cost accounting foundations and...

TRANSCRIPT

Chapter 8

The Master Budget

Cost Accounting

Foundations and EvolutionsKinney, Prather, Raiborn

Learning Objectives (1 of 2)

• Explain why budgeting is important

• Describe how strategic planning is related to budgeting

• Identify the starting point of a master budget and explain why it is the starting point

• Prepare various master budget schedules and explain how they relate to one another

Learning Objectives (2 of 2)

• Explain why the cash budget is important in

the master budgeting process

• List the benefits provided by a budget

• (Appendix) Explain how a budget manual

facilitates the budgeting process

Management

Planning is the cornerstone of effective management

Terms

• Budgeting - Formalizes plans and translates

qualitative narratives into a documented,

quantitative format

• Budget - Expresses a commitment to

planned activities and resource acquisition

and use

The Planning Process

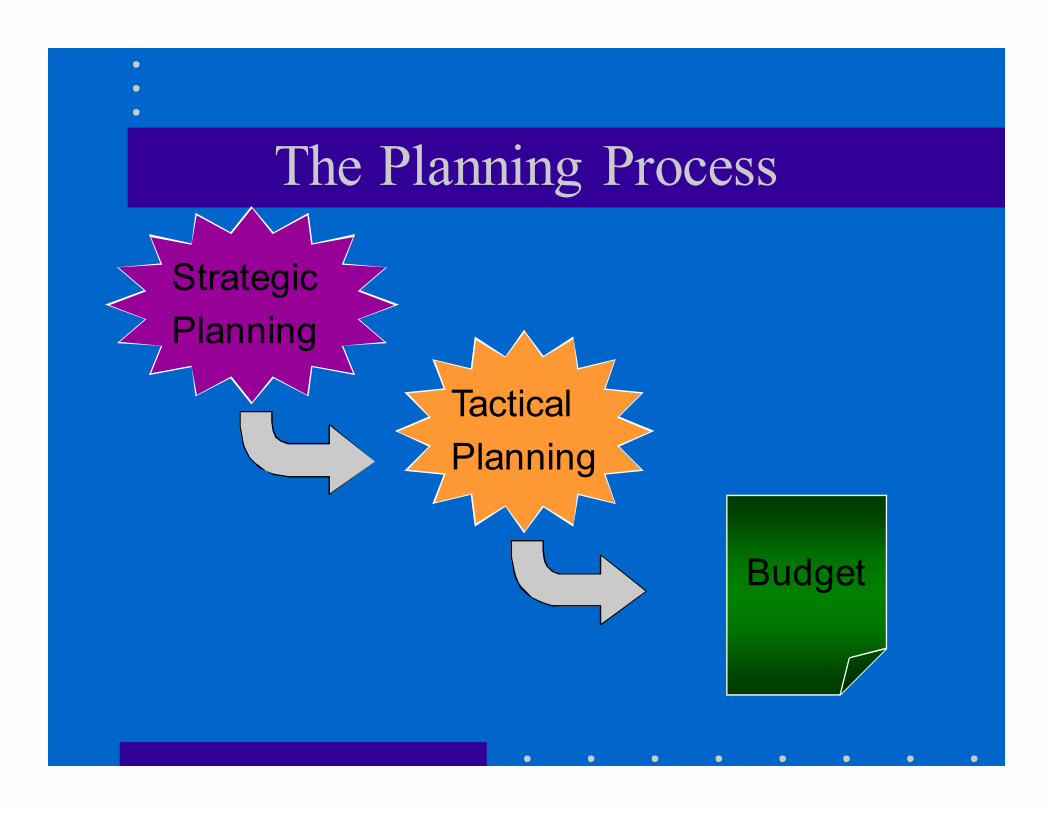

Strategic

Planning

Tactical

Planning

Budget

Strategic Planning

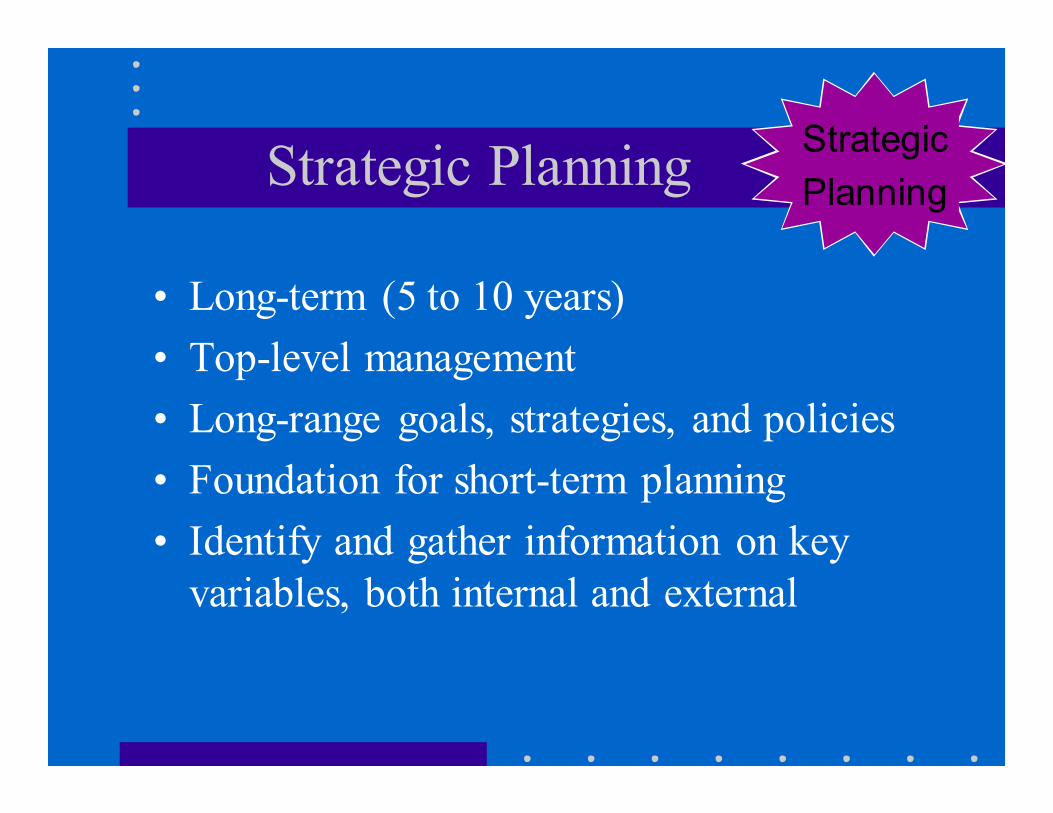

• Long-term (5 to 10 years)

• Top-level management

• Long-range goals, strategies, and policies

• Foundation for short-term planning

• Identify and gather information on key

variables, both internal and external

Strategic

Planning

Strategic Planning

Effective strategic planning requires that managers build

plans and budgets that integrate external considerations and

influences with internal factors

Strategic

Planning

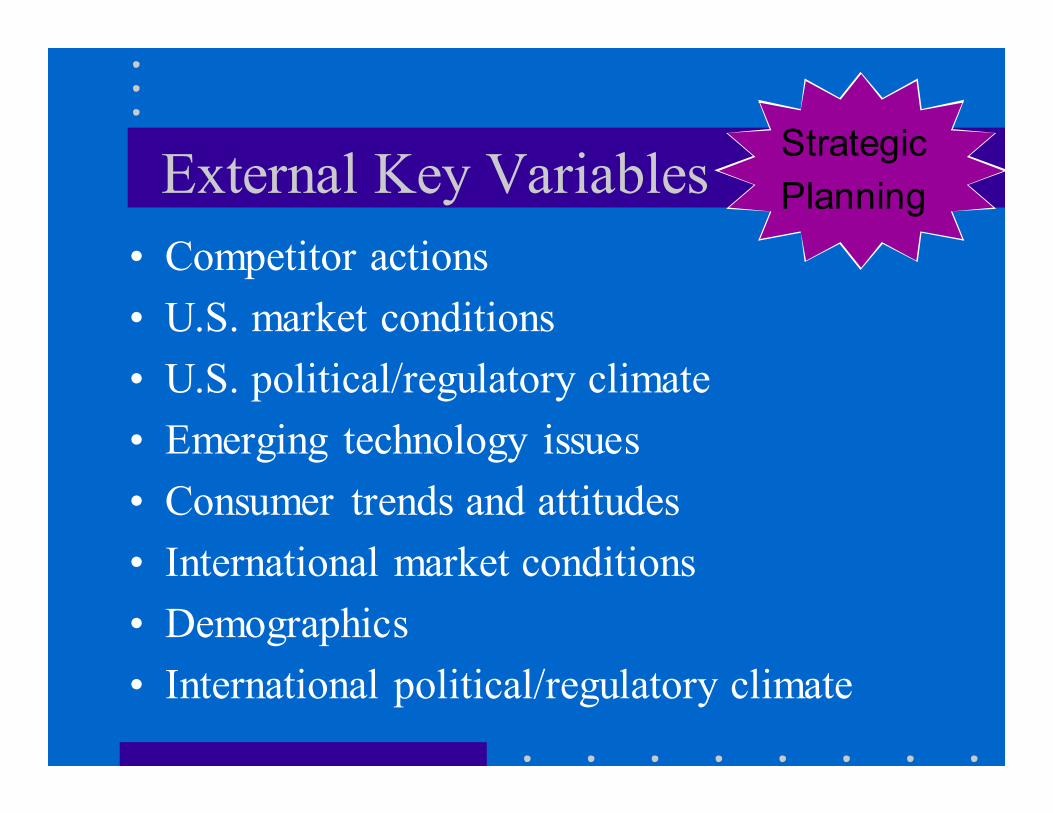

External Key Variables

• Competitor actions

• U.S. market conditions

• U.S. political/regulatory climate

• Emerging technology issues

• Consumer trends and attitudes

• International market conditions

• Demographics

• International political/regulatory climate

Strategic

Planning

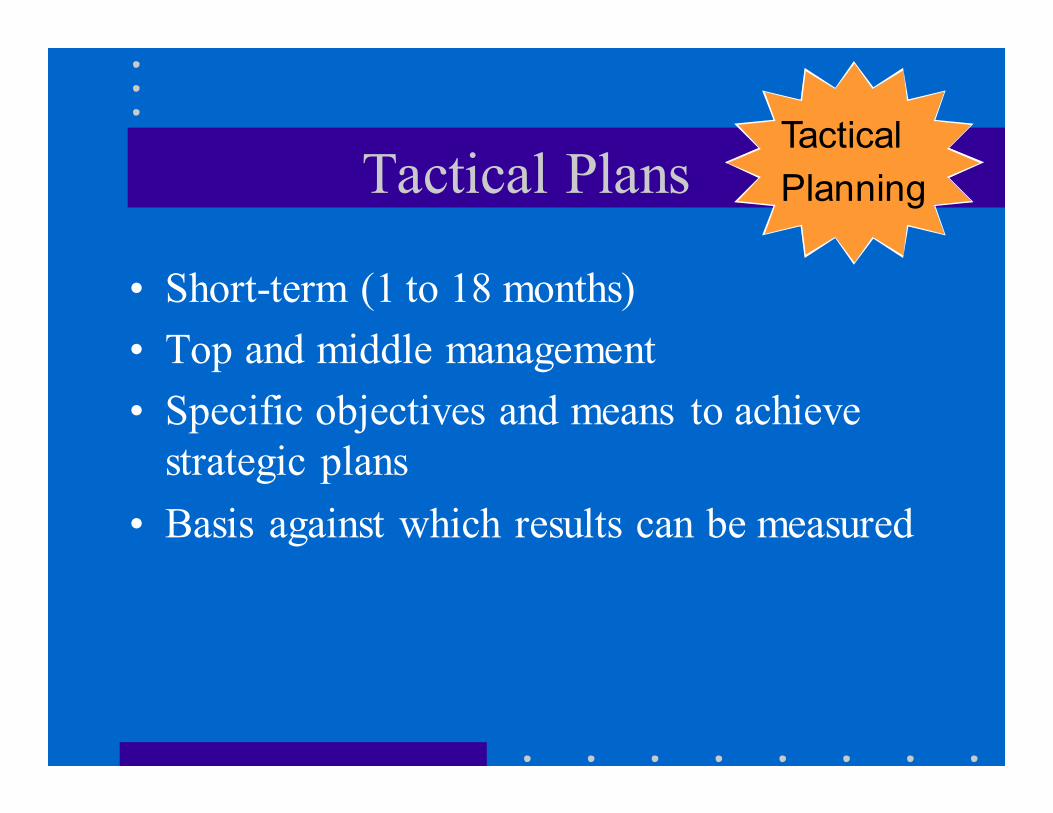

Tactical Plans

• Short-term (1 to 18 months)

