credit rating of firms

DESCRIPTION

its an iportant aspect of marketsTRANSCRIPT

e

A PROJECT REPORT ON

CREDIT RATING

SUBMITTED BY:-

AASTHA. V. JAGAD

T.Y.B.M.S. [SEMESTER V]

MITHIBAI COLLEGE OF MANAGEMENT

VILE PARLE (W), MUMBAI - 400 056

SUBMITTED TO

UNIVERSITY OF MUMBAI

ACADEMIC YEAR

2012-2013

PROJECT GUIDE

MR. NAVEEN ROHATGI

DATE OF SUBMISSION

25TH JULY, 2012

ACKNOWLEDGMENT

At the outset I would like to take the privilege to convey my gratitude to all those who co-operated, supported, helped and suggested me as to how the project could be completed. This project bears imprint of advices, from many people who were either directly or indirectly involved in it

The Internet has been a veritable treasure throve of information .The websites and the information they contained helped me to do the project in a much easier and better manner.

I am also desirous of placing on record profound indebtness to my guide Prof. Naveen Rohatgi for his valuable advices, guidance, precious time and support that he lent to me.

DECLARATION

I, Ms. AASTHA .V. JAGAD, of MITHIBAI COLLEGE OF MANAGEMENT

of TYBMS [Semester VI] hereby declare that I have completed my project, titled

‘CREDIT RATING’ in the Academic Year 2012-2013. The information

submitted herein is true and original to the best of my knowledge.

__________________________

Signature of Student

[Aastha.V.Jagad]

CERTIFICATE

I, MR. NAVEEN ROHATGI, hereby certify that Ms. AASTHA JAGAD of

Mithibai College of TYBMS [Semester VI] has completed her project, titled

‘CREDIT RATING’ in the academic year 2012-2013. The information submitted

herein is true and original to the best of my knowledge.

_______________________________ ______________________

Signature Of The Principal Signature Of The Project Guide

[Dr. Kiran V. Mangaonkar] [Mr. NAVEEN ROHATGI]

______________________

Signature of External Examiner

TABLE OF CONTENTS

INTRODUCTION....................................................................................................................................................................... 1

CREDIT RATING- MEANING............................................................................................................................................2

FEATURES.....................................................................................................................................................................................5

IMPETUS........................................................................................................................................................................................ 6

ORIGIN............................................................................................................................................................................................ 7

THE CREDIT RATING SYSTEM......................................................................................................................................9

CREDIT RATING AGENCY..............................................................................................................................................12

CREDIT RATING SYMBOLS...........................................................................................................................................17

CORPORATE CREDIT RATING....................................................................................................................................21

IPO GRADING/RATING..................................................................................................................................................... 23

SOVEREIGN CREDIT RATINGS...................................................................................................................................27

INDIVIDUAL CREDIT RATING IN INDIA..............................................................................................................30

USES OF RATINGS................................................................................................................................................................ 35

FUTURE OF CREDIT RATING IN INDIA................................................................................................................43

BENEFITS OF CREDIT RATING...................................................................................................................................43

NEED AND IMPORTANCE OF CREDIT RATING..............................................................................................46

PRACTICAL PROBLEMS WITH CREDIT RATING..........................................................................................49

REGUALTORY FRAMEWORK......................................................................................................................................51

SEBI GUIDELINES.................................................................................................................................................................53

REGISTRATION OF CREDIT RATING AGENCY..............................................................................................53

CODE OF CONDUCT............................................................................................................................................................58

COMPARISON OF REGULATIONS RELATED TO CREDIT RATING AGENCIES IN INDIA AND OTHER COUNTRIES................................................................................................................................................61

STANDARD & POOR'S........................................................................................................................................................64

CRISIL SME RATINGS:......................................................................................................................................................68

RECENT CREDIT RATING ARTICLES AND ACTIVITIES IN INDIA....................................................76

CONCLUSION...........................................................................................................................................................................79

BIBLIOGRAPHY..................................................................................................................................................................... 80

EXECUTIVE SUMMARY

A credit rating is an opinion from a credit rating agency about the creditworthiness of an issuer or

the credit quality of a particular debt instrument. Primarily, the rating opinion considers how likely

the issuer of the debt instrument is to meet its stated obligations, and whether investors will receive

the payments they were promised. A failure to meet such payments may be considered a default.

Credit rating agencies are placed as intermediate between investors and issuers of fixed income

securities. Their most important role is to minimize the existence of asymmetric information in the

marketplace. The role is central in operating the financial products has provided the credit rating

agencies with a tremendous power.

Despite the powerful position, is the credit rating industry subject to very weak regulation? The

credit rating agencies are by them self supposed to manage potential pitfalls in the rating process and

rating system. They are said to be self-controlled as no authority control how the agencies manage to

avoid potential pitfalls. The weak regulation and self-control provides the agencies with a high level

of freedom.

The mixture of power and freedom is a dangerous combination, if not managed well. The agencies

need to be fully aware of the responsibilities that naturally follow power and freedom. If they don’t

act as a responsible intermediate and perform trustworthy, the market will loose its faith to the

system.

CREDIT RATING

INTRODUCTION

The removal of strict regulatory framework in recent years has led to a spurt in the number of

companies borrowing directly from the capital markets. There have been several instances in the

recent past where the "fly-by-night operators have cheated unwary investors. In such a situation, it

has become increasingly difficult for an ordinary investor to distinguish between 'safe and good

investment opportunities' and 'unsafe and bad investments'. Investors find that a borrower's size or

names are no longer a sufficient guarantee of timely payment of interest and principal. Investors

perceive the need of an independent and credible agency, which judges impartially and in a

professional manner, the credit quality of different companies and assist investors in making their

investment decisions. Credit Rating Agencies, by providing a simple system of gradation of

corporate debt instruments, assist lenders to form an opinion on -the relative capacities of the

borrowers to meet their obligations. These Credit Rating Agencies, thus, assist and form an integral

part of a broader programme of financial disintermediation and broadening and deepening of the

debt market.

Credit rating is used' extensively for evaluating debt instruments. These include long-term

instruments, like bonds and debentures as well as short-term obligations, like Commercial Paper. In

addition, certificates of deposits, inter-corporate deposits, structured obligations including non-

convertible portion of partly Convertible Debentures (PCDs) and preferences shares are also rated.

The Securities and Exchange Board of India (SEBI), the regulator of Indian Capital Market, has now

decided to enforce mandatory rating of all debt instruments irrespective of their maturity.

1

CREDIT RATING- MEANING

A credit rating estimates the credit worthiness of an individual, corporation, or even a country. It

is an evaluation made by credit bureaus of a borrower's overall credit history. A credit rating is

also known as an evaluation of a potential borrower's ability to repay debt, prepared by a credit

bureau at the request of the lender. Credit ratings are calculated from financial history and current

assets and liabilities. Typically, a credit rating tells a lender or investor the probability of the

subject being able to pay back a loan.

Definition

According to the Moody’s, “A credit rating is an opinion on the future ability and legal obligation

of the issuer to make timely payments of principal and interest on a specific fixed income security.

The rating measures the probability that the issuer will default on the security over its life, which

depending on the instrument, may be a matter of days to 30 days or more. In addition, long term

ratings incorporate an assessment of the expected monetary loss, should a default occur.

According to Standard & Poor’s, “Credit rating help investors by providing an easily

recognizable, simple tool that couples a possibly unknown issuer with an informative and

meaningful symbol of credit quality”

A poor credit rating indicates a high risk of defaulting on a loan, and thus leads to high interest rates

or the refusal of a loan by the creditor.

