country profile - banking with citi | citi.com · country profile h onduras. basic data ... finance...

TRANSCRIPT

H O N D U R A S

Citi S

and

Ser

Co Over

Ba Sy

stemCle

arin

g

Sys

tem

For

Ex Con

trol

s

Inv

Oppo

Trade Regulations

COUNTRYPROFILE

ONDURASH

BASIC DATA

Capital City: Tegucigalpa

Land Area: 112,492 sq km

Population: 7.32 M (2008 estimate)

Main Towns:

Climate: Tropical on coast, moderate inland

Language: Spanish; English on Bay Islands

Measures: Metric system; also old Spanish units

Currency: 1 lempira (La) = 100 centavos. Average exchange rate in 2010: La18.9:US$1

Time: 6 hours behind GMT

Government:

1H O N D U R A S

Distrito Central * (922.2)San Pedro Sula (579.0)Choloma (188.2) La Ceiba (156.4)* Includes Tegucigalpa and Comayagüela

President Porfirio Lobo Sosa (PN) Vice-president María Antonieta de Bográn (PN)Agriculture Jacobo Regalado (PL) Culture & Sports Tulio Mariano Gonzalez-Defense Marlon Pascua (PN) Economy, Industry & Commerce Jose Lavaire

Education Marlon EscotoEnergy Emil Mahfuz HawitFinance Hector GuillenForeign Affairs

Arturo Corrales Álvarez (PDCH)

Health Arturo Bendaña (PN) Interior & Justice

Áfrico Madrid (PN)

Labor & Social Security

Felícito Ávila (PDCH) Natural Resources & Environment

Rigoberto Cuéllar Cruz (PL)

Planning & International Co-operation

Julio Raudales (PL)

Presidency

María Antonieta de Bográn (PN)Public Security

Pompeyo Bonilla (PN)

Public works, Transport & Housing

Miguel Pastor (PN)

Tourism

Nelly Jérez

Private Secretary to the Presidency

Reynaldo Sánchez (PN)

National Congress President Juan Orlando Hernández (PN)Central Bank President María Elena Mondragón (PN)

Source: The Economist Intelligence Unit as of February 2012

COUNTRY OVERVIEW

A. POLITICAL STRUCTURE

2H O N D U R A S

Official Name Republic of Honduras

Form of State Unitary republic

The Executive President, elected for a four-year term

National Legislature National Congress of 128 seats, comprising one member and one substitute member elected for every 35,000 people or fraction over 15,000 Legal System US-style Supreme Court system

National Elections November 2009 (legislative and presidential); next elections due November 2013 (legislative and presidential)

National Government Porfirio Lobo Sosa took office on January 27th 2010 following his victory in the Novem-ber 2009 election

Main Political Organizations Government: Partido Nacional (PN)Opposition: Partido Liberal (PL); Partido de Innovación Nacional y Unidad Social Demócrata (PINU-SD); Partido Demócrata Cristiano de Honduras (PDCH); Partido Unifi-cación Democrática (PUD)

Source: The Economist Intelligence Unit as of February 2012

Citi Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

The president, Porfirio Lobo, of the centre-right Partido Nacional (PN), has done much to return Honduras to normality following a coup d’état in June 2009, helping to restore international recognition as well as multilateral financing. Nevertheless, Mr. Lobo still faces a number of major challenges in strengthening the credibility of political institu-tions, combating rising crime and preventing a further polarization of the political envi-ronment, which could erode governability. The traditional two-party system, dominated by the PN and the centre-Left Partido Liberal (PL), has given way to a more fractured political environment, most notably as a result of the split between the former president, Manuel Zelaya (2006-09) and the PL, as well as the creation of his new party, Libertad y Refundación (LIBRE), which is expected to garner the support of the radical left. Although the constitution prevents him from running for president, Mr. Zelaya will retain a dominant position within his party, as he seeks to unite his support base and present LIBRE as a strong contender for the 2013 election. With the PL suffering some defec-tions to LIBRE, it will increasingly shift its attention towards the more centrist voters who find LIBRE’s discourse too radical. The PN will also seek to attract a more centrist support base, and has been keen in pursuing a strong social agenda, which at times has created tensions with conservatives and the private sector (who do not view his willing-ness to enact new taxes against business favorably). The effectiveness of the president’s strategy could also be jeopardized by the recent rise in unemployment and underem-ployment, which is helping to fuel criminality. However, security-related initiatives have managed to secure broad cross-party consensus, as well as public approval as a whole.

