critical analysis on the role of accounting in ethical & sustainability practices of royal dutch...

DESCRIPTION

A Critical Analysis on the Role of Accounting in Ethical & Sustainability Practices of Royal Dutch Shell PLCTRANSCRIPT

Ethics & Sustainability Accounting

Unit Assessment

Miss Archchana Vekneswaran - 12501207

Date of Submission: 19th August, 2013

Submitted in partial fulfillment for the degree of

Bachelor of Arts (Hons) Sustainable Performance Management

Word Count: 2216

An Analysis on Sustainability Practices of Shell and Role of Accountants

REPORT

A Critical Analysis on the Role of Accounting in Ethical & Sustainability Practices of

Royal Dutch Shell PLC

To : The Board of Directors – Royal Dutch Shell PLC

From : Management Accountant

Date : 19th August, 2013

ESA Unit Assessment - MMU1

An Analysis on Sustainability Practices of Shell and Role of Accountants

Executive Summary

As per TIG (2013), “With businesses focusing on generating profits, sustainability was not a

popular concern among companies up until recently”. Increased media attention, pressures from

NGO1s, rapid global information sharing has led to surge of sustainable business practices is

(TIG, 2013). So in order retain customers and employees CSR2 initiatives started to gain more

importance.

The following report critically analyses the sustainability and ethical policies and practices of a

multi-national energy corporation – Shell PLC, and the role of accountants in overcoming such

issues to avoid “green washing” initiatives to build up profits.

The findings suggest that the ethical and sustainability practices of Shell do not portray a picture

of corporate citizen. The sustainability reports are seen as a green washing initiative by most of

public institutions and NGOs. Even though Shell does some philanthropy and community

activities, it does not match the greater danger the company is imposing on the environment for

instance the dangerous Arctic drilling.

Even though accountants are not the people who would pop into mind when someone thinks of

sustainability initiatives of a company, it was found that accountants could play a vital role in

helping companies to be more sustainable in its operations by being in the roles financial

accountants, management accountants, auditors and counselors.

1 NGO - Non Government Organizations2 CSR - Corporate Social Responsibility

ESA Unit Assessment - MMU2

An Analysis on Sustainability Practices of Shell and Role of Accountants

Table of ContentsExecutive Summary.....................................................................................................................................2

1. Introduction.........................................................................................................................................4

1.1 Company Background..................................................................................................................4

1.2 Highlights of Global Energy Market.............................................................................................5

1.3 Existing Competition among Energy Giants.................................................................................6

1.4 Impacts from Regulatory Environment........................................................................................7

2. Critical Discussion on Sustainability Policies and Practices of Shell....................................................9

2.1 Background........................................................................................................................................9

2.2 CSR Initiatives of Shell........................................................................................................................9

2.3 Review and Critiques of Sustainability Policies & Practices of Shell.................................................10

3. Role of Accounting in Ethical and Sustainability Practices.................................................................15

Conclusion.................................................................................................................................................17

References.................................................................................................................................................18

List of Figures

Figure 1: Shell's Upstream and Downstream Product Portfolio..................................................................5Figure 2: World Demand Trend for Energy..................................................................................................5Figure 3: World Total Demand for Primary Energy Sources........................................................................5Figure 4: Per Capita Carbon Emissions per ton by Key Nations...................................................................6Figure 5: Top 6 oil companies of the world.................................................................................................7Figure 6: Details on Top Energy Corporations - 2008..................................................................................7Figure 7: Shell's CSR Initiatives..................................................................................................................10Figure 8: Shell Sustainability Policies.........................................................................................................11Figure 9: Impact of Social Footprint on Shell's Corporate Reputation.......................................................12

ESA Unit Assessment - MMU3

An Analysis on Sustainability Practices of Shell and Role of Accountants

1. Introduction

1.1 Company Background

Shell is one of the largest multinational energy and petrochemical companies headquartered in

Netherlands, which operate in approximately about 70+ countries with 87,000 employees (Shell

Sustainability Report, 2012). Its strategic vision is to be the top performing and most admired

refinery in Asia (Shell, 2013). It is a well-known enterprise for its technical innovation based on

R & D3 in the fields of renewable energy sources.

According to Shell (2013), “Shell’s activities provide low cost, safe and reliable energy supplies

for our customers, world-wide”. As stated by Zhikhareva (2013), Shell owns 15.35% global

market share which allows them to reach required profit margins to reinvest in innovation to

come up with differentiated products.

