currency risk outlook report – 2017 - … firms have taken a hard look at their currency risks and...

TRANSCRIPT

afex.com

March 2017

CURRENCY RISK OUTLOOK REPORT – 2017

2 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

No one will forget 2016 in a hurry. The rise of populism that was seen to underpin the ‘Brexit’ vote in the UK and the election of President Trump in the U.S. made sure of that. Political uncertainty has led to volatility in international currency markets, which was most profoundly seen in the fall in the value of sterling following the UK’s June 2016 referendum on EU membership, as well as a growing circumspection about the future of tariff-free trade and globalization’s unhalted decades-long march.

Providing global payment and currency risk management solutions for more than 35,000 clients worldwide, AFEX is uniquely positioned to understand the challenges of international commerce. At the same time, we work continuously to ensure we have the clearest view of issues and opportunities affecting the businesses we work with. Now in its third year, the Currency Risk Outlook is part of that work.

We questioned more than 650 of our SME client base worldwide, to explore their experiences and attitudes towards global trade, and their approaches towards managing currency risk.

The responses offer fascinating insight into the concerns and expectations for growing businesses trading beyond their domestic borders.

While this report highlights mounting uncertainty, particularly in regions that have witnessed at first hand political upheavals that are perceived in part as a backlash against globalization, it also reveals a business community that will continue to take advantage of the opportunities presented by global trade. In many ways, international trade has never been easier, nor the prizes greater, thanks in part to technology. The rise of online commerce platforms, such as Amazon, eBay and Etsy, coupled with advancements in payments technologies are making it easier for firms to buy and sell on the global stage.

At the same time, whole new markets are being created through the financial inclusion enabled by online and mobile technologies, presenting ever more opportunities for those trading internationally.

We hope you find the results valuable and, of course, welcome any questions they may prompt with regard to your own business.

Jan VlietstraChief Executive Officer, AFEX

Uncertain times

3 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

4

5

6

8

9

10

11

12

Contents

Executive summary 4

Exposure to currency risk & volatility expectations 5

Challenges to managing FX risk 7

Use of hedging tools 10

Drivers of hedging strategies 12

Attitudes to international trade 13

Challenges to international trade 15

Appendix 16

4 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

15%of surveyed firms in UK say they have 100% of their revenues exposed to currency risks

The third annual Currency Risk Outlook reveals that businesses trading internationally have been buffeted by currency volatility over the last 12 months and are anticipating more to come this year. Such anticipation is acutely felt by the UK contingent of respondents that had to contend with a steep decline in the value of Sterling following the EU referendum in June 2016 and where international trade policy is now being redefined.

However, this political earthquake, followed by the election of President Trump in the US at the end of 2016 seem to have had a dramatic impact on how many businesses look at international trade. Many firms have taken a hard look at their currency risks and international strategies, becoming more conservative about growth expectations and factoring in increased uncertainty. For example, currency hedging tools were more regularly used in 2016 than they were in 2015.

This trend looks set to continue in 2017 and is most pronounced in the UK. The increased use of currency hedging tools is not surprising since firms here have witnessed at first hand a large fall in the value of currency but across all markets, this is being driven by increased uncertainty about international markets and global economic policy.

Executive summary

56%of surveyed firms are expecting greater volatility in 2017 than last year

5 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Overall, firms’ exposure to currency risks has increased this year, with the average proportion of total revenue exposed increasing from 38% to 47%. This is highest in the UK where firms have over half (56%) of their revenue exposed. Indeed, 15% of UK firms have 100% of their revenues exposed to currency risks. While U.S. firms typically have a lower proportion of their revenue exposed than other regions (39%) this has increased by 10 percentage points since the survey was last conducted.

The majority of respondents (56%) are expecting greater volatility in 2017 than last year. This is the highest proportion since the started (2015=42%; 2014=37%), perhaps reflecting widespread uncertainty about the future of globalization and global trade and a growing recognition of the influence of political factors on currency movements. Firms in Australia are particularly expectant of volatility with 62% anticipating more, compared to just 4% saying they expect less.

40%44%

43%35%

56%

37%

2015 2016

Australia

UK

North America

What percentage of your revenue is exposed to currency risk?

Exposure to currency risk & volatility expectations

40%46%

29%

39%

38%

47%

Canada

USA

Total

6 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Percentage of respondents expecting greater currency volatility in 2017 than 2016. (previous year’s answers in dark orange)

62%

42%

56%

36%

39%

58%

53%

33%

52%44%

Australia

UK

North America

Canada

USA

42%

56%

Total

7 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

40%of surveyed firms in US say the biggest event has been US monetary policy

33%of surveyed firms in Australia say the US presidential election impacted currency risk mitigation strategies - this is more than domestic monetary policy (30%)

Global events have had a significant effect on respondents’ currency risk mitigation strategies over the last 12 months. Although these vary from country to country, by far and away the biggest single factor affecting any country is the Brexit decision for the UK, with 71% saying it has had an impact. UK monetary policy comes a distant second to that with one in five (22%) citing it as having an impact.

In the US the biggest event has been US monetary policy (cited by 40%), which is perhaps not surprising given the Federal Reserve announced the first interest rate rise in over 10 years and signaled more to come in 2017. Secondary issues here were Brexit (26%), the US presidential election (24%) and EU monetary policy (23%).

Events in the US were also dominant for firms in Canada and Australia. In Australia, US monetary policy (40%) and the US presidential election (33%) impacted currency risk mitigation strategies more than domestic monetary policy (30%).

In Canada, the oil price was also a significant factor influencing currency risk mitigation strategies, cited by 29%.

