cutting costs and increasing profits indaba 2014 presented by: hylton long date: 9 may 2014 © 2009...

TRANSCRIPT

CUTTING COSTS AND INCREASING PROFITS

INDABA 2014

Presented by: Hylton Long

Date: 9 May 2014

© 2009 Tourism Enterprise Partnership. All Rights Reserved

Introduction

• …”…”If the economy in general has a positive attitude towards entrepreneurship, this can generate cultural and social support, financial and business assistance and networking benefits that will encourage and facilitate potential and existing entrepreneurs.”

2012 GEM Global Report

Introduction

The South African economy has escaped much of the financial disasters experienced in the global economy. This can be attributed to the financial controls instituted by government e.g. FICA Act, Consumer Protection Act.

However another big challenge facing small business owners is their lack of financial responsibility in their business and their lack of understanding financial terminology especially wrt budgets and controlling expenses.

FactsFacts

• Primary objective of a small business is to “make a profit”.

• This is achieved through:

- best utilisation of resources

- healthy cash flow position & effective cash flow management

- effective budget system

- best loan conditions and interest rates

FactsFacts

• Very few people in business maintain financial records on a daily or monthly basis

• Very few businesses are aware of their cash flow situation at given times

• Most businesses fail because of the lack of management accounts (financial statements) and cannot access additional finance (loans) without these accounts

FactsFacts

• The majority of businesses have their management accounts (financial statements) done once at the end of the financial year which in most instances is too late to carry out a business rescue.

• The majority of businesses do not know or understand the management accounts drawn up by their Accountant and neither do they question them.

• The majority of businesses do not sit down with their Accountant and discuss their financials in detail with their Accountant.

Facts

• Very few business owners understand accounting terminology. In some instances they do not know what a debit or a credit is, cashbook, general ledger, cashflow statement, Cost of Sales.

• Very few business owners apply basic financial ratios to assist them in analysing their business.

• Very few business owners draw up an annual budget and measure performance against this budget

Why Keep Financial Records

• Enable’s owner to monitor financial position• Management of cash flow• Basis for decision making• Basis for projections for future income and

expenses• Potential investors/ buyers should we want to

sell. Gives us proof of the following:• - Proof of income• - Proof of net assets

Why Keep Financial Records

• Suppliers of goods, services and finance• - Evaluate credit risk• - Evaluate ability to pay when applying for finance

• SARS• - Legal right to examine records (Income Tax Act and

VAT Act)

Some Financial activities in a small business that are neglected or very little attention paid to include the following:•Budgets;•Cash flow management;•Record-keeping of all financial transactions and their results (invoices and expenses);•Controlling expenses;•Internal controls;•Analysis of financial statements (financial position of the business);

Neglected Financial Activities in a BusinessNeglected Financial Activities in a Business

Budgets

A complete budget that relates to the objectives of a particular business enhances the decision-making process and has the following uses:•It serves as a planning aid, and its compilation virtually always leads to refinement of the short-term plans.

•Budgets are an indispensable means of control and assist in cutting costs.

Budgets

• It serves as a means of conveying policy to subordinates who are responsible for implementing policy-specific guidelines.

• It is an instruction to subordinates and delegates the authority needed for them to act.

