dawn of the new decade - huon aquaculture

TRANSCRIPT

ANNUAL REPORT 2020HUON AQUACULTURE GROUP LIMITED

THE NEW DECADEDAWN OF

Contents02 Chairman’s and

Managing Director’s Review04 Review of operations10 Operating in unique environments12 Huon investment and innovation14 The Ronja Storm16 The outlook for the salmon market17 Huon’s approach to marketing18 Risk Management and Sustainability22 Financial Summary26 Board of Directors29 Directors’ Report46 Auditor’s Independence Declaration47 Corporate Governance Statement53 Financial Statements59 Notes to the Financial Statements102 Director’s Declaration103 Independent Auditor’s Report110 Shareholder Information112 Glossary of Terms114 Corporate Directory

Annual General Meeting 2020The Annual General Meeting of Huon Aquaculture Group Limited will be held online as a Virtual AGM on 30 October 2020. Details on how to participate will be included in the Notice of Meeting.

AFTER FIVE YEARS OF INVESTMENT AND INNOVATION

HUON AQUACULTURE IS READY TO DOUBLE ITS

PRODUCTION

1

Dear shareholder,This has been a milestone year in relation to Huon’s successful completion of a major capital investment program, finalising one of the business’ core strategic components of growing production capacity safely and sustainably. It also addressed key agriculture and climate risks associated with growing salmon in Australia, increasing our resilience to factors over which we have limited control. However the impacts on the business arising from a global pandemic have presented a unique set of challenges that Huon is not alone in having to manage.

Up until the end of March 2020, Huon had achieved its objective of making up the ground lost due to the setbacks in production from biological and weather events in FY2018 and FY2019. Biomass levels were back to where they would have been, had these setbacks not occurred and we were confident of exceeding our base-line harvest forecast for the year of 25,000 tonnes.

While Huon continued to operate through the most restrictive lockdown periods over the two months to the end of May, the closure of restaurants, clubs and the food catering industry more generally, virtually closed the food services sector in Australia during that period. While sales through retail channels were strong, Huon’s high exposure to the valuable food service channel meant that a significant drop in volumes in its wholesale market, accompanied by lower prices, was unavoidable. Access to export markets has also been interrupted since late March due to the disruption to international air freight services. Despite the disruptions during Q4, Huon achieved guidance volume with a 25,566 tonne harvest for FY2020. The strong performance of the 19 Year Class salmon, and some delay of the harvest in Q4, has the positive benefit of increasing our original expectations for the FY2021 harvest. It is now expected to be around 20% above the base line forecast of 30,000 tonnes, which will be a record for Huon.

Business performanceThe performance of Huon’s farming operations in FY2020 was the best for many years as good growing conditions, combined with increased productivity from the infrastructure, delivered through the investment program, produced better than expected fish performance. However, legacy issues in the first quarter of the financial year from the jellyfish issues in November and hot summer in 2018, continued to impact the growth of the 18 Year Class fish. This resulted in lower tonnages and weaker prices for the harvest in that period. In the final four months of FY2020 the harvest had to be slowed significantly due to the closure of many of our channels to market as a result of the COVID-19 pandemic.

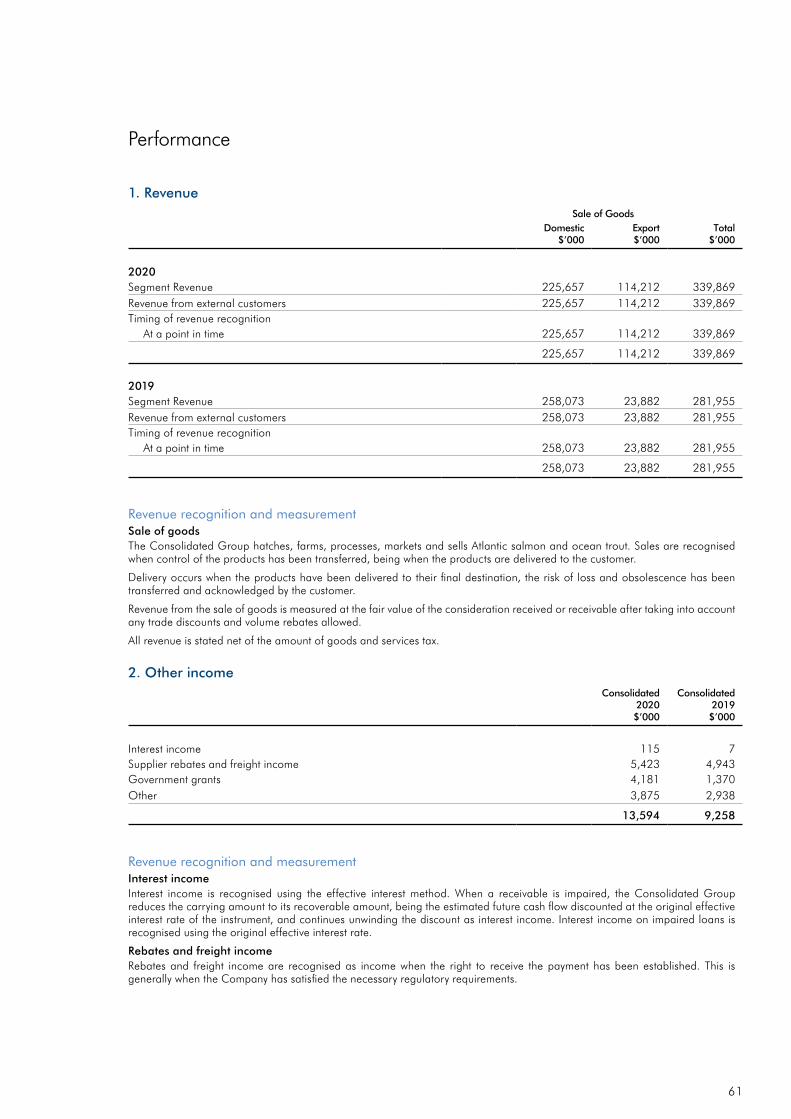

Huon delivered revenues of $339.9 million, an increase of 21% on the previous year, largely due to the 36% increase in harvest volumes from 18,849 tonnes to 25,566 tonnes. Revenues were impacted by an average 11% fall in salmon prices to $13.30/HOG kg due to the increased volumes sold through the lower priced export market and lower domestic wholesale pricing in the second half.

Huon’s statutory net result after tax (NPAT) recorded a profit of $4.9 million, down from $9.5 million in FY2019. This included a $1.5 million increase in the Fair Value Adjustment (FVA) due to the growth in biological assets over the year. The lower pricing environment resulted in a 14% fall in Operating EBITDA from $47.3 million to $40.8 million (pre AASB 16).

The increase in the FVA reflects the 28% increase in the overall fair value of biological assets during FY2020 from $209.1 million to $262.8 million (pre AASB 16) as Huon has focused on rebuilding and expanding its biomass. Following the strong performance of the 19 Year Class salmon, with high survival rates and improved feed conversion, the June biomass levels were higher than expected, but with easing average prices, the fair value did not represent the increased biomass holding. The June biomass levels will underpin the substantial increase in the harvest to at least 36,000 tonnes in FY2021.

The level of investment required to expand our business to take advantage of the continued growth in domestic demand for salmon and to develop new markets overseas, has seen net debt rise from $138.8 million to $167.3 million with gearing sitting at 53% (pre AASB 16).

Chairman’s and Managing Director’s Review

NEIL KEARNEY Chairman

PETER BENDER Managing Director and Chief Executive Officer

Following five years of investment and innovation Huon is set to double its harvest tonnage…

Huon Aquaculture Group Limited

Annual Report 2020

2

StrategyHuon’s growth has been guided by its commitment to an overarching business strategy based on three key requirements; – growing the market; – increasing production and enhancing operational

efficiency; and – operating safely and sustainably.

From 2014 to 2019 significant focus was placed on ensuring that the infrastructure was in place to enable Huon to increase production and operate efficiently.

This required a major investment in upgrading our systems and technology to a standard that is unquestionably world class. We have encouraged innovation and designed new approaches to the way we farm that has enabled us to build additional layers of efficiency and resilience into our business that will stand us in good stead over the long term. The arrival in Hobart of the wellboat Ronja Storm in February 2020, marked the completion of Huon’s infrastructure program which has been the central platform of its five year strategy to grow the business. As a result Huon’s harvest capacity has at least doubled to more than 40,000 tonnes.

