corporate venture capital

TRANSCRIPT

Corporate Venture Capital

Overview CVC

Structural Strengths and Weaknesses

Investment Trends, Sectors and Players

Problem Statement

Frameworks for Successful CVCs

Based on Investment Type

Based on CVC Prevalence

Analysis

Intel Capital

Exxon Enterprises

Google Ventures

Optimizing Corporate Alpha

2

Agenda

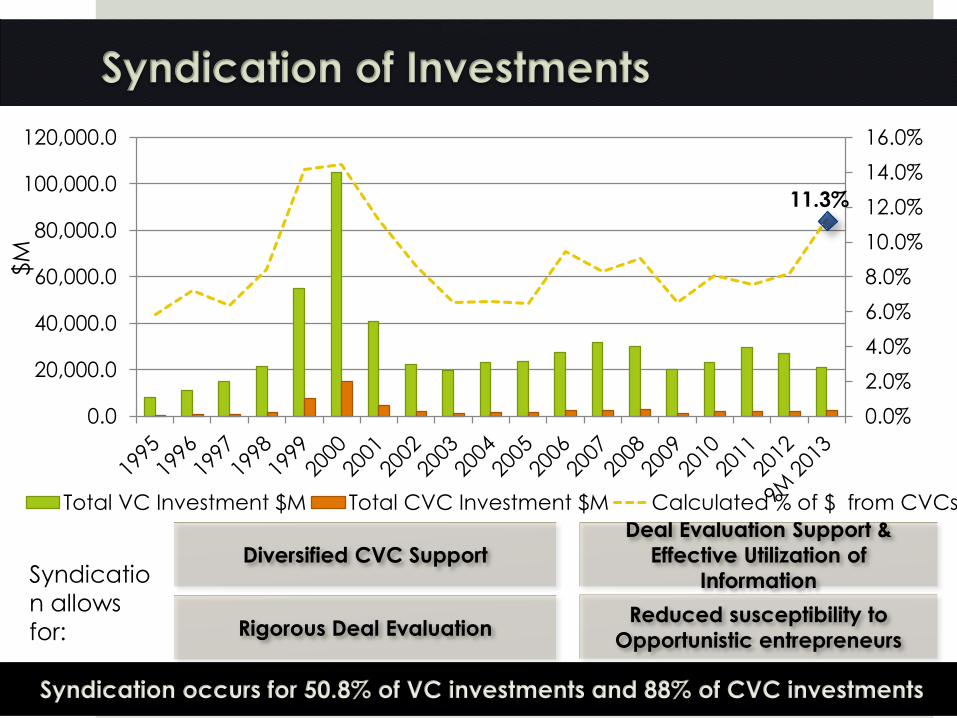

Syndication of Investments

Diversified CVC Support

Deal Evaluation Support &

Effective Utilization of

Information

Rigorous Deal EvaluationReduced susceptibility to

Opportunistic entrepreneurs

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0.0

20,000.0

40,000.0

60,000.0

80,000.0

100,000.0

120,000.0

Total VC Investment $M Total CVC Investment $M Calculated % of $ from CVCs

Syndicatio

n allows

for:

11.3%

Syndication occurs for 50.8% of VC investments and 88% of CVC investments

$M

CVC Objectives

› Intended to increase sales, reduce costs and by extension bolster profits

›Technological & business model innovations, opening new markets, ecosystem development, etc

Strategic type investments(unlike IVC)

›Largely focused on exit and buyout returnsFinancial

Investments(like IVC)

