corporate Spreads to Governments

Christopher ChuBarcap

UPDATED

Fundamentals suggest we are in the middle to late stages of the credit cycle

Leverage:** US

Gross

Net

Euro Area

US

7

AllianceBernstein.com

Corporate Spreads Remain Wider than Average

Through 30 September 2012Averages are for the periods shown; emerging-market debt is US-dollar denominated only. Source: Barclays Capital and AllianceBernstein

Spreads to Governments

Global Investment-Grade Corporates

Global High-Yield Bonds

Average

US CMBSs US AAA ABSs

Emerging-Market Debt US Mortgages

11

AllianceBernstein.com

Corporate Fundamentals Remain Relatively Strong…

9

…and cash positions, while below recent peaks, continue to be strong

Revenue and Operating EPS Trends: S&P 500

Growth is still positive, although trend is declining

Margins remain high in both investment-grade and high-yield industrial companies…

EBITDA Margin Trends: US Credit

Cash/Debt Ratios: US Investment Grade Corporates

Investment-Grade

High-Yield

Top chart and bottom as of end June 2012; Middle chart as of May 2012.Source: Bank of America Merrill Lynch, J.P. Morgan, Morgan Stanley

AllianceBernstein.com

…but Signs of Mid-Cycle Behavior Are Appearing

10

Earnings-per-share estimates are higher than during the financial crisis, but falling

Stock Repurchase Announcements: S&P 500

The number of share buybacks is increasing

EPS revisions as of September 21, 2012*Trailing three-month rateSource: Bank of America Merrill Lynch, Capital IQ, Morgan Stanley

Fewer ratings upgrades are causing the upgrades/downgrades ratio to decline

US Credit Ratings: Ratio of Upgrades to Downgrades

Weekly S&P 500 EPS Forward Estimates

Investment-Grade

High Yield*

Value of Announcements (Right) No. of Announcements (Left)

Initial Estimates Revised Estimates Final Outcome/Latest Estimates

20042005

20062007

2008

2009

2010

2011

20122013

AllianceBernstein.com

Opportunities in US High-Yield and Emerging-Market Corporates

11

We believe high-yield default rates should remain low

Forthcoming maturities in high-yield bonds are relatively low, suggesting modest refinancing risk

We see select opportunities in emerging-market corporates, which have strong fundamentals

Maturities Pipeline: High Yield Bonds vs. Leveraged Loans

Net Leverage: Emerging-Market vs. US Corporates**

**Net leverage less cash refers to the last 12 months ratio of debt capital (bank loans, bonds, etc.) to EBITDA (earnings before interest, tax depreciation and amortization)‡Data from J.P. Morgan; reflects par-weighted default rates. Recession scenario assumes that every bond trading below 70 cents on the dollar defaults. As of 4 September 2012. . Source: Moody’s Investors Service, JPMorgan Chase and AllianceBernstein

High-Yield Default Rate‡

BaseCase

Recession

High-Yield Defaults Remain Low (Percent)

AllianceBernstein.com

Australia8.9

Canada8.3

UK16.1

Japan2.6

US9.8

Globalizing Portfolios Has Diversified Interest-Rate Risk

Euro Area1.0

US5.9

Japan2.9

UK7.2

Australia0.3

Canada5.6

Japan1.4

UK-1.6

US-3.6

Euro Area4.1

Australia–5.9

Canada-1.9

20092008

UK10.4

Euro Area8.4

Australia15.1

US13.8

Japan6.7

Canada11.7

Euro Area2.6

2011

6.28.4 10.0 6.9

Country Returns Vary Across Cycles*

Global Bond Returns (Hedged to USD): Percent**

2010

13.5

BestPerformer

Worst Performer

Gap between

bestand worst

12

Past performance does not guarantee future results. These returns are for illustrative purposes only and do not reflect the performance of any fund.*Left graph as of 20 September 2012; right graph as of 30 September 2012**Returns represented by respective Barclays Capital government bond indices within each country. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. †EM currency represented by WisdomTree Dreyfus Emerging Currency Fund (CEW); global treasury hedged and unhedged represented by Barclays Capital Global Treasury Index; developed currency represented by PowerShares DB US Dollar Index Bullish Fund (UUP).Source: Barclays Capital, Bloomberg, Haver Analytics, J.P. Morgan, MSCI, National Accounts, S&P/Dow Jones, US Department of the Treasury and AllianceBernstein

