current hot topics in fixed income markets & public finance

TRANSCRIPT

Current Hot Topics in Fixed Income Markets & Public Finance

1

Presented & Recorded:November 18, 2020

RBC Capital Markets, LLC (“RBC CM”) is providing the information contained in this presentation for discussion purposes only and not inconnection with RBC CM serving as underwriter, investment banker, municipal advisor, financial advisor or fiduciary to a financial transactionparticipant or any other person or entity. RBC CM will not have any duties or liability to any person or entity in connection with theinformation being provided herein. The information provided is not intended to be and should not be construed as “advice” within themeaning of Section 15B of the Securities Exchange Act of 1934. The recipient should consult with its own legal, accounting, tax, financial andother advisors, as applicable, to the extent it deems appropriate.

The information contained in this presentation has been compiled from sources believed to be reliable, but no representation or warranty,express or implied, is made by the RBC CM, its affiliates or any other person as to its accuracy, completeness or correctness. The informationand any analyses in these materials reflect prevailing conditions and RBC CM’s views as of this date, all of which are subject to change. Theprinted presentation is incomplete without reference to the oral presentation or other written materials that supplement it.

The material contained herein is not a product of any research department of the RBC CM or any of its affiliates. Nothing herein constitutes arecommendation of any security regarding any issuer, nor is it intended to provide information sufficient to make an investment decision.

IRS Circular 230 Disclosure: RBC CM and its affiliates do not provide tax advice and nothing contained herein should be construed as tax advice.Any discussion of U.S. tax matters contained herein (including any attachments) (i) was not intended or written to be used, and cannot beused, by you for the purpose of avoiding tax penalties; and (ii) was written in connection with the promotion or marketing of the mattersaddressed herein. Accordingly, you should seek advice based upon your particular circumstances from an independent tax advisor.

This presentation is proprietary to RBC CM and may not be disclosed, reproduced, distributed or used for any other purpose without RBCCM’sexpress written consent. To the fullest extent permitted by law, RBC CM, any of its affiliates, or any other person, accepts no liabilitywhatsoever for any direct or consequential loss arising from any use of this communication or the information contained herein.

Disclaimer

2

PresentersBrian CooperDirectorBaker Tilly Municipal Advisors, LLC(614) [email protected]

Andrew LaskeyVice PresidentRBC Capital Markets(513) [email protected]

3

Topics to be Discussed Market Recap and Regulatory Update Long Term Debt vs. Short Term Debt OMAP Overview Capital markets issuance compared to a private placement or