Overall, volatility remains the biggest challenge to mitigating currency risk in 2017 with 59% of respondents saying that. This has increased dramatically in the UK from 55% in 2015 to 71% now. Conversely, this has decreased as a concern for US companies (2015=63%; 2017=45%) and Canadian companies (2015=66%; 2017=53%). For US companies, the biggest challenge to managing currency risk in 2017 is anticipated to be an uncertain global economic policy environment (56% compared to 33% in 2015). This is the first time this has been the biggest concern for US firms.

Challenges to managing FX risk

71%of surveyed firms in UK say that the Brexit decision had an impact

8 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Which global events have most affected your company’s currency risk mitigation strategy in the last 12 months? (Please choose all that apply)

13%

7%

10%3%3%

5%1%

40%12%

22%4%15%

12%

18%12%15%

23%

33%

30%40%

1%1%0%1%

1%

30%1%0%

8%5%

33%15%

31%25%

24%

19%10%

12%14%

16%6%

12%

5%6%

29%7%11%

6%1% 8%9%

6%

25%13% 27%25%

21%

26%34%

71%

European Union monetary policy

UK monetary policy

China monetary policy

U.S. monetary policy

Japan monetary policy

Australian monetary policy

Australia United States TotalUK Canada

U.S. presidential election

EU referendum in the UK (‘Brexit’)

Issues in the Eurozone

Drop in price of oil

None of these

We do not have a currency risk mitigation strategy in

place

9 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

12%11%

13%

13%15%

12%14%

13%

15%12%

20%17%

18%

19%19%

1%1%

1%

3%0%

58%71%

59%

53%45%

10%2%

6%

8%6%

48%34%

46%

48%56%

Accuracy/access to timely market data

Global economic policy uncertainty

Difficulty assessing currency exposure

Lack of currency expertise

Costs associated with hedging

Inadequate platform/automated process

Currency volatilty

What do you anticipate to be the biggest challenges to mitigating currency risk in 2017? (Please select all that apply)

Australia United States TotalUK Canada

10 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

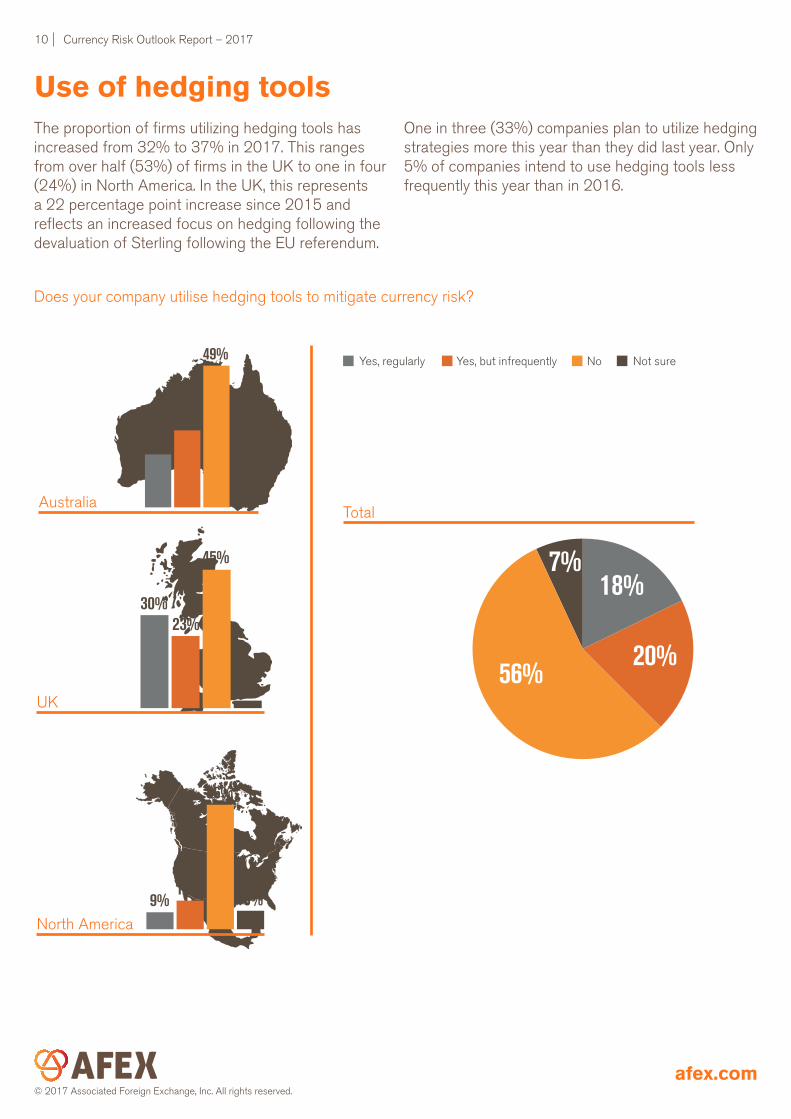

The proportion of firms utilizing hedging tools has increased from 32% to 37% in 2017. This ranges from over half (53%) of firms in the UK to one in four (24%) in North America. In the UK, this represents a 22 percentage point increase since 2015 and reflects an increased focus on hedging following the devaluation of Sterling following the EU referendum.

One in three (33%) companies plan to utilize hedging strategies more this year than they did last year. Only 5% of companies intend to use hedging tools less frequently this year than in 2016.

Does your company utilise hedging tools to mitigate currency risk?