Despite some internal divisions, the PN’s solid majority in the legislature (71 out of 128 seats) will be supportive of its ability to implement the economic agenda agreed with the IMF. Notwithstanding some slippages on the fiscal front, this agenda will shape macro-economic policy in the short term, and help to curb some of the entrenched privileges of strong public-sector groups. These include the teachers unions and public pension funds, both of which have been subject to long-awaited reforms in recent months (including the first major education reform in nearly half a century) in an effort to reduce their influence. There is also a consensus on the need to adopt more effective measures to fight crime. Honduras has the highest murder rate in the world as a result of gang and drug related activity. This situation is exacerbated by widespread corruption within the police, which has led to greater intervention by the military in police duties, in addition to other more controversial measures such as a recently passed law allowing for communications tapping.

B. POLITICAL OUTLOOK 2012 - 2016

3H O N D U R A S

COUNTRY OVERVIEW

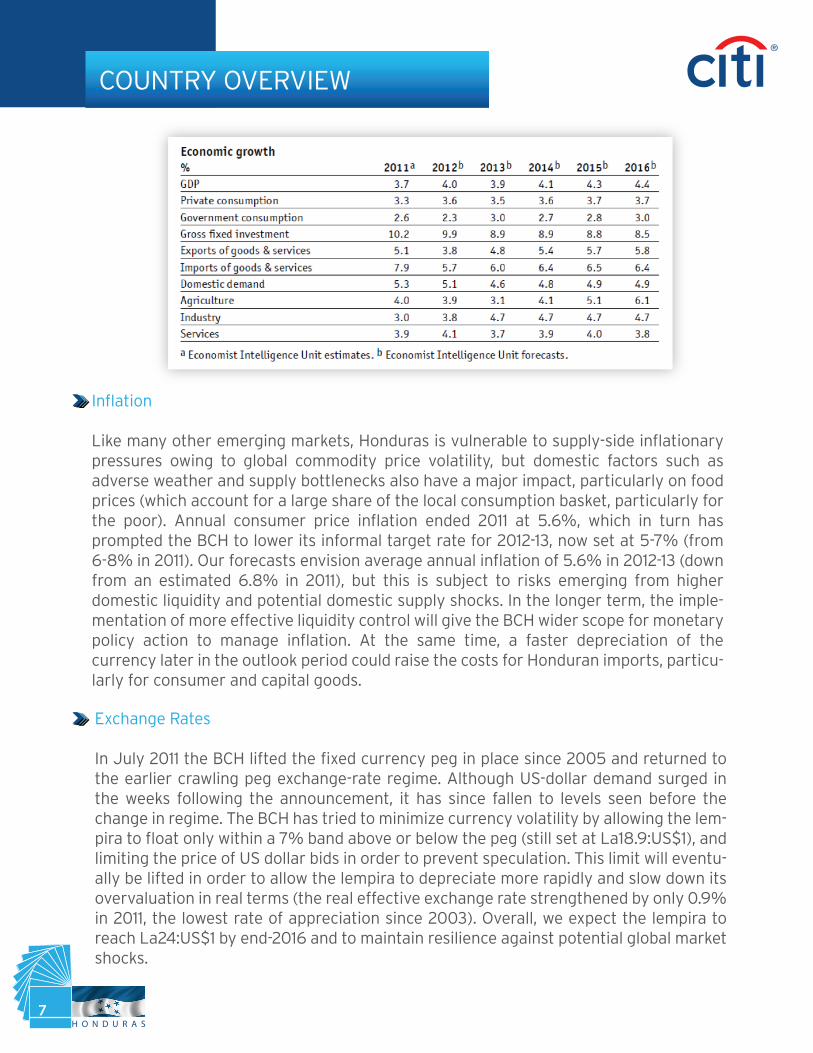

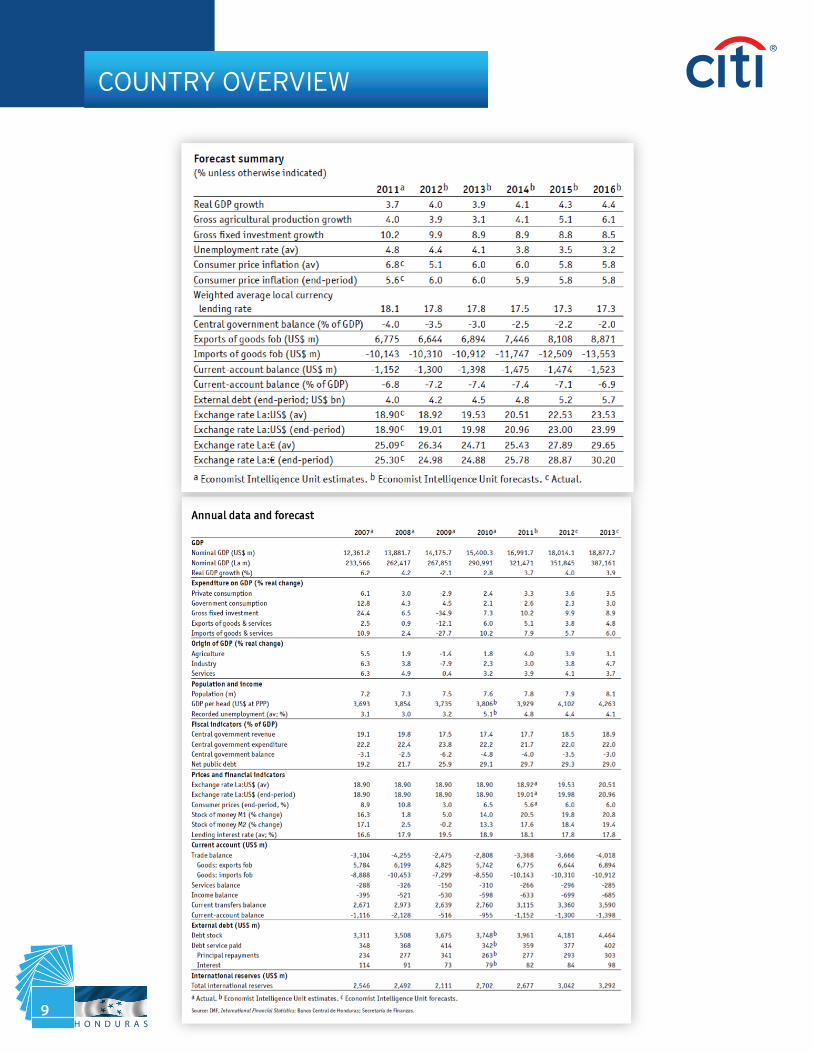

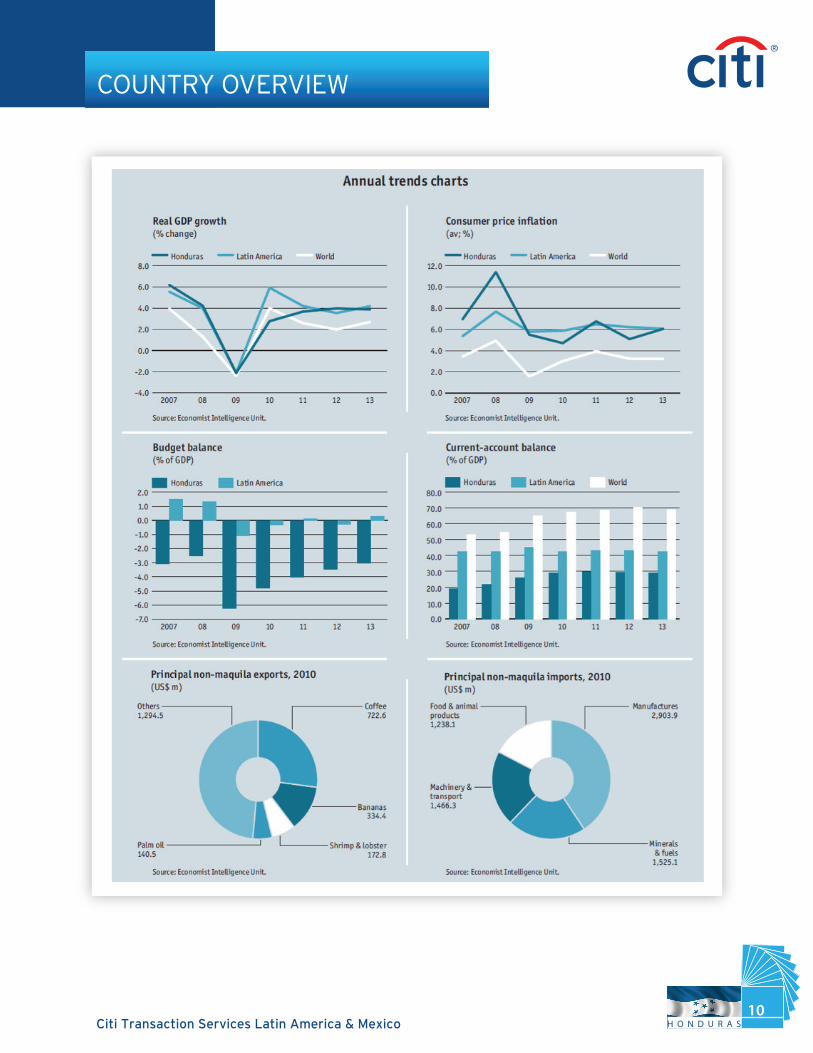

Consumer price inflation (CPI) ended 2011 at year-on-year rate of 5.6% and an annual aver-age of 6.8%, both among the lowest in the past two decades. The figures were also well within the 6-8% target range of the Banco Central de Honduras (BCH, the Central Bank) for the year. Contributing to the lower figure was the tightening of monetary policy in late 2011 (for the first time since August 2009), while there appeared to be little effect from the lifting of the lempira’s peg in July or from holiday-related spending. For the year on aver-age, the item which showed the highest rise in prices was transportation (12.6%) followed by fuel and utilities (8.3%), both of which were largely influenced by the oil price spike seen early in the year. Education costs grew by 7.6%, followed by hotels and restaurants (6.3%), and food and beverages (6.2%). Lower inflation has also allowed for