current status of the airport / airline industryardent.mit.edu/airports/asp_current_lectures/current...

TRANSCRIPT

Airport Systems Planning & Design / RdN

Dr. Richard de Neufville

Professor of Systems Engineering andCivil and Environmental Engineering

Massachusetts Institute of Technology

Current Status of the Airport / Airline Industry

Airport Systems Planning & Design / RdN

Current Status of the Air Transport Industry

Objective: To definecurrent situation major new factors

Topics:Airline and Airport RankingsCurrent Trends

• Shake-up / Disappearance of Network Airlines• Coming and Going of Transfer Hubs• Commercialization / Privatization of Airports

Airport Systems Planning & Design / RdN

Principal drivers of air transportation industry

Long-term 6% annual decrease in air fares: Driving comparable annual worldwide traffic growth

Commercialization: market economy management replaces government ownership and control in a regulated environment

Low-cost carriersSouthwest, AirTran, Jet Blue, Westjet, Ryanair, easyjet, etc

Globalization:transnational airline alliances and airport groups

Technical innovation: e-commerce, RJs, A380 NLA, satellite-based navigation

Airport Systems Planning & Design / RdN

Major Recent Events

Disappearance of Major Airlines TWA, Swissair, Sabena

Mergers of Japan Airlines and Japan Air Systems (2002)Air France and KLM (Sept 04)

Major BankruptciesUnited, US Airways, Air Canada – others near!

Surge by Low-Cost Passenger CarriersAir Tran, Ryanair, easyjet

Surge by Chinese CarriersCathay Pacific, China Airlines, EVA

… also by Fedex

Airport Systems Planning & Design / RdN

World Traffic, (Pax-Km x 109) World and IATA

Year IATAIATA World share, % IATA World

2003 2704 3236 83.5 (0.4) 12002 2770 3196 86 (1) (1)2001 2652 2912 91 (4) (4)2000 2757 3018 91 4 (2)1999 2657 3074 86 6 61998 2514 2888 87 7 41990 1600 2186 73 18 81987 1042 1763 59 9 81982 712 1263 56 4 41977 600 1036 58

Pax-km, Billions Annual Growth %

Source: IATA World Air Transport StatisticsNote: Change in Series; now includes charter travel

Airport Systems Planning & Design / RdN

IATA Members’ Traffic, Revenues, Yield, and CPI

Source: IATA World Air Transport Statistics

0

50

100

150

200

250

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Perc

ent o

f 199

1Traffic Revenues Yield Inflation

Airport Systems Planning & Design / RdN

Interpretation of Trends

Over past 13 years…Yields (revenues/unit distance) have dropped about 20%While inflation has risen about 50%So: costs on a constant basis cut in halfThus: traffic doubledImplying price elasticity about -1.3 > -1.0So total revenues grow as price drops

Airport Systems Planning & Design / RdN

Airports by millions of pax., 2003 (IATA data; US- Bold, hubs- italics)

Rank Airline Annual %2003 2002 2001 2000 1993 1993-2003

1 Atlanta 78.8 76.6 75.9 80.2 47.8 6.52 Chicago / OHare 69.4 66.5 66.8 72.1 65.1 0.73 London / Heathrow 63.2 63.0 60.7 64.6 47.6 3.34 Tokyo / Haneda 63.2 61.1 58.7 56.4 41.5 5.25 Los Angeles / Internatl 55.0 56.2 61.0 68.5 47.8 1.56 Dallas / Ft. Worth 53.2 52.8 55.2 60.7 49.7 0.77 Frankfurt / Main 48.1 48.1 48.6 49.4 31.9 5.18 Paris / de Gaulle 47.9 48.1 48.0 48.2 25.7 8.69 Amsterdam / Schiphol 39.8 40.6 39.5 39.6 20.1 9.810 Denver / International 37.5 35.7 36.1 38.7 32.6 1.511 Phoenix 37.4 35.6 35.5 35.9 23.5 5.912 Las Vegas 36.3 35.0 35.2 36.9 22.5 6.113 Madrid 35.4 33.7 34.0 32.8 17.3 10.514 Houston / Bush 34.1 34.4 34.8 35.2 20.3 6.815 Minneapolis / St. Paul 33.2 32.6 35.2 36.7 23.4 4.216 Detroit / Metro 32.7 32.4 32.3 35.5 24.2 3.517 New York / Kennedy 31.7 28.9 29.4 32.8 26.8 1.818 London / Gatwick 29.9 29.5 31.2 32.1 20.1 4.919 Miami / International 29.6 30.1 31.7 33.6 28.7 0.320 New York / Newark 29.6 29.0 30.5 34.2 25.8 1.5

