death of a partner 17-2 - mntaxclass.commntaxclass.com/files/ch_17_death_of_ptr.pdf · death of a...

TRANSCRIPT

• Tax year closes with respect to deceased partner (not Php).

• Passive losses may be deducted on final return (reduced by basis step-up).

• Decedent’s IRC sec. 743(b) adjustment disappears at death but beneficiary is entitled to a 743(b) adjustment.

Death of a Partner 17-2

• Successor’s outside basis:FMV of Php. Interest

+ Debt Share- IRD

• No deemed termination (IRC sec. 708(b)(1)(B)) on death of a partner because not a sale or exchange.

Death of a Partner 17-3

• IRC sec. 754 election. Inside basis steps up or down.

• Mandatory downward IRC sec. 743 adjustment if:

Php. asset I.B. > Php asset FMV by > $250,000

• No IRC sec. 743 Adj. for IRD

17-2Example 17-1

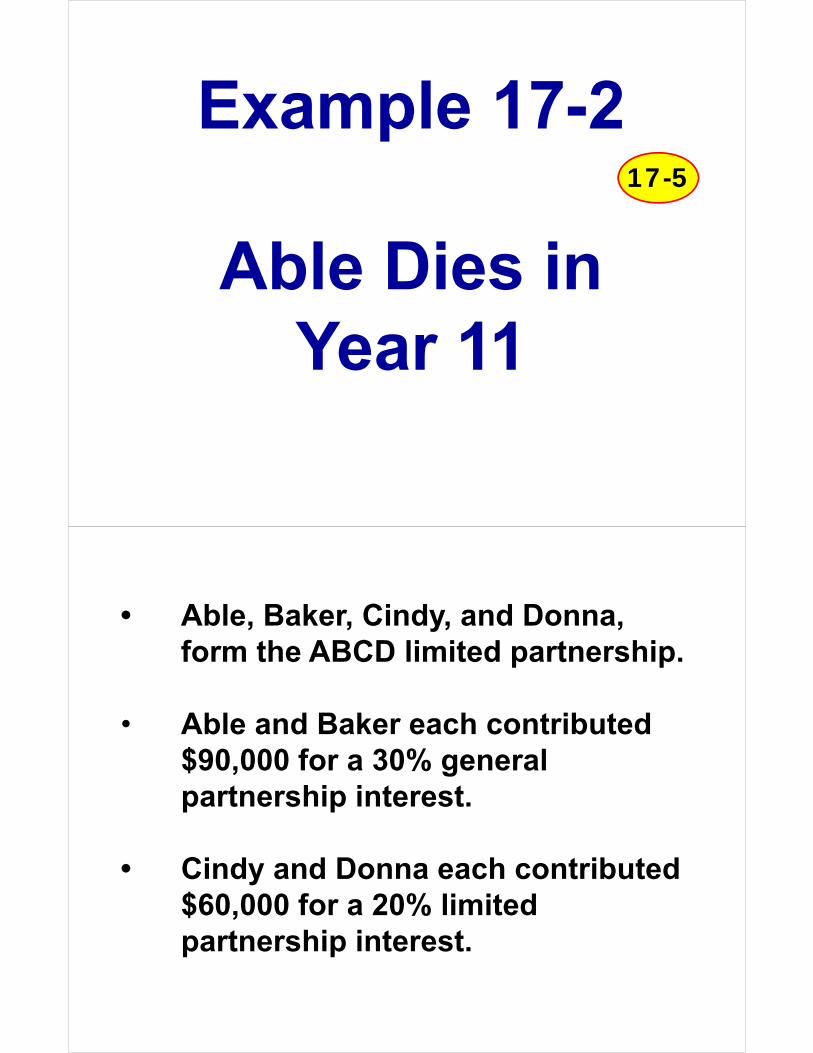

Example 17-2

Able Dies in Year 11

17-5

• Able, Baker, Cindy, and Donna, form the ABCD limited partnership.

• Able and Baker each contributed $90,000 for a 30% general partnership interest.

• Cindy and Donna each contributed $60,000 for a 20% limited partnership interest.

• The agreement contains a gain chargeback provision that allocates gain on the sale of depreciable property to the partners to the extent of the prior allocations of cost recovery deductions.

• Otherwise, profits and losses are allocated 30%, 30%, 20%, 20% to Able, Baker, Cindy, and Donna respectively.

•

• Immediately after formation, the partnership borrowed $600,000, recourse debt, and used the entire $600,000 to purchase a building (on leased land).