• Top and middle management

• Specific objectives and means to achieve

strategic plans

• Basis against which results can be measured

Tactical

Planning

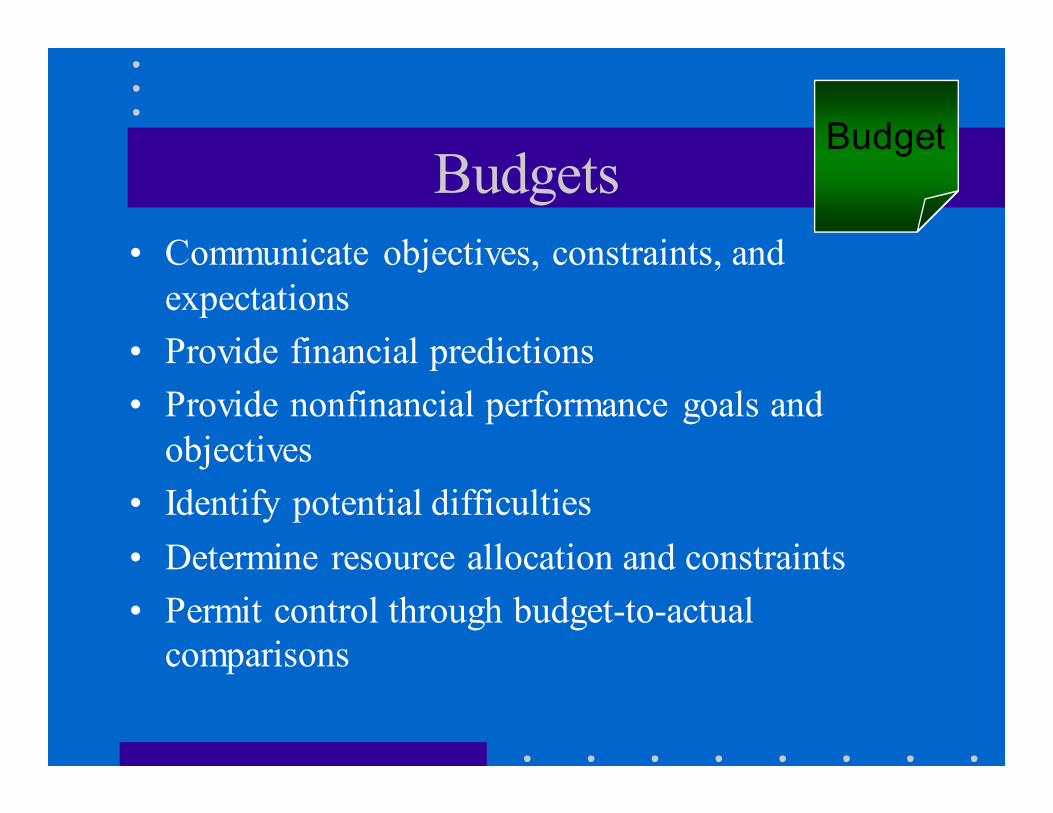

Budgets

• Communicate objectives, constraints, and

expectations

• Provide financial predictions

• Provide nonfinancial performance goals and

objectives

• Identify potential difficulties

• Determine resource allocation and constraints

• Permit control through budget-to-actual

comparisons

Budget

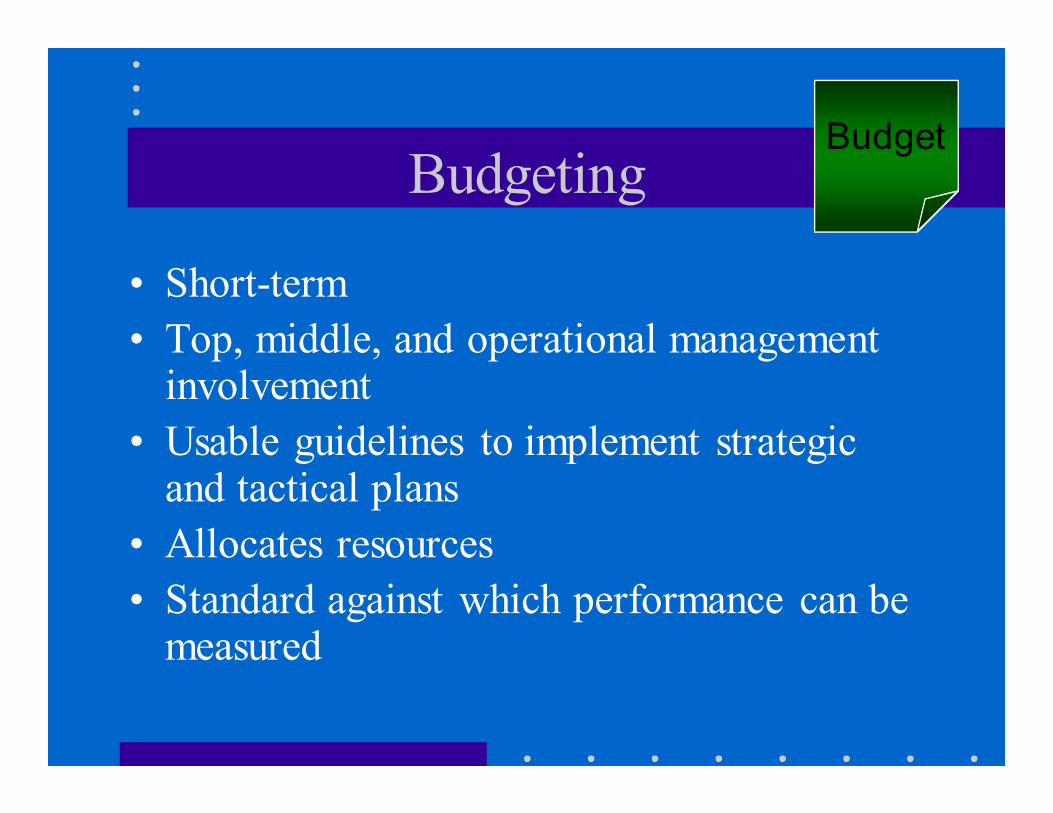

Budgeting

• Short-term

• Top, middle, and operational management involvement

• Usable guidelines to implement strategic and tactical plans

• Allocates resources

• Standard against which performance can be measured

Budget

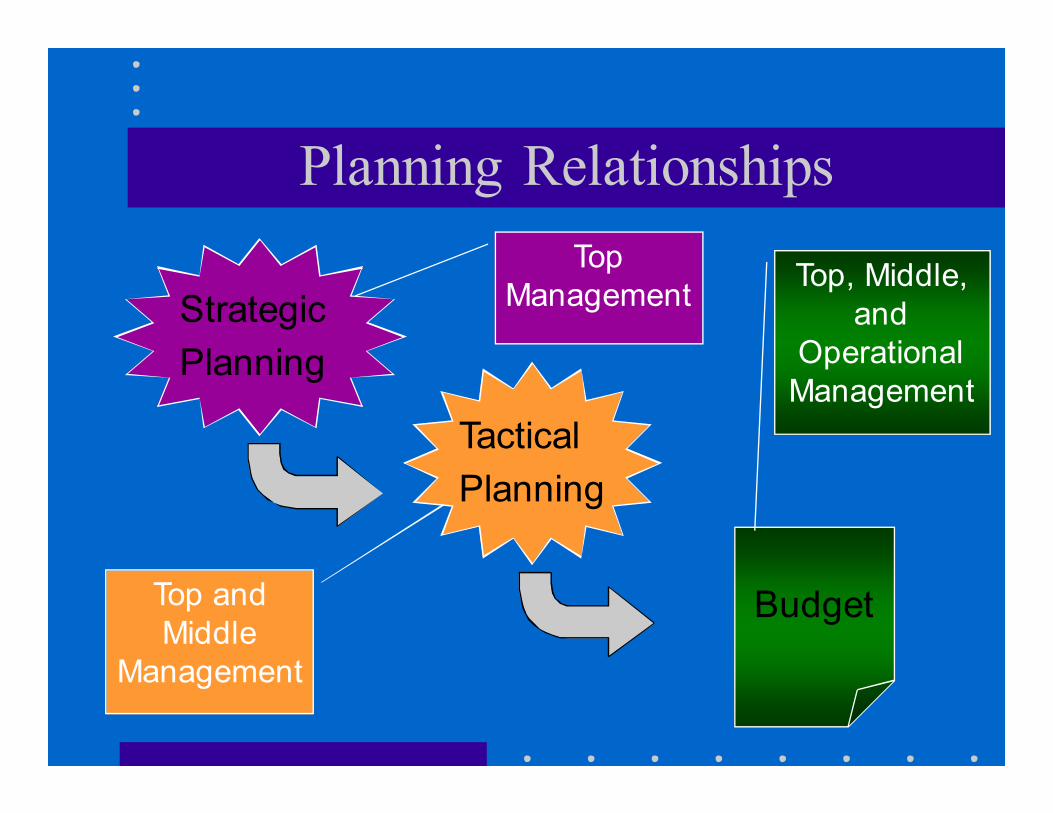

Planning Relationships

Strategic

Planning

Tactical

Planning

Budget

Top

Management

Top and

Middle

Management

Top, Middle,

and

Operational

Management

