crac bulletin - dsf.gov.mo · committee for the registry of auditors and accountants 1 january 2016...

TRANSCRIPT

Committee for the Registry of Auditors and Accountants 1 January 2016

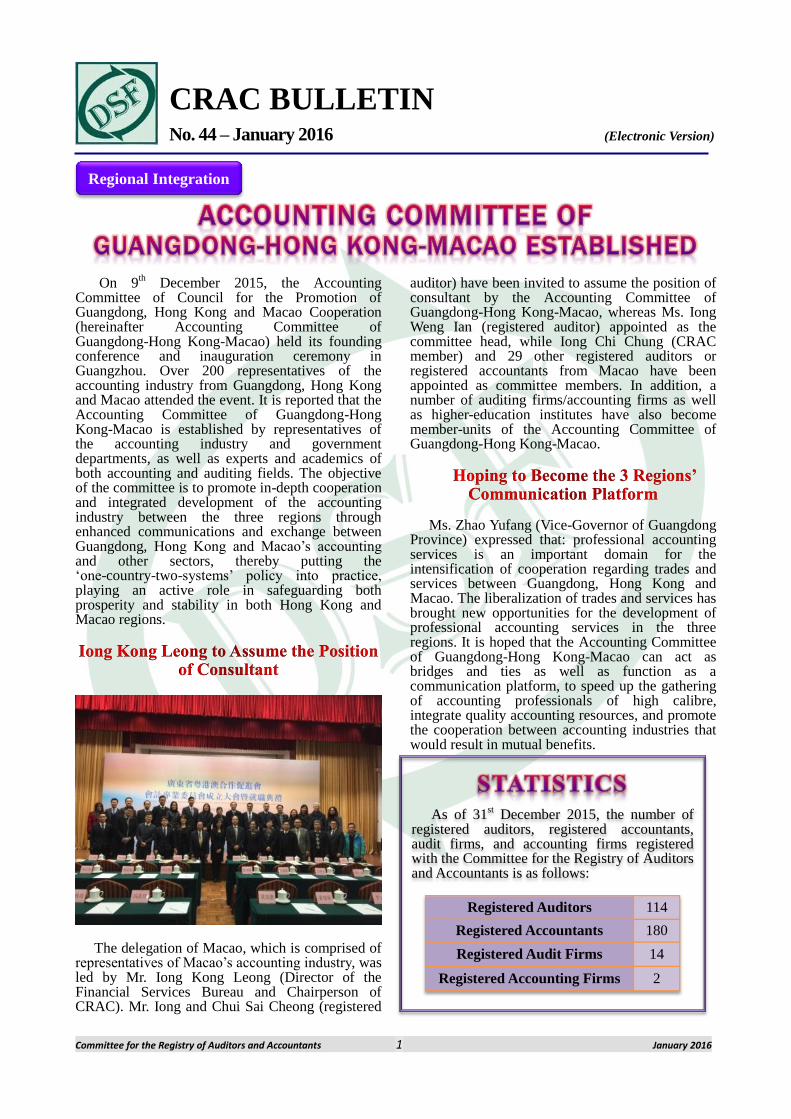

As of 31st December 2015, the number of

registered auditors, registered accountants, audit firms, and accounting firms registered with the Committee for the Registry of Auditors and Accountants is as follows:

Registered Auditors 114

Registered Accountants 180

Registered Audit Firms 14

Registered Accounting Firms 2

CRAC BULLETIN No. 44 – January 2016 (Electronic Version)

On 9th December 2015, the Accounting

Committee of Council for the Promotion of Guangdong, Hong Kong and Macao Cooperation (hereinafter Accounting Committee of Guangdong-Hong Kong-Macao) held its founding conference and inauguration ceremony in Guangzhou. Over 200 representatives of the accounting industry from Guangdong, Hong Kong and Macao attended the event. It is reported that the Accounting Committee of Guangdong-Hong Kong-Macao is established by representatives of the accounting industry and government departments, as well as experts and academics of both accounting and auditing fields. The objective of the committee is to promote in-depth cooperation and integrated development of the accounting industry between the three regions through enhanced communications and exchange between Guangdong, Hong Kong and Macao‟s accounting and other sectors, thereby putting the „one-country-two-systems‟ policy into practice, playing an active role in safeguarding both prosperity and stability in both Hong Kong and Macao regions.