• For simplicity, the building is depreciated over 10 years at $60,000 per year.

• The recourse debt was allocated $300,000 to Able and $300,000 to Baker (the general partners).

• None of the debt principal is due until Year 12.

• The partnership does not make an IRC sec. 754 election.

• Each year for the first ten years, other than depreciation, the income and expenses were equal; therefore, the partnership lost <$60,000> each year.

• By the end of year ten, the <$600,000> total losses (all attributed to depreciation) allocated to each partner over the ten year period is:

<$240,000> Able (GP)<$240,000> Baker (GP)<$60,000> Cindy (LP)<$60,000> Donna (LP)

Note: The LPs capital accounts cannot go negative so Cindy and Donna’s losses could not exceed $60,000 each.

ABCD Partnership O.B.

Tax Basis FMVCash $300,000 $300,000Building Cost $600,000Accum. Depr -$600,000= Building Adj. Basis $0 $600,000Total Assets $300,000 $900,000

Recourse Debt $600,000 $600,000Able (30% GP) <$150,000> $90,000 $150,000

(all debt)Baker (30% GP) <$150,000> $90,000 $150,000

(all debt)Cindy (20% LP) $0 $60,000 $0Donna (20% LP) $0 $60,000 $0

Total Debt + Capital $300,000 $900,000

17-6End of Year 10:

Year 11, Able Dies

Estate’s $390,000 Outside Basis:

$90,000 FMV of 30% GP Interest.+ $300,000 Debt Share- $0 IRD

$390,000 Outside Basis

No IRC sec. 754 Election:

No IRC sec. 743(b) Adjustment

With an IRC sec. 754 Election:

With IRC sec. 754 Election, $240,000 IRC sec. 743(b) Adjustment:

$390,000 Estate’s O.B.- $150,000 Estate’s I.B.*

$240,000 Upward Adj.

*<150,000> PTC + $300,000 (Debt Share)

Estate/beneficiary will be allocated MACRS depreciation on the $240,000 as if newly placed in service

Estate/beneficiary should note the $240,000 adjustment for future years to calculate O.B. using alternate rule.

If the Estate/beneficiary is liquidated with a cash distribution of $90,000, any gain?

No gain or loss. The estate’s amount realized of $390,000 equals the estates outside basis.

The Estate’s unused $240,000 IRC sec. 743(b) adjustment

shifts to the common balance

sheet for the continuing partners!

With 50% Estate Tax

Discount in FMV of Partnership

Interest 17-7

Year 11, Able Dies

Estate’s $345,000 Outside Basis:

$45,000 $90,000 x 50% (discount)+ $300,000 Debt Share- $0 IRD

$345,000 Outside Basis

With IRC sec. 754 Election, $195,000 IRC sec. 743(b) Adjustment:

$345,000 Estate’s O.B.- $150,000 Estate’s I.B.*

$195,000 Upward Adj.

*<150,000> PTC + $300,000 (Debt Share)

Estate/beneficiary will be allocated MACRS depreciation on the $195,000 as if newly placed in service

Sale (cap gain except 751(a))

v.Liquidation

of Decedent’s Successor

(invokes IRC sec. 736)

17-7

Sale Per Buy-SellAgreement

17-7

Example 17-3

Partnership liquidates successorfor $90,000

17-8

ABCD Partnership O.B.

Tax Basis FMVCash $300,000 $300,000Building Cost $600,000Accum. Depr -$600,000= Building Adj. Basis $0 $600,000Total Assets $300,000 $900,000

Recourse Debt $600,000 $600,000Estate (30% GP) <$150,000> $90,000 $390,000Baker (30% GP) <$150,000> $90,000 $150,000

(all debt)Cindy (20% LP) $0 $60,000 $0Donna (20% LP) $0 $60,000 $0

Total Debt + Capital $300,000 $900,000

After Able’s Death (pre-liquidation)

Impact of Liquidation on Estate:

$90,000 Cash+ $300,000 Deemed Cash- $390,000 Pre-distribution O.B.

$ 0 Gain or Loss (IRC sec. 731)

ABCD Partnership Tax Basis Sch. LTax Basis FMV

Cash $210,000 $210,000Building Cost $600,000Accum. Depr -$600,000= Building Adj. Basis $240,000 $600,000

Total Assets $450,000 $810,000

After Liquidation of Able’s EstateWith IRC sec. 754 Election

Estate’s 743(b) adjustment shifts to the common balance sheet

ABCD Partnership Tax Basis Sch. LTax Basis FMV

Cash $210,000 $210,000Building Cost $600,000Accum. Depr -$600,000= Building Adj. Basis $0 $600,000Total Assets $210,000 $810,000

After Liquidation of Able’s EstateWithout IRC sec. 754 Election

• Compare if the building instead were depreciable personal property and all gain is IRC sec. 1245 recapture.