3 R & D - Research and Development

ESA Unit Assessment - MMU4

Figure 1: Shell's Upstream and Downstream Product Portfolio

Source: Shell Annual Report (2010)Source: Shell Annual Report (2010)

An Analysis on Sustainability Practices of Shell and Role of Accountants

1.2 Highlights of Global Energy Market

IMF4 (2013) reports that the persistent increase in oil prices over the past decade shows that

global oil markets entered into period of increasing scarcity due to rapid growth of emerging

economies and downshift of trend in oil supply. Competition seems to be high among companies

in securing reserves for future production. The demand growth has triggered global CO2 emission

levels on fossil fuels since 1969 (BP, 2013).

Source: Shell (2011)

Among BRICS5 nations, highly populated economies such as China and India are facing an

energy intensive economic growth which leads to increase in demand for fossil fuels (Shell,

2013). IMF (2013) has also reported that “barrel of Brent crude oil crossed the US$100 threshold

in January 2011”. It is expected to continuously increase in the next 2-3 year period”.

Due to marked mobility of individuals and natural decline of existing natural sources the world

would need 40 million barrels of oil per day in future by 2030 (Brinded, 2010). “Unconventional

sources, mainly extra-heavy oil and gas-to-liquids, will take a growing share of world

production” says Brinded (2010). World has to invest more than $1 trillion each year on energy

research projects to come up with new energy sources which are yet to be found (Brinded, 2010).

This challenge is daunting.

4 IMF – International Monetary Fund5 BRICS – Brazil, Russia, India, China, South Africa

ESA Unit Assessment - MMU5

Figure

An Analysis on Sustainability Practices of Shell and Role of Accountants

Figure 4: Per Capita Carbon Emissions per ton by Key Nations

Source: HCF (2013)

When people use energy generated from fossil fuels 12.4 tons of emissions caused from

household activities and 11.7 tons from automotive usage (HCF, 2013). According to Shell

(2011), “The majority scientific view is becoming increasingly pessimistic about the potentially

devastating effects of climate change from greenhouse gases”. UN’s Coppengen summit 2009 to

come up with revised carbon emission target became a failure and Gulf of Mexico oil spill

created legitimate arguments on safety in producing oil and gas in an environmental friendly way

(Shell, 2011).

1.3 Existing Competition among Energy Giants

There are thousands of firms operating in the oil industry. But competition is relatively high

among large companies with high oil reserves. Small competitors serve to niche segments or to

particular countries (Investopedia, 2013).

Source: Google (2013)

ESA Unit Assessment - MMU6

Figure 5: Top 6 oil companies of the world

An Analysis on Sustainability Practices of Shell and Role of Accountants

1.4 Impacts from Regulatory Environment

Energy companies have to comply with global regulations on limits of exploration fields, CO2

emission controls etc. in order continue operations in various countries. In Canadian Alberta oil

sands Shell has to comply with Environmental Protection and Enhancement Act, Alberta Water

Act etc enforced by Federal Department of Fisheries and Oceans (Shell, 2009). Areas in which

constant monitoring will be conducted are:

Tailings Groundwater monitoring Wetland research Conservation and reclamation

ESA Unit Assessment - MMU7

Figure 6: Details on Top Energy Corporations - 2008

Source: Google (2013)

An Analysis on Sustainability Practices of Shell and Role of Accountants

Waste management etc (Shell, 2009)

After the BP6 oil spill in Mexico Gulf regulations are tightened. In America, Bureau of Ocean

Energy management, regulation and enforcement is keen on closely monitoring energy

companies (Krauss and Broder, 2011). But in the UK former Shell chairmen Smith being a part

of energy ministry of UK try to deregulate energy sector along with Charles Hendrey, the energy

minister of UK (Donnovan, 2011).

Shell is the market leader for energy in Nigeria where gas flaring causes trouble to the local

community at the cost of environment (Donnovan, 2011). $2.5 billion worth of waste is recorded

annually making Nigeria the second nation in gas flaring issues. President Goodluck Jonathan or

any other pressure groups aren’t taking any action against this issue (Donnovan, 2011).

Legislation which was developed in 2008 regarding these issues was not effective to date.

