creating a legacy: life insurance & charitable gifting

DESCRIPTION

Creating a Legacy: Life Insurance & Charitable Gifting. John Jordan, CFP Insurance & Estate Planning Specialist . Topics Covered. Testamentary Charitable Gifts Gifts given in the estate Donation receipts used to offset tax in the estate Preserve estate value - PowerPoint PPT PresentationTRANSCRIPT

Creating a Legacy:Life Insurance & Charitable

GiftingJohn Jordan, CFP

Insurance & Estate Planning Specialist

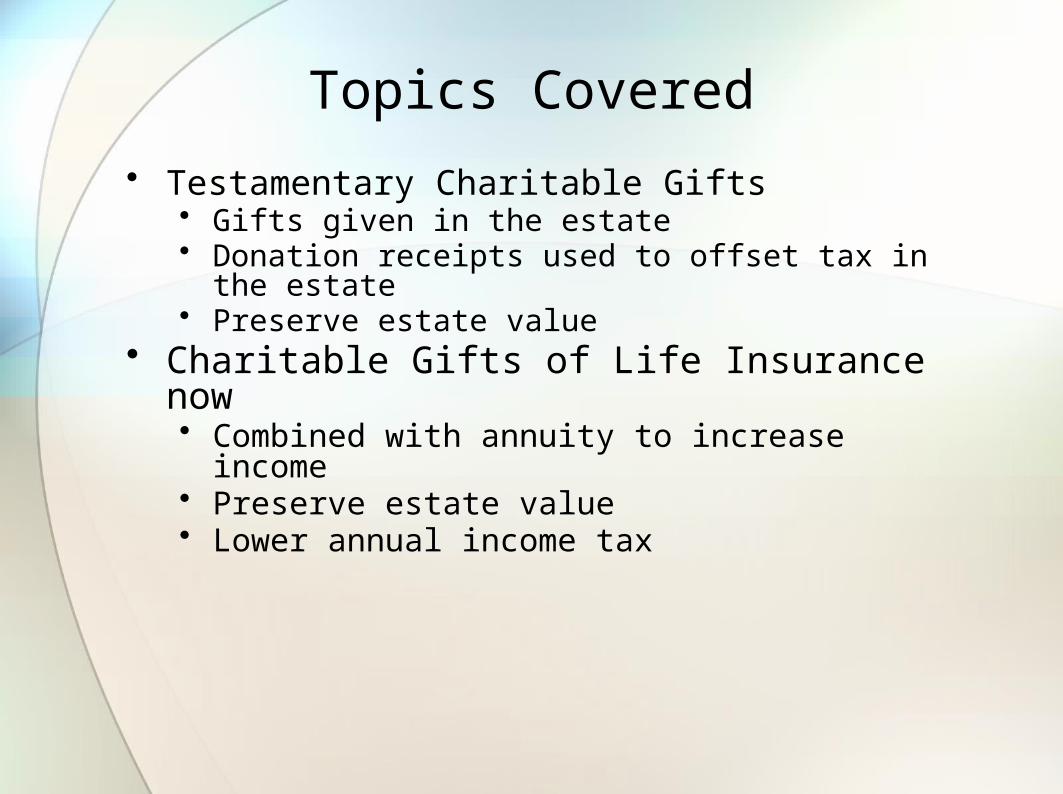

Topics Covered• Testamentary Charitable Gifts

• Gifts given in the estate• Donation receipts used to offset tax in the estate• Preserve estate value

• Charitable Gifts of Life Insurance now• Combined with annuity to increase income• Preserve estate value• Lower annual income tax

Where will your Social Capital Go?• By Default

• You have 2 beneficiaries when your estate settles• Your family and CRA

• Self Directed• Introduce charitable gifting into your estate plan• You now have 3 beneficiaries when your estate settles

• Your family, charity, and CRA

Self Directed Plan: Pick 2 of the 3!

