dear colleague - aasa · dear colleague: the american ... which includes materials from the...

TRANSCRIPT

Dear Colleague:

The American Association of School Administrators, through the AASA Center for System Leadership™,

is pleased to provide to every superintendent in America this highly anticipated Blueprints: A Guide to Public

School Plans 403(b) and 457(b) toolkit. The toolkit, which includes materials from the Internal Revenue Service,

is designed as an information “blueprint” for constructing a compliant 403(b) plan in accordance with new

IRS requirements.

The opportunity to provide this toolkit to all superintendents is made possible only through hours of advice

and support from key IRS officials and 403(b) experts, plus the generosity of four leading companies in financial

services. In particular, I am pleased to thank AIG Retirement, AXA Equitable, Horace Mann and ING for their

outstanding support and commitment to public education.

AASA cannot give tax advice. Although the toolkit may not answer all of your questions, it is an objective

approach to helping you feel confident about your school’s new responsibilities beginning Jan.1, 2009.

Because the plan you create for your school system will reflect the needs of your district, we recommend that

you use this toolkit in addition to seeking the advice of a tax attorney. The goal of Blueprints is to provide public

information in a way that supports your discussion among the school system, its employees and the plan’s

product providers.

I personally believe the Blueprints toolkit represents a significant resource for your efforts to become compliant

with the new requirements. The AASA Center for System Leadership placed an evaluation card in the right pocket

of the toolkit. We would appreciate your thoughts about the value of the Blueprints toolkit.

If you are a member of AASA, you will recognize this toolkit as another leading-edge member benefit. Other

benefits include The School Administrator magazine, electronic publications, unique professional development

opportunities, member discounts, advocacy, and member access to current, compelling information on the

AASA website.

If you are not a member of AASA, I invite you to join AASA for everyday access to our many professional

resources and to help make AASA a stronger voice in Washington. More information about 403(b) administration

will be forthcoming from AASA to our members. The best way for you to stay atop this information and other

critical issues is to take advantage of AASA’s news services and other member benefits. As your national resource

and federal advocate for public schools and our profession, we invite you to join us. A brochure on the opposite

panel in your toolkit offers more information about AASA membership.

We wish you well with your construction project and hope the Blueprints help.

Sincerely,

Paul D. Houston

Executive Director

American Association of School Administrators

Introduction to

A Guide to Public School Plans 403(b) and 457(b)

AmericAn AssociAtion of school AdministrAtors

Your guide to using the Blueprints Toolkit and Wall Chart

including

Blueprints Glossaryand General Provisions

2

Public school systems have been providing 403(b)

tax-sheltered annuity plans to their employees for

almost 50 years.

Congress enacted legislation that established 403(b)

annuity plans as a benefit to employees working for

non-profit establishments. This includes employees

performing services in education, health care,

and religious and charitable organizations.

As public service employees, these groups of workers

were not afforded the higher salaries, stock awards and

profit-sharing plans that were available to workers in

private industry. Congress provided this benefit to allow

an advantage for non-profit employees to prepare for

their retirement, allowing them to save money earned

before employment taxes were applied.

Today, the opportunity to set aside pre-taxed dollars

for retirement is still a recruitment tool and leading

benefit to employees in our school systems. It is with

these intentions that we strive to continue offering

this valuable benefit.

Originally, these plans were governed by relatively

few regulations. Through the years, there has been

a growing need for the U.S. Treasury and the

Internal Revenue Service to provide and update

403(b) plan guidance.

Compliance with 403(b) tax regulations now varies

greatly among the nation’s public school systems.

Many school systems have implemented procedures

that require plan providers to accept responsibility

for the proper administration of their accounts;

others have had little, if any, involvement with their

plans, hoping that plan providers have compliance

procedures in place.

The final IRS regulations for 403(b) plans, issued

on July 26, 2007, constitute the first comprehensive

guidance issued in more than four decades. They

include significant changes, including accountability

measures that school system leaders must know

about in order to properly administer their 403(b) plans.

The IRS previously has released regulations for 457(b)

plans that are also offered by many public school

systems. Both plan types are very similar. Public

schools are required to administer both types

of plans for compliance.

Background

Introduction to

A Guide to Public School Plans 403(b) and 457(b)

Introduction

3

About Blueprints: A Guide to Public School Plans 403(b) and 457(b)

Blueprints is a toolkit designed for school system

leaders by the American Association of School

Administrators through the Center for System

Leadership™. The Center is a learning organization

that fosters, develops and supports superintendents

of schools and other school system leaders who are

leading the transformation of public education.

First and foremost, it is important to remember that

these plans provide an excellent opportunity for your

employees to save for retirement with contributions to

a 403(b) plan. The 403(b) regulations allow for some

flexibility in plan design, so it is a good idea to become

familiar with all the materials in the toolkit.

The purpose of the toolkit is not to provide tax

or legal advice, but rather to provide information

to facilitate discussion among school system

administrators, product providers and employees

that leads to having tax-compliant retirement plans

by the Jan. 1, 2009, IRS deadline. School system

officials should consult an independent tax advisor

to obtain tax advice. A Blueprints toolkit is provided

to every public school system superintendent in

the United States. The Blueprints project is made

possible with generous grants from four leaders

in the financial services industry: AIG Retirement,

AXA Equitable, Horace Mann and ING.

About

4

A Guide to Public School Plans 403(b) and 457(b)

The enclosed 1. Blueprints wall chart (top right

pocket) provides a visual step-by-step guide

to becoming 403(b) compliant. Along with the

Glossary and General Provisions section of this

booklet, the Blueprints wall chart begins and

ends with the relationships and responsibilities

of three subgroups:

school system, which the IRS considers to be

the 403(b) plan sponsor (and superintendents

who typically are the point persons for the

403(b) program decisions and structure)

employee participants

plan providers

The wall chart allows superintendents to easily

see the responsibilities of each subgroup as

the current 403(b) program progresses toward

the new IRS requirements for a compliant

403(b) plan.

The 2. Glossary and General Provisions section of

this booklet contains explanations and descriptions

of terms found on the Blueprints wall chart. Though

it can be used as a resource for understanding

terms in the entire toolkit, the Glossary and General

Provisions booklet is designed as a supporting

document for the Blueprints wall chart. These

two tools should be used together.

3. Tools-You-Can-Use CD-ROM (inner right panel)

provides tools to help develop and maintain 403(b)

plans, as well as sample letters to communicate to

employees and providers, sample service provider

agreements, and IRS web links.

Records Retention

and Maintenance Checklist:

Records are vital for retirement plan compliance.

This tool identifies the records a school system

must retain and maintain for compliance.

Request for Information Form (RFI):

This assessment tool is designed to screen the

level of compliance services provided by prod-

uct providers. When used with the wall chart

(step 2), completed RFI forms help determine

which contracts may be available under the

plan. Product providers complete this form.

Two samples of RFI are included.

403(b) Employee Notice of Eligibility:

This form provides the required notice

to eligible employees about their rights to

participate in 403(b) plans and outlines

enrollment procedures. This notice is required

in order to meet the school system’s compliance

responsibility for universal availability.

Introduction

A Guide to Public School Plans

How to use the Blueprints tools:

5

Certified Service Provider Agreements:

Two sample service provider agreements are

provided as examples of agreements that

delineate shared plan responsibilities for the

school system and product providers. The

school system has certain responsibilities and

the product providers may be assigned to share

certain responsibilities. This type of agreement is

necessary to operate the plan under the terms

and conditions of the written plan.

Hot IRS Audit Issues:

This side-by-side comparison of 403(b) and

457(b) plans provides a quick way to view the

general elements of both plan types. The IRS

provides school systems an annual report that

identifies problem areas discovered during its

audits. This tool is a good resource to review

plan areas that may be out of compliance.

The highlighted areas in red are key areas

that have been identified by the IRS as

common audit concerns.

Employee Notification Letters:

Two sample employee letters are provided

notifying employees of changes in the school

system’s 403(b) plan.

Product Provider Letter:

This is a sample letter to provide notice to

product provider companies that their contracts

have been approved. This means they can offer

their contracts under the school system plan.

IRS Model Plan Language:

This Internal Revenue Service document offers

model language for a 403(b) plan and includes

rules for its plan language use. While parts of

the document do not apply to public school

systems, the model plan language can be used

in the adoption of an acceptable 403(b) plan.

Resources from the Internal Revenue Service:

This section provides links to relevant informa-

tion resources on the IRS website, including the

new 180-page set of IRS 403(b) regulations.

The powerful combination of tools in this toolkit

provides school system leaders with a blueprint for

building a compliant 403(b) employee retirement plan.

During construction of the written plan, the maximum

value of Blueprints may be realized in the combined,

simultaneous use of these three tools:

Blueprints wall chart –

Follow the step-by-step process

Glossary and General Provisions

section of this booklet – Apply terms,

general rules and conditions

Tools-You-Can-Use CD-ROM –

Connect Blueprints tools and link to

IRS resources

Blueprints tools

403(b) and 457(b)

6

Required Plan Provisions (See Blueprints wall chart.)

These six provisions are required in the employee retirement 403(b) plan: eligibility, contracts, benefits, nondiscrimination/universal availability, contribution limits and distributions.

Eligibility

Eligibility defines employees who can participate in the 403(b) plan.

Includes employees working directly or indirectly for the school system.

May not include independent contractors.

May not refer to employees by job classification.

May exclude employees who are eligible to participate in other plans that the school system offers, including 401(a), 401(k), 403(b) and/or government 457(b) plans.

May exclude nonresident alien employees.

May exclude student employees.

May exclude those who normally work fewer than 20 hours a week. Under the 403(b) rules, “normally less than 20 hours a week” is interpreted as performing fewer than 1,000 hours per year. Allows for annual “look back” for existing employees. Newly hired employees may be excluded if in the year of hire it is reasonably believed the employee will work fewer than 1,000 hours per year. Under the “look back” rule, if the employee has worked at least 1,000 hours in the previous year, he/she must be allowed to participate in the 403(b) plan in the current year.

Glossary and General Provisions

Glossary

The recently released Internal Revenue Service 403(b) regulations apply to any payroll-deducted elective deferrals, 403(b) Roth contributions, non-elective employer contributions, and employer-matched contribu-tions permitted under a school system’s 403(b) plan.

In the event that an employee has more than one 403(b) contract through the school system’s 403(b) program, the contracts will be aggregated as one 403(b) contract issued to the participant. The aggregated contracts are treated as if the employee has only one contract.

Loan aggregation rules apply to contracts and accounts to all plans of the school system including the 403(b) and other plans of the school system. A school system may have multiple plans, such as a 403(b) and a 457(b).

If the employee participates in both plans and if both plans offer a loan, both account values and outstanding loan amounts under each plan must be aggregated for purposes of qualifying the participant for a loan. School system plans may include plans offered by the state, county or city that are payroll-deducted by the school system. Examples of these would be a 401(a), 401(k), 403(b) and/or a 457(b).

For more detail, see Glossary, Loans, page 10.

7

Contracts

Two types of contracts meet the requirements for 403(b): annuity contracts issued by an insurance company and mutual fund custodial accounts (i.e., invested solely in mutual fund shares).

Multiple 403(b) contracts issued to a participant are required by the IRS to be aggregated as one 403(b) contract.

The school system’s written 403(b) plan may reference an external list of multiple contracts to satisfy the requirement that “contracts available under the plan” be identified in the written plan.

Benefits

The IRS Section Code 403(b) provides two types of benefits.

Elective salary deferrals and Roth 403(b) contributions are non-forfeitable (fully vested).

The participant’s contract may not be assigned to another party unless subject to a qualified domestic relations order.

Nondiscrimination/Universal Availability

All eligible employees must be given an opportunity to participate.

