cross-border financing projects

TRANSCRIPT

LAWPLUS

OMEGAWORLD CLASS

CORPORATE FINANCE LAW 2017

CROSS-BORDER FINANCING PROJECTS

22 September 2017

The St.Regis Bangkok

Kowit Somwaiya

Managing Partner

www.lawplusltd.com

LAWPLUS

The information provided in this document is general in nature and may not

apply to any specific situation. Specific advice should be sought before

taking any action based on the information provided. Under no

circumstances shall LawPlus Ltd. or any of its directors, partners and

lawyers be liable for any direct or indirect, incidental or consequential loss

or damage that results from the use of or the reliance upon the information

contained in this document. Copyright © 2017 LawPlus Ltd.

www.lawplusltd.com.

LAWPLUS 1

Presentation Topics

1. Updates on key legal issues and risks relating to cross-border financing

2017

2. Major legal issues in negotiating and drafting cross-border financing

contracts

3. Tax issues applicable to cross-border financing

4. Recommendations for effectively managing disputes arising from cross-

border financing

LAWPLUS 2

• Provision of mortgage agreement is void if it is contrary to:-

- Section 728 (lawsuit must be filed to enforce mortgage);

- Section 729 (conditions precedent for foreclosure);

- Section 735 (prior notice to transferee of mortgaged assets before enforcement).

• Mortgagor is not liable for more than value of mortgaged property (at the time of

foreclosure or enforcement).

• Mortgagee can sell mortgaged property by auction sale within 1 year from receiving a

notice for auction sale from mortgagor without filing a lawsuit.

• Transferee of mortgaged property can redeem mortgaged property anytime or within 60

days of receipt of a notice from the mortgagee.

Updates on key legal issues and risks relating to cross-

border financing 2017 - Amendments to CCC on Mortgages

LAWPLUS 3

• Type, purpose, amount, term of guaranteed obligation must be specified in guarantee

agreement.

• Guarantor is liable for only guaranteed amount.

• Agreement for personal guarantor to be liable jointly and severally with debtor is void. This

does not apply to corporate guarantor.

• Creditor must notify guarantor within 60 days from default date, otherwise the guarantor is

discharged from interest incurred after the 60-day period.

• If part of debt is forgiven and if the remaining debt is paid in full, guarantor is discharged.

• Prior consent for extension of time by a non-financial institution guarantor is not

enforceable.