The delegation of Macao, which is comprised of

representatives of Macao‟s accounting industry, was led by Mr. Iong Kong Leong (Director of the Financial Services Bureau and Chairperson of CRAC). Mr. Iong and Chui Sai Cheong (registered

auditor) have been invited to assume the position of consultant by the Accounting Committee of Guangdong-Hong Kong-Macao, whereas Ms. Iong Weng Ian (registered auditor) appointed as the committee head, while Iong Chi Chung (CRAC member) and 29 other registered auditors or registered accountants from Macao have been appointed as committee members. In addition, a number of auditing firms/accounting firms as well as higher-education institutes have also become member-units of the Accounting Committee of Guangdong-Hong Kong-Macao.

Ms. Zhao Yufang (Vice-Governor of Guangdong Province) expressed that: professional accounting services is an important domain for the intensification of cooperation regarding trades and services between Guangdong, Hong Kong and Macao. The liberalization of trades and services has brought new opportunities for the development of professional accounting services in the three regions. It is hoped that the Accounting Committee of Guangdong-Hong Kong-Macao can act as bridges and ties as well as function as a communication platform, to speed up the gathering of accounting professionals of high calibre, integrate quality accounting resources, and promote the cooperation between accounting industries that would result in mutual benefits.

Regional Integration

Committee for the Registry of Auditors and Accountants 2 January 2016

In November 2015, CRAC issued notification letters to all registered auditors and registered accountants regarding renewal of professional ID cards. In accordance with the corresponding laws, professional ID cards of registered auditors and registered accountants must be renewed on or before 1

st February each year. Applicants are

required to submit the application for renewal of professional ID cards during office hours at least 30 days prior to the renewal date. Applications should be submitted to any of the following locations: 1. CRAC office; 2. Recepção de Expediente (located on the 1

st Floor of the DSF Building); 3. „Taxation

Division‟ at the Integrated Services Centre; 4. Taipa Service Centre.

Upon receiving the applications, CRAC would notify each applicant (via registered mail) regarding the arrangements for fee payment and ID card collection. Meanwhile, applicants are particularly reminded that CRAC would only accept late applications for renewal up to 31

st March) under

special circumstances and with sufficient justifications, but applicants would be subject to an additional charge up to thrice the renewal fees; CRAC would not accept applications for renewal submitted after 31

st March, and failing to submit the

application in due time will result in automatic suspension of registration.

For enquiries, please contact CRAC office on 8599 5343 or 8599 5344.

In the fourth quarter of 2015, CRAC collaborated with foreign professional institutes in hosting four training sessions surrounding the topics of latest international trends and corporate risk management.

On 13th October 2015, the “Anti-Money

Laundering Trends‟ seminar presented the correlation between mutual evaluation and regional risk assessment. In addition, the seminar also presented Mainland China and Hong Kong‟s corresponding regulatory trends, and the instructor used case studies to help students better understand the issues.

It is reported that, the objective of the Financial

Action Task Force (FAFT) is to establish standards, promote effective implementation of laws, legislations and operational measures to combat money laundering, financing of terrorism as well as other threats to the integrity/completeness of international financial system. The content of the mutual evaluation, which correlates with FATF‟s 40

recommendations and 11 direct objectives, can be categorized into: technical compliance and effectiveness. The key speaker focused primarily on explaining two objectives: 1. Appropriate regulatory, monitoring and management measures that should be adopted by the regulator; 2. Preventive measures and mechanisms for reporting suspicious transactions equipped by financial institutions.

According to FATF‟s recommendations, each

country or region is required to identify, evaluate and understand its region‟s risks (cont. p3)

Reminder

Training News

Committee for the Registry of Auditors and Accountants 3 January 2016

(from p2:Training News)

associated with money laundering and financing of terrorism; meanwhile, they should adopt appropriate measures in response to the risk level i.e. adopting a risk-based approach. Hence, each country or region must perform a National Risk Assessment (NRA). On the basis of NRA, the FATF or Asia Pacific Group on Money Laundering (APG) would carry out the joint evaluation. The schedule for APG‟s field evaluation in Macao has already been planned in the 4

th quarter of 2016. For more

information, please visit the FATF website (http://www.fatf-gafi.org).

