course title:financial statement analysis course code:mgt-537 course instructor: dr. hafiz muhammad...

TRANSCRIPT

Course Title:

Financial Statement Analysis

Course Code: MGT-537

Course Instructor:

Dr. Hafiz Muhammad Ishaq

Total Lectures: 32

Previous Lecture Summary

Statement of Cash Flows

Financial Ratios and the Statement of Cash Flows,

Practical Exercises

Today’s Lecture Topics

Statement of Cash Flows

Operating Cash Flow/Current Maturities of Long-Term

Debt and Current Notes Payable,

Operating Cash Flow/Total Debt,

Operating Cash Flow Per Share,

Operating Cash Flow/Cash Dividends

Alternative Cash Flow,

Procedures for Development of the Statement of Cash Flows

Practical Exercises

Financial Ratios and the Statement of Cash Flows

• Statement of cash flows is relatively new– Required presentation began in 1987

• Cash flow financial ratios were slowly developed

• Traditional ratios relate balance sheet to income statement

Operating Cash Flow/Current Maturities of Long-Term Debt and Current Notes Payable

• Indicates a firm’s abilities to meet its current maturities of debt

• Higher ratio indicates better liquidity

Operating Cash Flow

Current Maturities of Long-Term Debtand Current Notes Payable

Operating Cash Flow to Total Debt

• Indicates a firm’s ability to cover total debt with the yearly operating cash flow

• Conservative approach is to include all possible balance sheet debt

Operating Cash Flow

Total Debt

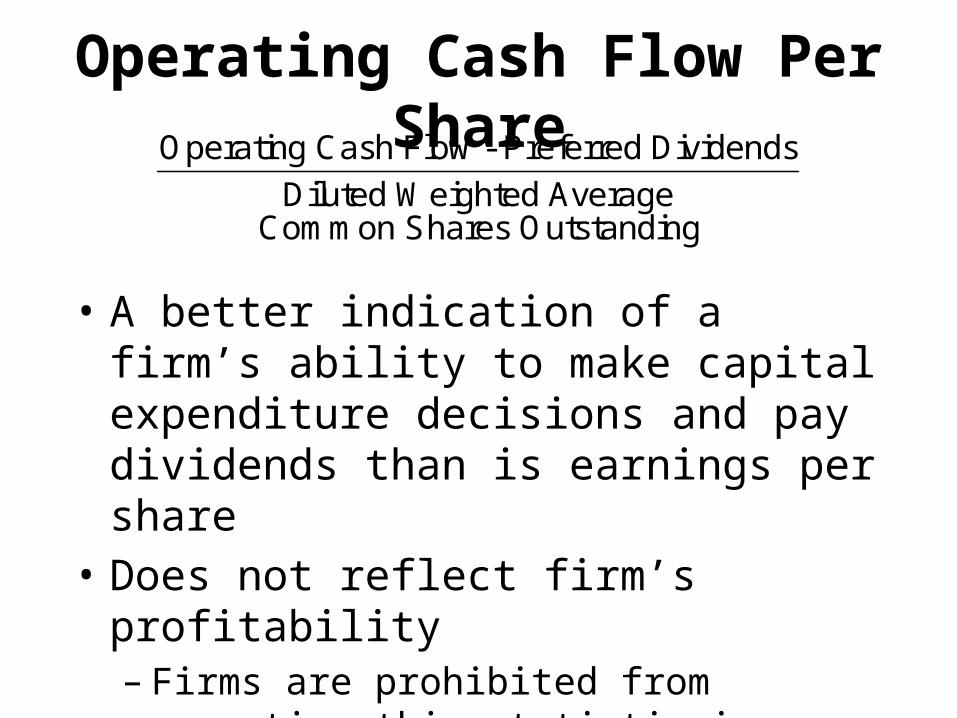

Operating Cash Flow Per Share

• A better indication of a firm’s ability to make capital expenditure decisions and pay dividends than is earnings per share

• Does not reflect firm’s profitability– Firms are prohibited from reporting this statistic

in financial statements or in the notes thereto

Operating Cash Flow - Preferred Dividends

Diluted Weighted AverageCommon Shares Outstanding

Operating Cash Flow to Cash Dividends

• Indicates a firm’s ability to cover cash dividends with the yearly operating cash flow