• Without IRC sec. 754 election, ordinary income to estate of $240,000 (and capital loss <$240,000>) per IRC sec. 751(b).

• But don’t miss the IRC sec. 732(d) election which eliminates the IRC sec. 751 exchange. 32

Example 17-4

Other Partner (Baker) buys out successor

for $90,000

17-9

Estate’s Sale to BakerAmount Realized:Cash $90,000Debt Relief $300,000

Total Amt. Realized $390,000

Outside Basis:Equity $90,000Debt $300,000Total Outside Basis -$390,000

Pre-look-through Gain $0

Estate’s capital gain or loss:

= Pre-look-through capital gain $0

- Estate’s share of “section 1250 capital gain”

-$ 240,000 $240,000

= Estate’s Residual Long-term capital gain of <loss>

<$240,000>

Without IRC sec. 754 Election:

With IRC sec. 754 Election no “Sec. 1250 capital gain”

Without IRC sec. 754 Election: Compare if IRC sec. 1245 Prop.

B’s IRC Sec. 751 Ordinary Income:B’s share of Unrealized Rec. $240,000

Without IRC sec. 754 Election: Compare if IRC sec. 1245 Prop.

B’s IRC Sec. 751 Ord. Income:B’s share of Unrealized Rec. $240,000

B’s capital gain or loss:Gain realized w/o IRC sec. 751 $0- IRC sec. 751 Ordinary Inc. - $240,000Capital gain or <loss> <$240,000>

Need a 754 Election; No IRC sec. 732(d) relief is available. Discourage sale.

Unique Impactof IRC sec. 754

Election on Successor of

Deceased Partner

• Tax Year of successor closes on liquidation.

• Successor remains a partner until fully liquidated.

• IRC sec. 754 election can eliminate unstated goodwill due to IRC sec. 743(b) inside basis increase.

Issue:

