credito valtellinese - gruppocreval.com · credito valtellinese società cooperativa a r.l. —...

TRANSCRIPT

CREDITO VALTELLINESESocietà Cooperativa a r.l. — Registered Offices: Piazza Quadrivio 8, Sondrio, Italy

Sondrio Company Register No. 118 — Registered Bank No. 489Parent Bank of the Credito Valtellinese Group — Registered Banking Group No. 5216.7

Internet: http://www.creval.it Email: [email protected] as of 30 June 2000: Share Capital Euro 146,095,407 — Reserves Euro 285,909,632

Report on operations for thefirst half of 2000

Credito Valtellinese Banking Group

— 2 —

Report on operations for the first half of 2000

— 3 —

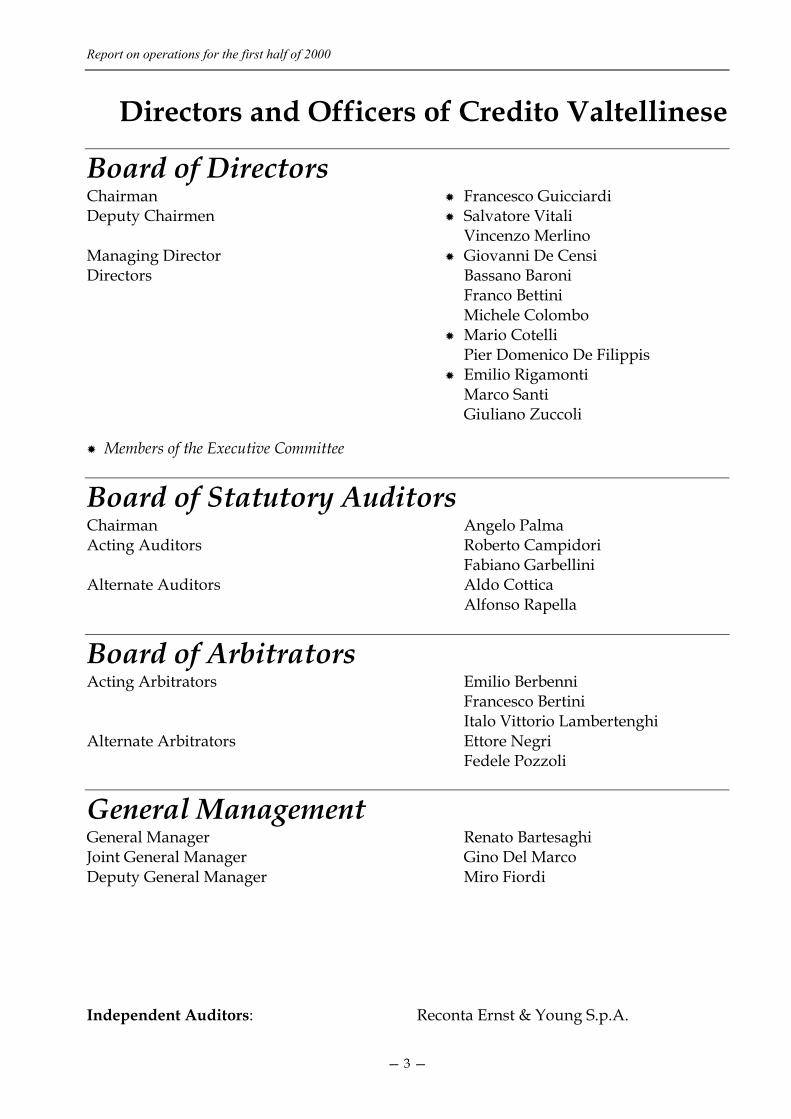

Directors and Officers of Credito Valtellinese

Board of DirectorsChairman ✹ Francesco GuicciardiDeputy Chairmen ✹ Salvatore Vitali

Vincenzo MerlinoManaging Director ✹ Giovanni De CensiDirectors Bassano Baroni

Franco BettiniMichele Colombo

✹ Mario CotelliPier Domenico De Filippis

✹ Emilio RigamontiMarco SantiGiuliano Zuccoli

✹ Members of the Executive Committee

Board of Statutory AuditorsChairman Angelo PalmaActing Auditors Roberto Campidori

Fabiano GarbelliniAlternate Auditors Aldo Cottica

Alfonso Rapella

Board of ArbitratorsActing Arbitrators Emilio Berbenni

Francesco BertiniItalo Vittorio Lambertenghi

Alternate Arbitrators Ettore NegriFedele Pozzoli

General ManagementGeneral Manager Renato BartesaghiJoint General Manager Gino Del MarcoDeputy General Manager Miro Fiordi

Independent Auditors: Reconta Ernst & Young S.p.A.

Credito Valtellinese Banking Group

— 4 —

Report on operations for the first half of 2000

— 5 —

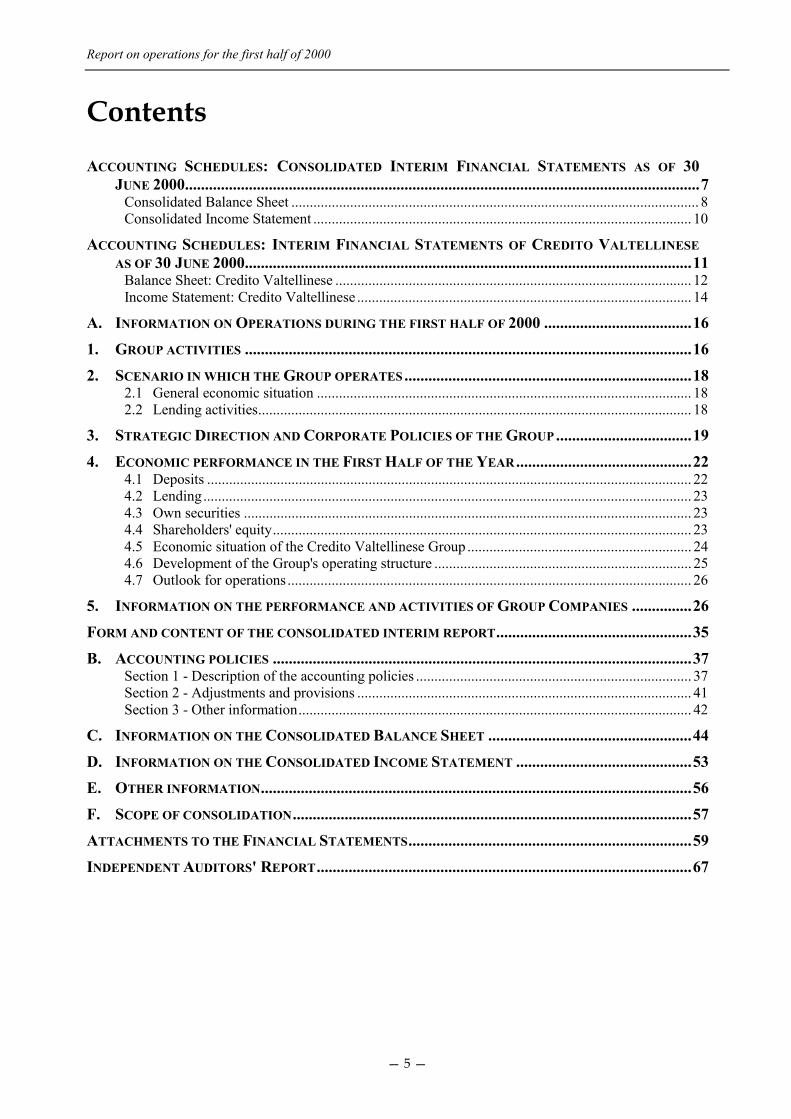

Contents

ACCOUNTING SCHEDULES: CONSOLIDATED INTERIM FINANCIAL STATEMENTS AS OF 30JUNE 2000.................................................................................................................................7

Consolidated Balance Sheet ............................................................................................................... 8Consolidated Income Statement ....................................................................................................... 10

ACCOUNTING SCHEDULES: INTERIM FINANCIAL STATEMENTS OF CREDITO VALTELLINESEAS OF 30 JUNE 2000................................................................................................................11

Balance Sheet: Credito Valtellinese ................................................................................................. 12Income Statement: Credito Valtellinese ........................................................................................... 14

A. INFORMATION ON OPERATIONS DURING THE FIRST HALF OF 2000 .....................................161. GROUP ACTIVITIES ................................................................................................................162. SCENARIO IN WHICH THE GROUP OPERATES ........................................................................18

2.1 General economic situation ...................................................................................................... 182.2 Lending activities...................................................................................................................... 18

3. STRATEGIC DIRECTION AND CORPORATE POLICIES OF THE GROUP ..................................194. ECONOMIC PERFORMANCE IN THE FIRST HALF OF THE YEAR............................................22

4.1 Deposits .................................................................................................................................... 224.2 Lending..................................................................................................................................... 234.3 Own securities .......................................................................................................................... 234.4 Shareholders' equity.................................................................................................................. 234.5 Economic situation of the Credito Valtellinese Group ............................................................. 244.6 Development of the Group's operating structure ...................................................................... 254.7 Outlook for operations.............................................................................................................. 26

5. INFORMATION ON THE PERFORMANCE AND ACTIVITIES OF GROUP COMPANIES ...............26FORM AND CONTENT OF THE CONSOLIDATED INTERIM REPORT.................................................35B. ACCOUNTING POLICIES .........................................................................................................37

Section 1 - Description of the accounting policies ........................................................................... 37Section 2 - Adjustments and provisions ........................................................................................... 41Section 3 - Other information........................................................................................................... 42

C. INFORMATION ON THE CONSOLIDATED BALANCE SHEET ...................................................44D. INFORMATION ON THE CONSOLIDATED INCOME STATEMENT ............................................53E. OTHER INFORMATION............................................................................................................56F. SCOPE OF CONSOLIDATION....................................................................................................57ATTACHMENTS TO THE FINANCIAL STATEMENTS.......................................................................59INDEPENDENT AUDITORS' REPORT..............................................................................................67

Credito Valtellinese Banking Group

— 6 —

Report on operations for the first half of 2000

— 7 —

Accounting Schedules:Consolidated Interim Financial Statements

as of 30 June 2000

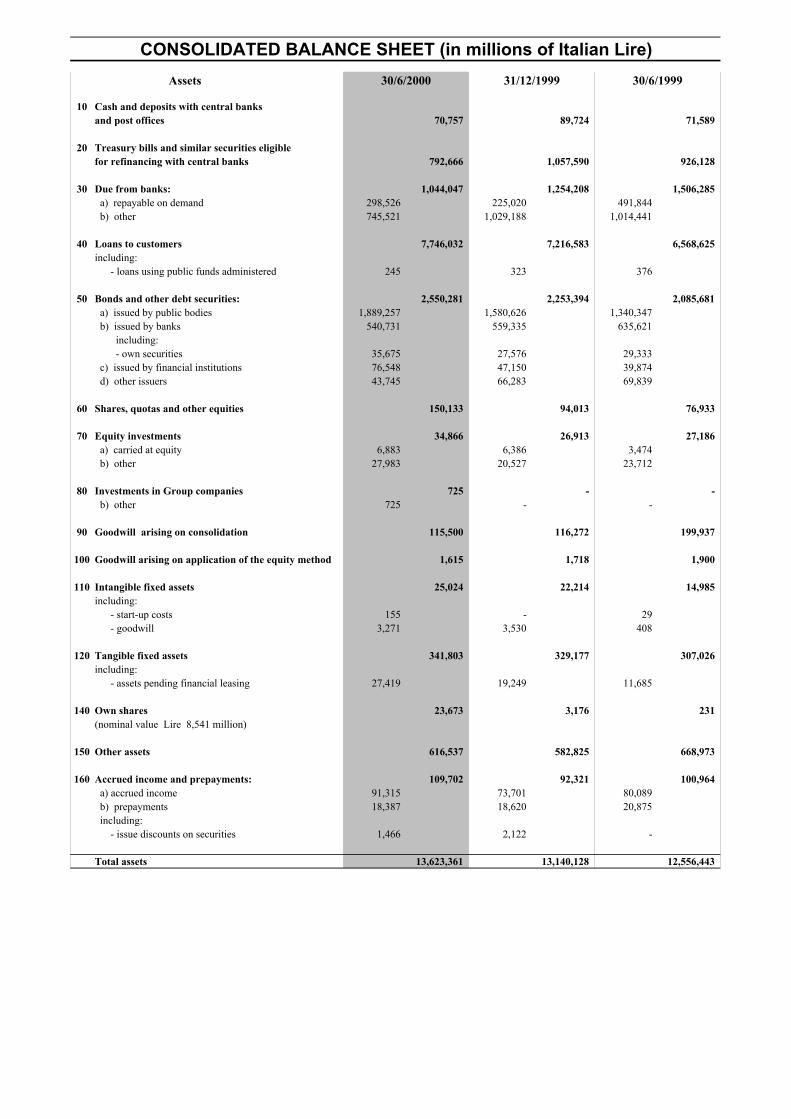

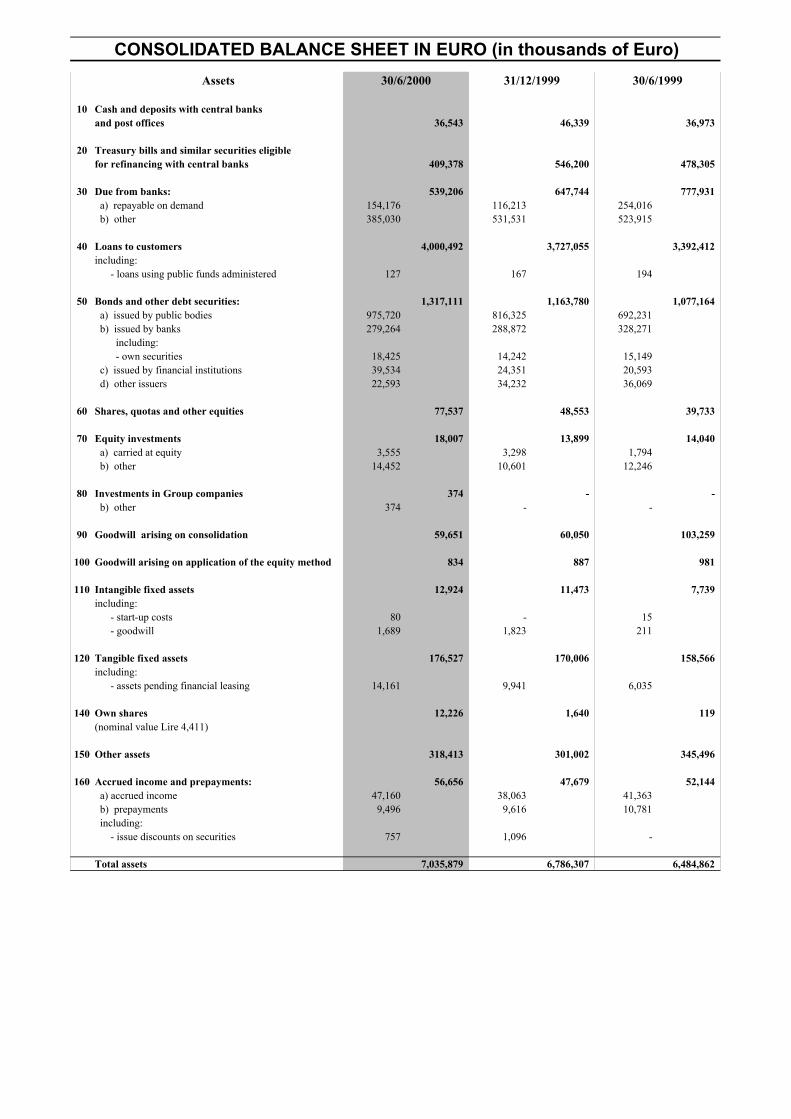

CONSOLIDATED BALANCE SHEET (in millions of Italian Lire) Assets 30/6/2000 31/12/1999 30/6/1999