Millions of Passengers

Airport Systems Planning & Design / RdN

Airports by millions of pax., 2003 (IATA data; US- Bold, hubs- italics)

In 2003, airport traffic mostly stagnated

Big drops in • Asian market (Hong Kong, Beijing, Singapore,

Tokyo – also Hawaii and San Francisco)• St Louis, Pittsburgh and Zurich as hubs close

Several airports have fallen lower in rankings (e.g. due to failures of TWA, Swiss, Sabena)

Airport Systems Planning & Design / RdN

Changes in Transfer Hubs

Big changes in recent years

New HubsBig: Paris/de Gaulle, Amsterdam, MunichSmall: London/Stansted

“Close” of old hubsPittsburgh (US shrinking to Philadelphia)St Louis (TWA merged out of existence)Zurich (collapse of Swissair)

Airport Systems Planning & Design / RdN

Airports by millions of pax., 2003 (IATA data; US- Bold, hubs- italics)

21 Bangkok 29.1 30.5 30.6 29.6 17.1 7.022 San Francisco / Internatl 28.8 30.7 34.6 41.2 32.0 -1.023 Orlando / International 27.3 26.7 28.2 30.8 21.5 2.724 Seattle / Tacoma 26.7 26.7 27.0 28.4 18.8 4.225 Hong Kong / C L K 26.4 33.5 32.6 32.7 24.4 0.826 Rome / Fuimicino 25.8 25.0 25.6 25.9 18.8 3.727 Toronto / Pearson 24.7 25.9 28.0 28.8 20.5 2.028 Philadelphia 24.7 24.4 23.9 24.9 16.5 5.029 Beijing / Pudong 24.4 27.2 24.2 21.7 *30 Sydney 24.2 23.4 24.3 23.5 16.6 4.631 Munich 24.0 23.0 23.6 23.1 12.5 9.232 Tokyo / Narita 23.5 25.8 25.4 27.4 20.0 1.833 Singapore 23.1 27.4 28.1 28.6 18.8 2.334 Charlotte 23.1 23.6 23.2 23.1 17.3 3.435 Boston / Logan 22.8 22.6 24.2 27.4 24.0 -0.536 Barcelona 22.5 21.2 20.7 19.8 *37 New York / LaGuardia 22.5 21.3 21.9 25.2 19.8 1.438 Paris / Orly 22.4 23.1 23.0 25.4 25.3 -1.139 Mexico City 21.7 20.3 20.6 20.7 *40 Cincinnati 21.2 20.9 17.3 22.5 12.3 7.2

Airport Systems Planning & Design / RdN

Airports by millions of pax., 2003 (IATA data; US- Bold, hubs- italics)

41 St. Louis / Lambert 20.4 25.6 26.7 30.5 19.9 0.342 Seoul/Gimpo 19.8 21.0 22.0 36.7 22.6 -1.243 Washington/Baltimore 19.7 19.0 * * *44 Manchester (UK) 19.5 18.6 19.5 12.8 5.245 Honolulu 19.4 21.1 21.1 22.7 22.0 -1.246 Palma de Mallorca 19.1 17.8 19.2 12.4 5.447 Osaka / Itami 18.8 * 19.3 20.5 *48 Fukuoka 18.8 * * * *49 London/Stansted 18.7 * * * *50 Jakarta 18.6 * * * *