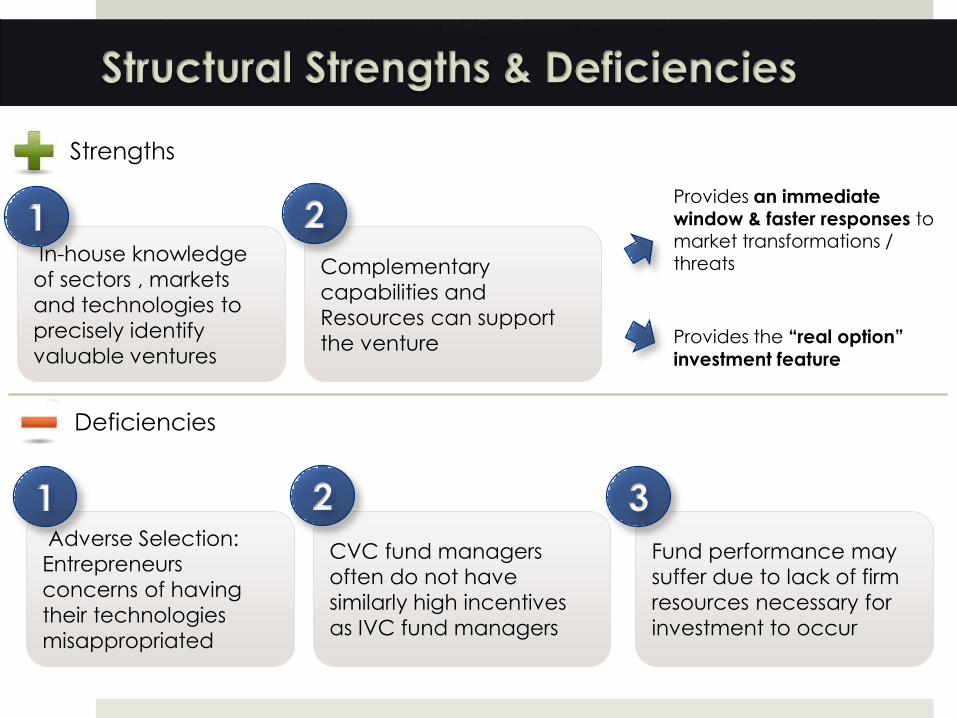

Structural Strengths & Deficiencies

In-house knowledge

of sectors , markets

and technologies to

precisely identify

valuable ventures

Complementary

capabilities and

Resources can support

the venture

21Provides an immediate window & faster responses to market transformations / threats

Provides the “real option”

investment feature

Adverse Selection:

Entrepreneurs

concerns of having

their technologies

misappropriated

CVC fund managers

often do not have

similarly high incentives

as IVC fund managers

21

Fund performance may

suffer due to lack of firm

resources necessary for

investment to occur

3

Strengths

Deficiencies

CVC – Measure of Value

Studies attempt to measure the value of CVC using Tobin’s Q, a statistical that

captures value of the firm beyond the value of its tangible assets

It is difficult to measure value of a CVC given that its

objectives are not purely financial and more strategic. Using

IRR is difficult as it is very difficult to distinguish individual

contributions of entities.

