csu operating fund reserves vs budget balance available

Post on 21-Dec-2015

220 views

TRANSCRIPT

CSU Operating FundReserves vs Budget Balance Available

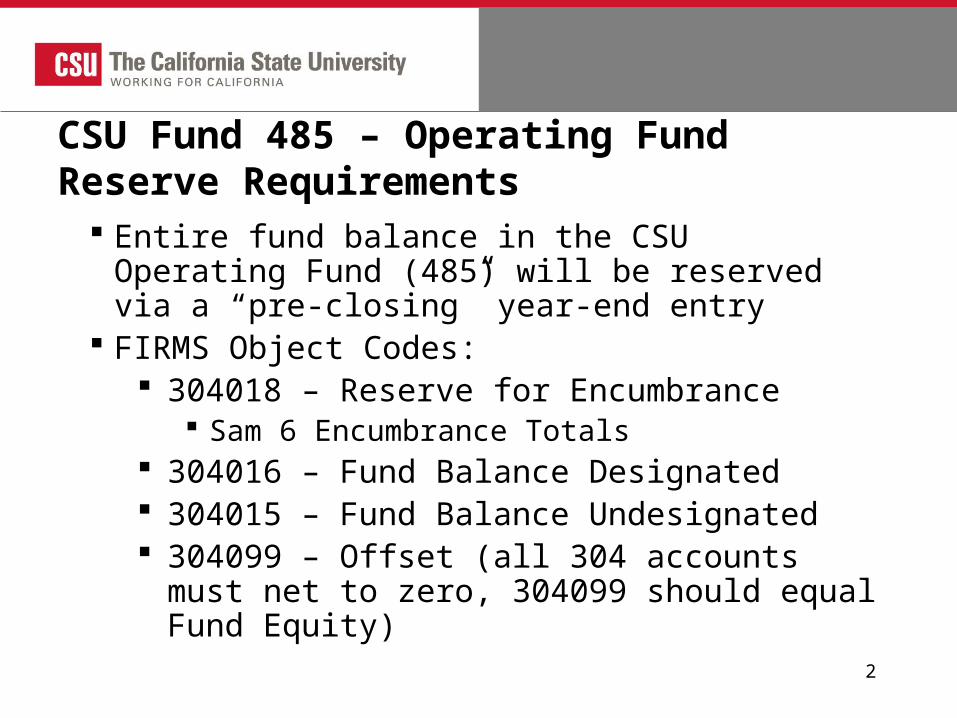

CSU Fund 485 – Operating Fund Reserve Requirements

Entire fund balance in the CSU Operating Fund (485) will be reserved via a “pre-closing” year-end entry

FIRMS Object Codes: 304018 – Reserve for Encumbrance

Sam 6 Encumbrance Totals 304016 – Fund Balance Designated 304015 – Fund Balance Undesignated 304099 – Offset (all 304 accounts must net to

zero, 304099 should equal Fund Equity)

2

Campus Unique Accounts

Campuses can establish multiple reserve/designation accounts for management purposes

Example: Mapped to 304016 - Designated

304800 – Designated for Divisions 304801 – Designated for University

Mapped to 304015 - Undesignated 304802 – Unallocated Campus Designation

3

Transition Year - New Activities Within CSU Fund 485 – CSU Operating Fund User Fees Activity previously accounted for in CSU Fund 467

– Student Fees Miscellaneous Course Fees Health Services Augmented Health Services Investment Activity related to CSU Fund 485

4

CSU Fund 485 FNAT Keys

5

FNAT Key

CSU

Fund

Code

FIRMS

Project Avail To

Required/O

ptional Use

126464 485 00000 All Required General CSU Fund 485 127942 485 INTAC All Required Interest Earnings on CSU Fund 485 127340 485 HSFEE All Optional Health Services Operations 127341 485 MISCF All Optional Miscellaneous Fees128101 485 USERF All Optional User Fees 126555 485 REIMB All Optional Reimbursed Activities

Using CSU Fund 485 FNAT keys

Separate FNAT Keys REQUIRE separate PeopleSoft Funds

SAM 6 will subtotal based on the FNAT Keys SAM 6 will show the summarized net income by FNAT

key Can be used to determine reserve entry

6

Sample SAM 6

7

FIRM Project Value display in the Section Header

SAM 6 Sub-totals based on the FIRMS Project Value (net income

that will close to reserve)

Adobe Acrobat 7.0 Document

Query to support SAM6

8

Fields

9

Criteria – Note the Groupings

10

Having Criteria

11

Output to Excel….

12

How much money is left?

Budget reconciles to accounting data Both Budget and Accounting should agree on the carry

forward balance Campus needs to develop its process for managing carry

forward balances

13

Budget and Accounting Agree

14

Reserve vs Budget Balance AvailableCampus

Operating Fund Investments User Fees Reimb ActSL001 SL900 MRXXX SL002

June 30, 2007 Equity A (21,532,201.32)$ -$ -$ -$ Portion of equity not allocated B 818,306.91$ -$ -$ -$

Etimated Revenue/Transfers in (89,425,348.42)$ (2,723,811.07)$ (602,227.92)$ (5,891,758.44)$ Expenditures 80,403,204.00$ 2,695,338.92$ 290,000.00$ 5,891,758.44$ Estimated Net Income C (9,022,144.42)$ (28,472.15)$ (312,227.92)$ -$

Estimated Equity @ June 30, 2008 (Total Reserves) A + C (30,554,345.74)$ (28,472.15)$ (312,227.92)$ -$