Zurich 17.0 17.7 21.0 22.7 13.1 3.0Washington / Dulles 17.0 17.9 20.0 *

Brussels 15.2 19.6 21.6 *Pittsburgh 14.2 18.0 19.9 19.8 18.5 -2.3

Washington / Reagan 14.2 16.1 -1.2

Airport Systems Planning & Design / RdN

Current Major Airport ProjectsBangkok, Guangzhou Major New Airports Nagoya/Chubu Airport in the SeaOsaka/Kansai New Island for 2nd runwayToronto Buildings, Runways, etcLondon/HRW Terminal 5 ($8 billion)Washington/Dulles Mid-field Pax Bldg, etcMadrid ; Miami/Intnatl Runway, BuildingsNY / JFK; SFO; Singapore; Rail transit Boston/Logan ; Pax Buildings, Roads

Airport Systems Planning & Design / RdN

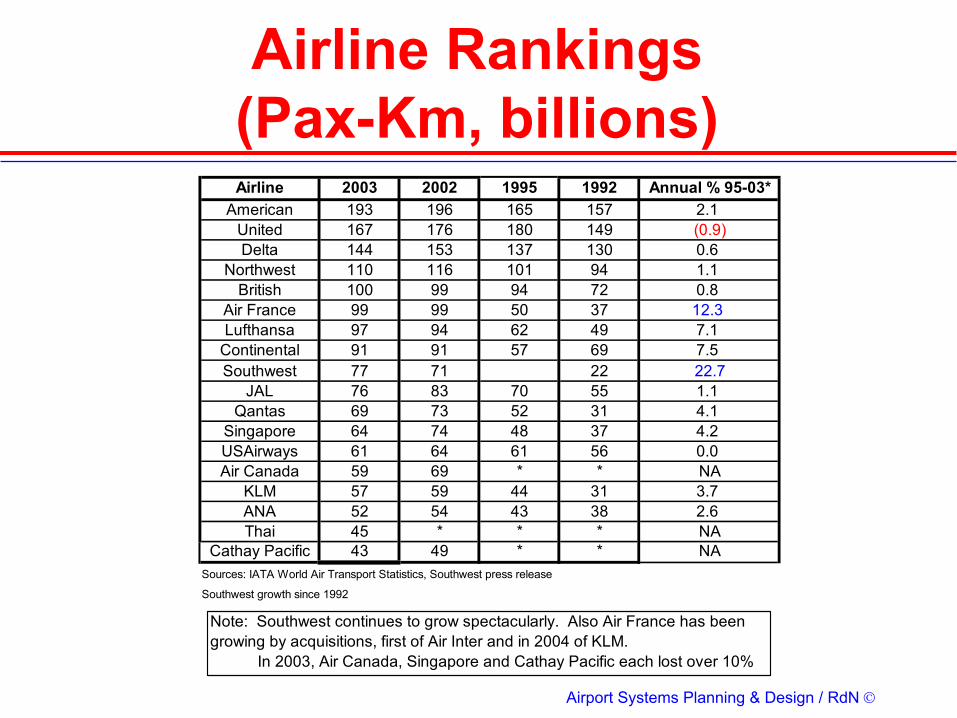

Airline Rankings (Pax-Km, billions)Airline 2003 2002 1995 1992 Annual % 95-03*

American 193 196 165 157 2.1United 167 176 180 149 (0.9)Delta 144 153 137 130 0.6

Northwest 110 116 101 94 1.1British 100 99 94 72 0.8

Air France 99 99 50 37 12.3Lufthansa 97 94 62 49 7.1

Continental 91 91 57 69 7.5Southwest 77 71 22 22.7

JAL 76 83 70 55 1.1Qantas 69 73 52 31 4.1

Singapore 64 74 48 37 4.2USAirways 61 64 61 56 0.0Air Canada 59 69 * * NA

KLM 57 59 44 31 3.7ANA 52 54 43 38 2.6Thai 45 * * * NA

Cathay Pacific 43 49 * * NASources: IATA World Air Transport Statistics, Southwest press release

Southwest growth since 1992

Note: Southwest continues to grow spectacularly. Also Air France has been growing by acquisitions, first of Air Inter and in 2004 of KLM. In 2003, Air Canada, Singapore and Cathay Pacific each lost over 10%

Airport Systems Planning & Design / RdN

Airline Rankings (Passengers, millions)

