customer-base concentration: implications for firm ... concentration: implications for firm...

TRANSCRIPT

Customer-base concentration:

Implications for firm performance and capital markets

Panos N. Patatoukas

Yale School of Management

Email: [email protected]

Tel: (203) 606-3740

This version: January 17, 2010

I gratefully acknowledge the guidance and encouragement from my dissertation committee

members: Brian Mittendorf, Shyam Sunder, Jake Thomas (Chair), and Frank Zhang. I also wish

to thank Rick Antle, Judith Chevalier, Ravi Dhar, Merle Ederhof, Alon Eizenberg, Roger

Ibbotson, Bige Kahraman, Myrto Kalouptsidi, Sang-Hyun Kim, Kalin Kolev, Stefan Lewellen,

Steven Malliaris, Nikolay Osadchiy, Philip Ostromogolsky, Ankur Pareek, Heather Tookes, Ari

Yezegel, Roy Zuckerman, and seminar participants at Yale School of Management, Athens

University of Economics & Business, the 9th

Trans-Atlantic Doctoral Conference at the London

Business School, the 6th

Accounting Research Workshop at the University of Bern, and the 2009

American Accounting Association Northeast Regional Meeting for their comments on earlier

versions. This paper is the recipient of the 2009 American Accounting Association Northeast

Region Best PhD Student Paper Award.

2

Customer-base concentration:

Implications for firm performance and capital markets

Abstract

In this paper, I examine whether and how customer-base concentration affects supplier firm

performance and stock market valuation. To this end, I compile a comprehensive sample of

supply chain relationships and introduce a measure, labeled CC, to capture the extent to which a

supplier‟s customer base is concentrated. In contrast to the conventional view of customer-base

concentration as an impediment to firm profitability, I document a positive contemporaneous

association between CC and accounting rates of return, which suggests that efficiencies accrue to

suppliers with concentrated customer bases. Consistent with a cause-and-effect link between

customer-base concentration and firm performance, analysis of intertemporal changes

demonstrates that CC increases predict efficiency gains in the form of reduced operating

expenses per dollar of sales and enhanced asset utilization. Using stock returns tests, however, I

find that investors systematically underreact to the implications of changes in customer-base

concentration for future firm fundamentals when setting stock prices. Over the thirty-year sample

period studied, a zero-investment trading strategy that exploits investors‟ underreaction yields

abnormal returns in the region of 10 percent per year.

Keywords: Customer-base concentration; DuPont profitability analysis; market efficiency.

JEL classification codes: M41; L25; G14.

3

1. Introduction

Relationships with major customers are conventionally considered to be an impediment

to supplier firm profitability. Reportedly, major customers pressure their dependent suppliers to

provide concessions such as lowering prices, extending trade credit, accelerating delivery times,

and carrying extra inventory. The popular press often highlights the “evils” of customer-base

concentration by reference to the case of Wal-Mart and its history of squeezing out every last

penny from its dependent suppliers (e.g., PBS Frontline 2004). However, research on

relationship marketing and operations management suggests that suppliers to major customers

may be able to achieve efficiencies in the form of decreased selling and administrative expenses,

and enhanced product distribution (e.g., Jackson 1985; Cowley 1988; Kalwani and Narayandas

1995). In addition, major customer relationships can foster information sharing along the supply

chain and help supplier firms streamline production and enhance working capital management

(e.g., Kalwani and Narayandas 1995; Kinney and Wempe 2002).

In this paper, I examine whether and how customer-base concentration affects supplier

firm performance and stock market valuation. To this end, I compile a comprehensive sample of

supply chain relationships in virtually all two-digit SIC industries over the thirty-year period

from 1977 to 2006, and introduce a measure to capture at the firm-year level the extent to which

a supplier‟s customer base is concentrated. My concentration measure, labeled CC, is an

application of the Herfindahl-Hirschman index and encompasses two elements of customer-base

diversification − namely, the number of major customers with which a supplier firm interacts and

the relative importance of each major customer in the firm‟s total revenue.

In contrast to the conventional view of major customer relationships, I find a positive

contemporaneous association between CC and accounting rates of return, which suggests that

4

suppliers with concentrated customer bases enjoy efficiencies. A detailed investigation of

operating performance drivers reveals that efficiencies accrue to more-concentrated suppliers in

the form of cost savings and enhanced working capital management. Specifically, more-

concentrated suppliers spend less on selling, general, and, administrative (SG&A) expenses per

dollar of sales, hold less inventory as a fraction of total assets, and experience higher inventory

turnover, as well as shorter cash conversion cycles. Accordingly, although more-concentrated

suppliers report lower gross margins, they experience higher operating profit margins and asset

turnover and, on the whole, tend to be more profitable.

A causal link between customer-base structure and performance implies that changes in

customer-base concentration are associated with changes in supplier firm performance. Indeed,

potential efficiency gains achieved through enhanced production coordination and inventory

management, cooperative advertising campaigns and marketing alliances with major customers,

are likely to flow gradually through a supplier‟s financial reporting system. To help assess the

existence of a causal link, I investigate the lead-lag association between changes in firm

performance and changes in customer-base concentration (ΔCC). Consistent with a cause-and-

effect relationship, I find that ΔCC is a strong leading indicator of one-year-ahead changes in

profit margins, asset turnover, and overall firm profitability. In particular, I find that increases in

customer-base concentration are subsequently followed by efficiency gains in the form of

reduced operating expenses per dollar of sales and enhanced asset utilization.

In order to address concerns of a spurious correlation between ΔCC and subsequent

changes in firm performance, I implement a two-stage regression approach. In the first stage, I

remove the component of ΔCC that is correlated with measurable characteristics of not only the

supplier firm but also of the supplier firm‟s customer base − including market capitalization,

5

book-to-market ratio, age, sales growth, distress risk, the number of reported business segments,

and product market share and competitiveness. In the second stage, I regress one-year-ahead

changes in firm profitability on the residual portion of ΔCC which is by construction orthogonal

to the characteristics considered. I find that residual ΔCC is a strong predictor of subsequent

changes in firm profitability; therefore, the lead-lag association between changes in firm

performance and changes in customer-base concentration is robust to spurious correlations.

Naturally, the question that emerges is to what extent investors use the forward-looking

information embedded in customer-base changes when setting stock prices. To address this

question, I employ annual-window association tests and find a significantly positive relationship

between ΔCC and inter-announcement stock returns. Additional analysis shows that ΔCC is

correlated with information not captured in reported accounting earnings and thus changes in

customer-base concentration are incrementally important in explaining stock returns.

Importantly, the positive sign of the association between ΔCC and contemporaneous stock

returns suggests that investors revise their beliefs and valuations in the direction of the

implications of customer-base changes for future firm performance. A related question is

whether investors are fully attentive to these implications when setting stock prices.

Bloomfield (2002) argues that limitations in investors‟ attention span can give rise to

stock market anomalies related to the forward-looking content of fundamental variables. The

setting examined here is no exception. Although stock prices react in year t to customer-base

concentration changes, future stock returns tests reveal that stock prices continue to drift over the

subsequent year in the direction of the initial change. An annual trading strategy that exploits this

pattern yields abnormal returns in the region of 10% per year. Multivariate regression analysis

6

further demonstrates that the predictive power of ΔCC is separate from that of previously

identified predictors of the cross-section of stock returns.

A thorough examination of alternative explanations makes it hard to reconcile stock-

return predictability based on ΔCC with the pricing of risk in efficient markets. In fact, the

evidence suggests that a plausible explanation is mispricing caused by investors‟ systematic

underreaction to the implications of changes in customer-base concentration for future firm

fundamentals. Consistent with this type of underreaction, I find that a disproportionate fraction

of the effect is clustered around subsequent earnings announcements dates. In addition, I

document that stock-return predictability tends to be stronger among firms that are a priori more

likely to be mispriced (e.g., firms with low analyst coverage and low institutional ownership).

The findings reported here have the potential not only to inform but also to redirect the

ongoing debate on the impact of major customers on supplier firm performance. This is the first

study to provide large-sample evidence on the association of customer-base concentration with

supplier performance at the firm level. This is also the first study to exploit the dynamics of

supplier firms‟ customer bases and implement lead-lag analyses that mitigate limitations inherent

in association tests of contemporaneous levels. My study not only establishes an important link

between customer-base structure and firm performance but also provides evidence of how

changes in customer-base structure lead subsequent changes in firm performance.

Overall, the evidence validates the relevance of disaggregated revenue disclosures for

financial statement analysis by demonstrating an economically important and statistically

significant link between customer-base concentration, firm fundamentals, and stock returns.