Shell has been receiving grants and cooperation for its energy exploration and renewable

resources production. In Alaska, Shell won a conditional approval from the Interior Department

for the project of oil drilling in Beaufort Sea in North Slope, Alaska (Krauss, 2011). The decision

is favorable to Shell as it has drawn the company near the arctic drilling after 5 years of

continuous struggle to get through regulatory hurdles.UK government granted permission for

London array (which includes Shell wind farms) to go ahead with the electricity project which is

in line with renewable energy production system to encourage environmentally friendly

production facilities (Shell corporate website, 2013).

Signature payments, taxes, royalties and commissions are major sources of income for countries

with energy resources (Shell corporate website, 2013). The UK government initiated EITI7 in

2002 to increase the transparency of revenues of oil and mineral activities. Shell ensures that host

countries too to stick to the EITI scheme. So they have been a part of Nigerian EITI to enhance

transparency in disclosing revenues to the government. It is also been promoted in Cameroon,

Kazakhstan etc.

The next chapter looks into a critical discussion on the policies and procedures of Shell PLC on

CSR.

6 BP – British Petroleum Corporation7 EITI – Extractive Industries Transparency Initiative

ESA Unit Assessment - MMU8

An Analysis on Sustainability Practices of Shell and Role of Accountants

2. Critical Discussion on Sustainability Policies and Practices of Shell

2.1 Background

After the criticisms on Shell regarding Nigerian oil platform sink in 1995, it has been the pioneer

to introduce first CSR report in 1998 (Ethical consumer, 2013). Shell established its first CSR

committee in 1997 (Shell, 1998). The £20 million strategy helped the company to rebuild its

public image and enhance reputation among the key decision makers and opinion formers

(Ethical consumer, 2013). A previously critique of Shell, SustainAbility’s involvement

contributed a lot in rebuilding the corporate brand (Ethical Consumer, 2013).

2.2 CSR Initiatives of Shell

Shell has taken substantial initiatives to comply with CSR. One of Shell’s corporate aims says to

engage responsibly in oil, gas and chemicals, which gives an indication that the CSR objective is

incorporated (Times corporate website, 2013). It is also said that in Shell’s R & D approaches to

seek for efficient energy sources with CO2 emissions (Times corporate website, 2013). It is said

in the case that through local partnership Shell tries to minimize the environmental impact on

local communities living near refineries (Times corporate website, 2013). Shell complies with

host country regulations and working with NGOs to address social issues and pollution related

environmental issues (Times corporate website, 2013).

The following figure displays Shell’s community projects, philanthropy and core projects in

terms of women empowerment, water conservation etc.

ESA Unit Assessment - MMU9

Figure 7: Shell's CSR Initiatives

An Analysis on Sustainability Practices of Shell and Role of Accountants

Source: Shell (2013)

2.3 Review and Critiques of Sustainability Policies & Practices of Shell

When it comes to sustainability practices Shell categorizes its initiatives into four as explained in

the figure below. However the policies did not reflect a positive picture in terms of performance

rankings by global agencies despite being a strong supporter of Kyto protocol and Shell is well

above the threshold levels. Such ratings include Carbon Disclosure Leadership Rankings

(CDLR), Dow Jones Sustainability Index, FTSE4Good Index and Shell was only been able to be

presented in Goldman Sachs ratings (Shell, 2013). According to Carus (2013), “Royal Dutch

Shell hardly has the best reputation when it comes to social justice and environmental impacts:

the dumping of the Brent Spar oil-rig; alleged human rights abuses in Nigeria; its controversial

plans to drill in the Arctic Ocean that recently stalled”.

The main factor behind this indices highlights the fact that Shell’s has been downgraded and

been omitted for is poor sustainability initiatives particularly in Nigeria and heavy investments in

energy intensive projects where the company has openly quoted that, “As our business grows

and production becomes more energy intensive, we expect the direct GHG8 emissions from

facilities we operate to rise in the coming years” (Shell, 2013). The company expects its

greenhouse gas emission levels would be higher than 74 million tons (Shell, 2013).

8 GHG – Green House Gas

ESA Unit Assessment - MMU10

An Analysis on Sustainability Practices of Shell and Role of Accountants

Figure 8: Shell Sustainability Policies

Source: Shell (2013)

Shell is a pioneer in very feasible scenario planning techniques where this helped the company to

develop an image of being a far sighted company among all energy giants (Holding, 2013).