Total Exits & Total Acquisitions by

parent companyContinuity of a CVC

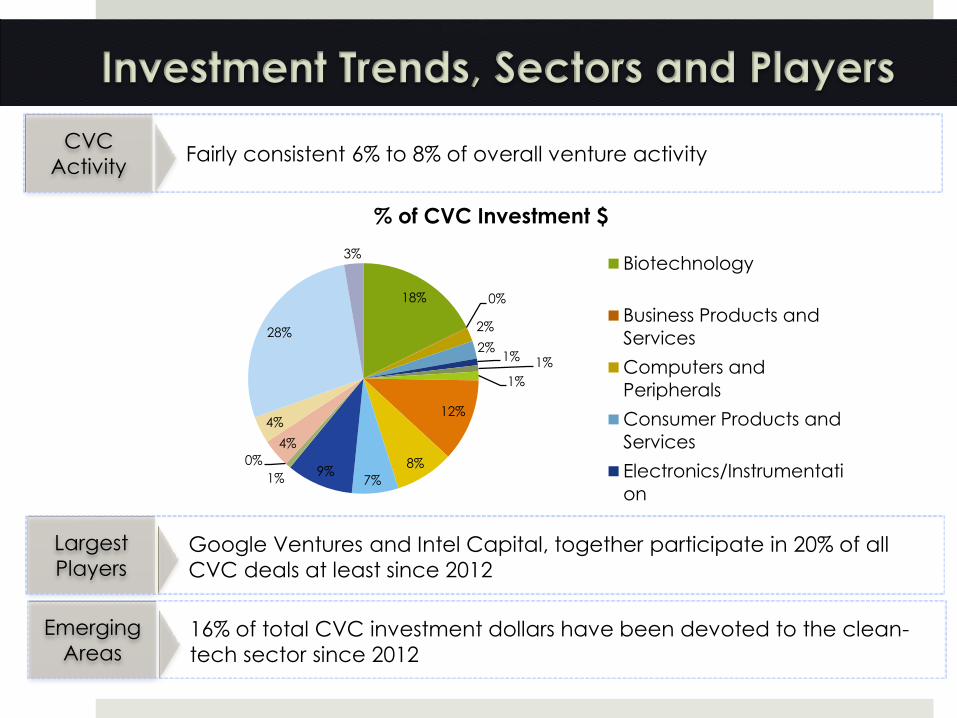

Investment Trends, Sectors and Players

CVC

ActivityFairly consistent 6% to 8% of overall venture activity

18% 0%

2%

2%1% 1%

1%

12%

8%

7%9%

1%

0%

4%

4%

28%

3%

% of CVC Investment $

Biotechnology

Business Products and

Services

Computers and

Peripherals

Consumer Products and

Services

Electronics/Instrumentati

on

Largest

Players Google Ventures and Intel Capital, together participate in 20% of all

CVC deals at least since 2012

Emerging

Areas16% of total CVC investment dollars have been devoted to the clean-

tech sector since 2012

Problem Statement

Median lifespan of corporate venture initiatives has traditionally

been one year making corporations hesitant to partake in CVC

CVC investments have been very cyclical over 40 years in line

with Independent VC investments. If the investments are strategic

and considering the strengths of CVC over Independent VC’s,

one would expect lesser correlation between the two.

Only 3% of CVC Investments have resulted in an acquisition by

the parent company

A conceptual term that captures all benefits that a CVC can get in terms

of sustained competitive advantage from their investments

Need for “Corporate α”

CVC Trends

Click to edit Master title style

Click to edit Master subtitle style

2014-12-13

Frameworks for successful CVC investments

CVC Success Frameworks

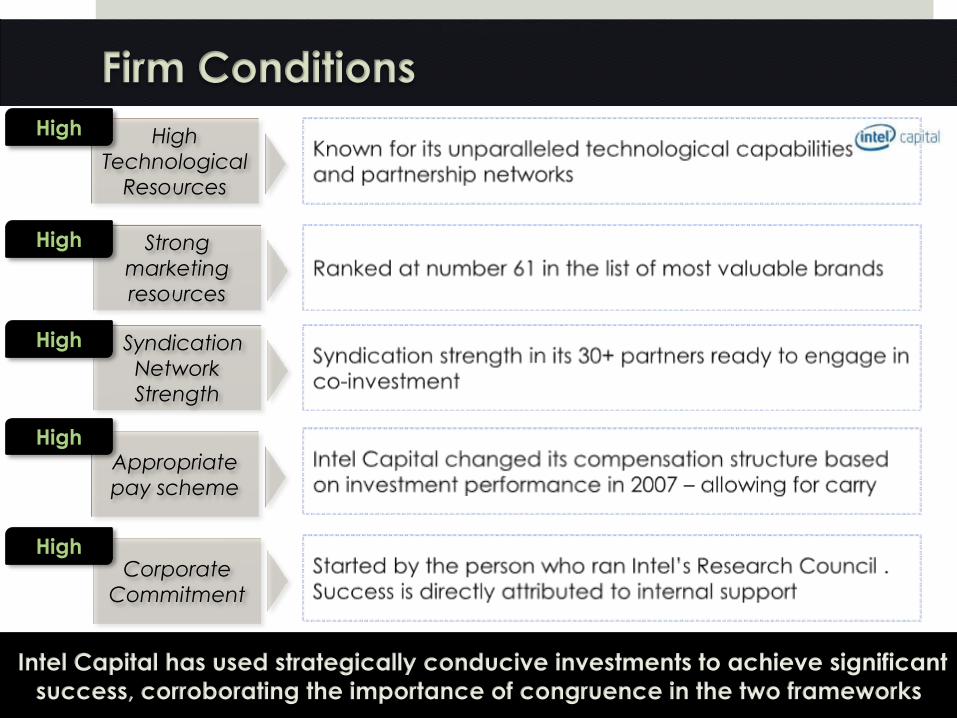

High Technological

Resources

Strong marketing resources

Syndication Network Strength

Appropriate pay scheme

Corporate Commitment

Firm Conditions

Industry Competition

IndustryConditions

Technological Change

Industry

Appropriability

Corporate

α

Investment Type

This framework is

established using academic

literature, and provides a

systematic approach to

achieve CVC investment

success

Interlinked

Industry and Firm

Conditions(Micro & Macro)

Analysis of 3 CVCs

Analysis of three real world examples to explore each framework individually and

establish linkage that exists between them to obtain investment success

Research shows that companies with the highest strategic orientation emerged

as the top-most performers in CVC investments

Investment

Type

CVC Trends

Click to edit Master title style

Click to edit Master subtitle style

2014-12-13

Intel Capital

Intel Capital

Intel Capital is a VC arm of the Intel

Corporation, and is considered

one of the most successful CVC

enterprises in the world

Approximately does 100 to 150 deals per year ranging from $300 to $500 M

Success rate of 41%

Of the 550 exits, 259 have been acquired by Intel

Cyclicality of

Investment

Parent company

Acquisitions

CVC

Continuity

Investment Type

Built up expertise in

multiple microprocessors

related sectors – Ex:

data centre and cloud

services

Invests in sub-sectors:

wearable technologies

(heads-up display (HUD)

devices, arm bands-

MYO etc.)

