dac working party on development finance statistics policy

TRANSCRIPT

Organisation for Economic Co-operation and Development

DCD/DAC/STAT/RD(2021)1

Unclassified English - Or. English

18 February 2021

Development Co-operation Directorate

Development Assistance Committee

DAC Working Party on Development Finance Statistics

Policy on harmonisation of coding of the financing instrument UN inter-agency

Pooled Funds between OECD-DAC and UN data standards

Informal meeting of the Working Party on Development Finance Statistics (WP-STAT)

3-5 March 2021 - Virtual meeting

This room document, prepared by the UN Chief Executives Board (CEB) Secretariat, provides advice

on which UN funds can be considered multilateral. The document is circulated for INFORMATION

under item 4 of the draft annotated agenda of the WP-STAT of 3-5 March.

Contacts: Ms Carmen Jiménez González ([email protected]); Ms Henriette Keijzers

JT03471456

OFDE

This document, as well as any data and map included herein, are without prejudice to the status of or sovereignty over any territory,

to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

2 DCD/DAC/STAT/RD(2021)1

Unclassified

Policy on harmonisation of coding of the financing

instrument UN inter-agency Pooled Funds between OECD-

DAC and UN data standards

Background

1. The United Nations (UN) system through the Secretariat of the UN Chief

Executives Board for Coordination (CEB Secretariat) is working with the Secretariat of the

Organisation for Economic Development and Cooperation’s Development Assistance

Committee (OECD-DAC) and the International Aid Transparency Initiative (IATI) on the

harmonisation of code lists used for each of the six data standards for UN system-wide

reporting of financial data. This collaborative process started in 2017 during the

formulation of the UN data standards and has continued after the adoption of these

standards in late 2018. This policy relates to the harmonisation of code lists used for

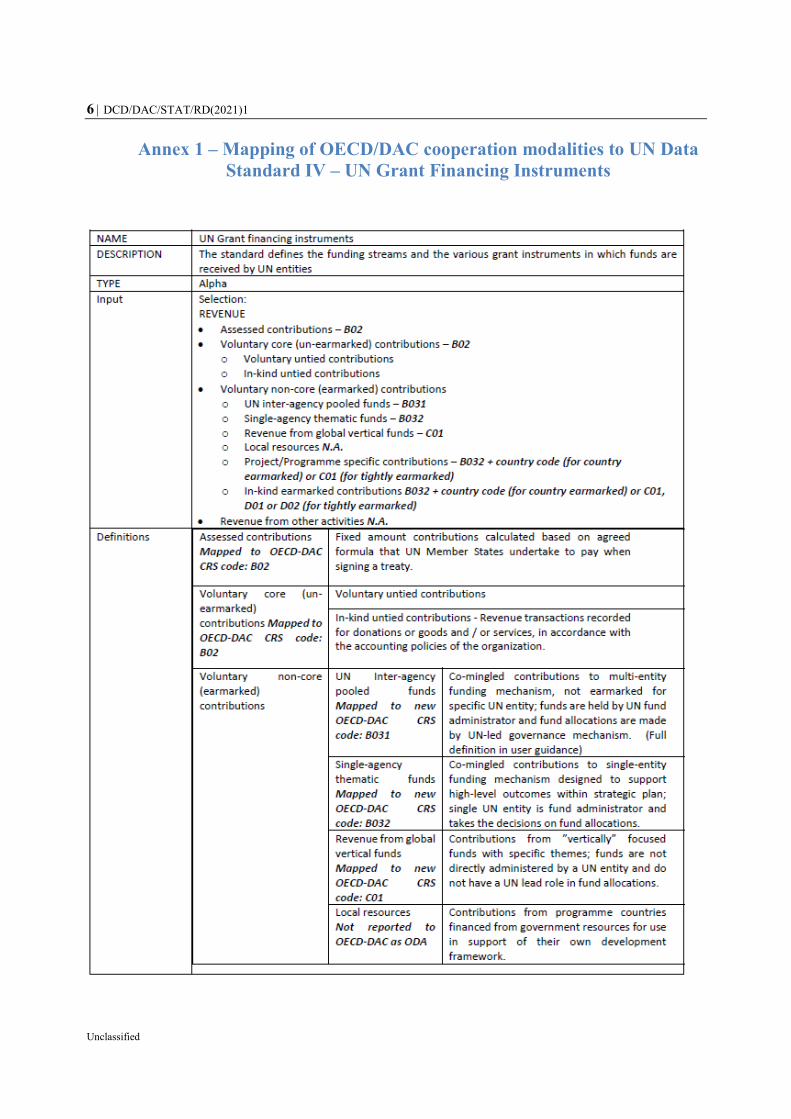

Standard IV: UN Grant financing instruments.