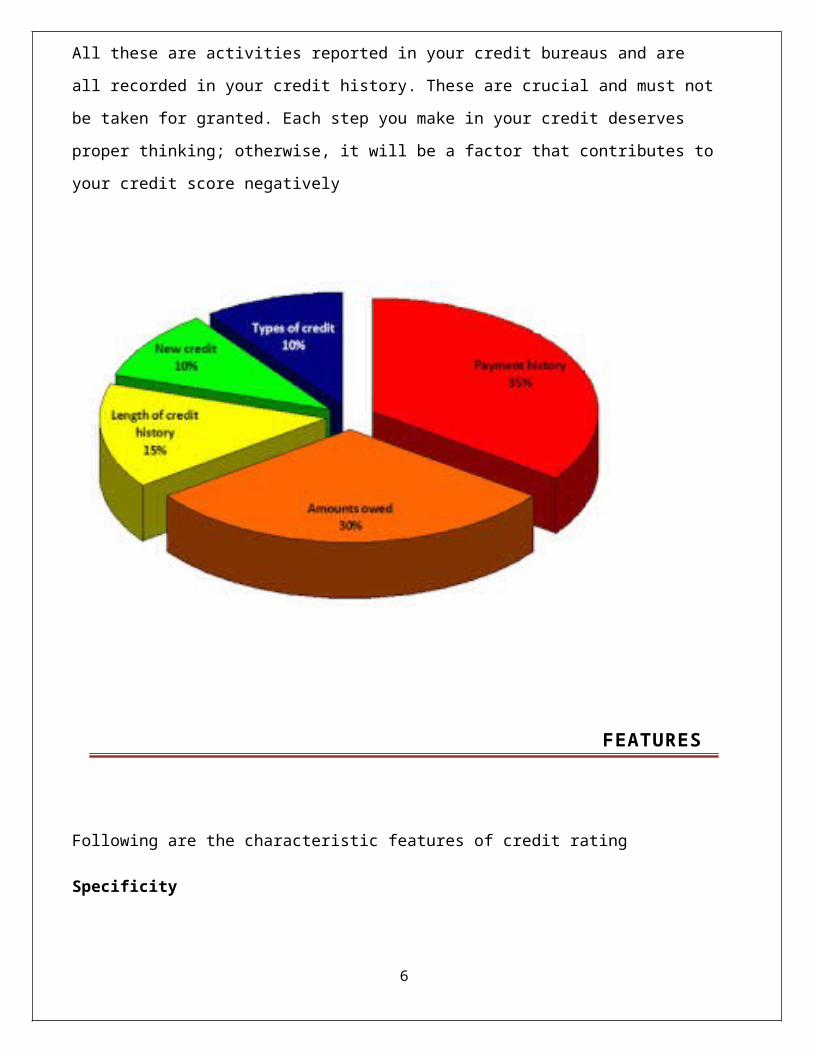

The following are few factors that contribute to an individuals credit score.

These are conditions that you have to avoid starting from getting your credit card application

approved.

1. When you make late payments, this affects 35% of your credit score negatively. Your creditor

informs your credit bureau and this affects your credit score. Make regular pays to avoid this.

It’s the only way to keep that 35%.

2. Worst of the factors that determine your credit score is when you don’t pay at all.

2

3. When you make a loan default. This is when you were not able to comply with the terms and

conditions.

4. When you have a longer credit history, it is better. 15% of your credit score is from the duration

of your credit history. You might not be so much in control of this factor that contributes to your

credit score because your history depends on the number of years you have been with a social

security number.

5. Another factor that determines credit score is that when you are charged off your account because

your creditors know that you really don’t want to pay, you will watch your credit score

backslide.

6. Lenders can send an account charged off to collection agencies. These agencies do the work of

getting you pay your bills. Yes, they could harass you just so you go with what your lenders

wanted and what you are supposed to do in the first place. Be careful with charge offs because

they are minor factors that contribute to your credit score yet they are significant.

7. Of the many factors that contribute to your credit score, when the court intervenes because you

cannot pay your bills, your credit history and score is affected negatively because you will be

considered bankrupt.

8. When you file for bankruptcy yourself, this becomes a factor that contributes to your credit

score. This is not the best last option to get out of debt. These three following, better, few solutions

are more favorable ways:

· Credit counseling

· Debt settlement

· Debt management program

9. Foreclosure of your home for not paying your mortgage is such a big deal among factors

contributing to credit score negatively.

3

10. Higher credit card balances will lead to credit card utilization. Remember that you should not

exceed your credit limits. Exceeded credit card limits is said to be a major factor contributing to

credit score negatively for over 90% of Americans with bad credit.

11. Connected to the previous factor contributing to bad credit is when you maxed out your credit

limit.

12. If you close your credit when it still contains balances, lenders will get the impression that the

limit is maxed out.

13. 10% of your credit score is from your credit inquiries or when you apply for multiple loans or

credit cards. In a short period of time, when you do credit card application several times, is not a

good thing for your score. It ruins it more.

All these are activities reported in your credit bureaus and are all recorded in your credit history.

These are crucial and must not be taken for granted. Each step you make in your credit deserves

proper thinking; otherwise, it will be a factor that contributes to your credit score negatively

4

FEATURES

Following are the characteristic features of credit rating

Specificity

The rating is specific to a debt instrument. It is intended as a grade and an analysis of the credit risk

associated with that particular instrument. Rating is neither a general purpose evaluation of the

issuer, nor an overall assessment of the credit risk to be involved in all the debts contracted by such

an entity.

Relativity

The rating is based on relative capability and willingness of the issuer of the instrument to service

debt obligations (both principal and interest), in accordance with the terms of the contract.

Guidance

The rating primarily aims at furnishing guidance to the investors/creditors in determining a credit

risk associated with a debt instrument/credit obligation.

Not a recommendation

The rating does not provide any sort of recommendation to buy, hold or sell an instrument, since it

does not take into consideration, factors such as market prices, personal risk preferences and other

considerations which may influence an investment decision.

Broad parameters

The rating process is based on certain broad parameters of information supplies by the issuer, and

also collected from various other sources, including personal interactions with various entities.

No guarantee

The rating furnished by the agency does not provide any guarantee for the completeness or accuracy

of the information on which the rating is based.

5

Qualitative and quantitative

While determining the rating grade, both quantitative as well as qualitative factors are employed.

The judgment is qualitative in nature, and the role of quantitative analysis is limited to assist in the

making of the best possible overall judgment

IMPETUS

The credit rating system originated in the United States in the seventies. The high levels of default,

which occurred after the Great Depression in the U.S Capital markets, gave the impetus for the

growth of credit rating. The default of $82 million of commercial paper by Penn Central in the year

1970, and the consequent panic of investors in commercial paper, resulted in massive defaults and

liquidity crisis. This prompted the capital issuers to get their commercial paper programs rated by

independent credit agencies. This according to them would give the required degree of comfort and

reassurance to their investors. Moreover, the real impetus for growth came when regulatory agencies

in the U.S made rating mandatory for institutions such as Government Pension Funds and Insurance

Companies, who could not buy securities rated below a particular grade. In addition, investors

themselves became aware of the rating mechanism, and started using ratings as extensively as a tool

for risk assessment. Merchant bankers, underwriters and other intermediaries involved in the debt

market also found the rating useful for planning and pricing the debt instruments.

Over the last two decades there have been many other factors that have contributed to the growth

and importance of the credit rating system in many parts of the world. They are:

The increasing role of capital and the money markets consequent to disintermediation.

Increased securitization of borrowing and lending consequent to disintermediation

Globalization of the credit market

The continuing growth of information technology

The growth of confidence in the efficiency of the market mechanism

The withdrawal of government safety nets and the trend towards privatization

6

ORIGIN

Credit rating has its origin in the financial crisis of the U.S. in 1837. Louis Tappan established the

first mercantile credit agency in New York in1841. The agency was used to assess the ability of

merchants to pay their financial obligations. Later on, it was acquired by Robert Dun, and its

first rating guide was published in 1859. In 1849, John Bradstreet set up similar agency, and it

published ratings book in 1857. In 1933, these two agencies were merged together to form Dun and

Bradstreet, which finally acquired the ‘Moody's Investors services’ in 1962.it is interesting to note

that Moody’s have a long history in the rating business, spanning over a period of more than a

hundred years.. In1900, John Moody laid stone of Moody’s Investors Services and in 1909 published

his ‘Manual of Railroad Securities’. The rating of utility and industrial bonds in 1904 followed this,

along with the rating of bonds issued by .S. cities and other municipalities in the early 1920’s.