Operating Cash Flow

Cash Dividends

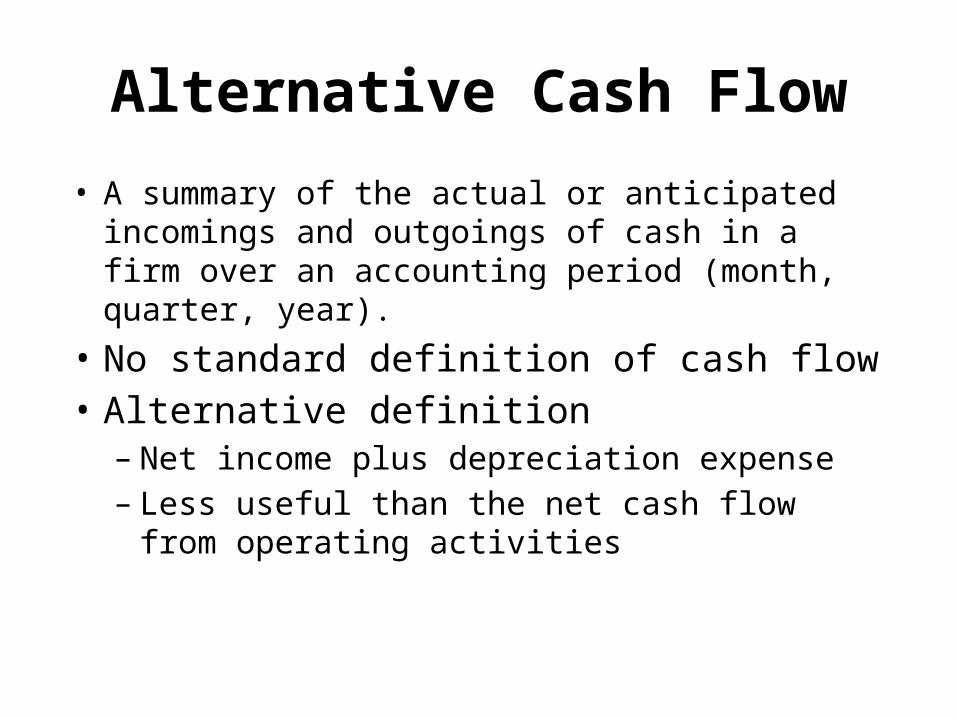

Alternative Cash Flow

• A summary of the actual or anticipated incomings and outgoings of cash in a firm over an accounting period (month, quarter, year).

• No standard definition of cash flow• Alternative definition

– Net income plus depreciation expense– Less useful than the net cash flow from

operating activities

Procedures to Develop the Statement of Cash Flows

Analyze all balance sheet accounts other than cash and cash equivalents.

Increase Decrease

Current assets Operating outflow Operating inflow

Noncurrent assets Investing outflow Investing inflow

Current liabilities Operating inflow Operating outflow

Long-term liabilities Financing inflow Financing outflow

Stockholders’ equity Financing inflow Financing outflow

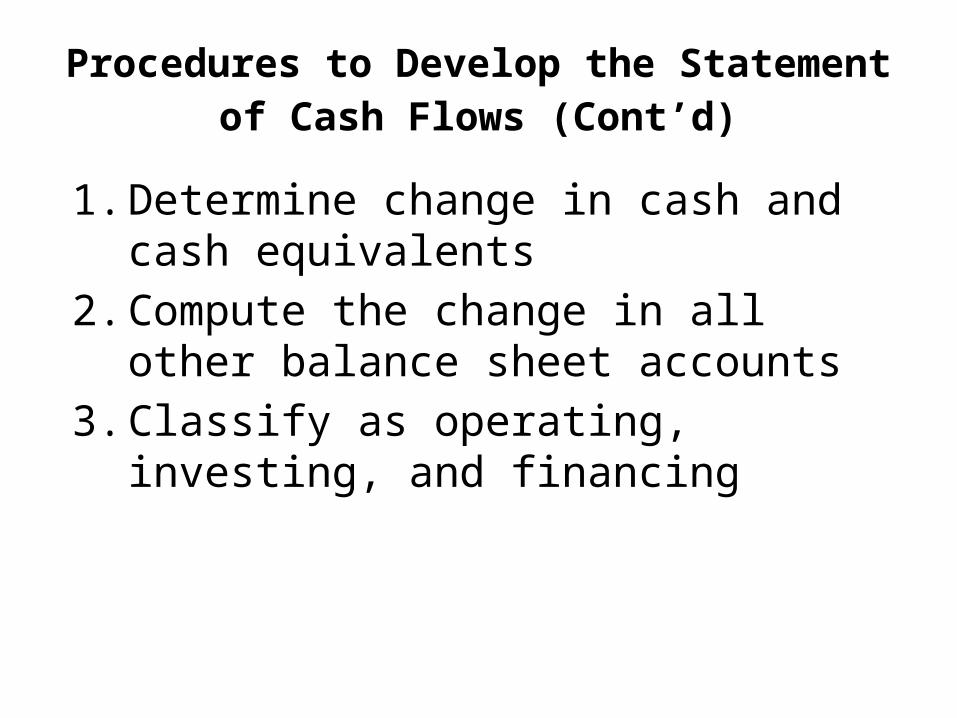

Procedures to Develop the Statement of Cash Flows (Cont’d)

1. Determine change in cash and cash equivalents

2. Compute the change in all other balance sheet accounts

3. Classify as operating, investing, and financing

Procedures to DevelopDirect Operating Cash Flows

1. Operating section describes income statement accounts as receipts or payments

2. Cash receipts• From customers• From other operating sources

3. Cash payments• For merchandise• To employees• For other operating expenses

Procedures to DevelopIndirect Operating Cash Flows

1. Begin with net income2. Eliminate gains and losses that relate to

investing and financing activities3. Add back or deduct adjustments to change

accrual-based net income to cash basis• Current noncash assets• Current liabilities