Airline 2003/4 2002/3 1995 1992 Annual % 95-03*American 89 94 80 86 1.4

Delta 84 90 87 83 (0.4)United 67 69 79 67 (1.9)

Southwest 66 64 * 28 12.3Northwest 53 54 49 44 1.0Lufthansa 44 44 33 27 4.2Air France 44 43 * 14 19.5

ANA 43 44 38 35 1.6US Airways 41 47 58 55 (3.7)Continental 38 40 35 38 1.1

British 35 34 32 25 1.2JAL 34 34 29 24 2.2

Iberia 25 24 * * NAQantas 24 24 * * NARyanair 23 21 NAAlitalia 22 22 21 20 0.6eastjet 22 21 NAKorean 21 22 22 20 (0.6)

Air Canada 20 23 * * NASAS 20 23 19 14 0.7

America West 20 19 17 15 2.2Japan Air Sys 19 21 * * NA

Westjet 7 6 * * NASources: IATA World Air Transport Statistics, airline press releases * Rates for 92-03

Note: The low-cost carriers continue to grow -- the legacy carriers stagnate US Airways and SAS lost over 10% in 2003

Airport Systems Planning & Design / RdN

Airline Rankings (Freight Tonne-Km, Billions)

Airline 2003 2002 1995 1992 % Change 00-02Fedex 13.2 13.0 7.0 5.8 11.1

Lufthansa 7.3 7.2 5.8 4.3 3.2Korean 6.9 6.0 4.3 2.7 7.6

UPS 6.7 6.6 * * NASingapore 6.7 6.8 3.7 2.9 10.1

Cathay Pacific 5.2 4.8 2.8 1.7 10.7Air France 4.9 4.9 4.4 3.3 1.4

China Airlines 4.7 4.5 * * NAEVA 4.7 4.1 * * NA

Japan 4.4 4.4 3.8 3.2 2.0Cargolux 4.3 4.2 * * NA

British 4.2 4.1 3.3 2.5 3.4KLM 4.1 4.0 3.6 2.4 1.7

Northwest 3.0 3.0 2.8 2.7 0.9Emirates 2.6 * * * NAAsiana 2.6 2.6 * * NA

American 2.6 2.6 2.4 1.6 1.0United 2.4 2.8 2.5 1.9 (0.5)Nippon 2.3 2.2 1.5 1.1 6.7

Source: IATA World Air Transport Statistics

Note: About 20% increases in 2003 for Korean, Cathay Pacific, EVA, Emirates

Airport Systems Planning & Design / RdN

Airline Rankings (Freight Tonne, millions)

Airline 2003 2002 1995 1992 % Change 00-02Fedex 13.2 13.0 7.0 5.8 11.1

Lufthansa 7.3 7.2 5.8 4.3 3.2Korean 6.9 6.0 4.3 2.7 7.6

UPS 6.7 6.6 * * NASingapore 6.7 6.8 3.7 2.9 10.1

Cathay Pacific 5.2 4.8 2.8 1.7 10.7Air France 4.9 4.9 4.4 3.3 1.4

China Airlines 4.7 4.5 * * NAEVA 4.7 4.1 * * NA

Japan 4.4 4.4 3.8 3.2 2.0Cargolux 4.3 4.2 * * NA

British 4.2 4.1 3.3 2.5 3.4KLM 4.1 4.0 3.6 2.4 1.7

Northwest 3.0 3.0 2.8 2.7 0.9Emirates 2.6 * * * NAAsiana 2.6 2.6 * * NA

American 2.6 2.6 2.4 1.6 1.0United 2.4 2.8 2.5 1.9 (0.5)Nippon 2.3 2.2 1.5 1.1 6.7

Source: IATA World Air Transport Statistics

Note: About 20% increases in 2003 for Korean, Cathay Pacific, EVA, Emirates

Airport Systems Planning & Design / RdN

Main Freight Airports(ACI data; US- Bold, hubs- italics)