2. In August 2020, the OECD-DAC Working Party on Development Finance

Statistics (WP-STAT) adopted the ‘Revised Proposal on Refinements to the Type of

Aid/Cooperation Modality Classification’, taking effect in principle on 1 January 2021.

The proposal was developed in consultation with the UN Multi-Partner Trust Fund Office

(MPTF Office) and the CEB Secretariat, and contains a mapping of the revised OECD-

DAC cooperation modalities to the UN Grant financing instruments (see Annex 1).

3. In subsequent discussions in the WP-STAT, OECD Members raised questions on

the reporting on general contributions to some UN inter-agency pooled funds, that – in line

with the earlier OECD-DAC classification system and reporting directives – had until then

been classified as recipients of “core” and “multilateral” funding in the OECD-DAC

system. This was notably the case for the Central Emergency Response Fund (CERF) and

the Peacebuilding Fund. The OECD-DAC Secretariat requested the CEB Secretariat and

MPTF Office to provide a recommendation on those UN inter-agency pooled funds,

general/non-earmarked contributions to which could/should be considered as multilateral

in the OECD-DAC system.

4. This policy on harmonisation of coding of the financing instrument UN inter-

agency Pooled Funds between OECD-DAC and UN data standards outlines the criteria that

DCD/DAC/STAT/RD(2021)1 3

Unclassified

individual UN pooled funds have to fulfil in order for the UN through the CEB Secretariat

to recommend to the OECD-DAC to classify them as ‘multilateral’ in the OECD-DAC

reporting system. The draft policy was prepared by the CEB Secretariat in its capacity as

the data steward for the UN data standards and reviewed by OECD/DAC Secretariat, IATI,

Development Coordination Office (DCO) and MPTF Office; inputs have been integrated

into this final version, which will be shared with the OECD-DAC Secretariat in order to

prepare a response to the WP-STAT.

Principles guiding policy

1. CEB Secretariat’s role as data steward for UN Data Standards: As the data

steward, the CEB Secretariat is responsible for developing policies that require an

interpretation of the UN data standards and approving these policies after an

appropriate consultation process.

2. Compliance with UN Data Standards: This policy cannot change the UN data

standards and must be fully aligned with these standards.

3. Advancing harmonization of codes between OECD-IATI-CEB: This policy is

meant to be effective in advancing the harmonization of the separate code lists for

financial reporting maintained by OECD-DAC, IATI and the CEB Secretariat,

thereby enhancing the overall transparency in reporting on financial flows of the

United Nations and other development partners.

4. Clarity for all partners: The policy is formulated so that it can be used by a UN

and non-UN audience. In its application, it uses data sources that are in the public

domain.

5. Easy to implement: The policy is formulated such that it is easy to implement and

involves only a limited workload on the part of the CEB Secretariat.

Policy on harmonisation of coding of the financing instrument UN Pooled Funds

5. The CEB Secretariat recommends to the OECD-DAC that the classification as

‘multilateral’ in the OECD-DAC reporting system (see definition in the existing

OECD-DAC reporting directives in annex 2) of any unearmarked contribution to a

global UN inter-agency pooled fund be based on the specific criteria outlined below.

The criteria for ‘Multilateral Character’ of the fund are the following:

The fund has received contributions in the last four years from ten or more

contributors that are either UN Member States or the European Union (which is a

full member of the OECD-DAC)1;

A least 80 per cent of the total contributions to the fund received in the last four

year have originated from UN Member States and the European Union; and

1 The ‘multilateral character’ of the fund thus becomes “comparable” to the multilateral character of UN Funds and Programmes,

which are established by the General Assembly and normally receive core contributions from at least ten core contributors. The four-year period coincides with the duration of the period covered by the QCPR and of the strategic plans of many of the UNSDG members. The explicit reference to a specific global pooled fund in the UN system-wide financing architecture for humanitarian and/or development activities, such as in the context of the 2016 World Humanitarian Summit or the 2019 Funding Compact, is another element to consider.

4 DCD/DAC/STAT/RD(2021)1

Unclassified

The average annual contribution to the fund is above USD 25 million per year.

Thus, the total contributions to a given fund would surpass 100 million in a four

years period.2

The criteria for ‘Contribution Character’ are the following:

Only pooled funds that are global in nature, i.e. not geographically earmarked to a

country, group of countries or region, are considered for inclusion on the list.

The percentage of total contributions to the fund that are earmarked by contributors

(e.g. to a sector/theme within the fund) is less than 5 per cent;

None of contributors to the fund has contributed more than 50 per cent of total

contributions;

6. This policy will be applicable to all UN Pooled Funds irrespective of the UN Fund

Administrator / Administrative Agent.

