corporate tax in malaysia: revenue, … paper/ic... · corporate tax in malaysia: revenue, ... of...

TRANSCRIPT

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 67

CORPORATE TAX IN MALAYSIA: REVENUE, COLLECTION AND ENFORCEMENT

Nor Shaipah Abdul Wahab Taylor’s Business School

Taylor’s University, Malaysia [email protected]

ABSTRACT

This study analyses Malaysian corporate tax position in contributing to the country’s economic position through Federal Government revenue. Discussions on the effective tax systems are centred on Adam Smith’s Canons of Taxation and The Mirrlees Review’s characteristic of effective tax system. Corporate taxation is found to be the highest contributor to Federal Government revenue compared to other components of direct taxes, i.e. individual tax, petroleum tax and other direct taxes. With a maximum contribution of 29.5 percent to the revenue across years, the composition of direct taxes to the total revenue is made up by corporate tax at the largest, followed by individual tax, petroleum

tax and others. This is consistent and significant for the 14-year period (2=39.9, p<0.01). This trend is expected to continue for future years due to effective enforcement policy of the tax authority.

Keywords: Corporate tax, Tax revenue, Tax collection

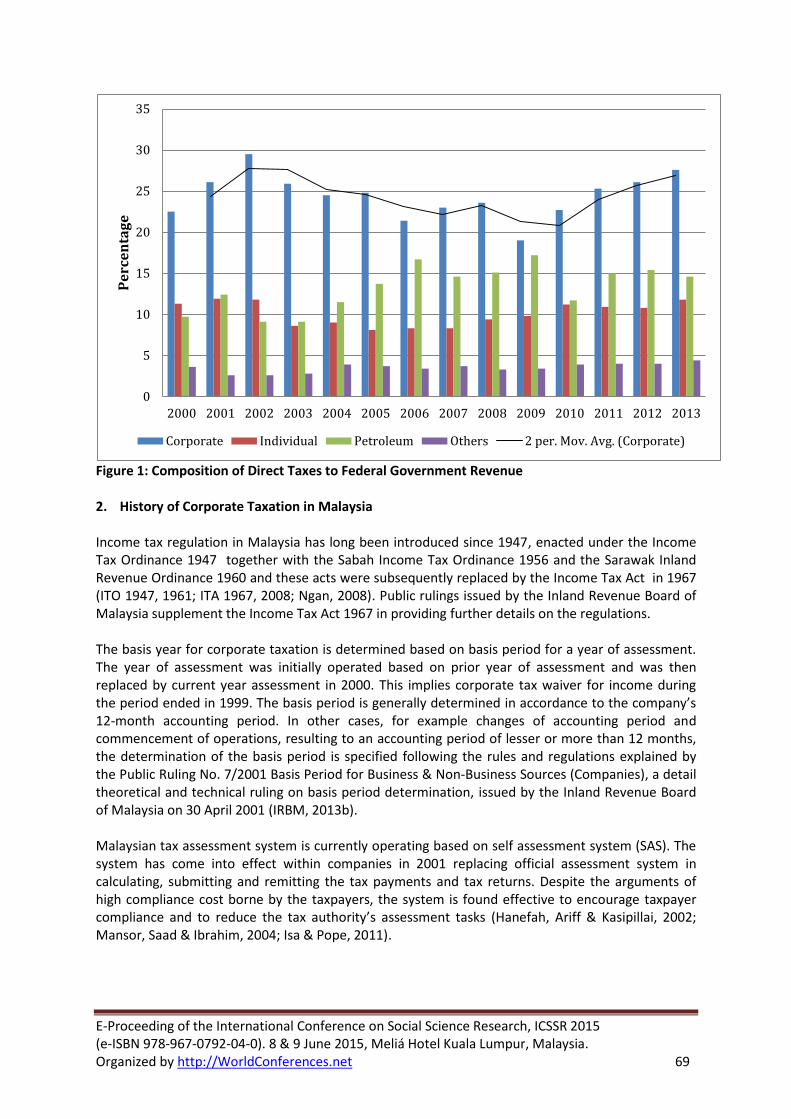

1. Introduction Corporate taxation, a component of direct taxes, is imposed in a year of assessment on Malaysian resident companies (ITA 1967, 2008). The residential status is determined through companies’ exercise of management and control. Management and control is normally deemed to be exercised in Malaysia in cases where the board of director meetings are held in the country and the meetings are argued should only be related to management and control of the companies (Tiley, 2005). Non-resident companies are obligated to Malaysian tax only on income accruing in or derived from sources within Malaysia (ITA 1967, 2008). For both residents and non-residents, foreign income is exempted from tax with the exception for resident companies that run sea and air transportation, insurance and banking businesses which are specified as subject to income tax under world scope basis compared to derivation basis for the others. Corporate taxation has long been identified as amongst the source of revenue to the Government. Despite this, there is limited number of studies that investigate the behaviour of Malaysian corporate taxation in contributing to the country’s income. The aim of this paper therefore is to analyse corporate taxation position as a source of revenue to the Malaysian Federal Government. Corporate taxation in Malaysia represents a significant portion of revenue to the Government. Table 1 displays the composition of components of