Airport Growth, % Hub2000 2002 2003 3-yr rate

Memphis 2.45 2.63 3.39 12.8 FedexHong Kong / CLK 2.27 2.10 2.68 6.0Anchorage 1.88 1.69 2.10 3.9Tokyo/Narita 1.93 1.68 2.15 3.8Seoul / Incheon 1.87 1.20 1.84 (0.5)Los Angeles 2.05 2.12 1.83 (3.6)Paris/de Gaulle 1.38 1.48 1.72 8.2Frankfurt 1.71 1.61 1.65 (1.2)Miami/Internatl. 1.64 1.64 1.64 0.0Singapore 1.71 1.53 1.63 (1.6)New York/Kennedy 1.83 1.50 1.63 (3.6)Louisville 1.49 1.47 1.62 2.9 UPSChicago/O'Hare 1.46 1.28 1.51 1.1Taipei 1.21 1.19 1.50 8.0Amsterdam 1.27 1.23 1.35 2.1London/Heathrow 1.40 1.26 1.30 (2.4)Shanghai/Pudong * * 1.19Indianapolis 1.17 1.15 0.98 (5.4)Dubai * * 0.96Bangkok 0.87 0.82 0.95 3.1New York/Newark 1.09 0.80 0.84 (7.6)Atlanta 0.87 0.74 0.80 (2.7)

Tons, Millions

Airport Systems Planning & Design / RdN

Main Freight Airports(ACI data; US- Bold, hubs- italics)

Osaka/Kansai 1.00 0.87 0.79 (7.0)Tokyo/ Haneda na 0.72 0.72Dallas/Fort Worth 0.90 0.79 0.67 (8.5)Beijing * * 0.66San Francisco 0.77 0.56 0.61 (6.9)Dayton 0.83 0.55 CNF/MenloSource: ACI web 2004 and World Report Mar/Apr 2001, 2002; Airport reports

Major increases at: Memphis, Paris/de Gaulle, Taipei, Shanghai/Pudong, Dubai, Beijing

Major decreases at: Los Angeles, Indianapolis, Osaka/Kansai, New York/Newark, Dallas/Fort Worth, San Francisco/Inter.

US Airports in Bold, Cargo hubs in Italics

Airport Systems Planning & Design / RdN

Airline Rankings (Employees, thousands)

Airline

2003 1992%Change

'92-'03 2003 1992 2003 1992American 78 91 (14) 1.1 0.9 2.5 1.7

United 63 84 (25) 1.1 0.8 2.7 1.8Delta 60 79 (24) 1.4 1.1 2.4 1.6

Air France 60 43 40 0.7 0.3 1.7 0.9British 50 47 6 0.7 0.5 2.0 1.5

Continental 40 36 11 1.0 1.1 2.3 1.9Northwest 39 46 (15) 1.4 1.0 2.8 2.0Lufthansa 39 48 (19) 1.1 0.6 2.5 1.0Southwest 33 11 200 2.0 2.5 2.4 2.0US Airways 27 47 (43) 1.5 1.2 2.3 1.2

Qantas 27 15 80 0.9 0.3 2.6 2.1Iberia 26 26 0 1.0 0.6 1.6 0.9Thai 26 19 37 0.7 0.5 1.7 1.1KLM 25 26 (4) 0.8 0.3 2.3 1.2

Malaysia 23 20 15 0.7 0.7 1.6 0.8Indian 20 * * 0.4 * 0.8 *Norm ~1.1 ~0.7 ~2.3 ~1.4

Sources: IATA World Air Transport Statistics, 99 data for Southwest from www.southwest.com

Pax / Emp Pax-km / Emp(thousands) (millions)

Employees(thousands)

Note: Major airlines have shed employees and improved labor productivity rapidly over decade. Air France is toward bottom end, Southwest is at top.