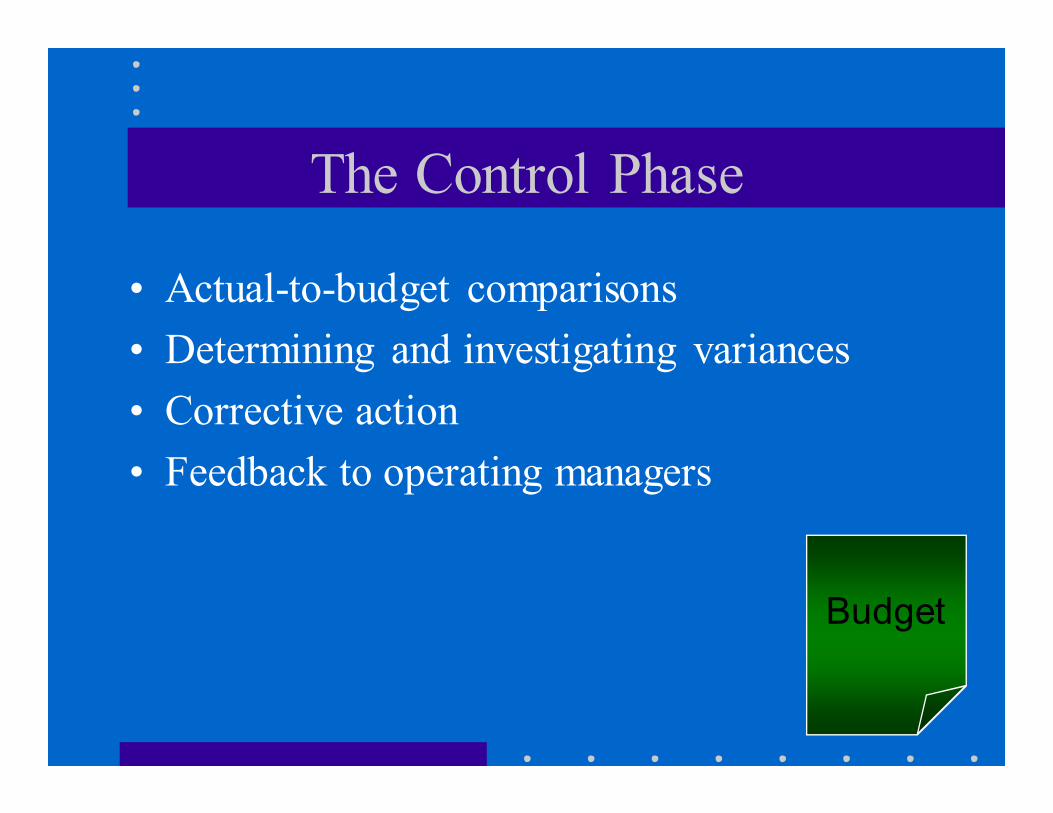

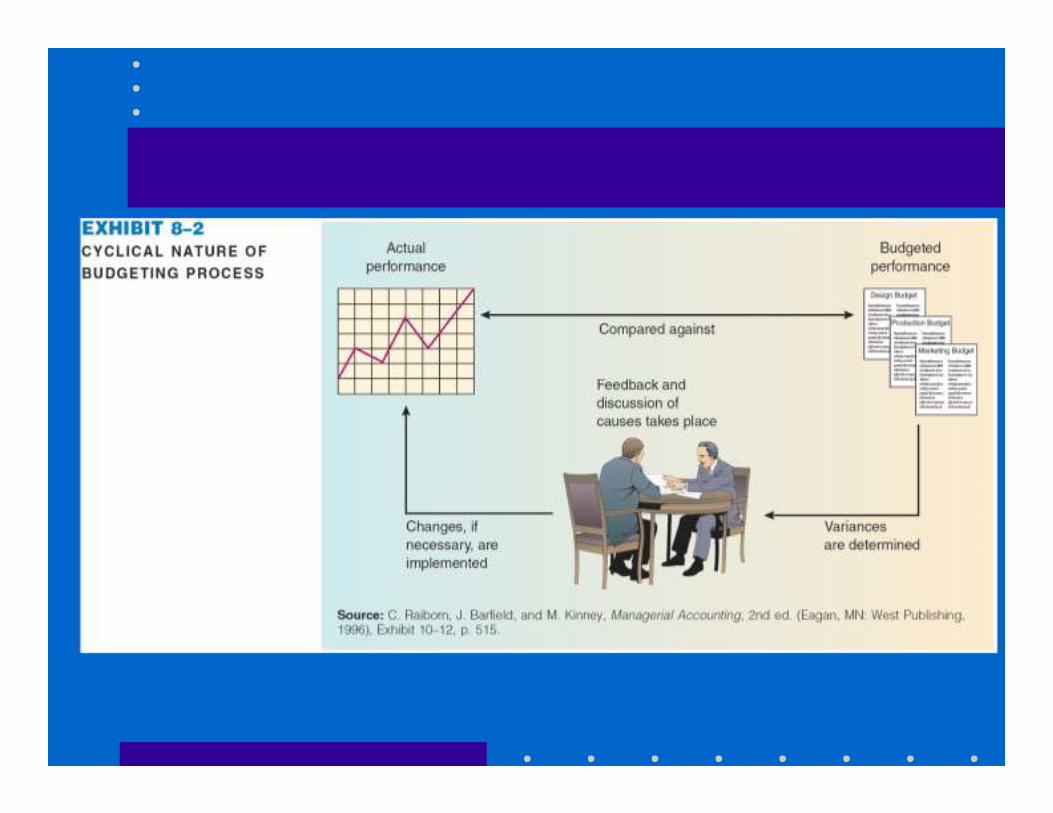

The Control Phase

• Actual-to-budget comparisons

• Determining and investigating variances

• Corrective action

• Feedback to operating managers

Budget

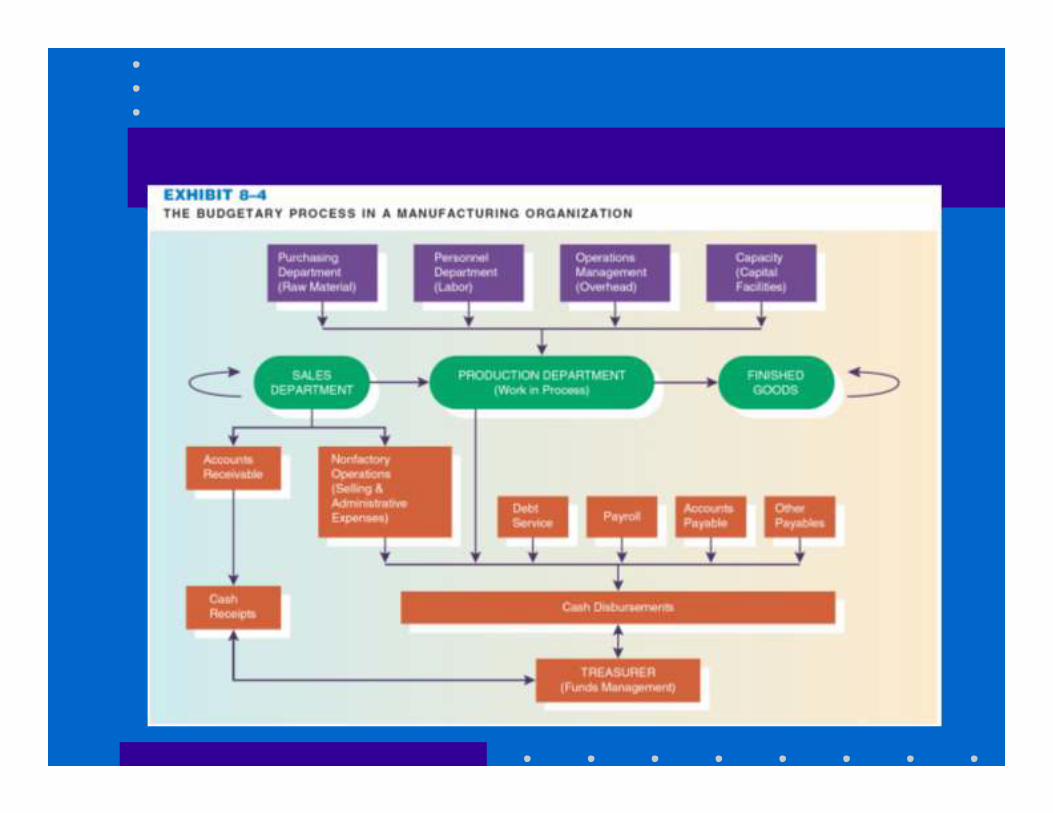

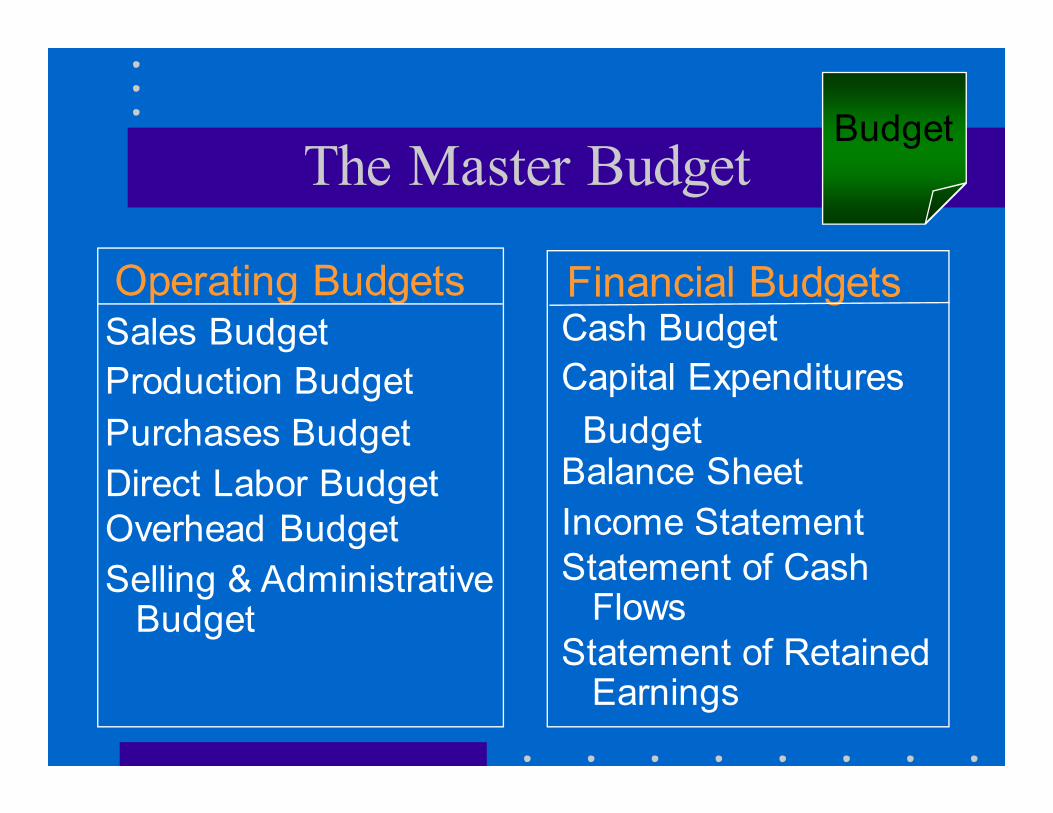

The Master Budget

• A comprehensive set of budgets, budgetary

schedules, and pro forma organizational

financial statements

• For a specific period of time

• Static – based on a single level of output

demand

• Interactive – departments generate and

consume information

The Master Budget

Operating Budgets Financial BudgetsSales Budget

Production Budget

Purchases Budget

Direct Labor Budget

Overhead Budget

Selling & Administrative Budget

Cash Budget

Capital Expenditures

BudgetBalance Sheet

Income Statement

Statement of Cash Flows

Statement of Retained Earnings

Budget

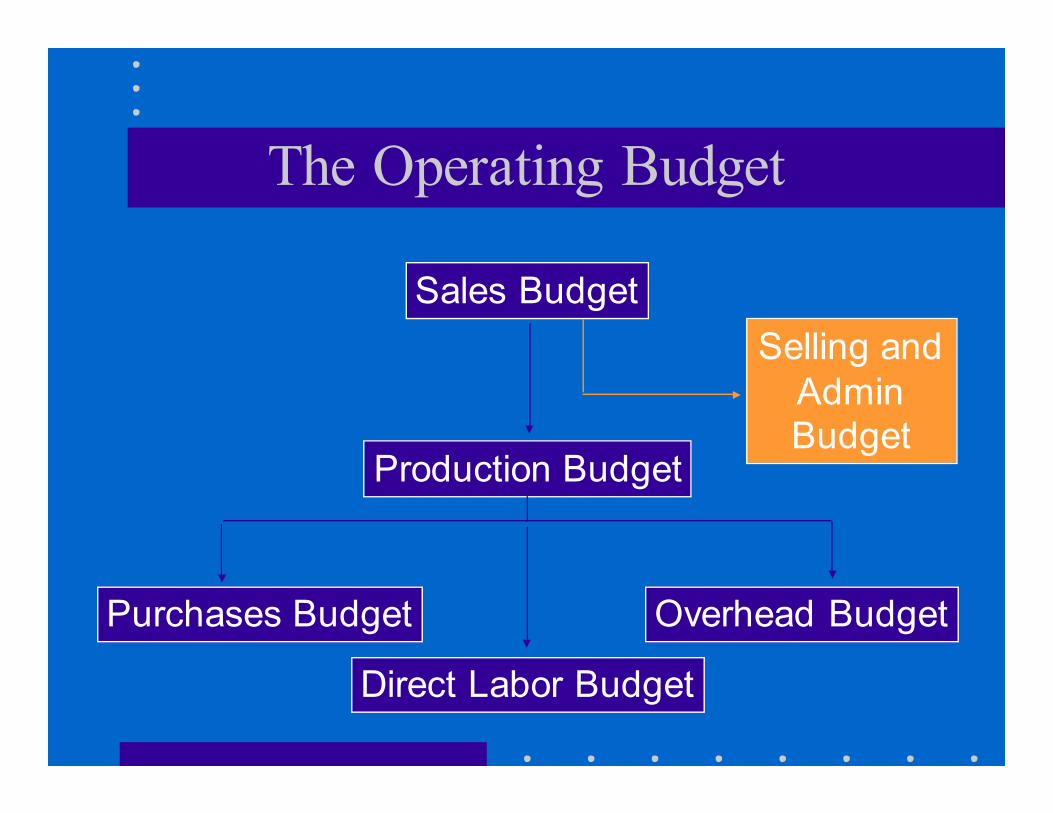

The Operating Budget

Sales Budget

Sales Forecast