Yes, regularly Not sureYes, but infrequently No

Use of hedging tools

49%

26%

18%

7%

45%

23%30%

3%56%

20%

18%7%

TotalAustralia

UK

66%

10%15%

9%North America

11 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

In 2017, do you expect to utilize strategies to mitigate currency risk:

3%

60%

37%

5%

66%

29%

6%

57%

37%

63%

33%

5%

TotalAustralia

UK

North America

More than in 2016

Same as 2016

Less than in 2016

12 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Increased uncertainty remains the primary driver for firms looking to extend their use of hedging strategies this year with 41% of respondents saying this (up from 32% in 2015). The biggest leap was in the US where the proportion citing increased market uncertainty went from 8% in 2015 to 37% this year. This has been largely at the expense of the pursuit of overseas business growth as a reason,

which went from 50% to 32% for US companies, perhaps suggesting a circumspect outlook on the international trading environment.

There was also a pronounced increase in the UK, from 30% in 2015 to 51%.

Why do you expect to utilize strategies to mitigate currency risk more than in 2016? (Please select main reason)

Drivers of hedging strategies

32%51%

41%

39%37%

28%2%

14%11%

18%

19%15%

21%

24%32%

21%32%

24%21%

18%

2%0%

1%0%

2%

Increased uncertainty in the markets

My company is more educated about hedging

strategies

Overseas business growth

Anticipating currency volatility in the regions we

conduct business

Increasing uncertainty regarding central banks

Australia United States TotalUK Canada

13 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

The respondent sample is fairly optimistic about their prospects for international trade. Half (50%) of respondents say they expect international trade levels to remain the same in 2017 and 37% expect it to increase. This is, however, slightly less than the 44% that were looking to grow internationally in 2015. Australian firms are particularly bullish about their international growth prospects with 52% saying they expect an increase this year. Conversely, in the UK expectations are being reined in and only 29% expect international trade levels to increase in 2017, compared to 46% in 2015.

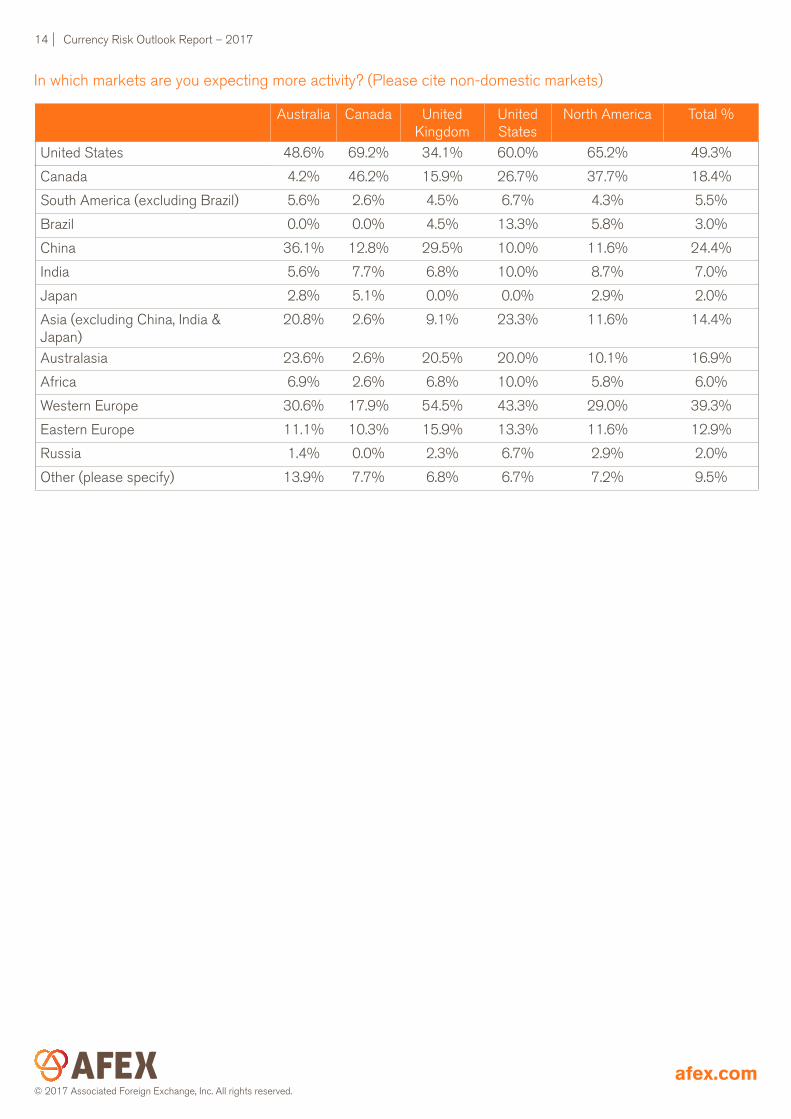

The US is identified as the market that looks set to benefit most from any growth, with 49% for firms looking to increase activity there. It is followed by Western Europe (39%) and China (24%).

The proportion of UK companies looking to increase exposure to China has doubled from 14% in 2015 to 30%. For US companies APAC is an increasing area of interest with Asia (exc. China, India & Japan) and Australasia expected to account for more activity than in 2015 (23% and 20% respectively, compared to 10% and 13% in 2015).

How do you expect your levels of international trade to change in 2017? (Please consider any exchange of raw materials, goods, services, etc.)