Accordingly, my study contributes to research on inter-organizational relationships and

intangibles as sources of firm value (e.g., Amir and Lev 1996; Lev 2001; Gosman, Kelly,

7

Olsson, and Warfield 2004). My findings also add to the growing evidence that investors

sometimes underreact to the forward-looking content of fundamental variables (e.g., Bernard and

Thomas 1990; Sloan 1996) and to the evolving literature on investors‟ limited attention to inter-

firm links (e.g., Menzly and Ozbas 2006; Cohen and Frazzini 2008).1 Finally, the inferences

drawn may be of interest to accounting standard setters who are currently considering ways to

revise the presentation of financial statements so as to provide improved disaggregated

information about firms‟ operations.2

The rest of the paper is organized as follows. Section 2 reviews related literature and

motivates the research questions. Section 3 describes the sample and provides descriptive

statistics. Section 4 examines the empirical link between customer-base concentration and firm

performance. Section 5 probes into the capital market implications of customer-base

concentration. Section 6 concludes and outlines directions for future research.

2. Background and research questions

The conventional view of customer-base concentration as an impediment to firm

performance can be traced at least as far back as the ideas of John Kenneth Galbraith on relative

bargaining power. In particular, J. K. Galbraith (1952) proposes that an important tactic in the

exercise of power consists in keeping the supplier in a state of uncertainty as to the intentions of

a major customer. The argument is that major customers often place orders around which the

production and investment of suppliers with concentrated customer bases become organized. A

1 Prior accounting research demonstrates that investors are not fully attentive to the forward-looking information

embedded in several fundamental variables, most notably earnings (e.g., Bernard and Thomas 1990) and earnings

components (e.g., Sloan 1996). Menzly and Ozbas (2006) use upstream and downstream definitions of industries

and present evidence of cross-industry price momentum. Similarly, Cohen and Frazzini (2008) find that the monthly

strategy of buying/selling firms whose customers had the most positive/negative returns in the previous month yields

abnormal returns, and argue that predictability is driven by investors‟ limited attention to inter-firm relations.

2 The latest updates regarding the joint project of the IASB and the FASB on “Financial Statement Presentation” can

be found at http://www.fasb.org/financial_statement_presentation.shtml.

8

shift in this practice imposes prompt and heavy losses, and thus the threat or even the fear of this

sanction is enough to provide customers with considerable bargaining power over transaction

prices and trade credit terms (Scherer 1970). In this spirit, Porter (1974) argues that “where

retailer power is high, the manufacturer's rate of return will be bargained down, ceteris paribus.”

Early research emphasizes the impact of customer power on supplier gross margins and,

consistent with the view that major customers exercise power vis-à-vis their relatively weaker

suppliers, finds that industry-level measures of customer bargaining power are associated with

lower supplier-industry gross margins (e.g., Lustgarten 1975; LaFrance 1979; Ravenscraft 1983).

However, Newmark (1989) shows that results of prior industry-level studies are misleading due

to measurement error in industry-level price-cost margins. Research extending the investigation

from the industry level to the firm level has also produced mixed results. To illustrate, on the one

hand, Galbraith and Stiles (1983) examine a sample of strategic business units of manufacturers

in the PIMS database and find that suppliers with diffused customer bases are associated with

higher operating profit margins. On the other hand, Kalwani and Narayandas (1995) report

higher levels of return on investment for a sample of 76 manufacturers in long-term relationships

with major customers.

These mixed findings have sparked an ongoing debate about the impact of customer

power on supplier profitability and, in fact, some argue that efficiencies may accrue to suppliers

with concentrated customer bases. In line with this argument, casual observation and academic

research in marketing and operations management suggest that increased customer-base

concentration may provide supplier firms with benefits, such as decreased cost of sales and

enhanced product distribution.3

3 As a real-life example, consider the case of Hasbro, Inc., one of the largest toy makers in the world. Hasbro

disclosed in its 2006 Annual Report the following information related to its customer base: “During 2006, sales to

9

For example, Jackson (1985) discusses how suppliers may be able to exploit their major

customers‟ reputations and brand names and use them as showcase accounts to attract other

customers. Cowley (1988) examines a sample of strategic business units in the PIMS database

for the years 1973-1976 and finds that selling and advertising costs tend to be lower when there

are fewer major customers to service. More recently, Kalwani and Narayandas (1995) propose

that manufacturers in long-term relationships with major customers are able to achieve cost

reductions in their SG&A expenses due to lower service costs, higher repeat sales and cross-

selling opportunities, and higher overall effectiveness of selling expenditures. In a similar vein,

Matsumura and Schloetzer (2009) argue that apparel industry suppliers can achieve cost savings

by engaging in collaborative marketing campaigns with their major customers.

A related stream of research in marketing and operations management proposes that

suppliers with concentrated customer bases can achieve enhancements in their working capital

management due to increased information sharing and improved production coordination along

the supply chain. In turn, increased production coordination can help concentrated suppliers

mitigate distortions common to supply chains (e.g., the bullwhip effect), reduce redesign costs,

and avoid delays in product development.4 Along these lines, recent empirical research provides

small-sample evidence that customer-supplier collaboration improves upstream inventory

management. Notably, Kalwani and Narayandas (1995) find that 76 manufacturers in long-term

relationships with major customers are able to reduce inventory holding and control costs.

our three largest customers, Wal-Mart Stores, Inc., Target Corporation, and Toys „R Us, Inc., represented 24%,

13%, and 11%, respectively, of consolidated net revenues, and sales to our top five customers accounted for

approximately 53% of our consolidated net revenues. While the consolidation of our customer base may provide

certain benefits to us, such as potentially more efficient product distribution and other decreased costs of sales and

distribution, increased customer concentration could also negatively impact our ability to negotiate higher sales

prices for our products and could result in lower gross margins than would otherwise be obtained if there were less

consolidation among our customers.”

4 The bullwhip effect (also known as “whiplash” or “whipsaw” effect) refers to the phenomenon where orders to the

supplier tend to have larger variance than sales to the customer (Lee, Padmanabhan, and Whang 1997).

10

Similarly, Matsumura and Schloetzer (2009) find enhanced inventory management capabilities

for a sample of 56 apparel industry suppliers with major customers. Case studies also illustrate

that partnerships between suppliers and their trusted major customers accelerate the deployment

of sophisticated procurement systems such as just-in-time (JIT) delivery (Kumar 1996).5

In summary, the results of industry-level studies are inconclusive, while those of firm-

level studies may not generalize to more representative samples, across industries, and over time.

Hence, the moment is ripe for an in-depth, large-sample study on the implications of customer-

base concentration for supplier firm performance. To this end, I compile a comprehensive

sample of 47,396 annual supplier-customer relations in virtually all two-digit SIC industries from

1977 to 2006, and introduce a measure to capture at the firm-year level the extent to which a

supplier‟s customer base is concentrated.

Specifically, the primary explanatory variable introduced in this study is firm i‟s

customer concentration (CC) in year t measured across the firm‟s J major customers, as

described below:

𝐶𝐶𝑖𝑡 = 𝑆𝑎𝑙𝑒𝑠𝑖𝑗 𝑡

𝑆𝑎𝑙𝑒𝑠𝑖𝑡

2𝐽

𝑗=1

(1)

where 𝑆𝑎𝑙𝑒𝑠𝑖𝑗𝑡 represents firm i‟s sales to major customer j in year t, and 𝑆𝑎𝑙𝑒𝑠𝑖𝑡 represents firm

i‟s total sales in year t. In essence, CC is an application of the Herfindahl-Hirschman index and

attempts to capture the extent to which a firm‟s customer base is more or less concentrated by

taking into account two elements of diversification: (i) the number of major customers with

5 Balakrishnan, Linsmeier, and Venkatachalam (1996) report for a sample of 46 JIT adopters that JIT-related

benefits (e.g., inventory turnover) are restricted to adopters with diffused customer bases (free adopters) and argue

that firms with concentrated customer bases (captive adopters) may be adopting JIT manufacturing to countervail

the adverse effects of price concessions to their major customers. However, Kinney and Wempe (2002), using an

extended sample of 201 JIT adopters, report no difference in the retention of JIT-related benefits across captive and

free adopters and argue that firms with concentrated customer bases enjoy lower downstream coordination costs.

11

which the firm interacts, and (ii) the relative importance of each major customer in the firm‟s

total revenue.6 The theoretical range of CC is between 0 and 1, where lower values correspond to

less concentrated customer bases and higher values correspond to more concentrated ones.