Airport Systems Planning & Design / RdN

Aircraft Inventory (Jet Fleet)

Airline 2003 2002 1995 % Change 95-03American 783 822 635 2.9

Delta 550 573 539 0.3United 532 567 556 (0.5)

Southwest 388 378 224 9.2Northwest 364 438 380 (0.5)Continental 342 352 314 1.1

Fedex 339 328 249 4.5Lufthansa 303 324 234 3.7

British 282 319 222 3.4US Airways 279 280 394 (3.6)

UPS 257 250 166 6.9Air France 230 252 156 5.9Air Canada 208 244 * NA

China Southern 191 122 * NAJAL 189 131 126 6.3

Iberia 149 147 * NAANA 149 * * NA

Qantas 144 141 * NASaudi 143 127 * NAKLM 142 * * NASAS 131 * 128 0.3

Alitalia 94 132 144 (4.3)Aeroflot 90 102 * NAeasyjet * 72 * NARyanair 67 67 * NA

Sources: IATA World Air Transport Statistics, airline web sites

Note: Biggest innovative airlines continue to grow and advance in rankings. Legacy airlines stagnate or shrink, absent consolidation.

Airport Systems Planning & Design / RdN

Economic Deregulation

DeregulationFull: USA, Canada, Australia, South AfricaMostly: European Union

Result: Competition, Cost CutsExisting Airlines have difficulty with staffNew Airlines start with new, younger staff with lower pay, more flexibility, less sense of entitlement...

Airport Systems Planning & Design / RdN

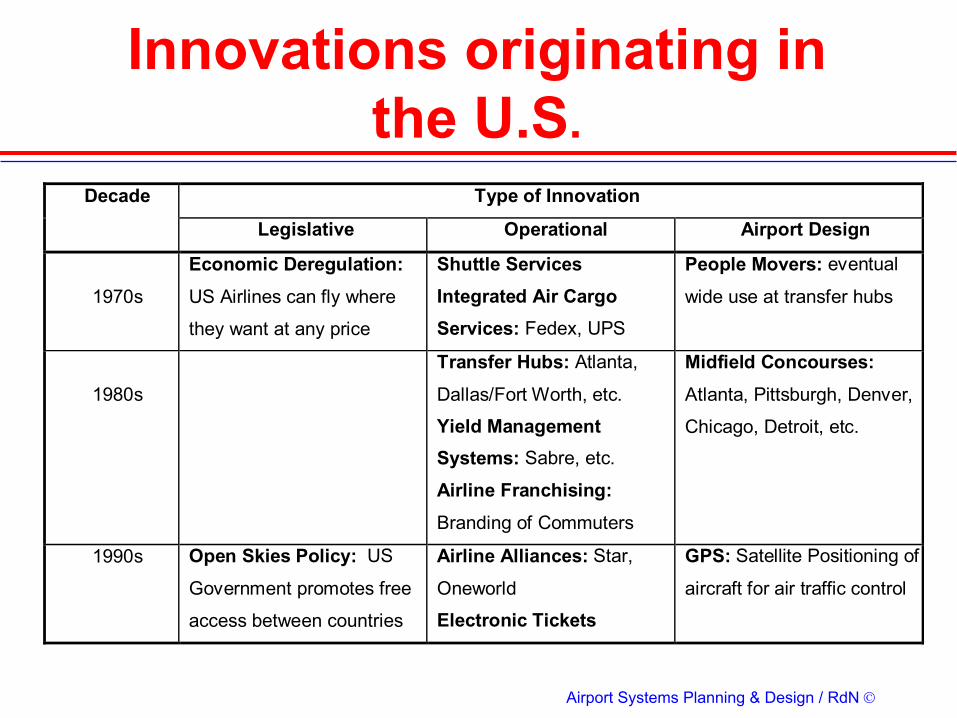

Innovations originating in the U.S.

Type of InnovationDecade

Legislative Operational Airport Design

1970s

Economic Deregulation:US Airlines can fly where

they want at any price

Shuttle ServicesIntegrated Air CargoServices: Fedex, UPS

People Movers: eventual

wide use at transfer hubs

1980s

Transfer Hubs: Atlanta,

Dallas/Fort Worth, etc.

Yield ManagementSystems: Sabre, etc.

Airline Franchising:Branding of Commuters

Midfield Concourses:Atlanta, Pittsburgh, Denver,

Chicago, Detroit, etc.