smoother minimum wage negotiations as public opinion was not worried that inflation would erode the nominal wage increases. The success of inflationary control is expected to continue during 2012-13 and will allow Mr. Lobo’s administration room for other needed structural reforms that are often unfeasible when inflation becomes a major public concern.

According to official estimates from the BCH, the real effective exchange rate (REER) in Honduras appreciated by 0.9% during 2011, the lowest rate of strengthening since 2003 (The Economist Intelligence Unit’s REER estimate is a slightly lower 0.6% strengthening). The figure was attributed largely to the lifting of the lempira’s peg to the US dollar, which had been maintained since 2005, as well as the lower rate of inflation, which slightly narrowed the gap with Honduras’ main trade partners, mainly the US as well as its Central American Neighbors, The REER with the latter showed a reduction of 0.1%, resulting in a modest gain in competitiveness. This is particularly important given the generally similar export-oriented economic structures of Honduras’ neighbors, most of which also belong to the Dominican Republic-Central American Free Trade Agreement (DR-CAFTA) with the US and must compete for similar investments such as maquila.

C. ECONOMIC PERFORMANCE

4H O N D U R A SCiti Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

Honduras has gained almost full international recognition following Mr. Zelaya’s return to Honduras in May 2011 after charges against him were dropped. This was highlighted by the country’s readmission to the Organization of American States (OAS) in June 2010. Further diplomatic efforts will be focused on strengthening economic and security ties with the US (Honduras’s major trade and investment partner and the main destination for Honduran emigrants), along with neighboring Central American economies within existing multilateral frameworks, such as the Sistema de la Integración Centroamericana (SICA, the Central American Integration System) and the Dominican Republic-Central America Free-Trade Agreement (DR-CAFTA). Along with its Central American neighbors, Honduras signed a free-trade agreement (FTA) with the EU, which is expected to come into force during 2012. Closer ties are also expected with Venezuela, particularly if Honduras accepts PetroCaribe oil financing funds to free up fiscal resources.