The strategic focus over the past year has been to concentrate on ensuring that the new infrastructure is operating in line with expectations, including the delivery of improved productivity. At the same time we have been accelerating our push to develop new markets offshore to take up the increased volume that is now in production. There is strong demand in these markets for access to a reliable, high quality and guaranteed supply of product and Huon is now in a position to meet that demand.

The spread of the COVID-19 pandemic across the globe since February 2020 put a halt to the momentum that had been building in the business to grow the market both domestically and through Asia. While it remains our most important strategic priority, the pace with which we are able to pursue this will be determined by the extent to which the pandemic continues to depress global economies and their ability to recover.

Capital ManagementIn FY2018 Huon committed to funding the expansion stage of its investment in infrastructure through existing borrowing facilities and cash flow. Reduced revenue in both FY2019 and FY2020, first due to the impacts arising from contact with jellyfish and a hot summer and then COVID-19, resulted in net debt running at a higher level during FY2020 than originally budgeted. In order to conserve cash flow for the increased operational requirements of the business, the board has suspended the payment of dividends for FY2020.

Capital expenditure was already planned to moderate beyond FY2019 as the business moved into a phase of bedding down the significant investments made over the previous two years. The primary focus in FY2020 was on extracting the production efficiencies that are a significant part of that process. Capital expenditure was $21.6 million which is below the previous estimate of $25-30 million in annual maintenance capex for the business.

This focus on debt reduction will remain a key priority in FY2021 including a continued focus on costs within the business as well as an extension of the dividend suspension.

PeopleThe wellbeing of our people is of paramount importance at Huon and our investment in developing protocols and procedures to protect our employees provided a strong framework for managing the health risks associated with COVID-19. The business was permitted to operate ‘as normal’ with modified policies and procedures to contain any potential outbreaks of the virus within the business. At the end of June, there had been no disruptions to the ongoing operations of the business.

Huon continued to focus on updating and developing its health and safety programs within the business which helped manage the growing workforce, however overall safety performance measures declined slightly during FY2020.

ConclusionThe last two years have presented some significant challenges to the business whether from the secondary impact of lost growth and increased mortalities from the jellyfish and hot summer encounter through to the temporary closure of markets and significant impact of the current COVID-19 pandemic.

While Huon’s underlying business strategy is unaffected by these events, a number of the operational benefits that we expected would be delivered following the completion of our significant investment program in 2019 have now been delayed until FY2022. As the global economy contemplates recession, it would be unrealistic to expect that our business will not be affected by the ongoing changes we have already witnessed in consumer behaviour and our access to traditional channels to market.

Your board is, however, confident that the investments made in recent years will support the growth of the business over the long term. A strong foundation has been put in place that will not only enable Huon to increase the production of salmon through its high energy sites but that it will do so sustainably. As Huon expands its production further next year it will continue to drive down operating costs per HOG kg, setting the business up to generate the growth in revenue, earnings and shareholder returns that we know it to be capable of once the current period of economic uncertainty ends.

On behalf of the Board I wish to extend our appreciation to all Huon employees for their efforts and commitment shown during the current pandemic. Our thanks also go to our customers, suppliers, local communities, and our shareholders for their support over the past year.

Neil Kearney Chairman

Peter Bender Managing Director and Chief Executive Officer

3

Operating overviewHuon Aquaculture’s financial performance in FY2020 was affected by the significant disruption of two of its main channels to market, wholesale and export, as a number of measures were implemented by the state and federal governments to contain the spread of the COVID-19 in 2H2020. Up to this point, the business was on track to achieving a strong uplift in revenue, underpinned by the favourable growing season over summer and the exceptional performance of the 19 Year Class salmon, as a result of the structural improvements that had been made over the previous two years.

Huon began FY2020 with a reduction in sales through the retail channel due to the completion of a three year contract to supply salmon to a major supermarket chain at the end of June 2019. In addition it was faced with continued poor fish growth in the 18 Year Class and harvest weights being slow to recover from the effects of gill necrosis which had developed as a consequence of the jellyfish bloom at the end of 2018. This resulted in low sales volumes in the first quarter as the business predominantly had small fish to sell, reducing its competitiveness in the wholesale market. It also meant export sales were difficult, particularly in the China market where there is a preference for larger fish.

Growth rates picked up in spring with fish size being more competitive in the wholesale market and more acceptable for export markets, allowing harvest rates to increase through the second quarter. The recovery of harvest size drove volume increases into the export channel which coincided with a sharp drop in international pricing, the lowest since 2015, due to Norway and Chile unexpectedly increasing their harvest levels for a short period. With exports accounting for 28% of revenue, the fall in spot export prices in the second and fourth quarters was the main contributor to the 11% drop in the weighted average sales price for FY2020.

The increased availability of fish together with larger fish size both support Huon’s commitment to focus on providing a reliable source of supply to our key markets both domestically and offshore. As contracted sales in international markets increase, there will be less exposure to the more volatile pricing environment of the spot export market.

In the retail channel, Huon made strong, direct gains during the year with fresh salmon sales up 48% as a result of new supply agreements and increased focus on customer development.

Performance improvementThere is however another story that sits behind these numbers. It is one that reflects the gains that have been made over the past year in lifting operating performance by changing the way Huon farms salmon.

The average fish harvest weight for the year was 5.04kg, the best in a decade and well above the average over that period of 4.53kg.

The 19 Year Class salmon is the first to benefit from the suite of changes that have been put in place along the length of the entire production chain – from the hatcheries to the Whale Point Salmon Nursery; the increased security provided by the fortress pens and more efficient bathing with custom designed wellboats; centrally controlled feeding from purpose built barges; and the POMV vaccine and new biosecurity protocols that put fish in the right farming areas at the right time to minimise the biological risk.

East of Yellow BluffHuon was granted an Environmental Licence for a new lease at Storm Bay, in the area known as East of Yellow Bluff, in May 2019. The new lease site, 1.5 kilometres from Bruny Island, is a key addition to the region as it enables Huon to deliver improved biosecurity in Storm Bay by including better separation of year classes of fish and is one of the key components of the industry biosecurity plan. Having fish in the right farming areas at the right time minimises the biological risk, including jellyfish mitigation, and at the same time provides efficiencies in the management of the biological stock.

The new lease has played a key role in the expansion of capacity at Storm Bay to 13,500 tonnes. In combination with Huon’s hatcheries, wellboat and growout facility it also maximises throughput options, lifting Huon’s total production capacity from 36,500 tonnes to more than 40,000 tonnes.

Whale Point Salmon NurseryThis new growout facility at Whale Point started operating at the beginning of 2019. In its first year it has enabled Huon to grow smolt to a larger size before putting them to sea – the 19 Year Class average size when released was 20% higher at 282 grams across all of our hatcheries. Fish transferred to sea in May 2019 were harvested in April 2020 at 4.6 HOG kg and represented the first Year Class to be produced from hatchery to harvest under Huon’s upgraded infrastructure and expanded capacity.

Review of operations

Huon Aquaculture Group Limited

Annual Report 2020

4

The final piece of infrastructure was commissioned in 2H2020, the transfer pipe, taking fish directly from the nursery to the wellboat. This transfer method eliminates the use of truck transfers, and improves fish health and performance following the transfer from freshwater to seawater, as the fish are less stressed.

Ronja StormIn February 2020 the wellboat Ronja Storm arrived in Tasmania. It is the most advanced fish bathing and transportation vessel in the world, and represents the completion of Huon’s two year strategy to invest in growth infrastructure. The vessel is designed to achieve increased production capacity and do so more efficiently. The Ronja Storm includes technical advancements including on board freshwater production, disinfection and oxygen generation. The large size is designed to facilitate bathing of Huon’s existing 240m pens in one load to ensure freshwater bathing is efficient and low stress on fish. An important operational benefit from the increased efficiency of this vessel is that the number of baths required by each pen will reduce over the fish lifecycle, as a consequence of not needing to pre-emptively bath them ahead of when required. An on-board grader will allow progressive harvesting in the latter stages of the fish lifecycle. By progressively harvesting a specific fish size, more fish per pen are expected to be grown without impacting Huon’s existing low stocking density.

Second 600T Feed Barge Huon’s second 600 tonne feed barge Hulk was launched in May. Constructed over the last two years the barge represents the completion of the sustainable fish feeding systems. Located in the high-energy sites at Storm Bay, the new barge has been designed to ensure that the fish can be fed in any weather, allowing them to fully realise their growth potential. The barge is fully automated and remotely controlled from the Hobart feed control room using cutting-edge video pellet-recognition software, meaning less feed wastage and a reduced environmental impact.