These scenarios explains that solar energy will be the key energy source by 2100 and earth could

only be able to absorb 565 gigatons of CO2 emissions whereas this hurdle would be reached

within next 16 years if the energy manufacturers didn’t switch sustainable energy reforms

(Holding, 2013). Having said that, with Shell’s history of well predicted and planned insights

into the future, how could they predict a carbon free future while there competitive strategy is

still to reposition themselves as the leader in oil and gas sectors? (Holding, 2013).

Shell has also sold their solar business in 2006 realizing low profitability compared to fossil fuels

raises the question on whether the large conglomerate hiding something from public reports.

Shell is deviating from its scenarios and investing in LNG9 plants and projects to capture more

than five time oil reserves of Saudi Arabia and spends a lot on conventional with more than $7

billion worth of investments on R & D (Holding, 2013). The organization doesn’t seem very

transparent in reporting on what they intent to do in future and hiding them inside acclaimed

social reports which could harm the stakeholders in terms of climate change in near future.

Would Shell be accountable then?

Shell is one of the energy firms to pursue Arctic drilling to explore new oil reserves in ice and

global environmental groups heavily criticized as this could initiate major and unexpected oil

spills and environmental catastrophes which could be detrimental. As per geologists the cleaning

plans are not up to the par and Shell’s has a glorified mop and bucket in the name of disaster

management plan (Green peace, 2013). With the history of oil spill in UK and in Nigeria, Shell

still claims that they could clean the mess of 90% whereas even 1-2% is not possible in this

offshore ice sea of Alaska (Green peace, 2013).

23% of Shell’s reserves are from Canadian Tar sands and this is an energy intensive project

which is high in its carbon emission levels and the communities around the tar sands faces health

issues and waterways are contaminated with chemicals. Shell’s explanation for this is that there

are producing something the society requires by complying regulations.

9 LNG – Liquefied Natural Gas

ESA Unit Assessment - MMU11

An Analysis on Sustainability Practices of Shell and Role of Accountants

Reserves Replacement Ratio (RRR) is very key ratio among public quoted energy companies

where the investors would be very pleased to invest based the availability of new oil reserve

discoveries and Shell might be a victim to this requirement and hence trying to stick to

conventional fossil fuels. People could recall that Shell overstated its reserves by 20% and faced

legal consequences (Greenpeace, 2013). Solar energy investments being low profitable might

make the investors channel their capital to other companies. This shows that Shell management