10 Cash and deposits with central banksand post offices 70,757 89,724 71,589

20 Treasury bills and similar securities eligiblefor refinancing with central banks 792,666 1,057,590 926,128

30 Due from banks: 1,044,047 1,254,208 1,506,285 a) repayable on demand 298,526 225,020 491,844 b) other 745,521 1,029,188 1,014,441

40 Loans to customers 7,746,032 7,216,583 6,568,625including: - loans using public funds administered 245 323 376

50 Bonds and other debt securities: 2,550,281 2,253,394 2,085,681 a) issued by public bodies 1,889,257 1,580,626 1,340,347 b) issued by banks 540,731 559,335 635,621 including: - own securities 35,675 27,576 29,333 c) issued by financial institutions 76,548 47,150 39,874 d) other issuers 43,745 66,283 69,839

60 Shares, quotas and other equities 150,133 94,013 76,933

70 Equity investments 34,866 26,913 27,186 a) carried at equity 6,883 6,386 3,474 b) other 27,983 20,527 23,712

80 Investments in Group companies 725 - - b) other 725 - -

90 Goodwill arising on consolidation 115,500 116,272 199,937

100 Goodwill arising on application of the equity method 1,615 1,718 1,900

110 Intangible fixed assets 25,024 22,214 14,985including: - start-up costs 155 - 29 - goodwill 3,271 3,530 408

120 Tangible fixed assets 341,803 329,177 307,026including: - assets pending financial leasing 27,419 19,249 11,685

140 Own shares 23,673 3,176 231(nominal value Lire 8,541 million)

150 Other assets 616,537 582,825 668,973

160 Accrued income and prepayments: 109,702 92,321 100,964 a) accrued income 91,315 73,701 80,089 b) prepayments 18,387 18,620 20,875 including: - issue discounts on securities 1,466 2,122 -

Total assets 13,623,361 13,140,128 12,556,443

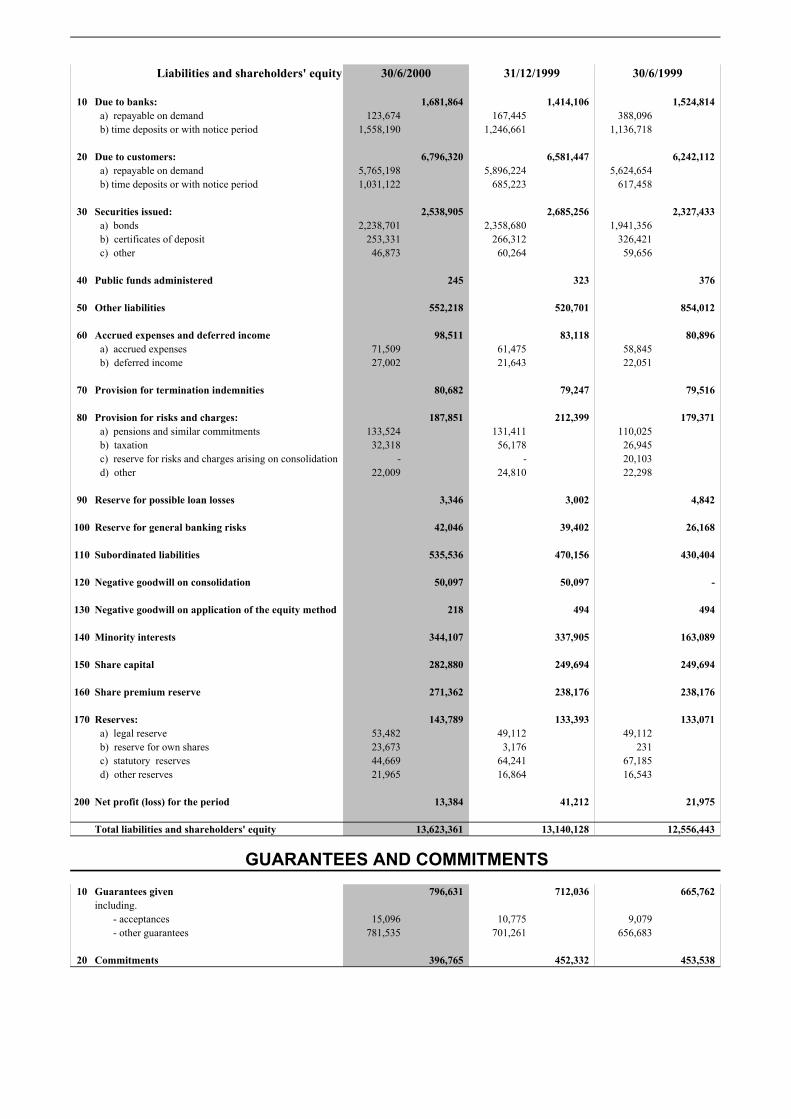

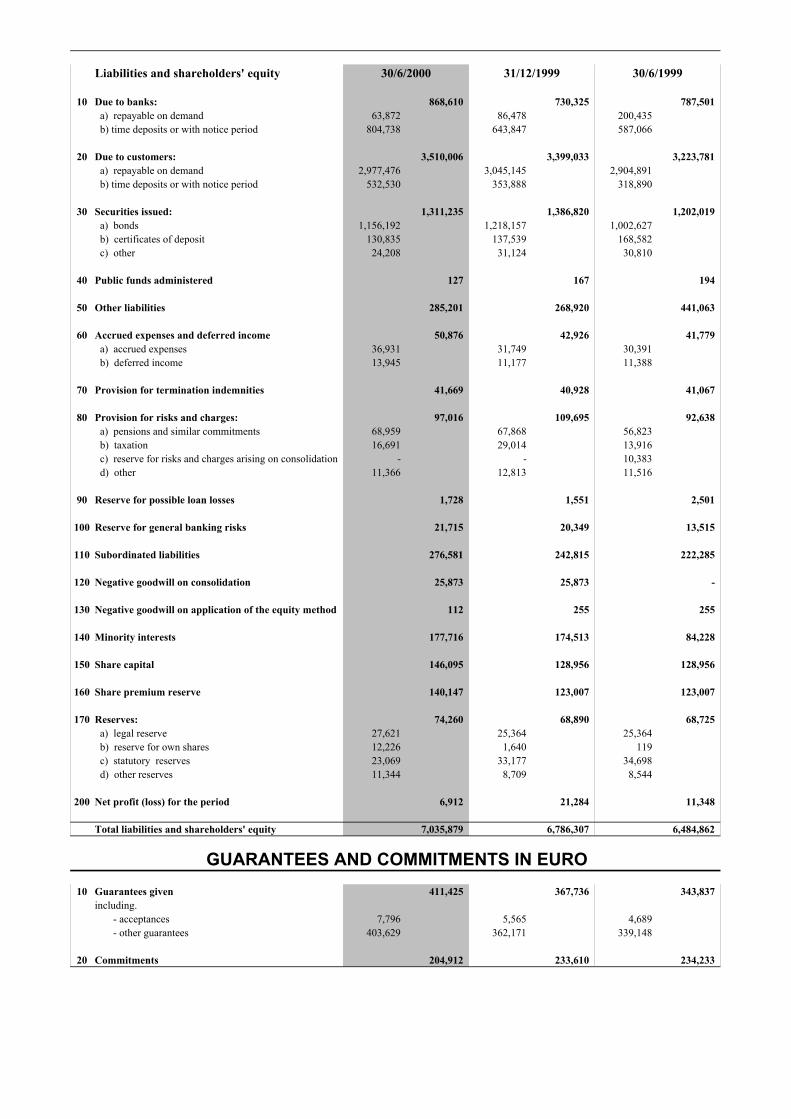

Liabilities and shareholders' equity 30/6/2000 31/12/1999 30/6/1999

10 Due to banks: 1,681,864 1,414,106 1,524,814 a) repayable on demand 123,674 167,445 388,096 b) time deposits or with notice period 1,558,190 1,246,661 1,136,718

20 Due to customers: 6,796,320 6,581,447 6,242,112 a) repayable on demand 5,765,198 5,896,224 5,624,654 b) time deposits or with notice period 1,031,122 685,223 617,458

30 Securities issued: 2,538,905 2,685,256 2,327,433 a) bonds 2,238,701 2,358,680 1,941,356 b) certificates of deposit 253,331 266,312 326,421 c) other 46,873 60,264 59,656

40 Public funds administered 245 323 376

50 Other liabilities 552,218 520,701 854,012

60 Accrued expenses and deferred income 98,511 83,118 80,896 a) accrued expenses 71,509 61,475 58,845 b) deferred income 27,002 21,643 22,051

70 Provision for termination indemnities 80,682 79,247 79,516

80 Provision for risks and charges: 187,851 212,399 179,371 a) pensions and similar commitments 133,524 131,411 110,025 b) taxation 32,318 56,178 26,945 c) reserve for risks and charges arising on consolidation - - 20,103 d) other 22,009 24,810 22,298

90 Reserve for possible loan losses 3,346 3,002 4,842

100 Reserve for general banking risks 42,046 39,402 26,168

110 Subordinated liabilities 535,536 470,156 430,404

120 Negative goodwill on consolidation 50,097 50,097 -

130 Negative goodwill on application of the equity method 218 494 494

140 Minority interests 344,107 337,905 163,089

150 Share capital 282,880 249,694 249,694

160 Share premium reserve 271,362 238,176 238,176

170 Reserves: 143,789 133,393 133,071 a) legal reserve 53,482 49,112 49,112 b) reserve for own shares 23,673 3,176 231 c) statutory reserves 44,669 64,241 67,185 d) other reserves 21,965 16,864 16,543

200 Net profit (loss) for the period 13,384 41,212 21,975

Total liabilities and shareholders' equity 13,623,361 13,140,128 12,556,443

GUARANTEES AND COMMITMENTS10 Guarantees given 796,631 712,036 665,762

including. - acceptances 15,096 10,775 9,079 - other guarantees 781,535 701,261 656,683

20 Commitments 396,765 452,332 453,538

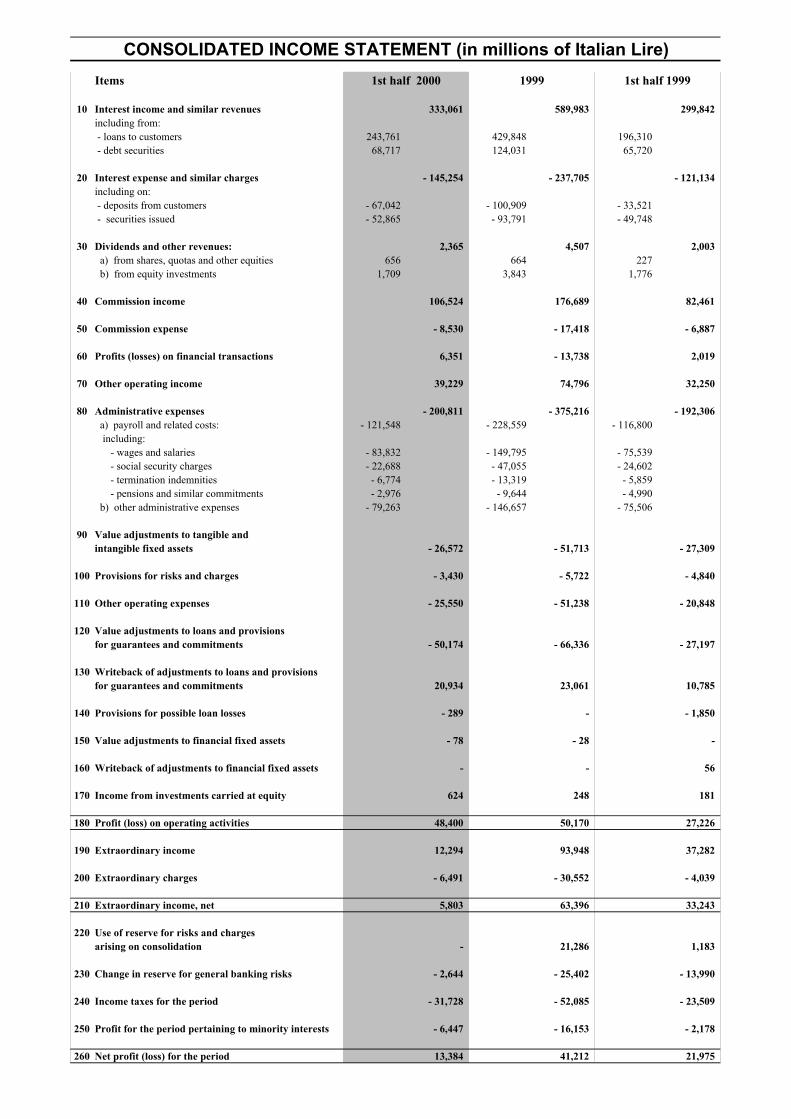

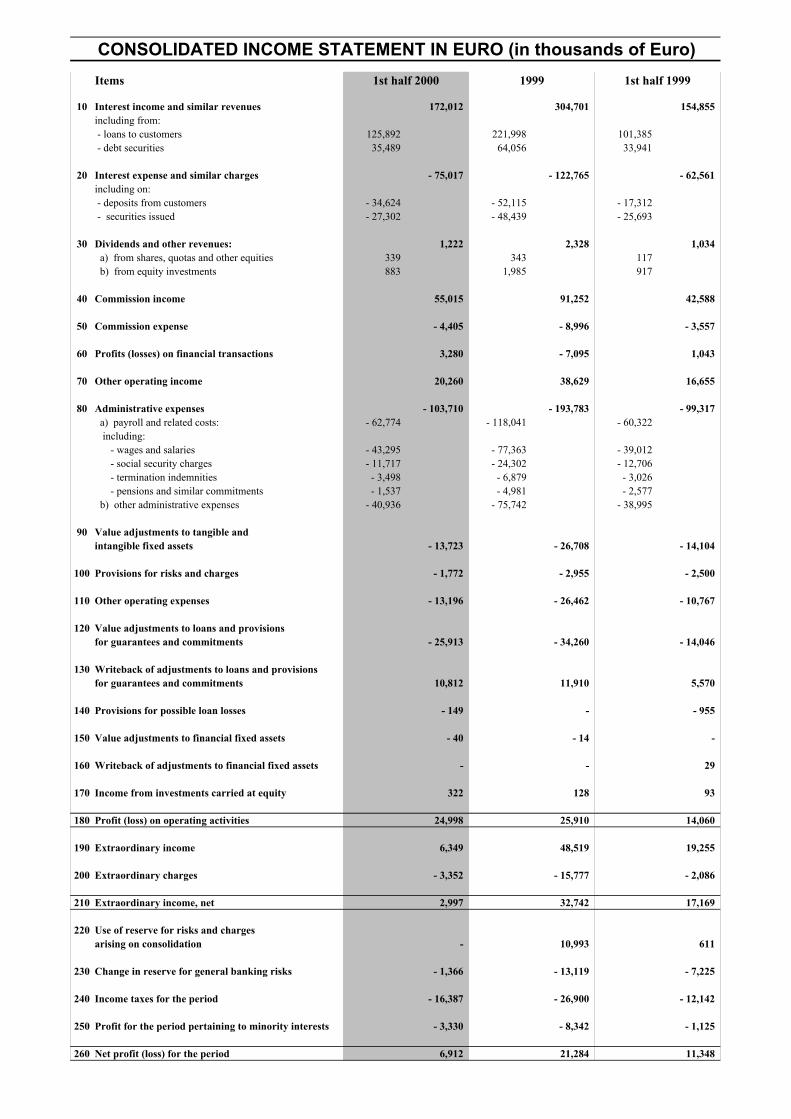

CONSOLIDATED INCOME STATEMENT (in millions of Italian Lire)Items 1st half 2000 1999 1st half 1999