In the first part of my empirical analysis, I investigate whether and how efficiencies

accrue to suppliers with concentrated customer bases by testing the association of CC with

contemporaneous firm profitability and profitability drivers. However, contemporaneous

association tests provide little basis for inferring causality. To help assess whether a causal

relationship may exist between CC and firm performance, I investigate the lead-lag association

between changes in firm performance and changes in customer-base concentration (ΔCC). The

idea underlying the intertemporal analysis is that potential efficiency gains achieved through

enhanced production coordination and inventory management, cooperative advertising

campaigns and marketing alliances with major customers are likely to flow gradually through a

supplier‟s financial reporting system. Hence, a causal link between customer-base structure and

performance implies that changes in customer-base concentration are associated with subsequent

changes in supplier firm performance.

In the second part of my analysis, I investigate the extent to which investors incorporate

fundamental information embedded in ΔCC when setting stock prices. In the spirit of Ball and

Brown (1968), I examine the association between ΔCC and contemporaneous stock returns.

Establishing statistical significance would suggest that the information in ΔCC is correlated with

information that is value-relevant to stock market participants. In future returns tests, I set up a

6 The measurement of diversification is central to the empirical investigation of the implications of customer-base

concentration for firm performance. All results reported in this study are robust to the following alternative CC

measures: (i) 𝐶𝐶𝑖𝑡 =1

𝐽

𝑆𝑎𝑙𝑒𝑠 𝑖𝑗𝑡

𝑆𝑎𝑙𝑒𝑠 𝑖𝑡

𝐽𝑗=1 , and (ii) 𝐶𝐶𝑖𝑡 =

𝑆𝑎𝑙𝑒𝑠 𝑖𝑗𝑡

𝑆𝑎𝑙𝑒𝑠 𝑖𝑡

2𝐽𝑗=1

𝑆𝑎𝑙𝑒𝑠 𝑖𝑗𝑡

𝑆𝑎𝑙𝑒𝑠 𝑖𝑡

𝐽𝑗=1 .

12

zero-investment trading strategy designed to exploit forward-looking information in ΔCC. If this

information is not fully reflected in current prices, then this strategy can earn abnormal returns.

3. Sample and descriptive analysis

The sample formation is based on FASB‟s and SEC‟s requirements that public firms

disclose the amount of revenue derived from each major customer.7 This information is available

in the COMPUSTAT Segment Files. The COMPUSTAT Segment Files provide the type and

name of a major customer along with the dollar amount of annual revenues generated from each

major customer.

I employ a phonetic string algorithm to match each customer name to the corresponding

identifying gvkey code of one of the companies listed in the COMPUSTAT Annual Files.

Following the automated phonetic matching, I inspect every match to ensure accuracy and

manually correct inaccurate and missing matches by hand-collecting information from the

COMPUSTAT database and the EDGAR database. Next, I combine the initial sample of

supplier-customer links with accounting data from the annual COMPUSTAT files and stock

returns data from the monthly CRSP files. Given that suppliers and customers may or may not

share the same fiscal year-end, I match each supplier with the most recent customer information

as of the month corresponding to the supplier‟s fiscal year-end.

7 Major customer disclosure requirements were initially established by the Statement of Financial Accounting

Standards No. 14 (SFAS 14) issued by the FASB in 1976. The requirement was amended in 1979 by SFAS 30 and

both SFAS 14 and SFAS 30 were superseded by SFAS 131 in 1997. More specifically, SFAS 14 §39 stipulates that

“if 10% or more of the revenue of an enterprise is derived from sales to any single customer, that fact and the

amount of revenue from each such customer shall be disclosed.” SFAS 131 §39 reiterates that “if revenues from

transactions with a single external customer amount to 10% or more of an enterprise‟s revenues, the enterprise shall

disclose that fact, the total amount of revenues from each such customer and the identity of the segment or segments

reporting the revenues.” Similar disclosure requirements are set by Regulation S-K of the SEC. Specifically, Item

101 (§c, vii) specifies that “the name of any customer and its relationship, if any, with the registrant or its

subsidiaries shall be disclosed if sales to the customer by one or more segments are made in an aggregate amount

equal to 10% or more of the registrant's consolidated revenues and the loss of such customer would have a material

adverse effect on the registrant and its subsidiaries taken as a whole.”

13

For a firm-year to be included in the sample it must have non-missing information about

customer concentration (CC), market value of equity (MV), profit margin measured as the ratio

of income before extraordinary items to net sales (PM), and asset turnover measured as the ratio

of net sales to the book value of total assets (ATO). To allow for a clear ranking of performance

and facilitate comparison with prior studies on firm profitability (e.g., Fairfield and Yohn 2001;

Soliman 2008), firm-years with negative profit margins are excluded. To further mitigate the

impact of distressed stocks, I exclude firm-years with negative book value of equity.8

The procedures and criteria described above yield a sample of 47,396 supplier-customer

relations for a total of 26,246 unique supplier firm-years from 1977 to 2006. Note that my

sample of unique supplier firm-years covers as much as 25.5% of the COMPUSTAT universe.

Observations are grouped based on the calendar year t corresponding to the fiscal year-end

month.

Since suppliers often disclose multiple major customers, for each of the financial

characteristics of supplier i‟s J major customers in year t I construct a weighted-average index

(CVAR) as follows:

𝐶𝑉𝐴𝑅𝑖𝑡 = 𝑤𝑖𝑗𝑡 × 𝐶𝑉𝐴𝑅𝑖𝑗𝑡

𝐽

𝑗=1

(2)

The weight 𝑤𝑖𝑗𝑡 is defined as 𝑆𝑎𝑙𝑒𝑠 𝑖𝑗𝑡

𝑆𝑎𝑙𝑒𝑠 𝑖𝑡

𝑆𝑎𝑙𝑒𝑠 𝑖𝑗𝑡

𝑆𝑎𝑙𝑒𝑠 𝑖𝑡

𝐽𝑗=1 , where 𝑆𝑎𝑙𝑒𝑠𝑖𝑗𝑡 is firm i‟s sales to major

customer j in year t and 𝑆𝑎𝑙𝑒𝑠𝑖𝑡 represents firm i‟s total sales in year t. To illustrate, 𝐶𝑀𝑉𝑖𝑗𝑡 is

the market value of supplier i‟s major customer j in year t and 𝐶𝑀𝑉𝑖𝑡 is the weighted-average

8 As an empirical matter, all inferences drawn in my paper are robust to the inclusion of firms with negative profit

margins and negative book value of equity. Also note that financial services firms (SIC codes 60-69) are included in

the sample and that all my results are insensitive to the exclusion of these firms.

14

market value of supplier i‟s J major customers in year t. A drawback of this index is that it is

measured only across major customers that can be identified on the COMPUSTAT Annual files.

Panel A of Table 1 summarizes the pooled empirical distributions of primary and control

variables. All variables and data sources are described in the Appendix. Several points are

noteworthy. First, the number of observations reported in the first column shows that data

availability requirements lead to different sample sizes for different variables. In the empirical

analysis, I do not require that all variables be jointly available but only those that are used in a

particular test. Second, there is evidence of significant variation in the levels of customer-base

concentration across supplier firms. The mean (median) value of CC is 0.107 (0.043) and the

interquartile range is from 0.015 to 0.121. There is also evidence of significant cross-sectional

variation in the changes of customer-base concentration. The mean (median) value of ΔCC is

−0.005 (0.000) and the interquartile range is from −0.016 to 0.012.

Another salient feature of the data is the asymmetry in the supplier-customer relationship.

Suppliers, on average, have 1.8 major customers and rely on each of them for 22% of their

annual sales.9 In contrast, suppliers‟ sales to identifiable major customers account, on average,

for 2.7% of each customer‟s cost of goods sold (CDEP). This asymmetry potentially reflects the

bias embedded in the data-generating process − namely, that, by definition, suppliers are reliant

on their major customers whereas major customers need not be reliant on their suppliers.10

Supplier firms also tend to be smaller, younger, and to experience higher sales growth and stock

returns than their identifiable major customers.

9 Note that firms often disclose information about customers that account for less than 10% of their annual sales if

the customer is important to their business.

10 This asymmetry, however, does not preclude the possibility that major customers are technologically dependent

on their suppliers.

15

At this point it may be useful to highlight that approximately 79% of the supplier-

customer relations are between firms in different two-digit SIC industries, consistent with the

fact that supply chain relations tend to develop across sectors. In addition, industry clustering is

unlikely to inhibit the analysis since there is a substantial degree of representation of the sample

firms across as many as 69 two-digit SIC industries. The three most represented industries are

Electronic & Other Electrical Equipment & Components, Except Computer Equipment (36),

Business Services (73), and Industrial & Commercial Machinery & Computer Equipment (35).