• Ask sales personnel

• Extrapolate past trends

• Use market research

• Employ statistical models

and simulation

Sales

Forecast

Sales Budget

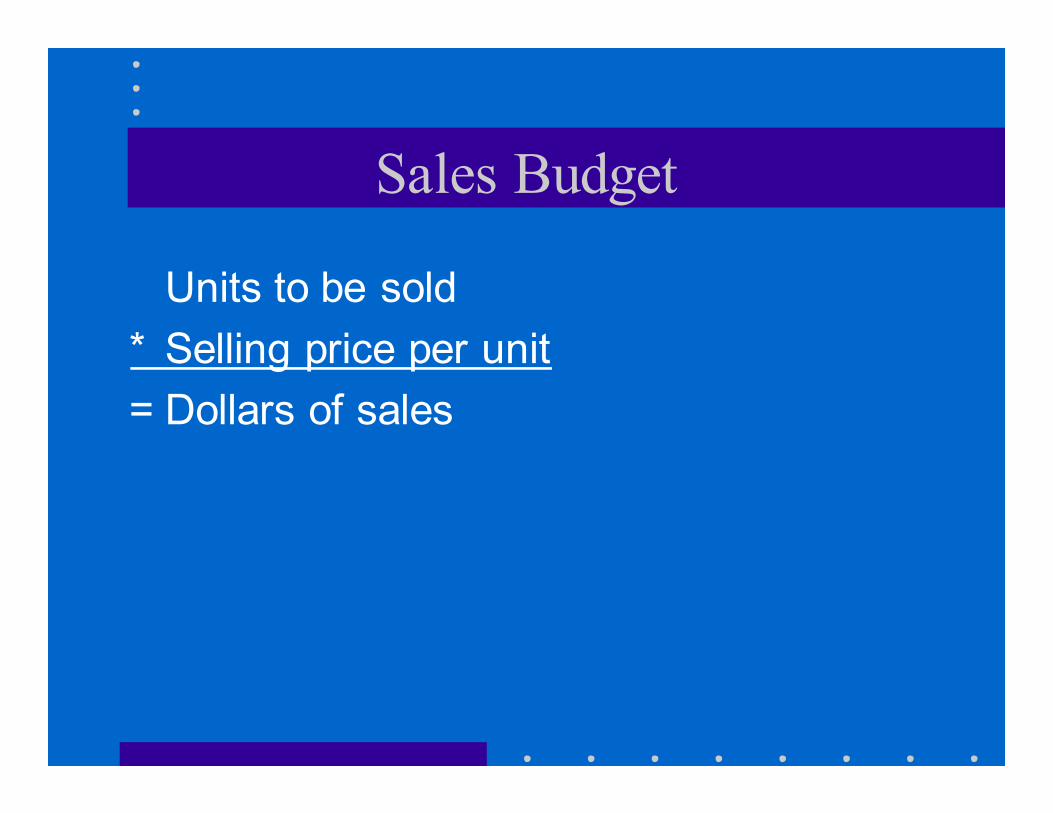

Units to be sold

* Selling price per unit

= Dollars of sales

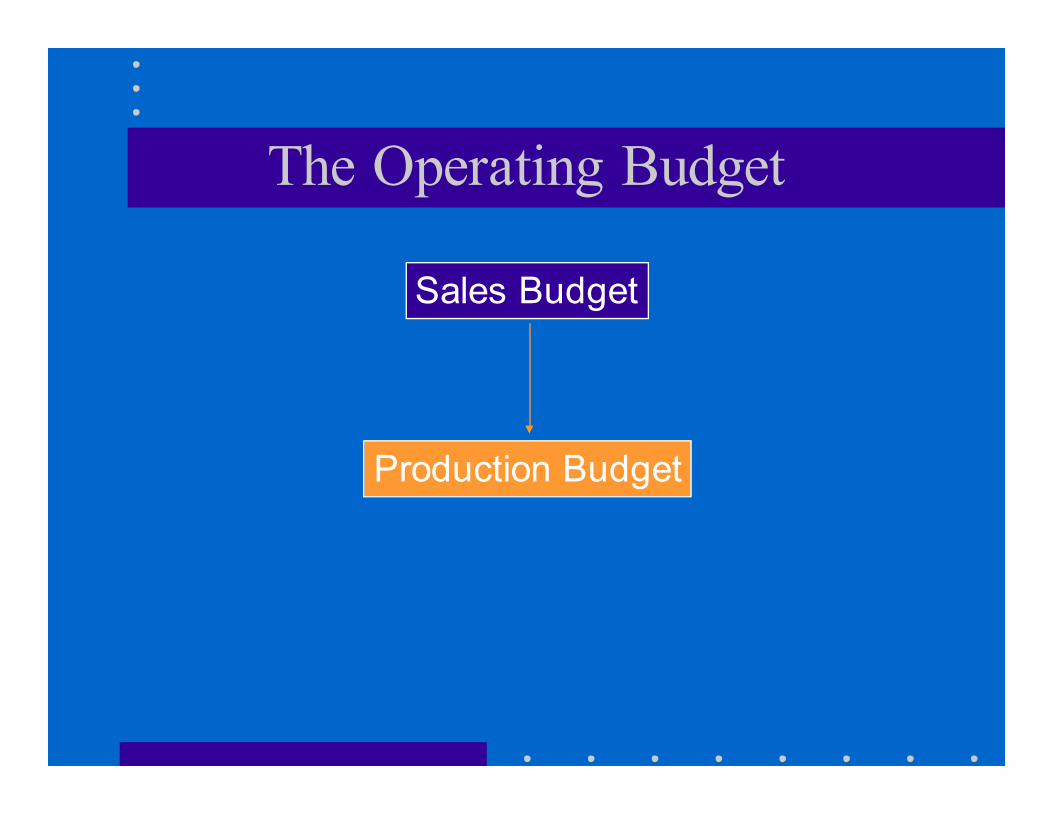

The Operating Budget

Sales Budget

Production Budget

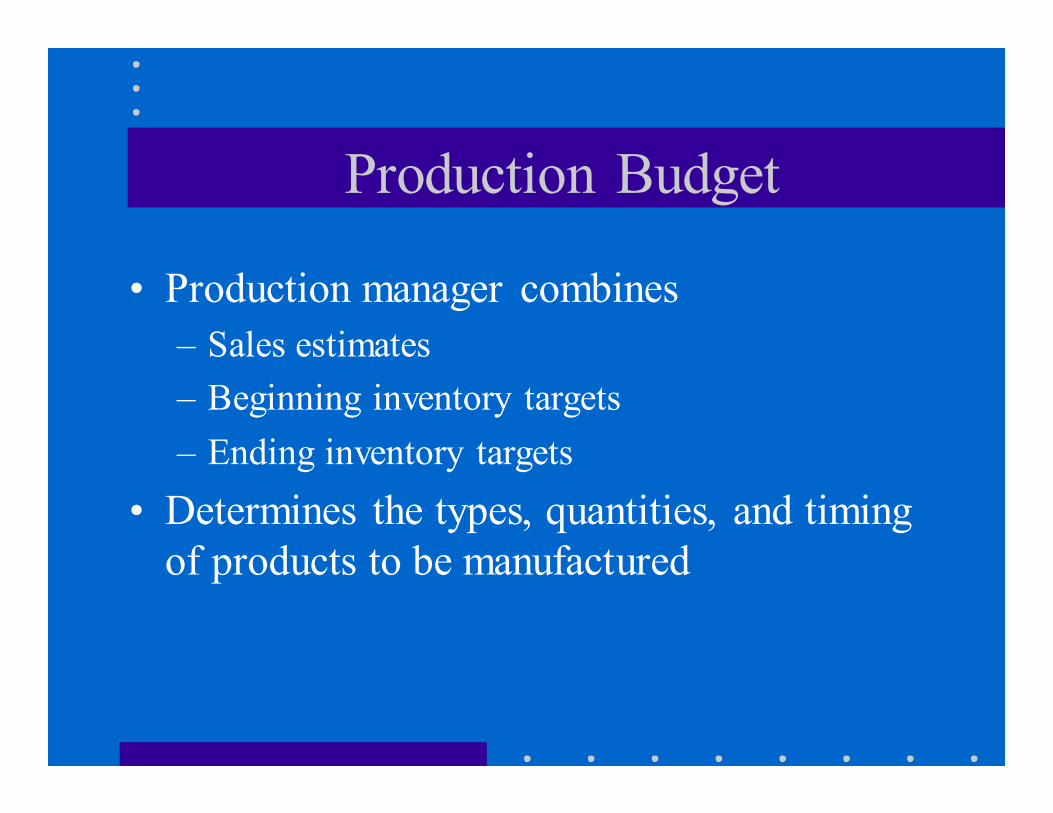

Production Budget

• Production manager combines

– Sales estimates

– Beginning inventory targets

– Ending inventory targets

• Determines the types, quantities, and timing

of products to be manufactured

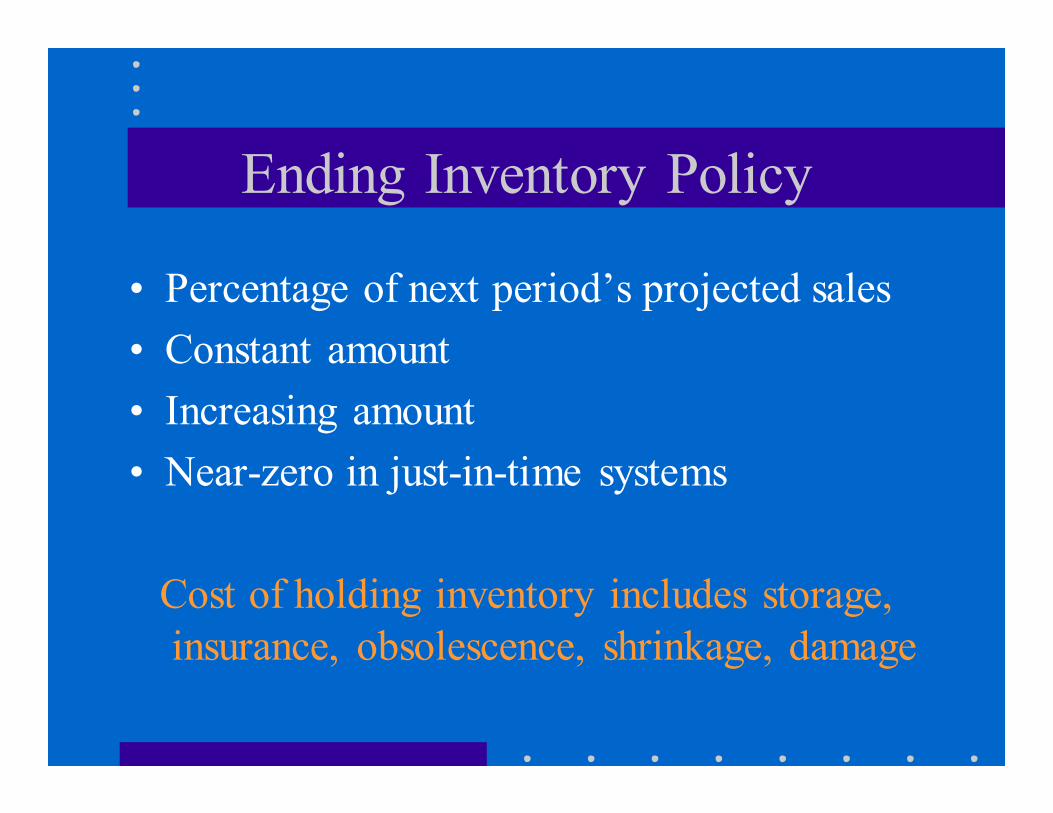

Ending Inventory Policy

• Percentage of next period’s projected sales

• Constant amount

• Increasing amount

• Near-zero in just-in-time systems

Cost of holding inventory includes storage,

insurance, obsolescence, shrinkage, damage

Production Budget

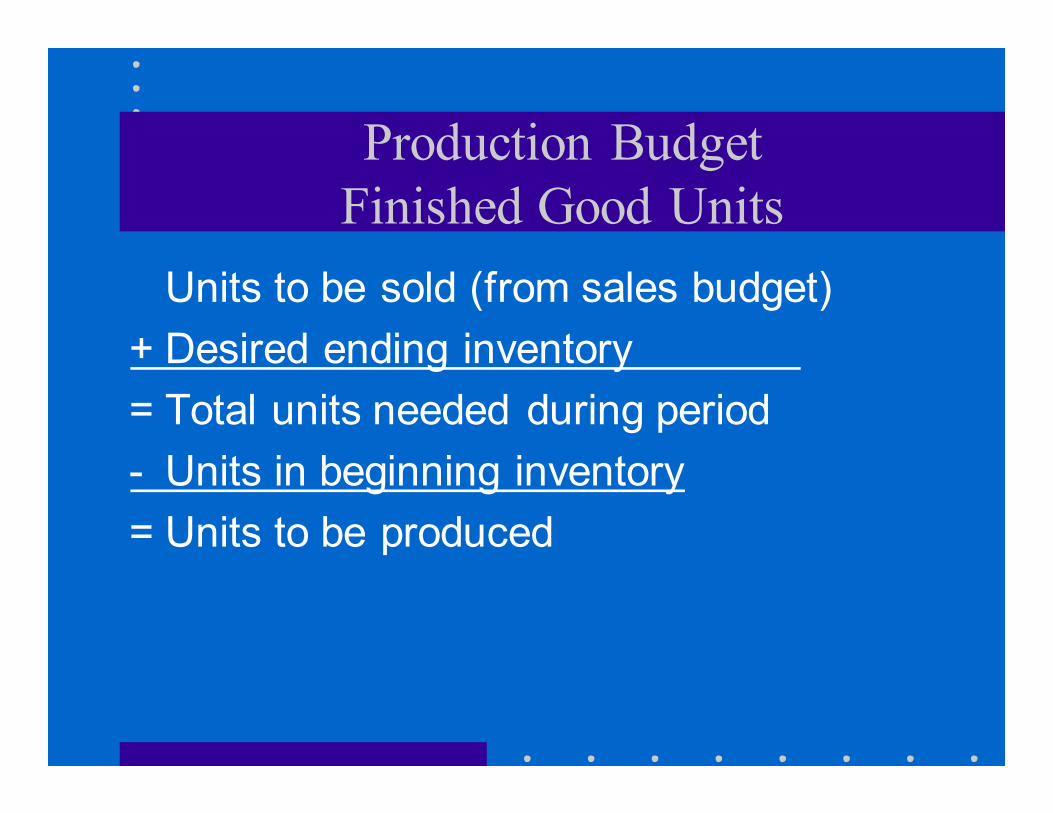

Finished Good Units

Units to be sold (from sales budget)