…It was an honest mistake…

We didn’t say we were going to

“Scrap the tax for you…”

We said we were going to

“Tax the crap out of you…”

Gifts of Charitable Life Insurance• Mike & Anita, age 65, concerned with amount of tax

owing in their estate• Want to preserve their estate for their family but

also provide a Charitable Gift• Have sufficient retirement income from

• RRIFs, • Work Pensions, • CPP, and OAS

• Have designated $120,000 to their charity which is set aside in T-Bills

• RRIFs total $300,000 between them• Potential tax liability of $139,230.00 on RRIFs

• Want to re-structure their affairs and look into alternative ways of charitable gifting

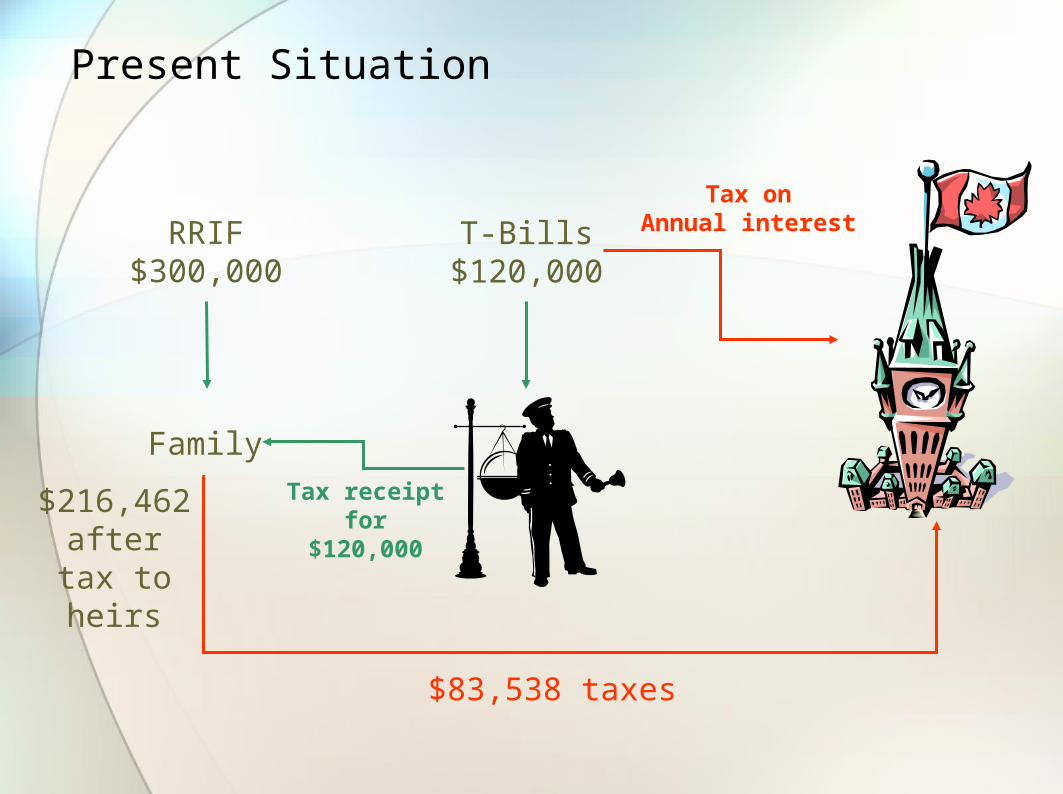

Present Situation

RRIF$300,000

Family

$83,538 taxes

T-Bills$120,000

Tax onAnnual interest

Tax receipt for $120,000$216,462

after tax to heirs

Gifts of Charitable Life Insurance• Enhanced Bequest and their estate preserved with a

“Joint-2nd-to-die” estate Universal Life insurance plan.• Perform an “Asset Shift” by moving the $120,000

over 5 years into the estate Universal Life insurance plan • Redundant assets are moved from a taxable environment

to a tax-sheltered environment• Estate value is instantly magnified• Tax free transfer of assets