1990s Open Skies Policy: US

Government promotes free

access between countries

Airline Alliances: Star,

Oneworld

Electronic Tickets

GPS: Satellite Positioning of

aircraft for air traffic control

Airport Systems Planning & Design / RdN

Privatized status of airlines, previously publicly owned

Airline Comments Stock sign Price, Sept 04 Aerolineas Argentinas Air Canada Near bankruptcy AC.TO 0.07 Air France Govt. owns 44% AKH 16 Air New Zealand Govt. owns 74% ANZFF.PK 0.26 Alitalia Near bankruptcy ALRMF.PK 0.25 British Airways BAB 41 Iberia Govt owns 5%

and Gold Share IBRLF.PK 3

Japan Air Lines Took over JAS JALSY.PK 14 Lufthansa (Germany) DLAKY.PK 11.5 Qantas Owns Australian QUBSF.PK 2.5 SAS (Scandinavia) Govts own 50% BASDF.DK 5.6

Airport Systems Planning & Design / RdN

Airline Market “Caps” (=price/share x shares)

Airline Symbol Market Capitalization2004 2001 Feb-03 Sep-03 Dec-03 Aug-04 US $, billions, Aug 04

UPS UPS 55 59 63 75 72 80.8Fedex FDX 42 52 66 70 82 24.5Southwest LUV 18 13 18 16 15 11.7Ryan Air * RYAAY 25 39 45 51 30 4.5British BAB 48 19 29 42 41 4.4Lufthansa DLAKY.PK * 9 14 16 11.5 4.4Air France AKH * * * * 16 3.4Jet Blue * JBLU 12 31 27 26 2.7American AMR 32 3 13 13 9 1.5easyjet EJETF.PK 3 4 4 5 3 1.2AirTran AAI 17 12 12 1.1Northwest NWAC 21 6 10 13 10 0.8Continental CAL 44 6 18 16 10 0.6Alaska ALK 33 19 29 28 22 0.6KLM KLMR.PK 15 7 11 16 12 0.6Delta DAL 38 9 14 12 4 0.5Westjet * WJA.TO 18 11 16 19 13 0.4America West AWA 10 2 10 12 7 0.2Hawaiian HA 3 2 1 3 7.8 0.2JAL JALSY.PK 6 11 13 13 14 NAUSAirways UAIR 13 0.2 Ch 11 6 2 0.1Air Canada ac.to 6 3 1 1 0.07 0United 33 1 Ch 11 NA 0 0Airborne Freight 14 15 mergedTWA 0 mergedSources: Yahoo Finance and Google *Adjusted for Stock Split

US $/Share

Airport Systems Planning & Design / RdN

Airport Market “Caps” (=price/share x shares)

Airport % Change US$, Billions2001 2002 2003 2004 2001 -2004 Market Cap

BAA 6.13 6.2 5.1 5.5 (10) 10.70Fraport * 25.6 19.6 23 NA 2.51Copenhagen 770 589 460 885 15 1.31AIAL (New Z.) 3.46 4.54 5.27 6.75 95 1.27Beijing 2.03 1.82 1.65 2.33 15 1.15Vienna 39.1 34.6 31.5 43.8 12 1.11TBI 0.81 0.62 0.52 0.64 (21) 0.65ASUR (Mexico) 18.1 13.4 13.9 18.4 2 0.55Malaysia 1.54 2.15 1.46 1.41 (8) 0.41Zurich 201 124 34 101 (50) 0.39Florence * * 15.8 9.8 NA 0.11Source: Jane's Airport World, Summer issues

Share Price, Local Money

Many airports are economically more powerful than airlines!

Airport Systems Planning & Design / RdN

Airline Alliances

Star Alliance -- United, Lufthansa, Air Canada, Varig, ANA, Singapore, Thai, Air New Zealand, SAS, Asiana, Bmi, LOT Austrian, Tyrolean, Spanair

oneworld -- American, British, Aer Lingus, Finnair, Iberia, Qantas, Cathay Pacific, Lan Chile

Wings -- KLM, Northwest, Continental SkyTeam -- Air France + KLM, Delta, Alitalia, Korean,

Aeromexico, CzechAeroflot? China Southern? Wings???