Selective breeding and POMV vaccineThe expansion in Huon’s production capacity carried with it a recognition it needed to increase access to the output from Tasmania’s industry-owned Selective Breeding Program. As a result Huon invested $2.5 million into the program which is run out of the Saltas hatchery. This takes Huon’s share of the biological output from

Saltas to 50% from 21%. Recent technological advances introduced at Saltas should see step change improvements in the future biological output from the program. With larger populations going to sea and recent technological advances at the hatchery, this move has ensured that Huon will maintain its ability to receive maximum benefit from the breeding program which is aimed at developing fish suited to the Tasmanian environment and to combat Amoebic Gill Disease (AGD). The broodstock from the Saltas hatchery are used in Huon’s other hatcheries.

This year the industry also implemented a trial vaccine for POMV. The vaccine, developed with support from government and industry, has proved extremely beneficial with no vaccinated pens coming down with POMV. All smolt going to sea in 2020 are being vaccinated with the new vaccine.

All these measures are part of an ongoing research effort that has at its core mitigating the impact of climate change on the future potential of the Tasmanian salmon industry, particularly through varying sea water temperatures. It has also been the underlying driver of Huon’s decision to move its growth in production offshore, positioning its marine leases in high energy sites where it is less likely fish will be impacted by this climate trend.

Expanding capacityFollowing the completion of Huon’s two year program of investing in infrastructure to drive the expansion of its production capacity, FY2020 heralded the beginning of that new growth phase.

During the first six months the biomass was rebuilt with the objective of returning production levels back to where they would have been if not for the biological and weather events encountered in the previous two years. The target for FY2020 was for a harvest of at least 25,000 tonnes with fish in production to support an increase in tonnage to over 30,000 tonnes in FY2021.

The strong performance of the 19 Year Class salmon reflects the investment in infrastructure, and biological improvements Huon has made, and we have increased our original outlook for FY2021 to at least 36,000 tonnes.

The increased volume of salmon available for sale in FY2020 and beyond enables Huon to meet the steady growth in demand in the domestic market at the same time as developing new markets in the Asian region. Growing the market, one of Huon’s three strategic pillars, is therefore where its primary focus will be in the years ahead.

5

Growing the marketHuon has been developing close relationships with a range of distributors and retail clients throughout Asia over the past 5 years, something that will assume greater importance now that its increased production capacity enables it to guarantee supply to this growing market. With a third of sales going offshore over FY2020, strong headway was made during the year into the contracted international retail space with volumes up 226% on the previous corresponding period (pcp). Importantly supply went into multiple outlets, reducing Huon’s reliance on any one customer. Even during the COVID disrupted second half, volumes to this segment rose 258% on pcp. In total, just over 6% of export revenue came from contracted volume in Asia.

The domestic retail channel accounted for 4,421 tonnes in FY2020 or 19% of sales compared to 5,510 tonnes (28% of sales) the previous year, following the completion of a large 3-year MAP contract in FY2019. Excluding this contract, Huon made strong, direct gains in the retail segment with salmon sales up 110% as a result of new supply agreements and increased focus on customer development. Good progress was also made in establishing a larger Ocean Trout retail market with fresh deli, branded MAP and branded smoked products now in distribution across major retail outlets.

At the beginning of FY2020 Huon’s branded points of distribution doubled to around 2,700 retail outlets around Australia, placing the Huon brand in its strongest position since listing. It underscores the importance of the Ingleburn processing and distribution facility in NSW in developing direct relationships with a range of food retailers as well as the major supermarket chains.

Huon expects to continue to expand branded distribution in all product segments both domestically and internationally over FY2021, following a strong year of distribution growth in FY2020. This will be supported by a significant above the line investment in marketing at the end of the first half to drive Huon Salmon consumption domestically. This investment will increase salmon’s share of voice in the protein market where there is significant underlying demand ready to be unlocked. Previous spends of this nature domestically have driven single year, double digit volume growth whilst maintaining price.

Rebuilding and growing supply through the retail channel is a key focus of Huon’s strategy to grow the market and will remain a focus for FY2021.

The domestic wholesale market remains a very important sales channel for Huon, accounting for 47% of sales in FY2020. This market was significantly disrupted in the last quarter of the year with volumes down 19% in the second half on pcp. Huon responded with discount pricing and marketing efforts to help stimulate demand for wholesale partners, focussing on volume through fresh fish shops, independent retailers, quick service restaurant outlets and e-commerce businesses.

Salmon pricesPrices in the domestic market remained strong in the first half with the wholesale channel continuing to record prices above $15.00/HOG kg and just under $14.50/HOG kg in the retail market. The situation changed abruptly in the second half as the pandemic took hold with prices falling by 9% across the wholesale domestic market. Compared to the record prices received the previous year ($15.63/kg) in the wholesale market, Huon averaged $14.71/kg in FY2020 while retail prices rose from $14.25/kg in FY2019 to an average $14.91/kg.

International salmon prices have been volatile during FY2020, despite a general acknowledgment that global demand continues to outstrip supply. During the first six months the world’s two largest salmon producing countries, Norway and Chile, increased their harvest levels over a three month period resulting in a sharp drop in international pricing to an average 47.6 NOK/kg, the lowest level since 2015. Huon’s harvest program was coincidentally set to sell record tonnages into the export market at this time. By December 2019 prices had bounced back to 71 NOK/kg however the timing of Huon’s export activities meant that it received an average export price in the first half of A$10.44/kg.

While the pandemic softened pricing during April and May, the average Fish Pool salmon price over the six months to June was 64 NOK/kg. This is consistent with long term forecasts by Rabobank that the salmon price from 2019 to 2021 would average 62-63 NOK/kg due to supply constraints affecting the major producing countries. Nevertheless a weaker Australian dollar during March and April resulted in Huon’s average export price in the second half only increasing to A$10.92/kg.

The progress achieved during FY2020 in growing sales into the contracted international retail space reduces Huon’s exposure to the volatile pricing of the spot export market. Over the year the average price on sales into this segment was A$13.46/kg.

Review of operations

FY2020 Channel mix% of total revenue

Wholesale 47% (64%) Retail: Domestic 19% (28%) Retail: International 6% (2%) Export 28% (6%)

FY20FY20

FY19

Huon Aquaculture Group Limited

Annual Report 2020

6

COVID-19On March 11, 2020 the World Health Organisation officially declared the global spread of the novel coronavirus (COVID-19), a pandemic. From that time a number of measures were implemented by the state and federal governments in Australia to contain the spread of the virus. This included the closure of Tasmania’s border to non-residents on 21 March and the implementation of a stage 3 lockdown across Australia from 30 March. International travel bans were also put in place from 24 March which had the immediate impact of restricting access to flights carrying freight as the major airlines progressively grounded their fleets.

Huon adhered to government guidelines and was permitted to continue all operations ‘as normal’, albeit with modified policies and procedures to contain any potential outbreaks of COVID-19 within the business. There were no disruptions to the ongoing operations of the business. The Company applied for the Australian Government Scheme ‘Jobkeeper’ and commenced receiving grants under the scheme in May.

During April and May the impact of the lockdown, in particular the closure of restaurants, clubs and the food catering industry more generally, virtually closed the food services sector in Australia. While sales through retail channels were strong, Huon experienced a significant drop in sales in its wholesale market during April and May due to its high exposure to the food service channel. Access to export markets was interrupted from late March due to the disruption to international air freight services.

The disruption to the international and domestic markets had a material impact on the second half results. The increased fish size and volumes available for harvest in Q4, with the commencement of the 19 Year Class harvest, should have delivered high returns. Following the outbreak of the pandemic, international prices that lifted in December and January entered another period of volatility. Huon’s strong position in supplying the food services sector was a disadvantage in the domestic market as consumers moved their purchases into retail.

Huon’s supply into domestic retail and retail fish shops increased, along with e-commerce channels, but this did not compensate for the loss of food services volume.

The increased consumer activity in these markets is however expected to deliver long term benefits through increased per capita consumption with more consumers now familiar with salmon as a weekly family menu item.

People and Safety

Safety and WellbeingA number of significant wellbeing programs were implemented during the financial year. These programs not only focused on reducing the risk of worker injury, but also on proactive initiatives to increase physical, emotional and financial wellbeing. These included Mental Health First Aid, individual briefings with superannuation experts and health checks.