10 Interest income and similar revenues 333,061 589,983 299,842including from: - loans to customers 243,761 429,848 196,310 - debt securities 68,717 124,031 65,720

20 Interest expense and similar charges - 145,254 - 237,705 - 121,134including on: - deposits from customers - 67,042 - 100,909 - 33,521 - securities issued - 52,865 - 93,791 - 49,748

30 Dividends and other revenues: 2,365 4,507 2,003 a) from shares, quotas and other equities 656 664 227 b) from equity investments 1,709 3,843 1,776

40 Commission income 106,524 176,689 82,461

50 Commission expense - 8,530 - 17,418 - 6,887

60 Profits (losses) on financial transactions 6,351 - 13,738 2,019

70 Other operating income 39,229 74,796 32,250

80 Administrative expenses - 200,811 - 375,216 - 192,306 a) payroll and related costs: - 121,548 - 228,559 - 116,800 including: - wages and salaries - 83,832 - 149,795 - 75,539 - social security charges - 22,688 - 47,055 - 24,602 - termination indemnities - 6,774 - 13,319 - 5,859 - pensions and similar commitments - 2,976 - 9,644 - 4,990 b) other administrative expenses - 79,263 - 146,657 - 75,506

90 Value adjustments to tangible andintangible fixed assets - 26,572 - 51,713 - 27,309

100 Provisions for risks and charges - 3,430 - 5,722 - 4,840

110 Other operating expenses - 25,550 - 51,238 - 20,848

120 Value adjustments to loans and provisionsfor guarantees and commitments - 50,174 - 66,336 - 27,197

130 Writeback of adjustments to loans and provisionsfor guarantees and commitments 20,934 23,061 10,785

140 Provisions for possible loan losses - 289 - - 1,850

150 Value adjustments to financial fixed assets - 78 - 28 -

160 Writeback of adjustments to financial fixed assets - - 56

170 Income from investments carried at equity 624 248 181

180 Profit (loss) on operating activities 48,400 50,170 27,226

190 Extraordinary income 12,294 93,948 37,282

200 Extraordinary charges - 6,491 - 30,552 - 4,039

210 Extraordinary income, net 5,803 63,396 33,243

220 Use of reserve for risks and chargesarising on consolidation - 21,286 1,183

230 Change in reserve for general banking risks - 2,644 - 25,402 - 13,990

240 Income taxes for the period - 31,728 - 52,085 - 23,509

250 Profit for the period pertaining to minority interests - 6,447 - 16,153 - 2,178

260 Net profit (loss) for the period 13,384 41,212 21,975

Report on operations for the first half of 2000

— 11 —

Accounting Schedules: Interim FinancialStatements of Credito Valtellinese

as of 30 June 2000

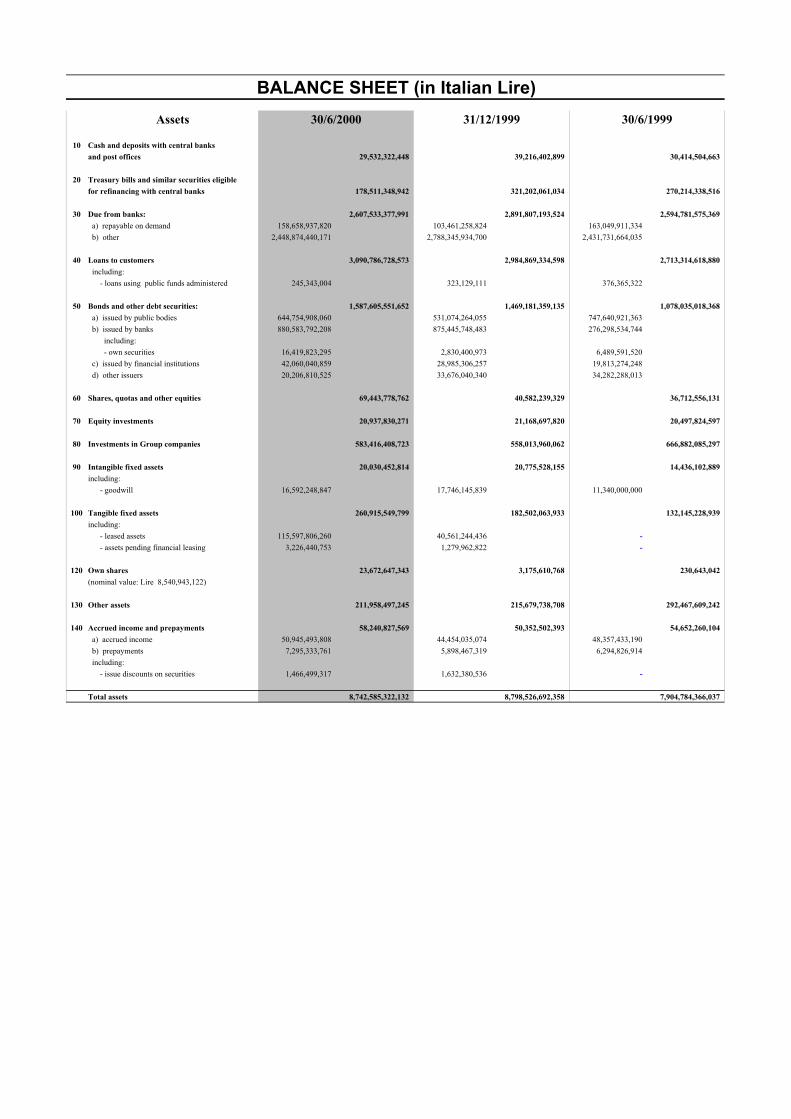

BALANCE SHEET (in Italian Lire)Assets 30/6/2000 31/12/1999 30/6/1999

10 Cash and deposits with central banksand post offices 29,532,322,448 39,216,402,899 30,414,504,663

20 Treasury bills and similar securities eligiblefor refinancing with central banks 178,511,348,942 321,202,061,034 270,214,338,516

30 Due from banks: 2,607,533,377,991 2,891,807,193,524 2,594,781,575,369 a) repayable on demand 158,658,937,820 103,461,258,824 163,049,911,334 b) other 2,448,874,440,171 2,788,345,934,700 2,431,731,664,035

40 Loans to customers 3,090,786,728,573 2,984,869,334,598 2,713,314,618,880 including: - loans using public funds administered 245,343,004 323,129,111 376,365,322

50 Bonds and other debt securities: 1,587,605,551,652 1,469,181,359,135 1,078,035,018,368 a) issued by public bodies 644,754,908,060 531,074,264,055 747,640,921,363 b) issued by banks 880,583,792,208 875,445,748,483 276,298,534,744 including: - own securities 16,419,823,295 2,830,400,973 6,489,591,520 c) issued by financial institutions 42,060,040,859 28,985,306,257 19,813,274,248 d) other issuers 20,206,810,525 33,676,040,340 34,282,288,013

60 Shares, quotas and other equities 69,443,778,762 40,582,239,329 36,712,556,131

70 Equity investments 20,937,830,271 21,168,697,820 20,497,824,597

80 Investments in Group companies 583,416,408,723 558,013,960,062 666,882,085,297

90 Intangible fixed assets 20,030,452,814 20,775,528,155 14,436,102,889including: - goodwill 16,592,248,847 17,746,145,839 11,340,000,000

100 Tangible fixed assets 260,915,549,799 182,502,063,933 132,145,228,939including: - leased assets 115,597,806,260 40,561,244,436 - - assets pending financial leasing 3,226,440,753 1,279,962,822 -

120 Own shares 23,672,647,343 3,175,610,768 230,643,042(nominal value: Lire 8,540,943,122)

130 Other assets 211,958,497,245 215,679,738,708 292,467,609,242

140 Accrued income and prepayments 58,240,827,569 50,352,502,393 54,652,260,104 a) accrued income 50,945,493,808 44,454,035,074 48,357,433,190 b) prepayments 7,295,333,761 5,898,467,319 6,294,826,914 including: - issue discounts on securities 1,466,499,317 1,632,380,536 -

Total assets 8,742,585,322,132 8,798,526,692,358 7,904,784,366,037

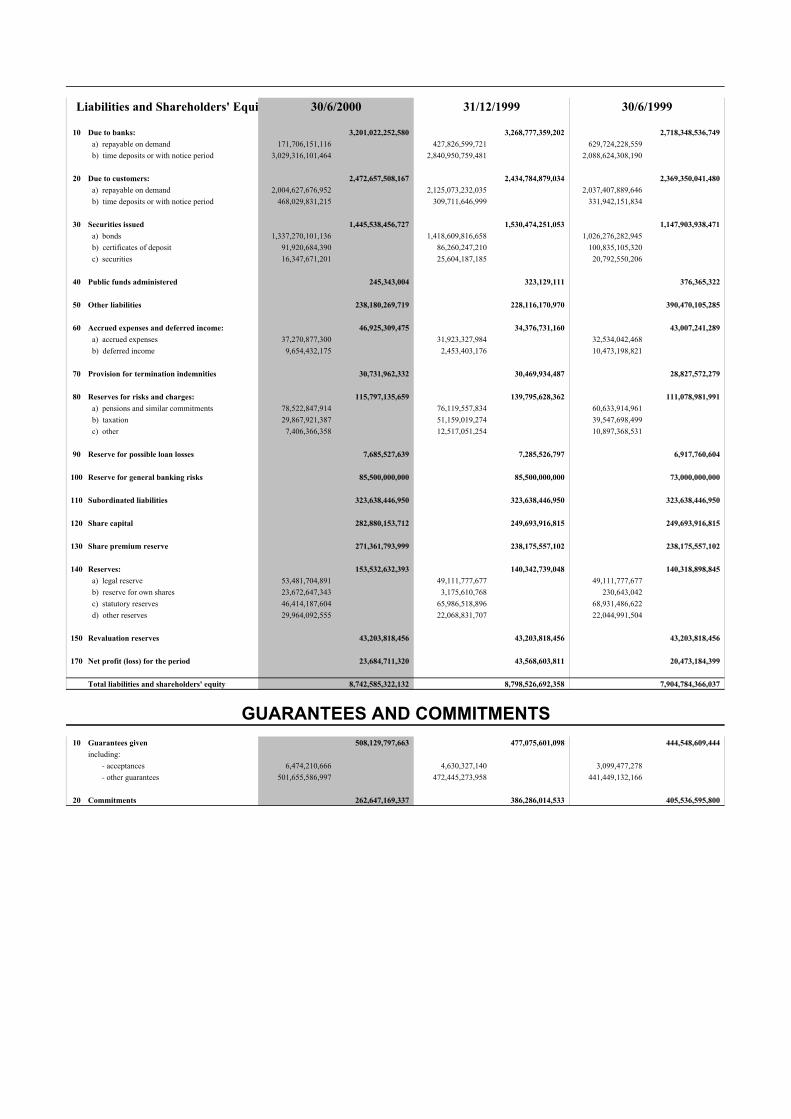

Liabilities and Shareholders' Equi 30/6/2000 31/12/1999 30/6/1999

10 Due to banks: 3,201,022,252,580 3,268,777,359,202 2,718,348,536,749 a) repayable on demand 171,706,151,116 427,826,599,721 629,724,228,559 b) time deposits or with notice period 3,029,316,101,464 2,840,950,759,481 2,088,624,308,190

20 Due to customers: 2,472,657,508,167 2,434,784,879,034 2,369,350,041,480 a) repayable on demand 2,004,627,676,952 2,125,073,232,035 2,037,407,889,646 b) time deposits or with notice period 468,029,831,215 309,711,646,999 331,942,151,834

30 Securities issued 1,445,538,456,727 1,530,474,251,053 1,147,903,938,471 a) bonds 1,337,270,101,136 1,418,609,816,658 1,026,276,282,945 b) certificates of deposit 91,920,684,390 86,260,247,210 100,835,105,320 c) securities 16,347,671,201 25,604,187,185 20,792,550,206

40 Public funds administered 245,343,004 323,129,111 376,365,322

50 Other liabilities 238,180,269,719 228,116,170,970 390,470,105,285

60 Accrued expenses and deferred income: 46,925,309,475 34,376,731,160 43,007,241,289 a) accrued expenses 37,270,877,300 31,923,327,984 32,534,042,468 b) deferred income 9,654,432,175 2,453,403,176 10,473,198,821

70 Provision for termination indemnities 30,731,962,332 30,469,934,487 28,827,572,279

80 Reserves for risks and charges: 115,797,135,659 139,795,628,362 111,078,981,991 a) pensions and similar commitments 78,522,847,914 76,119,557,834 60,633,914,961 b) taxation 29,867,921,387 51,159,019,274 39,547,698,499 c) other 7,406,366,358 12,517,051,254 10,897,368,531

90 Reserve for possible loan losses 7,685,527,639 7,285,526,797 6,917,760,604

100 Reserve for general banking risks 85,500,000,000 85,500,000,000 73,000,000,000

110 Subordinated liabilities 323,638,446,950 323,638,446,950 323,638,446,950

120 Share capital 282,880,153,712 249,693,916,815 249,693,916,815

130 Share premium reserve 271,361,793,999 238,175,557,102 238,175,557,102

140 Reserves: 153,532,632,393 140,342,739,048 140,318,898,845 a) legal reserve 53,481,704,891 49,111,777,677 49,111,777,677 b) reserve for own shares 23,672,647,343 3,175,610,768 230,643,042 c) statutory reserves 46,414,187,604 65,986,518,896 68,931,486,622 d) other reserves 29,964,092,555 22,068,831,707 22,044,991,504