Airport Systems Planning & Design / RdN

Alliances’ Market Shares

Alliance Measure Year

Star Oneworld Sky Team KLM/NW 2002 123 86 57 29 Pax

Millions 2003 118 84 56 282002 441 309 198 110 Pax-Km

Billions 2003 417 306 193 1042002 278 244 176 72 Employees

Thousands 2003 255 219 169 642002 24 18 13 7 % of IATA

Traffic 2003 25 18 13 7

Relative strength of Alliances has been stable. However, Air France KLM merger may lead to consolidation of Sky Team with KLM/NW

Airport Systems Planning & Design / RdN

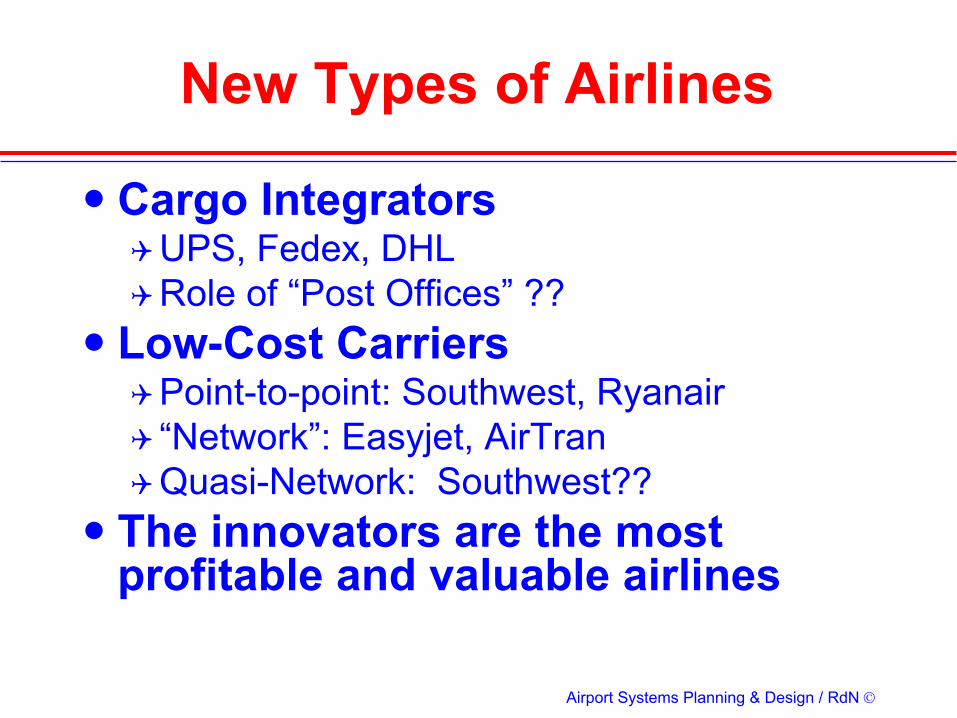

New Types of Airlines

Cargo IntegratorsUPS, Fedex, DHLRole of “Post Offices” ??

Low-Cost CarriersPoint-to-point: Southwest, Ryanair“Network”: Easyjet, AirTranQuasi-Network: Southwest??

The innovators are the most profitable and valuable airlines

Airport Systems Planning & Design / RdN

Challenge to TraditionalNetwork Carriers

Is their business model working?Will people pay enough for convenience of

• easy connection at hubs• big expensive passenger buildings• travel agents

If not, what will they do?Squeeze out costs (wages, standards) and survive on a more modest scale?Manage by having “cheap” partners• Delta -- Song; United -- Ted…

Or disappear? Swissair, USAir? United?

Airport Systems Planning & Design / RdN

Consequences for Airports

Cheaper travel will increase traffic Where will it go?

To traditional hubs of legacy majors?To/from leisure locations and homes?

• Malaga, Faro, Bali, etcTo secondary airports?

• London/Stansted, Frankfurt/Hahn, Rome/Ciampino, etc.

Airport customers likely to demand new locations, cheaper facilities

Airport Systems Planning & Design / RdN

Meanwhile...

The nature of the Airport Business is changing dramatically

More Commercially orientedLess Government controlMore competition from “new” entrants

• Providence, Cincinnati, Lübeck, Liverpool...

Not at all clear that current generation of airport professionals fully recognizes what this means