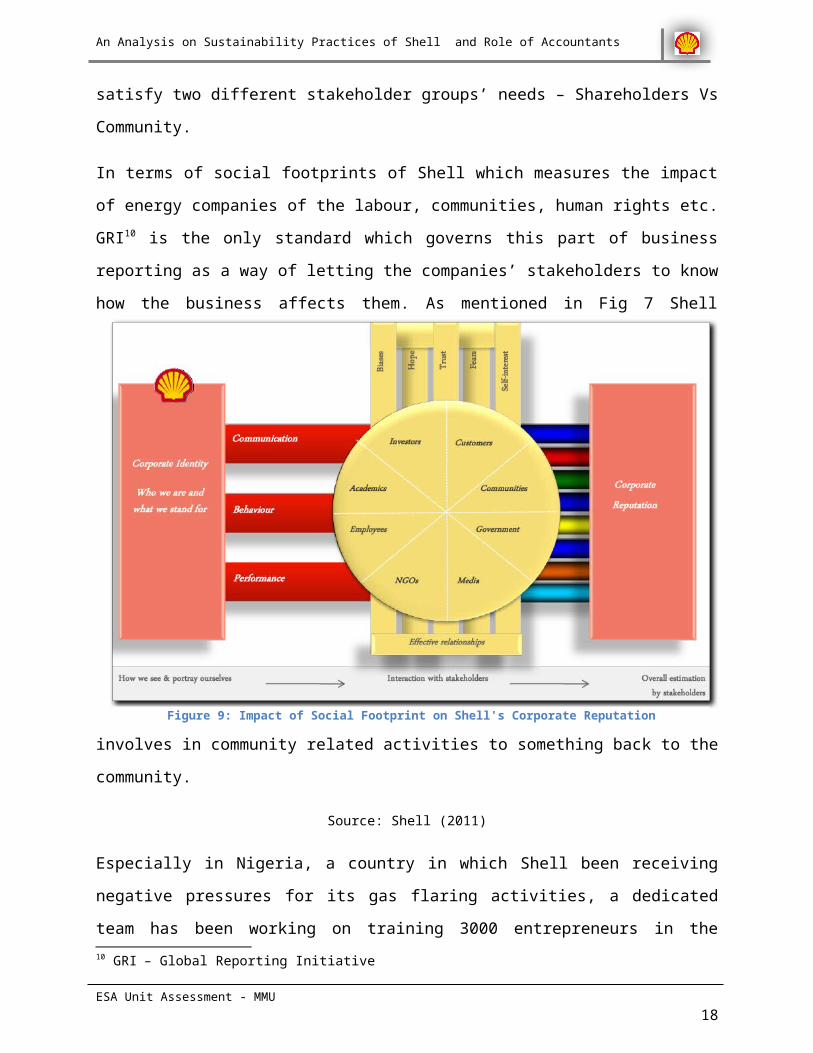

facing dilemma to satisfy two different stakeholder groups’ needs – Shareholders Vs

Community.

In terms of social footprints of Shell which measures the impact of energy companies of the

labour, communities, human rights etc. GRI10 is the only standard which governs this part of

business reporting as a way of letting the companies’ stakeholders to know how the business

affects them. As mentioned in Fig 7 Shell involves in community related activities to something

back to the community.

Source: Shell (2011)

10 GRI – Global Reporting Initiative

ESA Unit Assessment - MMU12

Figure 9: Impact of Social Footprint on Shell's Corporate Reputation

An Analysis on Sustainability Practices of Shell and Role of Accountants

Especially in Nigeria, a country in which Shell been receiving negative pressures for its gas

flaring activities, a dedicated team has been working on training 3000 entrepreneurs in the fields

of project management, catering, welding etc. (Shell, 2011). Shell Live WIRE program has been

helping local entrepreneurs to seek career opportunities which are suitable for their talents (Shell

live wire corporate website, 2011). Shell has also been engaged with road safety campaigned and

urged various governments around the world to avoid risky transportations (GRSP road safety

corporate website, 2011). Shell has invested more than $78 Million and been working with

UNAIDS for AIDS awareness campaigns also ensures that no person is discriminated based on

AIDS and tries to promote communities and families to engage in AIDS awareness initiatives

(Kaye and Shell corporate website, 2011).

However all these social welfare projects seem like a green washing attempt to hide the major

impact on the communities due to oil exploration. Earlier this year, a Dutch court ruled that

Shell’s Nigerian subsidiary guilty of burning out farming fields, destroying the natural

inhabitants and harming the communities due to gas flaring (Ugochukwu, 2013). As any third

world countries Nigerian delta has a very instable government with loopholes in the regulation

and Shell has been blamed to be using these gaps in the system for more than 50 years now

(Ugochukwu, 2013). Above mentioned case was the first victory of Nigerian community over

Royal Dutch Shell which indicates that it would awaken more pressures and the company might

face various litigations the environmental damage if they do not find alternative ways to gas

flaring.

It should also be noted that Shell as the major company with the second largest revenue holds

board positions in organizations which could lobby against Shell. This is very unhealthy practice

and Shell diverts all the board’s interest to satisfy their plans of expanding fossil fuel business

and even recommended UK government to wind up from their wind and solar projects and stick

to conventional techniques. Are they acting as good corporate citizen or just being very biased

towards preserving their self-interests to maximize profits and hurt the environment in which

they operate by manipulating the officials? Exxon Mobil – mostly accused as the bad guy of the

energy business, follows the social code very enthusiastically than Shell. (green peace, 2013).

On the other hand on a positive note, Shell established “Shell foundation” (Fig 7) since 2000 to

invest in sustainable development project worldwide (Europa, 2003). Since its inception, in has

created 21400 jobs and helped save 3.4 million tons of carbon (Carus, 2013). Shell disbursed

ESA Unit Assessment - MMU13

An Analysis on Sustainability Practices of Shell and Role of Accountants

about $111.9 million since 2000 to catalyze scalable and sustainable solutions to globally

developing challenges (Chapman, 2011). Shell centenary scholarship fund program helps 900

students around the world since 1998 for their higher studies in UK (Shell scholar corporate

website, 2011). Despite all the negativity on the independence of the foundation, this

establishment remains independent and drives toward development of technologies and new

business ventures.