If any one eligible employee has the ability to contribute elective salary deferrals and/or Roth 403(b) contributions in the amount of at least $200 per year, then each eligible employee must have the opportunity to participate.

In accordance with anti-conditioning requirements, a plan may not set entry requirements or annual dollar amounts for elective salary deferrals or Roth 403(b) contributions.

Anti-conditioning means that a plan cannot place conditions on an eligible employee that would set »requirements for entry.

Meaningful Communication

At the point of hire, and at least annually, each eligible employee must be notified of his or her right to participate in the school system’s 403(b) plan. This notice must be written and include the products available under the plan. The written notice must also include a list of actions the employee may take with regard to enrolling in and contributing to the plan, including how to:

stop contributions »

start contributions »

increase contributions »

decrease contributions »

change providers. »

If the plan permits a Designated 403(b) Roth Account contribution [see Glossary and General Provisions, page 8], the opportunity to make these Roth 403(b) contributions must be included in the notice. See the sample Employee Notice of Eligibility on the Blueprints Tools-You-Can-Use CD-ROM.

All eligible employees must receive, by direct delivery, a written annual notification of the school system’s 403(b) plans that are available.

8

General Provisions

Contribution Limits

The general limitation under Internal Revenue Code Section 415: 100 percent of compensation not to exceed the dollar amount established annually by the IRS (currently $45,000 in 2007, increasing to $46,000 in 2008). The Section 415 limit is 100 percent of income or the sum of employee elective deferrals and the employer contributions (annual additions).

General Limitation under Internal Revenue Code Section 402(g): The total of elective deferrals (including the 403(b) special catch-up amount) and Roth 403(b) contributions made in a year cannot exceed the dollar amount established annually by the IRS (currently $15,500 in 2007 and 2008).

This limit does » not include any age 50+ catch-up contributions.

Any elective deferrals or designated Roth contributions that a participant has made to any 401(k) or 403(b) »plan and any elective deferrals that a participant has made toward a SIMPLE plan or a salary-reduction simplified employee pension plan in the same year (regardless of the employer) counts toward this general limit.

Ordering of Catch-up Contributions: The 403(b) regulations provide that catch-up contributions must be made first to the 403(b) special catch-up amount (expansion of contribution limit) and then to the age-based catch up available to participants age 50 or older.

Excess Contributions: These must be corrected by April 15 of the year following the year of the deferral.

Timely Remittances: These contributions from the employer to the product provider are to be received within a reasonable time, but no later than 15 business days after the close of the month of the salary deduction.

See worksheet provided in IRS Publication No. 571 (Link to IRS on the Blueprints Tools-You-Can-Use CD-ROM.)

[For example, a teacher who has her own business and has a simplified employer plan (SEP) might be making contributions to it. The contributions to her SEP plan must be counted first against her contributions to her 403(b) plan to ensure she does not exceed the contribution limit.]

Post-severance employee contributions may be made up to 2½ months after the severance or the end of the year, whichever comes first. These contributions can be made if they would have been paid to the employee, had the employee not severed employment. This includes payments for accrued bona fide sick, vacation or other leave, but only if the employee would have been able to use the leave if employment had continued.

Post-retirement employer contributions, if available under the 403(b) plan, may be made up to 5 years after separation from service if they are employer non-elective contributions and are subject to the general limitation under Internal Revenue Code Section 415.

Glossary

9

Distributions (Benefits)

The following are all distributable events or allowable reasons to withdraw or distribute funds.

Severance of employment »

Attainment of age 59½ »

Death »

Disability »

Financial hardship contributions made after 1988. Both the value of the contributions and earnings »attributable to amounts as of Dec. 31, 1988, can be withdrawn if the product provider can track that value.

» Rollover Availability: Upon separation of service, a participant must be allowed to roll over his or her 403(b) account to an IRA or other eligible retirement plan in which the individual participates. Participants must receive advance notice of the opportunity to roll over amounts to preserve tax-deferred status.

» Required Minimum Distributions: When the participant reaches age 70½ or upon separation from service from the employer sponsoring the plan, whichever is later, the participant must take an annual Required Minimum Distribution.

» Distributions from Roth 403(b) Accounts: When Roth 403(b) funds can be distributed as described above, they will be considered Qualified Distributions, with earnings free from federal income tax. To qualify, the Roth 403(b) account must be at least five years old and the funds distributed are due to the participant reaching 59½ years of age, disability or death.

» Exceptions: School system contributions to annuity contracts, prior to the new IRS rules, are unrestricted unless the plan or the contract restricts them. After the regulations go into effect, Jan. 1, 2009, school system contributions into new accounts and contracts are restricted to: severance of employment, death, occurrence of a prior event (such as disability or reaching a stated age under the 403(b) plan), and financial hardship (to the extent permitted under the 403(b) plan).

Special rules for annuity contracts and custodial accounts:

Pre-1989 employee elective deferrals to annuity contracts do not require a distributable event »under the IRS rule. However, the plan or the contract may have restrictions.

Earnings attributable to pre-1989 employer contributions to custodial accounts may be distributed »for a financial hardship.

Optional Plan ProvisionsSchool systems should give careful consideration when selecting optional provisions to be included in the written plan. These provisions represent certain benefits that enhance the employee retirement 403(b) plan and are transactional in nature.

The IRS regulations permit a school system to delegate some or all of its administrative responsibilities to service providers. The IRS will not allow these tasks to be delegated to the employee participant.

The IRS regulations anticipate that schools may not wish to handle the day-to-day administration of its 403(b) program. As a result, a school may delegate some or all of its administrative responsibilities to service providers. Keep in mind that the IRS will not allow these tasks to be delegated to the employee participant.

10

Transfers

Under the regulations, transfers will be one of three types: (1) contract exchanges; (2) plan-to-plan transfers; or (3) transfers to purchase service credit.

1. Contract Exchanges: Transfers between approved contracts under the same 403(b) plan are called “contract exchanges.” The IRS requires that the school system and the product provider receiving the contract exchange agree to ongoing information-sharing beginning Sept. 25, 2007, which must be reduced to writing (whether as a part of a written plan or as a separate agreement) no later than Jan. 1, 2009. In addition, the contract receiving the exchange must ensure that the accumulated benefit remains unchanged (net of applicable contractual charges).

Amounts transferred prior to Sept. 25, 2007, are grandfathered from the contract exchange rules, provided that these contracts do not receive any subsequent contributions, transfers or rollovers.

Such exchanges may occur only if the plan permits. The new rules require that the contract receiving the exchange must impose withdrawal restrictions that are equal to or less than the contract being exchanged. They must satisfy an “accumulated benefit” test. This category of exchanges includes exchanges between contracts approved by the school system to receive ongoing contributions, as well those contracts that may receive exchanges but are not currently authorized by the school system to receive ongoing contributions to the 403(b) plan.

2. Plan-to-Plan Transfers: Under a plan-to-plan transfer, an employee may transfer an account from one 403(b) plan to a new or former employer’s 403(b) plan. The transferring 403(b) plan must permit the transfer out and the receiving 403(b) plan must permit the transfer in. In addition, the contract receiving the exchange must ensure that the accumulated benefit remains unchanged (net of applicable contractual charges).

3. Transfers to Purchase Service Credit: If permitted under both the 403(b) plan and the retirement system, a participant may transfer a 403(b) account to purchase service credit in the state retirement system.

QDRO (Qualified Domestic Relations Order)

The segregation of all or part of a participant account to satisfy a court-ordered divorce settlement is called a qualified domestic relations order.

Loans

If loans are permitted, plan provisions should detail loan conditions and terms and incorporate the IRS rules for determining the maximum amount available for a loan.

Specifically, the IRS requires that a participant’s account under all plans of the employer (including 401(a), 401(k), and/or 457(b)) be aggregated as a single participant account and that 50 percent of that vested participant account (up to $50,000) less any outstanding loan balance of the participant across all plans over the past 12 months be available for a loan.

If the loan amount is less than $10,000, the participant may borrow up to 100 percent of the account balance.

Financial Hardship Withdrawals

If permitted under the plan, a participant who has an immediate and heavy financial need may take a hardship withdrawal.

Financial hardship withdrawals are allowable provided that appropriate documentation of the hardship and the inability to meet that hardship from other financial resources is confirmed to the school system and/or product provider.

The 403(b) plan may require the participant to cease contributions to the 403(b) (and other voluntary contributions to other plans of the school system) for six months following the date of hardship.

GlossaryGeneral Provisions

11

Other Related Terms

Consequences of Failure To Comply with IRS RulesA failure to comply with IRS rules can result in disqualification of the contracts issued.All 403(b) contracts issued to participants under the school system’s 403(b) plan are disqualified if:

the school system fails to maintain a written plan

the school system fails to meet the universal availability/nondiscrimination requirements

the problem is not an “operational” problem.

An operational problem is one that arises because the plan did not follow the terms of the school system’s »written plan. If an operational defect occurs within one 403(b) contract, the result will be disqualification of all 403(b) contracts held for that employee. This is because multiple 403(b) contracts issued to a participant are required by the IRS to be aggregated as one 403(b) contract.

Accumulated Benefit The aggregated total benefit (meaning contributions and attributable earnings) to which a participant

or beneficiary is entitled to under the contract.

Annuity Contract A contract that is issued by an insurance company qualified to issue annuity contracts in a state

and that includes a provision to provide for a payment in the form of an annuity.

Beneficiary A person who is entitled to benefits in respect of a participant following the participant’s death

or an alternate payee pursuant to a qualified domestic relations order.

Designated Roth Account A post-tax elective deferral made to a 403(b) plan whose earnings may be distributed free

from federal income tax if the distribution meets the criteria for a qualified distribution.

Elective Deferral A contribution arrangement where employees can set aside part of their compensation as

a contribution to the 403(b) plan subject to certain limits in Internal Revenue Code Section 402(g).

Eligible Employee An employee performing services for a public school system who does not fit into a classification

that is specifically excluded by the Internal Revenue Code.

Includable Compensation The employee’s compensation received from an eligible employer that is includable in the participant’s

gross income for federal income tax purposes for the most recent period that is a year of service.

Information-Sharing Agreement An optional provision that allows participants to exchange all or a portion of their account balance with

product providers under certain IRS conditions. In the Blueprints CD-ROM document called IRS Model Plan Language, see pages 25-26, under “Contract and Custodial Account Exchanges.”

Participant An employee for whom a section 403(b) contract is currently being purchased, or an employee

or former employee for whom a section 403(b) contract has previously been purchased and who has not received a distribution of his or her entire accumulated benefit under the contract.

Plan Sponsor The school system building the plan.

Product Provider A company that creates and delivers 403(b) products.

QDRO (Qualified Domestic Relations Order) Segregation of all or part of a participant account to satisfy a court-ordered divorce settlement.

Rollover A required procedure in which an employee must be allowed, after separation of service, to move his/her 403(b) account balance out of the school system’s plan to another retirement plan. Allowing accounts to “roll over” into a school system 403(b) plan is an optional provision of the school system’s 403(b) plan.

American Association of School Administrators 801 N. Quincy St., 700 • Arlington, VA 22203

703-528-0700 www.aasa.org

Copyright © 2008 by the American Association of School Administrators. All rights reserved. More information is available at the AASA website.

Disclosure: This information is provided as information only and is not intended to be used to avoid tax penalties or to render tax or legal advice. The taxpayer should seek advice from an independent tax advisor. Neither the American Association of School Administrators nor AASA employees, contractors or sponsors offer legal or tax advice.

Wa

llC

ha

rt

A Guide to Public School Plans 403(b)

A G

uide

to

Publ

ic S

choo

l Pla

ns 4

03

(b)

WAll ChART

On July 23, 2007, the Internal Revenue Service and the U.S. Treasury

Department published final regulations for public school 403(b) plans.

The general effective date for the regulations is no later than January 1,

2009. School systems with union collective bargaining contracts may

have different effective dates.