A focus on injury management processes saw a reduction in the number and severity of Worker’s Compensation claims. However, increased lost time in injuries resulted a small increase in the LTIFR, despite a significant increase in production.

A major achievement was the development and implementation of individual Safety Management Systems for every vessel in Huon’s fleet and implementation of a business-wide chemical management system.

The business continued its focus on embedding ISO45001 – Standard for Work Health and Safety Management Systems, including the development of policy and procedures to manage any high-risk activity across the business. The proactive implementation of these Standards are an ongoing focus for the business aimed at not only reducing risks but also improving the wellbeing of Huon’s workforce and supporting people and leaders to manage safety effectively.

Developing People, Culture and LeadershipHuon’s Workforce Development Strategy continued to be implemented with employee capability development and the employee experience remaining a key focus. The Huon Leaders Program in 2019 which assisted Huon in building resilient leaders has been further supported by the introduction of the Welcome to Leadership Mentoring Program 2020. This supports newly promoted employees transition into their first Leadership role.

There continues to be a strong focus on growing the skill sets within Huon with nearly 90 employees currently completing a Certificate III Aquaculture (at June 2020). Other employees are completing VET sector qualifications in seafood processing, engineering fabrication, marine mechanical and electrical apprenticeships.

Language, literacy and numeracy support continue to be made available to employees requesting support to assist them in their everyday work.

Incident Rate (IR) Lost Time Injuries per 100 employees

FY18 FY19 FY20

0.971.00.79

Lost Time Injury Frequency Rate (LTIFR) Per million hours worked

FY18 FY19 FY20

44 5

Average Lost Time Rate (ALTR) Hours lost per employee

FY18 FY19 FY20

10

14 13

Employees

FY18 FY19 FY20

665600723

7

During the year, Huon also introduced the Innovation Program to bring our employees’ ideas to life. Since the Program’s launch, the Innovation Team has received and reviewed ideas from across the business and worked with a number of employees to further develop and implement their innovations.

Huon employs 723 people across the Group, an addition of 58 since 30 June 2019 to support the increase in production during the year.

Outlook Huon’s focus in FY2021, as it builds towards another step change in harvest volume, will be growing the market and locking in contracted sales. The expected increase in harvest volume for FY2021 of around 50% to at least 36,000 tonnes will be supported by both company and industry investment in marketing to increase salmon’s share of the protein market.

Huon’s channel mix is likely to be similar to that in FY2020 with around a third of sales going offshore. The strong foundation that was established in that year with international retail partners throughout Asia will continue to be built on, aiming to progressively increase the share of exports going to contracted international retail sales.

There will be a similar focus in the domestic retail channel, particularly on such segments as supermarkets, independent retail, quick service restaurants and the growing e-commerce space. It is these segments that will deliver the certainty of known volume that will underpin more stable Group financial performance over time. We expect retail sales to at least reflect the growth in demand, supported by our increased capability to supply fresh salmon to outlets in Sydney and the regions following the opening of our Ingleburn processing facility in NSW last year.

The strong performance of the 19 Year Class salmon combined with the slower harvest in Q4 is expected to deliver an average HOG weight in FY2021 in excess of 5.3kg. This, together with the reduced cost of managing this class due to the productivity benefits derived from the investment in new infrastructure and farming methods, is expected to deliver a cost of production (excluding freight) of under $9.50/HOG kg.

Revenue will depend on pricing and in FY2021 this will be driven both by global and domestic supply dynamics and the economic environment as countries globally manage their response to the pandemic. While we are confident of recording increased revenue given the strong uplift in volume, the volatility in pricing over FY2020 and the increased uncertainty about the economic outlook makes it difficult to form a view about trends in pricing over the course of the year.

We expect that FY2021 will continue to present challenges as economies emerge from the constraints imposed by COVID-19. We are however optimistic about our ability to deliver continued productivity improvements in the way we farm which will realise our long term goal of lowering operating costs.

Review of operations

Huon Aquaculture Group Limited

Annual Report 2020

8

9

Operating in unique environments

Map Key Office Processing facilities Farming regions

A Bridport HatcheryB Springfield HatcheryC Millybrook HatcheryD SALTAS HatcheryE Derwent HatcheryF New Norfolk Brood FacilityG Bagdad Brood FacilityH Lonnavale HatcheryI Forest Home HatcheryJ Whale Point Salmon Nursery

Huon is fortunate to farm in Tasmania’s unique environment, allowing the Company to raise salmon in locations in which they thrive. From the time Huon Salmon start their life in hatcheries up until they are harvested, their environment plays a vital role in their health, growth and quality.

Onshore

HatcheriesHatcheries allow Huon to mimic the natural lifecycle of salmon, synchronising batches of salmon to go out to sea at different times of the year, enabling the supply of fresh healthy fish all year round. Located throughout Tasmania, they allow Huon to take advantage of different water and environmental conditions and maintain high standards of biosecurity.

Whale Point Salmon NurseryWhale Point Salmon Nursery is the southern hemisphere’s first onshore salmon nursery and represents a step change in Huon’s production capability.

ProcessingThe Paramatta Creek and Ingleburn (Sydney) processing facilities are two of the most advanced in the world, ensuring the fish are as fresh as possible when they go to market.

Marine regions

Macquarie HarbourLess than 10% of Huon’s salmon production comes from Macquarie Harbour with stocking densities kept low in order to manage sustainable farming in this unique water system.

Huon River and D’Entrecasteaux ChannelHideaway Bay on the Huon River operates as the shorebase for Huon’s operations. This sheltered bay, with its calm waters, is where Huon manages its harvest as well as undertaking Australia’s only experimental and pre-commercial use fish feed trials.

Storm BayHuon began farming Storm Bay in 2014 as part of its long term growth strategy to shift salmon farming into high-energy offshore sites. The addition of the East of Yellow Bluff lease in Strom Bay doubles the capacity of Huon’s offshore sites.

Western AustraliaThe Western Australian Government has recently announced it will accelerate development of the Geraldton-based finfish nursery project, allowing Huon to unlock the next chapter of its plans to commercially farm Yellowtail Kingfish (YTK) in WA’s Midwest.

Storm Bay

Hideaway Bay

Macquarie Harbour

C

DF

B

TASM ANIA

A

LAUNCESTON

DEVONPORT

Parramatta Creek Processing Facility

HOBARTE

H I

J

G

Processing Facility

PERTH

MELBOURNE

TASMANIA HOBART

SYDNEY

BRISBANE

AUSTR ALIA

Huon Aquaculture Group Limited

Annual Report 2020

10

East of Yellow Bluff (late smolt)

Storm Bay (growout)

Two unused sites

Map Key Lease zones High-energy lease zones Land base facilities

Whale Point (nursery)

Port Huon (engineering workshop)

D’E

ntre

cast

eaux

Cha

nnel

Flathead Bay (early smolt)

Roaring (early smolt)

Garden Island (early smolt)Hideaway Bay

(service, research and harvesting)

Police Point (early smolt)

Zuidpool North (growout)

Zuidpool South (growout)

Huon River

Storm Bay

Tasman Sea

Hideaway Bay

11

Huon has a reputation for leading innovation across all areas of its operations which is supported by a highly skilled workforce with diverse and extensive expertise.

Huon investment and innovation

As a vertically integrated salmon producer, Huon’s operations span hatcheries, nurseries, marine farming, maintenance, harvesting, processing, value adding, marketing, sales and distribution.

Huon has invested $350 million over the past five years to ensure it is able to supply the growing demand for salmon in the years ahead. In order to operate on a larger scale, Huon has continued to innovate and engineer solutions by leveraging and developing technologies to position it at the cutting edge of aquaculture. Huon has a reputation for leading innovation across all areas of its operations which is supported by a highly skilled workforce with diverse and extensive expertise.

Hatcheries

Fish

Husbandry

Lighting

Processing

Nurseries

M

arine Farms Harvesting Pro

cessing Market

Feeding Fallowing

Value Added

Net

Management

Predator

Bathing

Maintenance

Program

Selec

tive Breeding

M

anagement

Huon Aquaculture Group Limited

Annual Report 2020

12

Huon has a reputation for leading innovation across all areas of its operations which is supported by a highly skilled workforce with diverse and extensive expertise.

Storm Bay

WellboatsRegular bathing and grading of salmon and harvest grade fish transferred to Hideaway Bay.