Investments to increase

Intel’s growth by inflating

the demand for its chips

- video, audio, graphics

hardware, and software

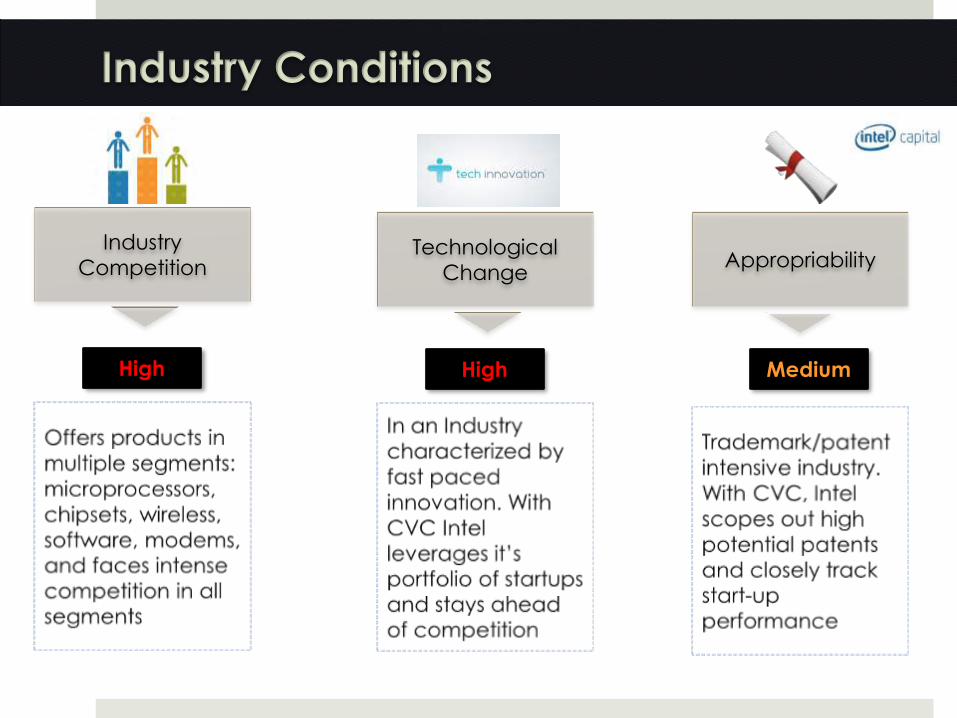

Industry Conditions

Industry

Competition Technological

Change Appropriability

High High Medium

Firm Conditions

High

Technological

Resources

Strong

marketing

resources

Syndication

Network

Strength

Appropriate

pay scheme

Corporate

Commitment

High

High

High

High

High

Intel Capital has used strategically conducive investments to achieve significant