Early 1920’s saw the expansion of credit rating industry when the POOR Publishing Company

published his first rating guide in 1916. Subsequently Fitch Publishing Company and Standard

Statistics Company were set up in 1924 and 1922 respectively. Poor Publishing Company and

Standard Statistics Company merged together in 1941 to form Standard and Poor’s which was

subsequently taken over by McGraw Hill in 1966. For almost 50 years after setting up of Fitch

Publishing in 1924, there were no major entrants in the field of credit rating. But since1970’s, a

number of credit rating agencies have been set up all over the world. These included the Canadian

Bond rating Service (1972), Thomson Bankwatch (1974) Japanese Bond Rating Institute (1975),

McCarthy Crisanti & Maffei (1975) (acquired by Duff & Phelps in 1991), Dominican Bond Rating

Service (1977), IBCA Limited(1978) and Duff & Phelps Credit Rating Company (1980). There are

other credit rating agencies too in operation in many other countries such as Malaysia, Philippines,

Mexico, Indonesia, Israel, Pakistan, Cyprus, Korea, Thailand, and Australia

In India, CRISIL (Credit Rating and Information Services of India Ltd.) was set up in 1987 as the

first rating agency followed by ICRA (formerly known as Investment Information & Credit Rating

Agency of India Ltd.) in 1991, and Credit Analysis and Research Ltd. (CARE) in 1994. All the three

agencies have been promoted by the All-India Financial Institutions. The rating agencies have

established their credit ability through their independence, professionalism, continuous research,

consistent efforts and confidentiality of information. Duff and Phelps has tied up with two Indian

NBFC’S to set up Duff and Phelps Credit Rating India (P) Ltd. in 1996

7

Exhibit 1 clearly brings out the history and growth of credit rating agencies the world over chronological order:

Year Credit Rating Agency

1841 Mercantile credit agency

1900 Moody’s Investors Service

1916 Poor Publishing Company (USA)

1922 Standard Publishing Company (USA)

1924 Fitch Publishing Company (USA)

1933 Dun & Bradstreet

1941 Standard & Poor (USA)

1966 McGraw Hill

1972 Canadian Bond rating Services

1974 Thomson Bankwatch (USA)

1975 Japanese Bond rating Service (JAPAN)

1975 McCarthy Crisanti & Maffie

1977 Dominican Bond rating Company

1978 I BCA Limited

1980 Duff & Phelps Credit Rating Company

1987 CRISIL (INDIA)

1991 ICRA (INDIA)

1994 CARE (INDIA)

1996 Duff and Phelps Credit Rating India (P) Limited

8

THE CREDIT RATING SYSTEM

Credit rating has facilitated authorities around the world to issue mandatory rating requirements.

For instance, specific rules restrict the entry of new issues that are rated below a

particular grade. Moreover they also stipulate different margin requirements for the mortgage of

rated and unrated instruments, and hence prohibit institutional investors from purchasing or holding

instruments that are rated below a particular level.

Growth Factors

Credibility and Independence

Ratings are considered valuable only as long as they are credible. Credibility arises primarily from

objectivity, which results from the rating agency being independent of the issuers business. The

investor is willing to accept the judgment only where such credibility exists. When increasing

number of investors are willing to accept the judgment of a particular rater, that rater than gaining

recognition as reputed rating agency. As expressed by Moody’s “The Rating Agency must do all it

can to reserve its credibility and integrity in the market place. As primary ingredient of credibility,

the agency must, maintain independence from all interested market forces, including issuers, security

underwriters, government.”

The credibility of a rating agency is also enhanced by other factors such as objectivity of

opinions, analytical integrity and consistency, professionalism, relevant expertise, strict rules of

confidentiality, timeliness of the rating review, announcement of changes, ability to reach a wide

range of investors through press reports, print or electronic publications, an investor friendly

research services.

Capital Market Mechanism.

A strong demand for investment related information is generated due to the reliance on the capital

market for resource allocation. Rating agencies provide this information. Investors consider rating an

important input for their investment decisions only when there is a perceived default risk.

9

Disclosure requirements.

Rating agencies have assumed importance on account of their task of assigning grades to securities

issued by companies. Moreover, it is becoming incumbent for companies, due to regulatory

guidelines, to have adequate corporate disclosure and to publish all the essential information

required by the investors. These guidelines require a mandatory disclosure of ratings.

Credit Education.

Credit rating serves as an effective educator on the modalities of arriving at valid judgments about

investing in securities. It is to be noted that the information should not only reach the investor, but it

must also enable them to make meaningful interpretations. The investor should also be aware of the

limitations of credit rating and should realize that the rating is not an insurance or guarantee against

default risk.

Creation of Debt Market

Credit rating is considered as an essential input for guiding investments in bonds. This assumes

significance in the context of substantial risks involved in their subscription. In fact, the continued

growth and evolution of the credit rating business depends on the size and growth of the debt market.

An active primary and secondary debt market is crucial for rating agencies to provide their services.

MAJOR ISSUES

Investment Vs speculative Grades.

Investment and speculative grades are two terms popularized by regulators. For instance, securities

that are rated below ‘BBB’ (S&P) or ‘Baa’ (Moody’s) are called non investment grade, or

speculative grade, or ‘junk bonds’. Rating agencies, however, do not recommend or indicate the

rating levels of instruments up to which one should or should not invest

Continuous Monitoring.

Credit rating agencies keep a constant surveillance during the life of the instrument for any

developments, until it is fully serviced by the company. In the absence of any specific developments,

such reviews are taken up periodically, either quarterly or annually. In addition, a formal and

extensive written review is taken up at least once a year. However there are some specific concerns

10

about the issuing entity, the review is taken up immediately. The grading is altered on the basis of

the changing debt servicing capability of the issuer.

Grade Surveillance

Where any major deviation from the expected trends of the issuers business occurs, or where any

event has taken place which may have an impact on the debt servicing capability of the issuer,

which could warrant a change in the rating, the rating agency put such ratings under grade

surveillance. This is done till such time the exact impact of the unanticipated developments is

analyzed and a decision is taken regarding the rating change. The grade surveillance listing may also

specify ‘positive’ or ‘negative’ outlooks.

Rating Ceiling

While rating an issue outside the issuer outside the issuer’s country of domicile, the international

credit rating agencies impose ceiling which is equal to the sovereign rating assigned to the country of

domicile. Accordingly rating of an instrument of any issuer domiciled in that country would be

placed above the sovereign rating of the country of domicile. This concept of sovereign rating

ceiling may not, however be applicable when domicile of the issuer in a country is wholly incidental

to an otherwise internationally dispersed business operation.

Evaluation of Line.

Evaluation of bank line policy is an important component of rating a commercial paper. However, it

is not a part of the rating criteria and the rating decision itself is not predicted on the strength of the

amount of bank lines.

Ownership Consideration.

It is invariably happens that ownership by a strong enterprise enhances the credit rating of an entity,

unless there exists a barrier separating the activities of the patent and subsidiary. The important

issues that are involved in deciding the relationship are mutual dependence, legal relationships, the

entity’s ability to influence the business of the other, and the importance of the operation of the

subsidiary to the owner.

11

CREDIT RATING AGENCY

A credit ratings agency is a company that assigns credit ratings to institutions that issue debt

obligations (i.e. assets backed by receivables on loans, such as mortgage-backed securities. These

institutions can be companies, cities, non-profit organizations, or national governments, and the

securities they issue can be traded on a secondary market.

A credit rating measures credit worthiness, or the ability to pay back a loan. It affects the interest rate

applied to loans - interest rates vary depending on the risk of the investment. A low-rated security

has a high interest rate, in order to attract buyers to this high-risk investment. Conversely, a highly-

rated security (carrying a AAA rating, like a municipal bond which is backed by stable government

agencies) has a lower interest rate, because it is a low-risk investment. These low-risk bonds are

available to a wide range of investors, whereas high-risk bonds cater to a narrow investing

demographic.

Companies that issue credit scores for individuals are usually called credit bureaus and are distinct

from corporate ratings agencies.

12

Definition:

"Credit Rating Agency" means any commercial concern engaged in the business of credit rating of

any debt obligation or of any project or programme requiring finance, whether in the form of debt or

otherwise, and includes credit rating of any financial obligation, instrument or security, which has

the purpose of providing a potential investor or any other person any information pertaining to the

relative safety of timely payment of interest or principal; [Section 65 (34)]

GLOBAL CREDIT RATING AGENCIES

John moody, with the publication of the first debt ratings as a a part of his Manual of Railroad

Securities, introduced the rating system in the US bond/securities market in 1909.the ratings were

associated with reports on the financial quality of 250-odd railroad companies operating in the US at

that time. Ratings began to play a more important role in the US capital markets after the Great

Depression, when high levels of default underscored the perception of risk in the fixed income

securities. To help assure the major institutional investors, who were critical to the economy, that

they were not further exposed to high defaults, government regulators stipulated that the big

institutions could not buy securities rated below a certain below a certain level. With the investors

exposing themselves to greater risk, it has become important to use the ratings extensively in bond

purchase and pricing decision. This resulted in a system, which served as a set of self regulatory

functions for the market participants.

In a developed economy, almost all the market participants are familiar with the rating process

and possess the experience to deal with new market developments. The market also helps to support

the value of the rating system to the market participants with factors such as high debt volume

unsupported by the government guarantee, and a liquid secondary market where the rating can be

useful in purchase decisions. The credit rating system is well established in the U.S debt markets.

Euro debt markets and international bank deposit markets are fairly well accepted in countries such

as UK, Canada and Australia, with a number of rating agencies operating in these markets.