Fortress Pens Designed to operate in one of

the roughest farmable waters in the world with a double net system,

which has reduced predator risk.

HarvestingThere is a direct relationship between harvesting and the quality and freshness of the end-products and by focussing on low-stress, humane, night-harvesting, using RSPCA-UK certified equipment, Huon consumers experience fresher, high quality salmon year-round.

Whale Point Salmon NurseryBy growing our salmon larger on land, we improve the efficiency of our overall production cycle by reducing the time our salmon spend at sea from 14 months, to 9-10 months. Importantly the reduced time at sea reduces Huon’s agricultural and environmental risks.

Forest Home HatcheryA second generation recirculation hatchery that delivers outstanding smolt quality and larger smolt sizes with a reduced environmental footprint

Feed BargesTwo of the largest unstaffed fully automated feed barges are moored at Storm Bay.

Feed control-roomFeeding is monitored from Huon’s

central feed control-room in Hobart. Automated feeding software ensures

fish are fed 24/7, 365 days a year, in all weather conditions.

High-energy offshore sitesDeeper, high-energy sites at Storm Bay mean that pens are located in areas with stronger currents and greater water movement. Resulting in better fish performance.

Hobart

Feeding

Bathing

Feeding

Hideaway Bay

Tasman Sea

13

The Ronja Storm

The Ronja Storm, the world’s largest and most technically advanced wellboat, arrived in Hobart during February 2020 and is now operational at Huon’s sites in the South East of Tasmania.

The Ronja Storm is the final piece of investment in Huon’s Controlled Growth Strategy and is pivotal to the Company’s production expansion. The largest wellboat in the world will reduce production costs, strengthen biosecurity requirements and deliver the safest salmon farming operations in the world.

What is a wellboat?Wellboats have wells or tanks for the storage and transport of live fish. The term was first used in the 17th century and, before modern refrigeration methods, wellboats allowed for the delivery of live fish to port. Today wellboats are used extensively in the aquaculture industry around the world. They eliminate the need for time intensive, noisy towing of pens back and forth through Tasmanian waterways. Wellboats also provide a much safer working environment for employees, particularly as Huon grows its offshore farming.

Huon was the first company globally to use a wellboat for the purpose of bathing fish in freshwater.

Since 2014, Huon has been farming with the Ronja Huon, its first, smaller wellboat. The experience gained over that time was applied to the design of the Ronja Storm.

What are the benefits?– Strengthened sustainability of farming operations

through the treatment of Amoebic Gill Disease (AGD), a key fish health challenge in Tasmania, by bathing fish in freshwater in the wells of the wellboat.

– Bathing can be timed for when the fish need it rather than having to maintain fixed schedules. This is expected to save several baths a year.

– The efficiency and size of the Ronja Storm means we will never get behind with our bathing programme.

– Over a full year more fish can be put into each pen, without increasing the stocking density, as the Ronja Storm can carry more in each load. Eliminating multiple trips will reduce stress on the fish resulting in less mortalities.

– An on-board grader enables fish that are too small for harvest to be separated out and returned to the pen. This will increase total production from each pen in a year from 500 to 800 tonnes up to 1,000 tonnes.

– Improved biosecurity as wellboats have removed the need to tow pens of live fish, thereby eliminating fish escapes and the potential spread of communicable fish diseases.

Huon Aquaculture Group Limited

Annual Report 2020

14

Bathing Salmon are bathed in freshwater for a few hours to treat

gill amoeba.

Size Matters• Length: 116m

Width: 23m

• Desalination capacity: 16.8 million litres a day

• Bathing capacity: a complete fortress pen in one load

• Fish loading capacity: 1,000 tonnes per hour

How it works

Well capacityThe Storm can hold in

excess of 800 tonnes of fish at a time across its four wells.

Smaller graded fish are returned to fortress pen and

larger fish retained on-board for transportation to harvest.

On-board desalinationProduces 700,000 litres per hour of freshwater. Has 5,000 tonnes of extra water storage so new freshwater can be made while bathing fish.

Advanced water control system monitors the

levels of CO2, Ammonia and oxygen.

Live fish graderThe fish loading system has a built-in live fish grader that allows for progressive harvesting of fish of a specific size.

The technology is more robust than ever – a specialised offshore power management system has been fitted to the Ronja Storm, the first in a wellboat, which reduces energy use and noise emissions. The vessel includes backup power systems that ensure it can continue to operate with a minimum of 50% power capacity in case of system failure. This is essential in delivering robust, secure fish welfare practices.

The Ronja Storm is an investment into Huon’s future by enabling expansion in offshore, more challenging farming environments. It strengthens Huon’s animal welfare and biosecurity practices, delivers unparalleled safe working conditions and provides tangible evidence that Huon is committed to working with communities to reduce its environmental footprint.

Size matters When farming offshore sites, where conditions are challenging almost every day, size matters. The Ronja Storm’s well capacity and ability to produce freshwater on-board means it can also do considerably more work when conditions are fine and easier for farm crews.

The Ronja Storm is laden with cutting edge technology: – Every well has 30 sensors installed which deliver

constant, real-time monitoring data back to the bridge. – The well capacity is almost treble that of the

Ronja Huon, allowing an entire 240 metre pen of fish to be bathed at one time (upwards of 800 tonnes) significantly improving bathing efficiency.

– An on-board desalination plant can produce 700,000 litres of freshwater every hour, minimising use of Tasmania’s freshwater resource and eliminating the need for frequent travel movements back to shore to get water.

– An adjustable live fish grader in the loading system which can grade 300 tonnes of fish per hour. This allows for removal of small fish which can be returned to pens, ensuring only the correct size fish for the market are harvested.

Bathing

15

The Outlook for the Salmon Market

1 Kontali Aquaculture Bulletin 2020 No 82 ABS Import Data

Huon is committed to growing per capita consumption of salmon and ocean trout through a significant investment in advertising and promotion in the domestic market. Huon expects to increase its branded distribution across Australia as it captures the majority of growth in the market.

Weak global supply growth likely to match softened demand in short-mid termThe global salmon market has been in a relatively strong position in terms of supply. In 2019 farmed Atlantic salmon grew 7% on the previous year to 2.6 Mn tonnes.1

Whilst supply growth in the next 2-3 years is forecast in be in the low single digit growth it is likely that there will be a supply imbalance (over supply) during this time, depending on the strength of food service market recovery post COVID-19.

International imports into the Australian market have remained stable at around 11,500 tonnes for the last three years. That is expected to continue through FY20212, if not decline, as Huon targets import replacement in food service and retail sales channels.

Demand for salmon affected by COVID-19 but outlook remains positiveAs land-based proteins continue to increase in price, salmon continues to look more affordable to consumers year after year. Salmon (and seafood) consumption is low in many developed markets with many salmon producers and industry lobby groups focused on driving increased consumption of salmon both inside and outside the home. Farmed salmon is also increasingly being viewed as a better ‘green’ alternative than other land-based proteins due to its low carbon dioxide output, low water consumption and efficient food conversion ratios.

Global price neutral demand is still sitting between 7% and 10% according to Pareto Securities but the current impact of COVID-19 is driving significant short term oversupply as producers seek to move volume in a constricted market environment.

Looking beyond lockdown restrictions, it is unlikely that the hotel, restaurant and catering segment (HoReCa) which is estimated to be responsible for 45% of global salmon consumption, will bounce back overnight. In China (one of the first countries to ease restrictions) only half of all restaurants have re-opened, and those that have are operating at only 40-50% of ‘normal’ capacity. It is also unlikely that growth of salmon at the retail level will offset this loss, particularly in Australia, due to low consumer penetration of salmon for cooking in the home.

Nevertheless, the long-term demand dynamics for salmon still remain strong with low levels of penetration in many markets indicating there is plenty of room for growth in more ‘normal’ market conditions.

Like the international market, the fundamentals of salmon as a protein source for Australia are strong over the long term. Huon estimates the total impact from COVID-19 on Australian demand has been a loss of approximately 2,000 HOG tonnes in FY2020.

4.2%

2022

F

4.3%

4.4%

22.4

%

3.8%

-1.3

%

7.0

%

2018

2015

2012

2005

2009

2002

7.1%

-5.7

%Li

ce a

nd A

lgae

Blo

om Depending on biological factors 2-6% growth is possible in the mid term

ISA

Out

brea

k

2.1%

1.5%

-1.3

%

8.2%

2019

2019

2013

2006

2010

2003

2.1%

2020

E

1.9

%20

21E

2017

2014

2007

2011

2004

2008

2001

Year on year change in global Atlantic Salmon supply and forecast (%)

6.5%9.