Practical Exercise

Melvin CompanyBalance Sheet

December 31, 2010, and 2009

Assets 2010 2009

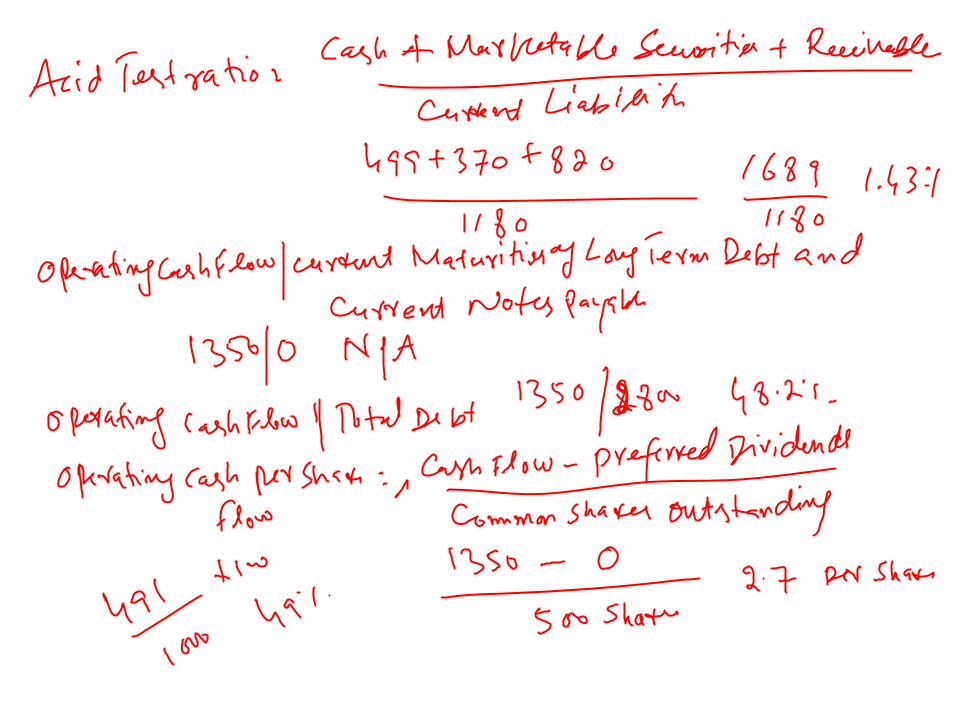

Cash $ 625 $ 499Marketable securities, 260 370Trade accounts receivable, less allowances

of 36 in 2010 and 18 in 2009 1,080 820Inventories, FIFO 930 870Prepaid expenses 230 220 Total current assets $3,125 $2,779

Investments

$ 820 $ 600

The following statements are presented for Melvin Company.

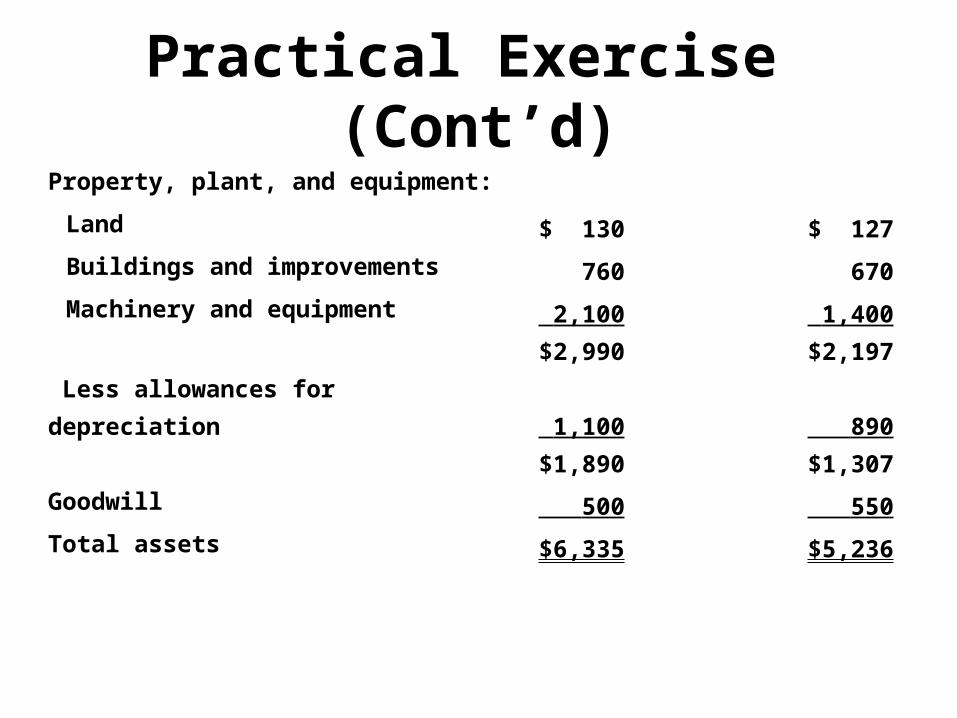

Practical Exercise (Cont’d)Property, plant, and equipment:

Land $ 130 $ 127

Buildings and improvements 760 670

Machinery and equipment 2,100 1,400 $2,990 $2,197

Less allowances for depreciation 1,100 890 $1,890 $1,307

Goodwill 500 550Total assets $6,335 $5,236

Practical Exercise (Cont’d)Liabilities and Shareholders' Equity Accounts payable $1,200 $ 900Accrued payroll 100 80Accrued taxes 300 200 Total current liabilities

$1,600 $1,180Long-term debt 900 750Deferred income taxes 300 280Shareholders' equity: Common stock 1,000 1,000 Retained earnings 2,535 2,026Total liabilities and shareholders' equity