Updates on key legal issues and risks relating to cross-

border financing 2017 - Amendments to CCC provisions on

Guarantees

LAWPLUS 4

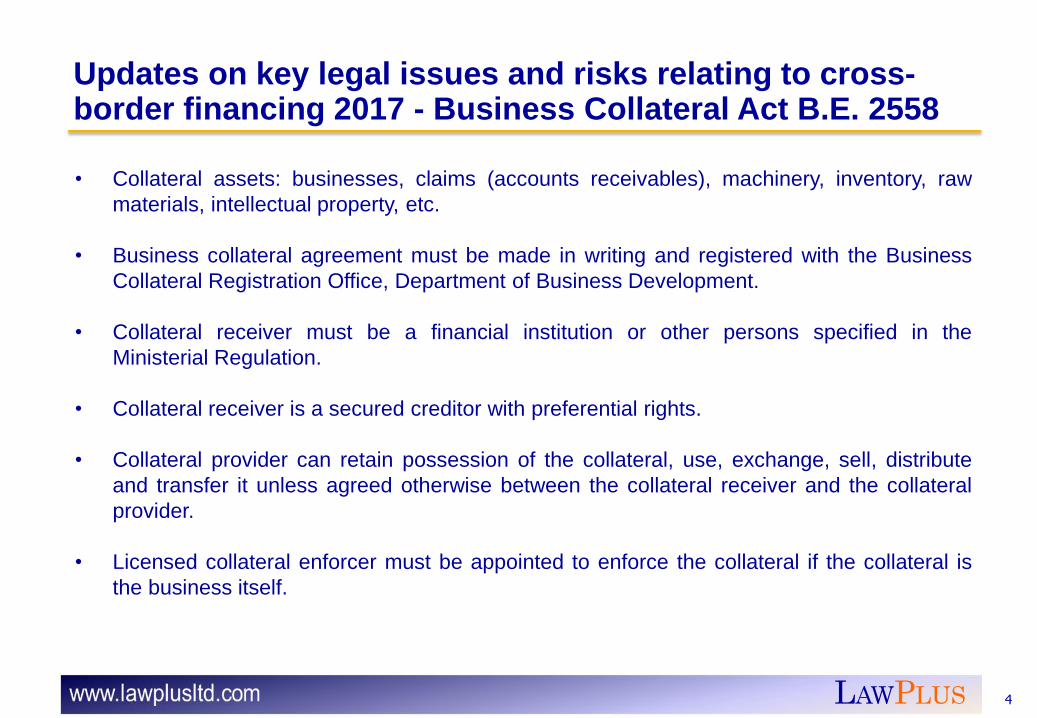

• Collateral assets: businesses, claims (accounts receivables), machinery, inventory, raw

materials, intellectual property, etc.

• Business collateral agreement must be made in writing and registered with the Business

Collateral Registration Office, Department of Business Development.

• Collateral receiver must be a financial institution or other persons specified in the

Ministerial Regulation.

• Collateral receiver is a secured creditor with preferential rights.

• Collateral provider can retain possession of the collateral, use, exchange, sell, distribute

and transfer it unless agreed otherwise between the collateral receiver and the collateral

provider.

• Licensed collateral enforcer must be appointed to enforce the collateral if the collateral is

the business itself.

Updates on key legal issues and risks relating to cross-border financing 2017 - Business Collateral Act B.E. 2558

LAWPLUS 5

• Official Receiver (OR) has power to approve or reject payment application, subject to

objection in Court within 14 days.

• Creditors Committee: Not less than 3, not more than 7.

• Minimum requirement for composition request: payment order, composition amount,

composition plan and procedures, payment period, plan for management of collateral

assets and guarantee.

• Creditor abroad can file for debt repayment after the 4-month period if there is a force

majeure event.

• Creditor in Thailand can file for debt repayment after the 2-month period if there is a force

majeure event.

Updates on key legal issues and risks relating to cross-

border financing 2017 - Amendments to Bankruptcy Act

(No. 8) B.E. 2558

LAWPLUS 6

• Business rehabilitation for individual and SME debtor.

• Debt not less than THB2 million for individual.

• Debt not less than THB3 million for group of persons, non-registered partnership, ROP,

limited partnership.

• Debt more than THB3 million but less than THB10 million for limited company.

• Cashflow test, in addition to liquidity test, etc. is allowed.

• Petition for rehabilitation must be accompanied by a rehabilitation plan approved by

creditors holding 2/3 of total debt.

Updates on key legal issues and risks relating to cross-

border financing 2017 - Amendments to Bankruptcy Act

(No. 9) B.E. 2559

LAWPLUS 7

Major legal issues in negotiating and drafting cross-border financing contracts – General Issues

• Cross-border financing has elements of a domestic loan transaction plus additional issues

and risks due to its cross-border character.

• Lender should be familiar with law of country of borrower and seek advice and opinion from

local lawyer on validity and enforceability of loan agreement and security documents under

relevant foreign law.

• Types of available collaterals (tangible or intangible, moveable or immovable) may differ

between jurisdictions.

• Procedures for enforcement of creditor’s rights under the loan and security documents in

jurisdictions of borrower and security providers can be complex.