School systems will need to take certain steps to comply with the

new regulations. For example, the new regulations require public school

systems to adopt a written plan that meets the IRS rules for form and

operation. The plan document must include provisions regarding such

issues as eligibility, benefits and limits, and must outline allocation of

responsibilities for the school system employee and plan provider.

In addition, special rules apply to certain types of transfers previously

referred to as 90–24 transfers. All 90–24 transfers made before

September 24, 2007 were grandfathered; those made after

Sept. 24, 2007, must adhere to new rules.

This chart outlines the major changes and what steps school systems

can take to ensure compliance by the deadline. A glossary of terms,

included in the toolkit’s right-hand pocket, helps explain the new

regulations and their implementation.

A Guide to Public School Plans 403(b)

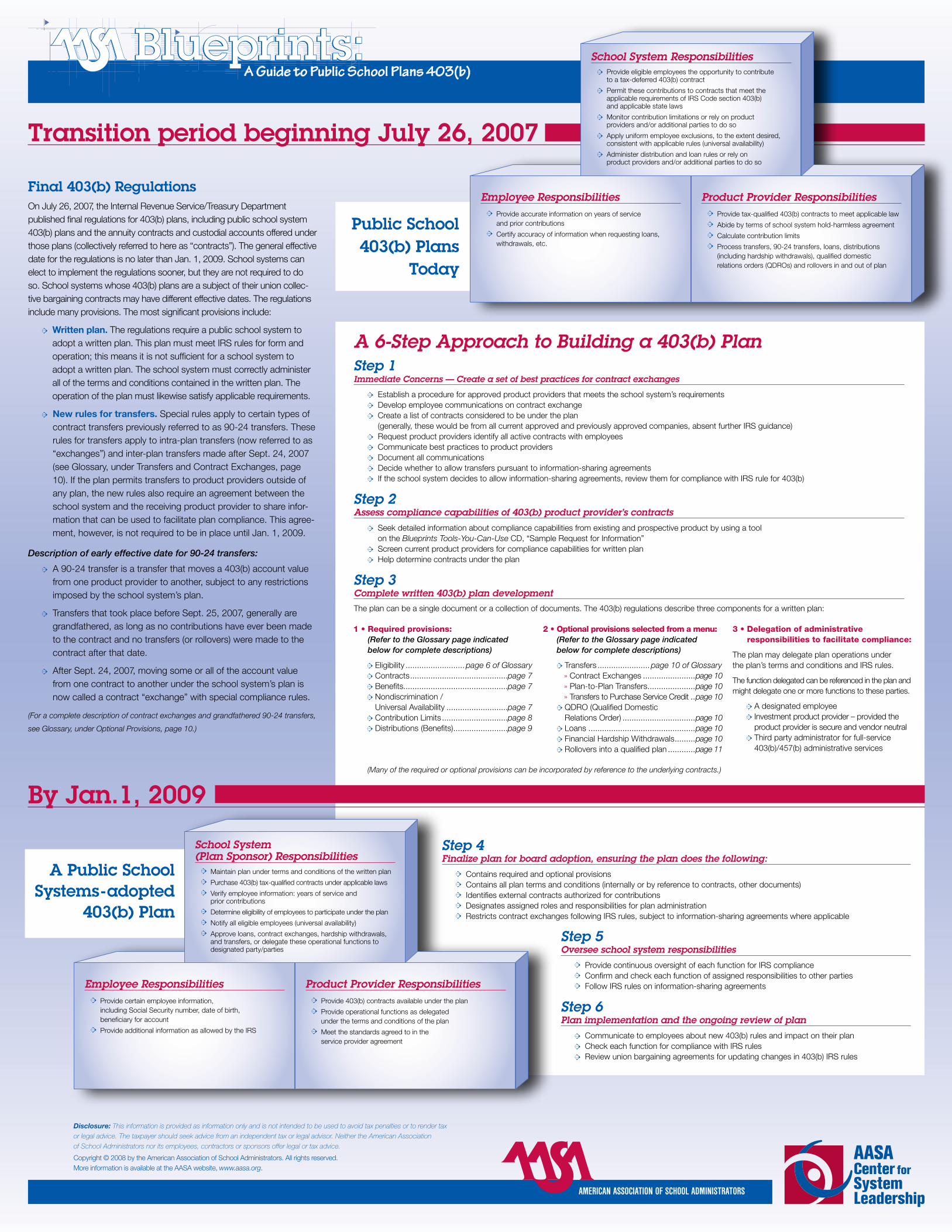

Final 403(b) RegulationsOn July 26, 2007, the Internal Revenue Service/Treasury Department published final regulations for 403(b) plans, including public school system 403(b) plans and the annuity contracts and custodial accounts offered under those plans (collectively referred to here as “contracts”). The general effective date for the regulations is no later than Jan. 1, 2009. School systems can elect to implement the regulations sooner, but they are not required to do so. School systems whose 403(b) plans are a subject of their union collec-tive bargaining contracts may have different effective dates. The regulations include many provisions. The most significant provisions include:

Written plan. The regulations require a public school system to adopt a written plan. This plan must meet IRS rules for form and operation; this means it is not sufficient for a school system to adopt a written plan. The school system must correctly administer all of the terms and conditions contained in the written plan. The operation of the plan must likewise satisfy applicable requirements.

New rules for transfers. Special rules apply to certain types of contract transfers previously referred to as 90-24 transfers. These rules for transfers apply to intra-plan transfers (now referred to as “exchanges”) and inter-plan transfers made after Sept. 24, 2007 (see Glossary, under Transfers and Contract Exchanges, page 10). If the plan permits transfers to product providers outside of any plan, the new rules also require an agreement between the school system and the receiving product provider to share infor-mation that can be used to facilitate plan compliance. This agree-ment, however, is not required to be in place until Jan. 1, 2009.

Description of early effective date for 90-24 transfers:

A 90-24 transfer is a transfer that moves a 403(b) account value from one product provider to another, subject to any restrictions imposed by the school system’s plan.

Transfers that took place before Sept. 25, 2007, generally are grandfathered, as long as no contributions have ever been made to the contract and no transfers (or rollovers) were made to the contract after that date.

After Sept. 24, 2007, moving some or all of the account value from one contract to another under the school system’s plan is now called a contract “exchange” with special compliance rules.

(For a complete description of contract exchanges and grandfathered 90-24 transfers,

see Glossary, under Optional Provisions, page 10.)

A 6-Step Approach to Building a 403(b) PlanStep 1 Immediate Concerns — Create a set of best practices for contract exchanges

Establish a procedure for approved product providers that meets the school system’s requirements Develop employee communications on contract exchange Create a list of contracts considered to be under the plan

(generally, these would be from all current approved and previously approved companies, absent further IRS guidance) Request product providers identify all active contracts with employees Communicate best practices to product providers Document all communications Decide whether to allow transfers pursuant to information-sharing agreements If the school system decides to allow information-sharing agreements, review them for compliance with IRS rule for 403(b)

Step 2 Assess compliance capabilities of 403(b) product provider’s contracts

Seek detailed information about compliance capabilities from existing and prospective product by using a tool on the Blueprints Tools-You-Can-Use CD, “Sample Request for Information”

Screen current product providers for compliance capabilities for written plan Help determine contracts under the plan

Step 3 Complete written 403(b) plan development The plan can be a single document or a collection of documents. The 403(b) regulations describe three components for a written plan:

Step 4 Finalize plan for board adoption, ensuring the plan does the following:

Contains required and optional provisions Contains all plan terms and conditions (internally or by reference to contracts, other documents) Identifies external contracts authorized for contributions Designates assigned roles and responsibilities for plan administration Restricts contract exchanges following IRS rules, subject to information-sharing agreements where applicable

Step 5 Oversee school system responsibilities

Provide continuous oversight of each function for IRS compliance Confirm and check each function of assigned responsibilities to other parties Follow IRS rules on information-sharing agreements

Step 6 Plan implementation and the ongoing review of plan

Communicate to employees about new 403(b) rules and impact on their plan Check each function for compliance with IRS rules Review union bargaining agreements for updating changes in 403(b) IRS rules

Transition period beginning July 26, 2007

By Jan.1, 2009

Public School 403(b) Plans

Today

1 • Required provisions: (Refer to the Glossary page indicated below for complete descriptions)

Eligibility .......................... page 6 of Glossary Contracts ...........................................page 7 Benefits..............................................page 7 Nondiscrimination /

Universal Availability ...........................page 7 Contribution Limits .............................page 8 Distributions (Benefits) ........................page 9

2 • Optional provisions selected from a menu: (Refer to the Glossary page indicated below for complete descriptions)

Transfers ....................... page 10 of Glossary » Contract Exchanges .......................page 10 » Plan-to-Plan Transfers .....................page 10 » Transfers to Purchase Service Credit ..page 10 QDRO (Qualified Domestic

Relations Order) ................................page 10 Loans ...............................................page 10 Financial Hardship Withdrawals .........page 10 Rollovers into a qualified plan ............page 11

3 • Delegation of administrative responsibilities to facilitate compliance:

The plan may delegate plan operations under the plan’s terms and conditions and IRS rules.

The function delegated can be referenced in the plan and might delegate one or more functions to these parties.

A designated employee Investment product provider – provided the product provider is secure and vendor neutral

Third party administrator for full-service 403(b)/457(b) administrative services

(Many of the required or optional provisions can be incorporated by reference to the underlying contracts.)

School System Responsibilities Provide eligible employees the opportunity to contribute

to a tax-deferred 403(b) contract

Permit these contributions to contracts that meet the applicable requirements of IRS Code section 403(b) and applicable state laws

Monitor contribution limitations or rely on product providers and/or additional parties to do so

Apply uniform employee exclusions, to the extent desired, consistent with applicable rules (universal availability)

Administer distribution and loan rules or rely on product providers and/or additional parties to do so

School System (Plan Sponsor) Responsibilities

Maintain plan under terms and conditions of the written plan

Purchase 403(b) tax-qualified contracts under applicable laws

Verify employee information: years of service and prior contributions

Determine eligibility of employees to participate under the plan

Notify all eligible employees (universal availability)

Approve loans, contract exchanges, hardship withdrawals, and transfers, or delegate these operational functions to designated party/parties

Employee Responsibilities Provide accurate information on years of service

and prior contributions

Certify accuracy of information when requesting loans, withdrawals, etc.

Employee Responsibilities Provide certain employee information,

including Social Security number, date of birth, beneficiary for account

Provide additional information as allowed by the IRS

Product Provider Responsibilities Provide tax-qualified 403(b) contracts to meet applicable law

Abide by terms of school system hold-harmless agreement

Calculate contribution limits

Process transfers, 90-24 transfers, loans, distributions (including hardship withdrawals), qualified domestic relations orders (QDROs) and rollovers in and out of plan

Product Provider Responsibilities Provide 403(b) contracts available under the plan

Provide operational functions as delegated under the terms and conditions of the plan

Meet the standards agreed to in the service provider agreement

A Public School Systems - adopted

403(b) Plan

AmericAn AssociAtion of school AdministrAtors

Disclosure: This information is provided as information only and is not intended to be used to avoid tax penalties or to render tax

or legal advice. The taxpayer should seek advice from an independent tax or legal advisor. Neither the American Association

of School Administrators nor its employees, contractors or sponsors offer legal or tax advice.

Copyright © 2008 by the American Association of School Administrators. All rights reserved. More information is available at the AASA website, www.aasa.org.