$6,335 $5,236

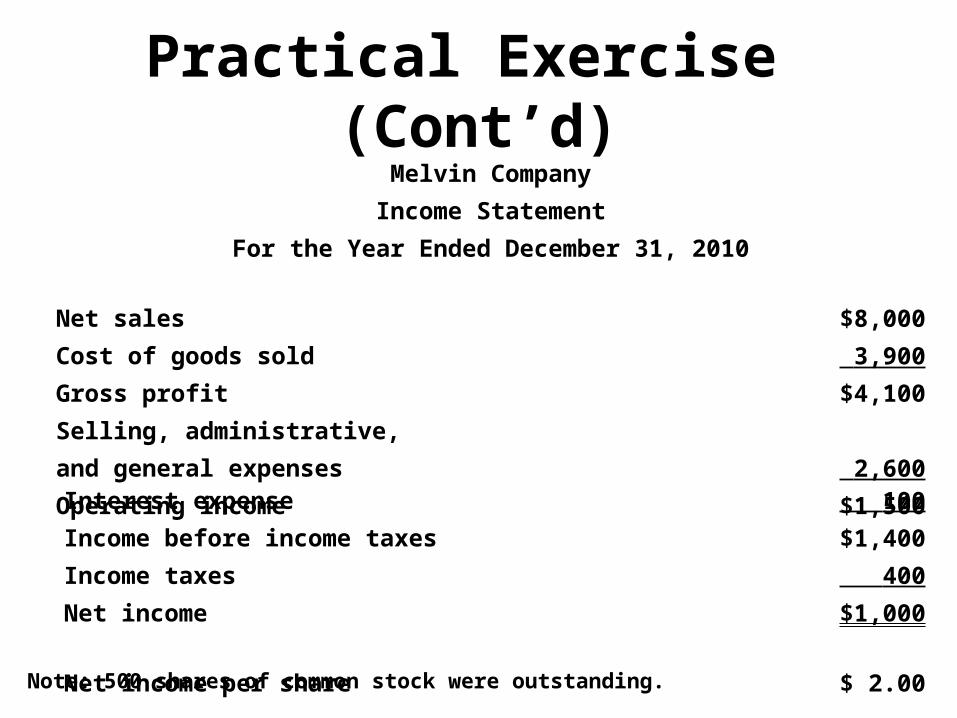

Practical Exercise (Cont’d)Melvin Company

Income StatementFor the Year Ended December 31, 2010

Net sales $8,000Cost of goods sold 3,900Gross profit $4,100Selling, administrative, and general expenses 2,600Operating income $1,500

Interest expense 100Income before income taxes $1,400Income taxes 400Net income $1,000

Net income per share $ 2.00

Note: 500 shares of common stock were outstanding.

Practical Exercise (Cont’d)Melvin Company

Statement of Cash FlowsFor the Year Ended December 31, 2010

Cash flows from operating activities:Net income $1,000 Adjustments to reconcile net income to net cash provided by Operating activities: Depreciation $210 Amortization 50 Increase in accounts receivable (260) Increase in inventories (60) Increase in prepaid expenses (10) Increase in accounts payable 300 Increase in accrued payroll 20 Increase in accrued taxes 100 350 Net cash provided by operating activities $1,350

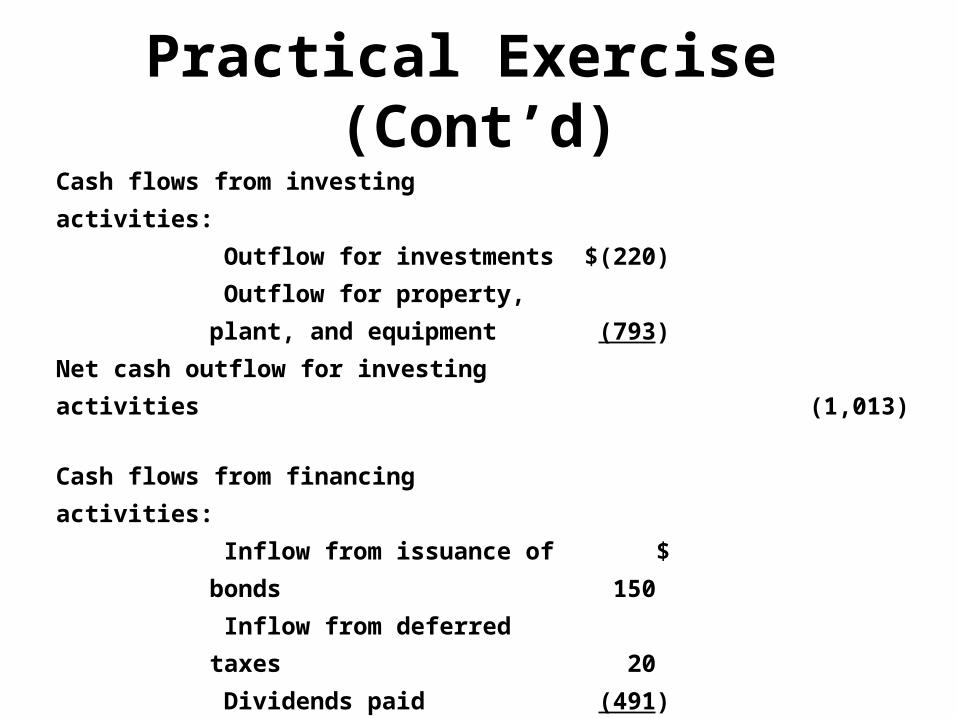

Practical Exercise (Cont’d)Cash flows from investing activities: Outflow for investments $(220)