direct taxes to the Federal Government Revenue. The proportions of the components are presented in column III, IV, V and VI respectively for corporate, individual, petroleum and other taxes. Throughout 14-year sample period (2000 to 2013), corporate taxation outnumbered other components of direct taxes, suggesting the Federal Government revenue has been consistently and substantially contributed by the corporate taxation.1 Contribution of corporate taxation to the revenue is at the highest rank in 2002 (29.5 percent), followed by 2013

1 Year 2000 is to reflect the starting year of current year assessment.

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 68

(27.6 percent), and 2012 (26.1 percent) and 2001 (26.1 percent) at the third rank. The lowest corporate tax composition is documented at 19 percent in 2009 but it is still relatively higher than other components (individual, petroleum and others). The contribution of individual tax becomes the third after the petroleum tax and this is followed by the other direct taxes component. Although the other taxes contribute least to the revenue, the magnitude is increasing throughout the years with the highest portion of 4.4 percent in 2013. The difference between the components of direct taxes, i.e. corporate, individual, petroleum and others, in the composition towards total revenue is

significant across the sample period (2=39.9, p<0.01). This suggests corporate tax is the consistent and significant highest contributor to the Federal Government revenue than the other counterparts. Table 1: Composition of Direct Taxes to Federal Government Revenue

Year Total tax revenue

(RM million)

Composition of direct taxes to total

revenue (%)

Composition to total revenue

Corporate tax (%)

Individual tax (%)

Petroleum tax (%)

Other direct

taxes (%)

I II III IV V VI

2000 61,864 47.1 22.5 11.3 9.7 3.6

2001 79,567 52.9 26.1 11.9 12.4 2.6

2002 83,515 53.1 29.5 11.8 9.1 2.6

2003 92,608 46.4 25.9 8.6 9.1 2.8

2004 99,387 49.0 24.5 9.0 11.5 3.9

2005 106,304 50.4 24.8 8.1 13.7 3.7

2006 123,546 49.8 21.4 8.3 16.7 3.4

2007 139,885 49.6 23.0 8.3 14.6 3.7

2008 159,793 51.4 23.6 9.4 15.1 3.3

2009 158,639 49.4 19.0 9.8 17.2 3.4

2010 159,653 49.5 22.7 11.2 11.7 3.9

2011 185,419 55.1 25.3 10.9 15.0 4.0

2012* 207,246 56.4 26.1 10.8 15.4 4.0

2013* 208,650 58.4 27.6 11.8 14.6 4.4

Source: Ministry of Finance, Malaysia http://www.treasury.gov.my * Estimated data Figure 1 exhibits the trend of compositions of components of direct taxes from 2000 to 2013. The trend line of 2-period moving average for corporate taxation indicates a slight fluctuation of proportion across years. The composition of corporate taxation has reached its peak in 2002 and at the other continuum, hit the lowest proportion in 2009.