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey A

1 of 7

Blueprints: A Guide to School System Plans 403(b) and 457(b) 403(b) Product Provider Compliance Questionnaire

Request for Information - Survey A

— For use as a sample only — Final 403(b) regulations were issued in July 2007, and will become effective Jan. 1, 2009. (Insert school system name here) ("Employer") is reviewing its 403(b) program to ensure compliance with existing and expected IRS rules for 403(b) plans and programs. This questionnaire is being sent to all product providers in Employer's 403(b) program. If multiple contracts or accounts are offered to the school system, a single questionnaire may be completed for all contracts for which the answers are identical. Otherwise, separate questionnaires should be completed and appropriately identified. Please respond to the questions below and return the completed questionnaire to (Insert name of business manager and address here) not later than (Insert deadline here).

1. Is your 403(b) contract or account an annuity contract that meets relevant

form requirements under Code Section 403(b)(1) or a custodial account that meets relevant form requirements under Code Section 403(b)(7), including: • deferral, distribution and loan limitations, • nontransferability (annuities only), and • direct rollover and minimum distribution requirements? Yes No

2. Is your 403(b) contract or account available to any employee who is

otherwise eligible to participate? For example, if it imposes a minimum annual contribution, is that minimum less than or equal to $200? Yes No

3. Are contribution limits monitored by your company for each employee who

participates in your 403(b) contract or account? Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey A

2 of 7

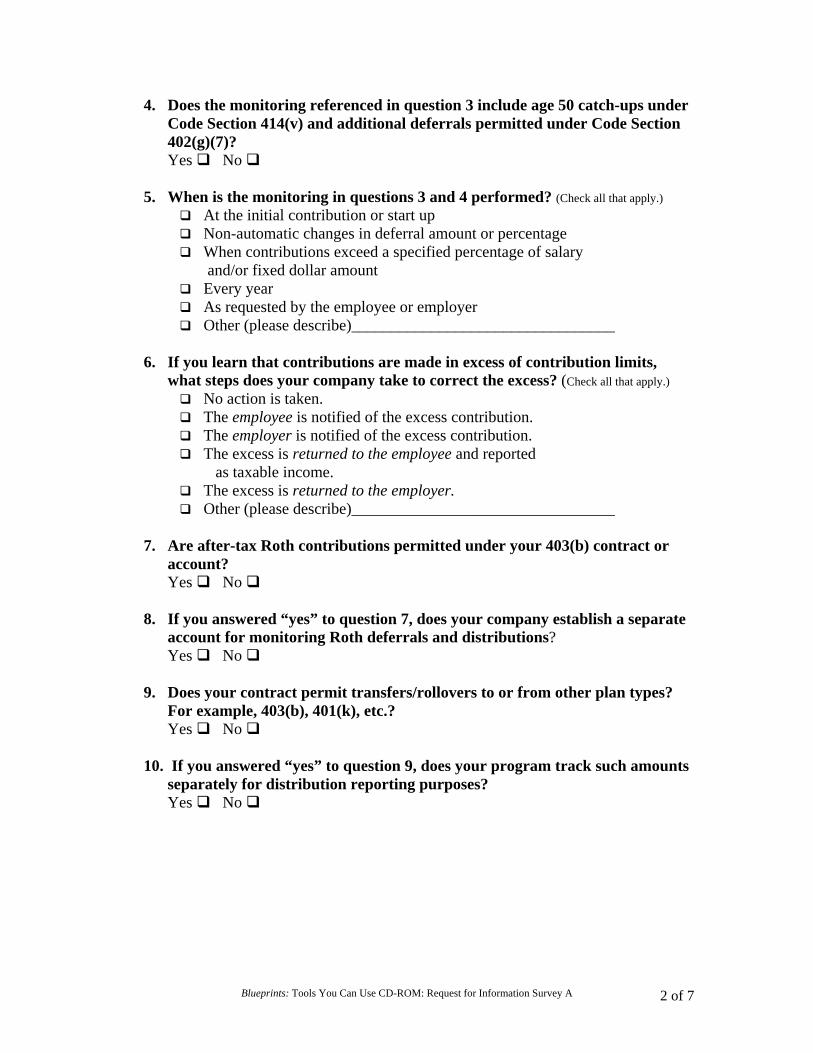

4. Does the monitoring referenced in question 3 include age 50 catch-ups under Code Section 414(v) and additional deferrals permitted under Code Section 402(g)(7)?

Yes No 5. When is the monitoring in questions 3 and 4 performed? (Check all that apply.)

At the initial contribution or start up Non-automatic changes in deferral amount or percentage When contributions exceed a specified percentage of salary

and/or fixed dollar amount Every year As requested by the employee or employer Other (please describe)_________________________________

6. If you learn that contributions are made in excess of contribution limits,

what steps does your company take to correct the excess? (Check all that apply.) No action is taken. The employee is notified of the excess contribution. The employer is notified of the excess contribution. The excess is returned to the employee and reported

as taxable income. The excess is returned to the employer. Other (please describe)_________________________________

7. Are after-tax Roth contributions permitted under your 403(b) contract or

account? Yes No

8. If you answered “yes” to question 7, does your company establish a separate

account for monitoring Roth deferrals and distributions? Yes No

9. Does your contract permit transfers/rollovers to or from other plan types?

For example, 403(b), 401(k), etc.? Yes No

10. If you answered “yes” to question 9, does your program track such amounts

separately for distribution reporting purposes? Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey A

3 of 7

11. Are loans permitted, or are they expected to be permitted, under an

employee’s 403(b) account? Yes No If you answered “yes” to question 11, please answer “a” and “b” below. If you answered “no” to question 11, please proceed to question 12.

(a) Are loans restricted to amounts that do not exceed the lesser of (i) $50,000 minus the highest outstanding loan balance during the preceding 12-month period, or (ii) 50% of the vested account balance or 100% of the vested account balance up to $10,000, whichever is greater?

Yes No (b) Is a default deemed to have occurred no later than the last day of the calendar quarter following the quarter in which a loan payment is missed?

Yes No

12. Generally, assets contributed to your 403(b) program may not be distributed to an employee, absent a distributable event such as death, disability, separation from service, attainment of age 59½, or hardship (if the contract permits). Please indicate below how your organization monitors the distribution of contributions made to the 403(b) program. Check all that apply.

No monitoring of distributions: the employee self-certifies all distribution

requests including hardship withdrawals. Separation of service is confirmed before processing post-separation

distributions. The employee must provide information regarding the amount and the

reason for the hardship distribution on the appropriate distribution form.

The employer is responsible for approving hardship withdrawals. The employer is responsible for approving all withdrawals. Hardship withdrawals are not permitted. Other (please describe)_____________________________

13. In accordance with Section 401(a)(9) of the Internal Revenue Code, are

distributions under the program required to begin the later of (i) April 1st of the calendar year following the calendar year in which an employee attains the age of 70½, or (ii) April 1st of the calendar year following the calendar year in which the employee terminates employment? Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey A

4 of 7

14. Do you notify contract holders of the requirement for distributions prior to

when your records indicate they will attain age 70½ , assuming that they are not still employed by the plan sponsor maintaining the plan? Yes No

15. Does your contract permit distributions required by a Domestic Relations

Order? Yes No

16. Does your record-keeping system include functions that can assist with

compliance among multiple vendors (i.e., for purposes of monitoring contribution limits, loans, if applicable, and hardship withdrawals, if applicable)? Yes No

17. Is your company’s cross-vendor compliance and/or common remitting system

vendor-neutral? (Vendor-neutrality should include not providing preferential access or preferential marketing treatment to an affiliated provider or other business partner or associate.) Yes No

18. Does your company provide access, at the school system’s level, to view single product provider data? Yes No

19. Does your company provide access, at the school system’s level, to view aggregate vendor data? Yes No

20. If your contract permits hardship withdrawals (referenced in question 12), is your program capable of reviewing and making determinations regarding hardship distributions and making available information on such withdrawals to the school system or another party? Yes No N/A Hardships not permitted under the contract.

If you answered “yes” to question 20, please answer “a” and “b” below. If you answered “no” or “N/A” to question 20, please skip to question 21.

(a) Does your system facilitate automatic cessation of deferrals

for a period of six months for any employee who received a hardship distribution? Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey A

5 of 7

(b) Does your system assist the sponsor by facilitating automatic

recommencement of deferrals for any participant who received a hardship distribution upon the satisfaction of the six-month suspension period? Yes No

21. Are your company’s participant records maintained at the school system group level?

Yes No 22. Is your company able to provide plan-level reports?

Yes No If you answered “yes” to question 22 please answer “a,” “b,” “c” and “d” below. If you answered “no” to question 22, please skip to question 23.

(a) Are these plan-level reports automated and available

online? Yes No

(b) Do these plan-level reports include information

reflecting participant hardship withdrawals? Yes No

(c) Do these plan-level reports contain plan-level

information reflecting participant loan activity? Yes No

(d) Can you provide plan-level reports upon request

(within a reasonable timeframe)? Yes No

Please attach a sample of your company’s plan-level report to your completed questionnaire. 23. Does your company maintain detailed procedures to protect the

confidentiality of all records maintained on your cross-vendor compliance and common remitter system? Yes No

24. Will your company agree to both enter into the attached product provider

agreement and, as referenced in that agreement, provide reasonable support to the school system in the event of an IRS audit of the 403(b) plan? Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey A

6 of 7

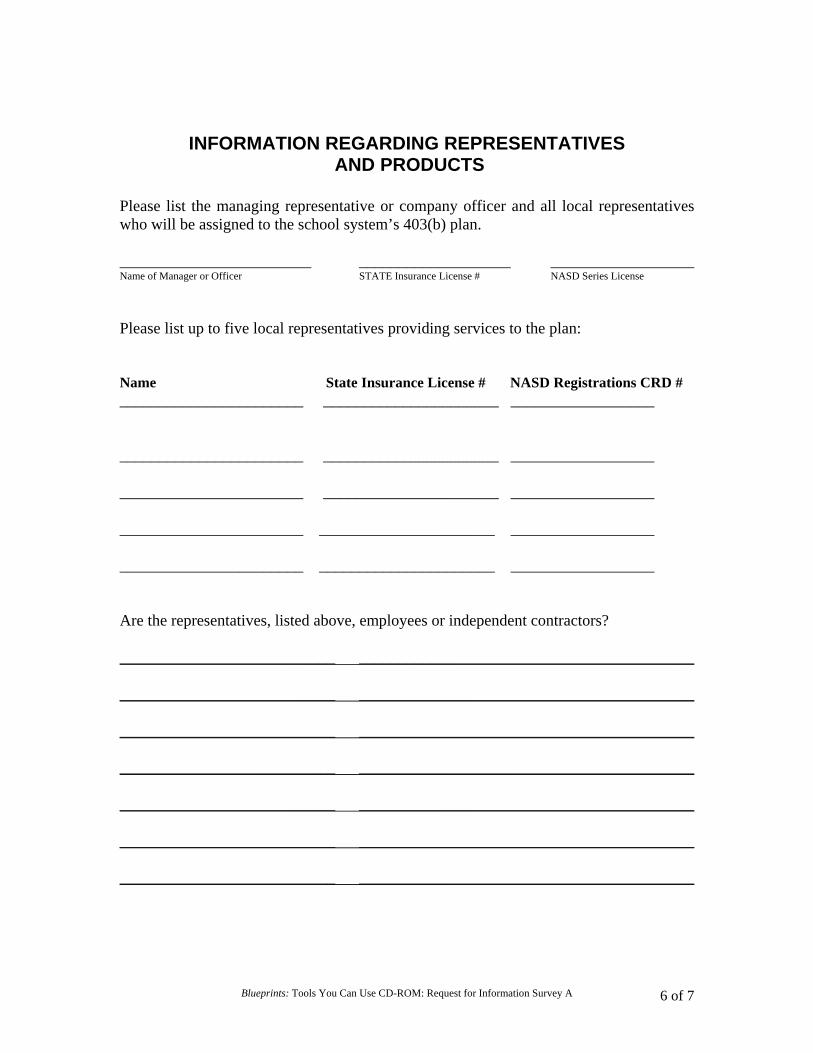

INFORMATION REGARDING REPRESENTATIVES AND PRODUCTS

Please list the managing representative or company officer and all local representatives who will be assigned to the school system’s 403(b) plan. ________________________ ___________________ __________________ Name of Manager or Officer STATE Insurance License # NASD Series License Please list up to five local representatives providing services to the plan:

Name State Insurance License # NASD Registrations CRD # _______________________ ______________________ __________________ _______________________ ______________________ __________________ _______________________ ______________________ __________________ _______________________ ______________________ __________________ _______________________ ______________________ __________________ Are the representatives, listed above, employees or independent contractors? ___________________________ __________________________________________ ___________________________ __________________________________________ ___________________________ __________________________________________ ___________________________ __________________________________________ ___________________________ __________________________________________ ___________________________ __________________________________________ ___________________________ __________________________________________

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey A

7 of 7

PRODUCT PROVIDER IDENTIFICATION ________________________________________________________________________ Company Name ________________________________________________________________________ Addresss ________________________________________________________________________ City, State, Zip

________________________________________________________________________ Web Address ________________________________________________________________________ Type of Company (i.e., insurance company, third-party administrator, brokerage, agency)

List each product to which the certification applies, by product name: Customer service phone number for employee account information. Please provide toll-free telephone number to the organization’s corporate office, if available: ( ) Telephone The undersigned officer of the company referenced above hereby certifies that information provided is correct and complete to the best of his or her knowledge and belief upon reasonable inquiry and review. The undersigned officer also agrees to cooperate with the school system in coordinating plan compliance across multiple providers.