Implementation of the Policy

1. Based on the policy and the analysis included in annex 3, the CEB Secretariat will

recommend to the OECD-DAC that the following four global UN Pooled Funds would be

classified as recipients of “multilateral” funding in the OECD-DAC system. Note that this

recommendation does not affect the classification of the revenue and expenditures of these

funds in the UN data standards under UN inter-agency pooled funds.

Central Emergency Response Fund (CERF)

Joint SDG Fund (new)

Peacebuilding Fund

UN COVID-19 Response and Recovery Fund (new)

2. In practice, the multilateral character of the contribution could be identified through the

bi_multi code 2 (it is recommended that the co-operation modality would remain B031 for

all UN pooled funds in line with the definition approved by WP-STAT members and the

classification of UN pooled funds as a separate UN grant financing instrument as per the

UN data standards).

3. Moreover, the CEB Secretariat will commit to the OECD-DAC to provide an annual

update, if any, of this list by 31 January of a given calendar year.

4. For UN Fund Administrators that consider that (an) additional UN Pooled Fund(s) they

administer should be included in the list, they should send a request to that effect to the

CEB Secretariat with a copy to DCO by 10 January of a given calendar year,

complemented with a justification of the request in line with this policy.

7. The UN Fund Administrator for the two pooled funds now recommended to be

added to the list of global UN Pooled Funds considered as ‘multilateral’ by OECD-DAC

will commit to provide the requested annual reporting to the OECD-DAC on the outflows

2 This is roughly the level of overall 2018 revenue of some of the smallest UN organisations such as UN World Tourism

Organisation (UNWTO) and the UN Institute for Training and research (UNITAR).

DCD/DAC/STAT/RD(2021)1 5

Unclassified

from these two pooled funds. This is similar to the reporting currently already being done

for the CERF and the Peacebuilding Fund.

8. Reference to this policy will be included in the UN data standards under FAQ

during the annual update of the data standards, but only after its application has been

approved at the level of OECD-DAC and integrated in the OECD-DAC reporting

directives.

9. The CEB Secretariat will review and update – if needed - this policy once per year

in January, to coincide with the annual review and update op the UN data standards.

Other issues

10. While preparing this policy, the CEB Secretariat has also reflected on other areas

in which further alignment between OECD-DAC channel codes and the UN data standards

is deemed useful. One area concerned some programmes that are named “trust funds” in

the UN-system financial context and have a separate OECD-DAC channel code, and that

are not classified by the UN system as either “UN inter-agency pooled fund” or “UN single-

agency thematic funds”. These “trust fund” are now listed in the parent category 41600

“Existing UN channels not included in Standard I - UN entity - of the UN Data Cube

reporting framework” based on the parent categories agreed at the WP-STAT December

2020 meeting.

11. The CEB Secretariat identified the respective UN entities, as per UN data standards,

that host these trust funds, and suggested that the link between the “trust fund” and UN

entity is clearly spelled out in the OECD-DAC reporting system. This suggestion has been

taken over and, as a result e.g., the United Nations Voluntary Fund for Victims of Torture

will now be indicated as being a sub entity of the United Nations High Commissioner for

Human Rights (OHCHR) in the notes column of the channel code classification.

12. Further, the CEB Secretariat has suggested that the “trust funds” classified as being

sub-entities in category 41600 are classified as B032 or B033 in terms of the OECD-DAC

co-operation modality; apart from the Montreal Protocol, they do not comply with the

criteria for being B031, but neither are they project-type interventions.

13. Moreover, a quick analysis was undertaken to see if these “trust funds” would

comply with key eligibility criteria for multilateral as described above for UN pooled funds.

The CEB Secretariat notes that all but two3 of the channels that will be listed under parent

code 41600 did not meet the “average annual contribution” criterium of USD 25 million

per year. With the exception of the Montreal Protocol and the United Nations Mine Action

Service (UNMAS), the total contributions to these “UN sub-entities” listed in 41600 is

estimated to be around the same magnitude or less than the total annual contributions of

the two UN pooled funds that have been recommended above to be classified as multilateral

aid.

3 The Montreal Protocol and UNMAS would meet the three criteria mentioned above for

“multilateral character” based on the information available on

http://www.multilateralfund.org/85/English/1/8503.pdf and https://unmas.org/en/how-we-are-

funded.