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 69

Figure 1: Composition of Direct Taxes to Federal Government Revenue 2. History of Corporate Taxation in Malaysia Income tax regulation in Malaysia has long been introduced since 1947, enacted under the Income Tax Ordinance 1947 together with the Sabah Income Tax Ordinance 1956 and the Sarawak Inland Revenue Ordinance 1960 and these acts were subsequently replaced by the Income Tax Act in 1967 (ITO 1947, 1961; ITA 1967, 2008; Ngan, 2008). Public rulings issued by the Inland Revenue Board of Malaysia supplement the Income Tax Act 1967 in providing further details on the regulations. The basis year for corporate taxation is determined based on basis period for a year of assessment. The year of assessment was initially operated based on prior year of assessment and was then replaced by current year assessment in 2000. This implies corporate tax waiver for income during the period ended in 1999. The basis period is generally determined in accordance to the company’s 12-month accounting period. In other cases, for example changes of accounting period and commencement of operations, resulting to an accounting period of lesser or more than 12 months, the determination of the basis period is specified following the rules and regulations explained by the Public Ruling No. 7/2001 Basis Period for Business & Non-Business Sources (Companies), a detail theoretical and technical ruling on basis period determination, issued by the Inland Revenue Board of Malaysia on 30 April 2001 (IRBM, 2013b). Malaysian tax assessment system is currently operating based on self assessment system (SAS). The system has come into effect within companies in 2001 replacing official assessment system in calculating, submitting and remitting the tax payments and tax returns. Despite the arguments of high compliance cost borne by the taxpayers, the system is found effective to encourage taxpayer compliance and to reduce the tax authority’s assessment tasks (Hanefah, Ariff & Kasipillai, 2002; Mansor, Saad & Ibrahim, 2004; Isa & Pope, 2011).

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Pe

rce

nta

ge

Corporate Individual Petroleum Others 2 per. Mov. Avg. (Corporate)

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 70

As to minimise double taxation issues, dividends distributed by companies are exempted in the hand of the recipients. This system is referred to as single-tier system. The system was first announced to be implemented in the year of assessment 2008 to supersede the imputation system enacted under Section 108 and Section 110 of the Income Tax Act 1967 (ITA 1967, 2008). The benefits of the transitions include reduction of administrative work in assessing tax on distributed dividends and in a similar vein, compliance cost of the dividend-paying companies can also be reduced. This implies single tier effect of dividend taxation at the corporate level as it is no longer assessed in the hand of the recipients who have received dividends at the net of corporate tax rates. Corporation tax rates in Malaysia have experienced gradual reductions across late 1980s (40 percent) to 2009 (25 percent). Table 2 provides details of the corporate tax rates including their rate of changes. The rate was at the maximum tip (40 percent) prior to a five percent-reduction in 1989 (35 percent). For the subsequent years, the reduction at most occurred at the rate of two percent in each 1994, 1995 and 1998. To accommodate small and mediums corporations, tax rates based on taxable income brackets was first introduced in 2003. Although the rate for the highest tax brackets remained unchanged in 2004, the significant increase of taxable income bracket for the lowest rate (20 percent), i.e. an increase of 400 percent (RM100,000 to RM500,000) for companies with paid-up capital lesser than RM2.5 million at the start of the basis period, was depicted as an effective strategy to support the government policy to further strengthen the country’s domestic small and medium enterprises. Following a constant-highest corporate tax rate from 1998 to 2006, a reduction was continued at a rate of one percent in each of the three subsequent years, 2007 to 2009, resulting to the lowest rate in the country’s corporate tax rate history (25 percent in 2009). Although the reductions in tax rates can be argued as could result to lesser contribution of corporation tax to the Federal Government revenue, a bivariate correlation analysis indicates insignificant correlation

between the corporate tax rate and the composition of corporation tax in the revenue (=0.4449, p=0.3767) suggesting a decrement in corporate tax rates is not necessarily correlated with changes in the magnitude of the composition corporate tax.2 This finding is, however, in contradiction with Abdul Wahab, Aripin, Md Idris and Che Ahmad (2007) that find changes in tax rates relate to changes in capital investment of companies. This provides insights for future research to further extend the analysis using multivariate analysis to confirm the relationship between the rates and the composition whilst simultaneously considering other country-specific characteristics. Table 2: Corporate Tax Rates