2016 2015

Attitudes to international trade

They will increaseThey will decrease They will stay the same

0

60

100

52%

39%

9%15%

54%

31%

17%

54%

29% 35%

57%

8% 12%

55%

33%

13%

50%

37%

Austra

lia

United

King

dom

Canad

a

North

America

United

Stat

esTo

tal

Austra

lia

United

King

dom

Canad

a

North

America

United

Stat

es0

60

100

42%

37%

21% 15%

45%

40%

12%

42%

46% 48%

41%

11% 14%

43%

43%

16%

41%

44%

Total

14 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

In which markets are you expecting more activity? (Please cite non-domestic markets)

Australia Canada United Kingdom

United States

North America Total %

United States 48.6% 69.2% 34.1% 60.0% 65.2% 49.3%

Canada 4.2% 46.2% 15.9% 26.7% 37.7% 18.4%

South America (excluding Brazil) 5.6% 2.6% 4.5% 6.7% 4.3% 5.5%

Brazil 0.0% 0.0% 4.5% 13.3% 5.8% 3.0%

China 36.1% 12.8% 29.5% 10.0% 11.6% 24.4%

India 5.6% 7.7% 6.8% 10.0% 8.7% 7.0%

Japan 2.8% 5.1% 0.0% 0.0% 2.9% 2.0%

Asia (excluding China, India & Japan)

20.8% 2.6% 9.1% 23.3% 11.6% 14.4%

Australasia 23.6% 2.6% 20.5% 20.0% 10.1% 16.9%

Africa 6.9% 2.6% 6.8% 10.0% 5.8% 6.0%

Western Europe 30.6% 17.9% 54.5% 43.3% 29.0% 39.3%

Eastern Europe 11.1% 10.3% 15.9% 13.3% 11.6% 12.9%

Russia 1.4% 0.0% 2.3% 6.7% 2.9% 2.0%

Other (please specify) 13.9% 7.7% 6.8% 6.7% 7.2% 9.5%

15 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

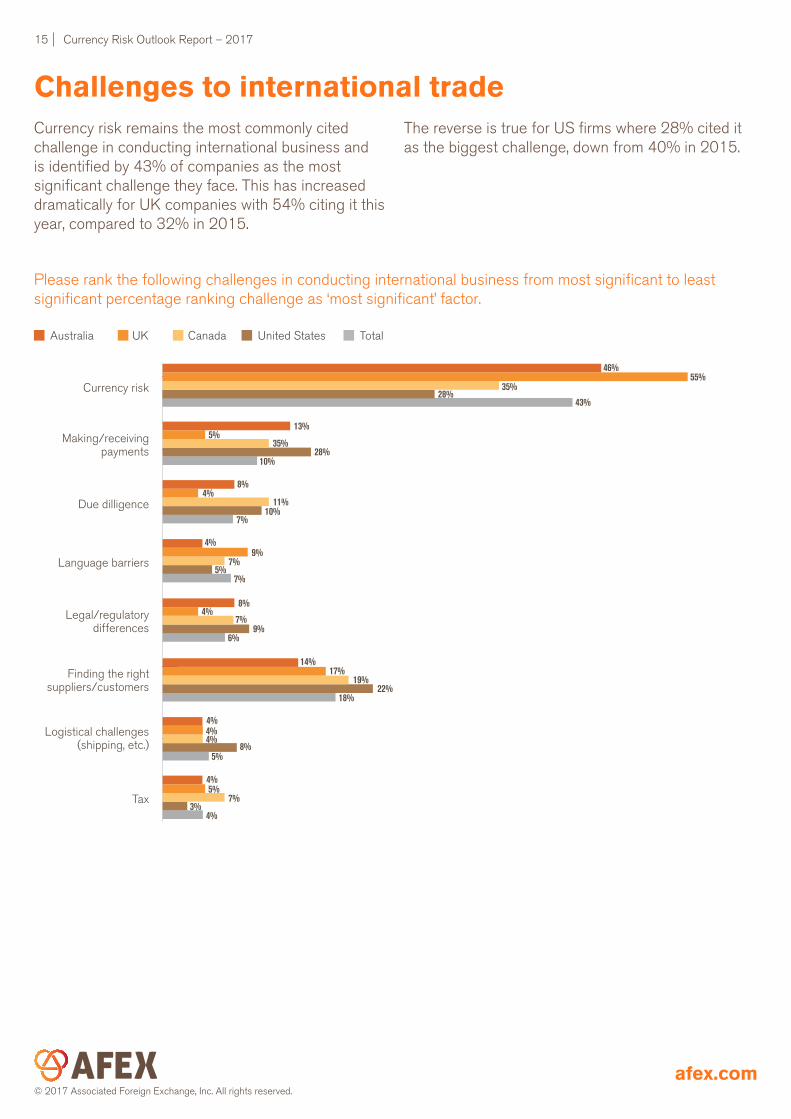

Currency risk remains the most commonly cited challenge in conducting international business and is identified by 43% of companies as the most significant challenge they face. This has increased dramatically for UK companies with 54% citing it this year, compared to 32% in 2015.

The reverse is true for US firms where 28% cited it as the biggest challenge, down from 40% in 2015.

Please rank the following challenges in conducting international business from most significant to least significant percentage ranking challenge as ‘most significant’ factor.

Challenges to international trade

46%55%

43%

35%28%

13%

10%

35%28%

5%

8%

7%

11%10%

4%

4%

7%5%

7%9%

8%

6%9%

7%4%

14%

18%22%

19%17%

4%

8%5%

4%4%

4%

4%

7%3%

5%

Currency risk

Making/receiving payments

Due dilligence

Language barriers

Tax

Logistical challenges (shipping, etc.)

Legal/regulatory differences

Finding the right suppliers/customers

Australia United States TotalUK Canada

APPENDIXFULL LIST OF RESULTS

17 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Australia United Kingdom North America Total %

Less than $2 million 52.2% 49.4% 47.6% 48.0%

$2-10 milion 35.2% 38.5% 36.9% 37.2%

$11-50 million 10.7% 9.8% 10.0% 10.6%

$51-100 million 1.3% 1.1% 2.2% 2.0%

$101-500 million 0.6% 1.1% 2.2% 1.7%

$501 million-1 billion 0.0% 0.0% 0.4% 0.2%

More than $1 billion 0.0% 0.0% 0.7% 0.5%

Full list of results

Which of the following best characterizes your company’s revenue?