1%10.1

%

12.2

%

5.4% 6.

9%

13.0

%

Source: Robobank

Huon Aquaculture Group Limited

Annual Report 2020

16

Huon’s Approach to Marketing

Strong contract focus for FY2021 and beyondFY2021 will be the year when Huon begins to realign its sales channels as the business moves more volume out of a trading environment, or the spot export market, into retail contracts in both the domestic and international markets.

Domestic retail sales volume growth is forecast to be strong through FY2021 as Huon benefits from increased exposure in this channel via newly won contracts.

International retail sales are also growing strongly with 170% volume sales growth recorded in FY2020 from new customers in new markets. Huon is in a strong position to continue growing this channel as it offers international retailers a distinct point of difference focused on Huon’s artisanal volumes when compared with global producers. Freshness to market in the key Asia region is another unique selling proposition.

Huon has also reduced its exposure to single export markets through the development of other regions, including North America where initial market interest and volume growth has been strong.

Prior to COVID-19, Huon’s wholesale business was on a strong growth trajectory and whilst that channel has been the most impacted by lockdown measures, it is expected to recover quickly as the economy emerges from COVID-19. Key areas of focus in this market continue to be quick service restaurants, sushi outlets, independent and specialty seafood retailers. At the same time Huon is using its strategically located processing facilities to move closer to the end customer.

FY2021 will continue to see high levels of trading volume internationally, given the large increase in production the business has generated following the completion of its controlled growth strategy. A conservative view has been adopted when forward pricing this volume and Huon is well placed to compete on product size and specifications in this market.

Positioning the Huon brand for long term sales growthHuon expects to continue to expand branded distribution in all product segments both domestically and internationally over FY2021, following a strong year of distribution growth in FY2020. This will be supported by a significant above the line investment in marketing at the end of the first half to drive Huon Salmon consumption domestically. This will be in addition to industry based marketing spend on both the seafood and salmon categories. This investment will increase salmon’s share of voice in the protein market where there is significant

underlying demand ready to be unlocked. Previous spends of this nature domestically have driven single year, double digit volume growth whilst maintaining price.

Huon is therefore confident that this initiative can deliver a major increase in domestic per capita consumption, even in a COVID-19 affected market.

There will be a strong focus on the launch of the entire Huon Salmon and Ocean Trout fresh pre-packed range into a major retailer in the December quarter. This will include a revamped Harvested By Night, Fresher By Day campaign, building on Huon’s already strong freshness credentials (a key purchase driver for consumers in seafood).

At the same time Huon continues to invest in its B2B loyalty program, Fresher Rewards, to ensure it maintains the strong connections and customer understanding it has established across the food service and wholesale environment. This program saw a 50% increase in users over the last quarter of FY2020 and the outlook remains strong for ongoing growth in the program.

Growth opportunities to watchThroughout FY2020 Huon continued to explore other sales channel opportunities with a particular focus on e-commerce. As COVID-19 took hold in the second half of FY2020 the business took advantage of its exposure to this channel, driving a 127% increase in volume whilst increasing value at a faster rate.

This channel to market is still coming off a low base however Huon’s own direct e-commerce experience and that of its channel partners in this sector, underpins a high level of confidence that there continues to be significant growth potential.

Huon is also exploring the opportunity for using salmon by-products in the pet food market with initial pet food product prototypes currently in development. Huon is set to trial these products in independent retail outlets in the first half of FY2021.

50%Increase in users of B2B loyalty program

‘Fresher Rewards’

170%Growth of volume sales in the international retail channel

127%Volume increase in e-commerce channel use

17

Risk Management and Sustainability

Agricultural RiskAll good farmers take a proactive and holistic approach to safeguarding the health and welfare of their stock. At Huon Aquaculture, this involves feeding quality diets, good site management, fish husbandry, biosecurity measures and vaccinating its stock.

Fish welfare is a priority for Huon. This is why we participate in the RSPCA Approved Farming Scheme, meeting the RSPCA’s detailed animal welfare standards for farmed Atlantic salmon. We are proudly the only seafood producer with RSPCA Approval.

Huon has been farming sustainably for over 30 years and, as with any farming endeavour, it is subject to a range of events with outcomes that can impact the supply of smolt, fish growth and mortality.

The most effective strategy to minimise exposure to such risk is good animal husbandry which demands care and innovation throughout the lifecycle of the fish. Preventing disease and the effective management of outbreaks, if they do occur, is integral to Huon’s farming methods.

Huon undertakes a range of measures to proactively and successfully manage its agricultural risk.

Biosecurity and Year Class separationGood biosecurity is critical in preventing and managing disease which is why Huon has been actively involved in the joint industry-government review and implementation of improved biosecurity measures.

The decision to shift the focus of operations and future growth to new lease areas in Storm Bay was reinforced by the benefits provided by tighter management of biosecurity across its operations. Huon now operates in three distinct biosecurity zones – the Huon River and D’Entrecasteaux Channel; Storm Bay; Macquarie Harbour.

Different year classes of fish have always been held on separate lease sites to avoid the transmission of disease organisms from older fish to the younger fish. Huon’s separation of smolt and growout by lease and zone is illustrated on page 11.

With the East of Yellow Bluff lease and the reorganisation of leases in the Huon River and D’Entrecasteaux Channel there is now increased distance between year classes.

Prevention of diseasesHuon’s Veterinary Health Plan is a living document that underpins good fish health and welfare practices. Huon fish are currently routinely vaccinated for a range of bacterial and viral diseases.

Over the past year, Huon has made continuous improvements to the pens including tighter bird nets and bird escape hatches. Huon utilises in-situ net cleaners to minimise the build-up of biofouling on the Fortress Pens. Regular cleaning is a high priority at Huon as this ensures high water flow through pens, maintaining maximum oxygen levels to fish.

WellboatsHuon was the first company globally to use a wellboat for the purpose of bathing fish in freshwater and now has two wellboats in service both designed to Huon specifications.

Both these vessels have supported Huon’s proactive approach to managing risk – by enabling the Company to safely farm in more exposed sites, improving operational efficiency (more fish can be bathed at one time), minimising fish losses by treating fish more quickly and efficiently (reducing AGD impact) and reducing Huon’s reliance on Tasmania’s valuable freshwater supply through the Ronja Storm’s on-board desalination facility.

Stocking densityLower stocking densities give fish more room to move and the freedom to express their natural behaviours. Huon operates with one of the lowest stocking densities in the world at approximately half the 15kg/m3 maximum stocking density allowed under the RSPCA Standards for salmon.

FallowingJust as a farmer rests their fields between their crops, Huon rests the seabed between stocking. This allows the seabed to naturally recuperate and break the cycle of any potential disease issues.

Huon’s strategy includes at least one month whole-lease fallowing each year for disease control and up to 18 months’ pen-bay fallowing every 2–3 years to return the benthos (sea floor) to baseline conditions. In addition, the seafloor beneath each stocked lease is inspected by ROV (remotely operated underwater vehicle) on a monthly basis with results provided periodically to the environmental regulator.

Feed supplyOver 50% of the input costs to salmon production is feed. Huon mitigates this risk by maintaining multiple sources of feed supply which are all sourced from Tasmanian-based mills. This reduces the risk of relying on imports and expands the supply chains for Tasmanian primary producers.

With access to regular supply of the right type of feed, production is not compromised.

Fortress PensHuon’s patented double-netted Fortress Pen technology continues to be integral to the successful expansion of Huon’s farming operations into high-energy offshore sites like Storm Bay.

When introduced, Huon’s in-house developed Fortress Pens were a world first. Key elements of the design include a fully enclosed walkway; nets made out of the same material used to make bullet proof vests to withstand the buffeting Tasmanian winds; and a design which minimises predation from seals and birds by restricting their access to the pens below and above the waterline.

Over the past year, Huon has made continuous improvements to the pens including tighter bird nets and bird escape hatches. Huon utilises in-situ net cleaners to minimise the build-up of biofouling on the Fortress Pens. Regular cleaning is a high priority at Huon as this ensures high water flow through pens, maintaining maximum oxygen levels to fish.

In addition, removing excess weight mitigates the risk of holes and tears which may result in wildlife incursion or fish escape.