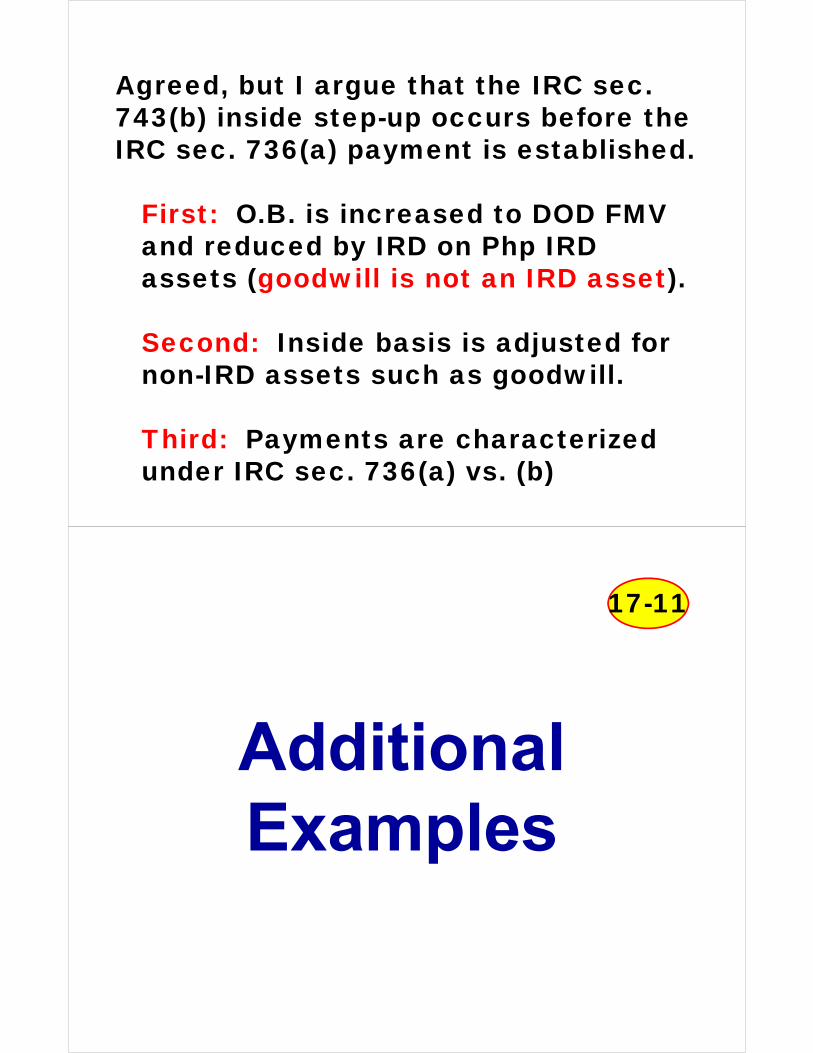

IRC sec. 753 declares that IRC sec. 736(a) payments are IRD (and 1014 denies a basis step up for IRD).

If payments for unstated goodwill fall within 736(a), then they are IRD, and clearly no basis step-up for those payments.

Agreed, but I argue that the IRC sec. 743(b) inside step-up occurs before the IRC sec. 736(a) payment is established.

First: O.B. is increased to DOD FMV and reduced by IRD on Php IRD assets (goodwill is not an IRD asset).

Second: Inside basis is adjusted for non-IRD assets such as goodwill.

Third: Payments are characterized under IRC sec. 736(a) vs. (b)

AdditionalExamples

17-11

17-11

43

Example 17-5Stated Goodwill Without

IRC sec. 754 Election

A personal service partnership

Decedent Alice’s interest is liquidated for $500,000 per buy out agreement

Step One – Estate O.B.The Estate’s outside basis is $475,000:

$500,000 (DOD FMV) minus $25,000 (estate’s share of IRD).

45

In my opinion, the estate’s outside basis would be the same even if the liquidating payments were for unstated goodwill (not an IRD Pshp. asset).

Step Two – Sec. 736(a)The $25,000 payment for the unrealized receivables (zero basis trade receivables) for services is a Sec. 736(a) guaranteed payment to the Estate:

$25,000 ordinary income to Estate

$25,000 deduction to partnership46

Step Three – Sec. 751 Exchange$500,000 (total payment)

- $ 25,000 Sec. 736(a) payment= $ 475,000 Sec. 736(b) payment

$30,000 is disproportionately too much non-751 assets; therefore, the Estate’s share of Sec 1245 recapture, $30,000, is deemed sold to the partnership for the $30,000 cash.

47

A Sec. 732(d) election is made; therefore, the Estate has a $30,000 inside basis in the Sec 1245 recapture: no gain!48

