creating a healthy plan for retirement 2019 (pdf) · (jpms), a registered broker-dealer and...

TRANSCRIPT

1

Creating a “Healthy” Plan for RetirementStrategies for paying your share of health care costs

INVESTMENT AND INSURANCE PRODUCTS ARE:• NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT A DEPOSIT OR

OTHER OBLIGATION OF, OR GUARANTEED BY, JPMORGAN CHASE BANK, N.A. OR ANY OF ITS AFFILIATES • SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

Average annual out-of-pocket health care costs per retiree

$18,360

$5,210

Age 65 (2018) Age 85 (2038)$0

$5,000

$10,000

$15,000

$20,000

Source: J.P. Morgan Asset Management, Guide to Retirement, 2018

INCLUDES:

• Medicare Part B (doctors, tests and outpatient care)

• Medicare Part D (prescription drugs)• Medigap plan • Dental, vision and hearing

DOESN’T INCLUDE:

• Long-term care

Health care isn’t only one of the biggest retirement expenses—it’s also the toughest to budget. How long will you live? What kind of care will you need? Where will prices be then?

Because it’s hard to know those answers, it can also be hard to know how much to set aside for health care. You don’t want to save so little that you can’t cover the costs or so much that it jeopardizes other goals.

.

How much is enough?Medicare isn’t free and doesn’t cover everything, which is why most retirees buy a supplemental “Medigap” policy to fill the holes. But neither of those plans covers most dental, vision and hearing services. When you add it all up, the average 65-year-old will pay about $5,200 this year—and costs are expected to more than triple to $18,360 by age 85, without even including the cost of long-term care.

Key takeaways ¡ Health care costs are hard to predict but must be included in a retirement plan.

¡ For a current 65-year-old, annual health care expenses are estimated at $5,200, rising to $18,360 by age 85.

¡ A written plan should reflect monthly savings, annual health care inflation and long-term care needs not covered by Medicare.

¡ Starting early can help reduce insurance costs and increase time for investment growth potential

2

Five tips when planning and investing for health care costs

1. Put your plan on paperMany people don’t think about health care when they’re working, but that’s the time to start preparing for a future without an employer’s medical plan. Consider consulting with a J.P. Morgan Advisor to develop a Customized Financial Analysis1 that clearly shows how health care costs impact your overall financial picture.

Few life experiences can derail a retirement faster than large, unexpected medical bills. An advisor can help you create realistic expectations for costs and a strategy to help pay for them.

Four out of five workers have not calculated how much they’ll need for health care during retirement.

Source: 2018 Retirement Confidence Survey, Employee Benefit Research Institute and Greenwald & Associates

FACTORS TO CONSIDER WHEN PLANNING FOR HEALTH CARE COSTS

Health statusCosts shown in the chart (on page 1) are averages. Plan to pay more if you need extra care or expensive prescriptions.

Marital statusThe chart (on page 1) shows costs per person; couples should prepare to pay more.

Current ageCosts shown are for people already in retirement. If you are under 65, your expenses will likely be higher due to health care inflation.

Life expectancyDepending on your family history and lifestyle, you may live longer than average—and incur higher expenses.

2. Expect health care to rise faster than other expensesRetirement planning experts at J.P. Morgan recommend assuming a 6.5%2 annual inflation rate when estimating health care spending throughout retirement, which is much higher than overall cost-of-living increases. At that pace, your medical outlays would double every 11 years.

You can’t always predict health care costs, but you can prepare for them. A sound plan combines investments with insurance to help pay the bills without jeopardizing retirement.