The “Liquidity and Credit Risk Management” seminar was held on 27

th October 2015, which was

presented with the neighbouring region‟s authorized institutions as background topic. (Editor‟s note: according to the corresponding regulations of Hong Kong Monetary Authority (HKMA), Hong Kong implements a three-tier authorization system, which can be categorized into licensed banks, restricted licensed banks, and deposit taking companies, which are collectively known as authorized institutions.

The content of liquidity management is primarily sourced from HKMA‟s Liquidity Risk Management (statutory guideline). This guideline provides detailed regulations regarding definition, source, and supervisory approach to liquidity risk as well as statutory liquidity ratio requirements. The content of credit risk management is sourced from another statutory guideline: Sound Systems and Controls for Credit Risk Management. This guideline provides detailed regulations regarding credit risk environment, procedures for approving credits, credit administration, measurement and monitoring, as well as controls over credit risk. These two guidelines are available from HKMA‟s website (http://www.hkma.gov.hk).

The “Awareness on OECD‟s Common Reporting Standard‟ seminar was held on 12

th

November 2015. During the seminar, the key speaker presented the specific requirements set in Common Reporting Standard (CRS), the proposed implementation timetable from each country or region, as well as the main divergence between this Standard and the existing system.

It is reported that OECD (Organization of

Economic Cooperation and Development)

published the Standard for Automatic Exchange of Financial Account Information, of which CRS forms a major part of the Standard. CRS is a new set of global standards that will require financial institutions to review and collect information that will enable them to identify the tax residency of account holders and to provide relevant information to the local tax administration authorities on an annual basis. In September 2014, Macao SAR has expressed its support to the new Standard. In order to fulfill its international obligations, Macao SAR will soon initiate the legislative procedures necessary for the amendments of relevant domestic laws to ensure timely compliance with the new Standard.

At the conclusion of the seminar, participants

expressed that they found the seminar very informative, as the content is related to the latest trend in international tax cooperation and its expected impact; in addition, the seminar has also raised participants‟ interest on this topic since Macao will soon perform the corresponding OECD obligations. For more information related to CRS, please visit the OECD website (http://www.oecd-ilibrary.org/taxation/standard-for-automatic-exchange-of-financial-account-information-for-tax-matters_9789264216525-en).

The “Challenges of Accounting and Auditing in the Hospitality Industry” seminar was held on 17

th

November 2015. The seminar kicked off by looking at various data regarding Macao‟s hospitality industry such as revenue trends and structure, analysis of macro-economic factors, and presentation of the general situation faced by Macao‟s hospitality industry; the seminar is then followed by a presentation of common risks faced by hospitality industry practitioners and related internal control as well as points to note when preparing corresponding financial statements.

The seminar also focused heavily on analyzing room revenue, food and beverage revenue, risk associated with construction-in-progress (CIP) and key internal controls. With regard to revenue, the speaker emphasized the importance of conferring power and review of corresponding activities such as price changes, preparation of cash and credit card reconciliations, transfer of revenue data between different systems (e.g. from management to accounting system), and adjustments of revenue among others. As for CIPs, the speaker presented the risks and key internal controls from the tendering process, ordering, payment all the way to recognition of CIPs.

Committee for the Registry of Auditors and Accountants 4 January 2016

The Macao venue for the People‟s Republic of China Certified Public Accountants Uniform Examinations 2015 (hereinafter CICPA Examinations) was successfully held on 17-18 October 2015. The Macao venue continued to hold a site for professional phase examinations this year, which took place at the Macao Productivity and Technology Transfer Centre. The professional phase examination is comprised of six subjects: Accounting, Auditing, Financial Management and Cost Management, Economic Law, Taxation Law, as well as Corporate Strategies and Risk Management. Examinations are held under a closed-book electronic format. The duration for each subject ranges between 2 to 3 hours.

The CICPA Examination is a national licensing examination, held in either September or October each year. The exams have been held in e-format since 2012, in other words, candidates receive questions and provide answers directly through computers.