Year of assessments

Company’s paid up capital

Taxable income bracket Corporate tax rate

(%)

Percentage of reduction

(%)

1988 and prior years

Not applicable Not applicable 40 -

1989 - 1992 Not applicable Not applicable 35 5

1993 Not applicable Not applicable 34 1

1994 Not applicable Not applicable 32 2

1995 – 1997 Not applicable Not applicable 30 2

1998 - 2002 Not applicable Not applicable 28 2

2003 Not more than RM2.5 million

On the first RM100,000 of taxable income

20 -

Remaining taxable income 28 -

2 To accommodate the corporate tax composition data (Table 4.1), the period for the analysis was abridged to

cover years from 2000. Corporate tax composition for 2000, 2004 and 2009 was weighted respectively for 2002 – 2002, 2004 – 2006, and 2009 – 2013.

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 71

More than RM2.5 million

Not applicable 28 0

2004 -2006 Not more than RM2.5 million

On the first RM500,000 of taxable income

20 0*

Remaining taxable income 28 0

More than RM2.5 million

Not applicable 28 0

2007 Not more than RM2.5 million

On the first RM500,000 of taxable income

20 0

Remaining taxable income 27 1

More than RM2.5 million

Not applicable 27 1

2008 Not more than RM2.5 million

On the first RM500,000 of taxable income

20 0

Remaining taxable income 26 1

More than RM2.5 million

Not applicable 26 1

2009 onwards Not more than RM2.5 million

On the first RM500,000 of taxable income

20 0

Remaining taxable income 25 1

More than RM2.5 million

Not applicable 25 1

* Note: Although the rate was similar with the previous year, the bracket was increased by RM400,000. Source: Inland Revenue Board, Malaysia http://www.hasil.gov.my/ 3. The Economic Approach to Malaysian Corporate Tax Design The intuition on ways of corporate tax and economic development interact is largely based on tax collection that flows to the government revenue to support the spending. In addition, many have argued corporate tax also interacts with a country’s economic competitive condition through its tax design (Boadway & Bruce, 1984; Myles, 1987; Boadway & Sato, 2009). Tax design is often referred to as a tax system and structure to achieve a country’s social and economic efficiency objectives while ensuring provision of public goods and limiting the horizontal and vertical inequalities among taxpayers (The Mirrlees Review, 2010). Characteristics of a good tax design are widely discussed based on Adam Smith’s “canons of taxation” (Adam, 1970) which is further argued by The Mirrlees Review (The Mirrlees Review, 2010) as incomprehensive due to the absence of four characteristics of “a given distributional outcome”. Assessing Malaysian corporate tax system using both characteristics will lead to the conclusion to rooms of improvement in all aspects as it is almost impossible to suit administrator’s and taxpayers’ needs all at once, clearly because of the parties’ objectives, needs, perceptions and definitions vary between and within each other. For example in the case of tax avoidance and evasion, what is “acceptable” to one party may not be acceptable to the others (Bond, Gammie & Whiting, 2006; Self, 2007). Self (2007) explains “acceptable avoidance” as a tax planning activity that comprises two elements: firstly, the relationship of the tax avoidance with business transaction and secondly, the relationship of the tax avoidance with commercial purpose. On the other hand, without these elements, a tax avoidance activity is considered as “unacceptable”. However, although an avoidance activity may have fulfilled these two conditions, it may still not be considered “acceptable” by the