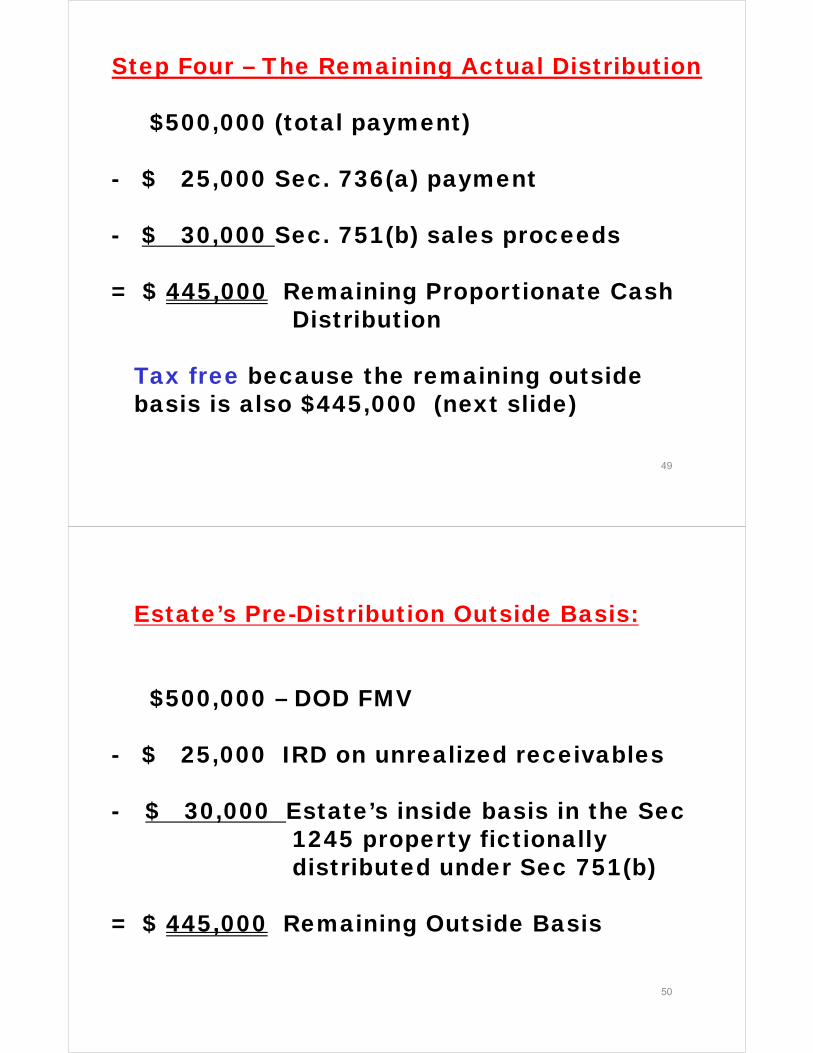

Step Four – The Remaining Actual Distribution

$500,000 (total payment)

- $ 25,000 Sec. 736(a) payment

- $ 30,000 Sec. 751(b) sales proceeds

= $ 445,000 Remaining Proportionate Cash Distribution

Tax free because the remaining outside basis is also $445,000 (next slide)

49

Estate’s Pre-Distribution Outside Basis:

$500,000 – DOD FMV

- $ 25,000 IRD on unrealized receivables

- $ 30,000 Estate’s inside basis in the Sec 1245 property fictionally distributed under Sec 751(b)

= $ 445,000 Remaining Outside Basis

50

17-17

51

Example 17-6Same as Ex. 17-5 With

Sec. 754 Election

Step One – Estate O.B. and Inside Basis

The Estate’s outside basis is $475,000:

$ 500,000 DOD FMV- $ 25,000 estate’s share of IRD=$ 475,000 Outside basis

The Estate’s share of inside basis is $170,000.

Sec. 743(b) adjustment = 305,000 ($475,000 – 170,000).

53

Step One – Sec. 755 Allocation of $305,000 Sec 743(b)

Adjustment

$275,000--goodwill

$30,000--Sec. 1245 recapture

54

Step Two – Sec. 736(a)The $25,000 payment for the unrealized receivables for services is a Sec. 736(a) guaranteed payment to the Estate:

$25,000 ordinary income to Estate

$25,000 deduction to partnership55

Step Three – Sec. 751 Exchange$500,000 (total payment)

- $ 25,000 Sec. 736(a) payment= $ 475,000 Sec. 736(b) payment

$30,000 is disproportionately too much non-751 assets; therefore, the Estate’s share of Sec 1245 recapture, $30,000, is deemed sold to the partnership for the $30,000 cash.

56

Due to the Sec. 754 election, the Estate has a $30,000 inside basis in the Sec 1245 recapture: no gain!

57

Step Four – The Remaining Actual Distribution

$500,000 (total payment)

- $ 25,000 Sec. 736(a) payment

- $ 30,000 Sec. 751(b) sales proceeds

= $ 445,000 Remaining Proportionate Cash Distribution

Tax free because the remaining outside basis is also $445,000

58

Partnership Common Adjustment:

Because the estate cannot use the $275,000 Sec 743(b) adjustment for the goodwill (it remains inside the partnership), Reg. 1.734-2(b) allows the partnership to make an adjustment to the common inside basis in the goodwill—up $275,000 (and amortizable over 15 years).

The continuing partners benefit from the Sec. 754 election.

59

17-17

60

Example 17-7Liquidation where only

non-cash asset is IRD

Decedent Alice’s interest is liquidated for $1,000,000 per buy out agreement with IRC sec. 754 election

Step One – Estate O.B. and Inside Basis

The Estate’s outside basis is $250,000:

$ 1,000,000 DOD FMV- $ 750,000 estate’s share of IRD=$ 250,000 Outside basis

The Sec. 754 election is irrelevant to the Estate because the only asset is IRD—no inside basis adjustment.

62

Step Two – Sec. 736(a)

None

63

Step Three – Sec. 751 Exchange

None

Step Four – The Remaining Actual Distribution

$ 1,000,000 (total payment)

- $ 250,000 (pre-distribution outside basis)

= $ 750,000 Sec. 731(a)(1) capital gain

The Sec. 754 election allows the continuing partners to make an upward adjustment to the basis in “capital gain property” by $750,000.