Approximately 800,000 candidates have applied to take the examinations in 2015, recording over 2 million participants in all subjects combined. The examinations have venues in all provinces,

Hong Kong and Macao. Starting 2010, an examination venue has been

established in Macao each year, offering much convenience to persons wishing to take CICPA Examinations in Macao. The Union of Associations of Professional Accountants of Macao is the examination representation office, while CRAC offers assistance with regard to the coordination of site set-up and promotional activities.

Online application for the CICPA Examinations 2016 will be open between 1-30 April 2016; actual examinations are scheduled as follow: integrated phase and English test to take place on 27

th August 2016, while professional phase to take

place on 15-16 October 2016. Please refer to the exam regulations 2016 for more information.

The examination regulations 2016 are expected to be available in March (in Chinese language only). Please visit the Chinese Institute of Certified Public Accountants (CICPA) website regularly for updates. Alternatively, please contact the CRAC office on 8599 5350 or the Union of Associations of Professional Accountants of Macao on 2835 6856 for enquiries.

CRAC hosts two rounds of licensing exams each year. Round II of the 2015 licensing examination for first-time registration and reinstatement of „registered auditors‟ and „registered accountants/accounting technicians‟ had successfully taken place between 28

th November

and 13th December 2015 at the training centre for

civil servants, located on the 6th Floor of Cheng

Feng Commercial Centre, Alameda Dr. Carlos d‟Assumpção. A total of 91 candidates have taken this round of exams (13 took exams for auditors, 78 for accountants). The table below presents data for each subject.

Date Subject

Number of Candidates

Registered Auditors

Registered Accountants

28th November 2015

General and Financial Accounting / General Accounting

3 50

29th November 2015 Macao Taxation Law 11 62

6th December 2015 Cost Accounting 1 38

12th December 2015 Commercial Code 11 47

13th December 2015 Auditing Standards 1 -

CICPA News

Examination News

Committee for the Registry of Auditors and Accountants 5 January 2016

At present, the „Statute of Auditors‟, approved by Decree-Law No.71/99/M of 1

st November, and

the „Statute of Registered Accountants‟, approved by Decree-Law No.72/99/M of 1

st November are

the governing regulations for the auditing and accounting professions of Macao. The two statutes provide regulations for auditors and accountants in terms of professional requirements, practice, setting-up firms, disciplinary responsibilities and criminal responsibilities. In addition, the „Code of Ethics for Registered Auditors‟, approved by Administrative Regulation No.36/2004 provides regulations for auditors and auditing firms‟ ethical conducts. We shall be looking at a couple of issues commonly encountered during practice. Please refer to the statutes and code of ethics referred above for specific regulations. Alternatively, please contact the CRAC office for enquiries.

Ans: Auditors and accountants are issued a professional license and professional ID card, the latter of which must be presented when they are dealing with the Financial Services Bureau in the capacity as auditors or accountants. In addition, it should be noted that, unless auditors and

accountants wish to update corresponding information, professional licenses need not be renewed each year; professional ID cards, however, are required to be renewed by 1

st February each

year.

Ans: No. However, if the corresponding professional qualification in auditing/accounting obtained abroad permits the individual to practice (in that region), they may apply to be exempted from taking certain exam subjects or have their internship obligations waved/shortened (if applicable). For instance, persons with practical qualifications in auditing obtained abroad may apply to be exempted from taking various subjects (such as General and Financial Accounting, Cost Accounting, and Auditing Standards) as well as having their internship obligations waved. Nevertheless, applicants are still required to pass certain exams deemed necessary by CRAC (such as Macao Taxation Law and Commercial Code in general) before they could be registered as auditors.

CRAC and the Union of Associations of Professional Accountants of Macao visited two accounting organizations in Shanghai (Shanghai Institute of Certified Public Accountants and Shanghai National Accounting Institute) on 17-19 October 2015. Mr. Yung Chi Chung and Lai Hang Sun Hans (CRAC members), who participated in these visits, consider the experience to be very fruitful. They expressed that: these visits allowed them to gain a much better insight into Shanghai‟s regulatory work on listed companies and Shanghai‟s training for the accounting profession, as well as to establish liaison mechanism with the two organizations; they believe that the knowledge they receive from this visit could be applied to CRAC‟s future work. (Editor‟s note: the Shanghai National Accounting Institute (SNAI) was established in September 2000, which is a direct subordinate unit of the Ministry of Finance. At present, the Institute is committed to provide master degree programmes for both accounting and auditing professions as well as advanced-level continuous education courses. Please visit the Institute‟s website (http://www.snai.edu) for more details.)