• Rearrange Beneficiary Designations

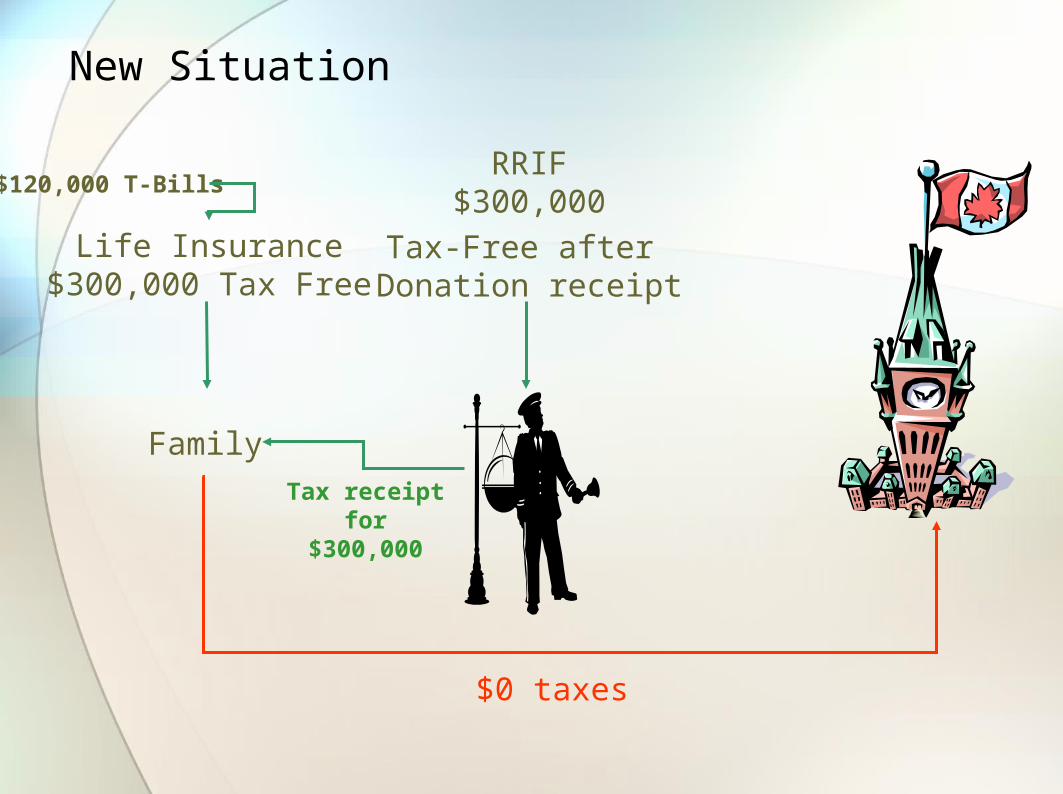

New Situation

Life Insurance$300,000 Tax Free

Family

$0 taxes

RRIF$300,000$120,000 T-Bills

Tax-Free after Donation receipt

Tax receipt for $300,000

Gifts of Charitable Life InsuranceNew Situation • Amount left to family

increased from $216,462 to $300,000

• Amount left to Charity increased from $120,000 to $300,000

• Amount left to CRA decreased from $83,538 to $0

To Fam

ily

To Ch

arity

To CR

A

0

50000

100000

150000

200000

250000

300000

Before After

Creating a Legacy:Life Insurance & Charitable

GiftingJohn Jordan, CFP

Insurance & Estate Planning Specialist

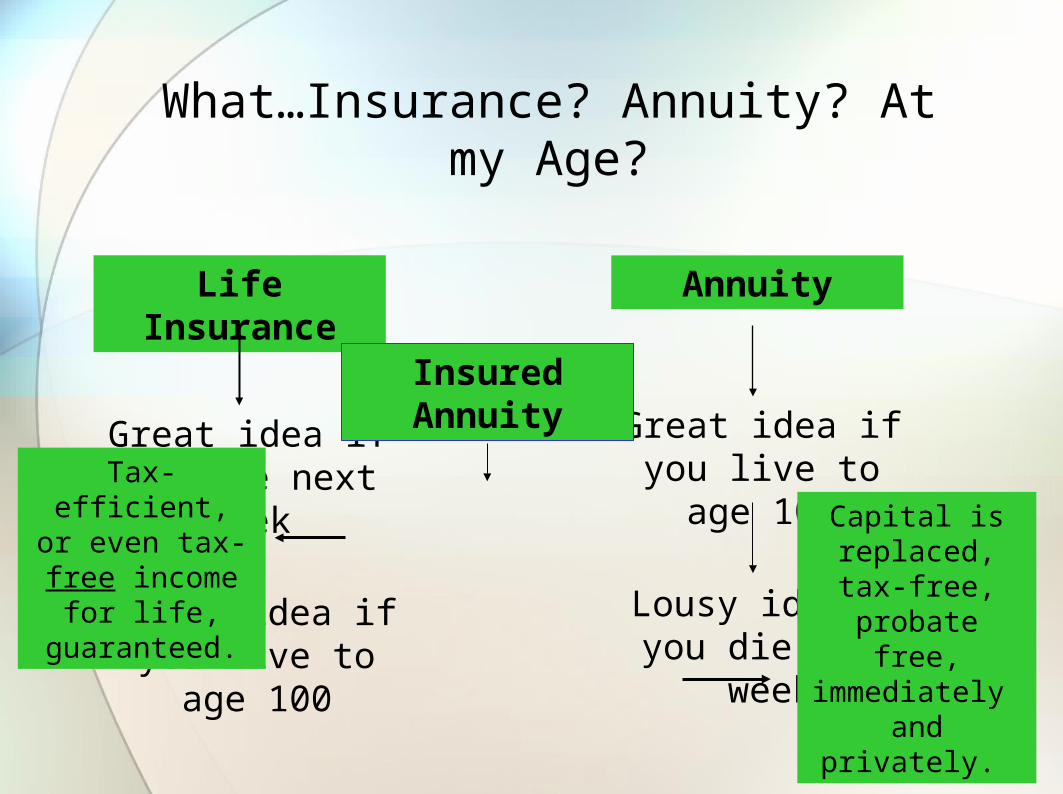

What…Insurance? Annuity? At my Age?

Life Insurance

Great idea if you die next week

Lousy idea if you live to age 100

Annuity

Great idea if you live to age 100

Lousy idea if you die next week

Insured Annuity

Capital is replaced, tax-free, probate

free, immediately and privately.

Tax-efficient, or even tax-free

income for life, guaranteed.

Gifts of Charitable Life Insurance• Marie is a healthy 74 year old widow• Retired Teacher• Gives $5,000 annually to charity• Has designated her RRIF (approx. $200k at mortality) and

$350,000 to charity in her Will with balance of estate to heirs ($1.6MM net worth)

• Marie’s Wish List1) Would like to increase annual charitable giving (additional

$5,000) without affecting income2) Doesn’t want to incur risk with investments3) Wants to keep a portion of GICs for future liquidity4) Wants to keep estate in tact for heirs