• Performance can be measured.• Goal orientation

Budgets

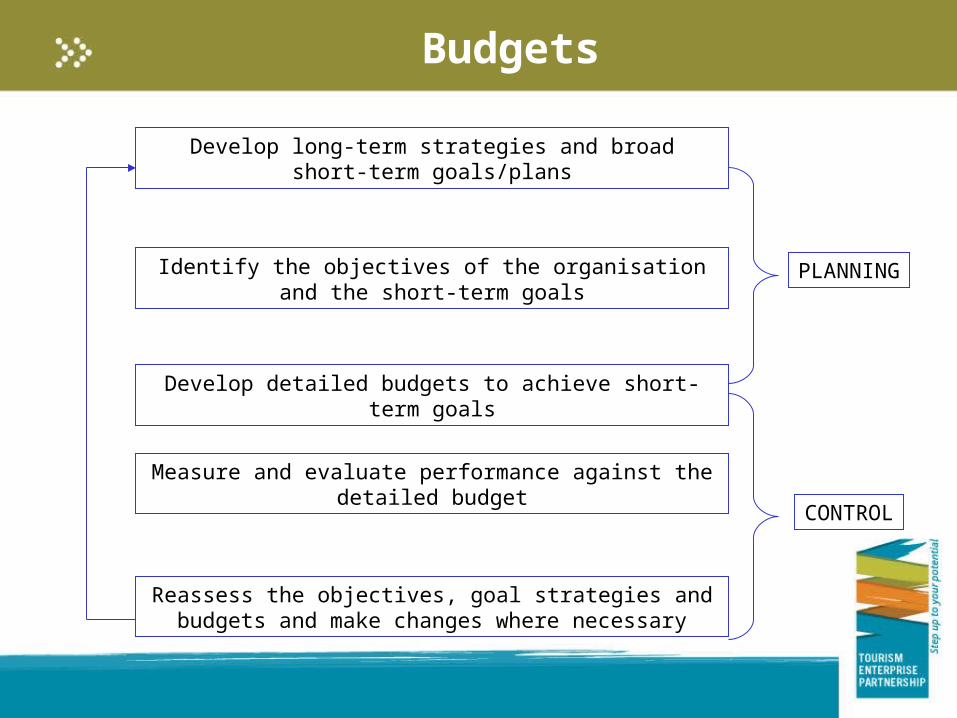

Develop long-term strategies and broad short-term goals/plans

Identify the objectives of the organisation and the short-term goals

Develop detailed budgets to achieve short-term goals

Measure and evaluate performance against the detailed budget

Reassess the objectives, goal strategies and budgets and make changes where necessary

PLANNING

CONTROL

Steps In Drafting A Budget

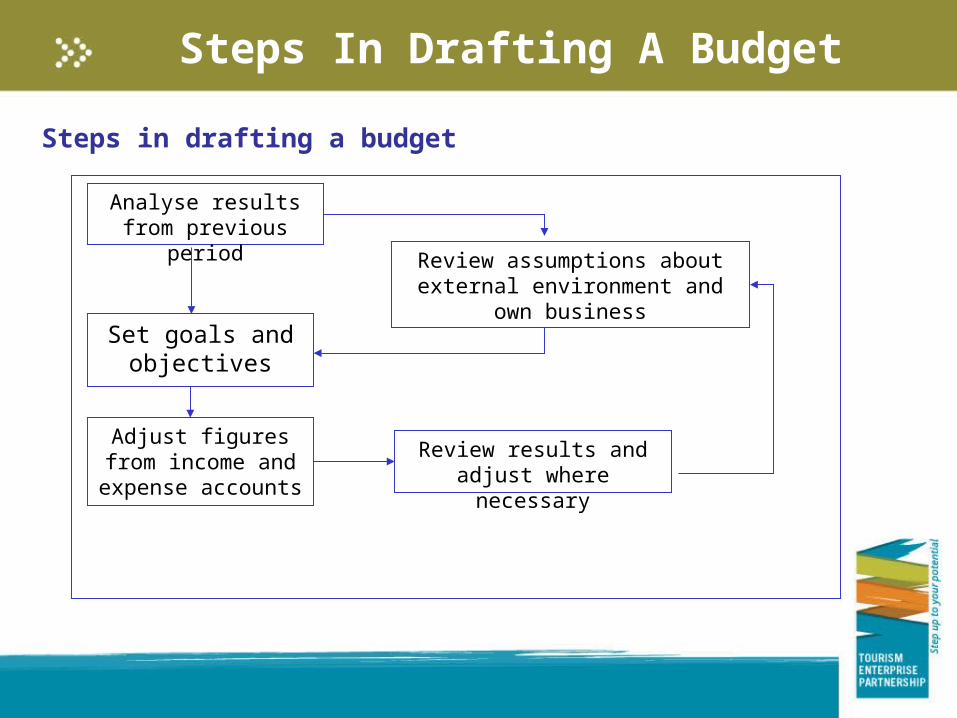

Steps in drafting a budget

Analyse results from previous period

Review assumptions about external environment and own business

Set goals and objectives

Adjust figures from income and expense

accounts

Review results and adjust where necessary

Cash Flow Management

Some Basic Internal Controls…• Trust nobody with cash!!• Bank all cash takings intact• Deposit takings every day• Physically secure inventory• Check bank statement yourself• Pay only on sight of original suppliers invoice• Check arithmetical accuracy of all documents• Open the post yourself

Managing cash flow

• Cash book that is regularly balanced – minimum monthly• Reconcile with bank statement – outstanding cheques,

debit orders that will still come off the bank• Know what you have sold and when you should receive

the cash• Monitor creditor purchases and payments• Plan in advance for month-end payments• Never issue a cheque unless there is adequate funds to

cover• Prioritise debt collection

Impact of poor cash management

• Inability to pay creditors on time [impacts on relationship, interest charges, penalties]

• Overdraft facilities used [increased interest payments]

• Employee dissatisfaction if salaries not paid on time

• R/D cheques, unpaid debit orders [poor relationship with bank]

Managing Debt

Some questions to ask about your clients debtors management

• Do your customers buy on credit?• Do you know how long they usually take to pay?• Do you know how much money is currently owed to your

business?• Do you keep a record of debtors• Have you been owed money for more than a year• Do you keep a record of overdue accounts

• What is your level of bad debts?