D. ECONOMIC FORECAST

5H O N D U R A S

COUNTRY OVERVIEW

With domestic wages among the highest, a legacy of the administration of the former presi-dent, Manuel Zelaya (2006-09), and the security situation deteriorating, maintaining a com-petitive exchange rate will be a key issue during the two remaining years of Mr. Lobos’ term, and is likely to result in efforts to weaken the lempira at a faster rate than was seen in 2011.

On the supply side, agricultural output should remain strong but will be subject to climate shocks, such as the heavy rains and floods that caused extensive crop losses in the past two years. Construction activity, which played an important role in supporting investment growth before the 2009 recession, is not expected to return to positive territory until 2012 at the earliest. Manufacturing activity, particularly the maquila (offshore assembly for re-export) trade, has grown only modestly after the global eco-nomic downturn of 2008-09 and will remain subject to variations in US import demand. Services will see some moderate growth in 2012-16, mostly on the back of telecommuni-cations, and business and financial services, but the tourism industry will find it difficult to shake off the perception of high crime rates at the same time as it struggles with depressed demand from the US.

Economic Growth

Although our baseline scenario envisions annual average GDP growth of 4% for 2012-13 (broadly in line with the 3.7% estimated growth for 2011), downside risks from an uncer-tain economic outlook in the US, Honduras’s most important trade and investment part-ner, will weigh on the short-term forecast. However, the domestic outlook will improve in the longer term, thanks to a more benign external environment, a pick-up in credit growth, and the investment and trade benefits brought by DR-CAFTA. As a result, we expect growth to average 4.3% in 2014-16.