LAWPLUS 8

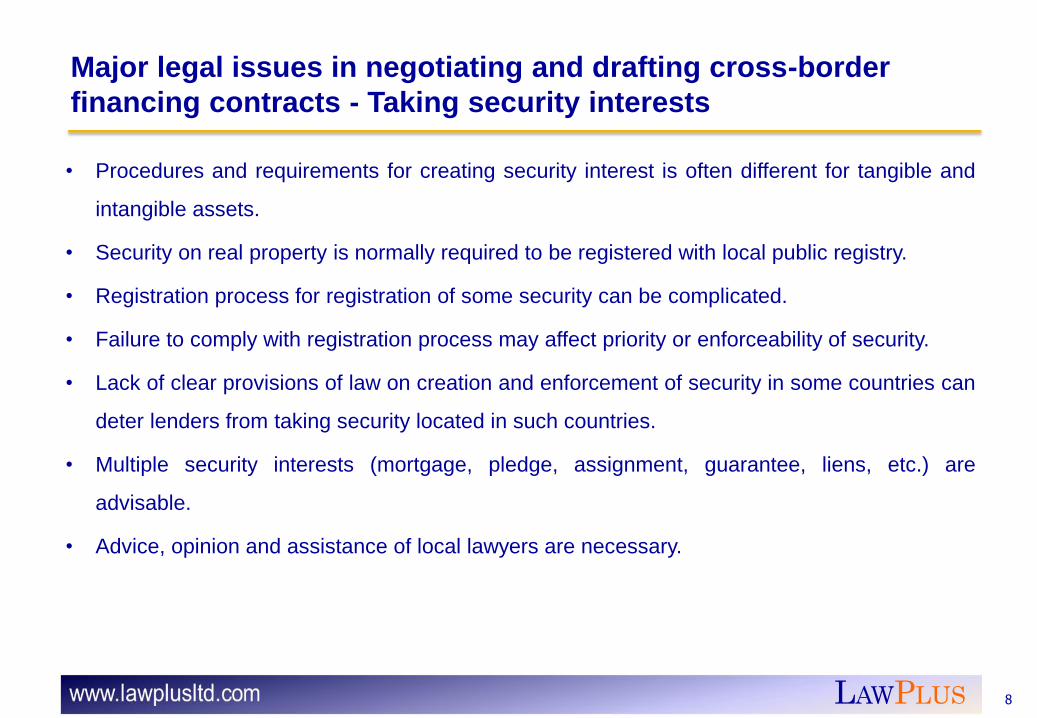

Major legal issues in negotiating and drafting cross-border

financing contracts - Taking security interests

• Procedures and requirements for creating security interest is often different for tangible and

intangible assets.

• Security on real property is normally required to be registered with local public registry.

• Registration process for registration of some security can be complicated.

• Failure to comply with registration process may affect priority or enforceability of security.

• Lack of clear provisions of law on creation and enforcement of security in some countries can

deter lenders from taking security located in such countries.

• Multiple security interests (mortgage, pledge, assignment, guarantee, liens, etc.) are

advisable.

• Advice, opinion and assistance of local lawyers are necessary.

LAWPLUS 9

• Law of foreign jurisdiction dictates types of enforcement and actions available to lender.

• Self-remedies or self-enforcement actions are generally not available.

• Foreign jurisdiction may require a court approval to enforce security.

• Notarization and translation of documents into the local language are normally required for

filing them with local court.

• Costs (court fees, lawyer fees, notarization and legalization fees, etc.) can be costly.

• Sometimes they are calculated by reference to the amount of claimed debts or the value of

collateral, or the security amount.

• Judicial procedures to enforce loan and security can take several years.

Major legal issues in negotiating and drafting cross-border

financing contracts - Enforcing a security over foreign assets

LAWPLUS 10

• If borrower is located or registered in a jurisdiction where enforcement risk is high,

collaterals in a risk-free country that can be enforced without reliance on law and court of

the borrower’s jurisdiction should be created, if possible.

• Offshore Share Pledge: a pledge of shares in a holding company that ultimately owns the

borrower (project finance in Myanmar where the holding company is located in Singapore).

• Offshore Collateral Account: borrower opens and maintains an offshore collateral bank

account in a risk-free country and borrower’s revenues are paid into that account by

customers of borrower.

Major legal issues in negotiating and drafting cross-border

financing contracts - Collateral in a risk-free jurisdiction

LAWPLUS 11

• Transaction might involve a number of jurisdictions, increasing the potential conflict between

laws of jurisdictions involved.

• Where the governing law is specified, local court may not recognize some provisions of

agreements even they are enforceable under the governing law.

• It is not always possible to choose foreign law as the governing law of security documents.

• Governing law for security documents is usually the law of the jurisdiction in which security

asset is located.

• Chosen governing law must be recognized and enforceable in jurisdictions where borrower

and security assets are located.

Major legal issues in negotiating and drafting cross-border

financing contracts – Selecting governing law

LAWPLUS 12

• Borrower may be required to withhold tax on some payment to the lender under the loan

agreement, e.g. interest, arrangement fee, management fee, etc.

• Double-tax treaty between jurisdictions of lender and borrower may address withholding tax

issues.

• In practice, loan agreement contains a “gross-up” provision requiring borrower to pay

lender for any withholding tax withheld from payment to lender.

• Stamp duties may be payable on loan agreement or collateral agreements.

• Failure to pay required stamp duties can make documents inadmissible as evidence

in court proceedings.

• Paying or sealing of stamp duties can be practically difficult.