In which country is your company headquartered?

Total %

Australia 24.0%

Canada 24.2%

China 0.9%

France 0.6%

Ireland 2.1%

Italy 0.5%

Jersey 0.3%

New Zealand 1.5%

Spain 0.3%

Sweden 0.0%

Switzerland 0.0%

United Kingdom 26.3%

United States 16.8%

Other 2.6%

18 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Australia United Kingdom North America Total %

Australia 49.5% 3.8% 4.3% 29.1%

Canada 1.1% 2.4% 27.3% 24.7%

China 10.0% 4.3% 4.9% 11.8%

France 3.6% 8.1% 4.0% 11.2%

Ireland 0.4% 5.4% 1.8% 6.3%

Italy 3.6% 7.3% 4.7% 10.6%

Jersey 0.0% 0.8% 0.2% 0.8%

New Zealand 7.9% 1.4% 2.2% 7.6%

Spain 1.4% 5.1% 2.8% 6.6%

Sweden 0.7% 4.1% 1.6% 3.9%

Switzerland 0.4% 2.7% 1.0% 2.5%

United Kingdom 5.4% 37.1% 6.3% 32.0%

United States 10.8% 7.9% 30.8% 35.6%

Other 5.4% 9.5% 8.1% 15.6%

Full list of results cont’d

In which country/ies does your company conduct most of its business? (Select all that apply)

United Kingdom

We will be raising the prices of our goods/services in the next 1-3 months 17.1%

We will be raising the prices of our goods/services in the next 4-6 months 6.5%

We will be raising the prices of our goods/services in the next 6-9 months 4.7%

We will be raising the prices of our goods/services in the next 9-12 months 2.4%

We have increased the prices of our goods/services 35.3%

None of these 34.1%

Do any of the following apply to you as a direct result of the devaluation of sterling following the EU referendum (“Brexit”) vote in June?

19 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Full list of results cont’d

Australia United Kingdom North America Total %

Agriculture, forestry, fishing & hunting 6% 7% 5% 5.4%

Mining, quarrying and oil & gas extraction 3% 2% 1% 1.7%

Utilities 1% 0% 0% 0.5%

Construction 5% 6% 2% 3.9%

Manufacturing 13% 16% 17% 16.5%

Wholesale Trade 28% 22% 21% 22.7%

Retail Trade 17% 8% 8% 10.9%

Transportation and warehousing 5% 5% 4% 4.4%

Information 3% 1% 1% 1.7%

Finance & insurance 1% 2% 0% 1.1%

Real estate and rental & leasing 2% 1% 3% 2.2%

Professional, scientific and technical services

1% 3% 5% 3.5%

Management of companies & enterprises 0% 0% 1% 0.5%

Administrative and support and waste management and remediation services

0% 0% 0% 0.0%

Educational services 1% 1% 2% 0.9%

Healthcare and social assistance 3% 1% 2% 1.7%

Arts, entertainment and recreation 1% 0% 4% 2.0%

Accommodation and food services 0% 2% 1% 1.3%

Other services (exc. public administration) 0% 0% 2% 0.6%

Public administration 0% 1% 0% 0.5%

Other (please specify) 10% 23% 20% 18.0%

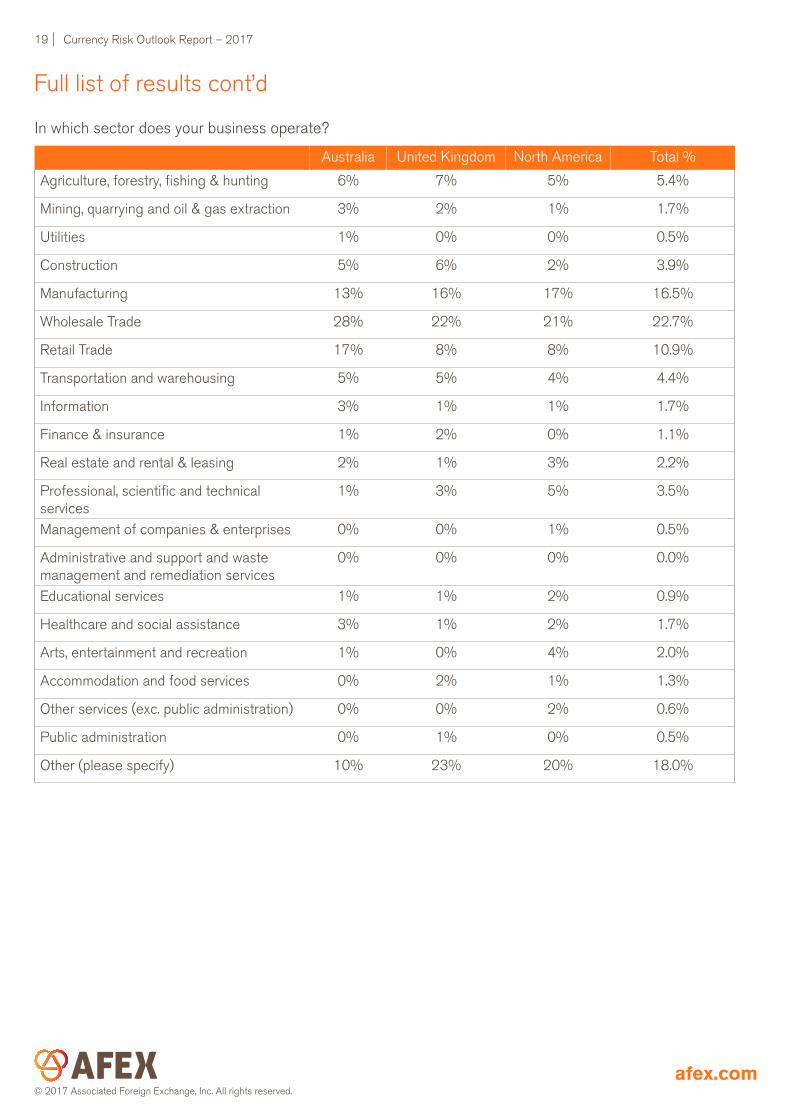

In which sector does your business operate?