These industries collectively account for roughly 30% of the total number of observations.11

Panel B of Table 1 reports Pearson and Spearman pair-wise correlations across variables.

The correlations of CC with firm characteristics imply that firms with more concentrated

customer bases tend to be smaller and younger, and to report higher sales growth. The positive

correlation between CC and ΔCC is consistent with mean-reversion in the levels of customer-

base concentration. Some preliminary findings are in order. First, the positive and significant (at

the 1% level) correlation of CC with ROA suggests that suppliers with more concentrated

customer bases tend to be more profitable. Second, the positive and significant (at the 1% level)

correlation between ΔCC and 𝛥𝑅𝑂𝐴𝑡+1 is consistent with an intertemporal association between

changes in customer-base concentration and supplier firm performance.

Lastly, Figure 1 examines time-series variation in the aggregate levels of customer-base

concentration. At the aggregate level, CC rises from 1977 to 1984, remains relatively stable

during the period leading to the enforcement of SFAS 131 in the end of 1997, and rises in the

post-1998 period. Consistent with an overall increasing trend in concentration, a regression of

the annual values of aggregate CC on time yields a positive and significant (at the 1% level)

11

My results are robust to the exclusion of supplier firms in the three most represented two-digit SIC industries.

16

estimated slope coefficient. Given that over the sample period studied COMPUSTAT has

expanded coverage of small firms, the increasing trend in CC may be an in-sample phenomenon

that is not necessarily reflective of macroeconomic trends.12

4. Customer-base concentration and firm performance

In this section, I investigate the empirical link between customer-base concentration and

supplier firm performance. The analysis proceeds in two steps. First, I examine the association of

the levels of customer-base concentration (CC) with supplier firm performance. Next, I exploit

the changes in customer-base concentration (ΔCC) and conduct lead-lag analyses that help assess

the existence of a cause-and-effect relationship between customer-base structure and supplier

firm performance.

4.1 Levels analysis

The conventional view of customer-base concentration as an impediment to supplier firm

performance emphasizes the impact of customer power on supplier gross margins. On the other

hand, research on relationship marketing and operations management argues that suppliers with

concentrated customer bases may achieve efficiencies in the form of lower marketing and

administrative expenses, higher asset utilization, and enhanced working capital management

capabilities. However, such efficiencies are unlikely to be reflected in suppliers‟ gross margins.

When compared to gross margins, accounting rates of return are deemed to measure overall firm

performance in a more comprehensive manner.

12

Consolidation trends in downstream industries are likely to constitute yet another source of time-series variation

in the aggregate levels of customer-base concentration. To see this point, note that consolidation in downstream

industries is likely to lead to a reduction in the number of downstream firms and, in turn, an increase in the

customer-base concentration of upstream firms. Indeed, Figure 1 shows that, at the aggregate level, CC increases

during the M&A waves of the mid-1980s and late-1990s.

17

In what follows, I investigate the empirical association between customer-base

concentration and accounting rates of return. Specifically, I estimate annual cross-sectional

regressions of the following form:

𝑃𝐸𝑅𝐹𝑂𝑅𝑀𝐴𝑁𝐶𝐸𝑖𝑡 = 𝛼𝑡 + 𝛽1𝑡𝐶𝐶𝑖𝑡 + 𝛽𝑘𝑡𝐶𝑖𝑡𝑘

𝐾

𝑘=2

+ 휀𝑖𝑡

(3)

The dependent variable in Equation (3) is firm performance as measured by return on assets

(ROA) and return on equity (ROE). ROA is the ratio of income before extraordinary items to the

book value of total assets, and ROE is the ratio of income before extraordinary items to the book

value of shareholders‟ equity.13

To understand the association of CC with profitability drivers, I decompose overall firm

profitability as 𝑅𝑂𝐴 =𝐼𝑛𝑐𝑜𝑚𝑒 𝐵𝑒𝑓𝑜𝑟𝑒 𝐸𝑥𝑡𝑟𝑎𝑜𝑟𝑑𝑖𝑛𝑎𝑟𝑦 𝐼𝑡𝑒𝑚𝑠

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠×

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠

𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠. The ratio of income before

extraordinary items to net sales measures profit margin (PM), while the ratio of net sales to total

assets measures asset turnover (ATO). This multiplicative decomposition, commonly known as

DuPont profitability analysis (see, e.g., Palepu, Healy, and Bernard 2004), is considered a useful

tool of financial statement analysis (Soliman 2008).14

Note that

𝑅𝑂𝐸 = 𝑅𝑂𝐴 ×𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠

𝑆𝑎𝑟𝑒 𝑜𝑙𝑑𝑒𝑟𝑠 ′𝐸𝑞𝑢𝑖𝑡𝑦, where the ratio of total assets to shareholder‟s equity

measures financial leverage.

The primary independent variable is CC as defined in Equation (1). Following prior

literature on the impact of buyer bargaining power on supplier firm performance (e.g., Kelly and

Gosman 2000), the vector of control variables (𝐶𝑘 ) includes the log of market capitalization

(MV), the log of firm age (AGE), sales growth (SG), financial leverage (FLEV), the number of

13

All my results hold after adjusting income for extraordinary items.

14 Soliman (2008) comprehensively explores the DuPont components and finds that the decomposition provides

useful information to market participants.

18

reported business segments (NSEG), and the Herfindahl-Hirschman index of the degree of

product market competition in the firm‟s industry (HHI). Industry dummies based on two-digit

SIC codes are included as additional regressors to control for industry fixed effects.

Table 2 reports the time-series means of the estimated coefficients. Statistical inference is

based on Fama-MacBeth (1973) t-statistics corrected for serial correlation using the Newey-West

(1987) adjustment with three lags.15

Columns 1 and 2 document the empirical association

between CC and overall firm profitability. After controlling for other firm characteristics, I find a

positive and significant (at the 1% level) association between CC and accounting rates of return.

The t-statistics for the coefficient estimates on CC are 9.47 and 5.00 for the ROA and ROE

models, respectively. Ceteris paribus, a one-standard-deviation increase in CC would increase

the mean value of accounting rates of return by 5%. Columns 3 and 4 examine separately the

association of CC with the two multiplicative components of overall firm performance. The

coefficient estimates reveal that CC is positively and significantly (at the 1% level) associated

with both asset turnover and profit margin.

To elucidate the association of CC with profit margin, I decompose income before

extraordinary items into operating income before depreciation and “other items.”16

Based on this

income decomposition, I break down profit margin into two additive components as 𝑃𝑀 =

𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐼𝑛𝑐𝑜𝑚𝑒 𝐵𝑒𝑓𝑜𝑟𝑒 𝐷𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡 𝑖𝑜𝑛

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠+

𝑂𝑡𝑒𝑟 𝐼𝑡𝑒𝑚𝑠

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠.17

The first component measures operating

15

All empirical tests reported in this paper are based on annual cross-sectional regressions and Fama-MacBeth

(1973) t-statistics corrected for serial correlation using the Newey-West (1987) adjustment. In unreported sensitivity

analysis, I repeat the entire study using pooled sample estimations and obtain similar results. In particular, I estimate

the models described in Equations (3) through (11) using pooled cross-sectional regressions with year and industry

fixed effects, and calculate t-statistics based on standard errors clustered by industry and year.

16 Note that “other items” capture all income statement line items that fall below operating income before

depreciation and above income before extraordinary items, including depreciation and amortization, interest

expense, non-operating income, special items, income taxes, and minority interest.

17 See Nissim and Penman (2001) for more details on profit margin decompositions.

19

margin (OM) and the second one measures non-operating margin (NOM). Columns 5 and 6

examine the association of CC with operating and non-operating margins. The finding here is

twofold. First, CC is positively and significantly (at the 1% level) associated with operating

margin (t-statistic = 4.74). Second, the association between CC and non-operating margin is

positive, albeit not significant at conventional levels. Therefore, operating margins are primarily

driving the positive association of CC with profit margins.

By definition, operating income before depreciation is equal to net sales minus cost of

goods sold and SG&A expenses. Accordingly, operating margin can be further decomposed into

gross margin minus the ratio of SG&A expenses to net sales or

𝑂𝑀 =𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠 −𝐶𝑜𝑠𝑡 𝑜𝑓 𝐺𝑜𝑜𝑑𝑠 𝑆𝑜𝑙𝑑

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠−

𝑆𝐺&𝐴 𝑒𝑥𝑝𝑒𝑛𝑠𝑒𝑠

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠.

