crs: are you ready? - pwc: audit and assurance ... are you ready? 24 november 2016 phil morris paul...

TRANSCRIPT

CRS: Are you ready?

24 November 2016

Phil MorrisPaul Beeson

www.pwc.com/im

Common Reporting Standard (“CRS”)Overview

• Model Agreement and Commentary published

• Global forum meeting in Berlin 29 October 2014.

• Around 100 jurisdictions committed to adopting CRS.

• Over 50 jurisdictions acting as “early adopters” of CRS.

• Local regulations in place.

•Domestic legislation implemented

What does this mean for you?

Financial institutions resident in CRS countries should report account holder information to their local tax authorities who will then exchange such information with countries where account holders are tax residents

What is CRS? Where are we? What is next?

• A number of countries may still join CRS.

• Ongoing due diligence requirements to meet.

• First reporting by 30 June 2017.

• Global standard for automatic exchange of financial account information between Governments.

PwC 2

As a consequence of the multilateral reporting requirement the CRS has an increased complexity compared to FATCA

FA

TC

A

CR

S

FATCA only bilaterally takes into account the interests of the USA, the CRS in contrary, has the multilateral interests of more than 50 jurisdictions; besides, specific and potentially deviating local requirements of the participating jurisdictions may raise further complexity.

PwC 3

Common Reporting Standard (“CRS”)Interaction with FATCA

Financial institution Account holders

Documentation

Local tax authority

Non participating

FFI

‘Payments’ not including consideration for the provision of goods or non-financial services

Reporting

on reportable accounts

FFI Reporting and Certifications

on reportable accounts IRS

• Obtain information on account holders

• Comply with required due diligence and verification procedures

• Obtain applicable waiver of disclosure limitations

Model 1 IGA reporting

on US reportable accounts and payments to NPFFIs

As with the Foreign Account Tax Compliance Act (FATCA), the CRS model imposes obligations on financial institutions (FIs) to: (1) identify reportable accounts (2) obtain the account holder identifying information and (3) report certain accounts to their local tax administration.

CRS reporting on reportable accounts

Number of reporting depends on location of Reporting FI

4

Automatic Exchange of Information

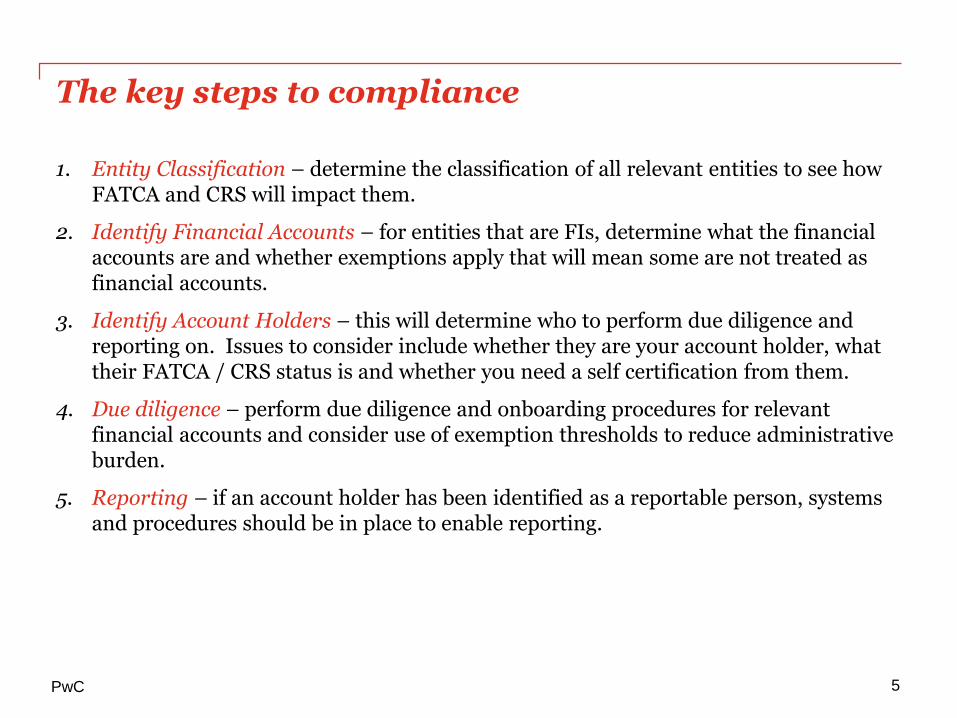

The key steps to compliance

1. Entity Classification – determine the classification of all relevant entities to see how FATCA and CRS will impact them.