success, corroborating the importance of congruence in the two frameworks

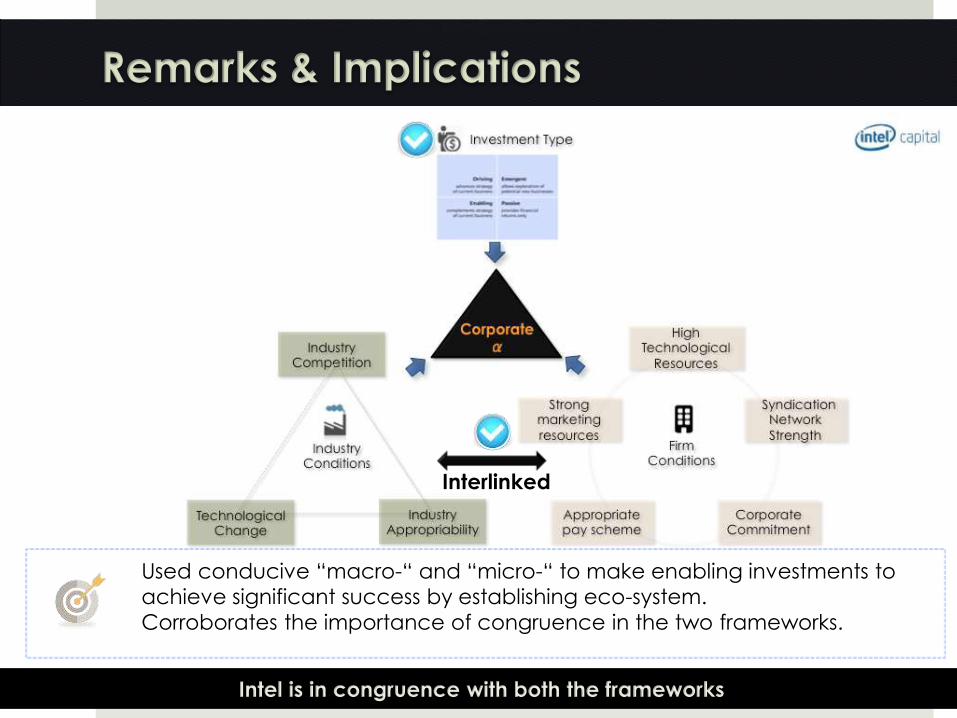

Remarks & Implications

Interlinked

Intel is in congruence with both the frameworks

Used conducive “macro-“ and “micro-“ to make enabling investments to

achieve significant success by establishing eco-system.

Corroborates the importance of congruence in the two frameworks.

CVC Trends

Click to edit Master title style

Click to edit Master subtitle style

2014-12-13

Exxon Enterprises

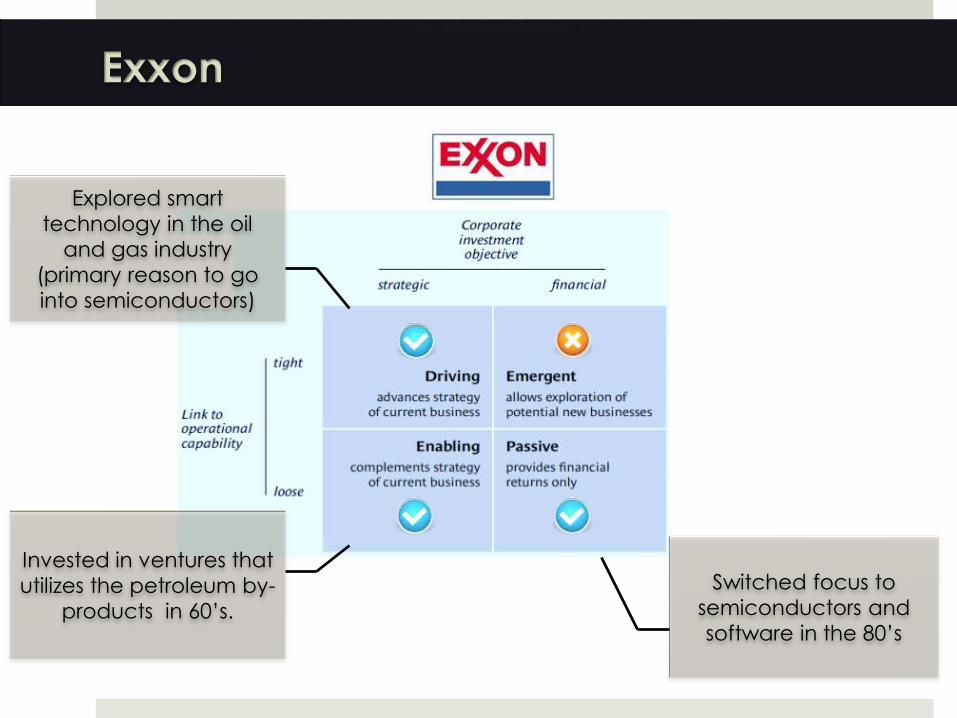

Exxon Enterprises

Founded in the 60’s and over the course of 20 years, the company

shifted from one line of business to another

1970’s to 1980’s - Carried out 2 stage venturing program

18 Ventures and 12M in

investment

19 Ventures

Stage

Stage

Valued at $218M by 1982

(IRR OF 51%)

None were successful

1980 : Acquisition of Zilog and Exxon’s $1B debacle

Acquired Zilog for $1BBut failed with the 16 bit

microproccessor

Exxon closed down Exxon Enterprises and sold the company for less than $1M.

Cyclicality of

Investment

Parent company

Acquisitions

CVC

Continuity

Exxon

Explored smart

technology in the oil

and gas industry

(primary reason to go

into semiconductors)

Switched focus to

semiconductors and

software in the 80’s

Invested in ventures that

utilizes the petroleum by-

products in 60’s.