________________________________________________________________________ Name (please print) _____________________________________ ________________________________ Signature Date Completed (_____)________________________ (_____)__________________________ Telephone FAX ________________________________________________________________________ E-mail Address

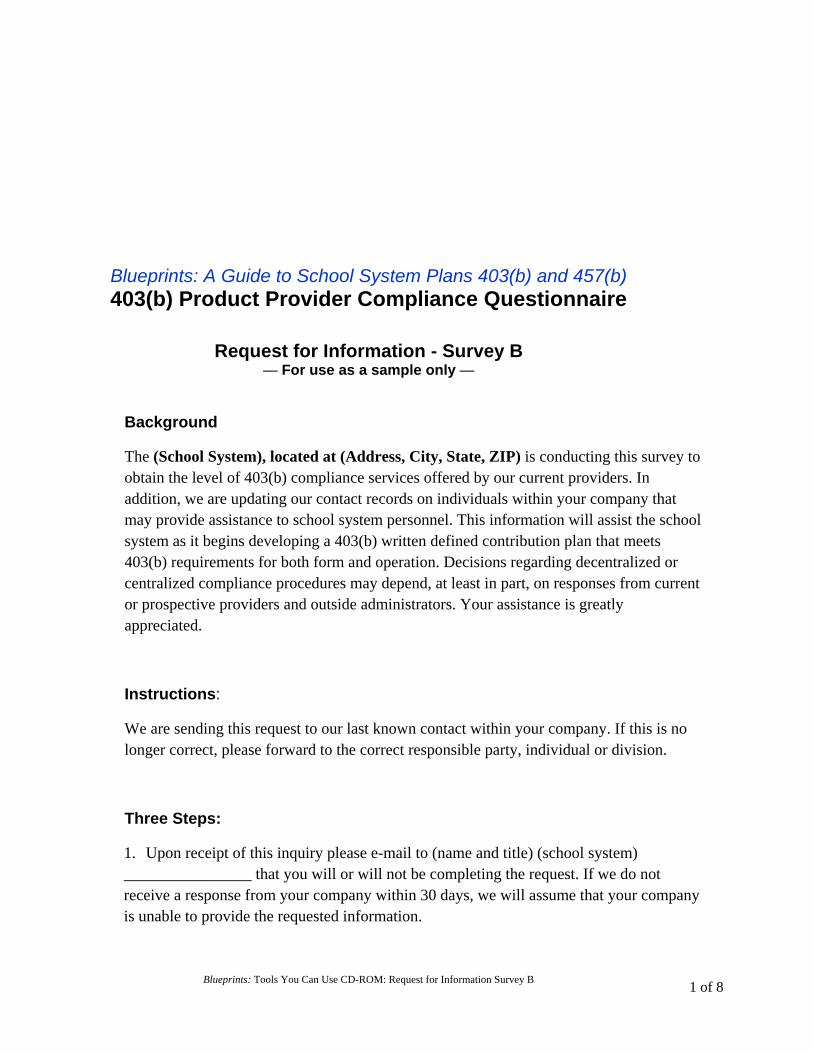

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

1 of 8

Blueprints: A Guide to School System Plans 403(b) and 457(b) 403(b) Product Provider Compliance Questionnaire

Request for Information - Survey B

— For use as a sample only —

Background

The (School System), located at (Address, City, State, ZIP) is conducting this survey to obtain the level of 403(b) compliance services offered by our current providers. In addition, we are updating our contact records on individuals within your company that may provide assistance to school system personnel. This information will assist the school system as it begins developing a 403(b) written defined contribution plan that meets 403(b) requirements for both form and operation. Decisions regarding decentralized or centralized compliance procedures may depend, at least in part, on responses from current or prospective providers and outside administrators. Your assistance is greatly appreciated.

Instructions:

We are sending this request to our last known contact within your company. If this is no longer correct, please forward to the correct responsible party, individual or division.

Three Steps:

1. Upon receipt of this inquiry please e-mail to (name and title) (school system) ________________ that you will or will not be completing the request. If we do not receive a response from your company within 30 days, we will assume that your company is unable to provide the requested information.

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

2 of 8

2. Please complete the survey within 15 business days after your acknowledgement.

3. The compliance survey questions need to be answered with yes or no. This is not a product survey. However, you will be asked to send a sample contract for all products currently offered to ________________ school system. Please do not include sales literature or any information not requested by the school system.

Product (Contract) Issuer Contact Information:

This information should be completed and signed by an officer of the company issuing the contract or the custodian of the custodial account. If you have received this survey as a broker, agent, agency or brokerage firm, please forward to the appropriate investment provider. If you are a third party administrator please fill out Section 1: Company Contacts and Section 3: Third Party Administrators.

Section 1: Company Contacts

_________________________________________________________________________Company Name

_________________________________________________________________________Headquarters: Officer in Charge

_________________________________________________________________________E-mail Address

_________________________________________________________________________Address

(_____)______________________________(_____)______________________________Telephone Fax

Regional Manager of Company :

________________________________________________________________________________Name of Regional Manager of Company NASD Registrations CRD #

________________________________________________________________________________Email Address

________________________________________________________________________________Address

________________________________________________________________________________City, State, Zip

(______)____________________________________(_____)_____________________________ Telephone Fax

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

3 of 8

Company representatives continued:

Please list all sales representatives that provide service to the school system. Please indicate whether the representatives are currently listed as representatives with the school system.

______________________________________________________________________Name

____________________________________________________________________________________ State Insurance License # NASD CRD Registration #

____________________________________________________________________________________Address

____________________________________________________________________________________Telephone Fax

Currently Listed as Representative with the School System? Yes No

______________________________________________________________________Name

____________________________________________________________________________________ State Insurance License # NASD CRD Registration #

____________________________________________________________________________________Address

____________________________________________________________________________________Telephone Fax

Currently Listed as Representative with the School System? Yes No

______________________________________________________________________Name

____________________________________________________________________________________ State Insurance License # NASD CRD Registration #

____________________________________________________________________________________Address

____________________________________________________________________________________Telephone Fax

Currently Listed as Representative with the School System? Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

4 of 8

SECTION 2: Contract Information. Applies to all 403(b) annuity contracts and 403(b)(7) custodial accounts.

All annuity contracts or custodial accounts offered meet the definition of an “annuity contract” or a “custodial account” pursuant to the provisions of Section 403(b) of the Internal Revenue Code and underlying regulations. Yes No

Circle all contract features available that apply to your contracts:

Loans Hardship withdrawals QDRO Contract exchanges

Transfers to purchase service credit Roth 403(b) Plan-to-plan transfers

Compliance Administrative Support:

1. Company has the ability to accept contributions in an electronic format. Yes No

2. Company will credit participant contributions into accounts, with investment directions on file, within the next business day, provided that contributions and associated paperwork is received by the company in good order.

Yes No

3. Company maintains historical information on participant accounts for a minimum of seven (7) years. Yes No

4. Company will calculate maximum allowable contributions for participants that exceed

402(g) and/or 415 limits annually, based upon information provided by the participant, the school system, and, if applicable, the designated administrator.

Yes No

5. Company will distribute all identified excess contributions as described in the school system’s written plan /or designated plan administrator in accordance with IRS regulations.

Yes No

6. Company maintains a school system website that allows the school system to have access to relevant participant information that is updated on a regular basis, determined either by the company or the school system, or both together.

Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

5 of 8

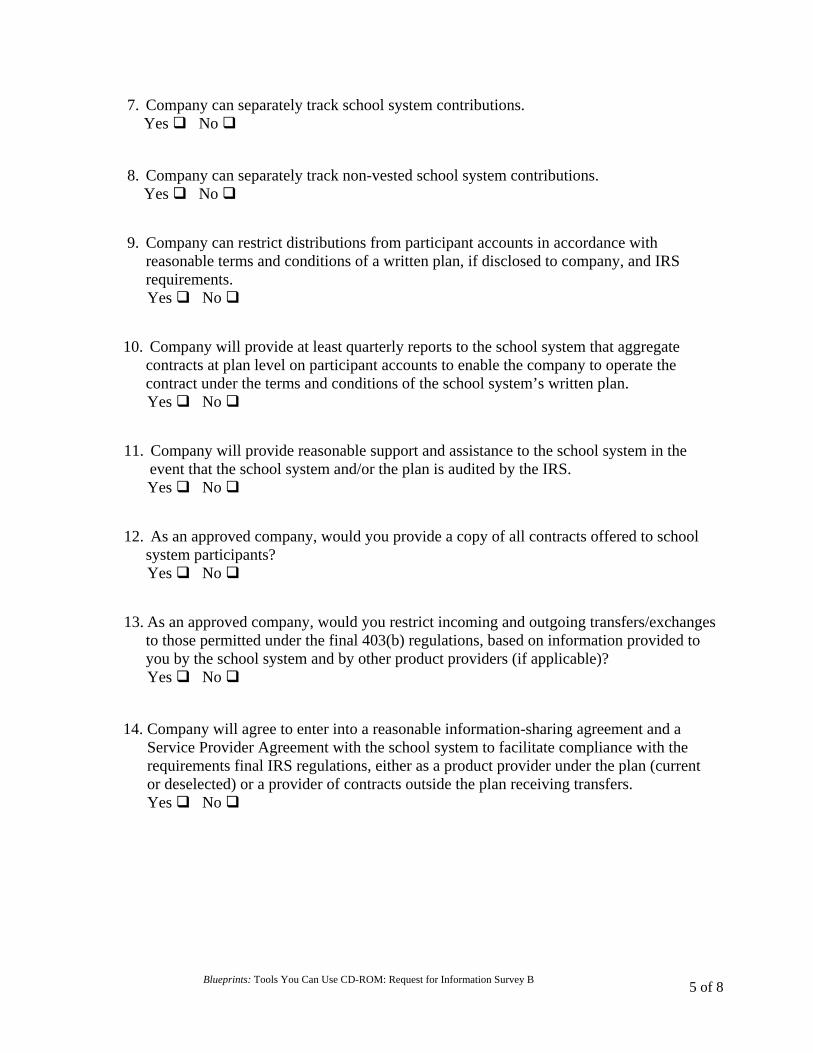

7. Company can separately track school system contributions. Yes No

8. Company can separately track non-vested school system contributions.

Yes No

9. Company can restrict distributions from participant accounts in accordance with reasonable terms and conditions of a written plan, if disclosed to company, and IRS requirements.