The Sec. 754 election benefits the continuing partners. 64

17-18

65

Example 17-8 Impact of Real Estate Bubble on

Liquidation Without IRC Sec. 754 Election

Before Bill’s Death

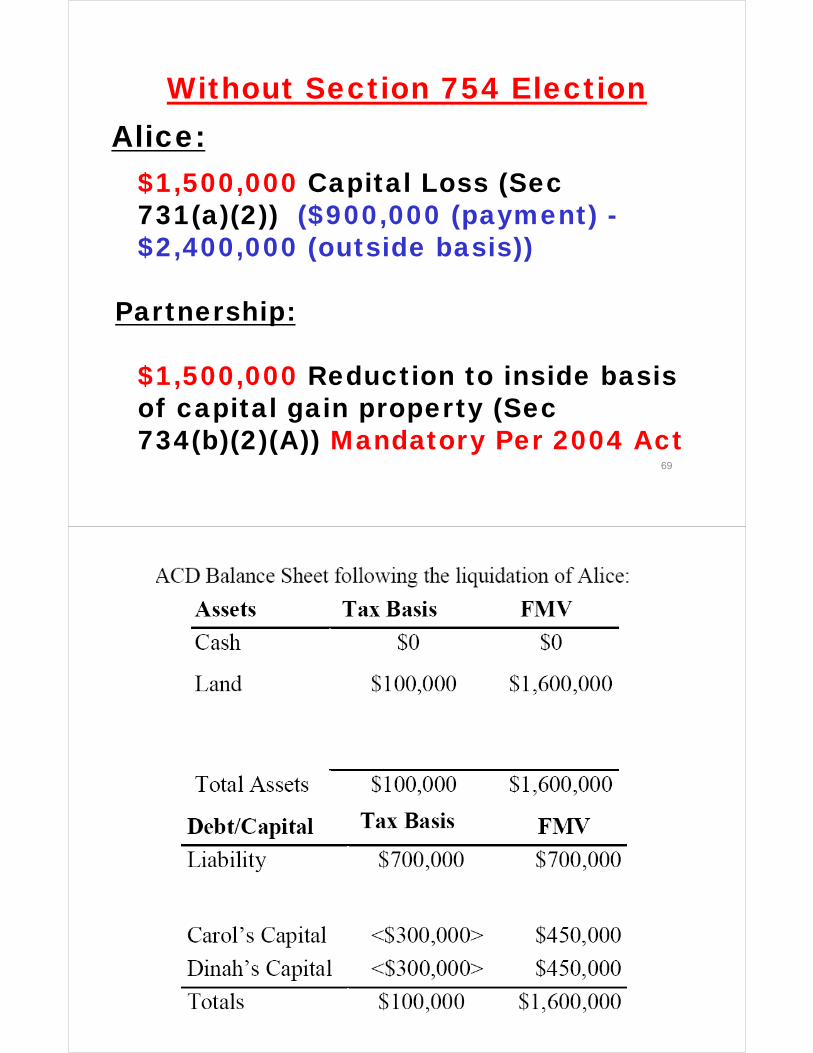

Without Section 754 ElectionAlice:

$1,500,000 Capital Loss (Sec 731(a)(2)) ($900,000 (payment) -$2,400,000 (outside basis))

Partnership:

$1,500,000 Reduction to inside basis of capital gain property (Sec 734(b)(2)(A)) Mandatory Per 2004 Act

69

Subsequent Sale of Land for $1,600,000 (basis $100,000):

Gain of $1,500,000 ($750,000 per partner).

71

17-21

73

Example 17-9 Purchase Compared to Liquidation

Still no Sec. 754 election.

Balance Sheet on Date of Sale: Alice’s outside basis is $2,400,000:

Impact of Sale:Alice:

$1,500,000 Capital Loss (Sec 741) ($900,000 (sales price) - $2,400,000 (outside basis))

Carol and Dinah

Each partner’s outside basis increases by the purchase price ($450,000 each).

75

Example 17-10 Sec. 754 election on Bill’s

death rescues the continuing partners

following Alice’s death (and the liquidation of

Alice’s estate).17-21

76

Before Bill’s Death

With Section 754 ElectionAlice:

$1,500,000 Capital Loss (Sec 731(a)(2)) ($900,000 - $2,400,000)

Partnership:$1,500,000 Reduction to inside basis of capital gain property (Sec 734(b)(2)(A))

$1,500,000 increase in inside basis of capital assets for Alice’s unused Sec 743(b) adjustment in the land.

78