direct loan Credit rating issues- COVID-19 impacts and other updates

4

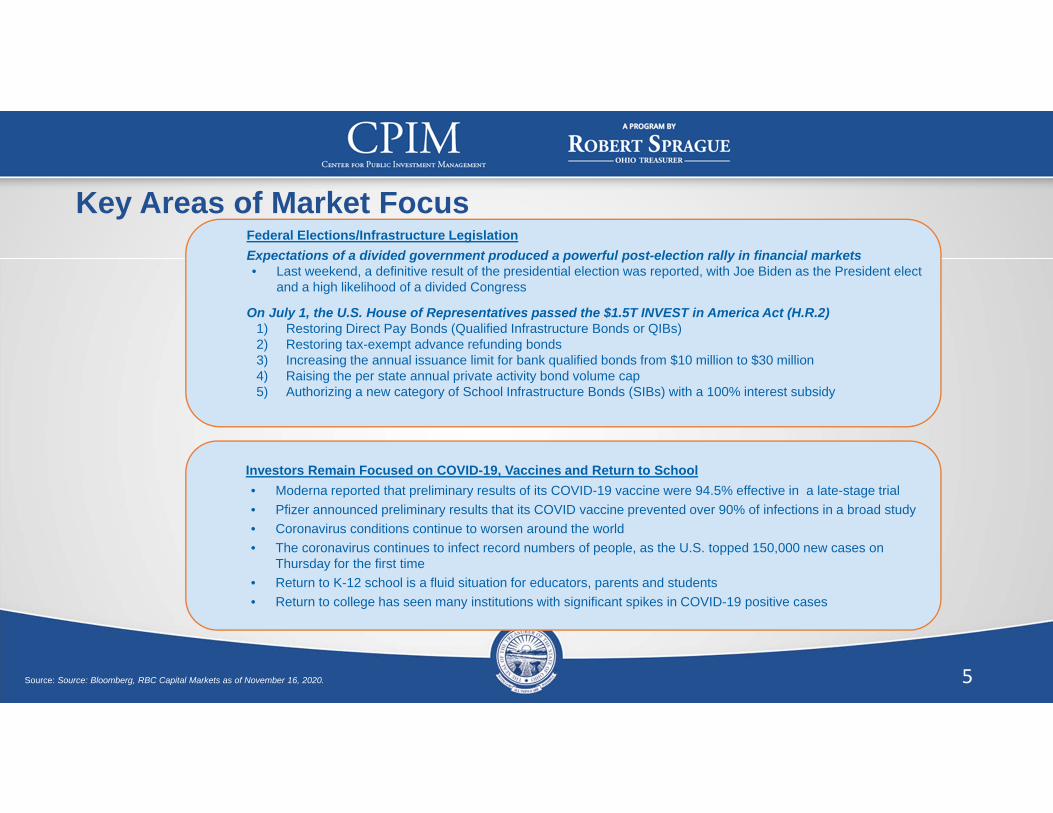

Key Areas of Market Focus

Source: Source: Bloomberg, RBC Capital Markets as of November 16, 2020. 5

Federal Elections/Infrastructure LegislationExpectations of a divided government produced a powerful post-election rally in financial markets• Last weekend, a definitive result of the presidential election was reported, with Joe Biden as the President elect

and a high likelihood of a divided Congress

On July 1, the U.S. House of Representatives passed the $1.5T INVEST in America Act (H.R.2)1) Restoring Direct Pay Bonds (Qualified Infrastructure Bonds or QIBs)2) Restoring tax-exempt advance refunding bonds3) Increasing the annual issuance limit for bank qualified bonds from $10 million to $30 million4) Raising the per state annual private activity bond volume cap5) Authorizing a new category of School Infrastructure Bonds (SIBs) with a 100% interest subsidy

Investors Remain Focused on COVID-19, Vaccines and Return to School• Moderna reported that preliminary results of its COVID-19 vaccine were 94.5% effective in a late-stage trial• Pfizer announced preliminary results that its COVID vaccine prevented over 90% of infections in a broad study• Coronavirus conditions continue to worsen around the world• The coronavirus continues to infect record numbers of people, as the U.S. topped 150,000 new cases on

Thursday for the first time• Return to K-12 school is a fluid situation for educators, parents and students• Return to college has seen many institutions with significant spikes in COVID-19 positive cases

Economic Overview

Source: Bloomberg and RBC Economics 6

Moody’s Analytics & CNN Business “Back to Normal Index” Moody’s Analytics and CNN Business have partnered to create a proprietary Back-to-Normal Index, comprised of 37 national and seven state-level

indicators The index ranges from zero, representing no economic activity, to 100%, representing the economy returning to its pre-pandemic level in March Ohio as a whole (87% “Back to Normal”) is recovering better than the United States (81% “Back to Normal”) This is due to many factors but includes a diversified economy not overly reliant on any one sector Leisure, hospitality, tourism and business travel are some slowest sectors to recover and face significant recovery challenges until people feel comfortable

in congregate settings

“Back to Normal Index” Ohio vs. United States from March to Today

Source: Moody’s Analytics & CNN Business. https://www.cnn.com/business/us-economic-recovery-coronavirus 7

Ohio K-12 School Reopening Models (As of Nov. 12, 2020)Current Education Models by District