Yes No

10. Company will provide at least quarterly reports to the school system that aggregate

contracts at plan level on participant accounts to enable the company to operate the contract under the terms and conditions of the school system’s written plan.

Yes No

11. Company will provide reasonable support and assistance to the school system in the

event that the school system and/or the plan is audited by the IRS. Yes No

12. As an approved company, would you provide a copy of all contracts offered to school system participants?

Yes No

13. As an approved company, would you restrict incoming and outgoing transfers/exchanges

to those permitted under the final 403(b) regulations, based on information provided to you by the school system and by other product providers (if applicable)?

Yes No

14. Company will agree to enter into a reasonable information-sharing agreement and a

Service Provider Agreement with the school system to facilitate compliance with the requirements final IRS regulations, either as a product provider under the plan (current or deselected) or a provider of contracts outside the plan receiving transfers.

Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

6 of 8

The undersigned officer certifies that to the best of his or her knowledge and, upon reasonable inquiry and review, the information affirmed is correct. The undersigned also agrees to cooperate with the school system in coordinating plan compliance across multiple contract issuers. _________________________________________________________________________Name Title _________________________________________________________________________Signature Date _________________________________________________________________________Telephone, Fax, E-mail

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

7 of 8

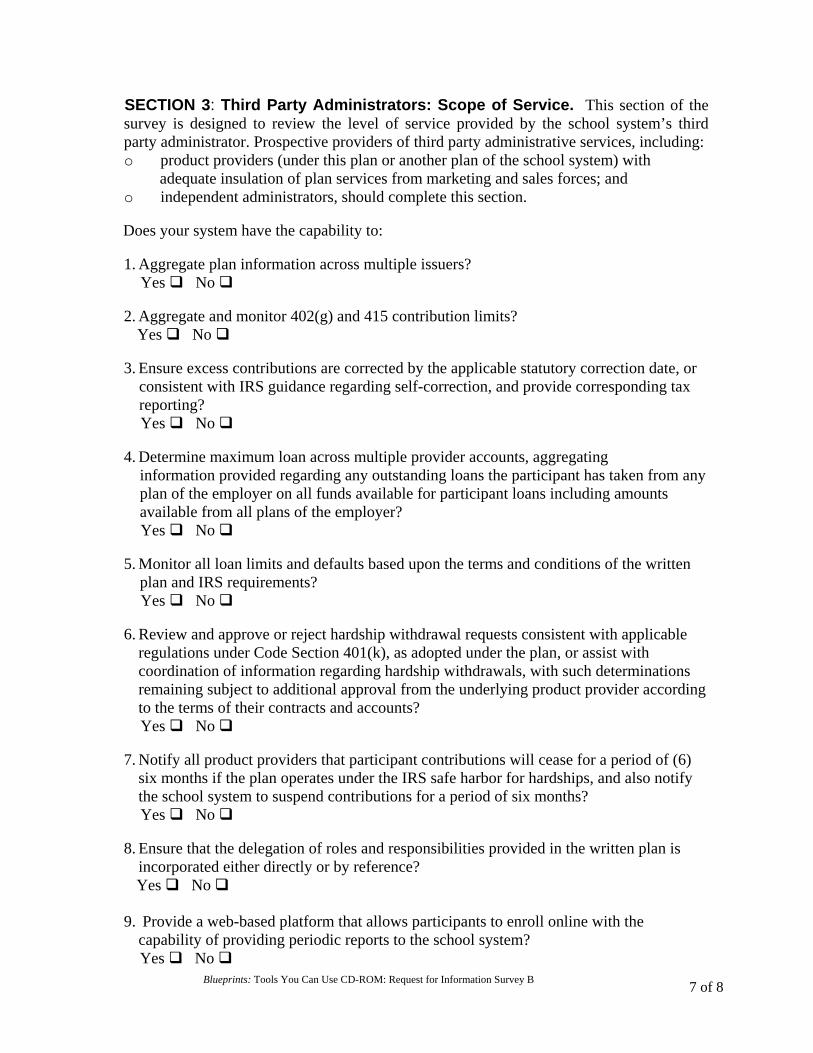

SECTION 3: Third Party Administrators: Scope of Service. This section of the survey is designed to review the level of service provided by the school system’s third party administrator. Prospective providers of third party administrative services, including: o product providers (under this plan or another plan of the school system) with adequate insulation of plan services from marketing and sales forces; and o independent administrators, should complete this section.

Does your system have the capability to:

1. Aggregate plan information across multiple issuers? Yes No

2. Aggregate and monitor 402(g) and 415 contribution limits? Yes No

3. Ensure excess contributions are corrected by the applicable statutory correction date, or

consistent with IRS guidance regarding self-correction, and provide corresponding tax reporting?

Yes No

4. Determine maximum loan across multiple provider accounts, aggregating information provided regarding any outstanding loans the participant has taken from any plan of the employer on all funds available for participant loans including amounts available from all plans of the employer? Yes No

5. Monitor all loan limits and defaults based upon the terms and conditions of the written plan and IRS requirements? Yes No

6. Review and approve or reject hardship withdrawal requests consistent with applicable

regulations under Code Section 401(k), as adopted under the plan, or assist with coordination of information regarding hardship withdrawals, with such determinations remaining subject to additional approval from the underlying product provider according to the terms of their contracts and accounts?

Yes No

7. Notify all product providers that participant contributions will cease for a period of (6) six months if the plan operates under the IRS safe harbor for hardships, and also notify the school system to suspend contributions for a period of six months?

Yes No

8. Ensure that the delegation of roles and responsibilities provided in the written plan is incorporated either directly or by reference?

Yes No 9. Provide a web-based platform that allows participants to enroll online with the

capability of providing periodic reports to the school system? Yes No

Blueprints: Tools You Can Use CD-ROM: Request for Information Survey B

8 of 8

Third Party Administrator Information: This information is provided by

_________________________________________________________________________Name Title _________________________________________________________________________Signature Date _________________________________________________________________________Telephone, Fax, Email

The undersigned officer for the organization: Certifies that the above information is correct and complete to the best of his or her knowledge and belief upon reasonable inquiry and review.

_________________________________________________________________________Name Title _________________________________________________________________________Signature Date _________________________________________________________________________Telephone, Fax, E-mail

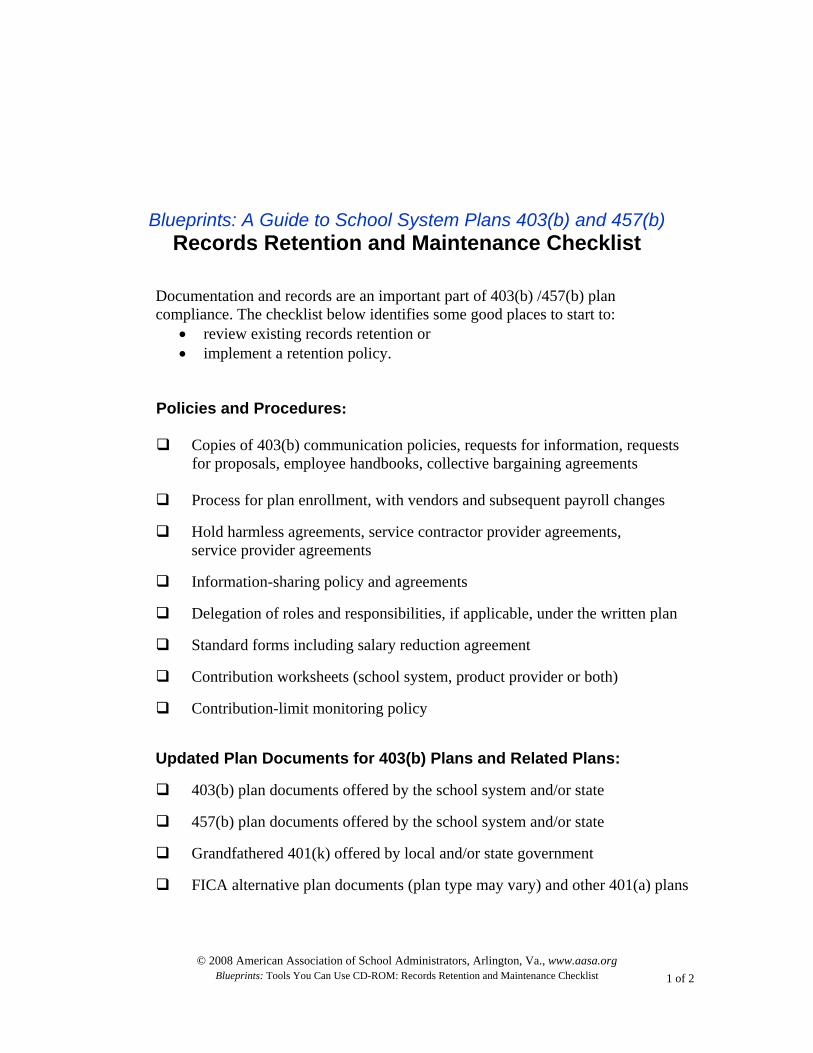

© 2008 American Association of School Administrators, Arlington, Va., www.aasa.org Blueprints: Tools You Can Use CD-ROM: Records Retention and Maintenance Checklist

1 of 2

Blueprints: A Guide to School System Plans 403(b) and 457(b) Records Retention and Maintenance Checklist

Documentation and records are an important part of 403(b) /457(b) plan compliance. The checklist below identifies some good places to start to:

• review existing records retention or • implement a retention policy.

Policies and Procedures:

Copies of 403(b) communication policies, requests for information, requests for proposals, employee handbooks, collective bargaining agreements

Process for plan enrollment, with vendors and subsequent payroll changes

Hold harmless agreements, service contractor provider agreements, service provider agreements

Information-sharing policy and agreements

Delegation of roles and responsibilities, if applicable, under the written plan

Standard forms including salary reduction agreement

Contribution worksheets (school system, product provider or both)

Contribution-limit monitoring policy

Updated Plan Documents for 403(b) Plans and Related Plans:

403(b) plan documents offered by the school system and/or state

457(b) plan documents offered by the school system and/or state

Grandfathered 401(k) offered by local and/or state government

FICA alternative plan documents (plan type may vary) and other 401(a) plans

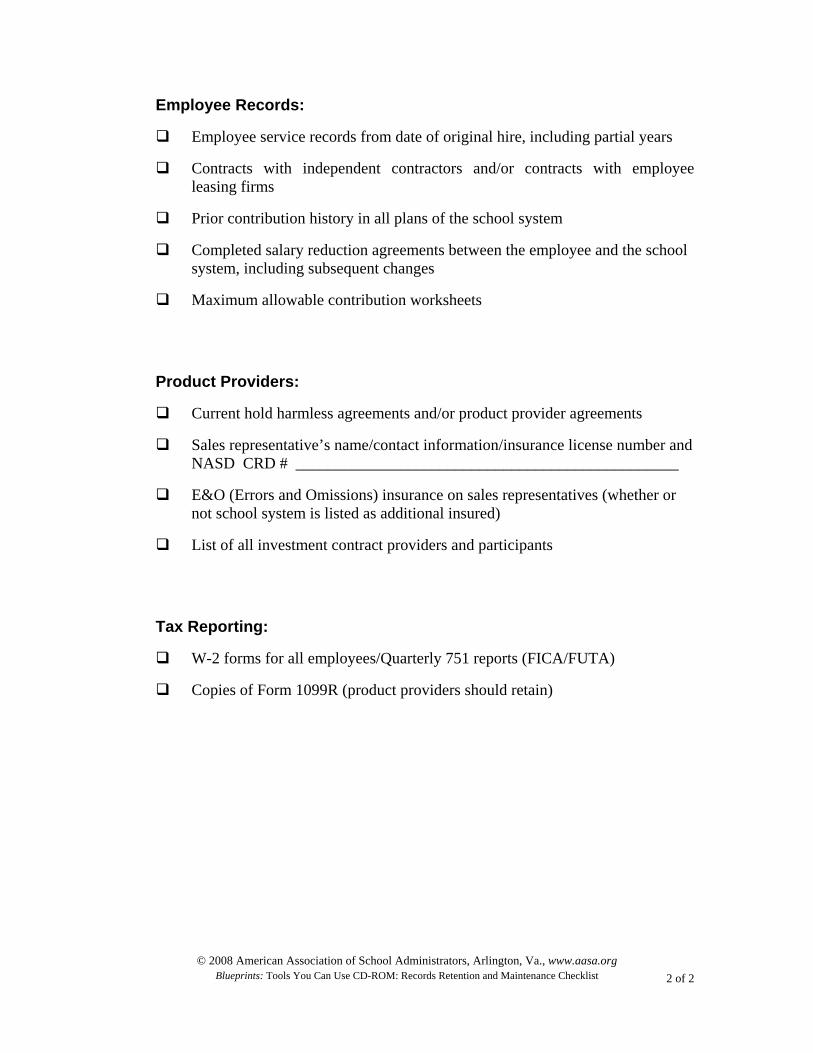

© 2008 American Association of School Administrators, Arlington, Va., www.aasa.org Blueprints: Tools You Can Use CD-ROM: Records Retention and Maintenance Checklist