+ Desired ending inventory

= Total units needed during period

- Units in beginning inventory

= Units to be produced

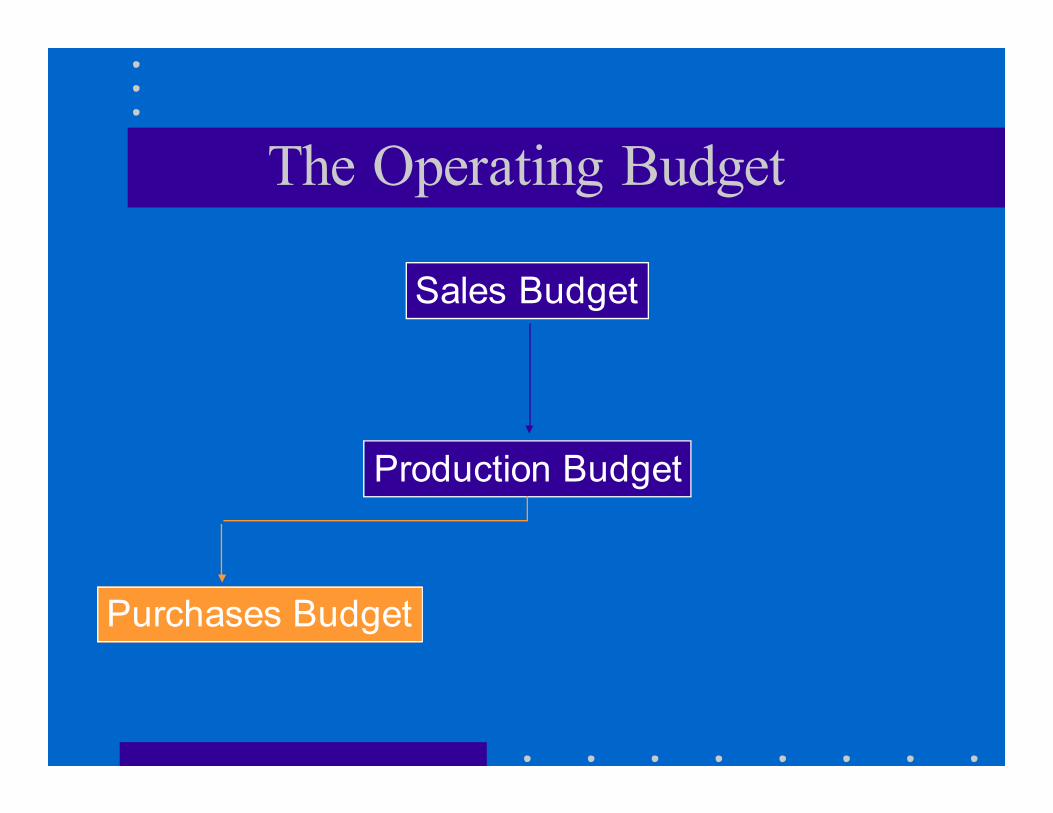

The Operating Budget

Sales Budget

Production Budget

Purchases Budget

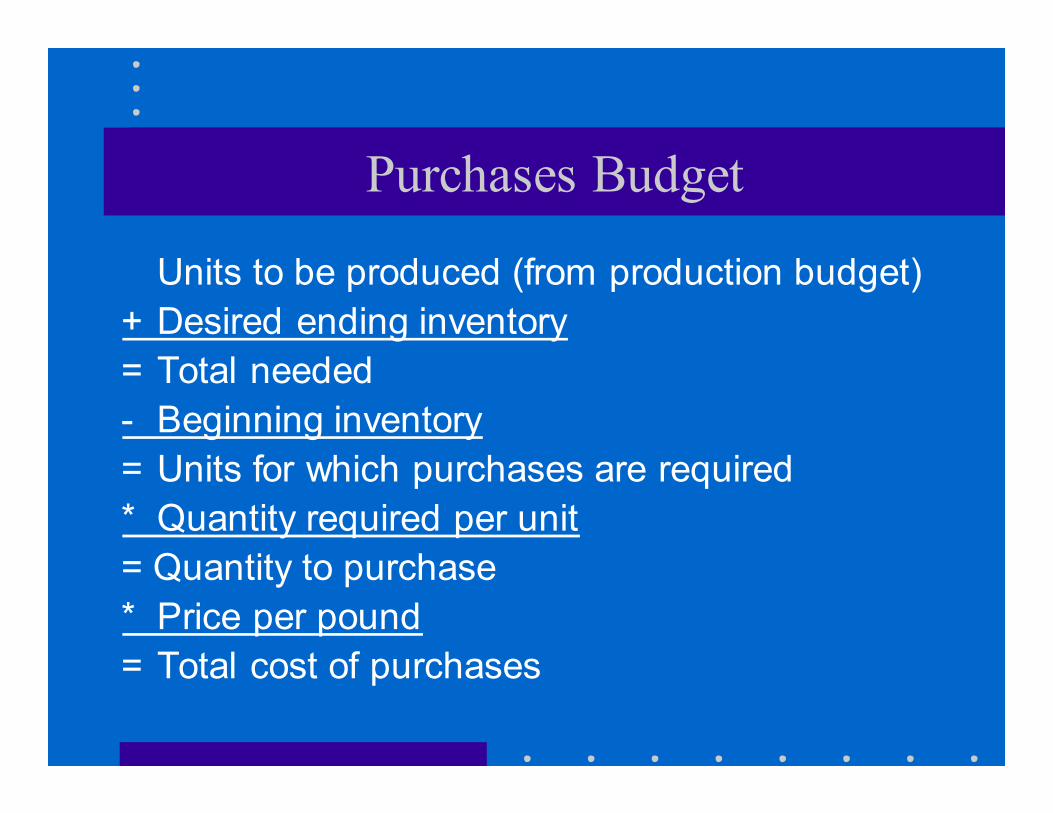

Purchases Budget

Units to be produced (from production budget)

+ Desired ending inventory

= Total needed

- Beginning inventory

= Units for which purchases are required

* Quantity required per unit

= Quantity to purchase

* Price per pound

= Total cost of purchases

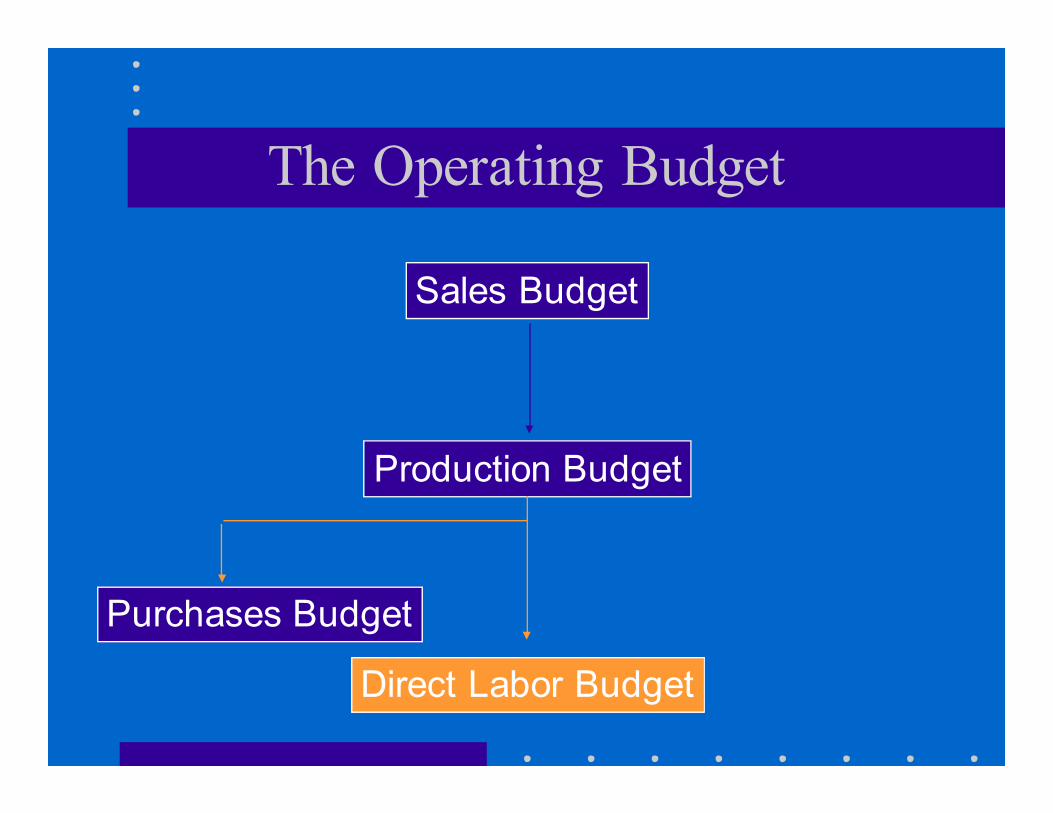

The Operating Budget

Sales Budget

Production Budget

Direct Labor Budget

Purchases Budget

Direct Labor Budget

• Total number of people

• Specific types of workers

• Production hours needed

• Costs

– Union contracts

– Minimum wage laws

– Fringe benefit costs

– Payroll taxes

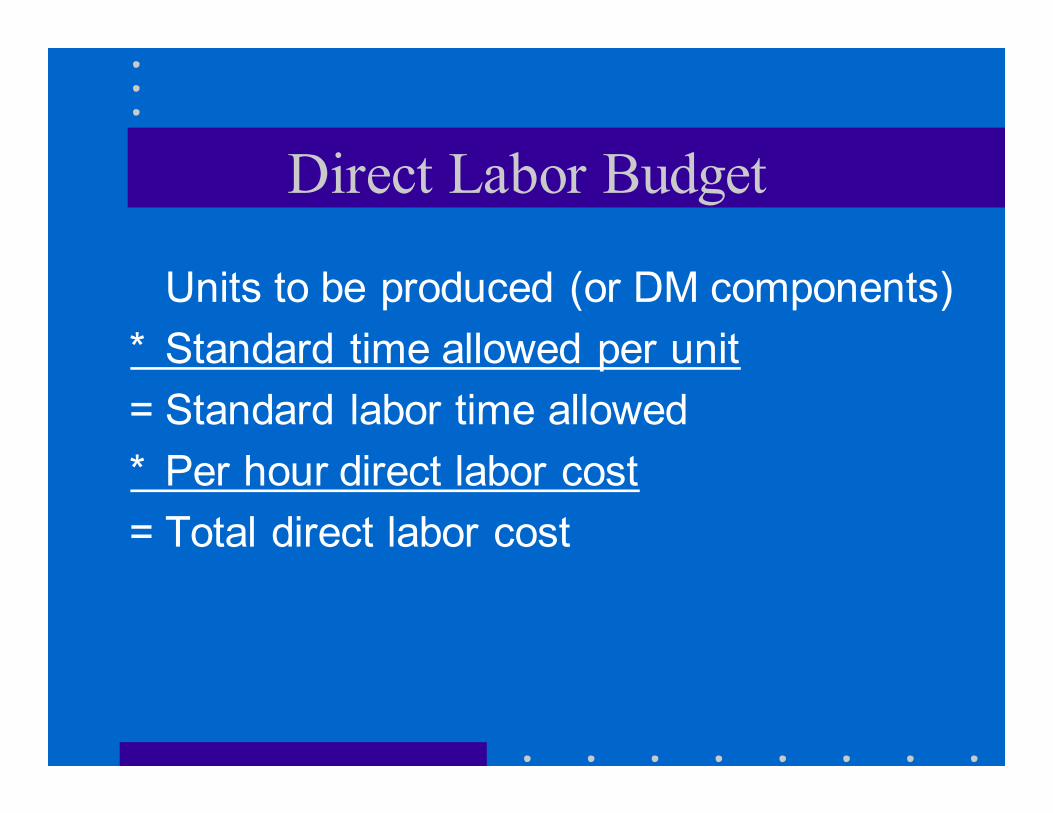

Direct Labor Budget

Units to be produced (or DM components)