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 72

authority since they define “acceptable” avoidance as only comprising any action to reduce tax liability by “very clearly” just taking advantage of tax reliefs (Bond et al., 2006). This indicates that those activities, from the authority’s point of view, that are not “very clearly” just taking advantage of tax reliefs are considered as “unacceptable” avoidance, which then, presumably, falls into the evasion category. Difficulties in differentiating “acceptable” and “unacceptable” avoidance are also admitted by Dave Hartnett, Deputy Chief Executive of Her Majesty Revenue and Customs, a UK tax authority, who states that, in general, “unacceptable” avoidance is said to be related to “aggression, artificial, and secrecy” and “things nobody wants in a tax system” (HMRC, 2008). These indications of “unacceptable” avoidance, especially “things nobody wants in a tax system”, lead to open interpretation and consequently introduce ambiguous understanding of the difference between “acceptable” and “unacceptable” avoidance among the related parties. This conflict is also discussed in detail by Slemrod (2004). In reviewing the demand for tax evasion, the author admits that there is no obvious line between avoidance and evasion, which then leads to the interpretation of tax planning as a matter of creative compliance. Based on the arguments, the definition of tax avoidance as a “completely acceptable” activity (Hoffman, 1961) varies according to different parties. 4. Research Design The data of this study was drawn from IRBM’s annual report and Ministry of Finance’s Economic Reports. To reflect the most current available data, the sample period covers 2000 to 2013. In addition to trend analysis, Chi-square tests were also conducted to determine the level of significance of the initial findings. 5. Corporate Tax Liabilities and Revenue across Years Corporate tax liability is calculated using the audited profit before tax as a base figure. Adjusting the profit to accommodate the tax provisions (under the ITA 1967 and Promotion of Investment Act 1986) leads to taxable income. The Promotion of Investment Act (1986) provides details about the provisions relating to tax incentives available for companies, e.g. pioneer status, investment tax allowance and industrial adjustment allowance. Tax provisions under the ITA 1967 include non-allowable deductions, non-taxable gains or income, capital allowance deductions and charge of disposal of business assets. To further understand the trend of collected corporate tax liability, Figure 2 illustrates the movement of the collection by the IRBM across years. The collection fluctuates suggesting that there are determinants to the trend line. Throughout the years, the IRBM hit the collection’s maximum peak in 2008. At the other extreme, the lowest collection is documented in 2000. The collections experience two periods of gradual declines, first, from 2002 to 2004, and second, from 2008 to 2009. Despite the declines in corporate tax rates, the collection is moving in an increasing manner demonstrating a counter argument on negative implication of corporate tax rate reductions on corporate tax collection. Although there is evidence on detrimental effect of reduction of tax rates on the tax collection, the incidents are observed to be infrequent compared to the other effects. The linear line of corporate tax collection, ceteris paribus, forecasts an increment of the collection across future years. This positively indicates an increment to the government’s cash flow. One, on the other hand, could argue that the positive slope trend could simply occur due to an increase in inflation. A future study that confirms the determinants of this collection is crucial to expand the boundary of this knowledge. The regressors should consider the determinants at both micro, for

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 73

instance, firm characteristics (e.g. Gupta & Newberry, 1997; Derashid & Zhang, 2003; Richardson & Lanis, 2007), and macro levels, for instance, economic condition, exchange rates and employment (e.g. Slemrod, 1990; S Stö & Traxler, 2005; Blackburn, Bose & Capasso, 2012).

Figure 2: Corporate Tax Collection (RM) A generic justification on the implication of enforcement by the authority to the collection lies on the effectiveness of the enforcement itself. To provide a graphical explanation to this, Figure 3 illustrates the movement of the corporate tax collection along with one of the compliance enforcements conducted by the IRBM, visiting the business premises. The bars compare the collection with the number of visited business premises from 2000 to 2010. Note that the unit of corporate tax collection is weighted at RM million so as to be comparable with the numbers of visit.