2. Identify Financial Accounts – for entities that are FIs, determine what the financial accounts are and whether exemptions apply that will mean some are not treated as financial accounts.

3. Identify Account Holders – this will determine who to perform due diligence and reporting on. Issues to consider include whether they are your account holder, what their FATCA / CRS status is and whether you need a self certification from them.

4. Due diligence – perform due diligence and onboarding procedures for relevant financial accounts and consider use of exemption thresholds to reduce administrative burden.

5. Reporting – if an account holder has been identified as a reportable person, systems and procedures should be in place to enable reporting.

PwC 5

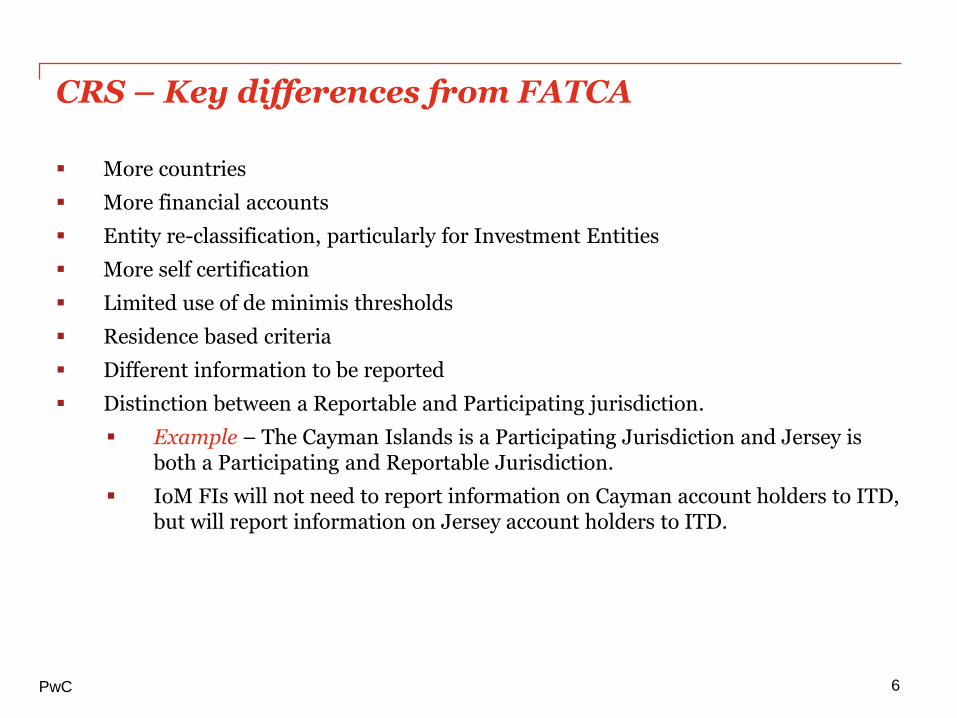

CRS – Key differences from FATCA

More countries

More financial accounts

Entity re-classification, particularly for Investment Entities

More self certification

Limited use of de minimis thresholds

Residence based criteria

Different information to be reported

Distinction between a Reportable and Participating jurisdiction.

Example – The Cayman Islands is a Participating Jurisdiction and Jersey is both a Participating and Reportable Jurisdiction.

IoM FIs will not need to report information on Cayman account holders to ITD, but will report information on Jersey account holders to ITD.

PwC 6

What should you be doing now?

Identifying participating entities within the group – identify the financial institutions, what their obligations are and where these obligations exist.

Project approach – Securing project resources and determining global governance and structure. Local laws require local expertise.

Effective gap analysis between CRS and FATCA and lessons learnt from FATCA implementation. How do the differences impact and how are they dealt with?

Information technology and systems changes - are existing IT systems up to speed or are additional resources needed?

Amending documentation – Do procedures/legal/regulatory documents need to be amended and how long will this take?

Compliance assurance - implementation, testing and on-going monitoring.