Industry Conditions

Industry

Competition Technological

change Appropriability

High High Low

We do an analysis in the context of the semiconductor industry

Firm Conditions

High

Technological

Resources

Strong

marketing

resources

Syndication

Network

Strength

Appropriate

pay scheme

Corporate

Commitment

Low

Low

High

The analysis is done in the context of the semiconductor industry

Low

Med

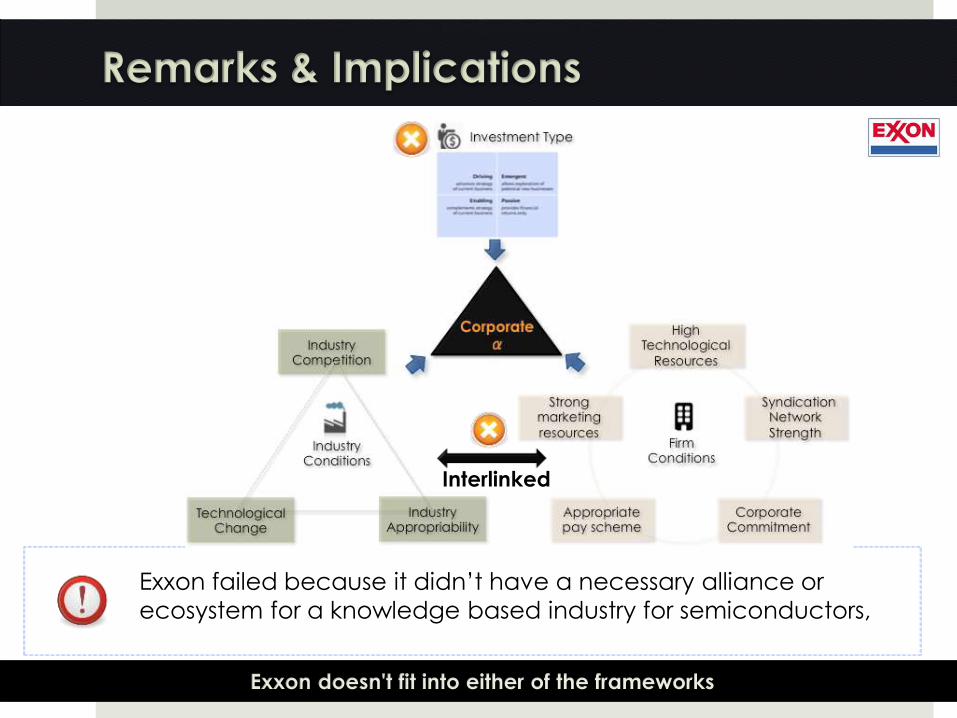

Remarks & Implications

Exxon failed because it didn’t have a necessary alliance or

ecosystem for a knowledge based industry for semiconductors,

Interlinked

Exxon doesn't fit into either of the frameworks

CVC Trends

Click to edit Master title style

Click to edit Master subtitle style

2014-12-13

Google Ventures

Google Ventures

Investment Philosophy: “We provide seed, venture growth and growth stage

funding to the best companies – not strategic investments for Google”

225 Companies 6 Different Sectors

Founded in 2009, with $100 million in commitment. Total total assets under

management has increased to over $1.5 billion

Second most successful in terms of exits behind Intel. But they have acquired

only 2 companies out of 225 companies they have invested in.