13

A brief note on the background of the major international rating agencies is as follows

Duff and Phelps Credit Rating Co (DCR)

DCR is a major international source of credit information. It has been in existence for over sixty

years. It rates all major types of fixed-income securities, long term and short term debt of

corporations, sovereign nations and financial institutions. It also rate4s structured financing,

mortgage backed securities and insurance companies. It has established joint ventures, largely in

Latin American countries and since 1992, also in Asian countries such as India and Pakistan.

Japan Credit Rating agency (JCR)

It was established in 1985 and was promoted by financial institutions, banks and insurance

companies in Japan. It provides ratings to foreign and domestic debt issuers.

Thomson BankWatch

14

This rating agency is based in Toronto, Canada. It is a subsidiary of the Thomson Corporation. It is a

rating agency exclusively offering grades of rating to financial institutions including banks,

securities firms and finance companies.

Big Three Rating Agencies in U.S are:

Moody’s investors service (Moody’s)

Standard & Poor’s corporation (S & P)

Fitch ratings

The Big Three credit rating agencies are Standard & Poor's, Moody's Investor Service, and Fitch

Ratings. Moody's and S&P each control about 40 percent of the market. Third-ranked Fitch

Ratings, which has about a 14 percent market share, sometimes is used as an alternative to one

of the other majors. In the wake of recent credit-market turmoil, some niche agencies are picking

up market share or at least additional visibility. Among the niche agencies are DBRS and Egan-

Jones.

15

There are 5 credit rating agencies in India. Namely

Credit Rating Information Services of India Limited (CRISIL)

Investment Information and Credit Rating Agency of India (ICRA)

Credit Analysis & Research Limited (CARE)

Duff & Phelps Credit Rating India Private Ltd. (DCR India)

ONICRA Credit Rating Agency of India Ltd.

16

CREDIT RATING SYMBOLS

Meaning

Credit Rating Agencies rate an instrument by assigning a definite symbol. Each symbol has a

definite meaning. These symbols have been explained in descending order of safety or in ascending

order of risk of non-payment.

For example, CRISIL has prescribed the following system for debenture issues:

CRISIL AAA

(Highest Safety)

Instruments with this rating are considered to have the highest

degree of safety regarding timely servicing of financial obligations.

Such instruments carry lowest credit risk.

CRISIL AA

(High Safety)

Instruments with this rating are considered to have high degree of safety

regarding timely servicing of financial obligations. Such instruments carry

very low credit risk.

CRISIL A

(Adequate Safety)

Instruments with this rating are considered to have adequate degree of

safety regarding timely servicing of financial obligations. Such instruments

carry low credit risk.

CRISIL BBB

(Moderate Safety)

Instruments with this rating are considered to have moderate degree of

safety regarding timely servicing of financial obligations. Such instruments

carry moderate credit risk.

CRISIL BB

(Moderate Risk)

Instruments with this rating are considered to have moderate risk of default

regarding timely servicing of financial obligations.

CRISIL B

(High Risk)

Instruments with this rating are considered to have high risk of default

regarding timely servicing of financial obligations.

CRISIL C

(Very High Risk)

Instruments with this rating are considered to have very high risk of default

regarding timely servicing of financial obligations.

CRISIL D

Default

Instruments with this rating are in default or are expected to be in default

soon.

Note: 1) CRISIL may apply '+' (plus) or '-' (minus) signs for ratings from FAA to FC to indicate the

relative position within the rating category.

17

You will note that as the value of symbol is reduced say from AAA to AA, the safety of timely

payment of interest and principal is decreased. While AAA indicates highest safety of timely

repayment, D indicates actual default or expected default on maturity. Different symbols indicate

different degrees of risk of repayment of principal and interest.

CRISIL Rating Symbols for Fixed Deposits

FAAA

("F Triple A") Highest

Safety

This rating indicates that the degree of safety regarding

timely payment of interest and principal is very strong.

FAA

("F Double A") High Safety

This rating indicates that the degree of safety regarding timely

payment of interest and principal is strong. However, the relative

degree of safety is not as high as for fixed deposits with 'FAAA'

ratings.

FA

Adequate Safety

This rating indicates that the degree of safety regarding timely

payment of interest and principal is satisfactory. Changes in

circumstances can affect such issues more than those in the

higher rated categories.

FB

Inadequate Safety

This rating indicates inadequate safety of timely payment of

interest and principal. Such issues are less susceptible to default

than fixed deposits rated below this category, but the

uncertainties that the issuer faces could lead to inadequate

capacity to make timely interest and principal payments.

FC

High Risk

This rating indicates that the degree of safety regarding timely

payment of interest and principal is doubtful. Such issues have

factors at present that make them vulnerable to default; adverse

business or economic conditions would lead to lack of ability or

willingness to pay interest or principal.

FD

Default

This rating indicates that the fixed deposits are either in default or

are expected to be in default upon maturity.

NM Instruments rated 'NM' have factors present in them, which

render the outstanding rating meaningless. These include

18

Not Meaningful reorganization or liquidation of the issuer, the obligation being

under dispute in a court of law or before a statutory authority etc.

Note: 1) CRISIL may apply '+' (plus) or '-' (minus) signs for ratings from FAA to FC to indicate the

relative position within the rating category.

19

CORPORATE CREDIT RATING

20

The credit rating of a corporation is a financial indicator to potential investors of debt securities

such as bonds. Credit rating is usually of a financial instrument such as a bond, rather than the

whole corporation. These are assigned by credit rating agencies such as A. M. Best, Dun &

Bradstreet, Standard & Poor's, Moody's or Fitch Ratings and have letter designations such as

A, B, C.

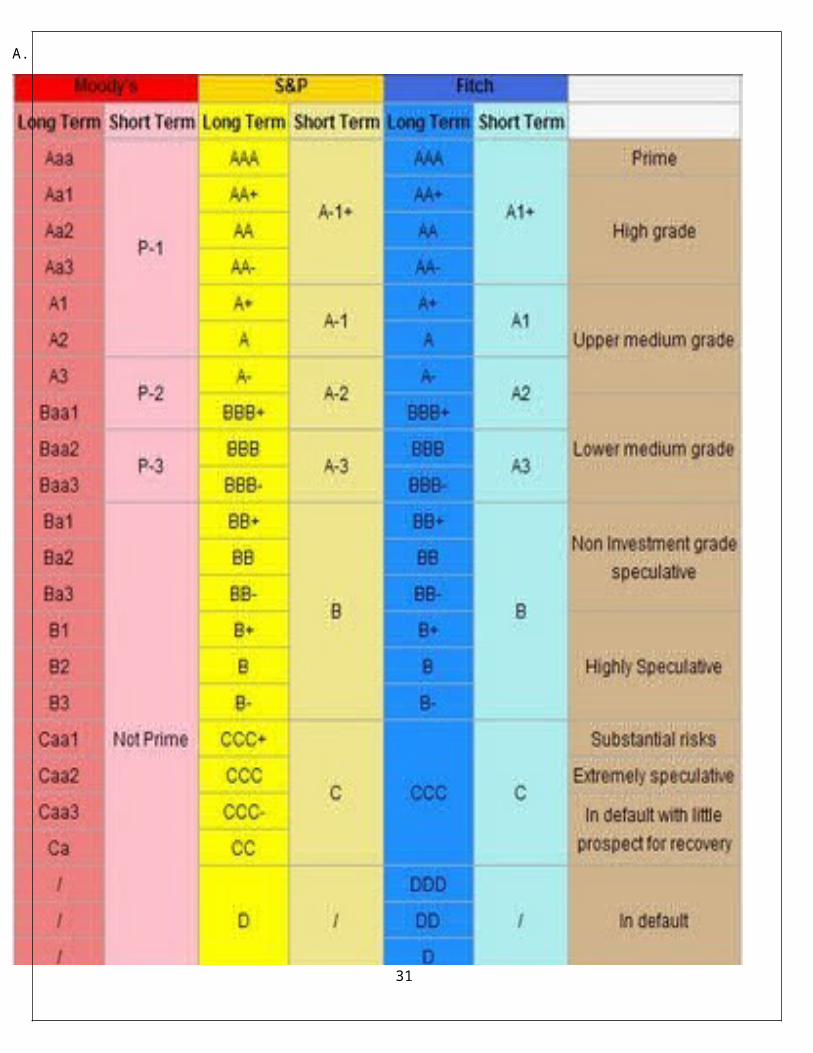

The Standard & Poor's rating scale is as follows, from excellent to poor: AAA, AA+, AA, AA-,

A+, A, A-, BBB+, BBB, BBB-, BB+, BB, BB-, B+, B, B-, CCC+, CCC, CCC-, CC, C, D. Anything

lower than a BBB- rating is considered a speculative or junk bond.