Source: Ohio Department of Education; http://education.ohio.gov/Topics/Reset-and-Restart as of Nov. 12, 2020 8

5-Day Return43%

Hybrid42%

Fully Remote15%

Ohio Public K-12 Students

Interest Rate Movements10 Year MMD and 10 Year UST5 Year MMD(1) and 5 Year UST 30 Year MMD and 30 Year UST

(1) MMD stands for Municipal Market Data; a daily index all municipal bond pricings are based off ofSource:Thomson Reuters 9

Overview of Municipal SupplyMonthly Projected Supply and Redemptions

30‐Day Visible Supply Secondary Market Bid‐Wanted Volume

Source: Bloomberg 10

Municipal Bond Fund FlowsAccording to data from Lipper, for the week ended November 11, 2020, weekly Municipal bond funds reported $1.17 billion of net inflows last week, following the previous week’s outflows of $954 million

All of the municipal bond subsectors reported inflows with the exception of the intermediate bond fund subsector

Four week moving average was positive at $350 million of inflows, up from last week’s number of $212 million

11

‐8.0

‐7.0

‐6.0

‐5.0

‐4.0

‐3.0

‐2.0

‐1.0

0.0

1.0

2.0

3.0

4.0

Billion

s

Flow Change 4‐WK Moving Average

Taxable Issuance Continues to IncreaseTaxable Market Commentary

Taxable issuance has increased annually since 2018 when the Tax Cuts and Jobs Act of 2017 eliminated the ability to advance refund tax exempt debt on a tax exempt basis In 2019 and 2020 a dramatic decline in taxable interest rates further increased the prevalence of taxable issuance in the municipal market In addition to taxable advance refundings some issuers have issued taxable debt for other reasons related to the use of proceeds

These include private use of proceeds and arbitrage purposes among other reasons Through October 30, 2020 taxable issuance has comprised 31% of the municipal market, the highest percentage of the muni market since

the height of the BAB & QSCB era (2010)

Source: Refinitiv (based on data available on October 30, 2020). 12

Advance Refundings with Taxable BondsTaxable Refunding Mechanics

Long-term taxable bonds can be issued which are not subject to the yield restriction and arbitrage rebate rules accompanying tax-exempt bonds Negative arbitrage in the escrow would still be a factor, just like in tax-exempt advance refundings

The shape of the US Treasury yield curve is a factor in determining the economic viability of taxable advance refunding bonds The current yield curve has steepened post COVID due to short term interest rates declining close to 0% but long term rates have declined to near historic all time lows

Taxable yields are almost always higher than tax-exempt yields, especially on the short and intermediate parts of the yield curve, potentially reducing the savings compared to those that could be realized in a tax-exempt advance refunding

US Treasury Yield Curve (Interpolated)

13

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

01/02/2020 11/16/2020

Source: www.treasury.gov (30 year yield curve completed using linear interpolation)

Bond Anticipation Notes: Advantages & Disadvantages Bond Anticipation Notes (BANs) are a commonly used tool to finance capital improvements for Ohio issuers

BANs typically have a maturity of one year or less At maturity, the BAN is refinanced with a new BAN, a bond or cash on hand (or a combination of the three)

BANs have the following advantages: BANs have the advantage of carrying a short-term interest rate, which is typically lower than long term bond rates BANs also allow for a more flexible repayment structure since the issuer can determine what amount of the principal

balance to pay down annually BANs typically are lower cost and take less time to bring to market (30 to 60 days)

BANs have the following disadvantages: A greater administrative burden as new legislation must be adopted, financing team must be engaged, and financing

must be completed annually Cost of issuance must be paid annually and as the BAN size becomes smaller, costs of issuance have a larger

impact on all in borrowing cost The interest rate is set annually which leaves the issuer susceptible to changes in interest rates (known as “interest

rate risk”)

14

Ohio Market Access Program (OMAP)State of Ohio – Ohio Market Access Program (OMAP) OMAP created in 2011 to lower borrowing costs on short-term notes issued by Ohio schools, cities and local

governments. OMAP provides credit enhancement on municipal notes via a standby note purchase agreement. Standard & Poor’s has assigned its highest municipal short-term note rating -- “SP-1+” -- to notes issued through

OMAP. Program credit enhancement saves money on debt service for Ohio municipal issuers by lowering the interest

rate paid on note issuances. The program leverages the state’s high short-term credit rating to help improve market access. Since 2014, the OMAP Program has been used for a total of over $800 billion in par amount of note issues and

has saved Ohio issuers a total of over $2.9 million in interest costs.