20 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

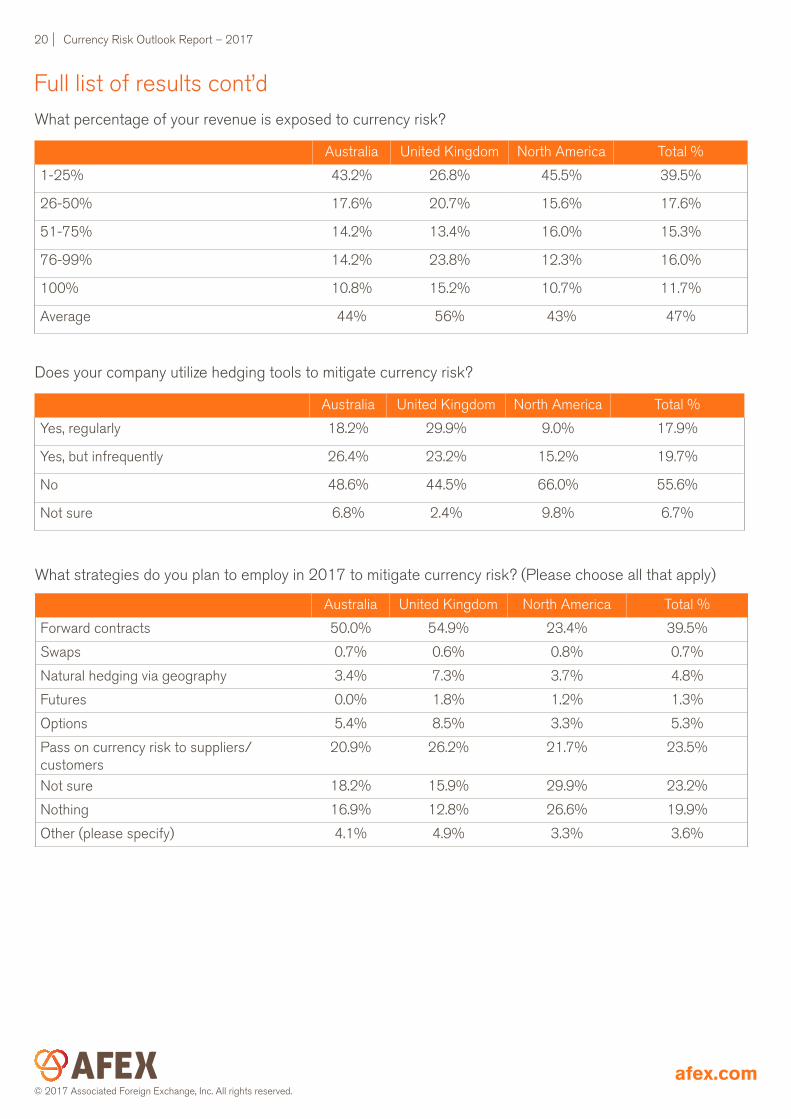

Australia United Kingdom North America Total %

1-25% 43.2% 26.8% 45.5% 39.5%

26-50% 17.6% 20.7% 15.6% 17.6%

51-75% 14.2% 13.4% 16.0% 15.3%

76-99% 14.2% 23.8% 12.3% 16.0%

100% 10.8% 15.2% 10.7% 11.7%

Average 44% 56% 43% 47%

Australia United Kingdom North America Total %

Yes, regularly 18.2% 29.9% 9.0% 17.9%

Yes, but infrequently 26.4% 23.2% 15.2% 19.7%

No 48.6% 44.5% 66.0% 55.6%

Not sure 6.8% 2.4% 9.8% 6.7%

What percentage of your revenue is exposed to currency risk?

Does your company utilize hedging tools to mitigate currency risk?

What strategies do you plan to employ in 2017 to mitigate currency risk? (Please choose all that apply)

Australia United Kingdom North America Total %

Forward contracts 50.0% 54.9% 23.4% 39.5%

Swaps 0.7% 0.6% 0.8% 0.7%

Natural hedging via geography 3.4% 7.3% 3.7% 4.8%

Futures 0.0% 1.8% 1.2% 1.3%

Options 5.4% 8.5% 3.3% 5.3%

Pass on currency risk to suppliers/customers

20.9% 26.2% 21.7% 23.5%

Not sure 18.2% 15.9% 29.9% 23.2%

Nothing 16.9% 12.8% 26.6% 19.9%

Other (please specify) 4.1% 4.9% 3.3% 3.6%

Full list of results cont’d

21 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Full list of results cont’d