12

YTD*

Euro Area7.9

Japan2.2

Canada1.7

US2.1

UK2.9

Australia2.8

1.0

-0.5

0.2

0.8 0.7

S&P 500 BarclaysCapital Global

TreasuryIndex

Hedged

BarclaysCapital Global

TreasuryIndex

Unhedged

Emerging-Market Currency

DevelopedCurrency

15.4 16.9

2.76.5

10.5 9.8

S&P 500 MSCI World BarclaysCapitalGlobal

TreasuryIndex Hedged

BarclaysCapital Global

TreasuryIndex

Unhedged

Emerging-Market

Currency

DevelopedCurrency

Three-Year Correlation to Equity†

Three-Year Volatility†

EM Currency Has Not Provided Diversification

AllianceBernstein.com 13

Diversification of Risks In an Uncertain Environment Is Highly Important

Annual Returns in USD (Percent)

Past performance does not guarantee future results. These returns are for illustrative purposes only and do not reflect the performance of any fund. Diversification does not eliminate the risk of loss. High yield is represented by the Barclays Capital US Corporate High Yield Index; EMD (Emerging Markets debt) USD are represented by the JPM EMBI-Global; EMD Local is represented by the JPM GBI-EM Index unhedged. Corporates (investment grade) are represented by Barclays Capital US Corporate Investment Grade. US Treasuries are represented by the Barclays Capital US Treasury Index. US MBSs are represented by Barclays Capital US MBS Index. Global Gov’t. (H) is represented by the Barclays Capital Global Aggregate Treasury Bond Index. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Please see the end of the presentation for index definitions.*Through 30 June 2012Source: Barclays Capital, JPMorgan Chase and AllianceBernstein

20092002 2003 2004 2005 2006 2007

Best

Worst

2008

Gap betweenBest and

worst

EMD USD 13.1

EMD USD 25.7

EMD USD 11.7

EMD USD 10.7

EMD USD 9.9

EMD Local29.1

EMD Local17.8

EMD Local23.1

EMD Local2.9

EMD Local12.0

EMD Local16.3

High Yield29.0

High Yield11.1

High Yield11.9

Inv.-Grade Corporate

4.3

Inv.-Grade Corporate

5.4

Inv.-Grade Corporate

8.2

US MBSs3.1

US MBSs4.7

High Yield2.7

Inv. Grade Corporate

1.7

US MBSs2.6

US MBS5.2

High Yield–1.4

Inv.-Grade Corporate

10.1

US MBSs8.8

Global Gov’t (H)

8.0

Global Gov’t (H)

4.8

Global Gov’t (H)

5.0

Global Gov’t (H)

3.3

EMD USD 6.3

High Yield1.9

Inv. Grade Corporate

4.6

US MBSs6.9

Global Gov’t (H)

5.6

Inv.-Grade Corporate

–4.9

EMD USD –10.9

EMD Local–6.9

High Yield–26.2

US MBSs8.3

Global Gov’t (H)

9.1

2011

EMD Local 13.1

EMD USD12.0

High Yield15.1

Inv.-Grade Corporate

9.0

US MBSs5.4

Global Gov’t (H)

3.6

US Treasuries

5.9

US Treasuries

11.8

US Treasuries

2.2

Global Gov’t (H)

2.0

US Treasuries

3.5

US Treasuries

2.8

US Treasuries

3.1

US Treasuries

9.0

US Treasuries

13.8

30.5 16.227.0 19.6 9.0 8.9 14.4 61.840.0

2010

Inv.-Grade Corporate

18.7

EMD USD 28.2

EMD Local16.6

High Yield58.2

US MBSs5.9

Global Gov’t (H)

1.0

US Treasuries

–3.6

11.5

USTreasuries

9.8

High Yield5.0

GlobalGov’t (H)

5.5

US MBSs6.2

EMD USD8.5

Inv.-GradeCorporate

8.2

EMD Local–6.4

YTD*

High Yield12.1

EMD USD14.7

Inv.-GradeCorporate

8.7

US MBSs2.8

GlobalGov’t (H)

