danske bank: meeting the new age · danske bank: meeting the new age ... global head of wealth...

TRANSCRIPT

Danske Bank: Meeting the new age

1 June 2016

Tonny Thierry AndersenExecutive Board memberGlobal Head of Wealth Management

Expenses (DKK bn)Net profit* (DKK bn)

*Before goodwill impairments ** Restated to reflect new business unit structure

Loan loss ratio (bps)

The steady improvement in financial results continues

- Driven by a strong cost focus and improvements in credit quality

4.9

Q116

7.1

20142013

13.0

17.7

2015 Q116

5.3

2015

23.2

21.8

2014

24.0

22.6

2013

23.8

ReportedRestated**-3

0

20

27

20142013 Q1162015

Danske Bank is closing the gap to peers

- And well on track to meet ROE target of above 12.5% in 2018*

13.213.8

12.712.8 13.1

5.0

3.6

20132012 Q1 2016

11.7***

2015

11.6**

2014

8.6**

Danske BankPeer average1)Return on equity (%)

1) Includes Nordea, SEB, Handelsbanken, Swedbank and DNB *At the latest **Before goodwill impairments charges **SEB figure excludes goodwill impairment and other one-off items Note: Figures are reported return on equity

Strong capital build up despite capital distributions

- CET1 at 15.0% after deducting for share buy-back of DKK 9bn

CET1 capital ratios and targets (%)

2.8

Q1 2016

15.0

2015

16.1

2014 Q1 2016 fully loaded

14.7

11.9

15.1

2013

14.7

Expected requirement

in 2019: 11.9%*

CET1 target

At least13%

Regulatory min. CET1 required*Excess capital

* Expected fully phased-in minimum CET1 requirement in 2019: min. CET1 requirement 4.5%, capital conservation buffer 2.5%, SIFI requirement 3%, countercyclical buffers 0.5% and CET1 component of Pillar II requirement.

Total payout ratio1

; %

Significant increase in payouts based on increased dividends and

share buy-backs

1. Based on year-end communicated distributions

2015

96%

46%

51%

2014

81%

43%

38%

2013

28%

2008 - 2012

0%

Dividend payout ratioShare buyback

Outlook for full-year 2016

1. Before goodwill impairment charge. Note: This guidance is subject to uncertainty and depends on economic conditions, including developments in monetary policy at central banks

Impairments

Expected at a low level

Expenses

Expected below the 2015 level1

Net profit

Expected in line with 2015 level1

Introducing Wealth Management

Wealth Management’s contribution to Group financials

Q1 2016 figures

Income & net fee income (share of group)*

4%

Lending & deposits (share of group)*

17%

46%

7%

Other Danske BankWealth Management

Facts

1,992 FTEs work in Wealth

~1.351bn DKK in AuM

Pre-tax return on equity at 25,6%

~95% of income in the Nordic countries

* Amongst wealthy personal customers

3

3

0 1

5

6

7

8

2 4 5 6 7 8 9

4

10 11 122

DenmarkFinland

Sweden

Norway

Austria

Germany

Portugal

Ireland

Italy

SpainUnited Kingdom

Belgium

France Switzerland Luxembourg

Netherlands

Yearly average growth in Wealth 2014-2020*, (%)

Yearly average growth in Wealth, %, 2008-2014*

Wealth Management is an attractive market

* Amongst wealthy personal customers

Aggregated

wealth*

Bn DKK

Market

share

2,9001,900 1,500 1,350

~3%~14%

~27%

~5%

And we see growth potential

In order to execute our vision we have identified four key enablers

Leading

Value Propositions

& Customer Experiences

1

23

Go-to-Market

Excellence

4

Winning People

& Culture

Operational

Excellence

Key focus: Digitalisation

12

2005 20202000 20152010 2025

Traditional consumers Digital nativesTransitionals

Within a few years a new breed of customer will dominate

— the ”digital natives”

13

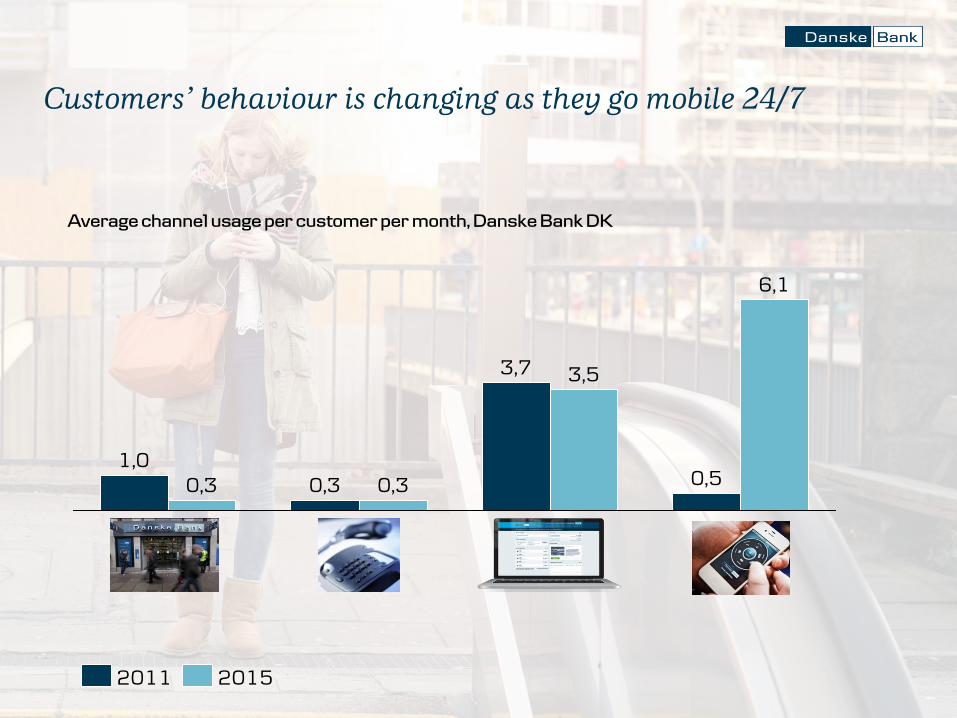

6,1

0,5

3,53,7

0,30,30,31,0

20152011

Average channel usage per customer per month, Danske Bank DK

Customers’ behaviour is changing as they go mobile 24/7

14

3,000

2,400

1,800

1,200

600

0

3,600

2006 2016

Active users; ’000

Onlinebank

Mobilbank

MobilePay

MobilePay is an example of exponential growth

15

March2016

May ’13

Jan ‘15 May ‘16

P2P

MobilePayOnline

June ‘15

POS with Dansk

Supermarked

MobilePayterminals

June ‘15

Receipts

The MobilePay family has gradually been expanded to build a

multisided platform

Invoice

16

“You don’t need a digital

strategy to succeed in this

World, you need a business

strategy for the digital age”

17

Project

X

Don’t be afraid to disrupt yourself

Everything that can be

digitized, will be

digitized, but...

Q&A session

www.danskebank.com/ir

Disclaimer

This presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of Danske Bank A/S in any jurisdiction or an inducement to enter into investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever

This presentation contains forward-looking statements that reflect management’s current views with respect to certain future events and potential financial performance. Although Danske Bank believes that the expectations reflected in such forward looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of various factorsmany of which are beyond Danske Bank’s control

This presentation does not imply that Danske Bank has undertaken to revise these forward-looking statements, beyond what is required by applicable law or applicable stock exchange regulations if and when circumstances arise that will lead to changescompared to the date when these statements were provided

Equity Story