Column 7 investigates the relationship between CC and gross margins (GM). The

coefficient on CC is negative and significant (at the 1% level) with t-statistic = −6.08. Consistent

with prior research on the impact of customer power on suppliers‟ gross margins (e.g., Kelly and

Gosman 2000), the negative association between CC and GM implies that more-concentrated

suppliers tend to report higher cost of goods sold per dollar of sales. The magnitude of the

estimated coefficient implies that, ceteris paribus, a one-standard-deviation increase in CC would

decrease the mean value of gross margins by 3%. This finding, however, is in sharp contrast with

evidence of a positive association between customer-base concentration and operating margins.

Therefore, the key implication is that more-concentrated suppliers enjoy higher operating

margins in spite of the fact that they report lower gross margins.

In turn, higher operating margins can be reconciled with lower gross margins only if

more-concentrated suppliers spend less on SG&A expenses per dollar of sales. Consistent with

this claim, the estimates reported in Column 8 imply that more-concentrated suppliers tend to

20

report significantly lower SG&A-to-sales ratios. The t-statistics for the coefficient estimate on

CC is −9.13 (significant at the 1% level). To gauge the magnitude of the coefficient estimate,

consider that a one-standard-deviation increase in CC would ceteris paribus decrease the mean

value of SG&A expenses per dollar of sales by more than 7%. Importantly, the association of CC

with SGA is strong enough to outweigh that between CC and GM and, in turn, to explain why

more concentrated suppliers experience higher operating margins than less concentrated ones.

At this juncture some robustness checks are in order. To address potential non-linearities

in the relation between firm performance and the explanatory variables, I re-estimate Equation

(3) using decile rank transformations of the right-hand side variables and find consistent results.

As an additional check, I repeat the analysis separately for each two-digit SIC industry, using

industry-by-industry pooled regressions with year fixed effects, and find that my results are not

sensitive to whether Equation (3) is estimated cross-sectionally or separately for each industry.18

Overall, the evidence supports that suppliers with more concentrated bases tend to be

more profitable because of efficiency gains in the form of enhanced asset utilization and reduced

SG&A spending per dollar of revenue earned. Next, I probe deeper into how these gains accrue

to more concentrated suppliers. To this end, I estimate the following annual cross-sectional

regression model:

𝐸𝐹𝐹𝐼𝐶𝐼𝐸𝑁𝑇𝑖𝑡 = 𝛼𝑡 + 𝛽1𝑡𝐶𝐶𝑖𝑡 + 𝛽𝑘𝑡𝐶𝑖𝑡𝑘

𝐾

𝑘=2

+ 휀𝑖𝑡

(4)

The dependent variable in Equation (4) measures a wide array of operating performance drivers.

The first set of variables focuses on inventory management and examines inventory turnover

(ITO) and inventory held as a fraction of total assets (IHLD). The second set considers the cash

18

I estimate industry-by-industry regressions using a pooled specification to ensure sufficient degrees of freedom for

each regression.

21

conversion cycle (CACC) and its components to gauge overall working capital management

efficiency.19

The right-hand side variables in Equation (4) are defined as before. Industry

dummies based on two-digit SIC codes are included to control for industry fixed effects. Results

from estimating Equation (4) are presented in Table 3.

Columns 1 and 2 test the association between CC and inventory management. I find that

CC is positively associated with inventory turnover and negatively associated with inventory

held as a fraction of total assets. The t-statistics on the estimated coefficients are large and

significant (at the 1% level), while the sign of the estimated coefficients implies that more-

concentrated suppliers experience higher inventory turnover and hold less inventory as a fraction

of total assets. To illustrate, a one-standard-deviation increase in CC would ceteris paribus

increase the mean value of inventory turnover by 13% and decrease the mean value of inventory

held per dollar of total assets by 5%.

Next, Column 3 documents a significantly positive association between CC and overall

working capital management efficiency as proxied by the cash conversion cycle.20

Columns 4

through 6 delve further into the association of CC with cash conversion cycle components.

Contrary to the view that major customers use their power to extract trade credit provisions from

their dependent suppliers (e.g., Scherer 1970), I do not find any systematic differences in the

receivables conversion cycles (RCP) of more-concentrated suppliers and less-concentrated ones.

In fact, more-concentrated suppliers tend to experience significantly longer payables conversion

periods (PCP) − as if they are able to extract extended trade credit provisions from their own

19

The cash conversion cycle (CACC) is defined as the inventory conversion period (ICP) plus the receivables

conversion period (RCP) minus the payables conversion period (PCP). ICP represents the efficiency of production

and inventory management, RCP measures a firm‟s ability to manage its downstream supply chain, and PCP

indicates the efficiency of upstream supply chain management,

20 Note that shorter cash conversion cycles indicate higher working capital management efficiency.

22

vendors − and shorter inventory conversion periods (ICP). The combination of these effects

induces an overall negative association between CC and cash conversion cycles.

Interestingly, the estimates reported in Column 7 reveal a negative and significant (at the

5% level) association between CC and provisions for doubtful accounts as a fraction of all

receivables (DOUBT). Stated otherwise, even though there is no systematic link between

customer-base concentration and trade credit provisions in the form of accounts receivable, the

collectibility of these receivables tends to be higher among more-concentrated suppliers.

To gain further insights, I also examine the association of CC with two salient line items

under SG&A – namely, advertising expenses per dollar of sales (ADV) and R&D expenses per

dollar of sales (RD). As a caveat, note that only a subsample of firms report advertising and

R&D expenses as separate line items. In my tests, I do not treat missing values but the inferences

drawn are not sensitive to whether or not I set missing values for advertising and R&D expenses

to zero.

In Column 8, I document a negative and significant (at the 1% level) association between

CC and ADV. In additional analysis (not reported for brevity), I find that subtracting advertising

expenses from SG&A expenses does not affect dramatically the magnitude and statistical

significance of the negative association between CC and SGA. Hence, cost savings in terms of

advertising expenses are only one of the reasons why more concentrated suppliers tend to report

higher operating margins than less concentrated ones.

Somewhat surprisingly, Column 9 reveals a positive and significant (at the 1% level)

association between CC and RD. In other words, suppliers with more concentrated customer

bases tend to spend more on R&D expenses per dollar of sales. This result is interesting for at

least two reasons. First, it implies that, in effect, R&D spending attenuates the overall negative

23

association between customer-base concentration and SG&A spending. Second, it provides a

new piece of evidence on how inter-firm relationships may foster innovativeness along the

supply chain.21

To summarize, the results reported in Tables 2 and 3 deliver a coherent message.

Although more-concentrated suppliers report lower gross margins, they spend less on SG&A and

advertising expenses per dollar of sales, hold less of their assets in inventory, as well as enjoy

higher inventory turnover and shorter cash conversion cycles. Accordingly, more-concentrated

suppliers experience not only higher operating and profit margins but also higher asset turnover

and, on the whole, tend to be more profitable.

4.2 Intertemporal changes analysis

A causal link between customer-base structure and performance implies that changes in

customer-base concentration are associated with changes in supplier firm performance. Indeed,

potential efficiency gains achieved through enhanced production coordination and inventory

management, cooperative advertising campaigns and marketing alliances with major customers,

are likely to flow gradually through a supplier‟s financial reporting system. Thus, a cause-and-

effect relationship predicts an intertemporal association between changes in customer-base

concentration and changes in supplier firm performance.

To help assess the existence of a causal link, I exploit the non-static nature of supplier

firms‟ customer bases and examine whether changes in customer-base concentration (ΔCC)

predict future changes in supplier firm performance. In particular, I estimate annual cross-

sectional regressions of the following form:

21

Several authors argue that the presence of trust in major customer relationships reduces the probability of

opportunistic behavior by any partner and increases the likelihood of customers and suppliers making relationship-

specific investments in specialized physical and human capital and intangibles such as R&D (see, e.g., Panayides

and Venus Lun 2009 and the references therein).

24

𝛥𝑃𝑅𝑂𝐹𝐼𝑇𝑖𝑡+1 = 𝛼𝑡 + 𝛽1𝑡𝛥𝐶𝐶𝑖𝑡 + 𝛽2𝑡𝑅𝑂𝐴𝑖𝑡 + 𝛽3𝑡𝛥𝑃𝑀𝑖𝑡 + 𝛽4𝑡𝛥𝐴𝑇𝑂𝑖𝑡 + 휀𝑖𝑡+1 (5)

The dependent variable in Equation (5) is the annual change in firm profitability between t and

t+1 measured relative to accounting rates of return. The primary independent variable is ΔCC

and it is defined as the annual change in customer-base concentration between t-1 and t. The set

of control variables is measured in t and includes the level of ROA and the changes in the

components of ROA − namely, changes in profit margins (ΔPM) and asset turnover (ΔATO).22

Industry dummies based on two-digit SIC codes are included to control for industry fixed effects.