Huon Aquaculture Group Limited

Annual Report 2020

18

NurseryHuon’s Whale Point Salmon Nursery is the only one of its kind in the southern hemisphere.

Huon’s success in growing salmon to a larger size on land (in a controlled environment) has reduced the time spent at sea by 30–40%. As a result Huon salmon is now being grown to harvest size in less than a year.

Larger smolt are more robust and less vulnerable to predation. This provides increased capacity to manage existing leases, lowering the environmental and biosecurity risk. The nursery has zero discharge to the environment due to the collection and composting of the fish nutrients for use by local land farmers.

Multiple site broodstock supplyHuon has broodstock facilities located at five, geographically separate sites around Tasmania, thereby guaranteeing supply.

This segregation of broodstock reduces biosecurity and production risks while each population is closely monitored to inform future breeding plans and to identify potential health issues.

Centralised Control of Operations including feed systemsHuon has long been a pioneer in feeding methods and technology. Its centralised feed operation has resulted in better control and oversight of on-water operations as well as supporting the Company’s move to offshore farming without compromising employee safety.

From the Hobart based control room, fish are remotely fed, to appetite, all at the same time. This replicates the fish’s natural behaviour and allows less dominant fish equal access to feed from anywhere in the pen.

National award-winning pellet-recognition software uses a combination of industrial automation and artificial intelligence to determine when the fish are no longer hungry. It then automatically turns off the feed, reducing feed wastage and minimising impact on the sea floor.

Locally-built feed barges, moored at each farming lease, are remotely operated from the control room. In the past year, the 600t Hulk, Huon’s seventh feed barge, joined the fleet, operating in Storm Bay.

Lift up SystemHuon’s Fortress Pens provide timely, automatic retrieval of fish mortalities, which is a critical component of good biosecurity management. Early detection and removal reduces the risk of potential spread of disease and minimises attraction of predators.

Huon’s control room operators also use cameras (positioned on pens and underneath the water) to identify and inspect any mortalities which minimises the use of divers, improving safety for on-water crews.

Social/Environmental RiskAs a fully vertically-integrated company, Huon’s compliance obligations span across all aspects of its operations. At the same time, Huon has a responsibility to ensure that its activities are understood by the communities in which it operates, and that its communication is transparent and authentic. Being part of any community brings with it a responsibility to do things that will help keep the community safe and connected.

Stakeholder engagementHuon encourages engagement with the community and others connected to, or invested in, activities associated with Huon’s operational footprint. Dedicated teams at Huon proactively manage relationships with all stakeholders including government, regulators, investors, suppliers, customers and communities.

Complaint management is undertaken transparently and evidence based data is regularly published in a bid to better inform stakeholders. Over the past year, significant effort has been invested in community educational activities to promote aquaculture as a career pathway.

Huon invests heavily in Tasmanian owned contractors and suppliers as well as providing direct funding into community grant schemes and sponsorships that focus on building capacity and resilience in regional communities.

Feed formulations including fishmeal/fish oilHuon fish are fed specialised diets that optimise health and performance at every stage of their lifecycle. All of Huon’s feed is now sourced from Tasmanian-based mills which reduces the risk of relying on imports, and expands the supply chains for Tasmanian primary producers.

Salmon rely on astaxanthin, an important anti-oxidant, for muscle growth and stimulation of the immune system as well as improving fertility and growth. It is also the source of salmon’s signature flesh colour. In the wild, astaxanthin is sourced from krill but is added to the diet of farmed salmon.

Huon has actively worked with feed suppliers to decrease the use of marine ingredients in feed. Huon has doubled the percentage of vegetables in its feed – now 60% compared with 31% in 2015.

Reducing the dependence on marine fish resources for aquaculture feed is increasingly receiving attention. This is why Huon only works with feed companies that ensure full traceability of feed ingredients and responsibly source marine ingredients from sustainably managed fisheries. Huon has also reduced the proportion of fishmeal in feed formulations by 20% from a high of 22% in 2013 to the current 18%.

AntibioticsConsumers are becoming increasingly conscious of inappropriate or excessive antibiotic use. Huon has not used antibiotics in its marine farming since 2016.

Antibiotics should only be used as a last line of defence and as such, Huon is continually working to develop proactive diet régimes and vaccines to allow stock to combat known illnesses and lead healthy lives. Huon voluntarily publishes its antibiotic usage as well as submitting fish stock for flesh testing, in addition to participating in the publicly available National Residue Survey.

19

Market RisksThe key market risks relate to the ability to maintain supply of product, market disruption factors and consumer confidence in the quality and safety of Huon’s product.

COVID-19On March 11, 2020 the World Health Organisation officially declared the global spread of the novel coronavirus, COVID-19, a pandemic. The potential key risks posed to Huon from the pandemic include operational, safety and market disruption.

Huon has adhered to government guidelines with no disruptions to the ongoing operations of the business.

The Australian food services sector of the wholesale market has been disrupted by the closure or severe restrictions placed on the operations of restaurants, clubs and the food catering industry, as a result of government imposed lockdowns. Access to the international salmon export markets was interrupted due to the disruption to international air freight services. Huon’s diversified presence in both the domestic and international market has enabled it to react and adapt to the changing conditions.

Product pricingHuon’s profitability and the market value of its biological assets are sensitive to salmon prices in both the domestic and international market. Prices are dependent on short and long term supply and demand variations, and market conditions. This risk is managed through Huon’s customer channel and product diversification strategies, through customer supply contracts and category marketing investment.

Product acceptance in the marketThe sale of any product is dependent on market perceptions of its quality and safety. Huon mitigates this risk through its rigorous quality assurance systems and constant product testing. Significant, ongoing marketing continues to raise the profile of the Huon brand as a premium product and position it for growth.

Diversification of channel mixReliance on one channel or a limited client base for the sale of any product introduces risk. Huon manages this through selling into the wholesale market, the retail sector both domestic and offshore via contracted sales, as well as through the export channel.

Workplace Health and SafetyProviding a workplace that is safe and ensuring that staff return home un-injured each day is a fundamental duty of all employers. It is also essential for attracting and retaining staff as well as providing an environment which supports learning, team work and innovation. Across the business, strengthening automation and use of technology has continued to secure jobs for the industry and Huon seeks out more and more ways to improve its operations.

Equipment and work processesHuon’s Fortress Pens are designed to protect staff from interactions with seals and provide a safe working environment. Extensive use of automation and technology is deployed throughout the business including in the areas of net cleaning and repair and remote feeding. The introduction of unmanned feed barges moored onsite at leases together with automated feeding, reduces the number of vessel movements and time employees spend on water.

At the Parramatta Creek processing facility, continuous modification to processes has included the introduction of automation and robot packers, minimising manual handling.

Training and professional developmentDevelopment of staff through training, increases productivity and reduces the risk of injury and accidents. It also increases the rate of staff retention. Huon staff continue to participate in development programs with many undergoing professional development including VET sector training courses specific to their role.

In addition, general literacy, numeracy and digital literacy support is offered to all employees and Huon continues to engage with the tertiary education sector to identify future workforce development requirements.

Third party, independent certification Huon seeks independent certification of its processes to assist with risk mitigation and as a means of validating compliance with global best-practice.

In 2018, Huon was the first (and remains the only) seafood producer in Australia to meet the RSPCA’s detailed animal welfare standards for farmed Atlantic Salmon, and cooperate with the rigorous ongoing assessments by the RSPCA to ensure compliance. The RSPCA Approved logo offers consumers the assurance that Huon Salmon have been farmed humanely and in an environment that meets their needs. The RSPCA’s standards currently don’t permit farming in Macquarie Harbour and therefore these salmon products won’t be labelled as RSPCA Approved. Currently less than 10% of Huon Aquaculture’s total salmon production is from Macquarie Harbour.

In 2012, Huon became the first Australian salmon producer to achieve the internationally recognised accreditation, Global G.A.P. This pre-farm gate standard covers the whole production process of the certified product from the hatchery to the point of harvest and packing and recognises ongoing, continuous improvement.

Risk Management and Sustainability

Huon Aquaculture Group Limited

Annual Report 2020

20

Huon is also a BRC AA-rated seafood processor. The BRC Global Standards specify requirements to be met to enable the production, packaging, storage and distribution of safe food and consumer products. These standards are specified by growing numbers of retailers and branded manufacturers across the globe. Huon’s Parramatta Creek processing facility first achieved BRC AA rating in 2016. At the time it was the first seafood processing facility in Australia to achieve the BRC AA rating.