2 of 2

Employee Records:

Employee service records from date of original hire, including partial years

Contracts with independent contractors and/or contracts with employee leasing firms

Prior contribution history in all plans of the school system

Completed salary reduction agreements between the employee and the school system, including subsequent changes

Maximum allowable contribution worksheets

Product Providers:

Current hold harmless agreements and/or product provider agreements

Sales representative’s name/contact information/insurance license number and NASD CRD # ________________________________________________

E&O (Errors and Omissions) insurance on sales representatives (whether or not school system is listed as additional insured)

List of all investment contract providers and participants

Tax Reporting:

W-2 forms for all employees/Quarterly 751 reports (FICA/FUTA)

Copies of Form 1099R (product providers should retain)

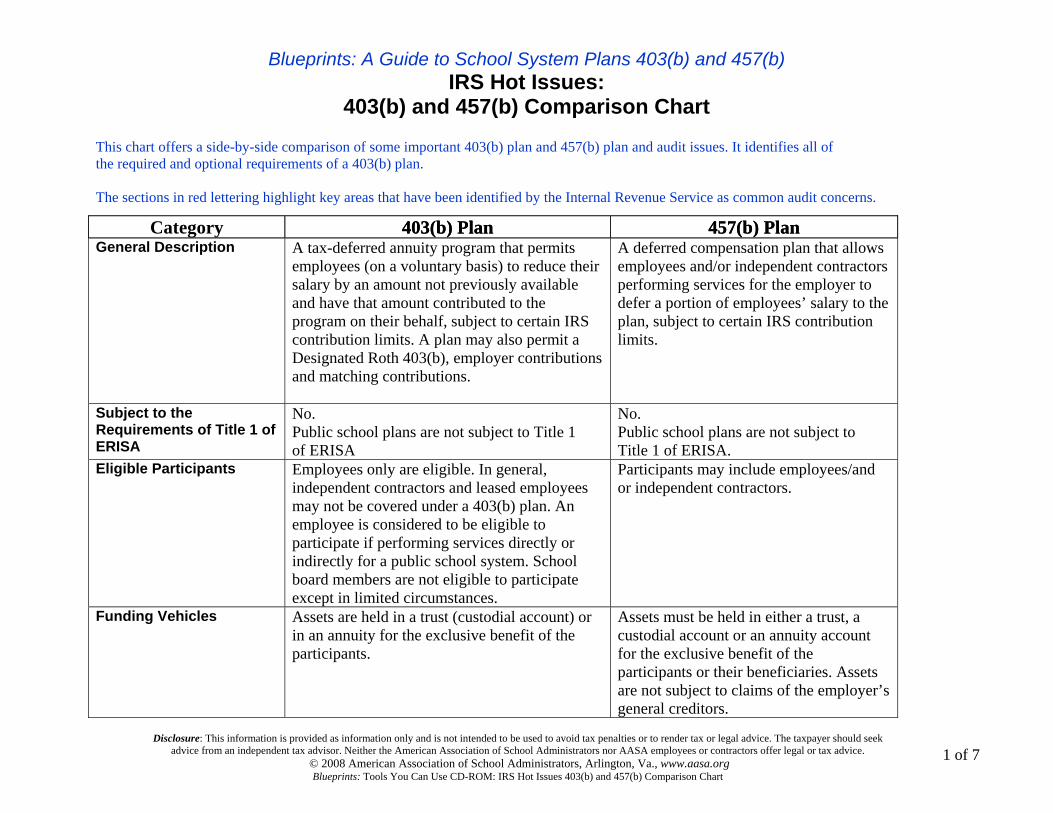

Blueprints: A Guide to School System Plans 403(b) and 457(b) IRS Hot Issues:

403(b) and 457(b) Comparison Chart

1 of 8 1 of 7Disclosure: This information is provided as information only and is not intended to be used to avoid tax penalties or to render tax or legal advice. The taxpayer should seek

advice from an independent tax advisor. Neither the American Association of School Administrators nor AASA employees or contractors offer legal or tax advice. © 2008 American Association of School Administrators, Arlington, Va., www.aasa.org

Blueprints: Tools You Can Use CD-ROM: IRS Hot Issues 403(b) and 457(b) Comparison Chart