13980

21582

27383 24558 23161

28058 30415

37575

46902

40265 43797

0

10000

20000

30000

40000

50000

60000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Mil

lio

ns

Corporate tax collection (RM) Linear (Corporate tax collection (RM))

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Corporate tax collection (RM millions)

Number of visited business premise

Expon. (Corporate tax collection (RM millions))

Expon. (Number of visited business premise)

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 74

Figure 2: Corporate Tax Collection (RM) The upward trend of the numbers of visited premise is obviously centred at the middle of the periods, from 2003 to 2006. This, in contradiction to the collection, raises the question on the achievement towards the enforcement’s objectives. The exponential trend lines explain the movement of both lines are parallel across year implying positive effect of the enforcement towards the collection. The prediction drawn from these lines suggests a decline in the gap between the corporate tax collection and the enforcement in the future. Considering the incremental trend of the collection over the enforcement activity throughout the last three years (2008 – 2010), one might debate that ceasing the enforcement activity would cause a further revenue loss to the government as the collection has started responding to the authority’s compliance-enforcement activity since then. Argumentatively, this is in contradiction with the exponential trend lines’ forecast. This leaves the future research with focus of attention of investigating whether the enforcement should be forgone only due to relative low collection in the years from 2003 to 2007 and the forecast drawn from the trend lines. 6. Conclusions Malaysian corporate taxation is regulated by the Income Tax Act 1967. Public rulings are issued by the IRBM to supplement the Act. The system for corporate tax is run using SAS from 2001. The taxation on profit distribution is based on single-tier system replacing imputation system in 2008. This implies tax on dividend is exempted in the hand of the receivers. Corporate tax rates in Malaysia experience several reductions from 1988 to 2009. From the highest rate at 40 percent to the lowest 25 percent, the results from the bivariate analysis find limited evidence on the correlation between the corporate tax rate and the composition of corporate tax in its contribution to Federal Government revenue. From the perspective of an economic approach, Malaysian corporate tax design is observed to have many more areas to improve. This is important as the loophole in the tax system may create opportunities for firms to avoid or evade the corporate tax. Studies in corporate tax field find evidence on tax planning opportunities created by ambiguity of the tax laws and firms’ specific characteristics. Tax planning interpretation is basically referring to tax avoidance and evasion. Tax planning activities among firms are mainly triggered by the availability of the opportunity to avoid tax. The activities are carried by firms with different objectives, for example increasing after-tax returns or increasing after-tax cash flow, but these objectives could be restricted by constraints of tax planning, for example, direct and indirect (non-tax) costs of tax planning. Factors that motivate tax planning activities are primarily based on the expected benefits of tax planning and this motivating factor could be moderated by other factors, i.e. corporate governance linked to stakeholders’ opinion considerations. Corporate governance in moderating tax planning activities is of interest to the researchers as shareholders have limited access to firms’ tax planning-related information. Therefore, there is a possibility of incongruence of tax planning objectives between the managers and the owners of the companies. This phenomenon, which is called conflict of interest, is widely explained in corporate governance literature. Managing and improving compliance create cost-effective challenge to the IRBM. Studies document the costs as comprising of administrative and compliance costs. To be effective, the corporate tax design has to entail low costs to both the authority and taxpayers. This consequently sheds lights on the issue of the effectiveness of the “visit enforcement” as the movement of the corporate tax collection along with the numbers of visited premises is predicted to be insignificantly different from

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 75

each other in the coming years. Overall, the findings suggest the government to levy sufficient corporate tax and respond to the increase administrative and compliance costs in its current enforcement strategies.