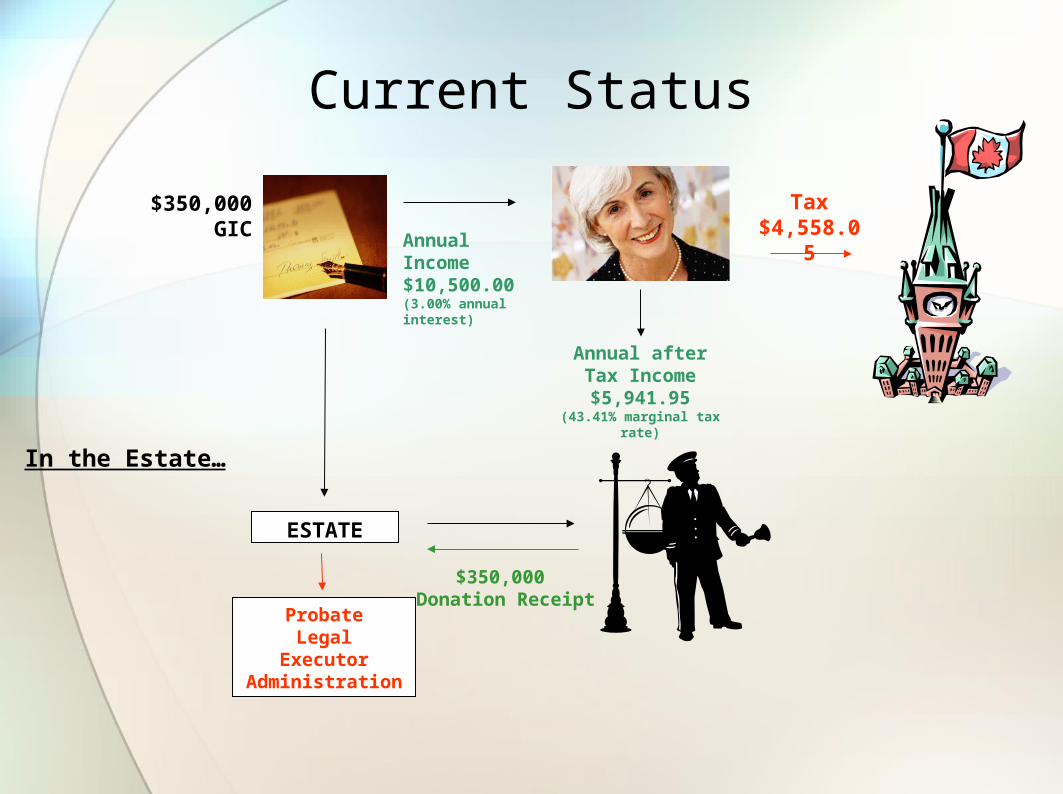

Gifts of Charitable Life Insurance• Income comprises:

• Teacher’s Pension• Interest income - $500,000 of GICs (3.00%)• RRIF• CPP• OAS is clawed back• Total Gross income - $107,022.15• Tax Payable - $32,201.86• After Tax Income - $74,820.29

Current Status$350,000

GIC Annual Income$10,500.00(3.00% annual interest)

Tax$4,558.05

Annual after Tax Income

$5,941.95(43.41% marginal tax rate)