Outflow for property, plant, and equipment (793)

Net cash outflow for investing activities (1,013)

Cash flows from financing activities: Inflow from issuance of bonds $ 150 Inflow from deferred taxes 20 Dividends paid (491)Net cash outflow for investing activities (321)Net increase in cash and cash equivalents $ 16

Practical Exercise (Cont’d)

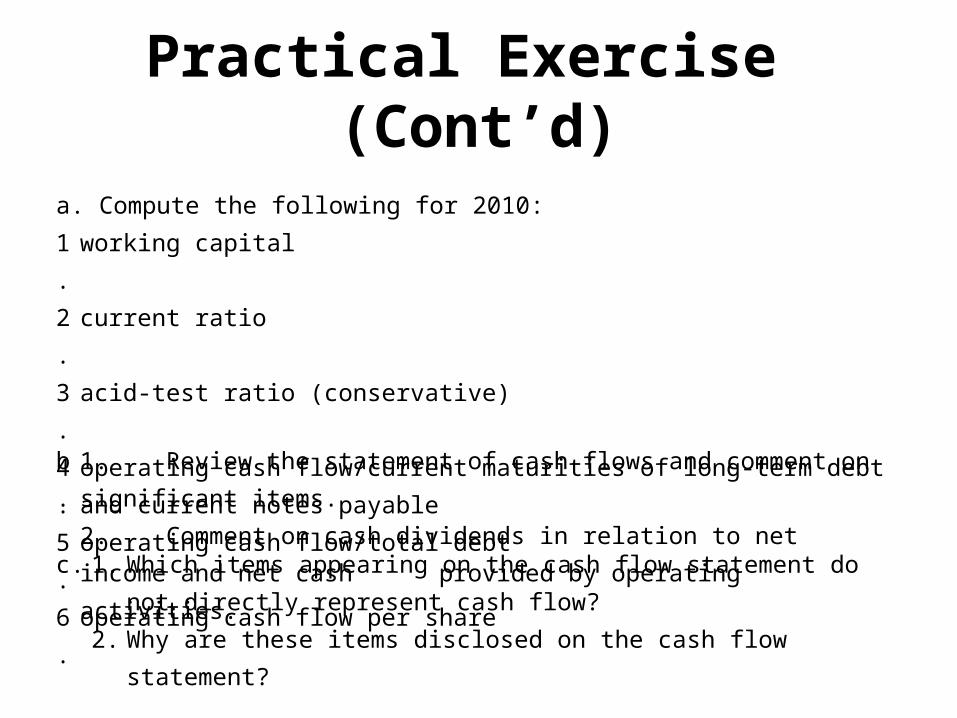

a. Compute the following for 2010:1. working capital2. current ratio3. acid-test ratio (conservative)4. operating cash flow/current maturities of long-term debt and current notes

payable5. operating cash flow/total debt6. operating cash flow per share

b. 1. Review the statement of cash flows and comment on significant items.2. Comment on cash dividends in relation to net income and net cash provided by operating activities.

c. 1. Which items appearing on the cash flow statement do not directly represent cash flow?

2. Why are these items disclosed on the cash flow statement?

B. (1)

• Net cash provided by operating activities was $1,350,

cash outflow for investing was $1,013, and net cash

outflow for financing activities was $321.

• Cash outflow for property, plant, and equipment was

significant in relation to cash provided by operations.

B. (2)

• Cash dividends represent 49% of net income and 36%

of cash provided by operating activities.

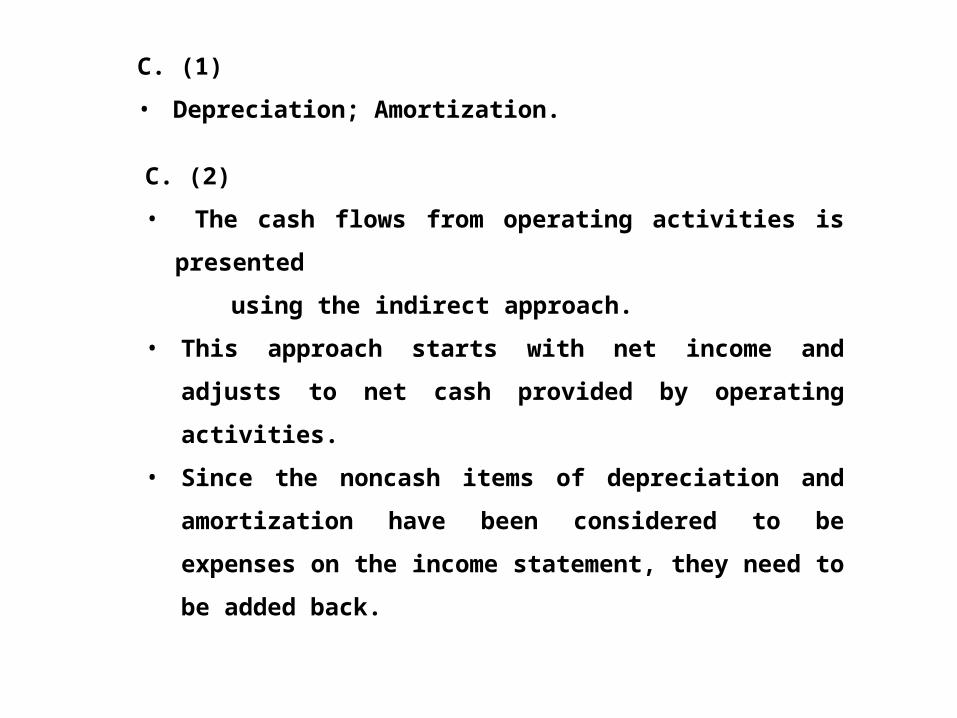

C. (2)

• The cash flows from operating activities is presented

using the indirect approach.