The Moody's rating system is similar in concept but the naming is a little different. It is as follows,

from excellent to poor: Aaa, Aa1, Aa2, Aa3, A1, A2, A3, Baa1, Baa2, Baa3, Ba1, Ba2, Ba3, B1, B2, B3, Caa1,

Caa2, Caa3, Ca, C.

A.M. Best rates from excellent to poor in the following manner: A++, A+, A, A-, B++, B+, B, B-,

C++, C+, C, C-, D, E, F, and S. The CTRISKS rating system is as follows: CT3A, CT2A, CT1A,

CT3B, CT2B, CT1B, CT3C, CT2C and CT1C. All these CTRISKS grades are mapped to one-year

probability of default.

21

A.

22

IPO GRADING/RATING

When the Securities and Exchange Board of India (SEBI) decided to scrap discretionary allotment

for qualified institutional buyers (QIBs) and switch to the more transparent proportionate allotment

system, it became the first regulator to stand up to the powerful investment banking community

anywhere in the world. Once the decision was taken, it was evident that the exaggerated outrage and

predictions that large institutional investors would shun IPOs were completely baseless.

That decision recognized the specific needs of the Indian capital market and was the result of

pressure from investor groups. The path to mandatory grading of IPOs has been rocky, with

enormous opposition from companies, investment bankers, fund managers, market experts and SEBI

board members. We learn that the final decision came about in the face of strong opposition by

certain board members (apparently not full-time) and that too only, with a twist in the tail, which

dilutes the original proposal. The alleged opposition of the regulator’s board members raises an

interesting question. All board-level discussions must, indeed, remain confidential in order to ensure

free and frank expression, but what is the fiduciary responsibility of board members of a watchdog

organization, who have no knowledge, training or expertise about capital markets, when they choose

to oppose recommendations of the Primary Market Advisory Committee that are endorsed by the

regulator? It is also important to remember that investor groups have been pressing for IPO grading

for several years; first with the Investor Education and Protection Fund(attached to the ministry of

23

company affairs), which developed cold feet and dropped even its plans for a pilot project and later

with the capital market regulator.

Over the years, those opposed to IPO grading have constructed several elegant arguments to rubbish

its utility, but from an investor standpoint, the logic is simple. The disclosure-based model adopted

by the regulator, leads to a bulky, jargon-filled prospectus that can neither be read nor understood by

the average investor; consequently, a simple, one-page evaluation of disclosures by an expert

agency, which also helpfully condenses its findings into a single numerical grade on a scale of five,

is clearly a blessing. The offer price of the IPO will remain an important factor in the final

investment decision—after all, even the best companies can be bad investments at the wrong price.

But that is a reasonable decision to leave to the investor.

Introduction

IPO grading is the grade assigned by a Credit Rating Agency registered with SEBI, to the initial

public offering (IPO) of equity shares or any other security which may be converted into or

exchanged with equity shares at a later date. The grade represents a relative assessment of the

fundamentals of that issue in relation to the other listed equity securities in India. Such grading is

generally assigned on a five-point point scale with a higher score indicating stronger fundamentals

and vice versa as below.

IPO grade1: Poor fundamentals

IPO grade2: Below-average fundamentals

IPO grade3: Average fundamentals

IPO grade4: Above-average fundamentals

IPO grade5: Strong fundamentals

IPO grading has been introduced as an endeavor to make additional information available for the

investors in order to facilitate their assessment of equity issues offered through an IPO.

IPO grading can be done either before filing the draft offer documents with SEBI or thereafter.

However, the Prospectus/Red Herring Prospectus, as the case may be, must contain the grade/s given

to the IPO by all CRAs approached by the company for grading such IPO.

The company desirous of making the IPO is required to bear the expenses incurred for

grading such IPO.

24

The company desirous of making the IPO is required to bear the expenses incurred for grading such

IPO.

IPO grading is not optional. A company which has filed the draft offer document for its IPO with

SEBI, on or after 1st May, 2007, is required to obtain a grade for the IPO from at least one CRA.

IPO grade/s cannot be rejected. Irrespective of whether the issuer finds the grade given by the rating

agency acceptable or not, the grade has to be disclosed as required under the DIP Guidelines.

However the issuer has the option of opting for another grading by a different agency. In such an

event all grades obtained for the IPO will have to be disclosed in the offer documents,

advertisements

IPO grading is intended to run parallel to the filing of offer document with SEBI and the consequent

issuance of observations. Since issuance of observation by SEBI and the grading process, function

independently, IPO grading is not expected to delay the issue process.

The IPO grading process is expected to take into account the prospects of the industry in which the

company operates, the competitive strengths of the company that would allow it to address the risks

inherent in the business(es) and capitalize on the opportunities available, as well as the company’s

financial position.

While the actual factors considered for grading may not be identical or limited to the following, the

areas listed below are generally looked into by the rating agencies, while arriving at an IPO grade

Business Prospects and Competitive Position

i. Industry Prospects etc.

ii. Company Prospects

Financial Position

Management Quality

Corporate Governance Practices

25

Compliance and Litigation History

New Projects—Risks and Prospects

It may be noted that the above is only indicative of some of the factors considered in the IPO grading

process and may vary on a case to case basis.

IPO grading is done without taking into account the price at which the security is offered in the IPO.

Since IPO grading does not consider the issue price, the investor needs to make an independent

judgment regarding the price at which to bid for/subscribe to the shares offered through the IPO.

IPO Grading is intended to provide the investor with an informed and objective opinion

expressed by a professional rating agency after analyzing factors like business and financial

prospects, management quality and corporate governance practices etc. However, irrespective

of the grade obtained by the issuer, the investor needs to make his/her own independent

decision regarding investing in any issue after studying the contents of the prospectus

including risk factors carefully.

As on date the following four credit rating agencies are registered with SEBI.

a) Credit Analysis & Research Ltd (CARE)

b) ICRA Limited

c) CRISIL

d) FITCH Ratings

26

SOVEREIGN CREDIT RATINGS

A sovereign credit rating is the credit rating of a sovereign entity, i.e., a national government. The

sovereign credit rating indicates the risk level of the investing environment of a country and is used

by investors looking to invest abroad. It takes political risk into account

The table shows the ten least-risky countries for investment as of June 2012. Ratings are further

broken down into components including political risk, economic risk. Euro money’s bi-annual

country risk index monitors the political and economic stability of 185 sovereign countries. Results

focus foremost on economics, specifically sovereign default risk and/or payment default risk for

exporters (a.k.a. "trade credit" risk).

A. M. Best defines "country risk" as the risk that country-specific factors could adversely affect an

insurer's ability to meet its financial obligations.

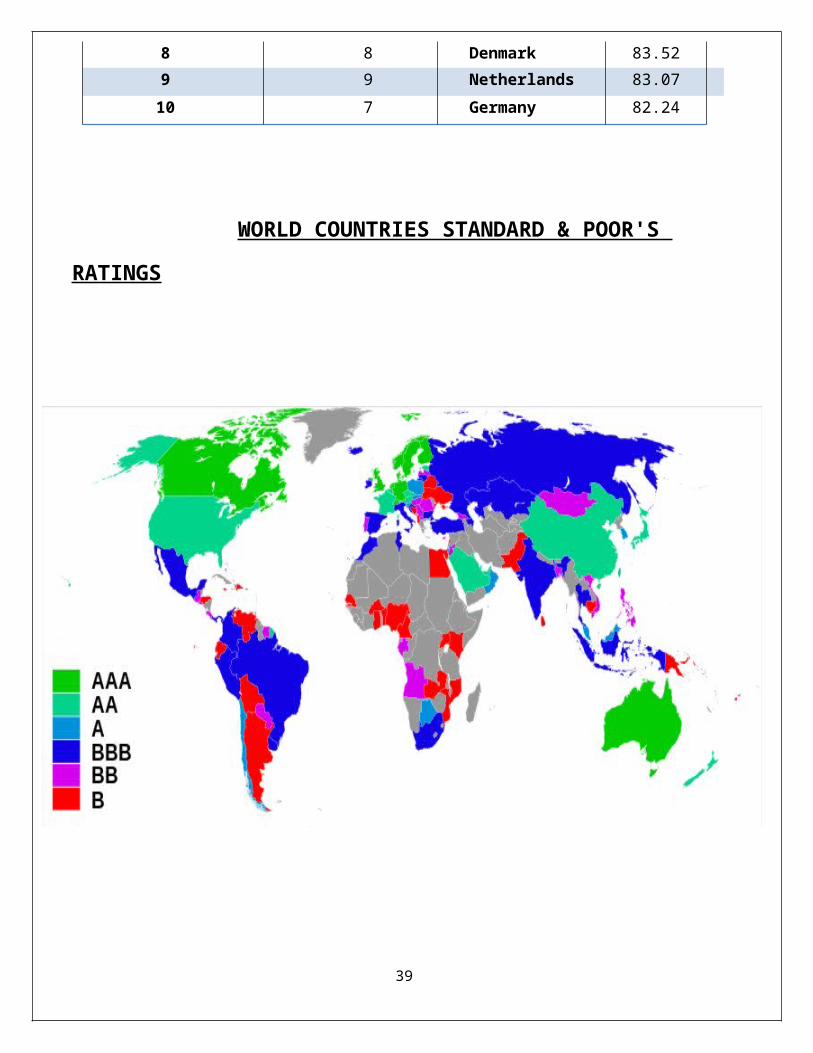

COUNTRY RISK RANKINGS (JUNE 2012)