On the demand side, private consumption will be aided by a recovery of workers’ remit-tances, although high unemployment (and underemployment) will remain a dampening factor. Government consumption growth is expected to remain low as a result of neces-sary fiscal adjustments in the short term, but should tick upwards once the presidential election approaches (in 2013). Fixed investment will continue to expand, boosted by greater financing availability and an improved domestic environment, but a recent series of new taxes on businesses could erode investor confidence. On the external side, real import growth will slightly outpace export growth, leaving net trade as a negative contributor to GDP throughout the outlook period. Long-term structural challenges to growth will include the need to improve infrastructure and education significantly, and to focus efforts more effectively on reducing the country’s plethora of social ills, notably widespread poverty, inequality and crime. Competition with other Central American economies may also put Honduras at a disadvantage, given its higher labor costs and crime rates compared with some of its neighbors.

COUNTRY OVERVIEW

6H O N D U R A SCiti Transaction Services Latin America & Mexico

Inflation

Like many other emerging markets, Honduras is vulnerable to supply-side inflationary pressures owing to global commodity price volatility, but domestic factors such as adverse weather and supply bottlenecks also have a major impact, particularly on food prices (which account for a large share of the local consumption basket, particularly for the poor). Annual consumer price inflation ended 2011 at 5.6%, which in turn has prompted the BCH to lower its informal target rate for 2012-13, now set at 5-7% (from 6-8% in 2011). Our forecasts envision average annual inflation of 5.6% in 2012-13 (down from an estimated 6.8% in 2011), but this is subject to risks emerging from higher domestic liquidity and potential domestic supply shocks. In the longer term, the imple-mentation of more effective liquidity control will give the BCH wider scope for monetary policy action to manage inflation. At the same time, a faster depreciation of the currency later in the outlook period could raise the costs for Honduran imports, particu-larly for consumer and capital goods.

Exchange Rates

In July 2011 the BCH lifted the fixed currency peg in place since 2005 and returned to the earlier crawling peg exchange-rate regime. Although US-dollar demand surged in the weeks following the announcement, it has since fallen to levels seen before the change in regime. The BCH has tried to minimize currency volatility by allowing the lem-pira to float only within a 7% band above or below the peg (still set at La18.9:US$1), and limiting the price of US dollar bids in order to prevent speculation. This limit will eventu-ally be lifted in order to allow the lempira to depreciate more rapidly and slow down its overvaluation in real terms (the real effective exchange rate strengthened by only 0.9% in 2011, the lowest rate of appreciation since 2003). Overall, we expect the lempira to reach La24:US$1 by end-2016 and to maintain resilience against potential global market shocks.

7H O N D U R A S

COUNTRY OVERVIEW

8H O N D U R A SCiti Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

External Sector

The current-account deficit began widening in 2010 and is forecast to peak at 7.4% of GDP in 2013-14, before falling on the back of a weaker currency and rising investments in the free zones. Trade has benefited mostly from a rise in agricultural prices (most notably coffee prices, Honduras’s largest single export), in contrast with the maquila sector, which has performed less well owing to sluggish US import demand (although in the longer term it will receive a boost from DR-CAFTA). However, high import requirements for fuel and manufac-tures will keep the trade deficit wide, at an average of 20.7% of GDP in 2012-16, even though a more flexible currency will aid competitiveness. Tourism is set to gain an increasing share of services exports, but the perception of high crime will erode Honduras’s attractiveness relative to other Central American and Caribbean destinations, keeping the services balance in mild deficit. Rising profit repatriation and interest payments on foreign debt will hold the income deficit steady at an average of 3.8% of GDP in 2012-16, while the current transfers balance will average 19.2% of GDP in 2012-13, as remittances from Hondurans working in the US increase. The current-account deficit will be financed mostly by inward foreign direct investment (FDI), which should reach US$1.6bn by 2016, as free zones expand and charter cities are set up. With multilateral and bilateral aid also flowing in, reserves should rise to US$3.9bn by end-2016, providing 3.4 months of import cover.

9H O N D U R A S

COUNTRY OVERVIEW

10H O N D U R A SCiti Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

11H O N D U R A S

COUNTRY OVERVIEW

COUNTRY OVERVIEW

12H O N D U R A SCiti Transaction Services Latin America & Mexico

B. CITIBANK IN HONDURAS

A. BANKS IN HONDURAS

BANKING SYSTEM

As of 2012 there are 17 commercial banks operating in Honduras, which accounted for 97.7% of the assets held by the financial system. Big financial conglomerates have increased their presence in Honduras, with Citibank (US) taking over Grupo Financiero Uno and Grupo Cuscatlan, Banco Agricola (Guatemala) purchasing Banco del Pais, and Davivienda Group (Colombia) purchasing HSBC (whom had previously purchased Ban-istmo). In addition, Banco de America Central (BAC) was purchased by Grupo Aval (Colombia), while Banco Procredit, a German bank specializing in microcredit, and a Mexi-can bank, Banco Azteca, have started operations in Honduras.