The customer experience – ensuring that the client relationship is suitably handled.

Training and communications - internal and external. Consider challenges associated with understanding of terminology, requirements and implementation impact.

7PwC

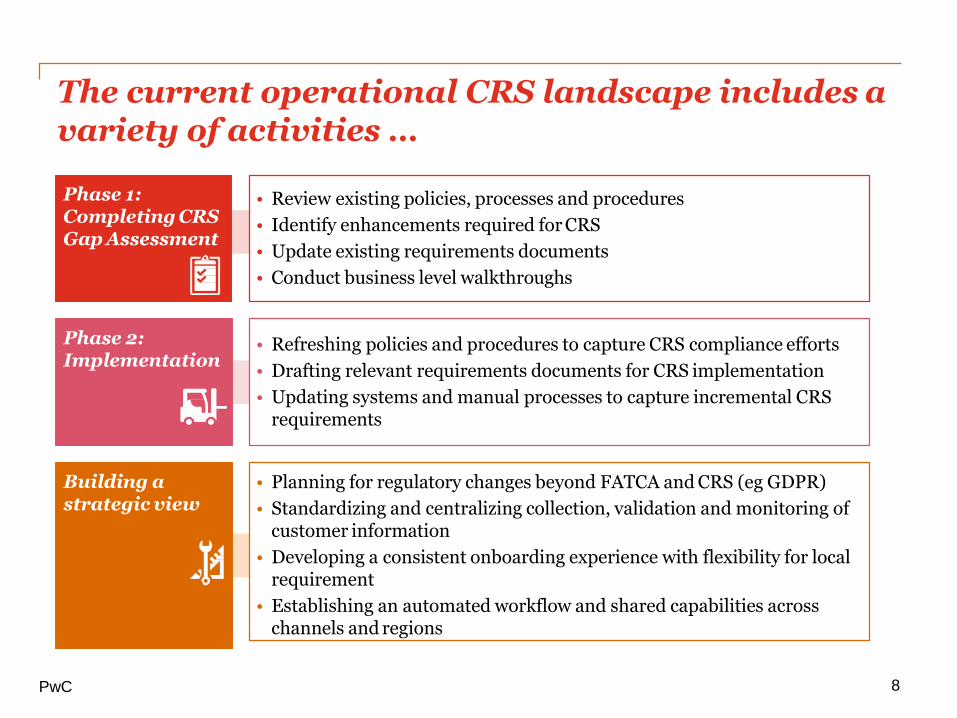

The current operational CRS landscape includes a variety of activities …

Phase 1: Completing CRS Gap Assessment

• Review existing policies, processes and procedures

• Identify enhancements required for CRS

• Update existing requirements documents

• Conduct business level walkthroughs

Phase 2: Implementation

• Refreshing policies and procedures to capture CRS compliance efforts

• Drafting relevant requirements documents for CRS implementation

• Updating systems and manual processes to capture incremental CRS requirements

Building a strategic view

• Planning for regulatory changes beyond FATCA and CRS (eg GDPR)

• Standardizing and centralizing collection, validation and monitoring ofcustomer information

• Developing a consistent onboarding experience with flexibility for local requirement

• Establishing an automated workflow and shared capabilities across channels and regions

8PwC

What are we seeing?

We are helping FIs and their customers understand their obligations. We can:

undertake business impact assessments

review strategic and operational models

provide AML/KYC solutions and remediation

provide information reporting capability

drive associated culture and conduct changes

support customer conversations and handle personal tax disclosures

provide post implementation reviews and ongoing assurance

providing training to relevant staff

9PwC

PwC Tax Information Reporting Ltd

Automatic Exchange of Information (AEoI) Reporting

www.pwc.co.uk

Multi functional integrated reporting software

PwC TaxInformation

Reporting

http://www.pwc.co.uk/services/tax/insights/information-reporting.html

PwC AEoI Reporting 11

PwC TaxInformation

Reporting

Integrated Solution

• Covers CRS, FATCA & UK CDOT • PwC global support for schema filing• Global country coverage• Direct mapping to your core data• Easily handles large volumes• Full audit trail• Coverage for trusts

Excel solution

• Covers CRS, FATCA & UK CDOT • No system integration• Excel to XML to filing• Ideal for lower volumes• Typical pre CRS solution• Global country coverage