The China-Japan-Korea Accounting Standards Setters‟ Meeting 2015 was held in Seoul, Korea on

23rd

November 2015. Mr. Yung Chi Chung (CRAC member), along with a CRAC staff, attended the meeting to gain insight into the latest development of standard setting and research projects of the three countries. With regard to research projects, the meeting focused on discussing two projects by the International Accounting Standards Board (IASB) – „Pollutant Pricing Mechanism‟ and „Conceptual Framework‟, and explored the pros and cons of research methods adopted on effect analysis for the International Financial Reporting Standards (IFRS).

The Asian-Oceanian Standard Setters Group (AOSSG) held its seventh annual meeting in Seoul on 25-26 November 2015. As a member of AOSSG, CRAC was represented by Mr. Yung Chi Chung (CRAC member) and a CRAC staff in attendance. This annual meeting was hosted by the Korea Accounting Standards Board (KASB), and representatives from AOSSG‟s 19 member organizations and IASB have attended the meeting. Main issues discussed in this meeting includes: AOSSG‟s feedback on IASB‟s key projects, joint research between AOSSG members, AOSSG strategic plan, AOSSG‟s pilot IFRS centre of Excellence (COE) programme in Nepal, and a new proposed model.

CRAC News

Practice Q & A

Committee for the Registry of Auditors and Accountants 6 January 2016

Committee for the Registry of Auditors and Accountants

Address : Rua da Sé No.30, Centro de Recursos da Direcção dos Serviços de Finanças, 1/F

Tel : (853) 8599 5343, 8599 5344 Fax : (853) 2838 9177

E-mail : [email protected] Website : http://www.dsf.gov.mo Accounting Standards Hotline

(853) 8599 5300

„The Mainland and Macao Closer Economic Partnership Agreement (CEPA) Agreement on Trade in Services‟ was signed in Macao on 28

th

November 2015. The agreement will come into effect starting 1

st June 2016. We shall briefly

present those content related to the accounting profession in this CRAC Bulletin. For more information regarding citizen treatment, regulations on restrictive measures retained and other specific issues, please visit http://www.cepa.gov.mo.

With regard to accounting, auditing and bookkeeping, Mainland China has liberalized the industry to service provider of Macao in the form of „citizen treatment‟ and „negative list‟. The specific commitment is: 1. Obligations involved: citizen treatment; 2. Restrictive measures retained: permanent residents of Macao who have acquired CPA status in China are permitted to become partners of accounting firms (established in the form of partnership) established in Mainland China, yet the controlling rights of the accounting firm must belong to residents of Mainland China. The specific requirements are based and carried out in accordance with the regulations set out by Ministry of Finance of China; Permanent residents of Macao who have become partners of a firm must have a fixed domicile in Mainland China, and must reside

in Mainland China for a period no less than six months each year.

Under the model of cross-border services, Mainland China promises to adopt a „positive list‟ as a form of liberalization for service providers of Macao. With regard to specific commitments on accounting, auditing and bookkeeping cross-border services, they shall be based on pre-existing liberalization measures referred in CEPA and its supplemental agreements, which covers CEPA, CEPA Supplemental Agreement, CEPA Supplemental Agreement V, CEPA Supplemental Agreement IX, and seven specific commitments referred in „Agreement between the Mainland and Macao on Achieving Basic Liberalization of Trade Services in Guangdong‟. For instance, „when auditors and accountants of Macao apply for practical qualifications in Mainland, their experience in auditing (duration) acquired in Macao will be regarded as equivalent to the same duration acquired in Mainland China‟, „when professional accounting practitioners of Macao whom has acquired CPA status in china apply to become partners of accounting firms established in Mainland, their experience in auditing (duration) acquired in Macao will be regarded as equivalent to the same duration acquired in Mainland China‟.

CEPA News