150 Revaluation reserves 43,203,818,456 43,203,818,456 43,203,818,456

170 Net profit (loss) for the period 23,684,711,320 43,568,603,811 20,473,184,399

Total liabilities and shareholders' equity 8,742,585,322,132 8,798,526,692,358 7,904,784,366,037

GUARANTEES AND COMMITMENTS10 Guarantees given 508,129,797,663 477,075,601,098 444,548,609,444

including: - acceptances 6,474,210,666 4,630,327,140 3,099,477,278 - other guarantees 501,655,586,997 472,445,273,958 441,449,132,166

20 Commitments 262,647,169,337 386,286,014,533 405,536,595,800

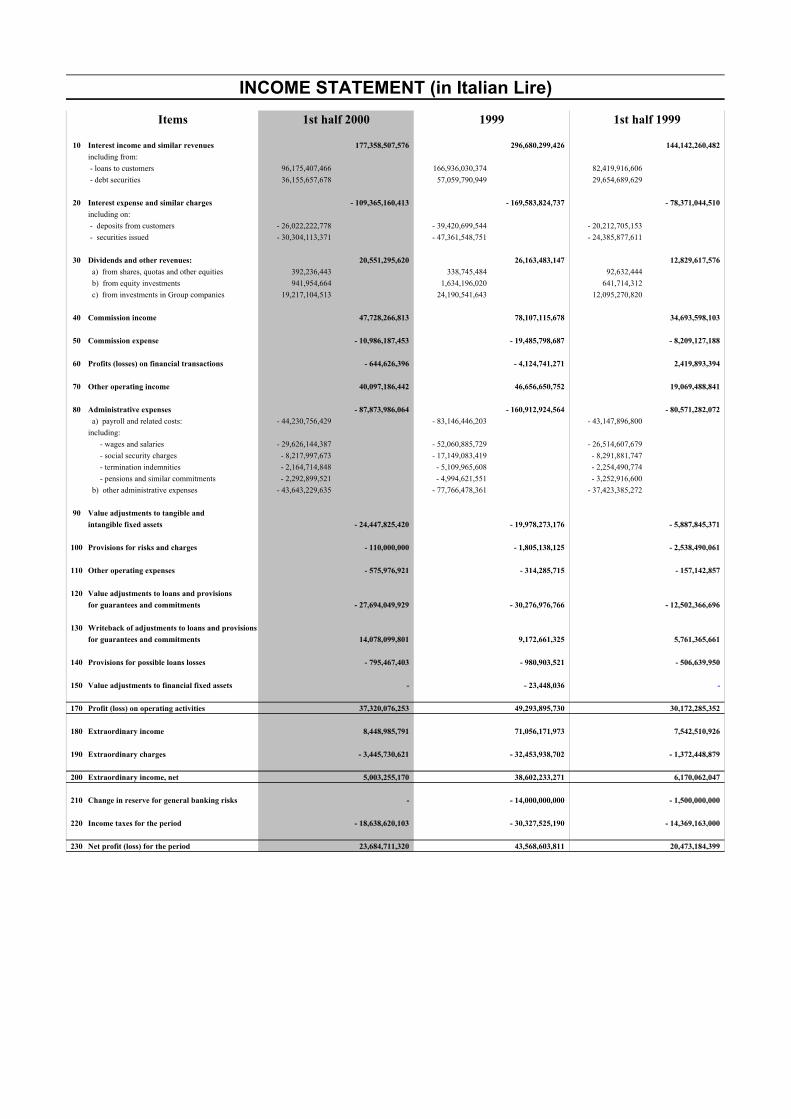

INCOME STATEMENT (in Italian Lire)Items 1st half 2000 1999 1st half 1999

10 Interest income and similar revenues 177,358,507,576 296,680,299,426 144,142,260,482including from: - loans to customers 96,175,407,466 166,936,030,374 82,419,916,606 - debt securities 36,155,657,678 57,059,790,949 29,654,689,629

20 Interest expense and similar charges - 109,365,160,413 - 169,583,824,737 - 78,371,044,510including on: - deposits from customers - 26,022,222,778 - 39,420,699,544 - 20,212,705,153 - securities issued - 30,304,113,371 - 47,361,548,751 - 24,385,877,611

30 Dividends and other revenues: 20,551,295,620 26,163,483,147 12,829,617,576 a) from shares, quotas and other equities 392,236,443 338,745,484 92,632,444 b) from equity investments 941,954,664 1,634,196,020 641,714,312 c) from investments in Group companies 19,217,104,513 24,190,541,643 12,095,270,820

40 Commission income 47,728,266,813 78,107,115,678 34,693,598,103

50 Commission expense - 10,986,187,453 - 19,485,798,687 - 8,209,127,188

60 Profits (losses) on financial transactions - 644,626,396 - 4,124,741,271 2,419,893,394

70 Other operating income 40,097,186,442 46,656,650,752 19,069,488,841

80 Administrative expenses - 87,873,986,064 - 160,912,924,564 - 80,571,282,072 a) payroll and related costs: - 44,230,756,429 - 83,146,446,203 - 43,147,896,800including: - wages and salaries - 29,626,144,387 - 52,060,885,729 - 26,514,607,679 - social security charges - 8,217,997,673 - 17,149,083,419 - 8,291,881,747 - termination indemnities - 2,164,714,848 - 5,109,965,608 - 2,254,490,774 - pensions and similar commitments - 2,292,899,521 - 4,994,621,551 - 3,252,916,600 b) other administrative expenses - 43,643,229,635 - 77,766,478,361 - 37,423,385,272

90 Value adjustments to tangible andintangible fixed assets - 24,447,825,420 - 19,978,273,176 - 5,887,845,371

100 Provisions for risks and charges - 110,000,000 - 1,805,138,125 - 2,538,490,061

110 Other operating expenses - 575,976,921 - 314,285,715 - 157,142,857

120 Value adjustments to loans and provisionsfor guarantees and commitments - 27,694,049,929 - 30,276,976,766 - 12,502,366,696

130 Writeback of adjustments to loans and provisionsfor guarantees and commitments 14,078,099,801 9,172,661,325 5,761,365,661

140 Provisions for possible loans losses - 795,467,403 - 980,903,521 - 506,639,950

150 Value adjustments to financial fixed assets - - 23,448,036 -

170 Profit (loss) on operating activities 37,320,076,253 49,293,895,730 30,172,285,352

180 Extraordinary income 8,448,985,791 71,056,171,973 7,542,510,926

190 Extraordinary charges - 3,445,730,621 - 32,453,938,702 - 1,372,448,879

200 Extraordinary income, net 5,003,255,170 38,602,233,271 6,170,062,047

210 Change in reserve for general banking risks - - 14,000,000,000 - 1,500,000,000

220 Income taxes for the period - 18,638,620,103 - 30,327,525,190 - 14,369,163,000

230 Net profit (loss) for the period 23,684,711,320 43,568,603,811 20,473,184,399

Report on operations for the first half of 2000

— 15 —

Report on Operations duringthe first half of 2000

Credito Valtellinese Banking Group

— 16 —

A. Information on Operations during the first half of 2000

1. Group activities

The Group is characterised by the banking activities carried out by the seven regionalbanks located throughout Italy, a finance company and by the operations of threecompanies who carry out complementary activities; the latter were formed for the purposeof decentralising certain collateral and support services with the aim of guaranteeinggreater efficiency and a higher degree of specialisation.Credito Valtellinese is the Parent Bank of the Banking Group bearing the same name,whose mission is to consolidate and develop relations with the socio-economic make-up ofthe regions in which it operates.

A commentary on the consolidated balance sheet and income statement balances of theCredito Valtellinese Group, the statement of highlights concerning the various companieswhich form the Group and the main transactions entered into during the period, ispresented below, together with information on strategic agreements and the newacquisitions concluded, in order to fully illustrate the size, structure and financial andequity position of the Group in its entirety.

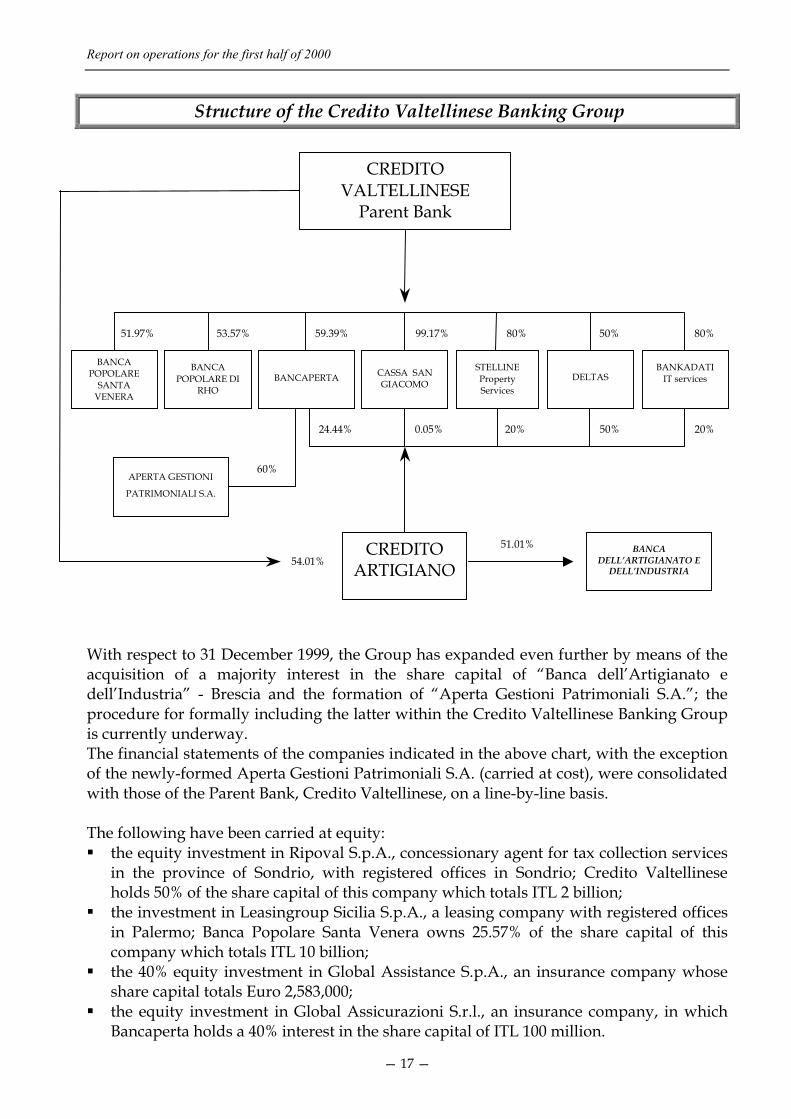

A breakdown of the Group and the related interest holdings (%) is illustrated in the chart"Group structure".

Report on operations for the first half of 2000

— 17 —

Structure of the Credito Valtellinese Banking Group

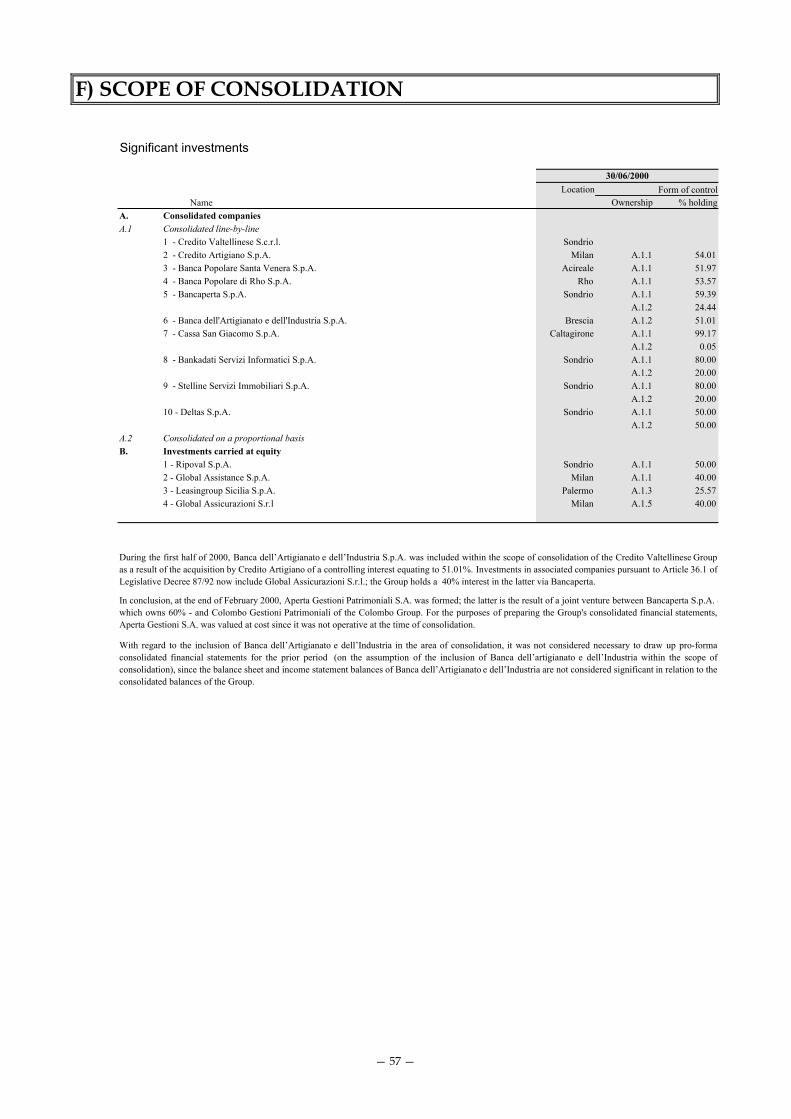

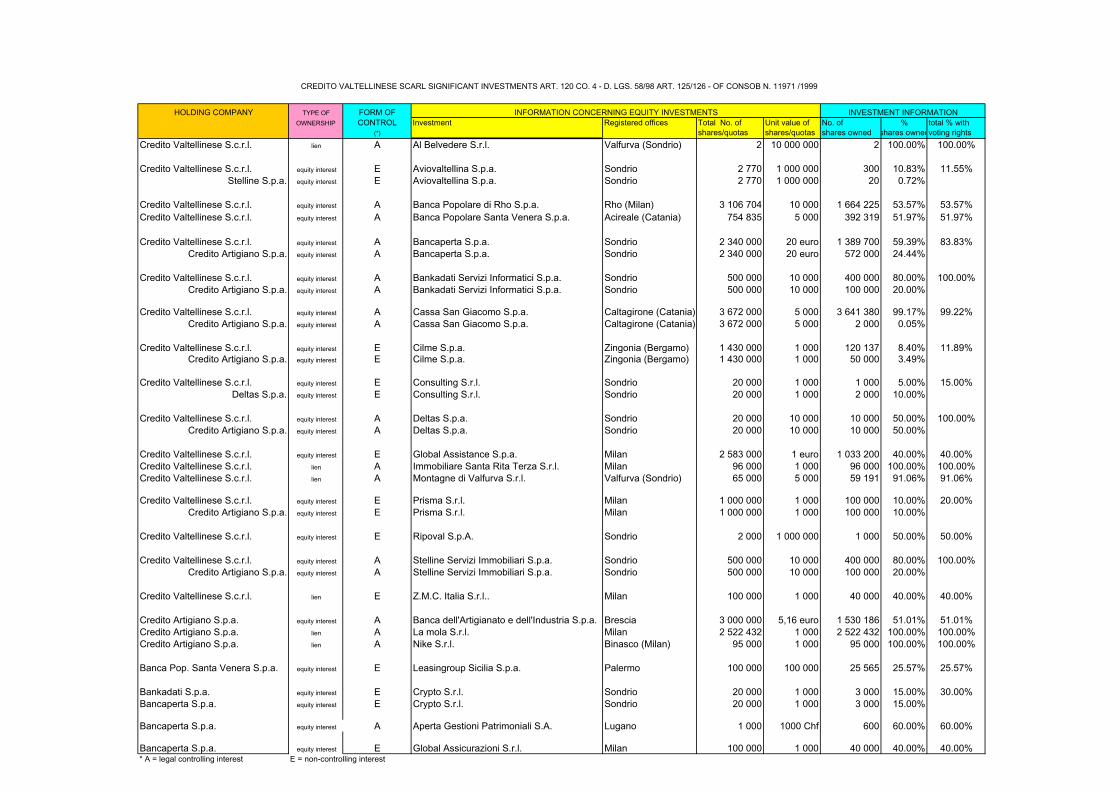

With respect to 31 December 1999, the Group has expanded even further by means of theacquisition of a majority interest in the share capital of “Banca dell’Artigianato edell’Industria” - Brescia and the formation of “Aperta Gestioni Patrimoniali S.A.”; theprocedure for formally including the latter within the Credito Valtellinese Banking Groupis currently underway.The financial statements of the companies indicated in the above chart, with the exceptionof the newly-formed Aperta Gestioni Patrimoniali S.A. (carried at cost), were consolidatedwith those of the Parent Bank, Credito Valtellinese, on a line-by-line basis.