Table 4 reports results from estimating Equation (5). An investigation of Columns 1 and

2 reveals that ΔCC positively predicts one-year-ahead changes in accounting rates of return. The

t-statistics for the coefficient estimate on ΔCC is 3.75 for the 𝛥𝑅𝑂𝐴𝑡+1 model and 2.86 for the

𝛥𝑅𝑂𝐸𝑡+1 model, both significant at the 1% level. Note that the control variables exhibit the

expected association with one-year-ahead changes in overall firm profitability. To illustrate, in

Model 1 the negative and significant (at the 1% level) coefficient estimate on ROA is in line with

well-documented patterns of mean-reversion in accounting rates of return (e.g., Beaver 1970;

Freeman, Ohlson, and Penman 1982), and the positive and significant (at the 1% level)

coefficient estimate on ΔATO is consistent with evidence in Fairfield and Yohn (2001) and

Soliman (2008).

According to the DuPont analysis, changes in overall firm profitability (as captured by

ROA) can be traced to changes in profit margins and asset turnover. Hence, the results

documented in Columns 1 and 2 provide prima facie evidence that increasingly concentrated

suppliers experience efficiency gains in the form of either improved profit margins or enhanced

22

Fairfield and Yohn (2001) find that disaggregating ROA into PM and ATO does not provide incremental

information for forecasting 𝛥𝑅𝑂𝐴𝑡+1, but that disaggregating ΔROA into ΔPM and ΔATO is useful in forecasting

𝛥𝑅𝑂𝐴𝑡+1.

25

asset turnover, or both. Columns 3 and 4 test separately the association of ΔCC with one-year-

ahead changes in profitability components. The main finding is that ΔCC is a significant

predictor of one-year-ahead changes in not only profit margins but also asset turnover. The t-

statistics for the coefficient estimate on ΔCC is 2.75 for the 𝛥𝑃𝑀𝑡+1 model and 2.93 for the

𝛥𝐴𝑇𝑂𝑡+1 model, both significant at the 1% level.

Interestingly, Column 5 documents a positive, albeit insignificant, association between

ΔCC and one-year-ahead changes in gross margins (𝛥𝐺𝑀𝑡+1). Holding quantities constant, this

finding is, in turn, consistent with two scenarios. First, changes in customer-base concentration

have no effect on either selling prices or per unit production costs. Second, changes in customer-

base concentration affect selling prices and per unit production costs in an almost exactly

offsetting way. Unfortunately, I cannot disentangle these scenarios because price and cost data

are not publicly available.

At this point note that the intertemporal association between changes in customer-base

concentration and changes in supplier firm performance is not sensitive to whether Equation (5)

is estimated cross-sectionally or separately for each two-digit SIC industry.23

Also note that my

results are not sensitive to whether I use the raw values or decile rank transformations of the

explanatory variables. Therefore, these results are omitted for brevity.

Another concern with the results of Table 4 is that ΔCC is correlated with variables that

are predictors of overall firm performance and hence the observed relationship between ΔCC and

one-year-ahead changes in accounting rates of return is spurious. In order to sort out whether the

empirical relation between ΔCC and subsequent changes in firm performance is due to spurious

correlations, I use a two-stage regression approach. In the first-stage regression, I estimate the

23

I repeat the analysis separately for each two-digit SIC industry, using industry-by-industry pooled regressions

with year dummies to control for time fixed effects, and find consistent results.

26

residuals from annual cross-sectional regressions of ΔCC on a vector of variables (𝛸𝜆 ) purported

to measure characteristics not only of the supplier firm but also of the supplier firm‟s customer

base:

𝛥𝐶𝐶𝑖𝑡 = 𝛾𝑡 + 𝛿𝜆𝑡𝛸𝑖𝑡𝜆

𝛬

𝜆=1

+ 𝛥𝐶𝐶𝑖𝑡𝑅𝐸𝑆

(6)

By construction, the residual from the first-stage regression model described in Equation (6)

(𝛥𝐶𝐶𝑅𝐸𝑆 ) represents the portion of ΔCC that is orthogonal to the variables included in the vector

𝛸𝜆 . In the second-stage regression, I re-estimate Equation (5) using residual changes in lieu of

observed changes in customer-base concentration. Results of the two-stage regression approach

are presented in Table 5. The table focuses on results for one-year-ahead changes in overall firm

performance as captured by return on assets (𝛥𝑅𝑂𝐴𝑡+1).

Columns 1 through 3 of Table 5 report second-stage results for three different measures

of 𝛥𝐶𝐶𝑅𝐸𝑆 . In Column 1, 𝛥𝐶𝐶𝑅𝐸𝑆 captures information that is orthogonal to characteristics of the

supplier firm including the log of market capitalization (MV), the log of book-to-market ratio

(BM), the log of firm age (AGE), sales growth (SG), Ohlson‟s (1980) measure of distress risk

(OSCOR), the number of reported business segments (NSEG), market share (MSHR), and the

Herfindahl-Hirschman index of competition in supplier‟s industry (HHI). In Column 2, 𝛥𝐶𝐶𝑅𝐸𝑆

captures information that is orthogonal to characteristics of the supplier firm‟s identifiable major

customers including the log of market capitalization (CMV), the log of book-to-market ratio

(CBM), the log of firm age (CAGE), sales growth (CSG), Ohlson‟s (1980) measure of distress

risk (COSCOR), the number of reported business segments (CNSEG), cost reliance on the

supplier firm (CDEP), market share (CMSHR), and the Herfindahl-Hirschman index of

competition in customers‟ industries (CHHI). Finally, in Column 3, 𝛥𝐶𝐶𝑅𝐸𝑆 captures

27

information that is orthogonal to all the above mentioned characteristics evaluated not only for

the supplier firm but also for the supplier firm‟s identifiable major customers.

The key finding of the two-stage regression analysis is that one-year-ahead changes in

overall firm performance are positively and significantly (at the 1% level) related to 𝛥𝐶𝐶𝑅𝐸𝑆 .

Across all three measures of residual changes in customer-base concentration, the t-statistics for

the coefficient estimates on 𝛥𝐶𝐶𝑅𝐸𝑆 are in excess of 3.00. Accordingly, the main inference here

is that the intertemporal association between changes in customer-base concentration and

changes in supplier firm performance is not subsumed by the correlation of ΔCC with a wide

array of variables omitted from the right-hand side of Equation (5).

To recap, I find that, although changes in customer-base concentration are uncorrelated

with subsequent changes in gross margins, ΔCC is a strong and robust predictor of one-year-

ahead changes in profit margins, asset turnover, and overall firm profitability. Even though the

lead-lag analysis of changes yields insights consistent with a cause-and-effect relationship

between customer-base concentration and supplier firm performance, I cannot definitely rule out

that the predictive power of ΔCC is subsumed by omitted correlated variables. To be clear, I also

cannot rule out the possibility of reverse causation running from subsequent changes in supplier

firm performance to current changes in customer-base concentration. At the minimum, however,

the evidence presented so far allows one to argue that changes in customer-base concentration

cause changes in supplier firm performance in the sense of Granger (1969).24

24

A variable X “Granger-causes” a variable Y if Y can be better predicted from past values of X and Y together than

from past values of Y alone, with other relevant information included in the prediction.

28

5. Customer-base concentration and stock returns

In this section, I investigate whether and how investors incorporate into stock prices

information related to changes in customer-base concentration. First, I examine the

contemporaneous association between ΔCC and stock returns. Then, I set up a zero-investment

trading strategy designed to exploit forward-looking information in ΔCC that has not been

efficiently priced by investors in year t.

5.1 ΔCC and contemporaneous stock returns

The results reported so far not only reveal an economically important and statistically

significant link between customer-base structure and firm performance, but also establish that

customer-base dynamics contain forward-looking fundamental information. Naturally, the

question that surfaces is whether and how investors use the information embedded in customer-

base concentration changes when setting stock prices.

To address this question, I examine the contemporaneous association between ΔCC and

inter-announcement stock returns. This research design is in the spirit of Ball and Brown (1968)

and has been used in subsequent research examining the value-relevance of accounting earnings.

Specifically, I estimate annual cross-sectional regressions of the following form:

𝑅𝐸𝑇𝑖𝑡 = 𝛼𝑡 + 𝛽1𝑡𝛥𝐶𝐶𝑖𝑡 + 𝛽𝑘𝑡𝐶𝑖𝑡𝑘

𝐾

𝑘=2

+ 휀𝑖𝑡

(7)

The dependent variable is RET and proxies for the return from holding the stock between

last year‟s earnings announcement and this year‟s announcement.25

RET is measured as the buy-

and-hold twelve-month stock return from nine months before the fiscal year-end to three months

25

Long-window association tests are likely to underestimate the market‟s reaction to news pertaining to customer-

base concentration. A more powerful test of whether and how investors price news related to changes in customer-

base concentration would entail the investigation of short-window stock returns. However, this investigation

requires data on the exact dates on which the news was released to the public. To my knowledge, these data are

currently unavailable and so I defer the short-window association tests to future research.