Australia United Kingdom North America Total %

More than in 2016 37.0% 37.2% 28.8% 32.7%

Same as in 2016 60.3% 57.3% 65.8% 62.7%

Less than in 2016 2.7% 5.5% 5.4% 4.7%

Australia United Kingdom North America Total %

Increased uncertainty in the markets 31.5% 50.8% 38.5% 40.5%

My company is more educated about hedging strategies

27.8% 1.7% 15.4% 13.7%

Overseas business growth 18.5% 15.3% 26.2% 21.1%

Anticipating currency volatility in the regions we conduct business

20.4% 32.2% 18.5% 23.7%

Increasing uncertainty regarding central banks

1.9% 0.0% 1.5% 1.1%

Australia United Kingdom North America Total %

Accuracy/access to timely market data 12.2% 10.8% 13.6% 12.5%

Global economic policy uncertainty 47.5% 33.8% 51.1% 45.7%

Difficulty assessing currency exposure 12.2% 14.0% 14.0% 13.0%

Lack of currency expertise 20.1% 17.2% 19.0% 18.4%

Costs associated with hedging 10.1% 1.9% 6.8% 6.3%

Inadequate platform/automated process 1.4% 1.3% 1.8% 1.4%

Currency volatilty 57.6% 71.3% 49.8% 58.9%

In 2017, do you expect to utilize strategies to mitigate currency risk:

Why do you expect to utilize strategies to mitigate currency risk more than in 2016? (Please select main reason)

Why do you expect to utilize strategies to mitigate currency risk more than in 2016? (Please select main reason)

22 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Full list of results cont’d

Australia United Kingdom North America Total %

European Union monetary policy 12.9% 17.8% 16.3% 15.4%

UK monetary policy 6.5% 22.3% 8.1% 12.3%

China monetary policy 10.1% 2.5% 2.3% 5.0%

U.S. monetary policy 39.6% 12.1% 36.2% 29.6%

Japan monetary policy 0.7% 0.6% 0.5% 0.5%

Australian monetary policy 29.5% 1.3% 1.8% 8.4%

U.S. presidential election 33.1% 14.6% 28.1% 25.2%

EU referendum in the UK ('Brexit') 19.4% 71.3% 16.3% 34.1%

Issues in the Eurozone 11.5% 14.0% 10.0% 12.1%

Drop in price of oil 5.0% 5.7% 19.9% 11.3%

None of these 5.8% 0.6% 8.6% 5.7%

We do not have a currency risk mitigation strategy in place

24.5% 12.7% 25.8% 21.3%

Australia United Kingdom North America Total %

Open an office 0.7% 0.0% 0.5% 0.4%

Close an office 0.7% 0.6% 0.0% 0.7%

Reduce the size of your business 6.5% 8.9% 3.6% 5.9%

Increase the size of your business 4.3% 3.8% 3.6% 3.6%

Enter a geographic market 2.2% 1.3% 1.8% 2.0%

Exit a geographic market 0.0% 1.3% 0.9% 1.1%

Hire more people 2.9% 2.5% 2.3% 2.5%

Reduce number of employees 5.8% 6.4% 3.2% 4.6%

Impose pay restrictions 0.7% 6.4% 1.8% 2.7%

Off shore growth 1.4% 1.3% 0.9% 1.3%

Postpone or cancel growth plans 8.6% 12.7% 5.9% 8.4%

Accelerate growth plans 5.0% 9.6% 4.5% 6.3%

None of these 74.8% 66.2% 78.7% 74.1%

Which global events have most affected your company’s currency risk mitigation strategy in the last 12 months? (Please choose all that apply)

Did currency volatility cause you to do any of the following in 2016? (Choose all that apply)

23 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Australia Canada United Kingdom

United States North America

Total %

Less than 2016 4% 5% 15% 13% 8% 9.3%

Same as 2016 34% 37% 34% 34% 36% 34.6%

More than 2016 62% 58% 52% 53% 56% 56.0%

Australia Canada United Kingdom

United States

North America Total %

They will decrease 8.7% 15.3% 16.6% 8.0% 12.3% 12.6%

They will stay the same 39.1% 54.2% 54.1% 56.8% 55.3% 50.4%

They will increase 52.2% 30.5% 29.3% 35.2% 32.4% 37.0%

Australia United Kingdom North America Total %

United States 48.6% 34.1% 65.2% 49.3%

Canada 4.2% 15.9% 37.7% 18.4%

South America (excluding Brazil) 5.6% 4.5% 4.3% 5.5%

Brazil 0.0% 4.5% 5.8% 3.0%

China 36.1% 29.5% 11.6% 24.4%

India 5.6% 6.8% 8.7% 7.0%

Japan 2.8% 0.0% 2.9% 2.0%

Asia (Excluding China, India & Japan) 20.8% 9.1% 11.6% 14.4%

Australasia 23.6% 20.5% 10.1% 16.9%

Africa 6.9% 6.8% 5.8% 6.0%

Western Europe 30.6% 54.5% 29.0% 39.3%

Eastern Europe 11.1% 15.9% 11.6% 12.9%

Russia 1.4% 2.3% 2.9% 2.0%

Other (please specify) 13.9% 6.8% 7.2% 9.5%

In regards to market conditions in 2017, do you expect currency volatility to be?

How do you expect your levels of international trade to change in 2017? (Please consider any exchange of raw materials, goods, services, etc.)

In which markets are you expecting more activity? (Please cite non-domestic markets)

Full list of results cont’d

24 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Australia Canada United Kingdom

United States

Total %

Currency risk 45.45% 34.86% 54.41% 28.21% 42.50%

Making/receiving payments 13.22% 11.01% 4.41% 15.38% 9.79%

Due dilligence 7.44% 11.01% 3.68% 10.26% 7.29%

Language barriers 4.13% 6.42% 8.82% 5.13% 7.08%

Legal/regulatory differences 7.44% 7.34% 3.68% 8.97% 6.46%

Finding the right suppliers/customers 14.05% 19.27% 16.91% 21.79% 17.92%

Logistical challenges (shipping, etc.) 4.13% 3.67% 3.68% 7.69% 4.79%

Tax 4.13% 6.42% 4.41% 2.56% 4.17%

Please rank the following challenges in conducting international business from most significant to least significant.