ESA Unit Assessment - MMU14

An Analysis on Sustainability Practices of Shell and Role of Accountants

3. Role of Accounting in Ethical and Sustainability Practices

Sustainability and accountability increased its prominence in the recent present when powerful

nations dominated poor countries, when the multinationals dominated and polluted the natural

environment and when there were increased concern on the human rights issues due to business

operations. As per Adams and Gonzalez (2007), “this concern leads the scholars to research on

social and environmental accounting which could trigger organisational change in a capitalist

system”. This develops a conflict based perspective that accounting plays an important role in

the perpetuation of social relations (Adam and Gonzalez, 2007: 333). Many companies including

Shell peruse sustainability accounting and reporting in order to maintain its status quo or to

maintain its own agenda to portray themselves as companies saving the Earth for the future

generations (Adams and Gonzalez, 2007).

Accountants play a vital role when it comes to social accounting where they provide the

mechanism for the firms to be accountable for what they do (Tilt, 2009). Corporate social

disclosure can be the responsibility for all three types of accountants. A financial accountant

could be responsible for the social and environmental aspects of the assets and liabilities and

report them in a standard way (Tilt, 2009). A management accountant could perform a cost

benefit analysis on the environmental issues and auditors could verify the numbers and impacts

to present the true and fair position of the said company (Tilt, 2009). GRI discloses its vision as

companies should report their social, economic and environmental performance in comparable

way to their financial records (Tilt, 2009). Thus the accountants become a group of individuals

ESA Unit Assessment - MMU15

“In terms of power and influence you can forget about the

church forget politics. There is no more powerful institution in

society than business. . . The business of business should not be

about money, it should be about responsibility. It should be

about public good, not private greed”

-Anitta Roddick (2000, cited in Tilt, 2009)

An Analysis on Sustainability Practices of Shell and Role of Accountants

making the company transparent and disclose the non-economic impact through sound and

transparent disclosures of triple bottom line reports (Tilt, 2009).

The International Federation of Accountants set a framework on how the accountants could play

a vital role when it comes to enhancing the corporate reporting stance of the business. According

to IFAC (2011),

Competent and versatile accountants in the finance departments should include

sustainability considerations into the business plans, strategies, capital expenditure

decision making, performance management reports and costing structures to improve the

sustainability of the decision made on the higher level.

In order to maintain integrated management it should involve management of

opportunities and risks and to provide insights to the analysis and decision making which

would enhance high value business partnering of professional accountants.

To improve the quality of external communication with stakeholders, accountants should

play a vital role to setup robust systems which could capture quality data and to maintain

and report them. They should play the role of project managers to put such systems into

practice, establish controls and process for continuous monitoring of the performance.

Be aware of the pressures of sustainability and be able to measure the social costs and

benefits in relation to the business case.

It is also essential that the accountants do not get involved in the management’s efforts towards

shadow accounting. They should carefully consider the changes in the regulatory environment in

relation to sustainable reporting to change the corporate reporting accordingly. Accountants

could benchmark the sustainability practices along with other similar business ventures to adapt

to good practices.

Professional accountants could act as the counselors when the management requires some

guidance in terms of environmental reporting. As accountants records are considered as the

business language, they should be competent enough to provide such advisory services by

continuously improving their skills and knowledge by involving in CPD11 activities. They should

be aware of the company’s emission trading schemes and carefully monitor market trends to help

the top tier make better decisions (IFAC, 2006).

11 CPD – Continuous Professional Development

ESA Unit Assessment - MMU16

An Analysis on Sustainability Practices of Shell and Role of Accountants

Conclusion

The ethical and sustainability practices of Shell do not portray a picture of corporate citizen. The

sustainability reports are seen as a green washing initiative by most of public institutions and

NGOs. Even though Shell does some philanthropy and community activities, it does not match

the greater danger the company is imposing on the environment for instance the dangerous

Arctic drilling. The corporate disclosure openly states how could they are in term of providing

what the community needs by clearly hiding the negative impacts it has on the universe through

its energy intensive operations.

Even though accountants are not the people who would pop into mind when someone thinks of

sustainability initiatives of a company, it was found that accountants could play a vital role in

helping companies to be more sustainable in its operations by being in the roles financial

accountants, management accountants, auditors and counselors.