15

Bonds: Advantages & Disadvantages Bonds are also commonly used tool to finance capital improvements for Ohio issuers

Bonds typically have a maturity of 5 to 40 years They typically carry fixed interest rates They typically have a call option allowing for the refunding of bonds for restructuring or savings 7 to 10 years after initial issuance

Bonds have the following advantages: Interest rates are fixed for the life of the issue so the payment schedule is known and can be budgeted for Financing is completed once without the need for annual financings and the administrative burden that comes with annual

financings

Bonds have the following disadvantages: The principal payment structure is fixed and cannot be modified (especially in the first 7 to 10 years in the non callable period) Historically interest rates on fixed rate bonds tend to be higher than those carried on short term securities like BANsWhen Bonds are sold in the capital markets an official statement must be prepared and credit rating must be obtained (neither of

which are required for a BAN issue)

16

Privately Placed Loan Considerations Bank loans are often solicited with the assistance of a solicitation agent

A solicitation agent’s role is to assist a municipal issuer in the structuring and solicitation of a direct loan This may involve: structuring the borrowing or refunding, soliciting lender offers through the distribution of a

term sheet, negotiating terms and assisting in post issuance closing and reporting requirements

If a bank loan solicitation process is run, a term sheet is typically distributed that describes all relevant details of the loan to prospective lenders. Details of the term sheet include: The borrowing amount The security of the loan (ex. General obligation, Lease Purchase, etc.) The credit rating (if applicable) The optional redemption date (if applicable) The repayment schedule A request to provide all fees charged to the borrower related to the borrowing

A solicitation agent will work with the District and Bond Counsel to create this document and disseminate to all active direct lenders in the Ohio market, review responses, and assist in finalizing terms and closing the transaction

17

Private Loans: Potential Benefits Potential benefits of a bank loan:

An offering document is not typically required (the Official Statement) dramatically reducing the amount of time associated with a bond issue

A credit rating is not typically required, again reducing issuance fees and time associated with a rating presentation to a credit rating agency, including presentation reviews, preparation and further annual surveillance

Privately placed bank loans are exempt from 15(c)2-12 (Continuing Disclosure)

The time from financing kickoff to closing is considerably shorter because of these factors This allows issuers to lock in interest rates and receive funds sooner than a comparable public market transaction

Many times interest rates are comparable to a typical public market bond issue A solicitation agent can provide public market interest rate estimates to compare a bank loan before an agreement

is reached to ensure the issuer is aware of available options and estimated interest rates associated with each

18

Private Loans: Limitations Lending Institutions that provide bank loans often do not wish to lend for longer final maturities

Generally 15 years and less is desired 20 years may be achievable, but the pool of lenders may be smaller

The size of the loan can affect the efficiency of a bank loan when compared to a publicly offered underwriting Often loans under $10 million are considered good candidates for a bank loan Some smaller community banks may have a lending limit that precludes participation

The type of security can also limit the prospective pool of lenders Some lending institutions may wish only to provide a direct loan under a general obligation pledge, and may not

provide a loan for a lease structure (COPS Issue)

19

Private Loans: Reporting Considerations While bank loans are exempt from continuing disclosure, the best practice is to publish bank loan information to

EMMA

Information to be posted to EMMA

Full Issuer Name, Name of Issue, Closing Date, Maturity Date, Interest Rate (if multiple maturities provide debt schedule), Security Type (general obligation/ revenue)

The District’s solicitation agent or bond counsel can assist with publishing this information to EMMA

If the District maintains a credit rating from Moody’s, Standard & Poor’s or Fitch, they require bank loan information to be sent to them

20

Credit Rating Agency Updates Thus far most rating agency action has been related to sectors, credits and taxes that have been particularly hard

hit by the COVID-19 pandemic These include transportation credits, entities or securities funded primarily through tourism related taxes,

select higher education institutions, etc.