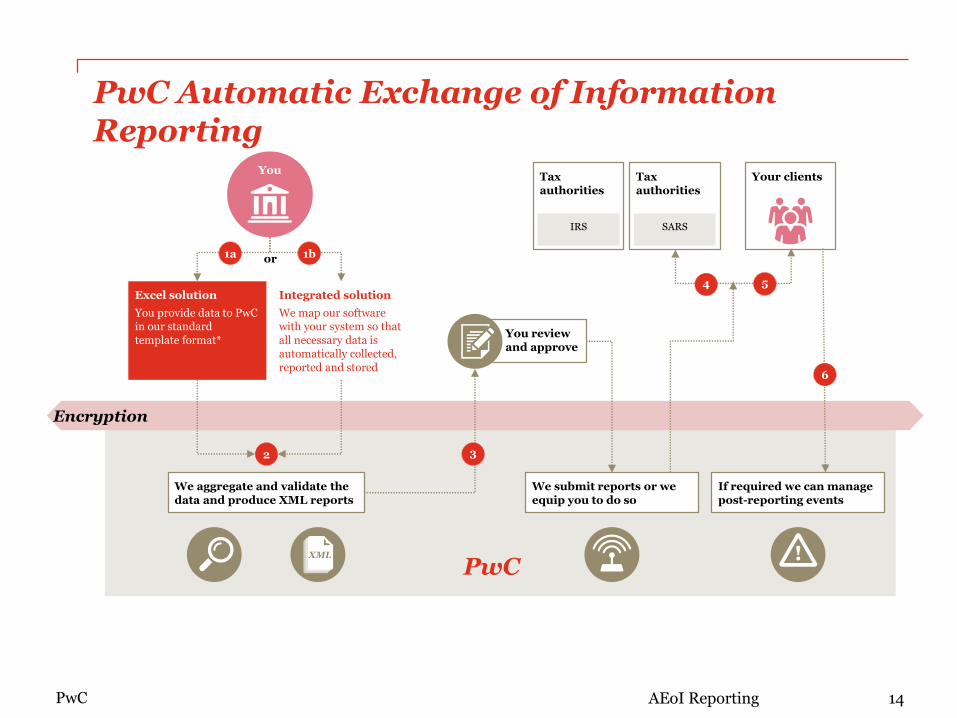

PwC Automatic Exchange of Information Reporting

Core system features• Penetrated tested by third parties and clients• In-built encryption• Disaster recovery facilities• Data quality issues highlighted• Monitoring of legislation changes

For further information please watch the video at http://www.pwc.co.uk/services/tax/insights/information-reporting.html

PwC 13AEoI Reporting

You review and approve

PwC Automatic Exchange of Information Reporting

Excel solution

You provide data to PwC in our standard template format*

Integrated solution

We map our software with your system so that all necessary data is automatically collected, reported and stored

Tax authorities

Tax authorities

Your clients

We submit reports or we equip you to do so

If required we can manage post-reporting events

We aggregate and validate the data and produce XML reports

Encryption

2

IRS SARS

1a 1bor

PwC

54

6

3

You

XML

AEoI ReportingPwC 14

Data Population

Simple 4 tab spreadsheet to complete

1 2 3 4

Financial Institution Details

Accounts & Beneficial Owners

Transactions (Optional)

Submission Summary (Optional)

• Type of Report (FATCA/CRS/CDOT)

• Jurisdiction (Sending/Receiving)• Report year• Identification Number• Contact Details

• Name• Address• GIIN• Identification Number• Due Diligence• Apply Threshold• Contact Details

• FIID• Acc No. & Type• Account Status• CCY• FX Rate Used• Acc Balances• Interest, Dividend & Other Income• Proceeds (Optional - Year 2017)

• Person Ref• Person Type• Status• Country Code• Tax ID No.• TIN Type

• FI ID• Account Number• Transaction ID • Date• Transaction Type• Amount

PwC 15AEoI Reporting

• Type of Report (FATCA/CRS/CDOT)

• Jurisdiction (Sending/Receiving)• Report year• Identification Number• Contact Details

• Name• Address• GIIN• Identification Number• Due Diligence• Apply Threshold• Contact Details

• Person Ref• Person Type• Status• Country Code• Tax ID No.• TIN Type

• FI ID• Account Number• Transaction ID • Date• Transaction Type• Amount

PwC

Reports

Several reports available to ensure you are confident that the data we are filing is accurate and correct. The reports currently available are:

• Data Issue Reports - (Mandatory data issues, Warnings)

• Client Indicia Report

• Multiple Client Report

• Reportable Accounts

• Non-Reportable Accounts (including reason why)

The reports can be produced in PDF or Excel/CSV

16AEoI Reporting

Data Issue Reports

WARNING

Does not just list missing optional fields.