• This approach starts with net income and adjusts to net

cash provided by operating activities.

• Since the noncash items of depreciation and amortization

have been considered to be expenses on the income

statement, they need to be added back.

C. (1)

• Depreciation; Amortization.

Practical Exercise

Arrowbell Company is a growing company. Two years ago it decided to expand in order to increase its production capacity. The company anticipates that the expansion program can be completed in another two years. Financial information for Arrowbell Company follows:Arrowbell CompanySales and Net IncomeYear Sales Net Income2001 $2,568,660 $145,8002002 $2,660,455 $101,6002003 $2,550,180 $ 52,6502004 $2,625,280 $ 86,8002005 $3,680,650 $151,490

Practical Exercise (Cont’d)Arrowbell CompanyBalance SheetDecember 31, 2005 and 2004

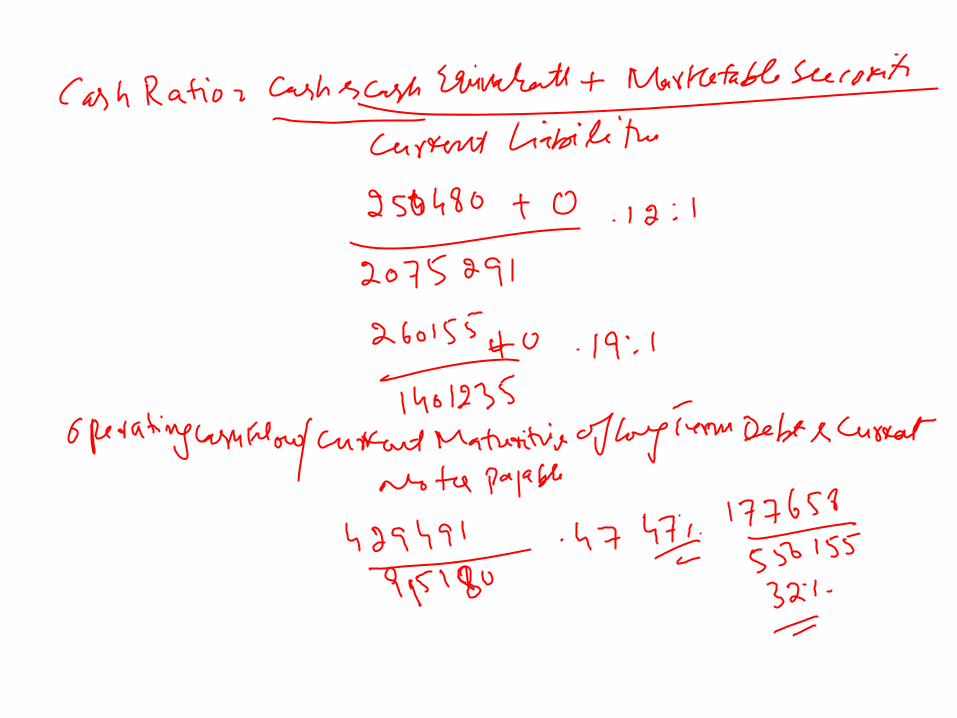

2005 2004AssetsCurrent assets:Cash $ 250,480 $260,155Accounts receivable (net) $760,950 $690,550Inventories at lower of cost or market $725,318 $628,238Prepaid expenses $ 18,555 $ 20,250Total current assets $1,755,303 $1,599,193Plant and equipment:Land, building, machinery, and equipment $3,150,165 $2,646,070Less Accumulated depreciation $ 650,180 $ 525,650Net plant and equipment $2,499,985 $2,120,420Other assets:Cash surrender value of life insurance $ 20,650 $ 18,180Other $ 40,660 $ 38,918