Commercial banks cater to a limited client base. Most assets are concentrated in a few hands as large banks, insurance companies and finance companies tend to be grouped together under holding companies with common shareholders. This system has allowed banks to shift assets with ease in response to changes in regulations and market conditions.

Citibank has been established in Honduras since 1965, and has 29 branches throughout the country.

Branch Locations• Tegucigalpa• San Pedro Sula• Various cities nationwide

Citibank, Honduras - Banking Services• Liquidity Management / Domestic & International Account Structures• Information Management• Payables Management• Receivables Management• Regional Implementations• Customer Service• Local Cash Management Services• Commercial Cards Offering: Local Issuance Capabilities• Trade Services (FX Management)

13H O N D U R A S

• Supply Chain Finance 1. LCA 2. Documentation 3. Back & Front End 4. OPS• Trade Finance (EAF)• Derivative Solutions• Structured Finance Solutions

The Honduran Banking Association (Asociación Hondureña de Instituciones Bancarias.AHIBA) runs a clearinghouse that provides private banks with an automated clearing mechanism for checks denominated in Lempiras and Dollars (local). The auto-mated process cuts the clearing time to 24 hours, regardless of the issuing bank’s loca-tion. The clearing of checks denominated in dollars can take much longer - from 8-45 days - depending on where the issuing bank is located.

A. CLEARINGHOUSE

CLEARING SYSTEM

B. LOCAL/FOREIGN CLEARING SYSTEM

Money transfers between branches of the same bank can be arranged in one hour or less. In 2004 Ahiba implemented an electronic interbank payment system to increase the efficiency of interbank transfers. Resolution 374.10/2006 passed in November 2006 by the Central Bank approved the Regulation of Electronic Payment Systems, allowing the central bank to set up an automated clearinghouse. The system, known as ACH Pronto (Automated Clearing House Pronto), went into effect in March 2007. With ACH Pronto, transfers from one bank to another, which previously took up to three days, are cleared immediately. The president of the central bank also signed the Treaty on Securi-ties Payment and Liquidation Systems for Central America and the Dominican Republic (Tratado sobre Sistemas de Pago y de Liquidación de Valores de Centroamérica y la República Dominicana), which looks to strengthen payments systems on a regional level.

14H O N D U R A SCiti Transaction Services Latin America & Mexico

Corporate Tax Rates

Corporate income tax rates are 15% for earnings up to and including La200,000 and 25% on amounts exceeding La200,000. Branches are taxed in the same manner as locally incorporated companies. Profits transferred to a head office are subject to a 35% withhold-ing tax. Very small companies with sales below La90,000 are exempt from income tax.

Other Taxes/Regulations

Despite losing out on more than US$148m yearly as a result of eliminating taxes on more than 74% of US imports (as required by the Dominican Republic-Central America Free-Trade Agreement, or DR-CAFTA), revenues from taxes have continued to be strong thanks to a strong economy and improvements in tax collection. Income tax collection grew by 27.9% in 2007 compared to 2006, to reach La2.35bn. This brings the tax burden to 16.3%, up from 15.4% in 2006. Receipts from sales and income tax, which each account for over one-third of all tax revenue, increased by 22.5% and 27.9%, respectively. Income tax reporting was made more efficient by the introduction of an Internet-based system.

As of April 24, 2012 the Ley de Seguridad Poblacional will take effect, whereby a contribu-tion of Lps 2 per every Lps 1000 withdrawn from accounts with average balances of Lps 120,000 will take effect. Some exceptions have been approved, such as tax payments, gov-ernmental entities, foreign embassies, etc.

B. TAXES

FOREIGN EXCHANGE CONTROLS

A. MARKETS

The FX regime in Honduras is regulated by the Central Bank. The Regime has been in place since 1994, and has allowed a relative stability in the FX rate during said period. The mechanics of the system are as follows:

Purchases

Exporters are required to sell all USD to the financial system, minus some exceptions, and banks in turn are required to sell to the BCH all currency purchased from exporters to the Central Bank.

Sales

All purchases of FX must go through a daily USD auction at the central bank. A maximum amount of $1.2MM per day can be purchased by Honduran nationals or registered compa-nies. Price is set at the auction according to the bids presented, bids must be within a band of 7% above and 7% below the base price established by the central Bank.