Tax issues applicable to cross-border financing - Withholding

Tax and Stamp Duties

LAWPLUS 13

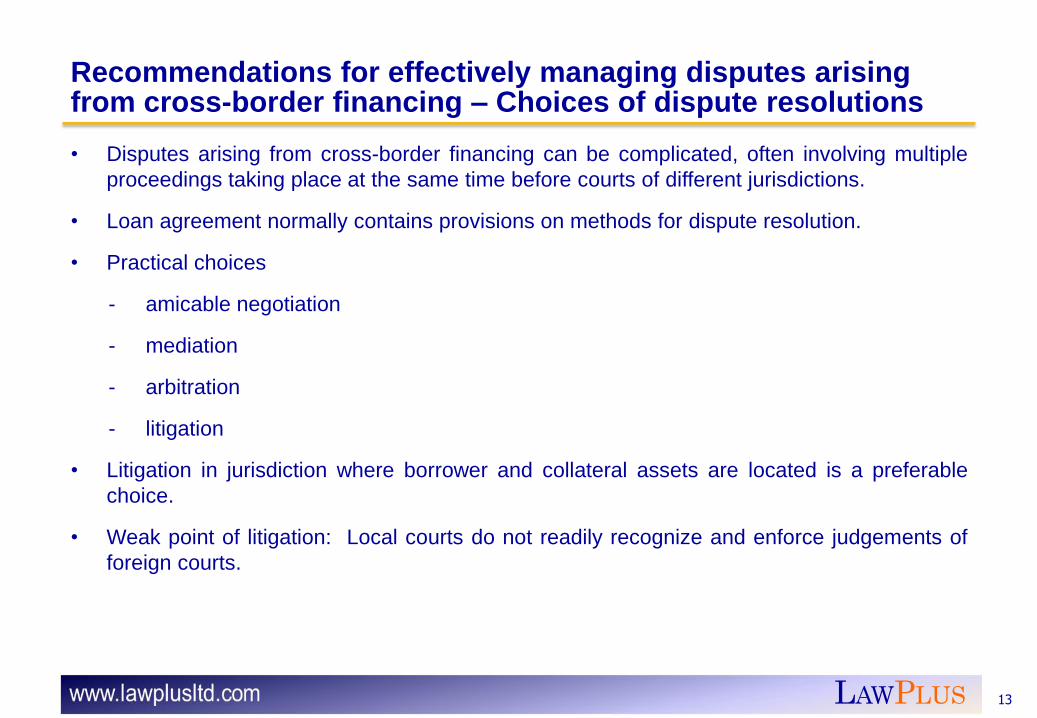

Recommendations for effectively managing disputes arising from cross-border financing – Choices of dispute resolutions • Disputes arising from cross-border financing can be complicated, often involving multiple

proceedings taking place at the same time before courts of different jurisdictions.

• Loan agreement normally contains provisions on methods for dispute resolution.

• Practical choices

- amicable negotiation

- mediation

- arbitration

- litigation

• Litigation in jurisdiction where borrower and collateral assets are located is a preferable

choice.

• Weak point of litigation: Local courts do not readily recognize and enforce judgements of

foreign courts.

LAWPLUS 14

Recommendations for effectively managing disputes arising from cross-border financing - Arbitration • Key advantages of international arbitration for resolving cross-border financing disputes:

- Enforcement: 148 countries are signatories of the New York Convention on Recognition

and Enforcement of Foreign Arbitral Awards, which provides for recognition and

enforcement of arbitral awards, with limited grounds for challenges.

- Neutrality: International arbitration allows parties to resolve their disputes in a neutral

forum.

- Confidentiality: The parties can specify in the dispute resolution clause that they will have

to maintain the confidentiality of the proceedings.

• Thailand is a member state of the New York Convention.

• Need to have an arbitration clause in loan agreement and collateral documents

LAWPLUS

Unit 1401, 14th Floor, 990 Abdulrahim Place, Rama IV Road, Bangkok 10500, Thailand

Tel. +66 (0)2 636 0662, Fax +66 (0)2 636 0663

Room 517, Yangon International Hotel, No. 330 Corner of Ahlone and Pyay Roads, Dagon Township, Yangon, Myanmar

Tel. +95 9 505 6667 and Tel. +95 92 6111 7006

www.lawplusltd.com

Contacts:

Kowit Somwaiya, Managing Partner [email protected] Prasantaya Bantadtan, Partner [email protected] Naddaporn Suwanvajukkasikij, Partner [email protected]