* Standard time allowed per unit

= Standard labor time allowed

* Per hour direct labor cost

= Total direct labor cost

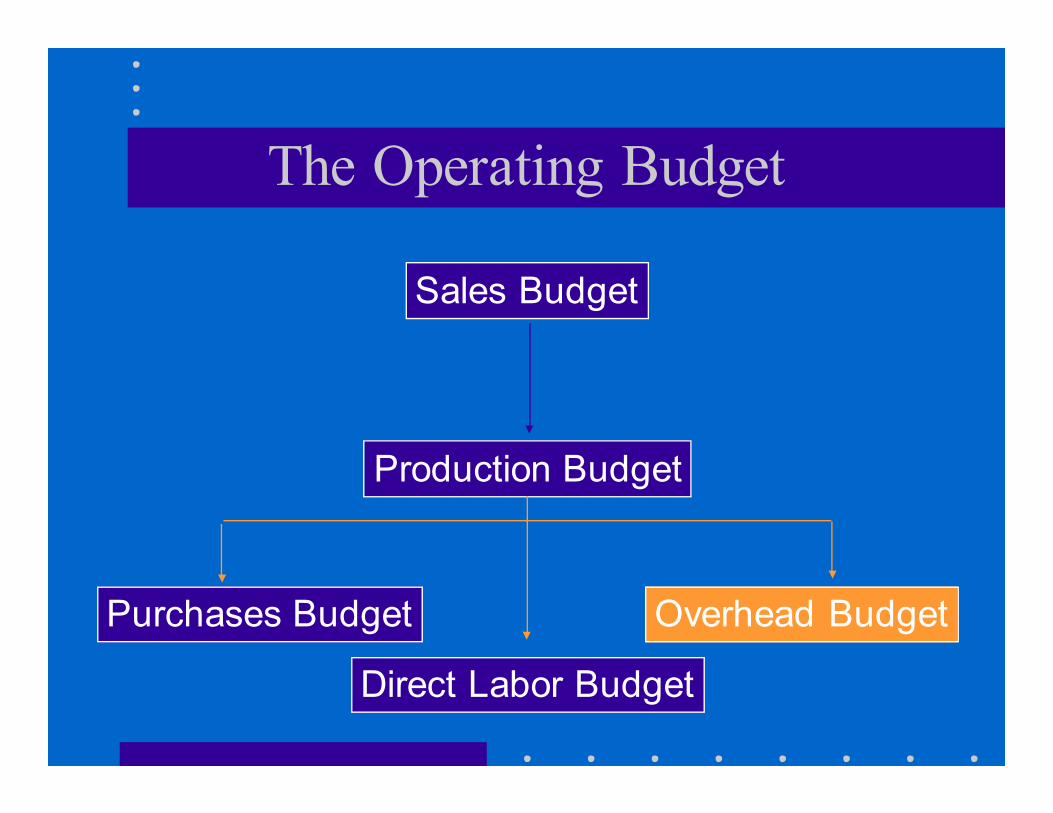

The Operating Budget

Sales Budget

Production Budget

Overhead Budget

Direct Labor Budget

Purchases Budget

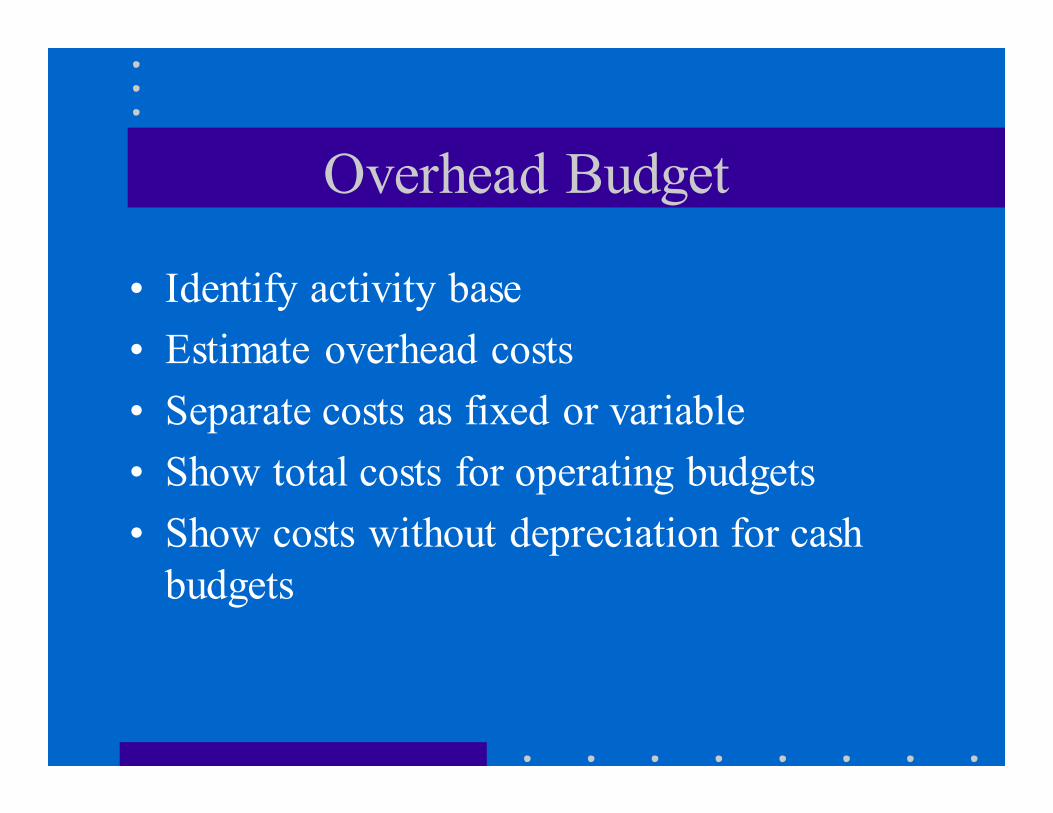

Overhead Budget

• Identify activity base

• Estimate overhead costs

• Separate costs as fixed or variable

• Show total costs for operating budgets

• Show costs without depreciation for cash

budgets

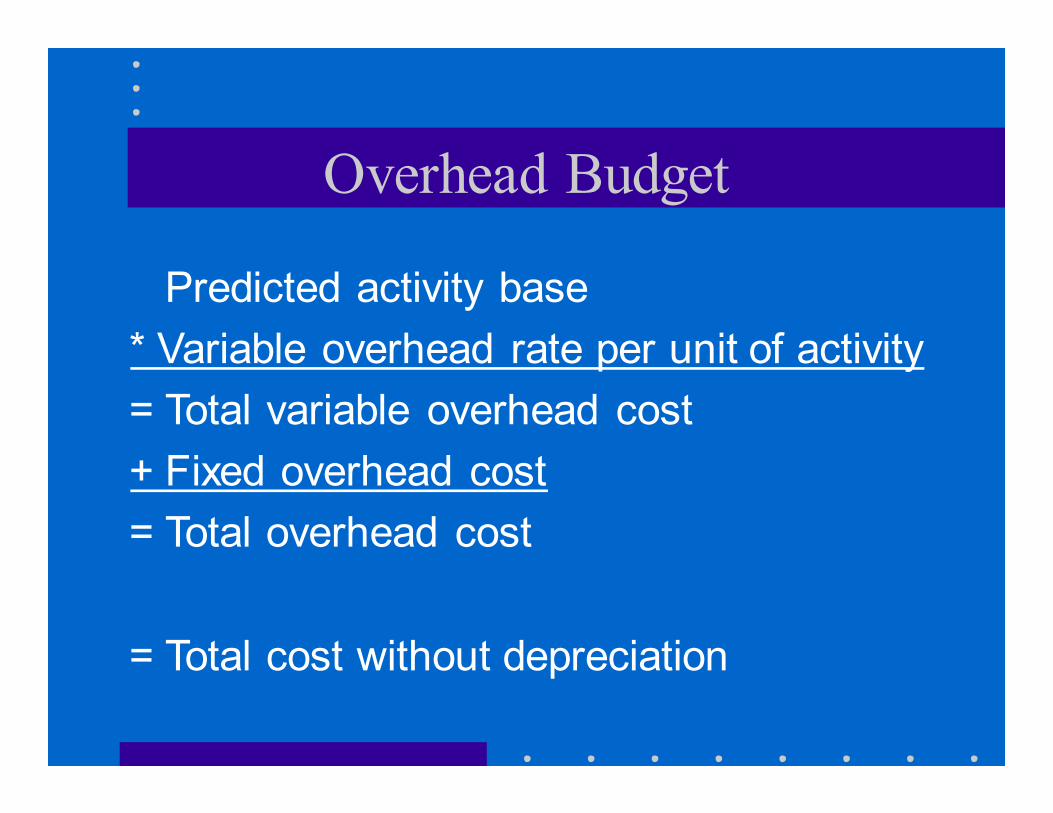

Overhead Budget

Predicted activity base

* Variable overhead rate per unit of activity

= Total variable overhead cost

+ Fixed overhead cost

= Total overhead cost

= Total cost without depreciation

The Operating Budget

Sales Budget

Production Budget

Overhead Budget

Direct Labor Budget

Purchases Budget

Selling and

Admin

Budget

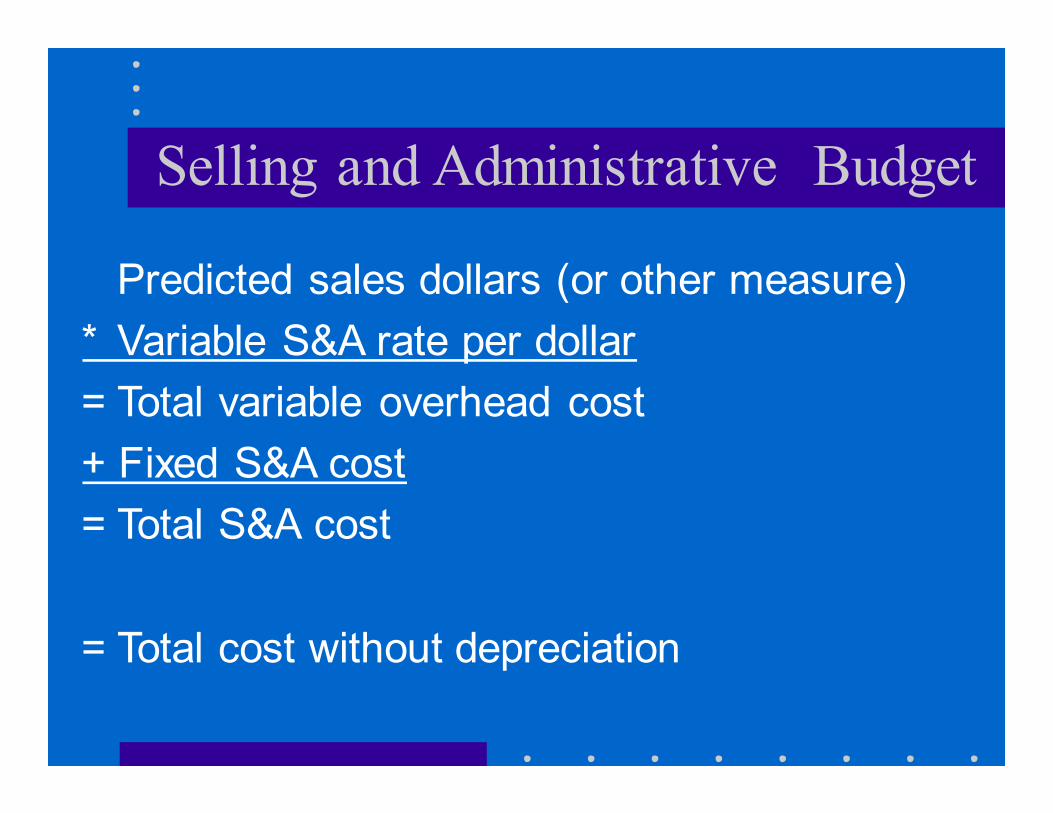

Selling and Administrative Budget

Predicted sales dollars (or other measure)