3.7

USTreasuries

2.1

13.5

EMD Local 15.6

AllianceBernstein.com

Lower Volatility Opportunities in Relative Value Strategies

Differentiated Stock Returns May Favor Relative Value Strategies*

Past performance and historical analysis do not guarantee future results.Left graph as of 31 December 2011; top right graph as of 31 March 2012; bottom right graph as of 30 June 2012An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. Please see end of presentation for index definition.*Market-neutral is represented by HFRI EH: Equity Market Neutral Index, Left graph: equities by S&P 500 Index and bonds by Barclays Capital US Aggregate Bond Index.**Correlation using rolling daily returns over six months. Correlation is a statistical measure of how two values move in relation to each other. Source: Bank of America Merrill Lynch, Barclays Capital, Bloomberg, FactSet, Hedge Fund Research, MSCI, S&P/Dow Jones, US Federal Reserve and AllianceBernstein

14

Market-Neutral Is Usually Detached from Market Fluctuations*

Intra-Market Correlations Fall**

MSCI World

S&P 500

Rat

io (

×)

Excess Return in Different Dispersion EnvironmentsRolling Three-Year Correlation of Market-Neutral Index

Correlations with Equities

Correlations with Bonds

Stability Traditional

Long/Short Concentrated

AllianceBernstein.com

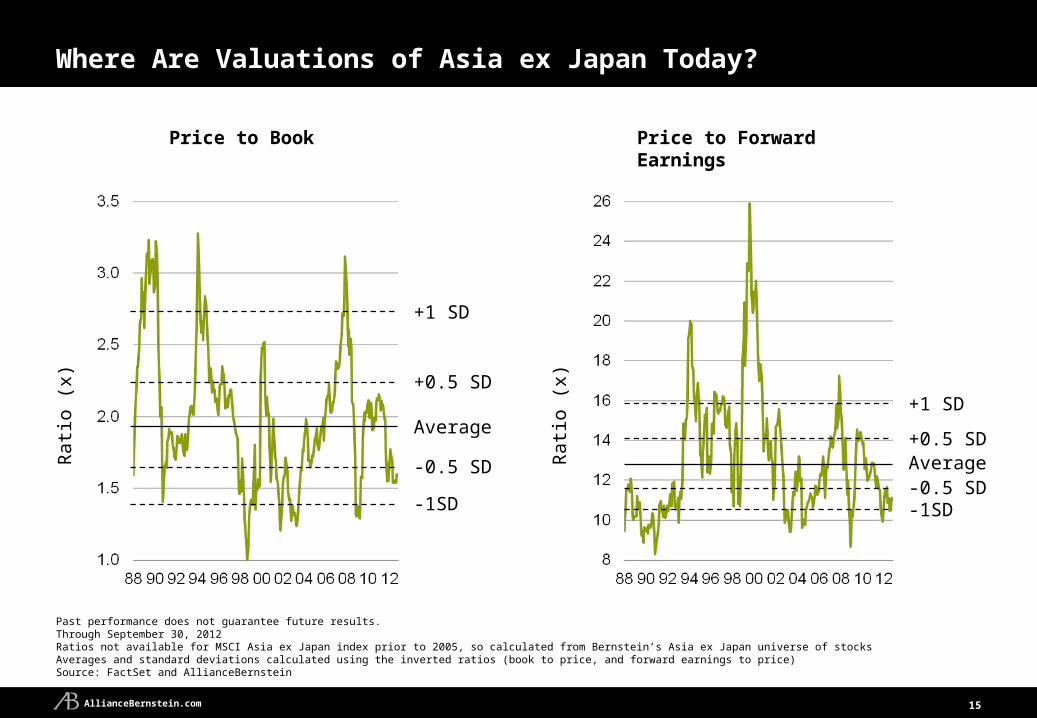

Where Are Valuations of Asia ex Japan Today?

15

Past performance does not guarantee future results.Through September 30, 2012Ratios not available for MSCI Asia ex Japan index prior to 2005, so calculated from Bernstein’s Asia ex Japan universe of stocksAverages and standard deviations calculated using the inverted ratios (book to price, and forward earnings to price)Source: FactSet and AllianceBernstein

Rat

io (

x)

Average

+0.5 SD

+1 SD

-1SD

-0.5 SD

Price to Book

Rat

io (

x)

Average+0.5 SD

+1 SD

-1SD-0.5 SD

Price to Forward Earnings

AllianceBernstein.com

Conclusion

16

Core bonds should be diversified, global and currency hedged to offset riskier assets

High-yield bonds appear attractive. Bear in mind that they are still subject to the fluctuating nature of investments

Stocks still seem attractive based on long-term valuations, but higher volatility and uncertainty warrant a modest underweight