3

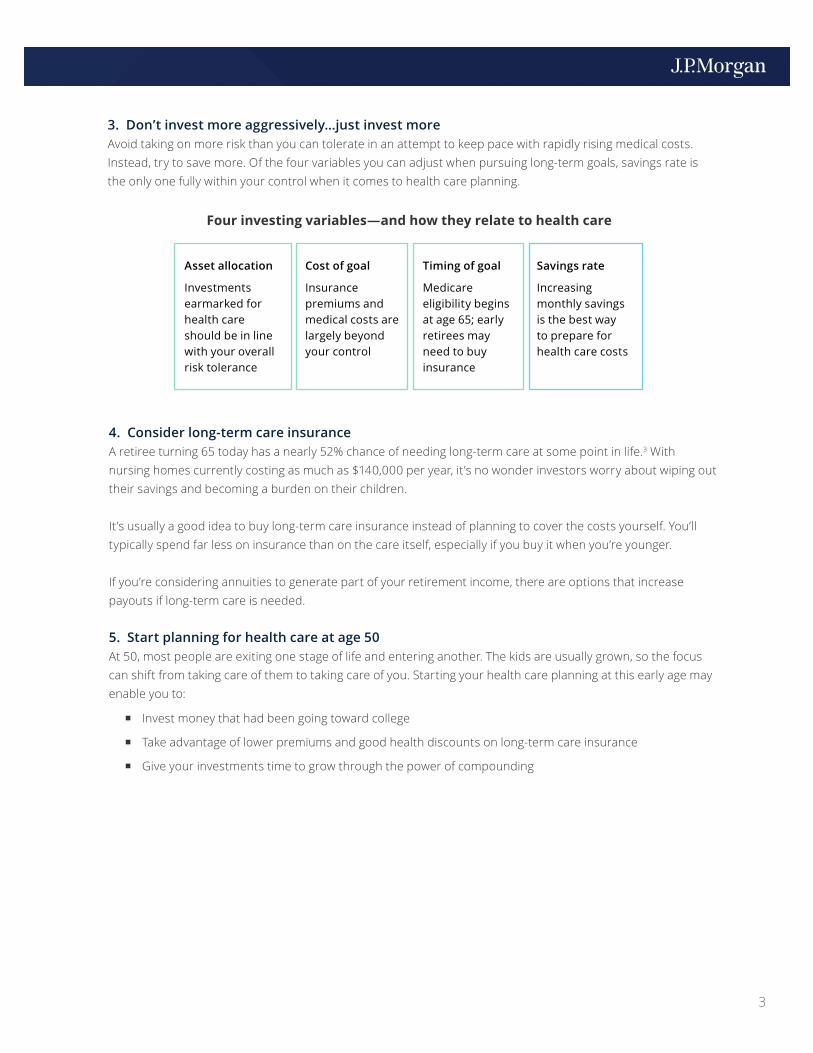

3. Don’t invest more aggressively…just invest moreAvoid taking on more risk than you can tolerate in an attempt to keep pace with rapidly rising medical costs. Instead, try to save more. Of the four variables you can adjust when pursuing long-term goals, savings rate is the only one fully within your control when it comes to health care planning.

Four investing variables—and how they relate to health care

Asset allocation

Investments earmarked for health care should be in line with your overall risk tolerance

Cost of goal

Insurance premiums and medical costs are largely beyond your control

Timing of goal

Medicare eligibility begins at age 65; early retirees may need to buy insurance

Savings rate

Increasing monthly savings is the best way to prepare for health care costs

4. Consider long-term care insuranceA retiree turning 65 today has a nearly 52% chance of needing long-term care at some point in life.3 With nursing homes currently costing as much as $140,000 per year, it’s no wonder investors worry about wiping out their savings and becoming a burden on their children.

It’s usually a good idea to buy long-term care insurance instead of planning to cover the costs yourself. You’ll typically spend far less on insurance than on the care itself, especially if you buy it when you’re younger.

If you’re considering annuities to generate part of your retirement income, there are options that increase payouts if long-term care is needed.

5. Start planning for health care at age 50At 50, most people are exiting one stage of life and entering another. The kids are usually grown, so the focus can shift from taking care of them to taking care of you. Starting your health care planning at this early age may enable you to:

¡ Invest money that had been going toward college

¡ Take advantage of lower premiums and good health discounts on long-term care insurance

¡ Give your investments time to grow through the power of compounding

4

1 The Customized Financial Analysis referenced is a tool that provides an additional resource in the evaluation of the potential risks and returns of investment choices. The projections or other information generated by the Customized Financial Analysis regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results.

2Source: J.P. Morgan Asset Management, Guide to Retirement, 20183Source: Morningstar, August 2018

Not all investment ideas referenced are suitable for all investors. Investing involves market risk, including the possible loss of principal. There is no guarantee that investment objectives will be reached. Diversification does not guarantee a profit or protect against a loss.

Opinions and estimates offered constitute our judgment as of the date of this material and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described herein may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Investment products and services are offered through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment advisor, member of FINRA and SIPC. Annuities are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. JPMS, CIA and J.P. Morgan Chase Bank, N.A. are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

© 2019 JPMorgan Chase & Co.

Next steps: Put these ideas into action

¡ Whether you invest on your own or with a J.P. Morgan Advisor, no retirement strategy is complete without accounting for health care.

¡ By starting early, planning carefully and saving generously, you can take the steps needed to prepare for your share of the costs while protecting against the unknown.

MORE FACTORS TO CONSIDER WHEN PLANNING FOR HEALTH CARE COSTS

IncomePremiums for Medicare Parts B and D are based on income—the more you have, the more you’ll pay.

GenderWomen typically live longer, meaning more years of expenses and a greater likelihood of needing long-term care not covered by Medicare.

State of residenceMedical costs can vary widely by state, especially for nursing homes, assisted living facilities and other long-term care.

Medicare reformsWith Medicare projected to begin running out of money in 2026, any reforms to the system are likely to increase your share of the costs.*

*Source: 2018 Medicare Trustee Report