* Variable S&A rate per dollar

= Total variable overhead cost

+ Fixed S&A cost

= Total S&A cost

= Total cost without depreciation

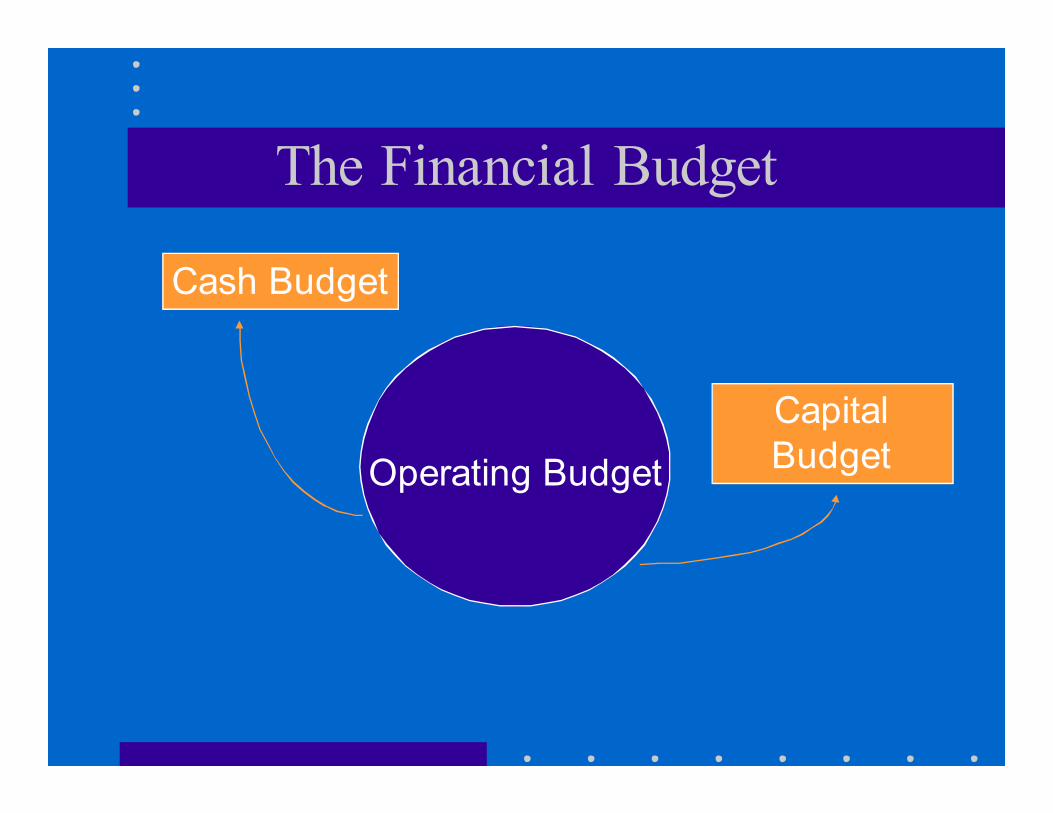

The Financial Budget

Operating Budget

The Financial Budget

Operating Budget

Cash Budget

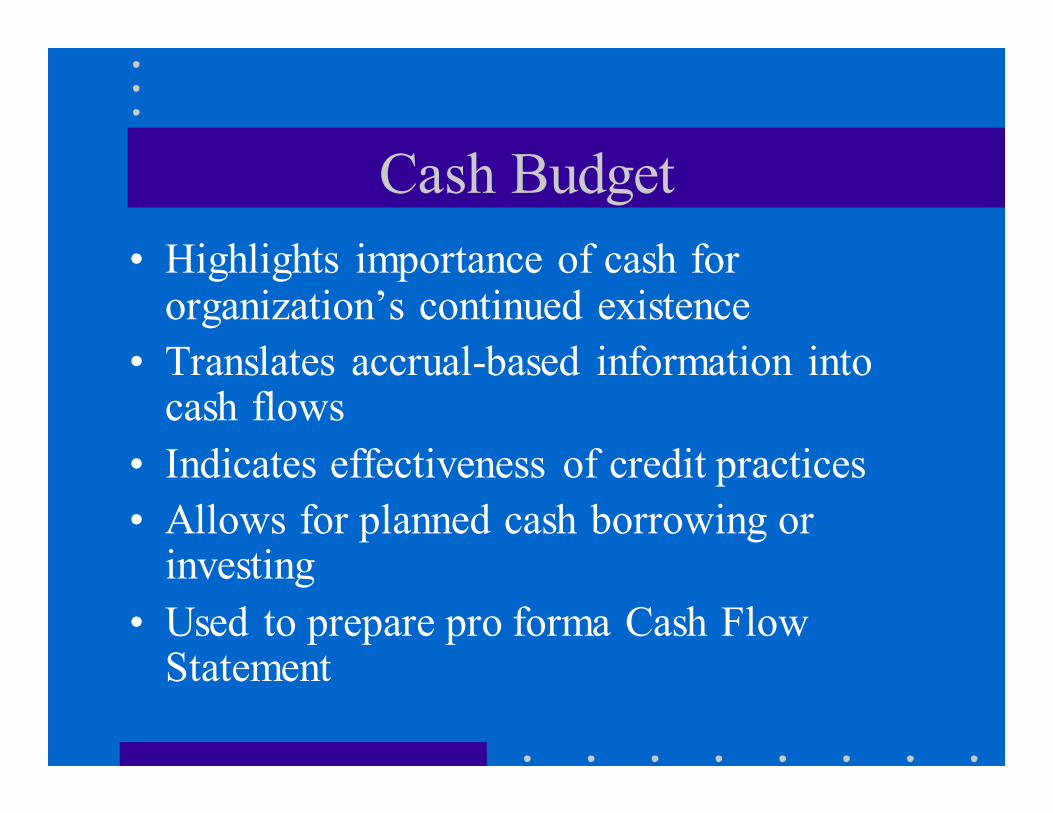

Cash Budget

• Highlights importance of cash for organization’s continued existence

• Translates accrual-based information into cash flows

• Indicates effectiveness of credit practices

• Allows for planned cash borrowing or investing

• Used to prepare pro forma Cash Flow Statement

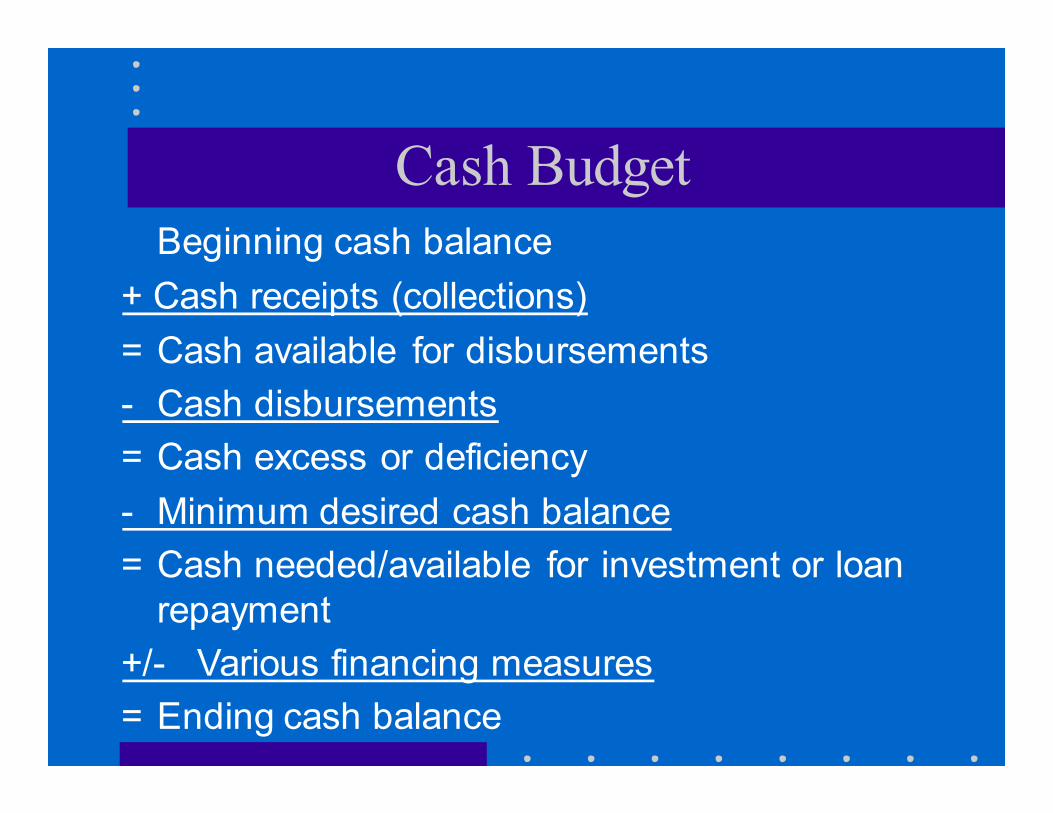

Cash Budget

Beginning cash balance

+ Cash receipts (collections)