Least risky countries, Score out of 100

Rank Previous

Country Overall score

1 1 Norway 90.37

2 2 Switzerland 88.83

3 3 Singapore 88.03

4 4 Luxembourg 87.90

5 4 Sweden 86.79

6 5 Finland 84.30

7 7 Canada 84.26

8 8 Denmark 83.52

9 9 Netherlands 83.07

10 7 Germany 82.24

27

WORLD COUNTRIES STANDARD & POOR'S RATINGS

28

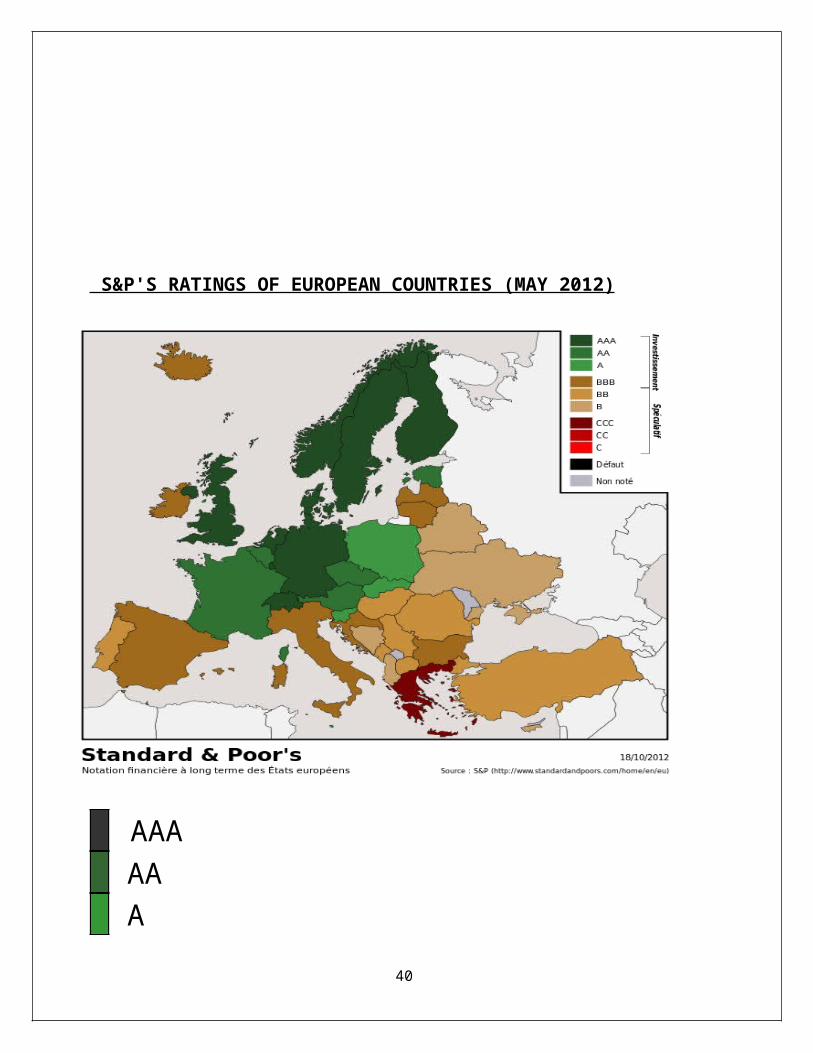

S&P'S RATINGS OF EUROPEAN COUNTRIES (MAY 2012)

AAA AA A BBB BB B CCC CC C Default no rating

29

INDIVIDUAL CREDIT RATING IN INDIA

Primer for Individuals

When it comes to risk management in Banks, the risk that takes the priority is "the credit risk".

The credit risk by definition means, risk of loans disbursed to various corporate and retail clients

will be paid back or not. For layman's understanding, a bank broadly has two main functions viz.

Assets and Liabilities. The main job of the liabilities side of a bank is to channelize savings in the

economy, designs various instruments, by which; money can be collected from the economy. This

could be in the form of saving bank accounts, current accounts, FDs etc. The money so collected,

is a liability on the bank as it has to repay the same to its customers with certain prevailing rate of

interest and hence the function is called Liability. Once money is collected from various sources,

the same has to be deployed at a profitable rate of return. The deployment could be in the form of

corporate lending, investing in projects or simply retail lending in the form of Personal Loans,

Vehicle loans, home loans, SME lending etc.

The basic principle of managing Credit Risk is diversification of portfolio. This means, that

lending to corporate borrowers is diversified in terms of different industries and within an

industry to different corporate. Lending is based on as per the underwriting standards of the bank

e.g. the repute of the company, past financials of the company including profitability over last

several years, shareholding pattern, qualitative study of management, project feasibility of the

project to be funded, future cash lows etc. Although all banks into corporate lending develop their

own individual underwriting policies, they also depend on the credit rating of a corporate by

accredited Credit Rating Agencies like CRISIL, ICRA and CARE. Even the Basel Committee on

Banking Regulation has accentuated on the importance of use of external credit ratings.

The retail segment in India, however, has been devoid of external agencies, which are into credit

rating of individuals i.e. retail customers. The lending to retail customers is done basis purely on

the lending policy of the bank, which vary from bank to bank, depending on the banks risk

appetite. In the United States, there are government funded repositories like Equifax, Trans-world,

Trans Union, Dun &Bradstreet etc, which act as credit rating agencies for retail borrowers. They

provide member banks/NBFCs with credit history of an individual in terms of loans that he has

paid in the past, loans that he is currently running, Credit Cards that he has held or currently

active with repayment history of the same. There are other vital information that the agency report

provide viz., if the borrower has ever filed for bankruptcy or if there is any litigation, court case

etc. pending against him. Based on the overall credit history of the customer, he/she is given a 30

credit rating, more popularly called, FICO score. This may vary from agency to agency but the

variation may not be more than 10%.However, the US system of credit rating individual could not

be replicated in India because of some practical difficulties. The most important being, absence of

a mechanism for identifying an individual. In the United States, each individual is issued a Social

Security Number or the SSN, when he/she is born. This SSN is a unique number and all

information related an individual, including social history, financial history, criminal history etc is

linked to ones SSN and therefore, collecting information about individual becomes much easier.

This is further facilitated by the presence of a system, which ensures that the information flows

freely between well coordinated government and public departments. Hence, information related

to individual can be stored at a common place and retrieved when required. Also, there are proper

laws in place, which requires all the public/private entities like banks, NBFCs etc. to share their

customer related data with the credit rating agencies. In India, the scenario has been different. The

is no concept of Social Security Number to identify an individual. The only way to identify a

customer is through name, address, Date of Birth (DoB) etc. However, with no sanctity of DoB

proofs or address proofs, it is very easy to fool the system. Till sometime bank, the only way for a

bank to know the credit history of a prospective customer was through its collection or field

verification agencies, which may or may not had information about the customer. Besides, banks

also did not pay any strict attention to the data sanctity of the customer at their end. This is,

particularly true to banks issuing Credit Cards.

With rising competition in the retail sector, there was a sharp rise in delinquency level of banks.

The need for Credit Rating Agency which could work like a repository for credit information of

individual was widely felt. As a first attempt in this direction, The Credit Information Bureau of

India Ltd or the CIBIL was incorporated in 2000. CIBIL was an effort of The Government of

India and the Reserve Bank of India. The first promoters and the member banks were the State

Bank of India (SBI) and HDFC. Necessary logistics and technology was provided by

internationally reputed credit rating agencies like Dun & Bradstreet and Trans-union. However,

the attempt was not efficacious initially, since most banks were reluctant about sharing their

customer data with other banks. This was further aggravated by the fact that the banks were not

under any legal obligation to share their data. However, with RBI's efforts, more and more banks

and NBFCs have joined hand in providing customer data to CIBIL and in return get data on the

customers on payment of some fees from CIBIL. This initiative called CIBIL has really been

helpful in curbing delinquency and banks have starting weaving their credit lending policy around

CIBIL.