Full list of results cont’d

25 Currency Risk Outlook Report – 2017

afex.com© 2017 Associated Foreign Exchange, Inc. All rights reserved.

Currency Risk Outlook Report - 2017

About AFEX

AFEX polled clients based in the United States, Canada, the United Kingdom and Australia, and across a wide range of industries, to determine their perspectives on currency risk and what strategies they employ to mitigate that risk. The survey was conducted from January 17th, through February 2nd 2017, with 662 respondents in total.

© 2017 Associated Foreign Exchange, Inc. All rights reserved. “AFEX” is the marketing trading name for the International Payment Solutions and Risk Management Solutions provided by several subsidiaries of Associated Foreign Exchange Holdings, Inc. Services in Australia are provided by Associated Foreign Exchange Australia Pty Ltd; in Canada by Associated Foreign Exchange, ULC; in Switzerland by Associated Foreign Exchange (Schweiz) AG; in Indonesia by PT. AFEX Indonesia; in the UK and the European Economic Area (EEA) on a cross-border basis by Associated Foreign Exchange Ltd; in the Channel Islands by AFEX Offshore Ltd; and in the U.S. by Associated Foreign Exchange, Inc. (collectively referred to as “AFEX” or “Associated Foreign Exchange”). For more information, visit www.afex.com. The AFEX name, logo and related trademarks and service marks, owned by Associated Foreign Exchange, Inc., are registered and/or used in the United States and many foreign countries. All other trademarks, service marks, and trade names referenced in this brochure are the property of their respective owners. Associated Foreign Exchange Australia Pty Limited ABN 119 392 586 and AFSL 305246, authorised and regulated by the Australian Securities and Investments Commission, Citigroup Centre, 2 Park Street, Suite D 38th Floor, Sydney NSW 2000. Registered Office: Grant Thornton Australia, Level 17 383 Kent Street, Sydney NSW 2000. Associated Foreign Exchange, ULC, 200 Front Street, Suite 2203, Toronto, ON M5V 3K2, registered as a Money Services Business with the Financial Transactions and Reports Analysis Centre of Canada and with the Autorité des marchés financiers (“AMF”). PT. AFEX Indonesia is a private limited company incorporated in Indonesia with its head office located at 45th floor, Menara BCA, Grand Indonesia, Jl. MH Thamrin No. 1, Jakarta Pusat 10310. PT AFEX Indonesia is licensed by the Bank of Indonesia as a Fund Transfer Operator (License Number: 17/158/DKSP/61). Associated Foreign Exchange (Schweiz) AG, Reg. No. CHE-114.547.009, with a registered place of business at Stampfenbachstrasse 5, 8001 Zurich. Associated Foreign Exchange Ltd (registered in England and Wales, Company Number 4848033, Registered Office Address: 4th Floor, 40 Strand, London WC2N 5RW), authorised by the Financial Conduct Authority under the Payment Services Regulations 2009 (Register Reference: 502593) for the provision of payment services and is registered as an MSB with HM Revenue & Customs (Registered No: 12159000). Associated Foreign Exchange Ltd, Italian Branch. Registered office: Piazza Pio XI 1, 20123 Milan, Italy. Tax code and VAT number: 08042310964. Registration number at the Chamber of Commerce of Milan: 08042310964. Authorised by the Bank of Italy to provide payment services in Italy and registered to the list of payment institutions established number 36043.8. Associated Foreign Exchange Ltd, Branch in Spain. Spanish registered office: Paseo de la Castellana nº 18, PL. 7º, 28046 Madrid, Spain (Bank of Spain code number: 6873). Tax code and VAT number: W8265977B. Authorised by the Bank of Spain to provide payment services in Spain as a branch of Associated Foreign Exchange Ltd. AFEX Offshore Limited is authorised and regulated by the Jersey Financial Services Commission for Investment Business and Money Service Business under the Financial Services (Jersey) Law 1998. Registered in Jersey (registered no. 117732). Associated Foreign Exchange, Inc., 21045 Califa Street, Woodland Hills, CA 91367, licensed and regulated by multiple State departments including the California Department of Business Oversight, New York State Department of Financial Services, Illinois Division of Financial Institutions, and Texas Department of Banking. For a complete listing of U.S. State licensing, visit https://www.afex.com/unitedstates. This report in whole or in part may not be duplicated, reproduced, stored in a retrieval system or retransmitted without prior written permission of AFEX. AFEX has based the opinions expressed herein on information generally available to the public. AFEX makes no warranty concerning the accuracy of this information and specifically disclaims any liability whatsoever for any loss arising from trading decisions based on the opinions expressed and information contained herein. Such information and opinions are for general information only and are not intended to present advice with respect to matters reviewed and commented upon. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject AFEX or its affiliates to any registration or licensing requirement within such jurisdiction. All material presented herein, unless specifically indicated otherwise, is under copyright to AFEX.

Established in 1979, AFEX is a leading global payment and risk management solutions provider that specializes in cross-border transactions and provides market expertise and unrivalled customer service for businesses and private clients. With a client base of over 35,000 active commercial customers worldwide, AFEX prides itself on tailoring its payment and foreign exchange services to meet its clients’ needs. AFEX’s online payment platform - AFEXDirect provides clients with one consolidated overview of their currency exposure and makes it easy for companies to manage international invoices. AFEX maintains offices across the Americas, EMEA and Asia Pacific. To find out more, please visit www.afex.com

afex.com