ESTATE

ProbateLegal

ExecutorAdministration

In the Estate…

$350,000 Donation Receipt

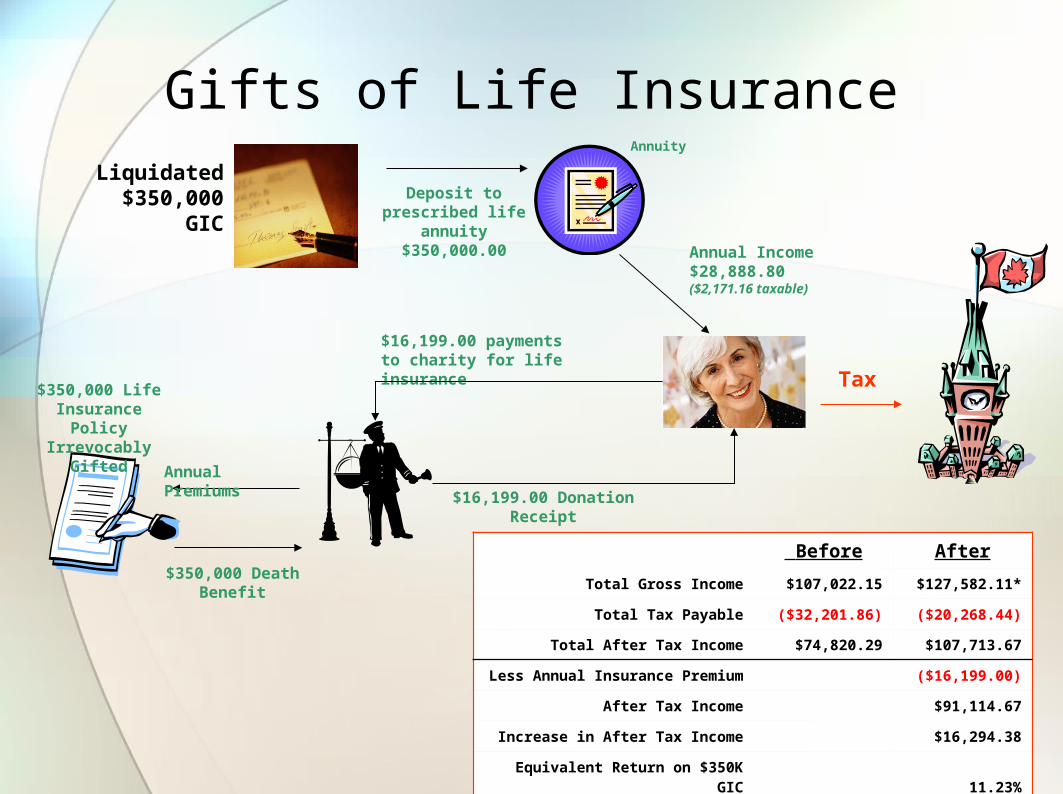

Gifts of Life InsuranceLiquidated

$350,000GIC

$16,199.00 payments to charity for life insurance

Deposit to prescribed life

annuity$350,000.00

Annuity

Annual Income$28,888.80($2,171.16 taxable)

Before AfterTotal Gross Income $107,022.15 $127,582.11*

Total Tax Payable ($32,201.86) ($20,268.44)

Total After Tax Income $74,820.29 $107,713.67

Less Annual Insurance Premium ($16,199.00)

After Tax Income $91,114.67

Increase in After Tax Income $16,294.38

Equivalent Return on $350K GIC 11.23%

*$98,693.31 taxable income

Annual Premiums$16,199.00 Donation

Receipt

$350,000 Death Benefit

$350,000 Life Insurance Policy

Irrevocably Gifted

Tax

Did We Achieve Marie’s Goals?

1) Would like to increase annual charitable giving (additional $5,000) without affecting income• Increased after tax income by $16,294.38

Yes No

2) Doesn’t want to incur risk with investments• Insured annuity – no investment risk

4) Wants to keep estate in tact for heirs• All estate values are kept in tact for heirs through

insurance and other assets

3) Wants to keep a portion of GICs for future liquidity• Still has $150,000 in GICs

Creating a Legacy:Life Insurance & Charitable

GiftingJohn Jordan, CFP

Insurance & Estate Planning Specialist

Case Study• Bill & Jane are retired school teachers in their early

70s• Both have good pensions, CPP, OAS payments, and

investment income. • Have just started taking the minimum on their RRIF• Have an income property and about $300k in an open

investment account• Open investments will continue to grow as they are

not needed for lifestyle• Projected tax liability at mortality (excluding income

property) is just over $100,000• No Charitable Intentions in their estate, but after

discussing estate benefits and asset preservation, they wanted to look into what could be done.

Case Study• Insurance plays a significant role in the estate

planning process• $300,000 Joint Last to Die

• Re-arrange beneficiary designations on RRIF• Provide direction to executors in the estate to gift the

amount necessary to bring taxable income to (or close to) $0

Creating a Legacy:Life Insurance & Charitable

GiftingJohn Jordan, CFP

Insurance & Estate Planning Specialist