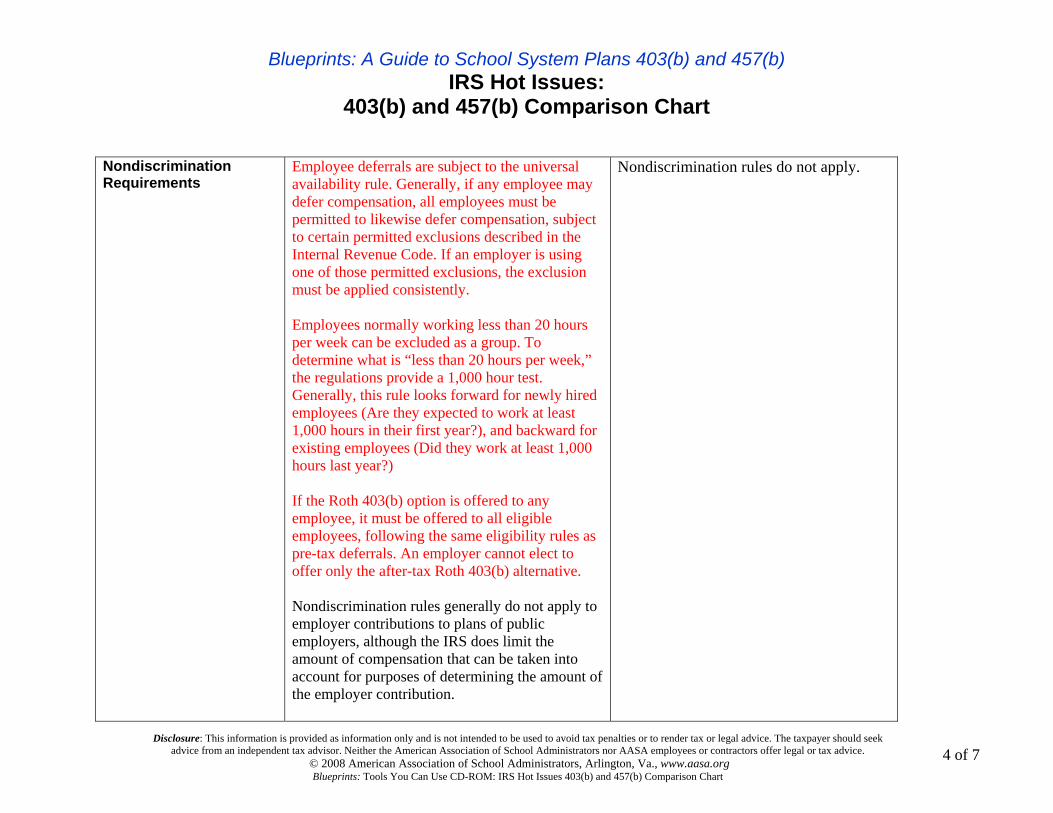

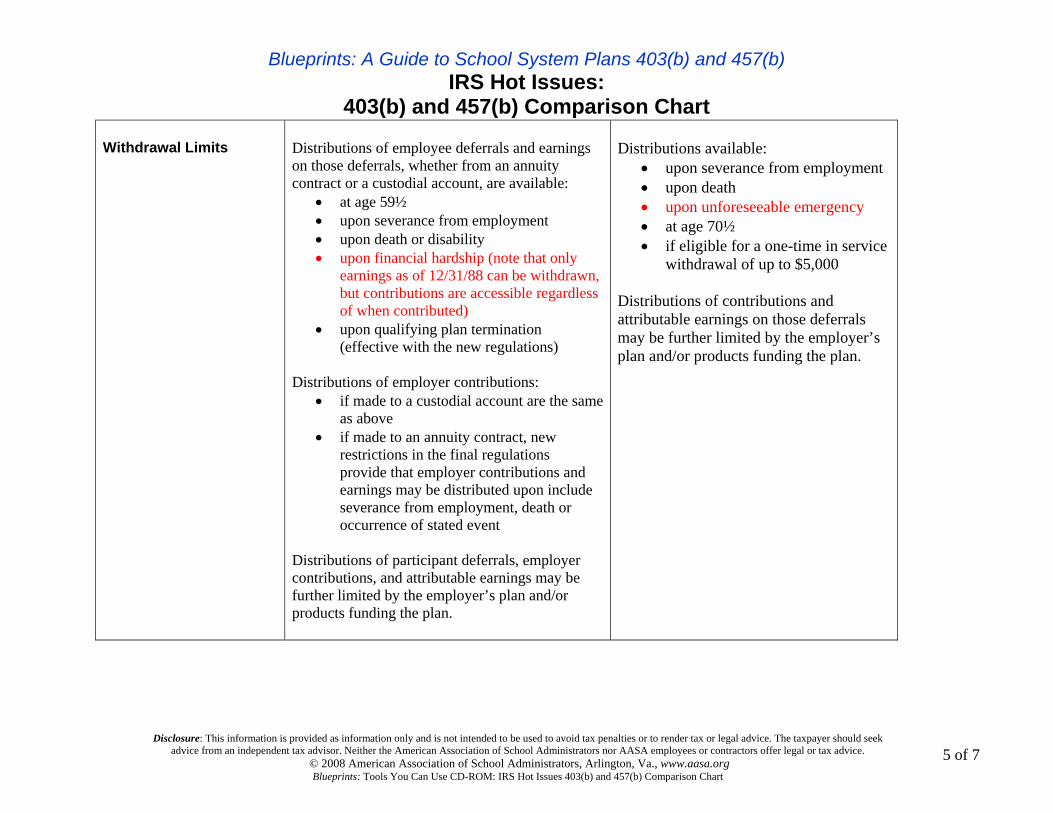

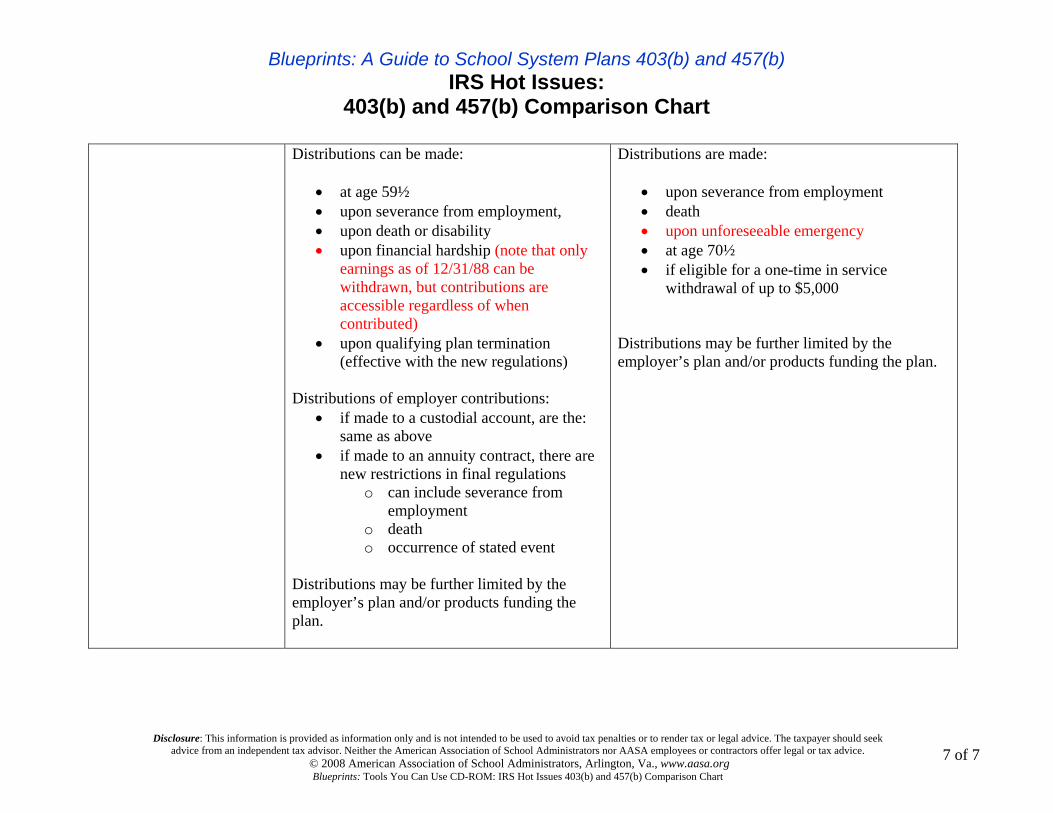

This chart offers a side-by-side comparison of some important 403(b) plan and 457(b) plan and audit issues. It identifies all of the required and optional requirements of a 403(b) plan. The sections in red lettering highlight key areas that have been identified by the Internal Revenue Service as common audit concerns.

Category 403(b) Plan 457(b) Plan

General Description A tax-deferred annuity program that permits employees (on a voluntary basis) to reduce their salary by an amount not previously available and have that amount contributed to the program on their behalf, subject to certain IRS contribution limits. A plan may also permit a Designated Roth 403(b), employer contributions and matching contributions.

A deferred compensation plan that allows employees and/or independent contractors performing services for the employer to defer a portion of employees’ salary to the plan, subject to certain IRS contribution limits.

Subject to the Requirements of Title 1 of ERISA

No. Public school plans are not subject to Title 1 of ERISA

No. Public school plans are not subject to Title 1 of ERISA.

Eligible Participants Employees only are eligible. In general, independent contractors and leased employees may not be covered under a 403(b) plan. An employee is considered to be eligible to participate if performing services directly or indirectly for a public school system. School board members are not eligible to participate except in limited circumstances.

Participants may include employees/and or independent contractors.

Funding Vehicles Assets are held in a trust (custodial account) or in an annuity for the exclusive benefit of the participants.

Assets must be held in either a trust, a custodial account or an annuity account for the exclusive benefit of the participants or their beneficiaries. Assets are not subject to claims of the employer’s general creditors.

403(b) Plan 457(b) Plan

Blueprints: A Guide to School System Plans 403(b) and 457(b) IRS Hot Issues:

403(b) and 457(b) Comparison Chart

2 of 8 2 of 7Disclosure: This information is provided as information only and is not intended to be used to avoid tax penalties or to render tax or legal advice. The taxpayer should seek

advice from an independent tax advisor. Neither the American Association of School Administrators nor AASA employees or contractors offer legal or tax advice. © 2008 American Association of School Administrators, Arlington, Va., www.aasa.org

Blueprints: Tools You Can Use CD-ROM: IRS Hot Issues 403(b) and 457(b) Comparison Chart

Contribution Limits

Employee voluntary deferrals are limited to an elective deferral limit under Code Section 402(g) (2007 and 2008: $15,500); subject to annual cost- of-living adjustments). An increase is available for employees with at least 15 years of service with the employer, provided that other requirements are satisfied. The maximum increase is $3,000 per year and $15,000 over a lifetime. The total of employee voluntary deferrals, non-elective employee contributions, and employer contributions is limited to dollar and percentage limits under Code Section 415(c):

• 100% of participant compensation up to

• $45,000 (2007) and $46,000 (2008) (subject to annual cost-of-living adjustments)

Age 50 catch-up provisions:

For an employee age 50 and older, once the employee has reached these contribution limits, he can contribute up to an additional $5,000 per year (in 2007 and 2008), subject to annual cost-of-living adjustments. This contribution does not count toward either the 402(g) or 415(c) contribution limit.

Total of employer and employee contributions is limited to 100% of includible compensation to $15,500 (for 2007 and 2008): subject to annual cost-of-living adjustment. An employee within 3 years of the year in which he reaches Normal Retirement Age, as defined in the 457 plan document, may be eligible to contribute a total of up to twice the basic limit. Use of this catch-up is limited to the amount of unused contributions in prior years that the 457(b) plan was available. For an employee age 50 and older, once the employee has reached these contribution limits, he can contribute up to an additional $5,000 per year (in 2007 and 2008), subject to annual cost-of-living adjustments, or the amount of the employee’s deferrals, whichever is less. An employee who is eligible for both the 457 special catch-up and the age 50+ catch-up in a 457(b) plan may only use the catch-up that yields the greatest amount.

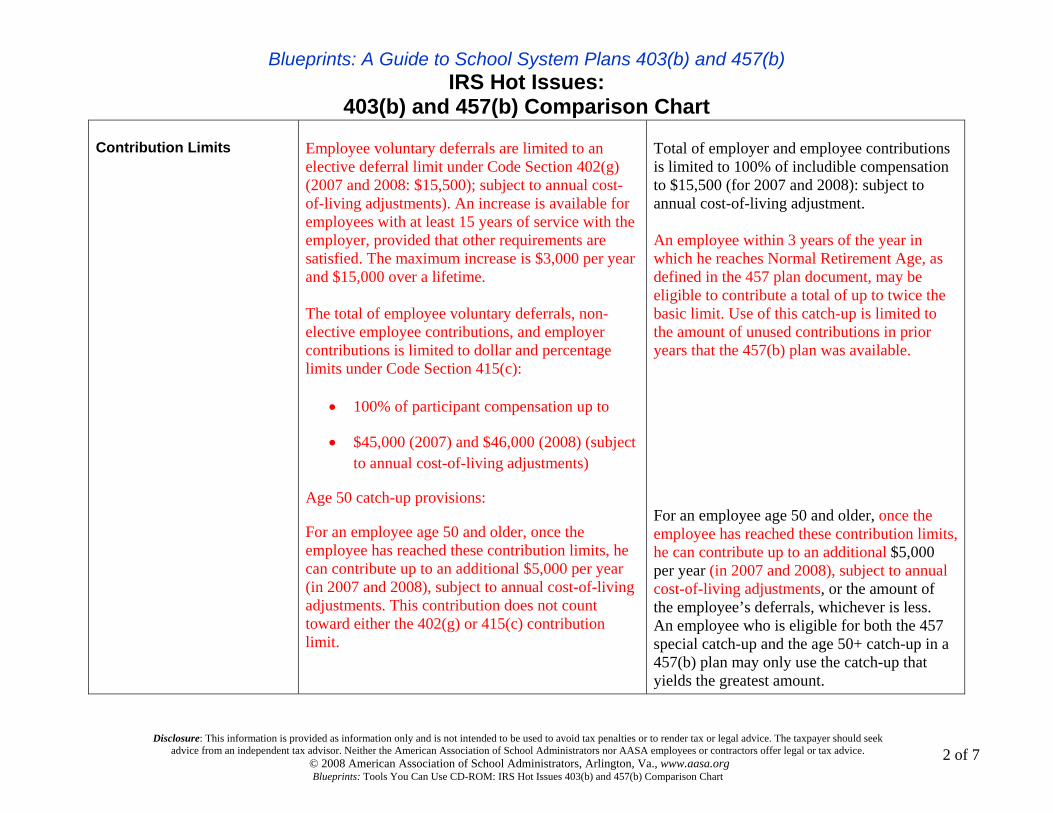

Blueprints: A Guide to School System Plans 403(b) and 457(b) IRS Hot Issues:

403(b) and 457(b) Comparison Chart

3 of 8 3 of 7Disclosure: This information is provided as information only and is not intended to be used to avoid tax penalties or to render tax or legal advice. The taxpayer should seek

advice from an independent tax advisor. Neither the American Association of School Administrators nor AASA employees or contractors offer legal or tax advice. © 2008 American Association of School Administrators, Arlington, Va., www.aasa.org

Blueprints: Tools You Can Use CD-ROM: IRS Hot Issues 403(b) and 457(b) Comparison Chart

Contribution Limits

General Rule: The annual total of employee deferrals (other than the age 50+ catch-up contribution), Roth 403(b), and any employer contributions cannot exceed the lesser of:

1. The section 415(c) limit on annual additions is, generally, the lesser amount of 100% includible compensation” up to $45,000 (2007) or $46,000 (2008) (subject to annual cost-of- living adjustments).

2. Section 402(g) limit on salary reduction contributions ($15,500 for 2007 and 2008, subject to annual cost-of-living adjustments). This limit takes into consideration all employee elective deferrals and Roth 403(b) contributions (other than the age 50+ catch-up contribution) of an individual.

In the special catch–up provision for employees who have completed at least 15 years of service with their current school employer, the annual deferral is increased by the lesser of:

o $3,000

o $15,000, reduced by amounts not included in gross income for prior years due to the catch-up election

o $5,000 times years of service with the employer, minus all amounts of prior years’ contributions attributable to elective deferrals made to the current employer’s plans

General Rule: Deferrals, including salary reduction contributions (other than the age 50+ catch-up contribution) and any employer contribution, cannot exceed the lesser of $15,500 (for 2007 and 2008) or 100 % of includible compensation. Subsequent annual cost-of-living adjustments are made in $500 increments The special catch-up provision may, generally, defer up to twice the general deferral limit for the three-year period prior to the year in which the participant attains the elected normal retirement age under the plan. In the age 50-and-over catch-up provision, participants who are at least age 50 may make an additional $5,000 (for 2007 and 2008) annual contributions. Subsequent annual cost-of-living adjustments are made in $500 increments. A participant is not allowed to use the special catch-up and the 50-and-over catch-up in the same year.

Blueprints: A Guide to School System Plans 403(b) and 457(b) IRS Hot Issues:

403(b) and 457(b) Comparison Chart

4 of 8 4 of 7Disclosure: This information is provided as information only and is not intended to be used to avoid tax penalties or to render tax or legal advice. The taxpayer should seek

advice from an independent tax advisor. Neither the American Association of School Administrators nor AASA employees or contractors offer legal or tax advice. © 2008 American Association of School Administrators, Arlington, Va., www.aasa.org

Blueprints: Tools You Can Use CD-ROM: IRS Hot Issues 403(b) and 457(b) Comparison Chart

Nondiscrimination Requirements