15H O N D U R A S

A. IMPORT AND EXPORT REGULATIONS

TRADE REGULATIONS

B. REGIONAL TRADE ASSOCIATIONS

All Honduran exports are free of taxes. The Dominican Republic Central American Free-Trade Agreement (DR-CAFTA), which replaced the Caribbean Basin Initiative (CBI), also provides US economic assistance for the region to aid private-sector development by financing essential imports and by establishing development banks, chambers of com-merce, skills-training programmes, industrial free zones and other essential infrastruc-ture. DR-CAFTA went into effect in April 2006 for Honduras. Costa Rica was the last country to ratify the treaty, in November 2008. DR-CAFTA makes permanent the ben-efits enjoyed under the CBI and is expected to attract new foreign investment to Hondu-ras, particularly in export-oriented sectors. Around 80% of US products can now enter the region duty-free, and nearly 100% of Honduran products can enter the US market duty-free.

On August 12 of 2011, Honduras and Canada signed a bi-lateral Free Trade Agreement which is expected to increase exports from Honduras to Canada by $350MM per year. Canadian investment is expected to amount to $240MM in maquila, as well as increase employment levels from 15,000 to 18,000.

The Northern Triangle

A free-trade agreement between Mexico, El Salvador, Guatemala and Honduras - known collectively as The Northern Triangle - took effect in April 2001. The region is negotiat-ing a similar trade agreement with the Andean Community. A free-trade agreement was signed in August 2007 between Colombia and the Northern Triangle countries. The European Union began negotiations on an agreement of association with Central America in 2007, which continued throughout 2008 with the goal of concluding in 2009.

16H O N D U R A SCiti Transaction Services Latin America & Mexico

B. TIME DEPOSITS

C. TREASURY BILLS

A. C.D.S

INVESTMENT OPPORTUNITIES

CDs are available at commercial banks in local currency and dollars. Interest rates for 90- to 180-day CDs are about 1.2 percentage points below those for commercial paper traded on the securities exchanges.?

Most commercial banks make available savings accounts and time deposits, with inter-est rates determined by the amount invested. Fixed-term deposits in local currency tend to be for short terms (generally 30, 60, 90 or 180 days).

Tax consequences. Interest earned on personal savings accounts, time deposits and certificates of deposit with balances of La50,000 or less are tax-free. For corporations, interest earned on these accounts is considered part of regular taxable income. For investors from abroad, there is a withholding tax of 5% on interest earned.

Central bank bonds (Letras del Banco Central), both in lempira and dollar denomina-tions, are traded on the securities market. Bills are auctioned on a biweekly basis with tenors upt to 34 days. The yield curve currently starts at 7 day paper at a rate of 6% and ends at 364 day paper at a yield of 9.7%. the market for these instruments is the most liquid Fixed income market in the country and total outstanding amount oscillates around $1Bn.

Tax consequences. Interest earnings are considered taxable Income for banks and Finan-cial institutions, but for non-banks, there is a special rate of 10% flat on interest income earned.

17H O N D U R A S

D. COMMERCIAL PAPER

E. STOCK MARKET

INVESTMENT OPPORTUNITIES

CP of between 30 and 180 days is issued in both lempiras and dollars. Interest rates on local-currency CP are typically the same as those of bank accounts. To date, there is no established rating system for the paper, nor do many companies publish financial informa-tion. Investment decisions are made on the basis of company prestige and a stockbroker’s advice. Companies do not tend to invest in one another’s CP, preferring instead to use banking accounts to invest cash.

Tax consequences. CP is subject to a 10% one-time capital gains tax at the time of sale

Only one securities market exists in Honduras: the Central American Stock Exchange (Bolsa Centroamericana de Valores.BCV), based in Tegucigalpa. As of November 2008 there were ten private companies registered with the BCV that were entitled to issue securities on the stock exchange (three more than in 2007): one finance company and nine banks. Any private business is eligible to trade and there are no special prohibitions that affect foreign companies. Other instruments traded on these exchanges include bankers’ acceptances, repurchase agreements, short-term promissory notes, government private debt conversion bonds and land-reform repayment bonds. The authorities hope that the creation of a region-wide register for foreign titles will be established in the near future to facilitate trading between stock markets in Central America.

18H O N D U R A SCiti Transaction Services Latin America & Mexico

We currently operating under two banking licenses: Banco de Honduras, S.A. and Banco Citibank de Honduras, S.A., both Citibank subsidiaries.