How the accountants at Shell could bail out the company from its green washing initiatives will

be discussed in the presenting on the upcoming board meeting.

ESA Unit Assessment - MMU17

An Analysis on Sustainability Practices of Shell and Role of Accountants

ReferencesAdams, A., & Gonzalez C, (2007), Engaging with organisations in pursuit of improved sustainability accounting and performance [online], Available from: www.emeraldinsight.com/0951-3574.htm [Accessed on 3rd June, 2013]

BP corporate website (2013) [online], Available from: http://www.bp.com/sectiongenericarticle800.do?categoryId=9036291&contentId=7067014 [Accessed on 8th July, 2013]

Brinded M., (2010), Challenges and Developments in the NOC- IOC relationship, [online], Available from: http://www.shell.com/home/content/media/speeches_and_webcasts/archive/2010/brinded_oxford_23072010.html [Accessed on 16th August, 2013]

British Petroleum (2013), BP Statistical Review [online]. Available from: http://www.bp.com/statisticalreview [Accessed on 27th August, 2013]

Carus, F., (2013), Can a foundation owned by a company such as Shell be truly independent?, [online], Available from: http://www.theguardian.com/sustainable-business/shell-foundation-sustainability-truly-independent [Accessed on 16th August, 2013]

Chapman C., (2011), New Shell foundation report highlights role of angel philosophy in achieving impact at sale [online], Available from: http://www.philanthropyuk.org/news/2010-11-24/new-shell-foundation-report-highlights-role-angel-philanthropy-achieving-impact-scal [Accessed on 7th August, 2013]

Donnovan J., (2013) Shell reserves fraud, [online], Available from: http://royaldutchshellplc.com/2008/05/22/jeroen-van-der-veer-and-the-shell-reserves-fraud-2/ [Accessed on 23rd July, 2013]

Donnovan J., (2013), Gas flaring increases in Nigeria Delta [online], Available from: http://royaldutchshellplc.com/2011/07/07/gas-flaring-increases-in-the-niger-delta/ [Accessed on 13th

July, 2013].

Donnovan J., (2013), Regulation of offshore Rigs Is a Work in Progress [online], Available from: http://royaldutchshellplc.com/2011/04/17/regulation-of-offshore-rigs-is-a-work-in-progress/ [Accessed on 13th July, 2013]

Donovan J., (2013), Former Shell chairman James Smith to lead deregulation of UK oil and gas industry [online], Available from: http://royaldutchshellplc.com/2011/09/07/former-shell-chairman-james-smith-to-lead-deregulation-of-uk-oil-and-gas-industry/ [Accessed on 13th July, 2013]

Ethical consumer corporate website (2013), [online], Available from: http://www.ethicalconsumer.org/CommentAnalysis/Features/CorporateSocialResponsibility.aspx [Accessed on 5th July, 2013]

Europa (2003), The international directory of corporate philanthropy [online], Available from: http://books.google.lk/books?id=R7MqvfrK7H8C&pg=PA377&lpg=PA377&dq=Shell+Philanthropy+projects&source=bl&ots=fnlukXnJoX&sig=kUZNAuyTgZQWtdnaqwfgPenktyE&hl=en&ei=9IuMTt4lxeitB-y-

ESA Unit Assessment - MMU18

An Analysis on Sustainability Practices of Shell and Role of Accountants

gYEC&sa=X&oi=book_result&ct=result&resnum=6&ved=0CFAQ6AEwBQ#v=onepage&q=Shell%20Philanthropy%20projects&f=false [Accessed on 7th August, 2013]

Google images corporate website, (2013) [online]. Available from: http://www.google.lk/imghp?hl=en&tab=wi [Accessed on 17th August, 2013]

Greenpeace (2013), Greenwash +20 [online], Available from: http://www.greenpeace.org/international/Global/international/publications/RioPlus20/GreenwashPlus20.pdf [Accessed on 18th August, 2013]

GRSP corporate website (2013), [online], Available from: http://www.grsproadsafety.org/ [Accessed on 6th July, 2013]

HCF corporate website (2013) [online], Available from: http://www.thehcf.org/emaila5.html [Accessed on 25th July, 2013]

Holding C., (2013), Shell’s Self-serving scenarios , [online], Available from: http://www.triplepundit.com/2013/03/shells-serving-scenarios/ [Accessed on 7th August, 2013]

IFAC (2006), Why Sustainability counts for professional accountants in business [online], Available from: http://www.ifac.org/sites/default/files/publications/files/why-sustainability-counts-f.pdf [Accessed on 18th August, 2013]

IFAC (2011) Sustainability Framework 2.0 [online], Available from: http://www.accountability.org/images/content/4/3/435.pdf [Accessed on 3rd August, 2013]

IMF (2011), World Economic Outlook 2011, Washington D.C, International Monitory Fund.