29

after the fiscal year-end.26

To mitigate survivorship bias, if a security delists during a particular

year, then the CRSP delisting return is included in RET.

The vector of control variables (𝐶𝑘 ) includes several variables known to have

explanatory power for stock returns. Following Ertimur, Livnat, and Martikainen (2003), I

interpret earnings news in the context of revenue and expense surprises and include as separate

regressors in Equation (7) the annual change in net sales scaled by the beginning of year market

value of equity (UREV) and the annual change in expenses scaled by the beginning of year

market value of equity (UEXP).27

As in Amir and Lev (1996) and Francis and Schipper (1999), I

also control for the ratio of income before extraordinary items scaled by the beginning of year

market value of equity (EP). Finally, following Soliman (2008), I include the annual change

between t-1 and t in profit margins (ΔPM) and asset turnover (ΔATO) as additional control

variables. Industry dummies based on two-digit SIC codes are included to control for industry

fixed effects.

Table 6 presents results from association tests based on Equation (7). Model 1 shows that

ΔCC is significant (at the 1% level) in explaining contemporaneous stock returns. The positive

association between ΔCC and stock returns implies that market participants interpret

increases/decreases in customer concentration as good/bad news for stock market valuation.

Importantly, Models 2 through 4 reveal that ΔCC is incrementally important in explaining

contemporaneous stock returns. In particular, the coefficient on ΔCC remains positive and

26

The assumption underlying the three-month gap between the fiscal year-end and the end of the return

measurement window is that annual earnings are released by the end of the third month after the fiscal year-end.

This assumption mimics the standard gap imposed to match annual accounting variables to price and return data

(see, e.g., Basu 1997). Imposing a six-month gap between the fiscal year-end and the end of the return measurement

window does not affect the tenor of my results.

27 If one assumes that annual net sales and expenses follow a random walk, then UREV and UEXP can be

interpreted, respectively, as measures of sales and expense surprises.

30

significant (at the 1% level) even after controlling for changes in revenues and expenses, the

level of earnings, and changes in profit margins and asset turnover.28

Note that, consistent with Ertimur et al. (2003), I find that (i) the sales surprise (UREV) is

positively associated with stock returns, whereas the expense surprise (UEXP) is negatively

associated with stock returns, and (ii) the sales surprise coefficient is greater in magnitude than

the absolute value of the expense surprise coefficient. Also consistent with prior literature, I find

that the levels of earnings are significant in explaining stock returns after controlling for changes

in the components of earnings. Finally, as in Soliman (2008) I find a positive and significant (at

the 5% level) association between changes in profit margins (ΔPM) and contemporaneous stock

returns. However, the negative sign of the estimated coefficient on ΔATO is the opposite from

that reported in Soliman (2008). The reason for this discrepancy is that my proxy of revenue

surprises is highly correlated with revenue growth.29

Collectively, the univariate and multivariate regression results reported in Table 6 suggest

that changes in customer-base concentration are correlated with value-relevant information not

captured in reported accounting earnings and profitability components. On the basis of this

evidence, one could argue that ΔCC is incrementally informative to stock market participants

when setting stock prices. Importantly, the positive sign of the association between ΔCC and

contemporaneous stock returns implies that investors revise their beliefs and valuations in the

direction of the implications of ΔCC for future firm performance. A related question is whether

investors are fully attentive to these implications. I turn to this question next.

28

Controlling for the levels of profit margins and asset turnover has no effect on my results.

29 Recall that changes in asset turnover measure growth in revenue relative to growth in total assets.

31

5.2 ΔCC and future stock returns

If investors are only partially attentive to customer-supplier links, then they are likely to

systematically fail to fully process the information of ΔCC for future firm profitability, and thus

a trading strategy that exploits this information can earn abnormal stock returns. In order to test

for return predictability based on ΔCC, I estimate annual cross-sectional regressions of the

following form:

𝑅𝐸𝑇𝑖𝑡+1 = 𝛼𝑡 + 𝛽1𝑡𝛥𝐶𝐶𝑖𝑡 + 𝛽𝑘𝑡𝐶𝑖𝑡𝑘

𝐾

𝑘=2

+ 휀𝑖𝑡+1

(8)

where 𝑅𝐸𝑇𝑡+1 is the one-year-ahead stock return, ΔCC is the change in customer-base

concentration between t-1 and t, and 𝐶𝑘 is a vector of control variables measured in t including

market value of equity (MV), book-to-market ratio (BM), accruals scaled by total assets (ACC),

changes in asset turnover (ΔΑΤΟ), and the Herfindahl-Hirschman index of the degree of

competition in the firm‟s industry (HHI). MV has been shown to be negatively correlated with

future stock returns (e.g., Banz 1981), BM controls for the positive correlation of book-to-market

ratios with future stock returns (e.g., Stattman 1980), ACC controls for the accruals anomaly of

Sloan (1996), ΔATO controls for the effect of Soliman (2008), and HHI controls for the negative

correlation of product market competition with future stock returns reported by Hou and

Robinson (2006).

I estimate Equation (8) using the scaled decile rankings of the regressors. Decile rankings

are obtained by independently sorting regressors each year. Rankings are then scaled to lie

between 0 (lowest) and 1 (highest). 30

The time-series of the coefficients can be interpreted as the

returns of zero-investment portfolios with weights at each time given by the rows of the matrix

30

On average, there are roughly seventy stocks in each annual decile portfolio so purely idiosyncratic firm-level risk

should diversify well (see, e.g., Statman 1987).

32

𝑊𝑡 = 𝛺𝑡′𝛺𝑡

−1𝛺𝑡

′ , where the matrix 𝛺𝑡 is the time-series of the set of independent variables

from the cross-sectional regression at t (see, e.g., Daniel and Titman 2006). Note that I find

consistent results using the raw values of the regressors.

Table 7 reports the time-series means of the estimated coefficients. The interesting

finding is that ΔCC is a strong predictor of one-year-ahead stock returns. Consistent with the idea

that investors may not be fully attentive to inter-firm links, the estimated coefficient on ΔCC is

positive and significant (at the 1% level) across all specifications considered. A comparison of

univariate and multivariate regression results reveals that the coefficients and t-statistics on ΔCC

remain relatively unchanged and hence the common variation of ΔCC with other predictors of

returns has little relation to one-year-ahead stock returns.

To illustrate, the estimated coefficient on ΔCC reported in Model 1 implies that a zero-

investment trading strategy based on the decile ranks of ΔCC delivers raw returns of 10.06% per

year with a t-statistic of 4.10 (significant at the 1% level).31

Importantly, in Models 2 through 5,

the estimated coefficients on ΔCC imply economically important and statistically significant (at

the 1% level) returns, ranging between 9.64% and 9.75%, even after hedging out exposure to

several predictors of the cross-section of stock returns.32

As a robustness check, I extend the set of control variables in Equation (8) to include: (i)

earnings-to-price ratios (EP), (ii) the annual change in earnings scaled by the beginning of year

price (ΔEARN), (iii) market model beta, (iv) volatility of stock returns, (v) contemporaneous

31

I also examine the association of ΔCC with one-year-ahead returns using a portfolio approach. Specifically, for

each of the thirty years from 1977 to 2006, I sort suppliers into decile portfolios based on ΔCC and then I measure

one-year-ahead portfolio returns. The portfolio approach yields results similar to those reported in Model 1 of Table

7, and therefore are omitted for brevity.

32 The estimated coefficients on the control variables are generally consistent with findings documented in prior

literature. In contrast to Hou and Robinson (2006), however, I do not find evidence that firms in industries with less

product market competition earn significantly lower future stock returns. Even though I do not attempt to reconcile

my findings with those of Hou and Robinson (2006), note that they report results for a different sample period

(1963-2001) and define industries using three-digit SIC codes.