31

The quality of CIBIL reports have further been helped by certain government measures like

introduction of PAN numbers and making the same mandatory for availing most banking

services. The PAN number may be considered as a very crude form of a Social Security Number,

since only taxpaying individuals apply for it i.e. people not falling in tax bracket or not wanting to

pay tax, may or may not have PAN no. But with regulators like RBI, Tax Departments etc making

PAN no. mandatory for availing banking and investment services, more and more percentage of

population (at least those wanting to avail credit) are now having a valid PAN no., which to a

large extent has done the same job what SSN does in the United States. Any technological

advancement in future, which may lead to better networking between banks, government agencies

like judiciary, RBI and CIBIL will only further improve the quality of CIBIL reporting. As of

now, CIBIL has not introduced any system of assigning any Credit Rating to individuals like the

FICO scoring as mentioned above. But this may be just round the corner. Also, a competition in

the credit rating field i.e. more set ups like CIBIL will not only see a further improvement in

quality in terms of services being provided to the banks and NBFCs but will also see cost

rationalization. Prior to CIBIL and along with CIBIL, there was information available in the

market but it was more scattered and specific. For example, Satyam Database, more popularly

known as MCNF database (Master Card Negative Feedback), is available in the market. The

MCNF database is the data of database of all delinquent customers who have defaulted in their

Master Card Credit Card. The customer could belong to any bank which issues Master Card

Credit Card. Besides this, most of the verification agencies in any particular area, are a rich source

of credit information, specially derogatory. Since most of these verification agencies are also

invariably collection agencies for multiple banks, they have their own database for derogatory

customers. There is a basic limitation to both MCNF database and data available with verification

agencies. One the data is very limited and does not cover sizable proportion of the credit seeking

population. MCNF covers only Master Card Credit Card while verification agencies have data of

their client banks only. Most of these verification agencies have their area of operation limited to

only one city or couple of cities in the same state but not beyond that. Second, the MCNF and

Verification Agencies have only derogatory data. So, if a match is found, then, the customer is a

bad credit or risky to lend, but if there is no match, it will not be prudent to assume that the

customer is a good credit or not risky to lend. CIBIL is however, a balanced approach, as it

contains all the credit history available for the customer, both good and bad.

32

How Does It Impacts Individuals

With set ups like CIBIL, there is a free flow of credit information between banks. All members

have access to the CIBIL database. Hence, it is becoming, increasingly difficult for chronic

defaulters to obtain credit from the banks. As mentioned before, most bank are weaving their

credit policy around CIBIL, MCNF and Verification Agency records, it is very important for

individuals to be aware and sensitive to their credit history.

It is a common observation with the people of younger age group, that, they carry multiple credit

cards, more as a matter of style statement, than, having an actual requirement of the same. This is

coupled with over spending and in their juvenile spirit, not paying. What they do not realize is

that this derogatory information is actually being stored against their name, add or PAN no.

somewhere, and when, later in their life, they are in actual need for credit, they do not get it. The

above given example is of a willful customer, but there are also common instances service related

issues with the banks, specially, credit card issuing banks e.g. annual fee levied when free credit

card promised or insurance premium charged without customer's knowledge. Instances could be

numerous, but unfortunately, itis the individual, who is impacted negatively in such a situation.

Often, after charging multiple late fees, interests etc, the default amount reported to CIBIL or

Satyam database, is quite high. Lending institution, prima facie, do not investigate in the

derogatory information and decline a loan or a credit card application upfront. Since, all banks are

free to make their own credit policy, a bank with low risk appetite and hence strict credit policy is

not likely to reconsider credit application, even if, in reality, it was not customer's fault.

What to Do / What Not to Do

The importance of a clean credit history is understood when emergency credit is required, for

example, a personal loan in order to meet immediate medical expenses or a home loan and the

same is denied because one did not bother to repay his credit card debts or his auto loan EMI or

resolve the dispute with a financier in the past. Since, most of us, especially in the middle class,

salaried or businessmen, will require a credit at some point of time either for a personal need,

building a house or for business purpose or a credit card, there are a few precautions that an

individual must take in his financial dealings. One must be very diligent and disciplined in

repaying his debts, EMIs, Credit Card payments etc. In rarity, if there is a delay in payment, one

should make sure, that, the payment with late payment charges if any, should not cross 30 days

past due. If late payment charges or any other charges are waived off by the bank specifically in

written, then only, such charges are not to be paid. If there is a dispute in payment, especially in 33

credit card related payments, one should make sure that the dispute is resolved and he has a

written record of the same in his possession. Some people think that settling an account for

something less than what is actual due is an easy way out. The settlement will only give them a

settlement letter, which is an indicator that they did not pay the full amount. Neither is their name

or record taken off from the derogatory history of the bank and hence CIBIL/Satyam records. In

case, the bank is at a fault, which it agrees on also, it is very important to acquire an apology letter

from the bank, clearly stating the issue and bank's apology on the same.

Most of us, keep getting calls from various Credit Card issuing bank's DSA (Direct Selling

Associates), which would make loads of promises and would request us to at least keep the card

for a year and then destroy the same after informing the bank of your intention of not using the

same. Such offers should be avoided, if one is NOT in need of that credit card. Since, one does

not need that card; it will be lying dormant in his pocket for a year. He would even forget the date

as to when the card is to be blocked. Since the card is free for only the first year, next year

beginning, he would receive a statement with annual fees levied. He will dispute it, not pay it. The

bank will keep following up and levying late payment and other incidentals charges, and report it

as a derogatory card to the CIBIL. The bank cannot blamed for the same, since, as per its terms

and conditions, the card was free for first year only and the customer did not bother to cancel it at

the end of the year. So, why, unnecessarily, call for a problem, when it can be easily avoided by

politely declining to accept for the card in the first place. The principle is simple. Do NOT avail a

credit if you DON'T need it.

SHORT-TERM RATING

A short-term rating is a probability factor of an individual going into default within a year. This is in

contrast to long-term rating which is evaluated over a long timeframe. In the past institutional

investors preferred to consider long-term ratings. Nowadays, short-term ratings are commonly used.

First, the Basel II agreement requires banks to report their one-year probability if they applied

internal-ratings-based approach for capital requirements. Second, many institutional investors can

easily manage their credit/bond portfolios with derivatives on monthly or quarterly basis. Therefore,

some rating agencies simply report short-term ratings.

34

USES OF RATINGS

Credit ratings are used by investors, issuers, investment banks, broker-dealers, and governments. For

investors, credit rating agencies increase the range of investment alternatives and provide

independent, easy-to-use measurements of relative credit risk; this generally increases the efficiency

of the market, lowering costs for both borrowers and lenders. This in turn increases the total supply

of risk capital in the economy, leading to stronger growth. It also opens the capital markets to

categories of borrower who might otherwise be shut out altogether: small governments, startup

companies, hospitals, and universities.

Ratings use by bond issuers

Issuers rely on credit ratings as an independent verification of their own credit-worthiness and the

resultant value of the instruments they issue. In most cases, a significant bond issuance must have at

least one rating from a respected CRA for the issuance to be successful (without such a rating, the

issuance may be undersubscribed or the price offered by investors too low for the issuer's purposes).

Studies by the Bond Market Association note that many institutional investors now prefer that a debt

issuance have at least three ratings.

Issuers also use credit ratings in certain structured finance transactions. For example, a company

with a very high credit rating wishing to undertake a particularly risky research project could create a

legally separate entity with certain assets that would own and conduct the research work. This

"special purpose entity" would then assume all of the research risk and issue its own debt securities

to finance the research. The SPE's credit rating likely would be very low, and the issuer would have

to pay a high rate of return on the bonds issued.

However, this risk would not lower the parent company's overall credit rating because the SPE

would be a legally separate entity. Conversely, a company with a low credit rating might be able to

borrow on better terms if it were to form an SPE and transfer significant assets to that subsidiary and

issue secured debt securities. That way, if the venture were to fail, the lenders would have recourse

to the assets owned by the SPE. This would lower the interest rate the SPE would need to pay as part

of the debt offering.

The same issuer also may have different credit ratings for different bonds. This difference results

from the bond's structure, how it is secured, and the degree to which the bond is subordinated to

other debt. Many larger CRAs offer "credit rating advisory services" that essentially advise an issuer

on how to structure its bond offerings and SPEs so as to achieve a given credit rating for a certain 35

debt tranche. This creates a potential conflict of interest; of course, as the CRA may feel obligated to

provide the issuer with that given rating if the issuer followed its advice on structuring the offering.