The following have been carried at equity:� the equity investment in Ripoval S.p.A., concessionary agent for tax collection services

in the province of Sondrio, with registered offices in Sondrio; Credito Valtellineseholds 50% of the share capital of this company which totals ITL 2 billion;

� the investment in Leasingroup Sicilia S.p.A., a leasing company with registered officesin Palermo; Banca Popolare Santa Venera owns 25.57% of the share capital of thiscompany which totals ITL 10 billion;

� the 40% equity investment in Global Assistance S.p.A., an insurance company whoseshare capital totals Euro 2,583,000;

� the equity investment in Global Assicurazioni S.r.l., an insurance company, in whichBancaperta holds a 40% interest in the share capital of ITL 100 million.

CREDITOVALTELLINESE

Parent Bank

BANCAPOPOLARE

SANTAVENERA

BANCAPOPOLARE DI

RHOBANCAPERTA CASSA SAN

GIACOMO

STELLINEPropertyServices

DELTASBANKADATI

IT services

CREDITOARTIGIANO

51.97% 53.57% 59.39% 99.17% 80% 50% 80%

0.05% 20% 50% 20%

51.01%54.01%

BANCADELL’ARTIGIANATO E

DELL’INDUSTRIA

24.44%

APERTA GESTIONI

PATRIMONIALI S.A.

60%

Credito Valtellinese Banking Group

— 18 —

The equity investment in Crypto was also carried at cost; the latter is a limited liabilitycompany with registered offices in Sondrio and share capital of ITL 20 million, owned viaBankadati S.I. (who holds a 15% interest) and Bancaperta S.p.A. (who holds a 15%interest).

2. Scenario in which the Group operates

Before analysing the results achieved by the Credito Valtellinese Group, we believe itexpedient to briefly comment in a general manner on the economic-lending scenario inwhich the Group operates.

2.1 General economic situationAt international level, the first half of 2000 saw an increase in world growth widespreadthroughout all areas, the epicentre being in the US which was to able to continue growingat a rate of over 5% per annum in the first two quarters of the year. Japan was alsoinvolved and started to show the first signs of an end to its period of stagnation, while inEurope the situation progressively picked up speed, until a growth rate of 3% wasachieved in the second quarter of the year.On the price front, the period saw a slight rise which was the result of two contrastingforces: the increases in production due to the technological revolution underway have infact curbed pressure deriving from the continual rise in the price of oil and raw materials.However, at international level an upwards trend in the cost of money has ensued. Theperiod was also affected by shifts in capital from Europe towards the US, a change whichhas furthered the constant erosion of the exchange rate of the single currency.Italy was also involved in the process currently underway; such involvement materialisingin grow in Gross Domestic Product at a rate of 2.8% on an annual basis — lower howeverthan the European average— and a rate of inflation of 2.7%, higher than the average rateof the “Euro-11”.The result has been a slow but continual loss in competitiveness, which can no longer beoffset by manipulation of exchange rates, and has manifested in the deterioration of thetrade balance. On a positive note, mention should be made of the improvement in publicfinances, with a annual deficit which has dropped below the threshold of 2% with respectto GDP, as well as grow in private consumer's expenditure and investments made bycompanies, backed by a highly confident climate.

2.2 Lending activitiesDuring the first half of the year under review, growth in bank loans continued presentingan increase of 11.7% compared to June 19991. A contributory factor to the rapid growth inlending was the low level of interest rates on loans and the steady demand for financinglinked to the upturn in manufacturing activities. 1 Source: Italian Banking Association: Monthly analysis of total banks with short-term and medium-to-long-term funding.

Report on operations for the first half of 2000

— 19 —

The rapid upturn in lending mainly concerned the long and medium-term element drawnalong essentially by growth in loans to households: the protraction in the latter's elevatedpropensity to borrow appears strictly linked to the continuance of favourable conditions interms of the cost of borrowing.The improvement in loan quality has also continued: the performance of the ratio net non-performing loans/Capital for Supervisory Purposes fell at the end of the first half of 2000to 21.2%, compared with 28.4% in the same period in 1999. 2In June 2000, bank deposits amounted to ITL 1,371,500 billion, disclosing growth on anannualised basis of 3.10%.As far as interest rates were concerned, in June 2000 the average rate on loans stood at6.23%, while the average current account interest rate was 1.79%. At the end of the first sixmonths of 2000, the spread between the average interest-bearing lending rate and theaverage rate on ordinary customer deposits (both denominated in Euro and in the EU-11currencies) came to 3.05 percentage points for Italy, up 34 basis points with respect to theaverage value during the first six months of 1999.

3. Strategic Direction and Corporate Policies of the Group

During the first six months of the new accounting period, important initiatives werelaunched, some of which had already been outlined in the 1999 annual financialstatements.The most significant events which occurred during the first half of the year are illustratedbelow.

New Strategic Plan - N.B.EDuring the course of the last six months, formulation of the 2000-2003 strategic plancontinued; the plan summarises objectives, operating guidelines and projects with the aimof outlining the strategic direction fundamental for the development of the co-ordinatedactivities of all the components of the Group over the medium-term.

Bancaperta S.p.A.In January, Bancaperta, the Web Bank of the Credito Valtellinese Group, launched the newservice denominated “@perto”, the current account designed specifically for exclusiveelectronic on-line use; this product launch forms part of the strategy targeted at enhancingthe range of services offered via screen-based channels.From March of this year, following the sale of Julius Baer funds via the Internet and “shopwindow securities” (selected financial investment proposals), the range of services offeredon the web by Bancaperta was enhanced by trading on-line activities. The latter permitcustomers to carry out transactions involving the purchase and sale of securities on theInternet in real time, by operating directly on the Italian Stockmarket. 2 Source: Italian Banking Association: Monthly analysis of total banks with short-term and medium-to-long-term funding.

Credito Valtellinese Banking Group

— 20 —

In April, an agreement was signed between Omnitel and the Credito Valtellinese Groupwhich anticipates the introduction of Bancaperta S.p.A. within the sphere of the Omnitelportal, as well as offering the Clientele of all the Group banks the possibility to carry outtransactions for trading and banking on-line by using innovative WAP technology. Theagreement in question will make it possible to enhance the means for benefiting from theweb-banking products and services developed and offered by the Credito ValtellineseGroup even further.During May, the share capital of this bank was increased from ITL 50 to 90 billion, bymeans of the entire utilisation of the remaining 40,000 warrants held by the shareholders.In June, the shareholders' meeting approved the project for the stockmarket listing of thecompany; in this context, conversion of the share capital into Euro was authorised and ashare capital increase against payment was decided which will take the current amountfrom Euro 46,800,000 to Euro 56,140,000, by means of the issue of 467,000 share with anindividual par value of Euro 20 each, to be offered as part of the Public Offer for Sale andSubscription whose end purpose is the listing of the company.During the whole of the six month period, formulation of the project for the listing of theweb bank of the Credito Valtellinese Group on the stockmarket continued. It is anticipatedthat the application for admission to the official trading lists will be presented by the endof this year.Lastly, shareholders are reminded that the current shareholding structure of Bancaperta(Credito Valtellinese, Credito Artigiano, Julius Baer, Cattolica Assicurazione, Colombo diLugano Group) will be supplemented by the entry of Elsag S.p.A, Genoa– part of theFinmeccanica Group (a company specialised in the field of Information andCommunication Technology), as well as GZ-Bank, Frankfurt (German central bank forpublic and co-operative loans).

Banca dell’Artigianato e dell’IndustriaDuring the first half of the year under review, the inclusion of Banca dell’Artigianato edell’Industria - Brescia within the Group was concluded, following the extremelysuccessful take-over bid launched by Credito Artigiano.This transaction led to the concentration of certain services within the Parent Company,Credito Artigiano, as well as the re-allocation of certain activities to the Group structuresdelegated to carry out management functions and provide operative support activities.

Quality certificationOn 1 June, the annual inspection carried out by CISQ CERT was concluded favourably atthe four Group companies which, in the last few years, have obtained quality certification.Credito Valtellinese, Credito Artigiano, Bankadati Servizi Informatici and Stelline ServiziImmobiliari, have therefore had their respective quality certification confirmed for 2000and the first four months of 2001.The long-term plan for quality certification anticipates the acquisition this year ofcompliance certification for Bancaperta S.p.A., with regard to the processes for the Group'sfinancial management and the telematic bank.

Report on operations for the first half of 2000

— 21 —

On a consistent basis with the growth strategies, both structural and operative, which havebeen established for some time now, several important agreements for strategiccollaboration were concluded during the period .

Banca Popolare Sant’AngeloDuring the period, the strategic alliance project with Banca Popolare Sant’Angelo wasfinalised. As of 31 December 1999, the Sicilian bank disclosed overall deposits of ITL 3,220billion, of which ITL 2,040 billion were direct deposits and ITL 1,280 billion indirectdeposits, including ITL 850 billion in managed savings; net lending came to ITL 1,270billion.The agreement signed initially anticipates the spin-off of the activities of Banca PopolareSant’Angelo Popolare, which will transfer two thirds of its assets to a small bank, theNuova Banca del Monte Sant’Agata. Subsequently, it is anticipated that the latter willchange its name to Banca Regionale Sant’Angelo S.p.A.; the Group will undertake anequity holding in the share capital of the new bank by means of a public purchase offer on55% of the new bank's capital which — on conclusion of the afore-mentioned transactions— will be launched by the subsidiary Credito Artigiano.By means of this operation, the Group will consolidate its presence within the Sicilianterritory, increasing its current number of branches on the island from 63 to 125.

GZ-Bank AGIn January of this year, an important strategic alliance between the Credito ValtellineseGroup and SGZ-Bank AG of Frankfurt was finalised; the latter is the German central bankfor public and co-operative loans.The objective of the agreement is the realisation of joint ventures in various sectors oflending and financial brokerage, with particular regard for the areas concerninginternational payment systems, corporate finance and the sale of funds via the Internet.During the course of the last six months, SGZ-Bank AG publicly announced its mergerwith GZB-Bank of Stuttgart; the new bank created as a result of the merger of the twoGerman institutions took on the name of GZ Bank AG. The latter thus became the leaderof the three central banks belonging to the system of German co-operative banks with 20%of the lending market in Germany.

Elsag S.p.A.During the first few months of 2000, the Credito Valtellinese Group and Elsag — acompany belonging to the Finmeccanica Group, leading supplier of software and ITservices— announced an important strategic alliance for the joint development of aninnovative service centre: Bankels web centre.The objective which forms the basis of this agreement is essentially to make Bankels webcentre an instrument capable of offering banking and financial operators — under total orpartial outsourcing arrangements — all the services based on the most innovativetechnology and IT architecture available on the market today.

Credito Valtellinese Banking Group

— 22 —

The agreement also anticipates the development of joint activities between Elsag and theGroup in the area of e-commerce and e-business, with the aim of developing complete,integrated and flexible solutions at the highest technological levels.

Aperta Gestioni Patrimoniali S.A.During the first half of the year under review, a new entity within the Credito ValtellineseGroup took shape, arising as a result of a joint venture between Bancaperta, web bank andbank specialised in the financial sector belonging to the Credito Valtellinese BankingGroup, and Colombo Gestioni Patrimoniali which belongs to the Colombo of LuganoGroup; the latter boasts consolidated experience in the area of asset management andspecialist business consultancy.For those customers who require personalised financial consulting solutions, it is essentialto avail of a valid point of reference capable of providing high quality, qualifiedconsultancy services.Via this new company, the Group aims to provide such assistance to its clientele andstrengthen its presence on one of the main financial markets, following the positiveexperience gained by means of its representative office.As part of a strategic plan directed at guaranteeing an increasingly more trenchantpresence of the Group within the Swiss territory, the transfer of our representative officefrom Lugano to Zurich was also decided.

4. Economic performance in the First Half of the Year

The first half of the year confirmed the positive operational trend of the CreditoValtellinese Group seen in previous accounting periods. The increase in business volumesconcerning the traditional activities of deposits and lending— as in all the servicesprovided to customers, even those of an innovative nature — represents the salientelement for this part of the year.

4.1 DepositsAs of 30 June 2000, direct deposits from customers3 totalled ITL 9,871 billion, disclosingan increase of 9.7% compared to the ITL 9,000 billion reported as of 30 June 1999.In more detail, as can be seen from the balance sheet liabilities, the item “Due tocustomers” (item 20 which includes current accounts, savings deposits and repurchaseagreements) rose to ITL 6,796 billion (+ 8.9%), while the item “Securities issued” (item 30which included bonds, certificates of deposit and other securities) amounted to ITL 2,539billion, up 9.1%. The component represented by subordinated liabilities has increased by24.4%, amounting at period end to ITL 536 billion.