We have not seen widespread rating changes based solely on the presumption of future budgetary challenges

Most Ohio municipalities entered the pandemic in a strong financial position holding historically high cash reserves

There is a belief that while municipalities will likely face challenges that they will be able to use cash reserves and manage expenses to maintain credit position

Future federal stimulus could provide additional funding to impacted municipalities

21

Credit Rating Agency Updates (Continued) On August 19, 2020 Standard & Poor's published “Credit Trends: U.S. Public Finance Upgrades Fall To A Historic Low”

There were 207 downgrades and only 9 upgrades, a historic low, in U.S. public finance Deteriorating financial conditions led to the most downgrades, with 64, followed by business conditions with 47 and liquidity with 41 These credit rating changes represent less than 1% of all S&P rated public finance entities A review of the downgrade list shows few, if any, Ohio local governments

Moody’s Investors Service upgraded 52 and downgraded 81 public finance entities in the second quarter of 2020 nationwide Within Ohio there were 2 upgrades and 1 downgrade in Q2 2020

Standard & Poor’s Historic Rating Actions by Quarter

Sources: Standard & Poor’s, Credit Trends: U.S. Public Finance Upgrades Fall To A Historic Low published August 19, 2020. Moody’s Investors Service MFRA Database search conducted on September 22, 2020 22

Moody's Rating Agency MethodologyMoody's develops a scorecard comprised of 4 factors: This indicative score can be further “notched” upward or downward based on qualitative factors, other pertinent statistics, or extreme results in any single statistic

Factor 1: Economy/Tax BaseWhy it MattersThe ultimate basis for repaying debt is the strength and resilience of the local economy. The size, diversity, and strength of a local government’s tax base and economy drive its ability to generate financial resources. The taxable properties within a tax base generate the property tax levy. The retail sales activity dictates sales tax receipts. The income earners living or working in the jurisdiction shape income tax receipts. The size, composition, and value of the tax base, the magnitude of its economic activity, and the income levels of its residents are therefore all crucial indicators of the entity’s capacity to generate revenues.

Factor 2: FinancesWhy it MattersA local government’s fiscal position determines its cushion against the unexpected, its ability to meet existing financial obligations, and its flexibility to adjust to new ones. Financial structure reflects how well a local government’s ability to extract predictable revenues adequate for its operational needs are matched to its economic base.

Factor 3: ManagementWhy it MattersBoth the legal structure of a local government and the practical environment in which it operates influence the government’s ability to maintain a balanced budget, fund services, and continue tapping resources from the local economy. The legal and practical framework surrounding a local government shapes its ability and flexibility to meet its responsibilities.

Factor 4: Debt/PensionsWhy it MattersDebt and pension burdens are measures of the financial leverage of a community. Ultimately, the more leveraged a tax base is, the more difficult it is to service existing debt and to afford additional debt, and the greater the likelihood that tax base or financial deterioration will result in difficulties funding fixed debt service expenditures.

Description of “Why it Matters” from Moody’s Investors Service US Local Government G.O. Debt Rating Methodology 23

Adjustments or Mitigating Factors The scorecard provides a grounds for discussion on certain quantifiable metrics used in the rating process, but the process still involves a significant degree of judgment

It is not a calculator. There are many qualitative factors that cannot be measured and overriding factors that are very important when making the final rating decision.

Below are some examples of adjustments that may be made to the rating:

Source: Moody’s Investors Service, Various publications 2018-2020 24