Some CRAs avoid this conflict by refusing to rate debt offerings for which its advisory services were

sought.

Ratings use by government regulators

Regulators use credit ratings as well, or permit ratings to be used for regulatory purposes. For

example, under the Basel II agreement of the Basel Committee on Banking Supervision, banking

regulators can allow banks to use credit ratings from certain approved CRAs (called "ECAIs", or

"External Credit Assessment Institutions") when calculating their net capital reserve requirements. In

the United States, the Securities and Exchange Commission (SEC) permits investment banks and

broker-dealers to use credit ratings from "Nationally Recognized Statistical Rating Organizations"

(NRSRO) for similar purposes. The idea is that banks and other financial institutions should not need

keep in reserve the same amount of capital to protect the institution against (for example) a run on

the bank, if the financial institution is heavily invested in highly liquid and very "safe" securities

(such as U.S. government bonds or short-term commercial paper from very stable companies).

CRA ratings are also used for other regulatory purposes as well. The US SEC, for example, permits

certain bond issuers to use a shortened prospectus form when issuing bonds if the issuer is older, has

issued bonds before, and has a credit rating above a certain level. SEC regulations also require that

money market funds (mutual funds that mimic the safety and liquidity of a bank savings deposit, but

without Federal Deposit Insurance Corporation insurance) comprise only securities with a very high

NRSRO rating. Likewise, insurance regulators use credit ratings to ascertain the strength of the

reserves held by insurance companies.

In 2008, the US SEC voted unanimously to propose amendments to its rules[2] that would remove

credit ratings as one of the conditions for companies seeking to use short-form registration when

registering securities for public sale.

This marks the first in a series of upcoming SEC proposals in accordance with Dodd-Frank to

remove references to credit ratings contained within existing Commission rules and replace them

with alternative criteria.

36

Under both Basel II and SEC regulations, not just any CRA's ratings can be used for regulatory

purposes. (If this were the case, it would present a moral hazard). Rather, there is a vetting process of

varying sorts. The Basel II guidelines for example, describe certain criteria that bank regulators

should look to when permitting the ratings from a particular CRA to be used. These include

"objectivity," "independence," "transparency," and others. Banking regulators from a number of

jurisdictions have since issued their own discussion papers on this subject, to further define how

these terms will be used in practice. (See The Committee of European Banking Supervisors

Discussion Paper, or the State Bank of Pakistan ECAI Criteria).

In the United States, since 1975, NRSRO recognition has been granted through a "No Action Letter"

sent by the SEC staff. Following this approach, if a CRA (or investment bank or broker-dealer) were

interested in using the ratings from a particular CRA for regulatory purposes, the SEC staff would

research the market to determine whether ratings from that particular CRA are widely used and

considered "reliable and credible." If the SEC staff determines that this is the case, it sends a letter to

the CRA indicating that if a regulated entity were to rely on the CRA's ratings, the SEC staff will not

recommend enforcement action against that entity. These "No Action" letters are made public and

can be relied upon by other regulated entities, not just the entity making the original request. The

SEC has since sought to further define the criteria it uses when making this assessment, and in

March 2005 published a proposed regulation to this effect.

On September 29, 2006, US President George W. Bush signed into law the Credit Rating Reform

Act of 2006.This law requires the US Securities and Exchange Commission to clarify how NRSRO

recognition is granted, eliminates the "No Action Letter" approach and makes NRSRO recognition a

Commission (rather than SEC staff) decision, and requires NRSROs to register with, and be

regulated by, the SEC. S & P protested the Act on the grounds that it is an unconstitutional violation

of freedom of speech. In the Summer of 2007 the SEC issued regulations implementing the act,

requiring rating agencies to have policies to prevent misuse of nonpublic information, disclosure of

conflicts of interest and prohibitions against "unfair practices".

Recognizing CRAs' role in capital formation, some governments have attempted to jump-start their

domestic rating-agency businesses with various kinds of regulatory relief or encouragement. This

may, however, be counterproductive, if it dulls the market mechanism by which agencies compete,

subsidizing less-capable agencies and penalizing agencies that devote resources to higher-quality

opinions.

37

Ratings use in structured finance

Credit rating agencies may also play a key role in structured financial transactions. Unlike a

"typical" loan or bond issuance, where a borrower offers to pay a certain return on a loan, structured

financial transactions may be viewed as either a series of loans with different characteristics, or else

a number of small loans of a similar type packaged together into a series of "buckets" (with the

"buckets" or different loans called "tranches"). Credit ratings often determine the interest rate or

price ascribed to a particular tranche, based on the quality of loans or quality of assets contained

within that grouping.

Companies involved in structured financing arrangements often consult with credit rating agencies to

help them determine how to structure the individual tranches so that each receives a desired credit

rating. For example, a firm may wish to borrow a large sum of money by issuing debt securities.

However, the amount is so large that the return investors may demand on a single issuance would be

prohibitive. Instead, it decides to issue three separate bonds, with three separate credit ratings—A

(medium low risk), BBB (medium risk), and BB (speculative) (using Standard & Poor's rating

system).

The firm expects that the effective interest rate it pays on the A-rated bonds will be much less than

the rate it must pay on the BB-rated bonds, but that, overall, the amount it must pay for the total

capital it raises will be less than it would pay if the entire amount were raised from a single bond

offering. As this transaction is devised, the firm may consult with a credit rating agency to see how it

must structure each tranche—in other words, what types of assets must be used to secure the debt in

each tranche—in order for that tranche to receive the desired rating when it is issued.

There has been criticism in the wake of large losses in the collateralized debt obligation (CDO)

market that occurred despite being assigned top ratings by the CRAs. For instance, losses on $340.7

million worth of CDOs issued by Credit Suisse Group added up to about $125 million, despite being

rated AAA or Aaa by Standard & Poor's, Moody's Investors Service and Fitch Group.

The rating agencies respond that their advice constitutes only a "point in time" analysis, that they

make clear that they never promise or guarantee a certain rating to a tranche, and that they also make

clear that any change in circumstance regarding the risk factors of a particular tranche will invalidate

their analysis and result in a different credit rating. In addition, some CRAs do not rate bond

issuances upon which they have offered such advice.

38

Complicating matters, particularly where structured finance transactions are concerned, the rating

agencies state that their ratings are opinions (and as such, are protected free speech, granted to them

by the "personhood" of corporations) regarding the likelihood that a given debt security will fail to

be serviced over a given period of time, and not an opinion on the volatility of that security and

certainly not the wisdom of investing in that security. In the past, most highly rated (AAA or Aaa)

debt securities were characterized by low volatility and high liquidity—in other words, the price of a

highly rated bond did not fluctuate greatly day-to-day, and sellers of such securities could easily find

buyers.

However, structured transactions that involve the bundling of hundreds or thousands of similar (and

similarly rated) securities tend to concentrate similar risk in such a way that even a slight change on

a chance of default can have an enormous effect on the price of the bundled security. This means

that even though a rating agency could be correct in its opinion that the chance of default of a

structured product is very low, even a slight change in the market's perception of the risk of that

product can have a disproportionate effect on the product's market price, with the result that an

ostensibly AAA or Aaa-rated security can collapse in price even without there being any default (or

significant chance of default). This possibility raises significant regulatory issues because the use of

ratings in securities and banking regulation (as noted above) assumes that high ratings correspond

with low volatility and high liquidity.

Credit rating agencies do not downgrade companies promptly enough. For example, Enron's rating

remained at investment grade four days before the company went bankrupt, despite the fact that credit

rating agencies had been aware of the company's problems for months. Some empirical studies have

documented that yield spreads of corporate bonds start to expand as credit quality deteriorates but

before a rating downgrade, implying that the market often leads a downgrade and questioning the

informational value of credit ratings. This has led to suggestions that, rather than rely on CRA ratings in

financial regulation, financial regulators should instead require banks, broker-dealers and insurance

firms (among others) to use credit spreads when calculating the risk in their portfolio.

Large corporate rating agencies have been criticized for having too familiar a relationship with

company management, possibly opening themselves to undue influence or the vulnerability of being

misled. These agencies meet frequently in person with the management of many companies, and advise

on actions the company should take to maintain a certain rating .Furthermore, because information

39

about ratings changes from the larger CRAs can spread so quickly (by word of mouth, email, etc.), the

larger CRAs charge debt issuers, rather than investors, for their ratings. This has led to accusations that

these CRAs are plagued by conflicts of interest that might inhibit them from providing accurate and

honest ratings. At the same time, more generally, the largest agencies (Moody's and Standard &

Poor's)are often seen as agents of globalization and/or "Anglo-American" market forces, that drive

companies to consider how a proposed activity might affect their credit rating, possibly at the expense