Equity allocations should diversify across strategies with diverse benchmark sensitivity and risk levels

Investment portfolios should be informed by the market environment and actively managed to capitalize on evolving opportunities

AllianceBernstein.com

Appendix

17

AllianceBernstein.com 18

AllianceBernstein.com 19

AllianceBernstein.com

A Word About Risk

The information contained herein reflects, as of the date hereof, the views of AllianceBernstein and sources believed by AllianceBernstein to be reliable. No representation or warranty is made concerning the accuracy of any data compiled herein. In addition, there can be no guarantee that any projection, forecast or opinion in this article will be realized. The views expressed herein may change at any time subsequent to the date of issue hereof. This article is provided for informational purposes only and under no circumstances may any information contained herein be construed as investment advice.

Fixed-Income Securities Risk. Investment in the fixed-income portfolios entails certain risks. Past performance is not a guide to future performance. Investment returns and principal value of these funds will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The value of underlying fixed-income investments of a portfolio can vary dramatically, in response to the activities and results of individual companies or because of general market and economic conditions and changes in currency exchange rates. The value of a portfolio’s investments may decline over short- or long-term periods. Specific fixed-income risks include interest rate risk, lower-rated and unrated investments risk, prepayment risk, sovereign debt obligations risk, corporate debt risk. These and other risks are described in a fund’s prospectus. Prospective investors should read the prospectus carefully and discuss risk and the portfolio’s fees and charges with their financial adviser to determine if the investment is appropriate for them.

This document is provided for informational purposes only and is not intended to be an offer or solicitation, or the basis for any contract to purchase or sell any security or other instrument, or for AllianceBernstein to enter into or arrange any type of transaction as a consequence of any information contained herein. Under no circumstances may any information contained herein be construed as investment advice.

Past performance is no guarantee of future results. There is no guarantee that any forecasts or opinions in these materials will be realized. The information herein reflects prevailing market conditions and our judgments as of the date of the presentation, which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. No representation or warranty is made concerning the accuracy of cited data. Opinions and estimates may be changed without notice and involve a number of assumptions which may not prove valid. In addition, there can be no guarantee that any projection, forecast or opinion in these materials will be realised. Neither this presentation nor any of its contents may be used for any purpose without the consent of AllianceBernstein.

20

AllianceBernstein.com

A Word About Risk

21

聯博基金﹙ AllianceBernstein﹚在台灣之總代理為聯博證券投資信託股份有限公司。聯博證券投資信託股份有限公司台北市 110信義路五段 7 號 57樓之 1 02-8758-3888聯博投信獨立經營管理

投資人投資以高收益債券為訴求之基金不宜占其投資組合過高之比重。基金高收益債券之投資占顯著比重者,適合『能承受較高風險之非保守型』之投資人。所列之境外基金經金管會核准或同意生效,惟不表示絕無風險。由於高收益債券之信用評等未達投資等級或未經信用評等,且對利率變動的敏感度甚高,故本基金可能會因利率上升、市場流動性下降、或債券發行機構違約不支付本金、利息或破產而蒙受虧損。本基金不適合無法承擔相關風險之投資人。

基金經理公司以往之經理績效不保證基金之最低投資收益;基金經理公司除盡善良管理人之注意義務外,不負責本基金之盈虧,亦不保證最低之收益,投資人申購前應詳閱基金公開說明書。

有關基金應負擔之費用〈含分銷費用〉及投資風險等已揭露於基金公開說明書中譯文及投資人須知,投資人可至境外基金資訊觀測站www.fundclear.com.tw或聯博網站 www.alliancebernstein.com.tw查詢,或請聯絡您的理財專員,亦可洽聯博投信索取。

投資於新興市場國家之風險一般較成熟市場高,也可能因匯率變動、流動性或政治經濟等不確定因素,而導致投資組合淨值波動加劇。本基金投資於以外幣計價之有價證券,匯率變動可能影響其淨值。

本文提及之經濟走勢預測不必然代表本基金之績效,本基金投資風險請詳閱基金公開說明書。

投資具有本金虧損風險,不保證必然有正報酬或達成投資人之目標。投資不必然獲利。本文件內容不得視為投資建議。請向財務顧問洽詢個人理財建議。

本文反映文件編製日觀點,僅供說明參考之用,資料來自聯博認為可靠之來源。聯博對資料之正確性不為任何陳述或保證,投資人不應僅以本文作為投資決策依據或投資建議。