Performs integrity checks.

Provides Intelligent checking.

It will come up with errors like this TIN has been used on a different client, are you sure this is correct.

There are two reports we provide to highlight data issues.

WARNING - Errors or possible errors which will not stop a filing.

MANDATORY – Data issues which would prevent filing.

Reports highlights which row in the spreadsheet is in error.

MANDATORY

The types of missing mandatory data items that are reported are likely to be one of the following:

• TIN (Dependent on jurisdiction & report)

• TIN country code

• Name or title, first name, last name

• Address

• Country code

• Postcode

• County

• Nationality

• Tax resident country

PwC 16AEoI Reporting

Client Indicia Report

Conflict of Indicia

If the client or party has one or more of the following data items conflicting with their status:

• Tax residency

• Address

• Country of TIN

• Passport (either first, second or third passport)

• Country of birth

• Certificate of Tax residency

To help the customer identify any possible errors in their assignment of an AEoI status. This report highlights clients which may have possibly been assigned the wrong AEoI status. We’ll determine the status of clients based on the data we hold and provide a report where it is different from the client’s actual status as provided by the customer. Some of the following criteria will be used in determining the client’s status in the report.

s.

PwC 17AEoI Reporting

Reportable accounts

This report lists the clients that will be reported in the AEOI report. It shows the details that will be reported ie. the client’s name, AEOI status, reference and lists the reportable portfolios.

For each client portfolio it shows:

• Valuation

• Interest

• Dividend

• Other Income

• Payments

As with all other operational reports it is available in PDF or Excel/CSV.

PwC 18AEoI Reporting

Client Notification

Send out client notification report/letter to your clients notifying them about what is to be reported on them.

Fully Customisable

Multiple languages and organisation’s branding can be applied.

PwC 20AEoI Reporting

Sign Off/Audit & Tax Authority/Client Enquiries

Filing

Register on your behalf and file the return in all the jurisdictions you operate in.

After filing there will be the inevitable enquiries from Tax Authorities and clients. We can help manage that and answer queries on your behalf. For all AEoI reports we issue we create and store a Snapshot!

Snapshot

A complete Snapshot of the actual data that was used in generating the AEoIreport is stored.

Using our software, it is possible for us to click on a client and see a snapshot of it’s data as at the time the report batch was generated, including accounts, transactions, etc.

So subsequent amendments of transactions on host systems do not cloud how the report was generated at the time. Thus helping in answering queries as to why certain figures were reported.

Tax authorities

Tax authorities

Your clients

We submit reports or we equip you to do so

If required we can manage post-reporting events

IRS HM Revenue & Customs

54

6

PwC 21AEoI Reporting

PwC Automatic Exchange of Information Reporting

In Summary - Key aspects

1. Providing you with the excel template or automatically extracting data from your system

2. Getting the data from you securely

3. Aggregating and validating the data

4. Creating the reports for you to approve

5. Filing reports with tax authorities and creating client reports

6. Creating a full audit trail to allow post filing queries to be handled effectively.

PwC 21AEoI Reporting

Contact details

Circular 230: This document was not intended or written to be used, and it cannot be used, for the purpose of avoiding US Federal, state or local tax penalties that may be imposed on any taxpayer.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLC, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2016 PricewaterhouseCoopers LLC. All rights reserved. 'PwC ' refers to PricewaterhouseCoopers LLC (a limited liability company in the Isle of Man), and may sometimes refer to the PwC network. Each member firm is a separate legal entity.

Phil MorrisTax Director

T: +44 (0) 1624 689 689E: [email protected]

Paul BeesonDirector

T: +44 (0) 781 2069717E: [email protected]