Does not exclusively use the traditional VC approach, and instead uses data

mining algorithms to make investment decisions

Cyclicality of

Investment

Parent company

Acquisitions

CVC

Continuity

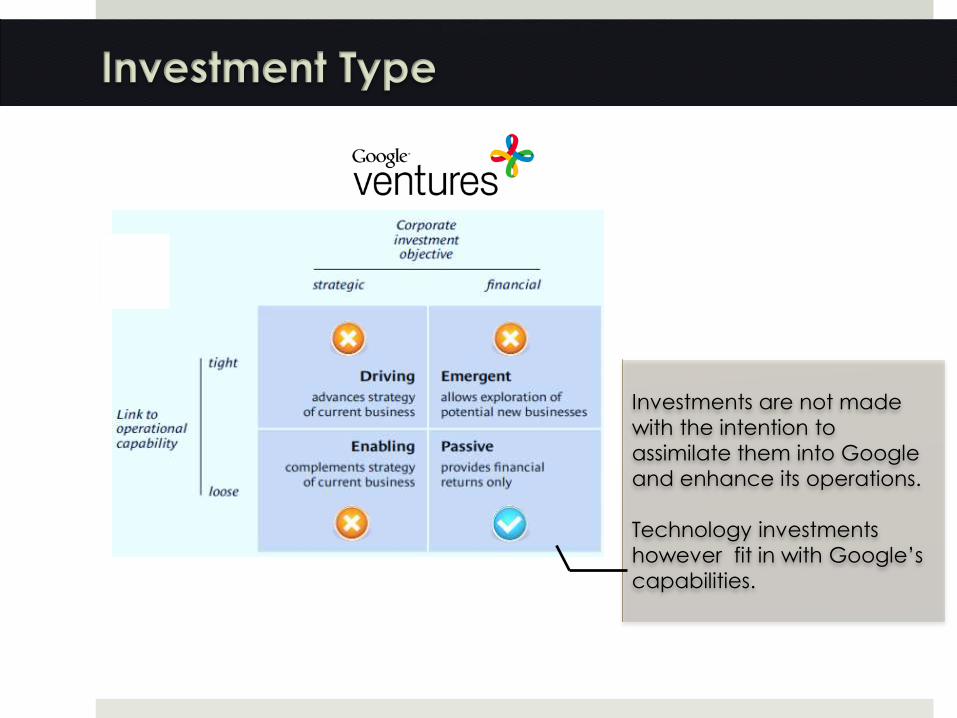

Investment Type

Investments are not made

with the intention to

assimilate them into Google

and enhance its operations.

Technology investments

however fit in with Google’s

capabilities.

Current Portfolio

Investmentsfocused on the development mobile apps and app development technologies

Notable StartupsUBERPocketTuneinStampedngmoco

Focused on the development of enterprise-focused software and data capacity solutions

Notable StartupsClouderaDocuSignHubspotOptimizelyDasient

Investments in firms participating in online commerce & online platforms

Notable StartupsNestAbout.meKabamFitStarNextDoor

Investmentsfocused on methods, not necessarily online technology, to improve health or further scienceNotable Startups23andMeOne Medical GroupFoundation MedicineAdimab