6 DCD/DAC/STAT/RD(2021)1

Unclassified

Annex 1 – Mapping of OECD/DAC cooperation modalities to UN Data

Standard IV – UN Grant Financing Instruments

DCD/DAC/STAT/RD(2021)1 7

Unclassified

Annex 2 - Existing OECD-DAC reporting directives

14. The definition of a multilateral contribution in the OECD-DAC Reporting

[DCD/DAC/STAT(2018)9] is as follows:

15. “17.” The definition of a multilateral contribution is based on two criteria: the

multilateral character of the recipient institution and the multilateral character of the

contribution. Donors’ contributions that satisfy both criteria by meeting the following tests

should be recorded under the heading "multilateral":

a) the recipient institution conducts all or part of its activities in favour of development

and developing countries; and

b) the recipient institution i) is an international agency, institution or organisation whose

members are governments, who are represented at the highest decision-taking level by

persons acting in an official capacity and not as individuals; or ii) is a fund managed

autonomously by a multilateral agency as defined in i); and

c) funds are pooled so that they lose their identity and become an integral part of the

recipient institution’s financial assets.

16. [Conditions a) and b) define the multilateral character of the agency. Condition c)

is a test of the multilateral character of the contribution.]

17. “18.” If it is not immediately clear whether funds provided to a multilateral

organisation can be considered as pooled, determination is made on the basis of the degree

of control over the disposal of the funds contributed. If, on scrutiny, it is found that the

donor country has maintained control over its contributions to such an extent that the

decisions regarding disposal of the funds are on balance taken at the donor’s discretion, the

flows concerned should be recorded as bilateral (these contributions are often referred to

as “multi-bi” or “earmarked” contributions). The relevant criteria are the extent to which

the donor country rather than the recipient institution specifies some or all of the following:

the recipient to which the funds will be granted or lent (particular emphasis is

placed on this criterion);

the project and purpose for which the funds are to be used;

the amount provided and its terms;

in the case of loans, the re-utilisation of amortisation and interest received.”

8 DCD/DAC/STAT/RD(2021)1

Unclassified

Annex 3 – Application of the proposed policy to global UN Pooled

Funds

UN Pooled Fund Name (only Funds with

contributions in 2019)

Administrative

Agent (UN Entity)

10 or more UN MS

or EU contributors

UN MS and EU > 80

% contributions

Average 2019-2020

contribution > 25 mill.

% of contributions

earmarked < 5 %

none of contributors

contribute > 50 %

Antimicrobial Resistance MPTF MPTF-O yes yes

ConflictRelatedSexualViolence MPTF-O yes yes yes

Counter Piracy Trust Fund MPTF-O yes yes

Elsie Initiative Fund MPTF-O yes yes

Financing Strategy 2030 Agenda MPTF-O yes yes

Human Rights Mainstreaming TF MPTF-O yes yes

Joint SDG Fund MPTF-O yes yes yes yes yes

Migration MPTF MPTF-O yes yes

One Planet MPTF MPTF-O yes yes

Partnership Act. on Green Econ MPTF-O yes yes

Peacebuilding Fund MPTF-O yes yes yes yes yes

Rural Women Economic Empowermt MPTF-O yes yes

SDG Fund MPTF-O yes yes

Spotlight Initiative Fund MPTF-O yes yes

The Lions Share Fund MPTF-O yes

UN REDD Programme Fund MPTF-O yes yes

UN Road Safety Trust Fund MPTF-O yes yes

UNITLIFE Trust Fund MPTF-O yes yes

UNPRPD Disability Fund MPTF-O yes yes yes

Womens Peace & Humanitarian TF MPTF-O yes yes

Working for Health MPTF MPTF-O yes yes

Central Emergency Response Fund (CERF)** OCHA yes yes yes yes yes

UN-Water Inter-Agency Trust Fund ** UNOPS yes ?

yes

UN Pooled Fund Name (Funds with MPTFO as AA,

established & capitalised in 2020)

Administrative

Agent (UN Entity)

10 or more UN MS

or EU contributors

UN MS and EU > 80

% contributions

2020 contribution > 25

mill.

% of contributions

earmarked < 15 %

non of contributors

contribute > 50 %

Generation Unlimited Trust Fd MPTF-O yes

Global Fund for Coral Reefs MPTF-O yes

UN COVID-19 Response & Recover MPTF-O yes yes yes yes yes

Note: Funds with (*) have a separate OECD/DAC CRS channel code, and their code is used instead of the channel of the administrative agent in OECD/DAC reporting

Note: Funds with ** were assessed using UN Pooled Funds database (for 2017-2019) and cerf.un.org/our-donors/contributions (for 2020); others were assessed using mptf.undp.org

CONTRIBUTIONS CHARACTER MULTILATERAL CHARACTERGlobal UN inter-agency Pooled Funds