Investopedia corporate website (2013), [online], Available from: http://www.investopedia.com/features/industryhandbook/oil_services.asp#axzz1ZFL7WEL7 [Accessed on 28th July, 2013]

Kaye L., (2013), Social Footprint, the other business impact, [online], Available from: http://www.triplepundit.com/2013/03/social-footprint-business/ [Accessed on 7th August, 2013]

Krauss C., (2011), Challenges ahead on Arctic Drilling [online]. Available from: http://www.upstreamonline.com/live/article276344.ece [Accesses from 13th August, 2013]

Shell (1998), Shell Sustainability Report, UK, Shell International BV

Shell (2010), Report on Royal Dutch Shell Plc and Oil sands, UK, Shell International BV.

Shell (2011), Accountability in communication, UK, Shell International BV.

Shell (2011), Annual Report 2010, Netherlands, Shell publishing

Shell (2011), Canada’s Oil Sands Issues and Opportunities – economics, UK, Shell International BV.

Shell (2011), Shell fact book 2009, UK, Shell International BV.

Shell (2011), Signals and Signposts, Shell International BV.

Shell (2012), Shell Sustainability Report 2012, Netherlands, Shell publishing

ESA Unit Assessment - MMU19

An Analysis on Sustainability Practices of Shell and Role of Accountants

Shell (2013), Sustainability Report [online], Available from: http://reports.shell.com/sustainability-report/2012/servicepages/downloads/files/entire_shell_sr12.pdf [Accessed on 7th August, 2013]

Shell corporate website, (2013) [online]. Available from: http://www.shell.com/home/content/aboutshell/at_a_glance/ [Accessed on 27th July, 2013]

Shell foundation corporate website (2013) [online], Available from: http://shellfoundation.org/pages/core_lines.php?p=corelines_content&page=breathing [Accessed on 8th August, 2013]

Shell livewire corporate website (2013) [online], Available from: http://www.shell-livewire.com/ [Accessed on 7th August, 2013]

Shell scholar corporate website (2013) [online], Available from: http://shellscholar.org/home/ [Accessed on 7th August, 2013]

The Prince Whales Charities (2012) Accounting for Sustainability [online], Available from: http://www.accountingforsustainability.org/wp-content/uploads/2012/07/A4S-Integrating-Reporting-and-Integrated-Thinking.pdf [Accessed on 3rd August, 2013]

The Times corporate website (2013), Balancing stakeholder needs at Shell, [online], Available from: http://www.thetimes100.co.uk/case-study--balancing-stakeholder-needs--76-403-1.php [Accessed on 15th August, 2013]

TIG (2013), [online], Available from: http://issues.tigweb.org/csr?gclid=CL7OrPHO0asCFUl76wod9XB2Uw [Accessed on 5th July, 2013]

Tilt, C (2009), Corporate Responsibility, Accounting and Accountants [online], Available from: www.springer.com/cda/content/.../cda.../9783642026294-c1.pdf [Accessed on 3rd August, 2013]

Ugochukwu, P. (2013), CSR in the Nigerian oil and gas sector, [online], Available from: http://www.academia.edu/2700307/Corporate_Social_Responsibility_in_the_Nigerian_Oil_and_Gas_Sector_Legal_barriers_facing_claims_of_environmental_liability_against_Multinational_oil_companies_in_Nigeria [Accessed on 16th August, 2013]

Zhikhareva A., (2013) Shell tops in Sales, Wawa most efficient and Chevron flexes its pricing power [online]. Available from: http://newsandresearch.metisresources.com/2011/05/12/shell-tops-in-sales-wawa-most-efficient-chevron-flexes-its-pricing-power/ [Accessed on 27th July, 2013]

ESA Unit Assessment - MMU20