Credit policy – Key questions

Can the business answer the following• Will we sell on credit• What percentage of total sales should be on credit• Will there be a selling price differential – cash discount• How will clients qualify for credit• Who will assess the applications• What will the conditions be• How will the debtors accounts be managed

Controlling Expenses

During these challenging economic times, managing expenses has increasingly become a priority for many small-business owners. When reviewing your expenses, consider the following:•Watch expenses from day one.•Don’t confuse business and personal expenses.•Keep detailed and accurate purchasing records.•Run reports early and often•Continue financial responsibility.•Look at cutting down on expenses

.

Responsible Lending

We all know that small business lending is down. Still, despite the lending challenges facing small business owners, there are still loans being approved and, although it’s never easy nowadays, qualified small business owners are getting approved for many different forms of financing to start, build and grow their businesses.

Responsible Lending

Some of the aspects a business owner must be aware of when borrowing money for the business:•Remember you will have to supply collateral - Can you borrow the money you need without pledging any collateral to the bank? - What is a reasonable collateral request based on the

loan you’re requesting? .

Responsible Lending

• Not Being Committed to Maintaining (or improving) your Personal Credit

Although bank financing is challenging to get, it’s always going to be the cheapest form of funding your business. There are “alternative” financing options galore but it should always be your goal to get your business to be “bankable.” In other words, you want to be able to obtain your loans and lines of credit from a registered financial institution e.g. SEFA, IDC, Banks who

Are their to assist small businesses.

Responsible Lending

• Not Knowing the Impact of Your Loan on Your Budget and Cash Flow

- What impact does the loan have on your Budget? There are two important factors

here:

Use the funding you obtain for RGA (revenue-generating activities).

Keep in mind that cash flow is usually more important than interest rates i.e. if you can extend a loan period in exchange for a little higher interest rate, consider what lower payments mean to cash flow.

Responsible Lending

• Choosing the Wrong Loan for Your Purpose

Do you need a loan or a line of credit? Based on your credit, business, industry, collateral, revenue, profit, etc., do you know what your borrowing options are? If you understand what your options are, you can choose the loan solution that’s best for you.

Responsible Lending

So the questions each business owner must ask themselves when taking on debt is:•Explore your reasons for borrowing•Plan effectively•Examine short-term vs. long-term debt•Base new debt on current needs

By applying these simple questions you will ensure that when you lend money you have taken all aspects into consideration and will be able to meet your monthly commitments.

Financial Ratios Analysis

• Management Accounts is not just about preparing financial statements it also entails being able to interpret these financial statements.

• How do we do this? By applying various financial ratios. These ratios will highlight any serious problems relating to your business from a cash flow perspective.

• Speak to your Accountant and let him explain these ratios to you as they can help you in cutting costs and increasing profits.

Types of Financial Ratios

• Liquidity Ratios- Used to determine the company's ability to pay off its short term debt. Some examples

• Profitability Ratios- Used to determine average mark-up %, average Gross Profit % and Net Profit Margin %

• Efficiency Ratios

- Used to calculate average debtors collection period and average creditors payment period. Also used to determine average stock

Financial Resolutions

Just like individuals draw up a list of New Year’s resolutions to steer their life in a desired direction, the small business owner should jot down resolutions that’ll make for a successful financial year. But where to start? With the basics of course. Here are 4 financial resolutions to start with:•I will draw up a realistic budget•I will manage the cash flow better•I will assess all expenses•I will reduce my personal spending

Closure

In closing being financially responsible is crucial as you advance your business. When you address these financial responsibilities, discussed briefly today, for small businesses, you will be rewarded with financial flexibility as you grow the company.

You need to be in control of your income and expenses and apply all possible methods to ensure you control your costs thereby increasing profits

Thank you

© 2009 Tourism Enterprise Partnership. All Rights Reserved