= Cash available for disbursements

- Cash disbursements

= Cash excess or deficiency

- Minimum desired cash balance

= Cash needed/available for investment or loan

repayment

+/- Various financing measures

= Ending cash balance

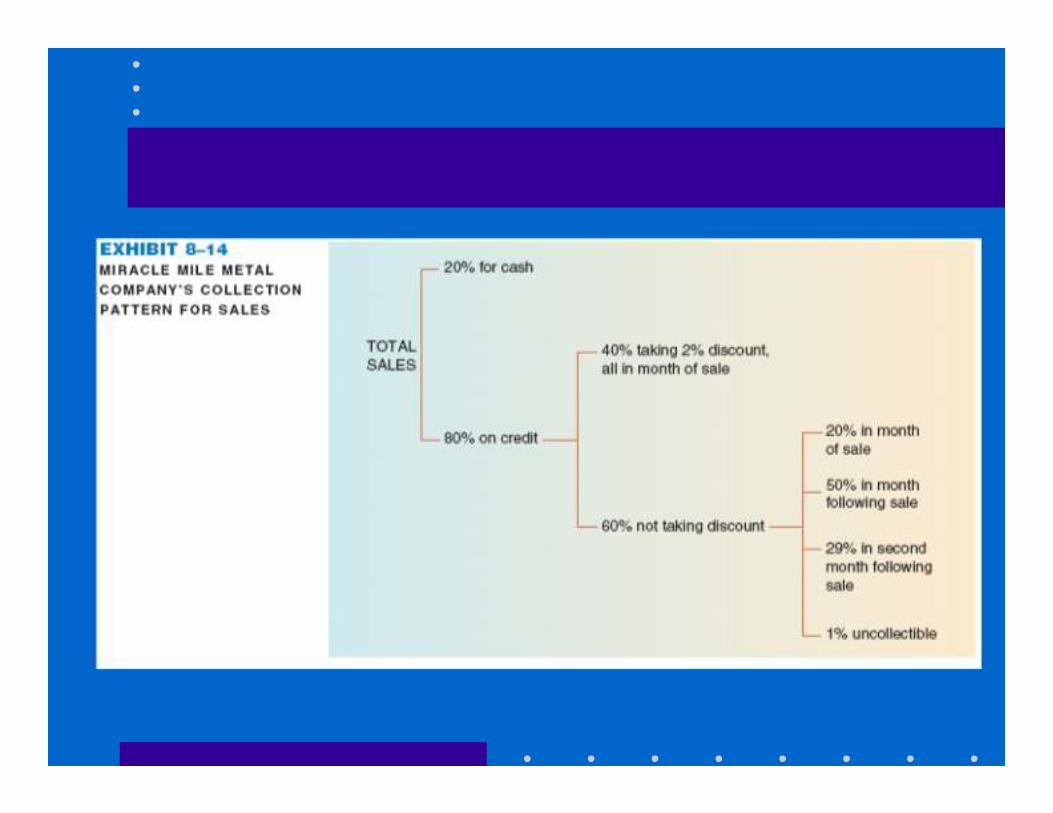

Cash Collections/Disbursements

• Collections

– Sales

• Cash

• Accounts Receivable

• Disbursements

– Purchases

• Cash

• Accounts Payable

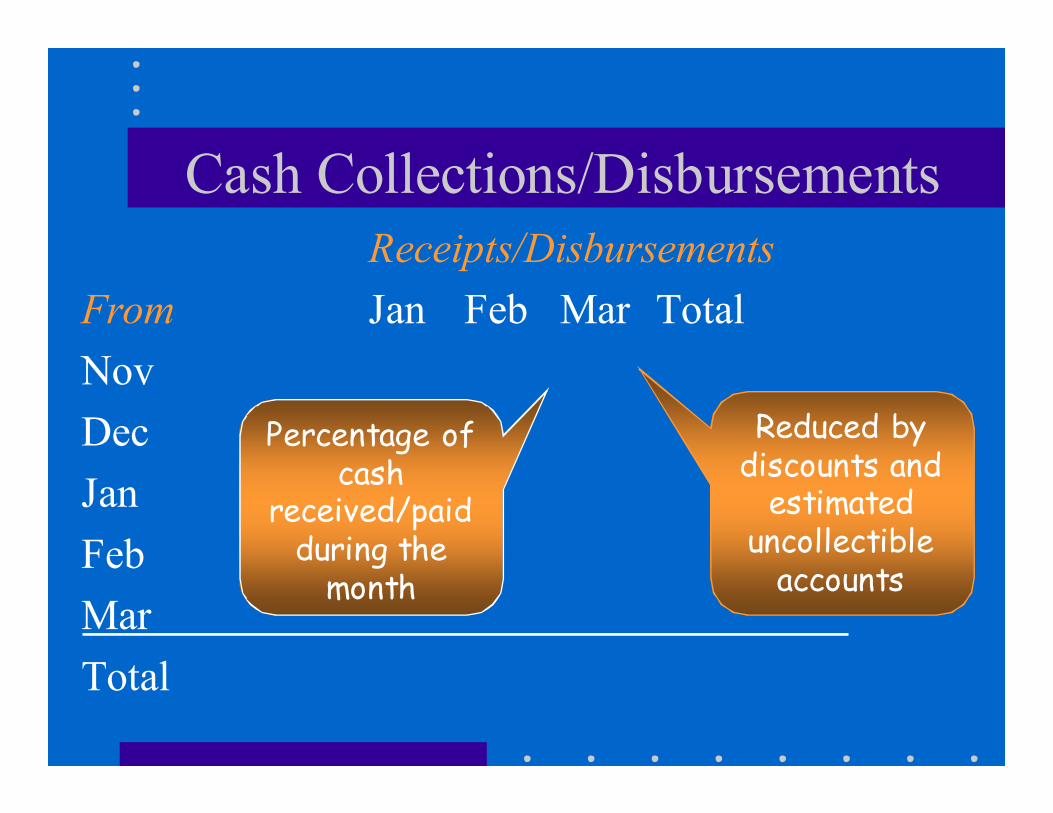

Receipts/Disbursements

From Jan Feb Mar Total

Nov

Dec

Jan

Feb

Mar

Total

Cash Collections/Disbursements

Reduced by discounts andestimated

uncollectible accounts

Percentage of cash

received/paid during the month

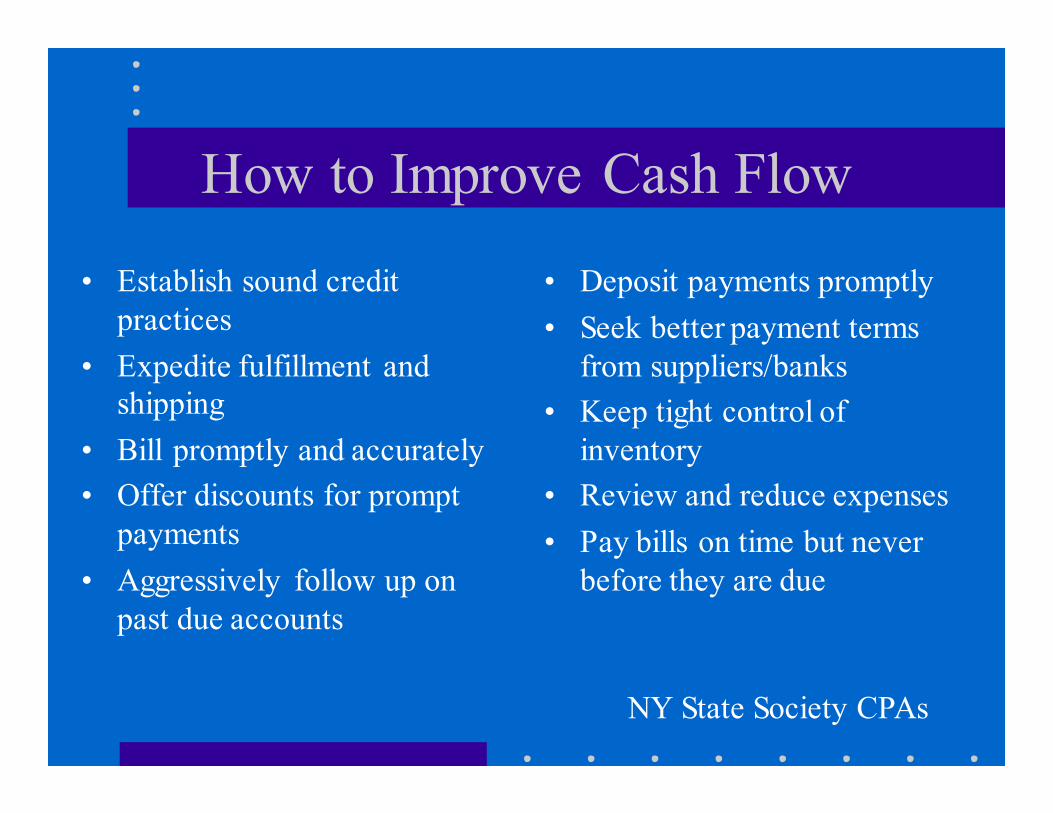

How to Improve Cash Flow

• Establish sound credit

practices

• Expedite fulfillment and

shipping

• Bill promptly and accurately

• Offer discounts for prompt

payments

• Aggressively follow up on

past due accounts

• Deposit payments promptly

• Seek better payment terms

from suppliers/banks

• Keep tight control of

inventory

• Review and reduce expenses

• Pay bills on time but never

before they are due

NY State Society CPAs

The Financial Budget

Operating Budget

Cash Budget

Capital

Budget

Capital Budget

• Long-term fixed asset needs

– Plant

– Equipment

• Payment points

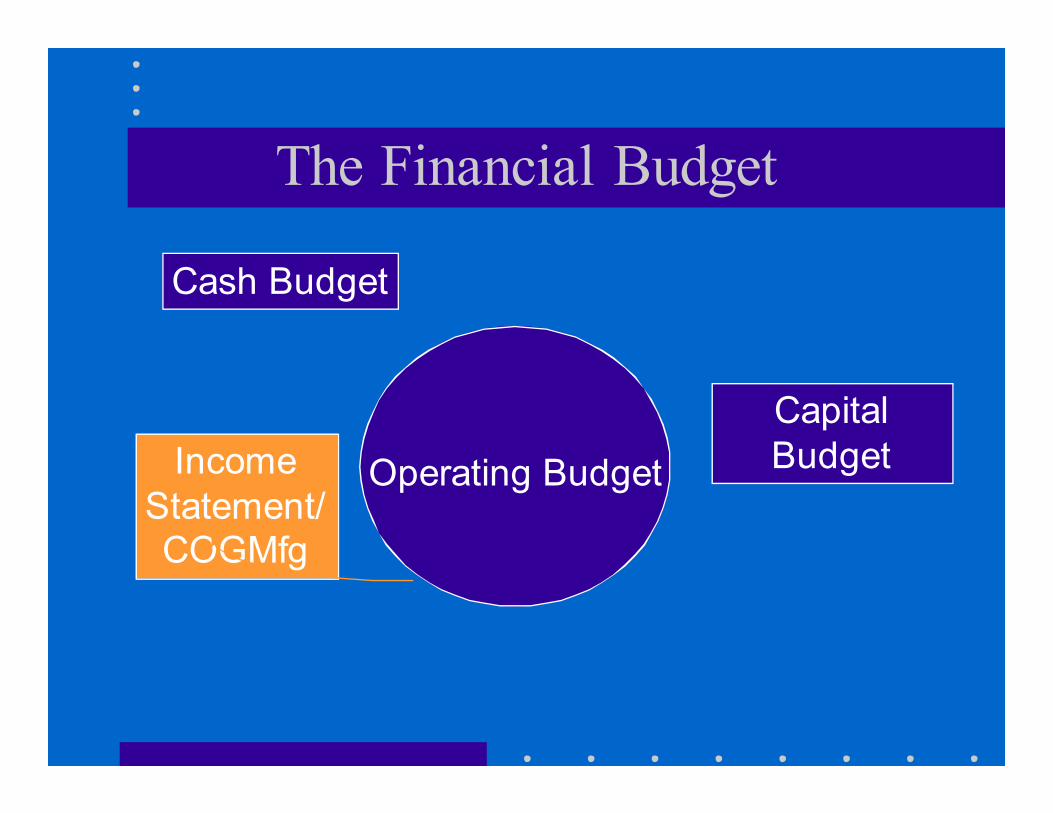

The Financial Budget

Operating Budget

Cash Budget

Capital

BudgetIncome

Statement/

COGMfg

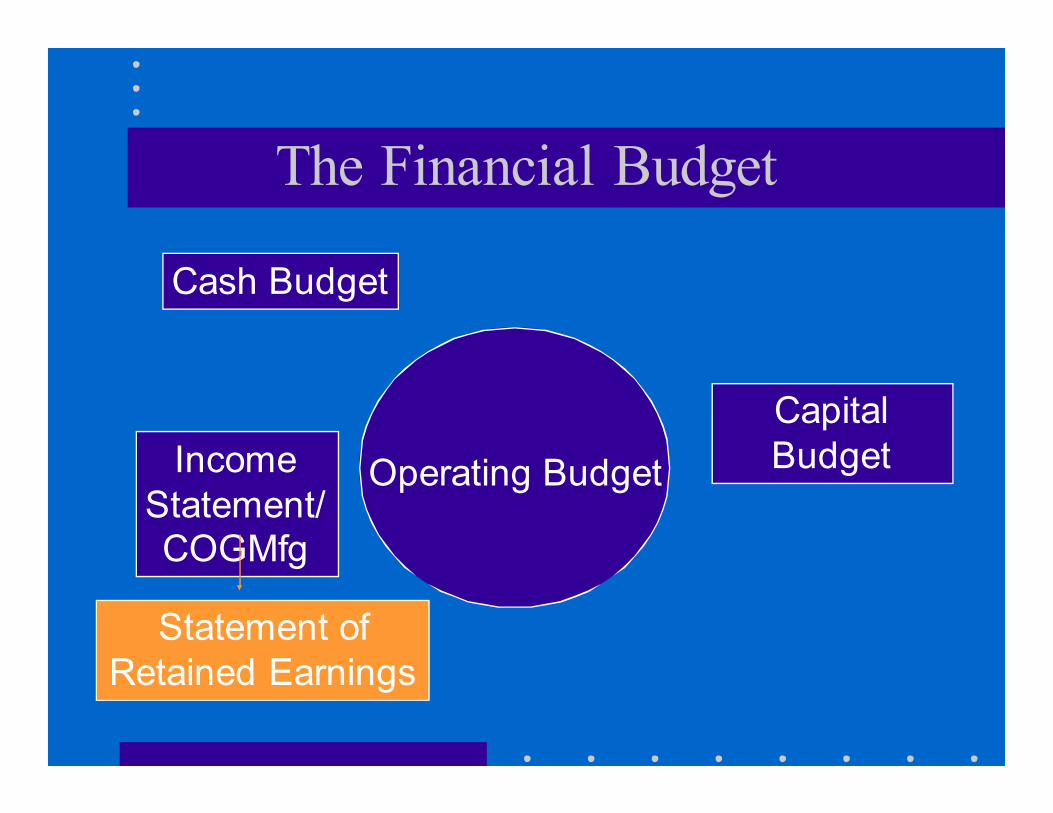

The Financial Budget

Operating Budget

Cash Budget

Capital

BudgetIncome

Statement/

COGMfg

Statement of

Retained Earnings

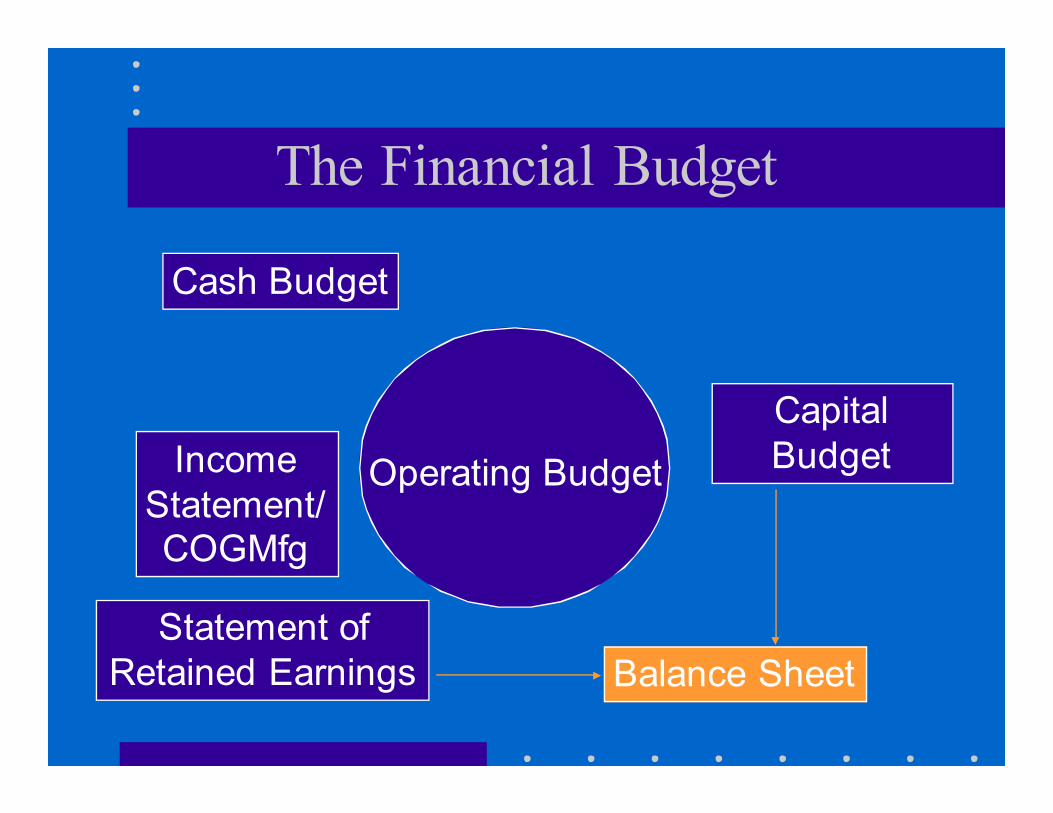

The Financial Budget

Operating Budget

Cash Budget

Capital

BudgetIncome

Statement/

COGMfg

Statement of

Retained Earnings Balance Sheet

The Financial Budget

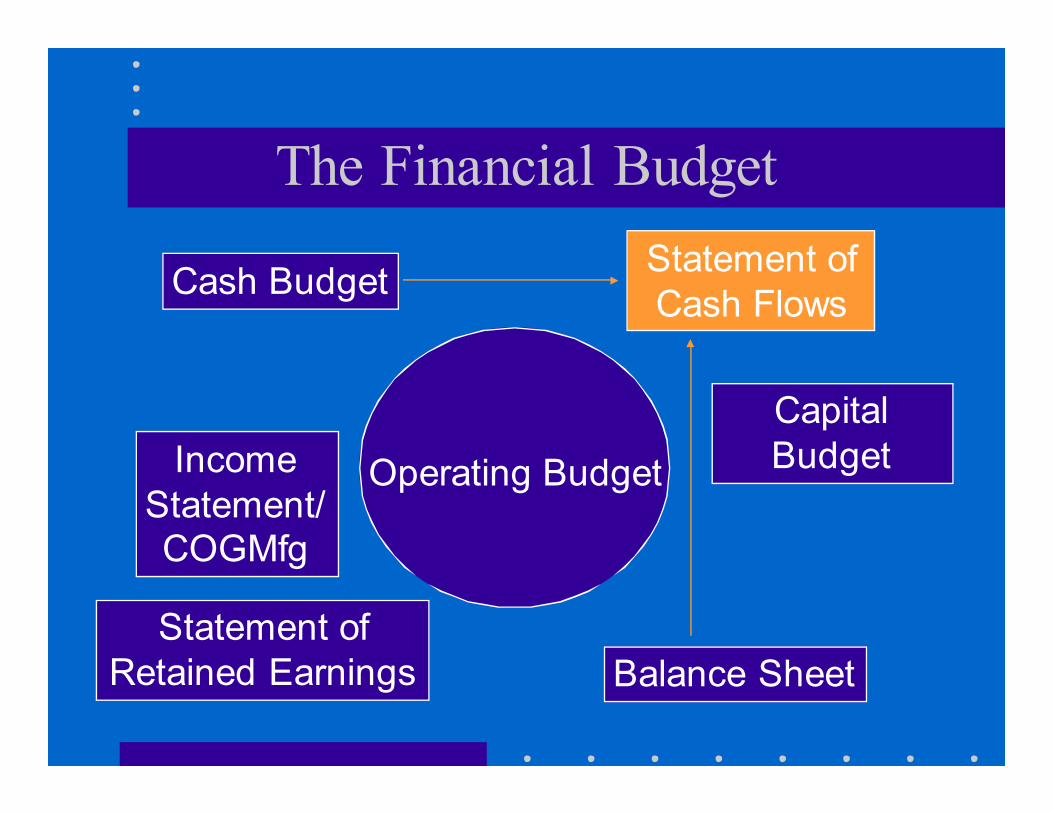

Operating Budget

Cash Budget

Capital

BudgetIncome

Statement/

COGMfg

Statement of

Retained Earnings Balance Sheet

Statement of

Cash Flows

Budgets Provide

• Guide to align activities and resources with

organizational goals

• Vehicle to promote employee participation,

cooperation, and departmental coordination

• Tool to enhance planning, controlling,

problem solving, and evaluating

Budget

Budgeting Provides

• Basis to sharpen responsiveness to internal

and external factors

• Model to view future performance and

consider alternative measures

• Benchmark to judge organizational

effectiveness and efficiency

Budget

Budgeting Terms

• Continuous budgeting

– 12-month rolling budget

Budgeting Terms

• Continuous budgeting

• Budget slack

– intentional underestimation of revenue

– intentional overestimation of expenses

Budgeting Terms

• Continuous budgeting

• Budget slack

• Participatory budget

– developed by top management and operating

personnel

Budgeting Terms

• Continuous budgeting

• Budget slack

• Participatory budget

• Imposed budgets

– developed by top management

– imposed on operating personnel

Activity Budget

• Connect line items in budget to list of

activities

• Raise awareness of non-value-added

activities

• Question and reduce non-value-added costs

Budget

Budget Manual

• Statements of budgetary purpose and its

desired results

• Listing of specific budgetary activities to be

performed

• Calendar of scheduled budgetary activities

• Sample of budgetary forms

• Original, revised, and approved budgets

Questions

• How are strategic and tactical planning

related to budgeting?

• In what order are the master budget

schedules prepared?

• Why is the cash budget important in the

master budgeting process?