Driving Potential

Enabling Potential

Emergent Potential

Passive Current

Portfolio

Only 2 Companies were acquired by Google out of the 225 startups

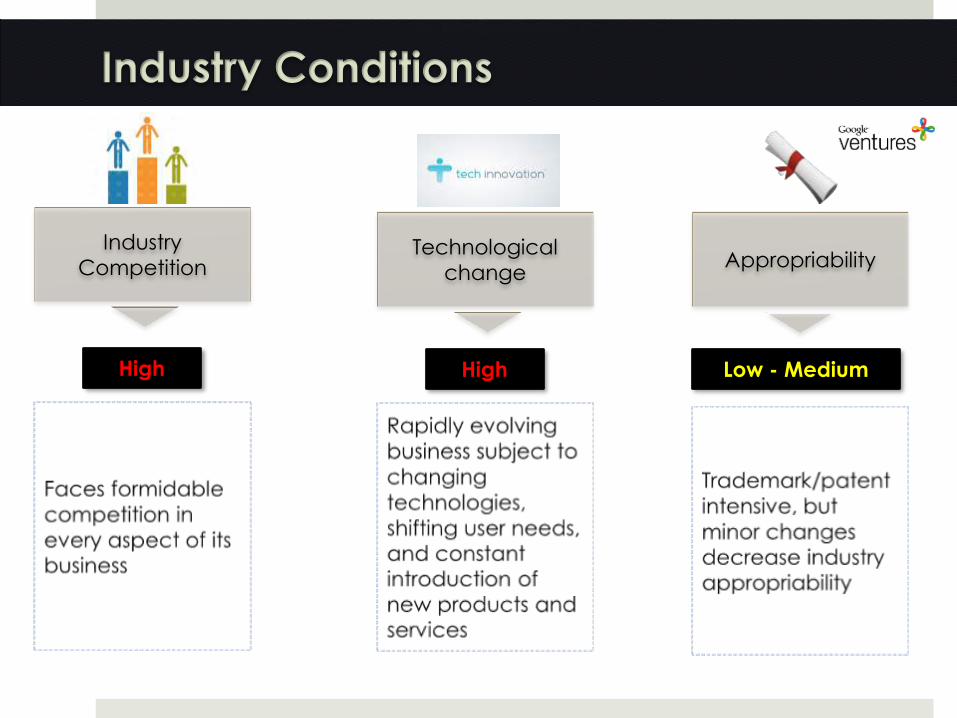

Industry Conditions

Industry

Competition Technological

change Appropriability

High High Low - Medium

Firm Conditions

High

Technological

Resources

Strong

marketing

resources

Syndication

Network

Strength

Appropriate

pay scheme

Corporate

Commitment

High

High

High

High

High

Google’s success rate simply in terms of exits has been very good and second

only to Intel

Remarks & Implications

Google Venture’s approach to VC is purely an IVC one and

attempts to leverage its internal resources

Interlinked

Google Ventures is congruent with first framework, but fits into the second

Optimizing Corporate α

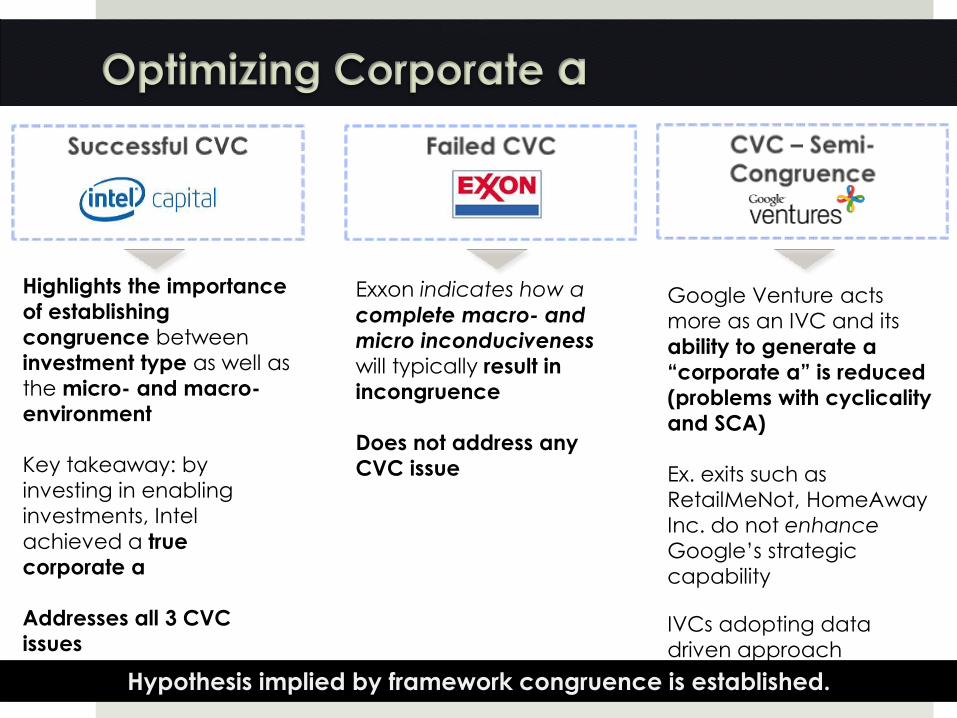

Highlights the importance

of establishing

congruence between

investment type as well as

the micro- and macro-

environment

Key takeaway: by

investing in enabling

investments, Intel

achieved a true

corporate α

Addresses all 3 CVC

issues

Exxon indicates how a

complete macro- and

micro inconduciveness

will typically result in

incongruence

Does not address any

CVC issue

Google Venture acts

more as an IVC and its

ability to generate a

“corporate α” is reduced

(problems with cyclicality

and SCA)

Ex. exits such as

RetailMeNot, HomeAway

Inc. do not enhance

Google’s strategic

capability

IVCs adopting data

driven approach

Hypothesis implied by framework congruence is established.

Refining the Framework: Sub-Investment Type

SuccessfulCVCs

Program Objective Driving Enabling Emergent Passive

Market development ★ ★ ★

New Product Development

★

New Product Dev & Talent Recruitment

★

Seed / “real option” investments

★

New biotech product development

★

Intel Capital has been doing so well because they had/have a very strong enabling focus, which makes it less cyclical to IVC investment

0.00.51.01.52.02.53.0

Coefficient of Variation for CVC Investments

Compared to Total VC InvestmentsCVC Investments Compared to Total VC Investments

**Parent acquisition information not available, so relegated to cyclicality to measure strategic value-add

CVC Trends

Click to edit Master title style

Click to edit Master subtitle style

2014-12-13

Course : Venture Capital

Research by :

Sergey Mokin

Rajan Kalsi

Isaac Bamgboje

Aditya Tripuraneni

Arun Krishna