Total other assets $ 16,310 $ 57,098Total assets $4,316,598 $3,776,711

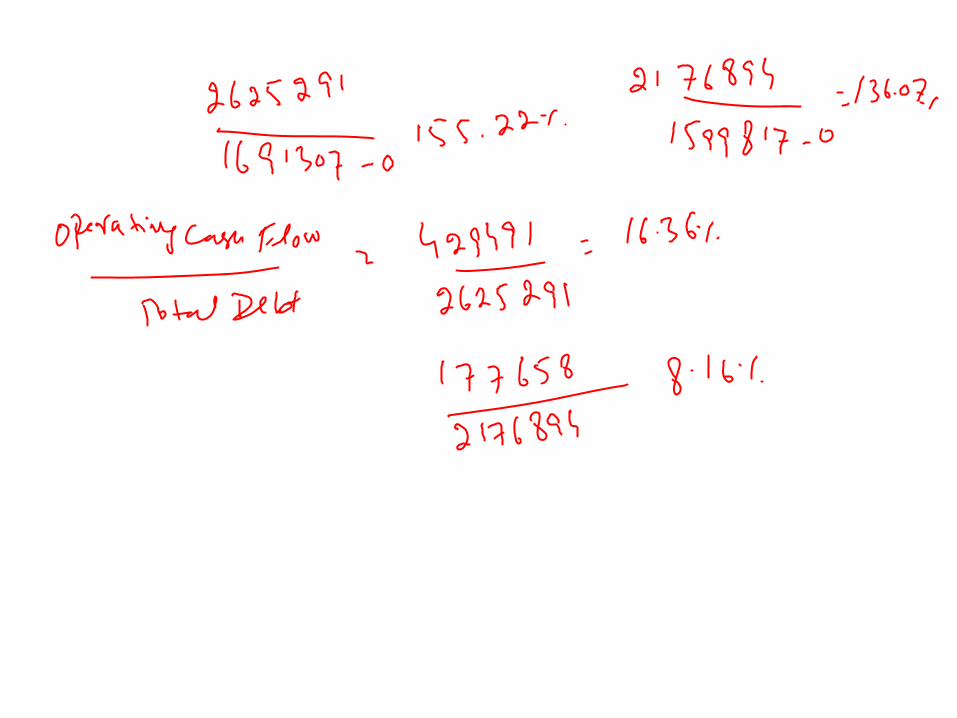

Practical Exercise (Cont’d)Liabilities and Stockholders’ EquityCurrent liabilities:Notes and mortgages payable, current portion $ 915,180 $ 550,155Accounts payable and accrued liabilities $1,150,111 $ 851,080Total current liabilities $ 2,075,291 $ 1,401,235Long term notes and mortgages payableLess current portion above $ 550,000 $ 775,659Total liabilities $2,625,291 $2,176,894Stockholders’ equity:Capital stock, par value $1.00; authorized800,000; issued and outstanding600,000 (2005 and 2004) $600,000 $600,000Paid in excess of par $890,000 $890,000Retained earnings $201,307 $109,817Total stockholders’ equity $1,691,307 $1,599,817Total liabilities and stockholders’ equity $4,316,598 $3,776,711

Practical Exercise (Cont’d)Arrowbell CompanyCash Flow statementDecember 31, 2005 and 2004Cash flows from operating activities 2005 2004Net Income $151,490 $86,800Noncash expenses revenues lossesAnd gains included in income:Depreciation 134,755 102,180Increase in accounts receivable (70,400) (10,180)Increase in inventories (97,080) (15,349)Decrease in prepaid expensesIn 2005, increase in 2004 1,695 (1,058)Increase in accounts payable And accrued liabilities 309,031 15,265Net cash provided by operating activities 429,491 177,658

Practical Exercise (Cont’d)Cash flows from investing activities: Proceeds from retirement of Property plant and equipment 10,115 3,865Purchase of property plant

And equipment (524,435) (218,650)Increase in cash surrenderValue of life insurance (2,470) (1,845)Other (1,742) (1630)Net cash used for investing activities (518,532) (218,263)Cash flows from financing activities:

Retirement of long term debt (225,659) (50,000)Increase in notes and mortgages payable 365,025 159,155Cash dividends (60,000) (60,000)

Net cash provided by financing activities 79,366 49,155Net increase (decrease) in cash $(9,675) $8,550

Practical Exercise (Cont’d)Required:

a. Comment on the short term debt position, including computations of current ratio, acid test ratio, cash ratio and operating cash flow /current maturities of long term debt and current notes payables

b. If you were a supplier to this company what would you be concerned about?c. Comment on the long term debt position including computations of the debt

ratio, debt/equity, and debt to tangible net worth and operating cash flow/total debt. Review the statement of operating cash flows.

d. If you were a banker, what would you be concerned about if this company approached you for a long term loan to continue its expansion program?

e. What should management consider doing at this point in regard to the company’s expansion program?

A. Comment

• The usual guideline for the current ratio is two to one.

• Arrowbell Company had a 1.14 to 1 ratio in 2004 and a .85 to 1

ratio in 2005.

• The usual guideline for the acid-test ratio is one to one.

Arrowbell Company had a .68 to 1 ratio in 2004 and a .49 to 1

ratio in 2005.

• The cash ratio dropped from .19 in 2004 to .12 in 2005. The

working capital in 2004 was $197,958, and in 2005 it had

declined to a negative $319,988.

• The short-term debt position appears to be very poor.