Companies operating in Honduras are moving toward concentrating their cash manage-ment needs with one full service bank as a mean of optimizing treasury flows. Technol-ogy customization is becoming a driving force in the banking sector. Clients have more sophisticated demands, and are therefore requiring efficient, state-of-the-art products to meet their goals. Competition among financial service providers continues through the development of automated products and services.

A. GENERAL BUSINESS TERMS AND CONDITIONS

B CITIBANK’S ACCOUNT SERVICES SOLUTIONS IN HONDURAS

CITI SOLUTIONS & SERVICES

C. CITIBANK’S PAYMENT SOLUTIONS IN HONDURAS

- Local Currency and US Dollars(*) Checking and Savings Accounts - Accounts for Resident and Non-Resident Companies- DDA NY

Documentation requirements to open accounts

• Articles of incorporation and amendments• Certification of the current Board of Directors , signed by the Secretary of the Board• Power of attorney issued to officer(s) of the company• Account opening contract signed by the legal representative• Signature cards• Photocopy of tax ID • Other documentation based on local regulations

Citibank offers clients payments solutions designed for both local and overseas pay-ments. Companies may select the combination of services needed to meet both their domestic and international payment requirements.

- Citibank Paylink- Citiconnect Online Payment Channel- Tax Payments

19H O N D U R A S

D. CITIBANK’S COLLECTIONS SOLUTIONS IN HONDURAS

E. CITI TRADE SOLUTIONS

F. DELIVERY SYSTEMS AVAILABLE

G. DERIVATIVE SOLUTIONS

H. STRUCTURED FINANCE SOLUTIONS

CITI SOLUTIONS & SERVICES

Speedcollect

a. Passive and Active Collectionsb. Pick up Services

Trade Services

- SBLC’s- Import and Export Collections- Import and Export LC’S- Bank Guarantees

Working Capital and Supply Chain Management (Trade Finance)

- Import and Export Finance- Supply Chain Finance

Export Agency Finance

- Global Electronic Banking Platform: Citidirect Electronic Banking- Regional Banking Platform: Netbanking Regional

- Non Delivery Forwards- Swaps- Customized Hedging Mechanisms

- Syndications- Corporate Finance

20H O N D U R A SCiti Transaction Services Latin America & Mexico

21H O N D U R A S

CONTACT INFORMATION

Sales Heads

Industry Sector Heads

Carolina JuanTreasury and Trade Solutions Client Sales ManagementLatin America & Mexico HeadCiti Transaction ServicesEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026

Industrials SectorInes Vargas BarreraEmail: [email protected]: +52 (181) 8366 - 5190Of. Phone: +52 (81) 1226 - 8525

Branding, Consumer and Healthcare SectorOscar MazzaEmail: [email protected]: +1 (305) 588 - 9396Of. Phone: +1 (305) 347 - 1336

Technology, Media and Telecom SectorGabriel KirestianEmail: [email protected]: +54 (911) 3301 - 4826Of. Phone: +54 (11) 4329 - 1516

Energy, Power and Chemicals SectorPeter LangshawEmail: [email protected]: +55 (11) 6183 - 6958Of. Phone: +55 (11) 6183 - 6958

Public SectorJorg PaascheEmail: [email protected]: +52 (1) 55 5453 - 0103Of. Phone: +52 (55) 2226 - 6020Based: Mexico DF, Mexico

Non Bank FI Sector (NFBI)Ricardo DessyEmail: [email protected]: +54 (911) 6641 - 9752Of. Phone: +54 (11) 4329 - 1471Based: Buenos Aires, Argentina

BrazilAdoniro CestariEmail: [email protected]: +55 (11) 7130 - 9447Of. Phone: +55 (11) 4009 - 7838Based: Sao Paulo, Brazil

Central AmericaEvelin MadridEmail: [email protected]: + 506 8701 - 4529Of. Phone: +506 2588 - 7541Based: San Jose, Costa Rica

MexicoMiguel YtuarteEmail: [email protected]: +52 (1) 55 4088 - 2284Of. Phone: +5255 (1226) 8895Based: Mexico DF, Mexico

Andean RegionCarolina JuanEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026Based: Bogota, Colombia

ArgentinaAdrian ScosceiraEmail: [email protected]: +54 (911) 5674 - 6966Of. Phone: +54 (11) 4329 - 1194Based: Buenos Aires, Argentina

Citi Transaction Serviceswww.transactionservices.citi.com

© 2012 Citibank, N.A. All rights reserved. Citi and Arc Design is a trademark and service mark of Citigroup Inc., used and registered throughout the world. All other trademarks are the property of their respective owners.