Huon is also HACCP certified. Safe food production is achieved by applying HACCP techniques to ensure that potential hazards during the process are recognised, monitored and controlled.

Finally the Australian Quarantine and Inspection Service (AQIS) also undertakes regular inspections and assesses Huon’s certification process compliance to approve the sale of Huon products overseas.

In late 2019, Huon’s Forest Home hatchery farmland received organic certification from the National Association for Sustainable Agriculture Australia enabling a third party artisan cheese and milk producer to label its products as organic.

Managing Climate and Environmental RiskHuon has proactively taken steps to manage and mitigate the impact of climate change on their operations. The first step was pioneering offshore farming in Tasmania, where dissolved oxygen levels and water temperatures are better for the fish. Huon has been successfully farming offshore in Storm Bay since 2014 and it is a key component in Huon’s proactive management of climate change.

Other steps include selectively breeding fish that perform better in warmer waters; undertaking trials with global feed companies to develop an easy-to-digest summer diet; and investing in renewable energy sources.

Salmon farming is one of the most efficient ways of using natural resources to produce a healthy protein. It has a low carbon footprint, high energy and protein retention efficiency and low water footprint. Across all the different farmed animals, the Global Salmon Initiative has found that the Feed Conversion Ratio of salmon is the most efficient of all farmed animals. While a kilogram of beef meat requires between 6–10kgs of feed, a kilogram of salmon meat requires just 1.2–1.5kgs.

An example of the Huon’s efforts to mitigate the risk of climate change is its involvement in an industry selective breeding program. This produces high performing broodstock adaptable to Tasmania’s farming conditions. Since the founder populations were recruited, there has been a steady increase in genetic gain where growth potential and amoeba resistance have improved by roughly 2–3% a year. Initial results from the family-based program replicated those seen from earlier mass selection which identified that amoeba resistance is a heritable trait and can be increased through the generations. In the past year, Huon purchased a larger share in the program to ensure ongoing access to a bigger pool of genetically elite breeders.

Warming waters are a key challenge of salmon farming globally and a joint feed trial between Huon and BioMar, a leading feed company, aims to reduce the impact on stock by creating a better performing summer diet.

The aim of the current trial is to help the fish digest and convert feed in summer temperatures that are higher than their preferred range. Given that warming waters are a global issue for salmon farming, it is expected that the research taking place in Tasmania will have positive implications global. The trial is being conducted at Huon’s Hideaway Bay trial pens, which have hosted in-house and commercial feed trials for many years.

A further example of Huon’s commitment to managing the impact of climate change on public waterways is our participation in a research program into Giant Kelp run jointly by the Institute of Marine & Antarctic Studies (IMAS) and The Climate Foundation.

Giant Kelp has endless applications from being used in food and fertiliser, bioplastics, and high-value nutraceuticals. It also has the added benefit of being extremely fast-growing, providing habitat for numerous other species and soaks up nutrients in the water. However, warming Tasmanian waters have caused an alarming reduction in the size of the giant kelp forests in the State, leaving valuable food-webs at risk. The strengthening of the Eastern Australian Current is the primary reason for the decline in giant kelp. This is why Huon is supporting IMAS and The Climate Foundation to cultivate warm-water tolerant strains on our Storm Bay leases to assess their potential for the restoration of Tasmania’s kelp forests.

There is a company wide focus to reduce the costs of energy from the supply side. Huon is also involved in the Blue Economy – Cooperative Research Centre, partnering with other research institutions to examine current and future renewable energy options.

21

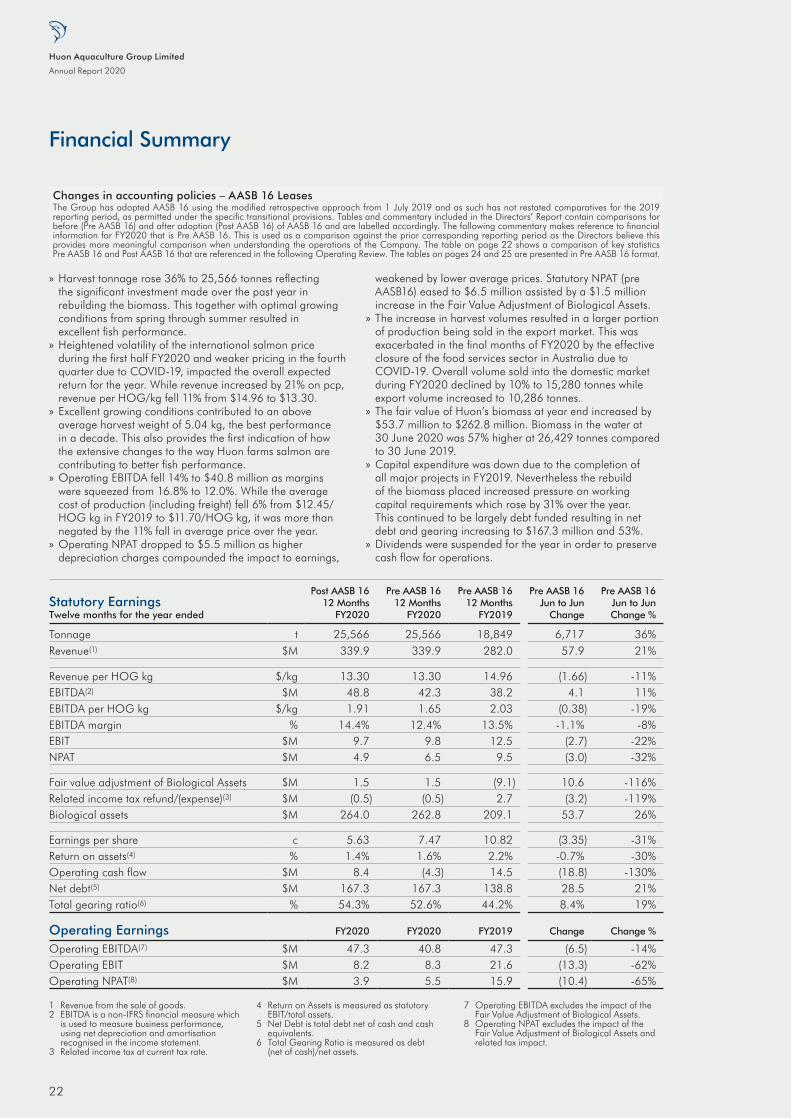

Financial Summary

» Harvest tonnage rose 36% to 25,566 tonnes reflecting the significant investment made over the past year in rebuilding the biomass. This together with optimal growing conditions from spring through summer resulted in excellent fish performance.

» Heightened volatility of the international salmon price during the first half FY2020 and weaker pricing in the fourth quarter due to COVID-19, impacted the overall expected return for the year. While revenue increased by 21% on pcp, revenue per HOG/kg fell 11% from $14.96 to $13.30.

» Excellent growing conditions contributed to an above average harvest weight of 5.04 kg, the best performance in a decade. This also provides the first indication of how the extensive changes to the way Huon farms salmon are contributing to better fish performance.

» Operating EBITDA fell 14% to $40.8 million as margins were squeezed from 16.8% to 12.0%. While the average cost of production (including freight) fell 6% from $12.45/ HOG kg in FY2019 to $11.70/HOG kg, it was more than negated by the 11% fall in average price over the year.

» Operating NPAT dropped to $5.5 million as higher depreciation charges compounded the impact to earnings,

weakened by lower average prices. Statutory NPAT (pre AASB16) eased to $6.5 million assisted by a $1.5 million increase in the Fair Value Adjustment of Biological Assets.

» The increase in harvest volumes resulted in a larger portion of production being sold in the export market. This was exacerbated in the final months of FY2020 by the effective closure of the food services sector in Australia due to COVID-19. Overall volume sold into the domestic market during FY2020 declined by 10% to 15,280 tonnes while export volume increased to 10,286 tonnes.

» The fair value of Huon’s biomass at year end increased by $53.7 million to $262.8 million. Biomass in the water at 30 June 2020 was 57% higher at 26,429 tonnes compared to 30 June 2019.

» Capital expenditure was down due to the completion of all major projects in FY2019. Nevertheless the rebuild of the biomass placed increased pressure on working capital requirements which rose by 31% over the year. This continued to be largely debt funded resulting in net debt and gearing increasing to $167.3 million and 53%.

» Dividends were suspended for the year in order to preserve cash flow for operations.