33

stock returns (RET), (vi) customer-base returns (CRET), (vii) Ohlson‟s (1980) O-Score measure

of distress risk (OSCOR), (viii) financial leverage (FLEV), (ix) firm age (AGE), (x) supplier

industry returns, and (xi) customer industry returns. In unreported analysis, I find that the

estimated coefficients on ΔCC are insensitive, in terms of both magnitude and statistical

significance, to the inclusion or exclusion of these additional controls.33

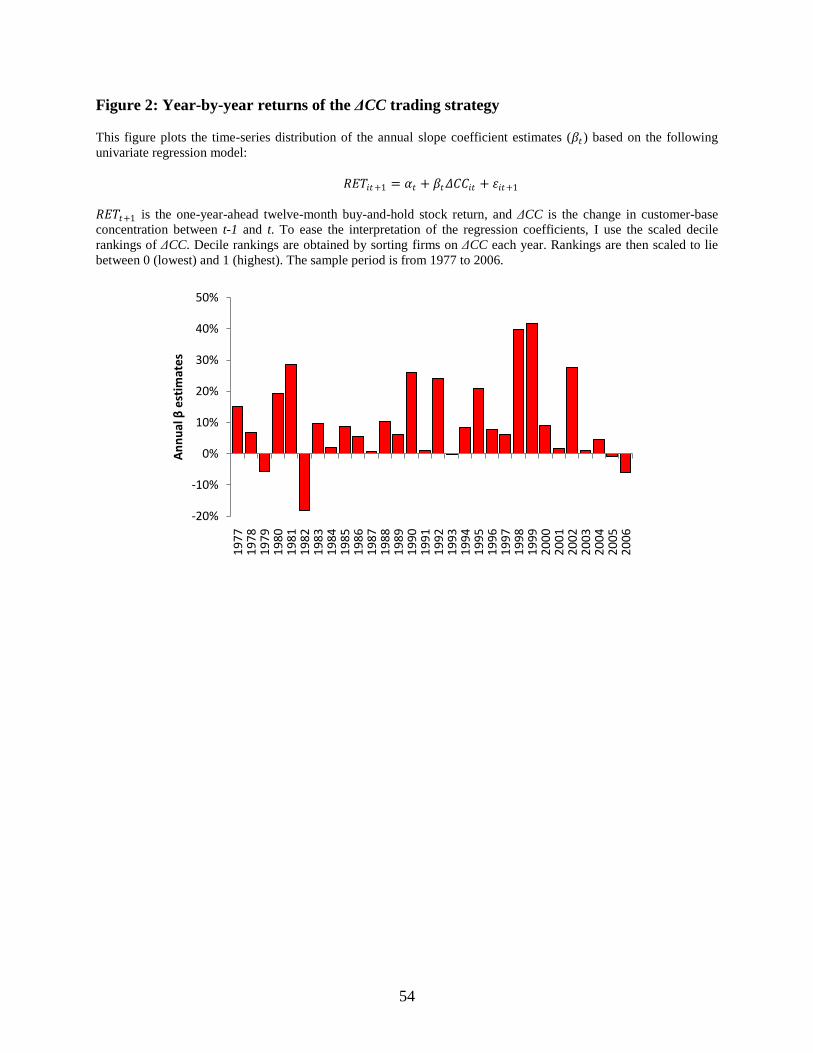

To allay concerns that the performance of the ΔCC trading strategy is due to period-

specific shocks, I provide in Figure 2 the time-series distribution of the annual coefficient

estimates on ΔCC based on Model 1 of Table 7 (i.e., before hedging out exposure to other

predictors of returns). Recall that the annual coefficient estimates capture the year-by-year raw

performance of a zero-investment strategy based on the decile ranks of ΔCC. The figure reveals

that the ΔCC strategy delivers positive returns in most years studied. Further, the infrequent

negative returns are small.

Taken together, the evidence implies that although stock prices react in year t to

customer-base concentration changes, stock prices continue to drift over the subsequent year in

the direction of the initial change. In order to gauge the magnitude of the drift, I measure the

return earned in year t as a fraction of the total return earned from t to t+1 on a long/short

portfolio based on ΔCC. If stock prices react sluggishly, then this fraction will be less than 100%.

Consistent with underreaction, I find that, on average, long/short portfolio returns in t account for

52% of the total portfolio returns earned from t to t+1. Stated otherwise, stock prices, on

average, underreact to information about customer-base concentration changes by 48%.

33

The estimated coefficients on the additional control variables are generally consistent with prior literature.

However, in contrast to Dichev (1998), I do not find evidence of a significant negative premium for distress risk.

Given that the distress-risk effect is driven by the low returns of the most distressed firms (Griffin and Lemmon

2002), this discrepancy is likely due to under-sampling of high distress risk firms. Also note that I find an

insignificant association between customer base stock returns (CRET) and one-year-ahead supplier stock returns.

This finding is entirely consistent with the short-lived nature of the customer momentum effect documented by

Cohen and Frazzini (2008).

34

5.3 The ΔCC effect: Compensation for risk or mispricing?

If the market is efficient then the robust positive association between ΔCC and one-year-

ahead returns implies that changes in customer-base concentration are accompanied by changes

in the systematic risk of supplier firms. In what follows, I investigate this risk-based explanation.

The analysis presented here makes it hard to reconcile the phenomenon with the pricing of risk in

efficient markets. In fact, the evidence suggests that mispricing caused by investors‟ systematic

underreaction to the implications of ΔCC for future firm fundamentals is a plausible explanation.

5.3.1 ΔCC and changes in risk

Sunder (1973; 1975) argues that abnormal returns‟ estimates can be biased if firm risk is

a non-stationary parameter that changes with time. In a similar vein, if changes in customer-base

concentration are related to changes in the risk of supplier firms then the performance of the

ΔCC strategy may be only seemingly abnormal. I explicitly test this possibility using annual

cross-sectional regressions of the following form:

𝛥𝑅𝐼𝑆𝐾𝑖𝑡 = 𝛾𝑡 + 𝛿𝑡𝛥𝐶𝐶𝑖𝑡 + 휀𝑖𝑡 (9)

where ΔRISK measures the change in firm risk between t-1 and t relatively to an extensive array

of risk proxies including (i) market model beta, (ii) Fama and French (1993) three-factor beta,

(iii) raw volatility of stock returns, (iv) idiosyncratic volatility of stock returns defined relative to

the Fama and French (1993) three-factor model, (v) raw dispersion in analysts‟ earnings

forecasts, (vi) distress risk as captured by Ohlson‟s (1980) probability of default, and (vii)

liquidity risk measured as proposed in Amihud (2002).

A risk-based explanation of the ΔCC effect requires a positive association between ΔCC

and changes in firm risk. Contrary to this explanation, I find that the estimated slope coefficient

for Equation (9) is not significantly different from zero for all risk proxies considered (these

35

results are omitted for brevity). Nevertheless, the lack of association between ΔCC and ΔRISK

may be due to measurement error in the risk proxies considered.

A related explanation of the ΔCC effect is that changes in customer-base concentration

are accompanied by changes in expected returns because customer-base concentration per se

represents risk that is of special hedging concern to investors. If customer-base concentration is,

in fact, a priced risk factor, then investors should require higher returns from holding stocks of

suppliers with more concentrated customer bases and hence one should observe a positive

association between CC and expected returns. In a companion working paper, I investigate this

possibility by testing the association of CC with a measure of ex-ante expected returns.34

My

findings do not support this alternative explanation. After controlling for previously identified

cross-sectional determinants of ex-ante cost of capital (e.g., market model beta, volatility of

returns, market capitalization, book-to-market, leverage, analysts‟ consensus long-term growth

forecasts, analyst coverage, dispersion in analysts‟ one-year-ahead earnings forecasts), I do not

find evidence of a positive premium for customer-base concentration.

5.3.2 ΔCC and long-run stock returns

An investigation of long-run stock returns provides further evidence as to whether a risk-

based explanation can account for the positive association between ΔCC and one-year-ahead

stock returns. The idea is simple. If changes in customer-base concentration are accompanied by

permanent changes in the risk of supplier firms, then the positive association between ΔCC and

future stock returns should extend beyond the one-year-ahead horizon.

I examine the ability of ΔCC to predict long-run stock returns by estimating annual cross-

sectional regressions of the following form (for τ = 2, 3, and 4):

34

Following Gebhardt, Lee, and Swaminathan (2001), I compute ex-ante cost of capital, at the firm-year level, as

the internal rate of return that equates current stock market value with the present value of prevailing analysts‟

forecasts of future flows.

36

𝑅𝐸𝑇𝑖𝑡+𝜏 = 𝛼𝜏𝑡 + 𝛽𝜏𝑡𝛥𝐶𝐶𝑖𝑡 + 휀𝑖𝑡+𝜏 (10)

Contrary to the risk-based explanation, I find that the predictive power of ΔCC for future stock

returns gradually fades away and becomes insignificant past year t+2.

5.3.3 Variation with firm characteristics

A growing line of research in accounting and finance argues that mispricings tend to be