Budget Balance Available - (SAM 6) D 24,658,956.00$ 28,472.15$ 296,589.92$ -$

Difference Between BBA & Equity A + C + D (5,895,389.74)$ (0.00)$ (15,638.00)$ -$

Difference is made up of: Unallocated Equity B 818,306.91$ -$ -$ -$ Encumbrances @ June 30, 2008 (SAM 6) E 5,077,082.83$ -$ 15,638.00$ Sub-total 5,895,389.74$ -$ 15,638.00$ -$

Unallocated reserves from Prior Year B 818,306.91$ -$ -$ -$ Budget Balance from Current Year D 24,658,956.00$ 28,472.15$ 296,589.92$ -$ add back Encumbrances E 5,077,082.83$ -$ 15,638.00$ -$ Total Funds to be reserved 30,554,345.74$ 28,472.15$ 312,227.92$ -$

Budget and Accounting agree

Now you agree on the total…

Reserve entries are based on management’s plans for spending

Carry Forward to Divisions/Departments Carry Forward for Centrally maintained budgets Carry Forward for Encumbrances Unallocated Funds Etc

Budget Balance Available is used to determine the “owner” and/or classification of reserves

15

Revenue

Revenue Balances are usually centrally maintained by the campus

“Unscheduled” balances at year end will be part of the total equity amount that needs to be reserved

For ease of identification, all revenues could be fully allocated so that the budget balance available for all revenues is zero

By default, all funds will be identified based on the BBA within the expenditure budget

16

17

Cal Poly Sam 6 @ June 30, 2007 – all revenues

are fully scheduled

18

Adobe Acrobat 7.0 Document

Sample June 30, Sam 6 (P&L) and Trial Balance

Managing Reserve Balances thru the year

19

Reserve Balances by Accouting Period

Account Description 2007-0 2007-6 2007-11 Total304018 Reserve for Encumbrances (3,160,689) 0 0 (3,160,689)304099 Fund Bal Reserves Offset 21,532,201 2,303,826 0 23,836,028304800 Reserve-Division Oblig (016) (12,779,668) 0 0 (12,779,668)304801 Res-Campus Oblig (016) (3,950,759) (3,126,605) 0 (7,077,364)304802 Unallocated Camp Reserves (015 (1,641,086) 822,779 0 (818,307)305002 Fund Balance-Continuing Approp (21,532,201) 0 0 (21,532,201)

Fund Balance (21,532,201) 0 0 (21,200,189)

Sample entries PRIOR to June 30, 2008, Reserve entries

20

Reserve Balances by Accouting Period

Account Description 2007-0 2007-6 2007-12 Total304018 Reserve for Encumbrances (3,160,689) 0 3,160,689 0304099 Fund Bal Reserves Offset 21,532,201 2,303,826 (23,836,028) 0304800 Reserve-Division Oblig (016) (12,779,668) 0 12,779,668 0304801 Res-Campus Oblig (016) (3,950,759) (3,126,605) 7,077,364 0304802 Unallocated Camp Reserves (015 (1,641,086) 822,779 818,307 0305002 Fund Balance-Continuing Approp (21,532,201) 0 21,532,201 0

Fund Balance (21,532,201) 0 21,532,202 0

Budget and Accounting Agree

21

Reserve vs Budget Balance AvailableCampus

Operating Fund Investments User Fees Reimb ActSL001 SL900 MRXXX SL002

June 30, 2007 Equity A (21,532,201)$ -$ -$ -$ Portion of equity not allocated B 818,307$ -$ -$ -$

Etimated Revenue/Transfers in (89,425,348)$ (2,723,811)$ (602,228)$ (5,891,758)$ Expenditures/Tranfers Out 80,403,204$ 2,695,339$ 290,000$ 5,891,758$ Estimated Net Income C (9,022,144)$ (28,472)$ (312,228)$ -$

Estimated Equity @ June 30, 2008 (Total Reserves) A + C (30,554,346)$ (28,472)$ (312,228)$ -$

Budget Balance Available - (SAM 6) D 25,076,253$ 28,472$ 296,590$ -$

Difference Between BBA & Equity A + C + D (5,478,093)$ (0)$ (15,638)$ -$

Difference is made up of: Unallocated Equity B 1,235,604$ -$ -$ -$ Encumbrances @ June 30, 2008 (SAM 6) E 4,659,786$ -$ 15,638$ Sub-total 5,895,390$ -$ 15,638$ -$

Unallocated reserves from Prior Year B 818,307$ -$ -$ -$ Budget Balance from Current Year D 25,076,253$ 28,472$ 296,590$ -$ add back Encumbrances E 4,659,786$ -$ 15,638$ -$ Total Funds to be reserved 30,554,346$ 28,472$ 312,228$ -$

Budget and Accounting agree

Sample Final Reserve Balances

22

Account Description 2007-0 2007-6 20070-12 Total304018 Reserve for Encumbrances (3,160,689) - (1,499,097) (4,659,786) 304099 Fund Bal Reserves Offset 21,532,201 2,303,826 6,718,319 30,554,346 304800 Reserve - Division Oblig (12,779,668) - (3,769,704) (16,549,372) 304801 Res- Campus Oblig (3,950,759) (3,126,605) (1,032,220) (8,109,584) 304802 Unallocated Campus Reserves (1,641,086) 822,779 (417,297) (1,235,604) 305002 Fund Balance - Continuing Approp (21,532,201) - (9,022,148) (30,554,349)

Reserve in the non-operating funds

Could reserve all equity in 304016 Designated Balances If this is your choice, you could create an allocation to

do the reserve entry in these funds

23

www.calstate.edu