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 76

References Abdul Wahab, N. S., Aripin, N., Md Idris, K., Che Ahmad, A. (2007). The implication of tax rates on corporate capital investment. Malaysian Accounting Review, 6(1), 45-64. Abdul Wahab, N. S., Holland, K. (2012). Tax planning, corporate governance and equity value. The British Accounting Review, 44(2), 111-124. Adam, S. (1970). The Wealth of Nations. Harmondsworth: Penguin. Blackburn, K., Bose, N., Capasso, S. (2012). Tax evasion, the underground economy and financial development. Journal of Economic Behavior and Organization, 83(2), 243-253. Boadway, R., Bruce, N. (1984). A general proposition on the design of a neutral business tax. Journal of Public Economics, 24(2), 231-239. Boadway, R., Sato, M. (2009). Optimal tax design and enforcement with an informal sector. American Economic Journal: Economic Policy, 1-27. Bond, S., Gammie, M., Whiting, J. (2006). Tax avoidance, The IFS Green Budget January 2006, available on the internet at http://www.ifs.org.uk/budgets/gb2006/06chap10.pdf Accessed 14 October 2009. Carr, S., Chan, C. (2005). New Zealand's fringe benefit tax 20 years on: An empirical investigation into employers' perceptions. In Fisher, R. & Walpole, M. (Eds.) Global Challenges in Tax Administration. Birmingham: Fiscal Publication, 322-339. Derashid, C., Zhang, H. (2003). Effective tax rates and the “industrial policy” hypothesis: Evidence from Malaysia. Journal of International Accounting, Auditing and Taxation, 12(1), 45-62. Desai, M. A., Dharmapala, D. (2009). Corporate tax avoidance and firm value. The Review of Economics and Statistics, 91 (3), 537-546. Gupta, S., Newberry, K. (1997). Determinants of the variability in corporate effective tax rates: Evidence from longitudinal data. Journal of Accounting and Public Policy, 16(1), 1-34. Hanefah, M., Ariff, M., Kasipillai, J. (2002). Compliance costs of small and medium enterprises. Journal of Australian Taxation, 4(1), 73-97. Hanlon, M., Mills, L., Slemrod, J. (2007). An empirical examination of corporate tax noncompliance. In Auerbach, A. J., Hines Jr, J. R. & Slemrod, J. (Eds.) Taxing Corporate Income in the 21st Century. New York: Cambridge University Press, 171-210. Hanlon, M., Slemrod, J. B. (2009). What does tax aggressiveness signal? Evidence from stock price reactions to news about tax shelter involvement. Journal of Public Economics, 93(1-2), 126-141. Hansford, A., Pilkington, C., Lymer, A. (2005). Filing self assessment tax returns by internet: The impact on taxpayer compliance in the UK. In Fisher, R. & Walpole, M. (Eds.) Global Challenges in Tax Administration. Birmingham: Fiscal Publication, 256-257.

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 77

HMRC (2008). Questions-transcript, Podcasts, available on the internet at http://www.hmrc.gov.uk/podcasts/questions-transcript.pdf Accessed 4 November 2009. Hoffman, W. H. (1961). The theory of tax planning. The Accounting Review, 36(2), 274-281. IRBM (2013a). Forms, available on the internet at http://www.hasil.gov.my Accessed 19 May 2013. IRBM (2013b). Public Ruling, available on the internet at http://www.hasil.gov.my/goindex.php?kump=5&skum=5&posi=3&unit=1&sequ=1 Accessed 19 May 2013. IRBM (2013c). Tax Rates of Company, available on the internet at http://www.hasil.gov.my Accessed 19 May 2013. IRBM CEO (2004). LHDN Bukan Seperti Along, Kami Tidak Kejar VIP tetapi Mahu Membersihkan Hutang, Kemaskini Data, Utusan Malaysia, available on the internet at http://ww2.utusan.com.my/utusan/special.asp?pr=PR11&y=2004&dt=0125&pub=Utusan_Malaysia&sec=Rencana&pg=re_04.htm Accessed 30 January 2011. IRBM CEO (2010). Manfaat Kutipan Hasil Negara, Utusan Malaysia, available on the internet at http://www.hasil.gov.my/pdf/pdfam/Manfaatkutipanhasi.pdf Accessed 30 January 2011. Isa, K., Pope, J. (2011). Corporate tax audits: Evidence from Malaysia. Global Review of Accounting and Finance, 2(1), 42-56. ITA 1967 (2008). Income Tax Act 1967 (With Completed Rules & Regulations). Selangor: International Law Book Services. ITO 1947 (1961). Income Tax Ordinance, 1947 (Malayan Union Ord. No. 48 of 1947) Together with Subsidiary Legislation Made Thereunder: Incorporating All Amendments Up to the 1st February, 1961, and Pioneer Industries (Relief from Income Tax) Ordinance, 1958 (No. 31 of 1958). Federation of Malaya, Government Press. Mansor, M., Saad, N., Ibrahim, I. (2004). The self-assessment system and its compliance costs. Journal of Financial Reporting and Accounting, 2(1), 1-15. Mills, L. F., Erickson, M., Maydew, E. L. (1998). Investment in tax planning. The Journal of the American Taxation Association, 20(1), 1-20. Ministry of Finance (2013). Economic Report, available on the internet at http://www.treasury.gov.my Accessed 19 May 2013. Myles, G. D. (1987). Tax design in the presence of imperfect competition: An example. Journal of Public Economics, 34(3), 367-378. Ngan, W. S. (2008). Post-colonial legal developments. In Sundaram, J. K. & Ngan, W. S. (Eds.) Law, Institutions and Malaysia Economic Development. Singapore: National University of Singapore, 54 - 79.