3 The aggregate comprises item 20 “due to customers”, item 30 “securities issued”, item 40 “public fundsadministered" and item 110 “subordinated liabilities”

Report on operations for the first half of 2000

— 23 —

The components of indirect deposits came to ITL 14,693 billion, an increase of 17.4%compared with 30 June 1999. All elements of managed savings rose, amounting to ITL6,196 billion, up 8.1%.Total deposits, comprising direct and indirect customer funding, therefore amounted toITL 24,564 billion at the end of the first half of 2000, up ITL 3,047 billion on the sameperiod last year (+14.2%).

4.2 LendingDuring the first half of the year, total cash loans granted to customers amounted to ITL7,746 billion, an increase of 17.9% compared to the same period in the prior year.The continual increase recorded in the disbursement of loans is accompanied, as always,by constant attention paid to the analysis of the solvency and ability of the counterpart tomeet the commitments undertaken, in part in relation to the area of economic activity andthe inherent potential in the reference markets.Total net non-performing loans at the end of the period came to ITL 252 billion.The ratio of non-performing loans to total lending came to 3.25%, compared with 3.56% inthe same period last year. The degree of coverage of writedowns4 came to 61.07% of grossnon-performing positions.In terms of loan concentration, the reporting of “Significant Exposures”— positions equalto or greater than 10% of Capital for Supervisory Purposes — was non-existent as of thedate of this report.

4.3 Own securitiesThe aggregate of securities owned by the Group, comprising item 20 “Treasury bills andsimilar securities eligible for refinancing with central banks”, item 50 “Bonds and otherdebt securities ” and item 60 “Shares, quotas and other equities”, amounts to ITL 3,493billion versus ITL 3,405 billion at the end of 1999. Dealing securities came to ITL 3,394billion, while the investment portfolio rose during the period from ITL 66 billion to ITL 99billion, with an increase therefore of ITL 33 billion.

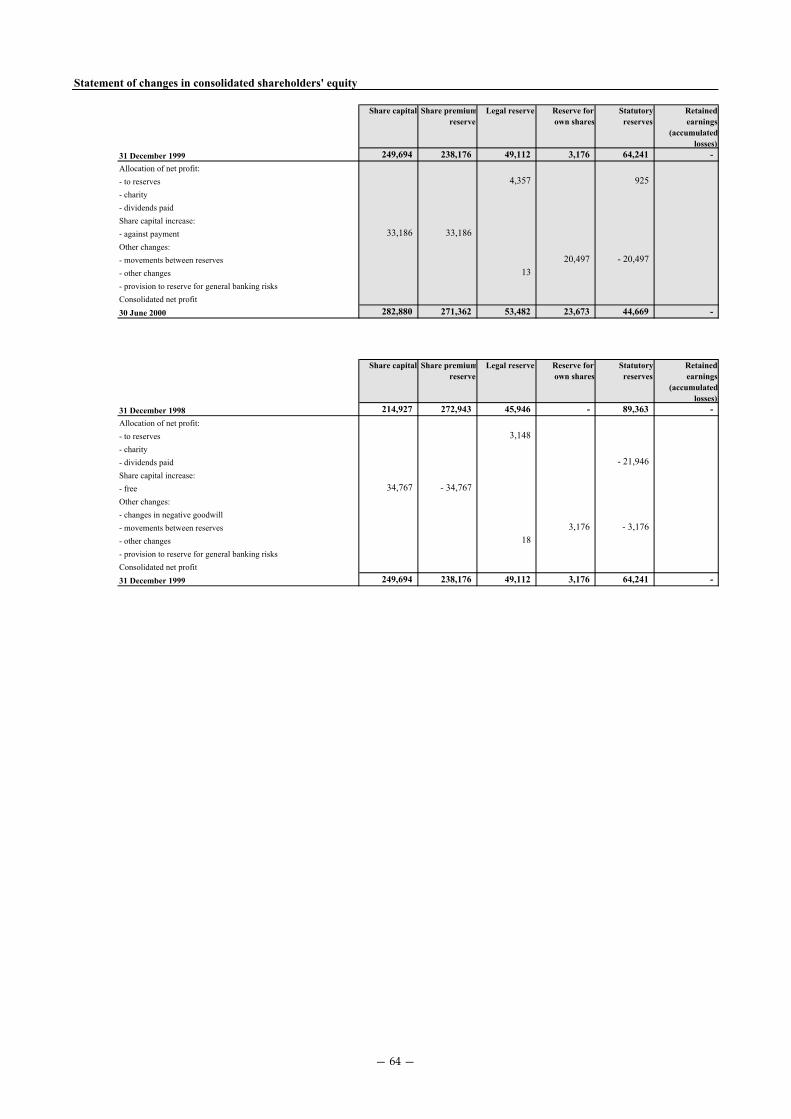

4.4 Shareholders' equityThe Group's shareholders' equity at the end of June 2000 totalled ITL 804 billion, as againstITL 752 billion at the end of 1999.The increase — ITL 52 billion — is due to the effect of the following transactions:� the share capital increase linked to the exercise of warrants for the “Credito Valtellinese

2% 1999-2004 ” bond issue, equating in total to ITL +66 billion, of which ITL 33 billionin principal and ITL 33 billion in issue premiums;

� the distribution of dividends and profits amounting to ITL – 30 billion;� the provision to the reserve for general banking risks amounting to ITL + 3 billion;� consolidated results for the period totalling ITL +13 billion.

4 The balance refers to the ratio between total writedowns on non-performing positions (gross exposure).

Credito Valtellinese Banking Group

— 24 —

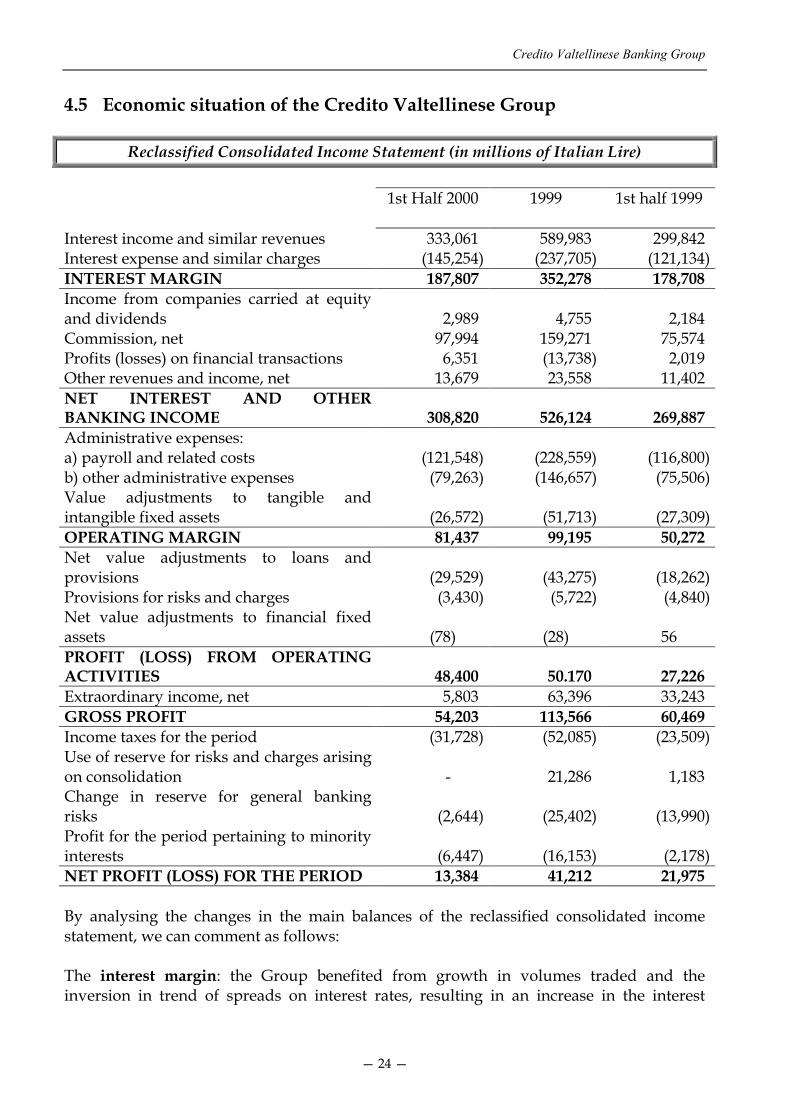

4.5 Economic situation of the Credito Valtellinese Group

Reclassified Consolidated Income Statement (in millions of Italian Lire)

1st Half 2000 1999 1st half 1999

Interest income and similar revenues 333,061 589,983 299,842Interest expense and similar charges (145,254) (237,705) (121,134)INTEREST MARGIN 187,807 352,278 178,708Income from companies carried at equityand dividends 2,989 4,755 2,184Commission, net 97,994 159,271 75,574Profits (losses) on financial transactions 6,351 (13,738) 2,019Other revenues and income, net 13,679 23,558 11,402NET INTEREST AND OTHERBANKING INCOME 308,820 526,124 269,887Administrative expenses:a) payroll and related costs (121,548) (228,559) (116,800)b) other administrative expenses (79,263) (146,657) (75,506)Value adjustments to tangible andintangible fixed assets (26,572) (51,713) (27,309)OPERATING MARGIN 81,437 99,195 50,272Net value adjustments to loans andprovisions (29,529) (43,275) (18,262)Provisions for risks and charges (3,430) (5,722) (4,840)Net value adjustments to financial fixedassets (78) (28) 56PROFIT (LOSS) FROM OPERATINGACTIVITIES 48,400 50.170 27,226Extraordinary income, net 5,803 63,396 33,243GROSS PROFIT 54,203 113,566 60,469Income taxes for the period (31,728) (52,085) (23,509)Use of reserve for risks and charges arisingon consolidation - 21,286 1,183Change in reserve for general bankingrisks (2,644) (25,402) (13,990)Profit for the period pertaining to minorityinterests (6,447) (16,153) (2,178)NET PROFIT (LOSS) FOR THE PERIOD 13,384 41,212 21,975

By analysing the changes in the main balances of the reclassified consolidated incomestatement, we can comment as follows:

The interest margin: the Group benefited from growth in volumes traded and theinversion in trend of spreads on interest rates, resulting in an increase in the interest

Report on operations for the first half of 2000

— 25 —

margin of 5.1% (ITL 187.8 billion at the end of June 2000), when compared with the sameperiod in the previous year.

Net interest and other banking income totalled ITL 308.8 billion, compared with ITL269.9 billion as of 30 June 1999, up 14.4%.The contribution from the item concerning net commission is increasingly significant invalue, and in the first six months of 2000 came to nearly ITL 98 billion, an increase of29.7%. Trading activities made it possible to achieve profits from financial transactions ofITL 6.4 billion (ITL 2 billion in the first half of 1999).Auditing activities carried out by the Group enabled the rise in operating costs to be cut to3.5%, despite the presence of important investment initiatives underway in areas of greatgrowth potential. In detail: payroll and related costs amounted to ITL 121.5 billion,compared with ITL 116.8 billion in the first half of 1999, up 4.1%; other administrativeexpenses also disclosed modest growth (ITL 79.3 billion compared with ITL 75.5 billion, anincrease of 5%). Value adjustments on tangible and intangible fixed assets fell by 2.7%,from ITL 27.3 billion to ITL 26.6 billion over the two interim periods.

As a consequence of the above-mentioned performances, the operating margin came toITL 81.4 billion, up by 62% compared to the same period in the prior year when the figurewas ITL 50.3 billion.Adjustments and provisions provided in the period were carried out as specified below,in accordance with the prudent accounting policies:- ITL 29.5 billion for net value adjustments to loans and provisions;- ITL 3.4 billion for provision for risks and charges;- ITL 78 million for net value adjustments to financial fixed assets.

It is necessary to emphasis that — as can be seen from the attached reclassified incomestatement — the Group closed the period with profit from operating activities of ITL 48.4billion, an improvement of 77.8% compared with the same balance in the first half of lastyear which came to ITL 27.2 billion.

Taking into account net extraordinary income of ITL 5.8 billion, income taxes for theperiod totalling ITL 31.7 billion, the change in the reserve for general banking risks of ITL2.6 billion and net profit for the period pertaining to minority interests amounting to ITL6.4 billion, operations for the first six months presented net profit of ITL 13.4 billion,compared with the result in the first half of 1999, which totalled ITL 22 billion. It shouldalso be mentioned that the net profit for the first half of 1999, was significantly influencedby around ITL 28 billion in net advanced taxes recorded among extraordinary income.

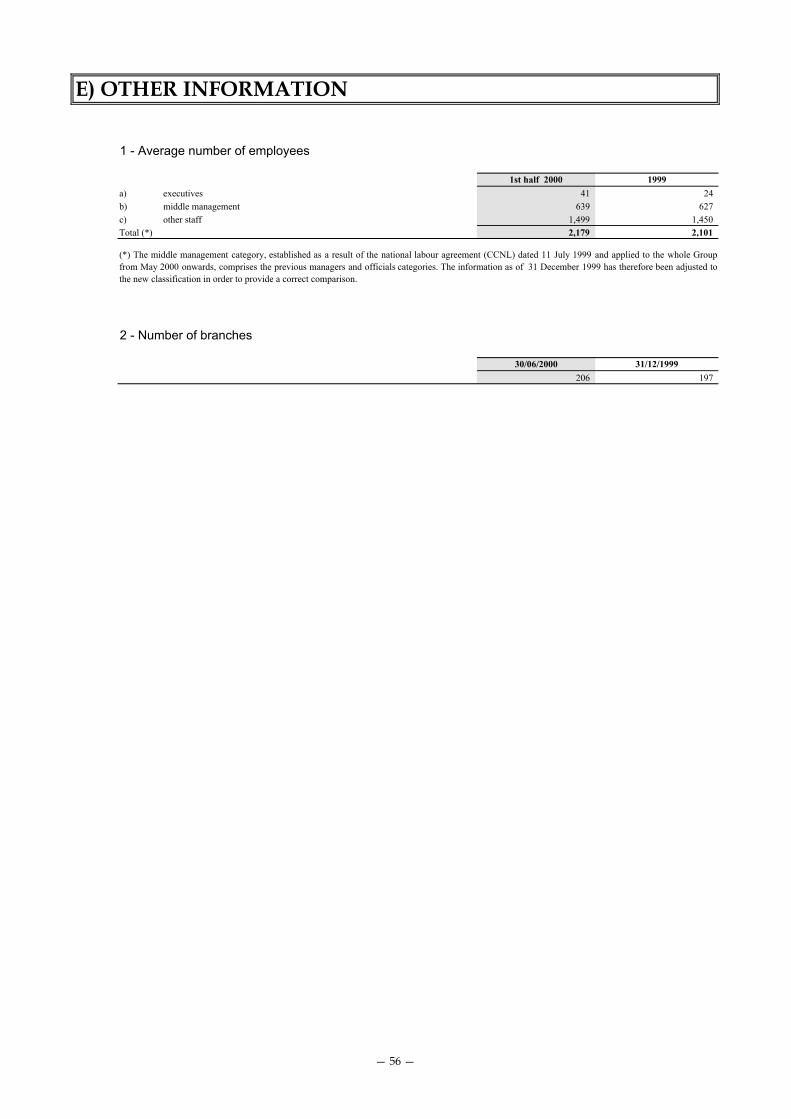

4.6 Development of the Group's operating structureAs part of the continuation of the projects for the gradual extension of the territorialnetwork originally planned, during the first half of the year 8 new branches were opened,in addition to the headquarters in Brescia of the newly acquired Banca dell’Artigianato edell’Industria.The territorial network of the Group as of 30 June 2000, therefore comprised 206 branches.

