d i p l om a i n bookkeeping - content.upskillist.com

TRANSCRIPT

BOOKKEEPINGD I P L O M A I N

Lesson 6: Cash payments

The purchases cycle

Lesson 6

Types of payments

Petty cash

Cash payments journal

Practical examples

Lesson Objectives

Lesson 5 review

CRJ

Types of revenue

Receipts cycle

Receipting cycle

Order Delivery PayBilling

Types of revenue

GoodsServices

InterestDividends

Operating Non-operating

Layout of the CRJ

CRJ-01

Debit

Date Invoice Description Amount Account Reference Accounts Receivable Cash Other

Credit

CASH RECEIPTS JOURNAL

Expenditure Cycle

Importance of the cash cycles

• Critical for operations

• Spending as important asincoming cash

• Policies and procedures

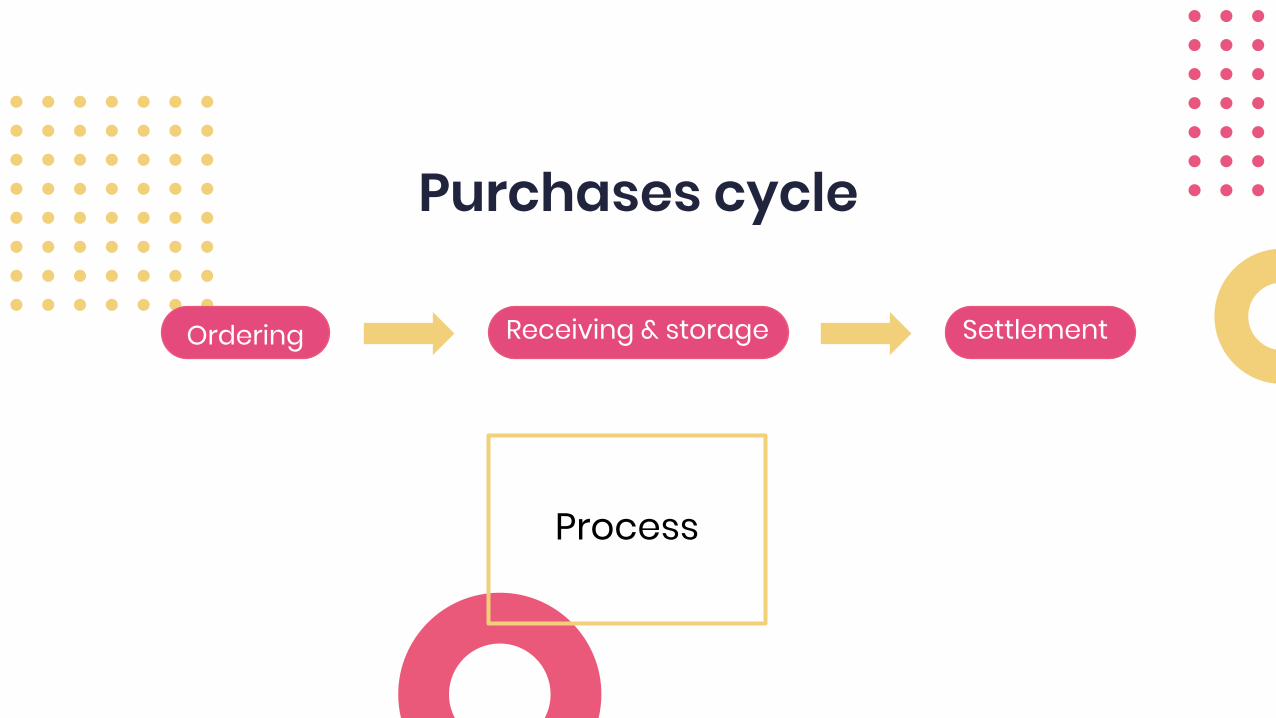

Purchases cycle

Process

Ordering Receiving & storage Settlement

1. OrderingInternal/external request

Item

Quantity

Price

2. Receiving• Compare to order

• Check quality

• Add to a list

• Receive invoice

3. SettlementCash payment

Returns

Other adjustments

Record entry

Supporting documents

• Purchase requisition

• Purchase order

• Goods received

• Invoice

• Statement

Accounts impacted• Expenses (I/S)

• Assets (B/S)

• Bank (B/S)

• Payables (B/S)

Master listsSuppliers master listing

Preferred vendor listing

Preferred vendors• Best price

• Best quality

• Discounts

• Payment terms

Process

Generate purchase order

Receive invoice

Purchases journal

Generate disbursement

Impact CPJ

Need to order items Delivery of goods Billing Settlement

There are three key steps in the purchases cycle.

TRUE

Expenditure Types

Cycles impacted• Inventory

• Equipment and supplies

• Logistics

• Capital purchases

• Services

• Operating items

• Once-off

StandardBlanketContractPlanned

Purchases orders

Petty cash

• For purchases where the bankcharges would be an unnecessaryexpense

• Immaterial amount of cash onhand for smaller purchases

• Unplanned expenditure

Petty cash

• Physical cash in a lockedbox

• Cash card

• Controls around petty cash

z

Petty cash

• Imprest system

• General ledger

• Petty cash vouchers

• Log

• Reconciliations

• Receipts recorded asexpenses

Examples

• Printer ink

• Postage

• Office supplies or stationery

• Coffee and tea

• Fuel and parking

• Reimbursements

1. Transfer funds from bankaccount to petty cash account

2. Log disbursements andreimbursements

3. Capture receipts as expenses4. Prepare reconciliation5. Top-up petty cash account

Process

You can use petty cash to purchase a few pens for the office.

TRUE

Cash Payments Journal

Settlement

• Receipt of goods creates legalobligation

• Payment upon receipt ofinvoice

CPJBook of first entry

Records all payments using cash

aka disbursements

• Purchases

• Suppliers

• Rent

• Salaries

• Insurance

Process

1. Capture sourcedocument

2. Updatesubsidiary ledger

3. Post to thegeneral ledger

Details

• Date

• Reference number

• Payee details

• Credit column

• Account debited

• Amounts

Layout

CPJ-01

Credit

Date Disbursement Description Amount Account Reference Accounts Payable Purchases Other

Debit

CASH PAYMENTS JOURNAL

Other considerations• Tax

• Differs from country to countryand state to state

• Paid to vendor

• Reduce tax liability to be paid overto the revenue service

You can record purchases made on credit in the CPJ.

FALSE

ChallengeCreate the general journals for

the transactions shown in the

cash payments example.