E-Proceeding of the International Conference on Social Science Research, ICSSR 2015 (e-ISBN 978-967-0792-04-0). 8 & 9 June 2015, Meliá Hotel Kuala Lumpur, Malaysia. Organized by http://WorldConferences.net 78

Ott, K. (2005). The evolution of the informal economy and tax evasion in Croatia. In Fisher, R. & Walpole, M. (Eds.) Global Challenges in Tax Administration. Birmingham: Fiscal Publication, 313-321. PIA 1986 (1986). Promotion Investment Act. Kuala Lumpur: International Law Book Services. Porcano, T. (1986). Corporate tax rates: Progressive, proportional, or regressive. Journal of the American Taxation Association, 7(2), 17–31. Richardson, G., Lanis, R. (2007). Determinants of the variability in corporate effective tax rates and tax reform: Evidence from Australia. Journal of Accounting and Public Policy, 26(6), 689-704. S Stö, S., Traxler, C. (2005). Tax evasion and auditing in a federal economy. International Tax and Public Finance, 12(4), 515-531. Samuelson, R. A. (1996). The concept of assets in accounting theory. Accounting Horizons, 10(3), 147-157. Self, H. (2007). Acceptable tax avoidance? The Tax Journal, 9-10. Slemrod, J. (1990). Optimal taxation and optimal tax systems. The Journal of Economic Perspectives, 4(1), 157-178. Slemrod, J. (2004). The economics of corporate tax selfishness. National Tax Journal, 57(4), 877-899. Slemrod, J. B., Blumenthal, M. (1996). The income tax compliance cost of big business. Public Finance Review, 24(4), 411-438. Slemrod, J. B., Yitzhaki, S. (2002). Tax avoidance, evasion, and administration. In Auerbach, A. J. & Feldstein, M. (Eds.) Handbook of Public Economics Volume 3. Amsterdam: Elsevier Science B.V, 1425-1470. The Mirrlees Review (2010). Tax by Design. Oxford: Oxford University Press. Tiley, J. (2005). Revenue Law 5th ed. Oxford: Hart Publishing. Vos, D. (2005). Tax administration for all taxpayers. In Fisher, R. & Walpole, M. (Eds.) Global Challenges in Tax Administration. Birmingham: Fiscal Publication, 12-22. Wilson, R. (2009). An examination of corporate tax shelter participants. The Accounting Review, 84(3), 969-999. Woellner, R., Coleman, C., Mckerchar, M., Walpole, M., Zetler, J. (2005). Identifying the psychological costs of tax compliance. In Fisher, R. & Walpole, M. (Eds.) Global Challenges in Tax Administration. Birmingham: Fiscal Publication, 268-287. Zimmerman, J. L. (1983). Taxes and firm size. Journal of Accounting and Economics, 5(2), 119-149.