Credito Valtellinese Banking Group

— 26 —

To support the traditional branches, the development of alternative channels continued: atthe end of June 2000, the Group availed of 241 automatic banking outlets, 4,634 Points ofSale, 3,638 remote banking points, 34,200 Internet contracts and 12,782 Phone Bankingcontracts.

The growth in the workforce — again linked to the effective corporate needs, present andexpected — has made it possible to maintain the degree of efficiency at satisfactory levels.The Group's workforce as of 30 June numbered 2,179 employees, an increase of 4.5%compared to the same period last year.Intense activities concerning the professional up-dating and training of the workforcecontinued throughout the period, involving 3,946 training days and 1,339 employees(61.4%) from all grades.

4.7 Outlook for operationsThe positive trend in volumes traded together with the improvement in spreads and thefavourable performance of income from services, provides the basis for a further increasein profitability during the second half of the year.As far as the future growth of the activities of the Credito Valtellinese Group areconcerned, the objectives for economies of scale and scope persist, constituting thereasoning behind our company-network model.Therefore, realisation of the activities linked to the functional and instrumental integrationof all the Group companies will continue, as anticipated by the strategic plan: thecompletion of said activities, which are currently underway, will gradually permit thevarious companies to benefit from the desired increases in efficiency and competitiveness.

Significant events which occurred after 30 June 2000 include the start-up of theprocedures required for the purchase by the Parent Bank Credito Valtellinese of a furthershareholding in Banca Popolare di Rho.

5. Information on the performance and activities of GroupCompanies

In order to provide more comprehensive information, we have briefly commented on theperformance and the economic results achieved by each of the Group companies.

Credito Valtellinese

The Parent Bank, Credito Valtellinese, saw a further improvement in its balance sheet andincome statement results.As far as administered assets were concerned, direct deposits amounted to over ITL 4,242billion (+ 10.4% compared with June 1999), while the indirect component disclosed amuch more significant increase of 19.5%, totalling ITL 6,697 billion.

Report on operations for the first half of 2000

— 27 —

More specifically, due to the progressive diffusion of managed investments throughout allcustomer segments, Asset Management activities rose by 5.5%, while direct investments inmutual funds rose by 87.3%.Total customer deposits therefore amounted to over ITL 10,939 billion, an increase of15.8%.Thanks to the favourable performance of demand for loans deriving from the territorialarea in which the Bank operates and in witness of the support given to companies, privateindividuals and households, loans to customers totalled ITL 3,091 billion, disclosing asignificant increase of 13.9% when compared with the first half of 1999.The ratio of non-performing loans to total lending fell from 2.36% to 2.23%.

An analysis of the income statement results discloses that the interest margin, in thepresence of substantial growth in volumes traded, came to ITL 68 billion, up 3.4% on thefirst six months of 1999.The favourable performance of income from services (+ 63.2%, including leasing charges)was not however matched by a similar positive trend in results from financial transactions.As a result of the above performances, net interest and other banking income — whichsums up the total of revenues from operating activities — amounted to ITL 164.2 billion(ITL 126.4 billion in the first half of 1999, up by around 29.9%).Operating costs totalled ITL 112.2 billion (+ 29.9%) during the period under review. Infact, the substantial stability of payroll and related costs (+ 2.5%) contrasts withconsiderable increase in other administrative expenses and amortisation and depreciationfollowing the disposal by Bancaperta of its leasing business (carried out as of 1° July 1999);as a result of this transaction the two figures are not comparable.The operating margin therefore came to ITL 51.8 billion (ITL 40 billion in the periodJanuary-June 1999), disclosing an increase of 29.7%.Net of the remaining adjustments and provisions, income from operating activities —which comprises the excellent results achieved by all the elements of core bankingactivities— amounted to ITL 37.3 billion, an increase of 23.7% with respect to the sameperiod in the previous year.The balance of extraordinary activities (ITL 5 billion) and income taxes for the first sixmonths amounting to ITL 18.6 billion resulted in net profit for the period of ITL 23.7billion, up by 15.7% compared with the first six months of 1999.As a result of the opening of four new branches — Bulgarograsso (Como), Albavilla(Como), Galbiate (Lecco) and Cocquio Trevisago (Varese) — the territorial network of theParent Bank as of 30 June 2000 numbered 72 agencies.

Credito Valtellinese Banking Group

— 28 —

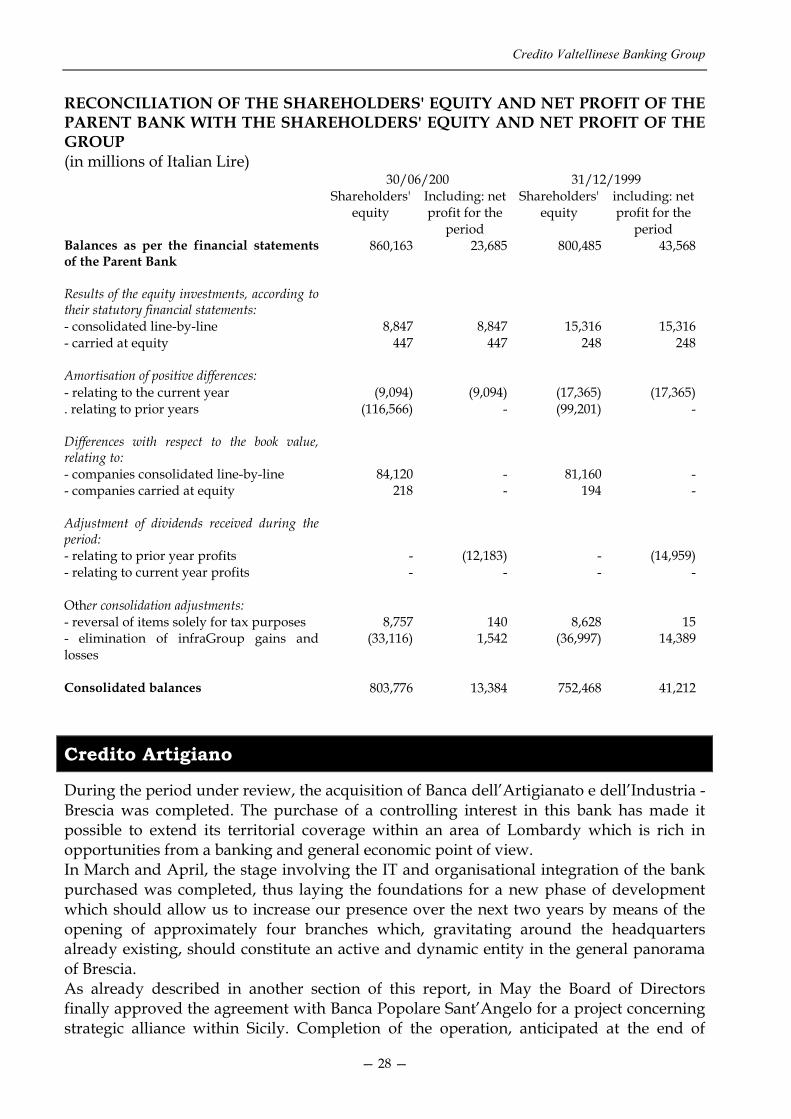

RECONCILIATION OF THE SHAREHOLDERS' EQUITY AND NET PROFIT OF THEPARENT BANK WITH THE SHAREHOLDERS' EQUITY AND NET PROFIT OF THEGROUP(in millions of Italian Lire)

30/06/200 31/12/1999Shareholders'

equityIncluding: netprofit for the

period

Shareholders'equity

including: netprofit for the

periodBalances as per the financial statementsof the Parent Bank

860,163 23,685 800,485 43,568

Results of the equity investments, according totheir statutory financial statements:- consolidated line-by-line 8,847 8,847 15,316 15,316- carried at equity 447 447 248 248

Amortisation of positive differences:- relating to the current year (9,094) (9,094) (17,365) (17,365). relating to prior years (116,566) - (99,201) -

Differences with respect to the book value,relating to:- companies consolidated line-by-line 84,120 - 81,160 -- companies carried at equity 218 - 194 -

Adjustment of dividends received during theperiod:- relating to prior year profits - (12,183) - (14,959)- relating to current year profits - - - -

Other consolidation adjustments:- reversal of items solely for tax purposes 8,757 140 8,628 15- elimination of infraGroup gains andlosses

(33,116) 1,542 (36,997) 14,389

Consolidated balances 803,776 13,384 752,468 41,212

Credito Artigiano

During the period under review, the acquisition of Banca dell’Artigianato e dell’Industria -Brescia was completed. The purchase of a controlling interest in this bank has made itpossible to extend its territorial coverage within an area of Lombardy which is rich inopportunities from a banking and general economic point of view.In March and April, the stage involving the IT and organisational integration of the bankpurchased was completed, thus laying the foundations for a new phase of developmentwhich should allow us to increase our presence over the next two years by means of theopening of approximately four branches which, gravitating around the headquartersalready existing, should constitute an active and dynamic entity in the general panoramaof Brescia.As already described in another section of this report, in May the Board of Directorsfinally approved the agreement with Banca Popolare Sant’Angelo for a project concerningstrategic alliance within Sicily. Completion of the operation, anticipated at the end of

Report on operations for the first half of 2000

— 29 —

series of transfers and corporate and administrative fulfilments, is by way ofapproximation fixed for February 2001.

The excellent equity and income performance reported in the past by Credito Artigianohas once again been confirmed. On a comparative basis with 1999 in fact, direct deposits— comprising Amounts due to customers, Securities issued and Subordinated liabilities —rose by 16.8% to ITL 4,149 billion.Indirect deposits also showed favourable growth (+ 12%) amounting to ITL 6,514 billion,bringing total deposits to over ITL 10,663 billion. As part of this aggregate, managedsavings increased on an annualised basis by 12.6%, reaching ITL 2,503 billion.Lending (up 29.1% compared with the end of the first half of 1999) totalled ITL 3,029billion and bore witness to the intense efforts made in supporting the local economy.The prudent management of lending activities was confirmed by the extent of net non-performing loans which fell from 2.36% to 1.97% as a percentage of total lending.

As far as the income statement was concerned, the interest margin — represented by thebalance of interest income totalling ITL 139.3 billion and interest expense amounting toITL 71.8 billion — came to ITL 67.5 billion compared with ITL 62.1 billion in June 1999 (up8.8%).Commission and income received on services provided to customers continued to show afavourable trend (+ 17.8%); as a result of these performances, net interest and otherbanking income came to ITL 121.8 billion, disclosing an improvement of 16.7%.Overheads in their entirety showed a modest increase of ITL 3.5 billion (+ 4%); in detail,payroll and related costs remained more or less unchanged (- 0.1%), other administrativeexpenses rose by 11.4%, while adjustments to tangible and intangible fixed assets fell by9.8%.The operating margin, thanks to a growth trend in revenues which was significantlybetter than that concerning costs, amounted therefore to ITL 32.3 billion, or rather 76.8%up on the result reported in the first half of 1999. As we have already mentioned, thisresult is the outcome, on the one hand, of the improvement in income from services —demonstrating the efficiency of the bank with regard to the development of commercialactivities— and, on the other hand, the positive contribution from profits on financialtransactions.Net profit for the period, after having provided for current income taxes, rose by 20% andcame to ITL 10.8 billionAs a result of the opening of the branches in Besana Brianza (Milan), Cinisello Balsamo(Milan), Rescaldina (Milan), as well as Agency No. 3 in Florence, the number of the bank'soutlets rose to 66.

Banca Popolare Santa Venera

Total deposits from customers — up by 16.4% compared with the first half of 1999 —amounted to over ITL 2,326 billion, drawn along by the increase in direct deposits of16.3%, amounting to ITL 1,411 billion. Indirect deposits came to over ITL 915 billion, up16.4% on June 1999.

Credito Valtellinese Banking Group

— 30 —

The increase in lending amounted to ITL 867 billion (+ 11.7%) at the end of the period andbears witness to the ability of the bank to support the economic activity of the region. Theimprovement in the quality of lines of credit granted is confirmed by the fact that the ratioof non-performing loans to total loans has dropped to 9.3%.

During the first half of the year, the bank reported an interest margin of around ITL 29.8billion; income from services (ITL 18.8 billion or + 24.4% compared with the first half oflast year) further increased its incidence in terms of percentage on net interest and otherbanking income, from 36.6% to 38.3%. The latter result confirms the efforts made by thebank along the strategic route to diversifying revenues.With the contribution from financial operations, net interest and other banking incomecame to ITL 49.1 billion, an improvement of 18.7% compared with the same period in 1999.Total operating costs — ITL 40.7 billion — showed contained growth (+ 4.1%) whichreduced the incidence in terms of percentage on net interest and other banking incomefrom 94.71% to 83.04%. Within this aggregate, payroll and related costs (ITL 20.8 billion),other administrative expenses (ITL 18 billion) and adjustments to tangible and intangiblefixed assets (ITL 2 billion) showed contained growth.The operating margin came to ITL 8.3 billion, up by around 281%.Net adjustments to loans, provisions for risks and charges and the provision to the reservefor possible loan losses, amounted overall to ITL 4.2 billion, down 11.5% compared withthe first six months of 1999. The minor necessity for adjustments meant that profit fromoperating activities totalled ITL 4.3 billion.As a result of the decreased contribution of extraordinary items and an increase in theincome tax liability for the period, net profit for the period amounted to approximatelyITL 2 billion, up by 45.8% compared with the first half of 1999.At the end of June, the Banca Popolare Santa Venera network comprised 50 branches with401 employees

Bancaperta

Bancaperta is now a virtual bank which presents itself as a financial broker at the serviceof the private customer by means of the integrated use of several distribution channels(phone banking, Internet Banking, web-tv). It also represents the individual stronghold ofthe Group for matters concerning the handling of home and corporate bankingapplications, electronic payment systems and the management of all the insurance and"bank insurance" matters.In this bank all the financial activities of the Credito Valtellinese Group have beenconcentrated, with particular reference to centralised treasury services, asset management,portfolio management (positions managed as of 30 June 2000: 41,659 for 24,591 customersequating to a total of Euro 2,635 million) and private banking.On a consistent basis with the new strategic mission assigned to Bancaperta, in July 1999steps were taken to dispose of its leasing business to the Parent Bank Credito Valtellinese:in this way, the bank ceased to undertake lending risks relating to leasing activities andnow concentrates on its new mission and its new strategic objectives.