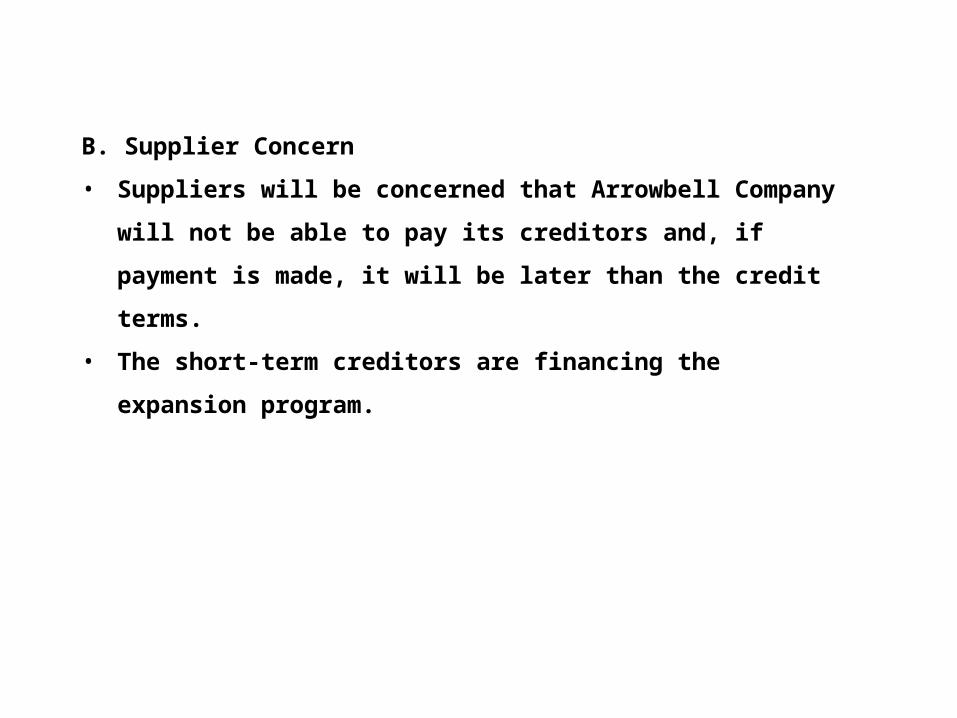

B. Supplier Concern

• Suppliers will be concerned that Arrowbell Company will not be

able to pay its creditors and, if payment is made, it will be later

than the credit terms.

• The short-term creditors are financing the expansion program.

C. Comments

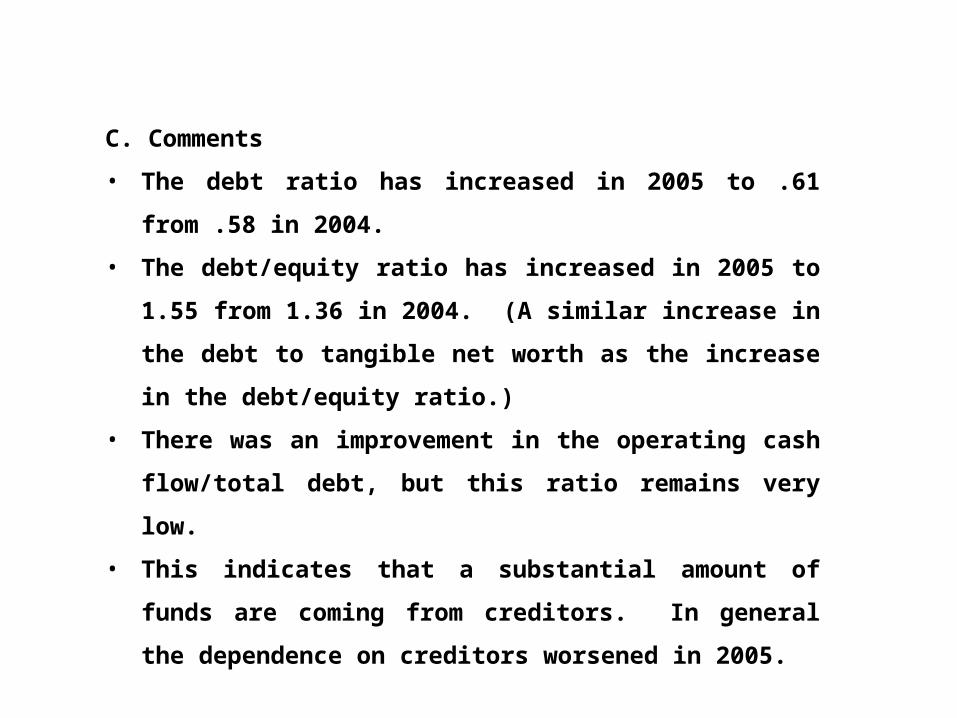

• The debt ratio has increased in 2005 to .61 from .58 in 2004.

• The debt/equity ratio has increased in 2005 to 1.55 from

1.36 in 2004. (A similar increase in the debt to tangible net

worth as the increase in the debt/equity ratio.)

• There was an improvement in the operating cash flow/total

debt, but this ratio remains very low.

• This indicates that a substantial amount of funds are

coming from creditors. In general the dependence on

creditors worsened in 2005.

Comments (Cont’d)

• Not enough information is available to compute the times

interest earned, but we can estimate this to be between 2

and 3, based on the earnings and the debt. We would like

to see the times interest earned to be higher than this

amount.

• The review of the Statement of Cash Flows indicates that

long-term creditors are going to be concerned by the use

of debt to expand property, plant, and equipment.

• They also are going to be concerned by the payment of a

dividend while the working capital is in poor condition

D. Banker Concern

• A banker would be especially concerned about the short-

term debt situation.

• This could lead to bankruptcy, even though the firm is

profitable.

• A banker would be particularly concerned why

management had used short-term credit to finance long-

term expansion.

E. Management Consideration

• Management should consider the following or a combination of the

following:

• Discontinue the expansion program at this time and get the short-

term debt situation in order. Tighten control of accounts receivable

and inventory, along with using funds from operations to reduce

short-term debt.

• Issue additional stock to improve the short-term liquidity problem and

the long-term debt situation. Because of the poor record on

profitability and the way that management has financed past

expansion, additional stock will probably not be well-accepted in the

market place at this time.

Lecture Summary

Statement of Cash Flows

Operating Cash Flow/Current Maturities of Long-Term

Debt and Current Notes Payable,

Operating Cash Flow/Total Debt,

Operating Cash Flow Per Share, Operating

Alternative Cash Flow

Procedures for Development of the Statement of Cash Flows

Practical Exercises