Report on operations for the first half of 2000

— 31 —

The main balance sheet aggregates disclose direct deposits totalling ITL 484 billion andindirect deposits amounting to ITL 5,196 billion, with a particularly marked growth trendfor managed deposits.The interim result also takes into account the disposal of the leasing business to the ParentBank, with the consequent reduction in income and costs from one interim period toanother.The income statement discloses a negative interest margin of ITL 6.6 billion, which is animprovement on the corresponding results a year earlier which came to ITL –9.0 billion.Net commission rose during the period to ITL 11.2 billion (up 9.7%); likewise, profits onfinancial transactions registered an increase when compared to the first half of theprevious year.As a result of the decrease in the contribution from other net income — such as leasingcharges following the afore-mentioned disposal of the leasing business — net interest andother banking income fell (- 20.6%) with respect to the result reported in thecorresponding period last year.Operating costs fell by 22.6%, this decrease was linked to the lesser need to chargeamortisation due to the afore-mentioned disposal of the leasing business. As a result of theabove balances, the operating margin stood at around ITL 6 billion, up by 36.9%compared with the ITL 4.4 billion reported in the previous year.The first half of 2000 therefore closed with net profit of ITL 3.2 billion, an increase of 58.3%compared with the first half of 1999.

Banca Popolare di RhoAs far as the main balance sheet aggregates as of 30 June 1999 were concerned, directdeposits from customers amounted to ITL 81.2 billion, an increase of 33.6% comparedwith the same figure in 1999, while indirect deposits were also up and amounted to ITL79.5 billion (+ 29.8%).Loans to customers disclosed steady progress: at the end of June, the balance amounted toITL 75.3 billion (up 22.3%).

The economic results achieved during the period ended June 2000, saw the interestmargin, ITL 2.6 billion, benefit from growth of 19.8%.Income from services rose by 39.8%, and totalled ITL 1.1 billion. As a result of the above,net interest and other banking income amounted to ITL 3.7 billion, up 23.8%.The operating margin, calculated taking into account operating costs andamortisation/depreciation, amounted to ITL 224 million, as against ITL 19 million in thefirst half of 1999.Deducting net adjustments on loans and provisions totalling ITL 775 million,extraordinary losses and income taxes for a total of ITL 41 million, the interim periodclosed with a net loss of ITL 592 million.

Credito Valtellinese Banking Group

— 32 —

Cassa San Giacomo

The overall total of direct deposits from customers came to ITL 320 billion, down 2.7%compared with ITL 329 billion at the end of June 1999.Indirect deposits amounted to ITL 122 billion, up 11.8% compared to the ITL 109 billionreported in the same period last year. Of this total, the increase in managed savings, whichrepresents approximately 33.5% of the entire aggregate, came to 21%. Total deposits at theend of June 2000 amounted to ITL 442 billion, as against ITL 438 billion at the end of June1999.Loans to customers totalled ITL 146 billion during the period under review (- 13.1%compared with the end of June 1999). The net total of non-performing loans came to ITL21.5 billion, compared with ITL 22.6 billion in the same period last year.

The interest margin for the first half of 2000, totalled ITL 7.1 billion, up by 1.4% on acomparative basis with the prior year.Net commission (up 22.6%) and other net income increased (+ 108.8%); profits on financialtransactions fell (ITL -332 million versus ITL +1,701 million in the previous year), in partas a result of the application of the accounting policy "mark to market" on portfoliosecurities.Net interest and other banking income therefore amounted to ITL 9.8 billion, comparedwith ITL 10.8 billion in the first half of 1999.Total operating costs came to ITL 9.4 billion, and comprised ITL 4.7 billion in payroll andrelated costs, ITL 4.1 billion in other administrative expenses and ITL 0.7 billion in valueadjustments on tangible and intangible fixed assets.The operating margin, deriving from the difference between net interest and otherbanking income and total operating costs, amounted to ITL 0.4 billion as of 30 June 2000(ITL 1.6 billion in the first six months of 1999).The income statement of the bank as of 30 June 2000, disclosed a negative result, mainlyattributable to the value adjustments made on loans and the extraordinary result; thecontribution of the afore-mentioned items produced a net loss for the period of around ITL581 million.At the end of June, the workforce of Cassa San Giacomo numbered 100 employees.

Banca dell’Artigianato e dell’Industria

The new subsidiary officially entered the Group at the end of January 2000, after thesuccessful conclusion of the public purchase offer launched by Credito Artigiano. Thisbank operates with a main branch in Brescia and as of 30 June 2000 availed of directdeposits totalling ITL 59 billion and indirect deposits amounting to ITL 86 billion; itgranted loans to customers for around ITL 76 billion.

With regard to its income statement results, the interest margin has nearly doubled withrespect to the corresponding period in the prior year (up 96.1%) and amounts to ITL 2.4billion.

Report on operations for the first half of 2000

— 33 —

Net income from revenues and services showed positive performance and took netinterest and other banking income to around ITL 3 billion, up 94.4% on an annual basis.Operating costs, ITL 2.4 billion, disclosed an increase of approximately 29%, resulting inan operating margin of ITL 556 million (+ 258.4%).Profit from operating activities is determined (ITL 127 million) after having madeappropriate provisions for adjusting total loans for ITL 429 million (up 18.8%); at the endof the first half of 2000, the bank disclosed positive results closing with a net profit of ITL8 million.

The organisational model of the Credito Valtellinese Group anticipates, alongside theregional banks, the existence of independent units specialised with regards to role andfunction, which are capable of providing services — with a view to economies of scale andoperating synergies — to all the Group companies.The supply transactions for goods and services, provided by the three complementarycompanies have involved: training and managerial consultancy, the management andmaintenance of property and general security services, and the management of theGroup's Information System. The following companies belong to these specialised units:Deltas, Stelline Servizi Immobiliari and Bankadati S.I.

Deltas

The activities of this company in the first half of 2000, were directed at supporting theinitiatives linked to the managerial support and control of the strategic approach of thevarious Group companies.The economic results for the period produced net profit of ITL 82 million, more or less inline with the forecasts made.

Stelline Servizi Immobiliari

Stelline Servizi Immobiliari handles the management of the extensive property belongingto the Group. During the period, the company continued to provide services to Groupbanks: more specifically, carrying out studies and research in the property and urbanplanning sector, the development of architectural, technical systems and design projects,the construction of bank branches, management of the maintenance of properties,alongside technical support activities for loan disbursement and property-related technicalassistance targeted at the recovery of loans.The company has balance sheet assets of ITL 53.7 billion and equity of ITL 5.8 billion. Theeconomic result for the period disclosed net profit of ITL 86 million.

Credito Valtellinese Banking Group

— 34 —

Bankadati Sistemi Informativi

The provision of IT services to Group banks, already linked up at the end of the prior year,continued without interruption.As from April 2000, the newly acquired Banca dell’Artigianato e dell’Industria was also setup so that it could use the Group's information system. By contrast, migration is currentlybe completed on the single information system which acts a reference point for all thebranches of Banca Popolare Santa Venera and Cassa San Giacomo.At the time of migration to the Group's information system, which essentially concernedBanca dell’Artigianato e dell’Industria - Brescia and the measures still being carried out onthe branch network of the Sicilian banks, active joint efforts were made in order to limitthe impact both on customers and on the personnel involved.Bankadati closed the period with net profit of approximately ITL 381 million.

TRANSACTIONS WITH SUBSIDIARY COMPANIES (ALSO JOINTLY WITH THIRDPARTIES) OR THOSE SUBJECT TO INDIVIDUAL MANAGEMENT NOT INCLUDED

WITHIN THE SCOPE OF CONSOLIDATION, AS WELL AS ASSOCIATED ANDPARENT COMPANIES AND COMPANIES CONTROLLED BY THE LATTER

Amounts due to and from associated companies (1)(balances in millions of Italian Lire)

Assets TotalLoans to customers 11,384Intangible fixed assets 287Tangible fixed assets 2Other assets 55Accrued income and prepayments 157LiabilitiesDue to customers 16,793Other liabilities 65Guarantees and commitmentsGuarantees given 12,600Economic transactions between associated companies (1)(balances in millions of Italian Lire)Revenues TotalInterest income and similar revenues 310Interest expense and similar charges 39Commission income 4Other operating income 64CostsAdministrative expenses 872Other operating expenses 361(1) Transactions with subsidiary companies or those subject to individual management not included in thescope of consolidation, and those with Parent Companies and companies controlled by the latter.

Report on operations for the first half of 2000

— 35 —

Form and content of the consolidated interim report

Form and content of the consolidated interim reportThe consolidated interim report for the period ended 30 June 2000 has been prepared inaccordance with the provisions of the Regulations approved by the Consob underResolution No. 11971 dated 14 May 1999 and subsequent amendments.The financial statements include Credito Valtellinese (Parent Bank) and the companiesoperating in the lending and financial sector, or those whose primary activity iscomplementary to that of the Parent Bank, and in which the latter directly or indirectlyholds a majority interest in the share capital or avails of sufficient votes to exercise adominant influence at ordinary shareholders' meetings.Among the accounting schedules included in this report, is a list of the companiesincluded within the scope of consolidation and equity investments carried at equity.

Consolidation principlesThe consolidation principles adopted are those laid down by Legislative Decree No.87/1992 as well as the accounting principles in force in Italy or, in the absence thereof,those issued by the International Accounting Standards Committee (I.A.S.C.).The book value of investments in subsidiary companies, whose financial statements areconsolidated line-by-line, is eliminated against the related share of the shareholders'equity. The elimination is carried out with reference to the values in effect at the time theinvestments were acquired.Any differences arising from such elimination,:� if positive (purchase cost of the investment greater than the related share of its equity),

are allocated to the consolidated balance sheet assets under the item “Goodwill arisingon consolidation”;

� if negative (purchase cost of the investment less than the related share of its equity), arerecorded among the consolidated liabilities under the item “Negative goodwill arisingon consolidation”.

Minority shareholders are allocated the portion of shareholders' equity and net resultspertaining to them.Equity investments in associated companies, i.e. those where the interest held is between20% and 50%, are carried at equity.For these companies:� the additional book value with respect to the share of equity pertaining to the Group,

which arose at the time of acquisition, is recorded among the consolidated balancesheet assets under the item “Goodwill arising on application of the equity method”;

� the lower book value with respect to the share of equity pertaining to the Group, isrecorded among the consolidated liabilities under “ Negative goodwill arising onapplication of the equity method ”.

Any changes in shareholders' equity subsequent to the date taken as the basis forcalculating these differences are classified under the item “Income (loss) from investmentscarried at equity ”, if they refer to the income or loss of these investments.

Credito Valtellinese Banking Group

— 36 —

Goodwill arising on consolidation and application of the equity method is attributable tothe payment of goodwill and amortised over a period of 10 years, deemed in keeping withthe duration of the investment.Dividends recorded in the financial statements of the Parent Company concerning equityinvestments in companies included within the scope of consolidation or those carried atequity, are eliminated. The related tax credit is offset against taxation for the period.The effects of intraGroup transactions between companies included in the scope ofconsolidation are eliminated. Taxation relating to adjustments made at the time ofconsolidation are also taken into consideration, if they meet the necessary criteria.Investments in which the interest held is less than 20% are carried at cost.Investments which are considered insignificant for the purpose of providing a true andfair view of the financial and equity situation of the Group and its consolidated results forthe period, are also carried at cost.

Currency used for the preparation of the financial statementsThe balances shown in the schedules included in the consolidated interim report areexpressed in millions of Italian Lire. A balance sheet and income statement drawn up inthousands of Euro have also been included within this report.

Financial statements adoptedThe consolidated interim financial statements have been prepared on the basis of financialstatements prepared as of and referring to the period ended 30 June 2000.

Reasons for the differences with respect to forecasts made at the time of the quarterlyreport.Differences in the balances of the balance sheet items presented in the interim report as of30 June 2000, when compared to the estimates made at the time of drawing up thequarterly financial statements referring to the same date, are limited both in absolute andpercentage terms. They were determined by the re-allocation of items in transit and non-liquid portfolios to the pertinent balance sheet accounts, as anticipated in the explanatorynotes accompanying the quarterly financial statements.

Report on operations for the first half of 2000

— 37 —

B. Accounting policies

Section 1 - Description of the accounting policies

The accounting policies adopted for the preparation of the consolidated interim financialstatements are consistent with those used by the Parent Bank and the other companies inthe Group.The accounting principles and policies adopted are consistent with those used for theannual financial statements as of 31 December 1999 and the interim statements as of 30June 1999.

1. Loans, guarantees and commitments

Amounts due from banksAmounts due from banks are stated at their estimated realisable value, taking any forecastlosses into account.

Loans to customersThe book value of loans, including total contractual and overdue interest accrued,coincides with their estimated realisable value. The latter value is calculated as total loansoutstanding less expected losses of principal and interest, defined on the basis of a specificanalysis of all non-performing and problem loans as well as the inherent risk of loss,which could emerge in the future on other loans.The original value of the loans is reinstated in subsequent periods should the reasons forany adjustments (writedowns) cease to apply.Loans to customers also include those concerning leasing contracts held by the ParentBank and by the subsidiary Bancaperta S.p.A., determining using financial leaseaccounting methods in accordance with the procedures anticipated by the Bank of ItalyCircular No. 166 dated 30 July 1992 and subsequent amendments. These amounts arevalued taking into account the recovery value of the assets leased as well as the relateddepreciation. Said depreciation was calculated as follows:� with reference to assets under financial lease up to 31 December 1994: by calculating

depreciation with reference to the duration of the contract quota and commensuratewith the cost of the assets less the redemption price; from 1992, the depreciable value ofleased assets was increased as a result of revaluations under Law 413/91;

� with reference to assets under financial lease as from 1 January 1995: depreciation wasbased on the financial repayment plan.

Other amounts dueSince no losses are anticipated for other amounts due, they are stated at nominal valuewhich coincides with their estimated realisable value.

Credito Valtellinese Banking Group

— 38 —

Guarantees and commitmentsGuarantees given are recorded at the total value of the commitments undertaken. Risksassociated with guarantees given are covered by a specific provision to the reserve forrisks and charges.Securities to be received are stated at the forward price contractually established with thecounterpart.

2. Securities and off-balance sheet transactions (excluding foreign currencytransactions)

2.1 Investment securitiesInvestment securities are valued at their original purchase cost, and are written down toreflect any permanent losses in value.

2.2 Dealing securitiesDealing securities listed on organised markets are stated at their market value.Therefore securities not held as financial fixed assets are valued as follows:� securities listed on organised markets are valued at market understood as the average

of prices struck during the last month of the period;� unlisted securities are valued at the lower of formation cost (determined on a LIFO

basis) and their market value; the latter is considered to be equal to their estimatedrealisable value, calculated on the basis of the market prices of securities with similarcharacteristics listed on organised markets and the value obtained by discountingfuture financial flows generated by interest and principal using the appropriate marketrate of interest. The solvency status of the issuer is also taken into account.

Writedowns made in prior accounting periods are eliminated, should the reasons for theirapplication cease to apply.